Liquidity Void Zone Detector [PhenLabs]📊 Liquidity Void Zone Detector

Version: PineScript™v6

📌 Description

The Liquidity Void Zone Detector is a sophisticated technical indicator designed to identify and visualize areas where price moved with abnormally low volume or rapid momentum, creating "voids" in market liquidity. These zones represent areas where insufficient trading activity occurred during price movement, often acting as magnets for future price action as the market seeks to fill these gaps.

Built on PineScript v6, this indicator employs a dual-detection methodology that analyzes both volume depletion patterns and price movement intensity relative to ATR. The revolutionary 3D visualization system uses three-layer polyline rendering with adaptive transparency and vertical offsets, creating genuine depth perception where low liquidity zones visually recede and high liquidity zones protrude forward. This makes critical market structure immediately apparent without cluttering your chart.

🚀 Points of Innovation

Dual detection algorithm combining volume threshold analysis and ATR-normalized price movement sensitivity for comprehensive void identification

Three-layer 3D visualization system with progressive transparency gradients (85%, 78%, 70%) and calculated vertical offsets for authentic depth perception

Intelligent state machine logic that tracks consecutive void bars and only renders zones meeting minimum qualification requirements

Dynamic strength scoring system (0-100 scale) that combines inverted volume ratios with movement intensity for accurate void characterization

Adaptive ATR-based spacing calculation that automatically adjusts 3D layering depth to match instrument volatility

Efficient memory management system supporting up to 100 simultaneous void visualizations with automatic array-based cleanup

🔧 Core Components

Volume Analysis Engine: Calculates rolling volume averages and compares current bar volume against dynamic thresholds to detect abnormally thin trading conditions

Price Movement Analyzer: Normalizes bar range against ATR to identify rapid price movements that indicate liquidity exhaustion regardless of instrument or timeframe

Void Tracking State Machine: Maintains persistent tracking of void start bars, price boundaries, consecutive bar counts, and cumulative strength across multiple bars

3D Polyline Renderer: Generates three-layer rectangular polylines with precise timestamp-to-bar index conversion and progressive offset calculations

Strength Calculation System: Combines volume component (inverted ratio capped at 100) with movement component (ATR intensity × 30) for comprehensive void scoring

🔥 Key Features

Automatic Void Detection: Continuously scans price action for low volume conditions or rapid movements, triggering void tracking when thresholds are exceeded

Real-Time Visualization: Creates 3D rectangular zones spanning from void initiation to termination, with color-coded depth indicating liquidity type

Adjustable Sensitivity: Configure volume threshold multiplier (0.1-2.0x), price movement sensitivity (0.5-5.0x), and minimum qualifying bars (1-10) for customized detection

Dual Color Coding: Separate visual treatment for low liquidity voids (receding red) and high liquidity zones (protruding green) based on 50-point strength threshold

Optional Compact Labels: Toggle LV (Low Volume) or HV (High Volume) circular labels at void centers for quick identification without visual clutter

Lookback Period Control: Adjust analysis window from 5 to 100 bars to match your trading timeframe and market volatility characteristics

Memory-Efficient Design: Automatically manages polyline and label arrays, deleting oldest elements when user-defined maximum is reached

Data Window Integration: Plots void detection binary, current strength score, and average volume for detailed analysis in TradingView's data window

🎨 Visualization

Three-Layer Depth System: Each void is rendered as three stacked polylines with progressive transparency (85%, 78%, 70%) and calculated vertical offsets creating authentic 3D appearance

Directional Depth Perception: Low liquidity zones recede with back layer most transparent; high liquidity zones protrude with front layer most transparent for instant visual differentiation

Adaptive Offset Spacing: Vertical separation between layers calculated as ATR(14) × 0.001, ensuring consistent 3D effect across different instruments and volatility regimes

Color Customization: Fully configurable base colors for both low liquidity zones (default: red with 80 transparency) and high liquidity zones (default: green with 80 transparency)

Minimal Chart Clutter: Closed polylines with matching line and fill colors create clean rectangular zones without unnecessary borders or visual noise

Background Highlight: Subtle yellow background (96% transparency) marks bars where void conditions are actively detected in real-time

Compact Labeling: Optional tiny circular labels with 60% transparent backgrounds positioned at void center points for quick reference

📖 Usage Guidelines

Detection Settings

Lookback Period: Default: 10 | Range: 5-100 | Number of bars analyzed for volume averaging and void detection. Lower values increase sensitivity to recent changes; higher values smooth detection across longer timeframes. Adjust based on your trading timeframe: short-term traders use 5-15, swing traders use 20-50, position traders use 50-100.

Volume Threshold: Default: 1.0 | Range: 0.1-2.0 (step 0.1) | Multiplier applied to average volume. Bars with volume below (average × threshold) trigger void conditions. Lower values detect only extreme volume depletion; higher values capture more moderate low-volume situations. Start with 1.0 and decrease to 0.5-0.7 for stricter detection.

Price Movement Sensitivity: Default: 1.5 | Range: 0.5-5.0 (step 0.1) | Multiplier for ATR-normalized price movement detection. Values above this threshold indicate rapid price changes suggesting liquidity voids. Increase to 2.0-3.0 for volatile instruments; decrease to 0.8-1.2 for ranging or low-volatility conditions.

Minimum Void Bars: Default: 10 | Range: 1-10 | Minimum consecutive bars exhibiting void conditions required before visualization is created. Filters out brief anomalies and ensures only sustained voids are displayed. Use 1-3 for scalping, 5-10 for intraday trading, 10+ for swing trading to match your time horizon.

Visual Settings

Low Liquidity Color: Default: Red (80% transparent) | Base color for zones where volume depletion or rapid movement indicates thin liquidity. These zones recede visually (back layer most transparent). Choose colors that contrast with your chart theme for optimal visibility.

High Liquidity Color: Default: Green (80% transparent) | Base color for zones with relatively higher liquidity compared to void threshold. These zones protrude visually (front layer most transparent). Ensure clear differentiation from low liquidity color.

Show Void Labels: Default: True | Toggle display of compact LV/HV labels at void centers. Disable for cleaner charts when trading; enable for analysis and review to quickly identify void types across your chart.

Max Visible Voids: Default: 50 | Range: 10-100 | Maximum number of void visualizations kept on chart. Each void uses 3 polylines, so setting of 50 maintains 150 total polylines. Higher values preserve more history but may impact performance on lower-end systems.

✅ Best Use Cases

Gap Fill Trading: Identify unfilled liquidity voids that price frequently returns to, providing high-probability retest and reversal opportunities when price approaches these zones

Breakout Validation: Distinguish genuine breakouts through established liquidity from false breaks into void zones that lack sustainable volume support

Support/Resistance Confluence: Layer void detection over key horizontal levels to validate structural integrity—levels within high liquidity zones are stronger than those in voids

Trend Continuation: Monitor for new void formation in trend direction as potential continuation zones where price may accelerate due to reduced resistance

Range Trading: Identify void zones within consolidation ranges that price tends to traverse quickly, helping to avoid getting caught in rapid moves through thin areas

Entry Timing: Wait for price to reach void boundaries rather than entering mid-void, as voids tend to be traversed quickly with limited profit-taking opportunities

⚠️ Limitations

Historical Pattern Indicator: Identifies past liquidity voids but cannot predict whether price will return to fill them or when filling might occur

No Volume on Forex: Indicator uses tick volume for forex pairs, which approximates but doesn't represent true trading volume, potentially affecting detection accuracy

Lagging Confirmation: Requires minimum consecutive bars (default 10) before void is visualized, meaning detection occurs after void formation begins

Trending Market Behavior: Strong trends driven by fundamental catalysts may create voids that remain unfilled for extended periods or permanently

Timeframe Dependency: Detection sensitivity varies significantly across timeframes; settings optimized for one timeframe may not perform well on others

No Directional Bias: Indicator identifies liquidity characteristics but provides no predictive signal for price direction after void detection

Performance Considerations: Higher max visible void settings combined with small minimum void bars can generate numerous visualizations impacting chart rendering speed

💡 What Makes This Unique

Industry-First 3D Visualization: Unlike flat volume or liquidity indicators, the three-layer rendering with directional depth perception provides instant visual hierarchy of liquidity quality

Dual-Mode Detection: Combines both volume-based and movement-based detection methodologies, capturing voids that single-approach indicators miss

Intelligent Qualification System: State machine logic prevents premature visualization by requiring sustained void conditions, reducing false signals and chart clutter

ATR-Normalized Analysis: All detection thresholds adapt to instrument volatility, ensuring consistent performance across stocks, forex, crypto, and futures without constant recalibration

Transparency-Based Depth: Uses progressive transparency gradients rather than colors or patterns to create depth, maintaining visual clarity while conveying information hierarchy

Comprehensive Strength Metrics: 0-100 void strength calculation considers both the degree of volume depletion and the magnitude of price movement for nuanced zone characterization

🔬 How It Works

Phase 1: Real-Time Detection

On each bar close, the indicator calculates average volume over the lookback period and compares current bar volume against the volume threshold multiplier

Simultaneously measures current bar's high-low range and normalizes it against ATR, comparing the result to price movement sensitivity parameter

If either volume falls below threshold OR movement exceeds sensitivity threshold, the bar is flagged as exhibiting void characteristics

Phase 2: Void Tracking & Qualification

When void conditions first appear, state machine initializes tracking variables: start bar index, initial top/bottom prices, consecutive bar counter, and cumulative strength accumulator

Each subsequent bar with void conditions extends the tracking, updating price boundaries to envelope all bars and accumulating strength scores

When void conditions cease, system checks if consecutive bar count meets minimum threshold; if yes, proceeds to visualization; if no, discards the tracking and resets

Phase 3: 3D Visualization Construction

Calculates average void strength by dividing cumulative strength by number of bars, then determines if void is low liquidity (>50 strength) or high liquidity (≤50 strength)

Generates three polyline layers spanning from start bar to end bar and from top price to bottom price, each with calculated vertical offset based on ATR

Applies progressive transparency (85%, 78%, 70%) with layer ordering creating recession effect for low liquidity zones and protrusion effect for high liquidity zones

Creates optional center label and pushes all visual elements into arrays for memory management

Phase 4: Memory Management & Display

Continuously monitors polyline array size (each void creates 3 polylines); when total exceeds max visible voids × 3, deletes oldest polylines via array.shift()

Similarly manages label array, removing oldest labels when count exceeds maximum to prevent memory accumulation over extended chart history

Plots diagnostic data to TradingView’s data window (void detection binary, current strength, average volume) for detailed analysis without cluttering main chart

💡 Note:

This indicator is designed to enhance your market structure analysis by revealing liquidity characteristics that aren’t visible through standard price and volume displays. For best results, combine void detection with your existing support/resistance analysis, trend identification, and risk management framework. Liquidity voids are descriptive of past market behavior and should inform positioning decisions rather than serve as standalone entry/exit signals. Experiment with detection parameters across different timeframes to find settings that align with your trading style and instrument characteristics.

Zmienność

Spot-Futures SpreadSpot-Futures Spread Indicator

A comprehensive indicator that automatically calculates and visualizes the percentage spread between spot and perpetual futures prices across multiple exchanges.

Key Features:

Automatic Exchange Detection - Automatically detects your current exchange and finds the corresponding spot/futures pair

Smart Fallback System - If the counterpart isn't available on your exchange, it automatically searches across 7+ major exchanges (Binance, Bybit, OKX, Gate.io, MEXC, KuCoin, HTX) and uses the first valid match

Multi-Exchange Support - Works with 14 exchanges including Binance, Bybit, OKX, MEXC, BitGet, Gate.io, KuCoin, and more

Clear Exchange Attribution - Shows exactly which exchanges are providing spot and futures data in the statistics table

Configurable Moving Average - Track the average spread with customizable period

Standard Deviation Bands - Identify unusual spread conditions with Bollinger-style bands

Built-in Alerts - Get notified when spread crosses bands or zero (parity)

Statistics Table - Real-time stats showing current spread, MA, std dev, and bands

Manual Override Options - Advanced users can manually specify exchanges and symbols

How It Works:

The indicator calculates the spread as: (Futures Price - Spot Price) / Spot Price × 100

Positive spread = Futures trading at a premium (contango)

Negative spread = Futures trading at a discount (backwardation)

Zero = Parity between spot and futures

Use Cases:

Funding Rate Analysis - Correlates with perpetual funding rates

Arbitrage Opportunities - Identify significant spot-futures divergences

Market Sentiment - Premium/discount indicates bullish/bearish positioning

Cross-Exchange Analysis - Compare spreads when spot and futures are on different exchanges

Smart Features:

Works whether you're viewing a spot or futures chart

Automatically handles exchange-specific perpetual contract naming (.P, PERP, SWAP, etc.)

Color-coded visualization (green for premium, red for discount)

Customizable colors and display options

Background shading based on spread direction

Perfect For:

Crypto traders monitoring funding rates, arbitrage traders, market makers, and anyone interested in spot-futures dynamics across multiple exchanges.

Getting Started:

Simply add the indicator to any spot or perpetual futures chart. It will automatically detect the exchange and find the corresponding pair. The statistics table shows which exchanges are being used for maximum transparency.

Note: The indicator automatically ignores invalid symbols, so you'll never see errors even if a specific pair doesn't exist on a particular exchange.

Kudos to @AlekMel that made the "Spot - Fut Spread v2" indicator that I enhance the Automatic detection feature which was not working in some case.

Stochastic Ensembling of OutputsStochastic Ensembling of Outputs

🙏🏻 This is a simple tool/method that would solve naturally many well known problems:

“Price reversed 1 tick before the actual level, not executing my limit order”

“I consider intraday trend change by checking whether price is above/below VWAP, but is 1 tick enough? What to do, price is now whipsawing around vwap...”.

“I want to gradually accumulate a position around a chosen anchor. But where exactly should I put my orders? And I want to automate it ofc.“

“All these DSP adepts are telling you about some kind of noise in the markets… But how can I actually see it?”

The easy fix is to make things more analog less digital, by synthesizing numerous noise instances & adding it to any price-applied metric of yours. The ones who fw techno & psytrance, and other music, probably don’t need any more explanations. Then by checking not just 2 lines or 1 process against another one, you will be checking cloud vs cloud of lines, even allowing you to introduce proxies of probabilities. More crosses -> more confirmation to act.

How-to use:

The tool has 2 inputs: source and target:

Sources should always be the underlying process. If you apply the tool to price based metric, leave it hlcc4 unless you have a better one point estimate for each bar;

Target is your target, e.g if you want to apply it to VWAP, pick VWAP as target. You can thee on the chart above how trading activity recently never exactly touched VWAP, however noised instances of VWAP 'were' touched

The code is clean and written in modular form, you can simply copy paste it to any script of yours if you don't want to have multiple study-on-study script pairs.

^^ applied to prev days highs and lows

^^ applied to MBAD extensions and basis

^^ applied to input series itself

Here’s how it works, no ML, no “AI”, no 1k lines of code, just stats:

The problem with metrics, even if they are time aware like WMA, is that they still do not directly gain information about “changes” between datapoints. If we pick noise characteristics to match these changes, we’d effectively introduce this info into our ops.

^^ this screenshot represents 2 very different processes: a sine wave and white noise, see how the noise instances learned from each process differ significantly.

Changes can be represented as AR1 process . It’s dead simple, no PHD needed, it’s just how the current datapoint is related (or not) to the previous datapoint, no more than 1, and how this relationship holds/evolves over time. Unlike the mainstream approach like MLE, I estimate this relationship (phi parameter) via MoM but giving more weights to more recent datapoints via exponential smoothing over all the data available on your charts (so I encode temporal information), algocomplexity is O(1), lighting fast, just one pass. <- that gives phi , we’d use it as color for our noise generator

Then we just need to estimate noise amplitude ( gamma ) via checking what AR1 model actually thought vs the reality, variance of these innovations. Same via exponential smoothing, time aware, O(1), one pass, it’s all it does.

Then we generate white gaussian noise, and apply 2 estimated parameters (phi and gamma), and that’s all.

Omg, I think I just made my first real DSP script xd

Just like Monte Carlo for risk management, this is so simple and natural I can’t believe so many “pros” hide it and never talk about it in open access. Sharing it here on TradingView would’ve not done anything critical for em, but many would’ve benefited.

∞

Rasta Long/Short — StrategyThe Rasta Long/Short Strategy is a visual and educational framework designed to help traders study momentum shifts that appear when a fast EMA interacts with a slower smoothed baseline.

It is not a signal service. Instead, it is a research tool that helps you observe transitions, structure, and behavior across different market conditions and smoothing contexts.

The script plots:

A primary EMA line (fast reaction wave).

A Smoothed line (your chosen smoothing method).

Color-coded fog regions showing directional bias.

Optional DNA rung connections between the two lines for structural comparison.

Together, these allow a deeper study of how momentum pushes, volatility compression, expansions, and drift emerge around fast/slow EMA interactions.

✦ Core Idea

The Rasta Long/Short mechanism studies how price behaves when the fast EMA crosses above or below a smoothed anchor.

Rather than predicting price, it reveals where transitions occur across different structures, timeframes, and smoothing techniques.

The Long/Short logic simply highlights flips in directional structure.

It is not intended for real-time signals or automated execution; it is intended for understanding market movement.

✦ Smoothing Types (Explained)

The strategy allows experimenting with several smoothing families to observe how they transform the fast EMA:

SMA (Simple Moving Average)

Averaged, slower response. Good for stability comparisons.

EMA (Exponential)

Faster reaction, more responsive, smoother behavior during momentum.

RMA (Wilder’s)

Used in RSI calculations; steady, well-balanced response.

WMA (Weighted)

More weight to recent bars; bridges SMA and EMA dynamics.

None

Raw EMA vs EMA interaction with no secondary smoothing.

Each smoothing type provides unique structural information and can lead to different interpretations.

✦ Modes of Study

Designed for multi-timeframe research:

1H / 4H — Momentum flow mapping and structural identification.

Daily / Weekly — Higher-timeframe rotations, macro structure transitions.

1–15m — Microstructure studies, noise vs trend emergence.

Use the built-in Strategy Tester to explore entry/exit context, but treat results as research, not predictive performance.

✦ Components (Visual Study Tools)

EMA Line (Fast)

Primary reactive wave. Shows fast directional shifts.

Smoothed Line (Slow)

Trend baseline / reference structure.

Fog Region

Highlights fast-vs-smoothed directional alignment.

DNA Rungs (Optional)

Structural “bridges” showing the exact relationship between waves on each bar.

Useful for studying separation, compression, and expansions.

✦ Educational Insights

This strategy helps illuminate:

How fast and slow EMAs interact dynamically.

How structure changes precede trend emergence.

Where volatility compresses before expansion.

How noise, drift, and clean reversals differ.

How different smoothers alter the interpretation of the same price data.

The goal is clarity — not prediction.

✦ How to Use

Apply to any timeframe or instrument.

Enable or disable fog depending on preferred visibility.

Use DNA rungs for close structural comparison.

Observe long/short flips as educational reference points — not signals.

Study transitions visually, then backtest using the Strategy Tester for pattern research.

✦ Disclaimer

This script is provided for educational and research purposes only.

It does not provide trading signals, financial advice, or recommendations.

Past behavior does not indicate future performance.

Always practice risk-aware study and consult qualified financial professionals when needed.

✦ Author

Michael Culpepper (mikeyc747)

Creator of the Rasta framework and related market structure studies.

ATRP & Volatility Table - AIMAN93The ATRP & Volatility Table is a simple yet powerful tool designed to quantify market volatility and help traders adapt their position sizing accordingly.

It calculates the Average True Range Percentage (ATRP) — the ATR value relative to current price — and classifies market conditions into three volatility levels: LOW, MEDIUM, or HIGH. Based on the volatility level, it suggests an indicative risk percentage to guide your trade management.

This visual tool displays real-time ATRP, volatility classification, and corresponding risk percentage in a compact on-chart table. Ideal for systematic traders who rely on volatility-based decision-making, position sizing, or risk management models.

Features:

- Dynamic ATRP calculation for any symbol or timeframe

- Customizable colors for text and background

- Automatic volatility classification (low / medium / high)

- Suggested risk percentage for each volatility level

Keltner Channels BandsKeltner Channels Bands - パブリッシュ用説明文

日本語版

タイトル

Keltner Channels Bands (Multi-Timeframe)

説明文

概要

シンプルで視認性の高いケルトナーチャネルインジケーターです。マルチタイムフレーム機能を搭載し、どの時間足でも上位足のケルトナーチャネルを表示できます。

特徴

グレーカラーでチャートを見やすく保持

マルチタイムフレーム対応(デフォルト: 1時間足)

4時間足以上で自動非表示機能(チャートの見やすさを維持)

EMAまたはSMAの選択が可能

ATR倍率とバンド幅を自由にカスタマイズ

トレードコンセプト

ケルトナーチャネルは、価格のボラティリティに基づいたトレンド追従型インジケーターです。

基本的な使い方:

トレンド判定: 価格がバンドの上部で推移している場合は上昇トレンド、下部で推移している場合は下降トレンド

エントリー: 価格がバンド外に出た後、バンド内に戻るタイミングでトレンド方向へエントリー

エグジット: 価格が中心線(MA)に到達、または反対側のバンドに接近した時

ブレイクアウト: バンドを勢いよく突破した場合、新たなトレンドの始まりを示唆

推奨設定:

スイングトレード: Length 20, Multiplier 2.2, 1時間足または4時間足

デイトレード: Length 20, Multiplier 2.0, 5分足または15分足で1時間足を表示

注意事項

このインジケーターは単独での使用ではなく、他のテクニカル指標やプライスアクションと組み合わせて使用することを推奨します。

English Version

Title

Keltner Channels Bands (Multi-Timeframe)

Description

Overview

A simple and visually clean Keltner Channels indicator with multi-timeframe capabilities. Display higher timeframe Keltner Channels on any chart timeframe.

Features

Clean gray color scheme for better chart visibility

Multi-timeframe support (Default: 1-hour)

Auto-hide on 4H+ timeframes to maintain chart clarity

Choice between EMA or SMA

Customizable ATR multiplier and band width

Trading Concept

Keltner Channels is a volatility-based trend-following indicator that helps traders identify trend direction and potential entry/exit points.

Basic Usage:

Trend Identification: Price staying near upper band indicates uptrend; near lower band indicates downtrend

Entry Signals: Enter in trend direction when price returns inside the bands after moving outside

Exit Signals: Consider exits when price reaches the center line (MA) or approaches the opposite band

Breakout Trading: Strong momentum breaks through the bands may signal the start of a new trend

Recommended Settings:

Swing Trading: Length 20, Multiplier 2.2, 1H or 4H timeframe

Day Trading: Length 20, Multiplier 2.0, Display 1H channels on 5M or 15M charts

Disclaimer

This indicator should not be used alone. Combine it with other technical indicators and price action analysis for better trading decisions.

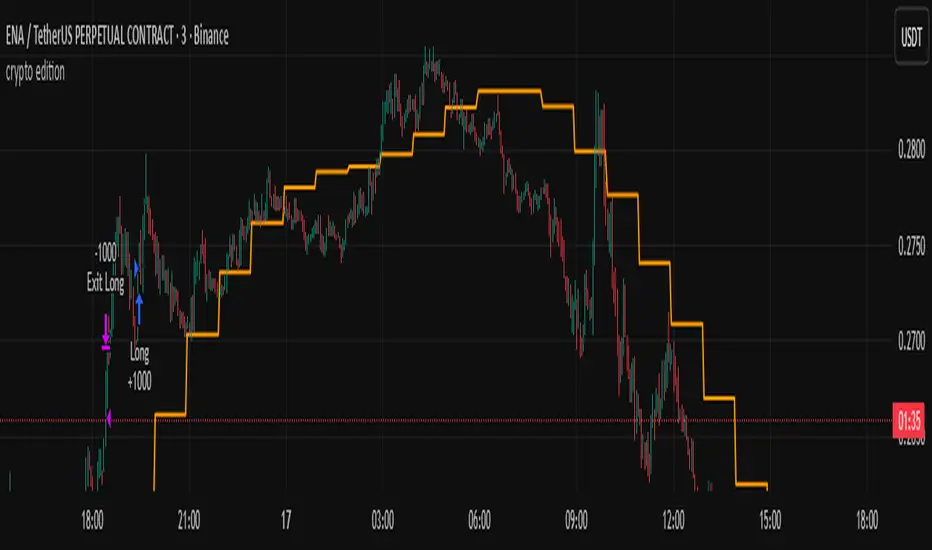

crypto editionUnlock the power of advanced algorithmic trading with this high-precision Crypto Trend-Following Strategy, engineered to adapt to any timeframe, yet highly optimized for lower-timeframe trading (M1–M15) where volatility creates exceptional opportunities — especially on small-cap and newly listed crypto coins.

Trend-Adaptive 3-Band Reversal CloudThis indicator plots a trend-adaptive, volatility-based 3-band cloud on your chart to visually contextualize potential high-probability reversal, balance, and exhaustion price zones — all in strict alignment with TradingView’s house rules and best compliance practices.

How It Works

Trend Detection:

The script determines short-term trend direction using two adjustable EMAs (fast and slow). When the fast EMA is above the slow, the environment is classified as an uptrend; when below, as a downtrend.

Adaptive Bands and Clouds:

Around the dynamic trend baseline, three cloud “bands” are drawn using multiples of an ATR (Average True Range) volatility filter, automatically adjusting for evolving market conditions:

Middle Band (Fair Value Zone): Area around the baseline, where price is statistically balanced.

Upper Outer Band: In an uptrend, this shows a potential 'exhaustion/overextension' area; in a downtrend, it can act as a deep pullback or reversal area.

Lower Outer Band: In an uptrend, this highlights a possible 'deep pullback/reversal' area; in a downtrend, it becomes the potential exhaustion zone.

Contextual RSI Markers:

When price is in one of the outer bands and RSI is overbought (upper) or oversold (lower), a tiny diamond marker appears on that band as extra context — offering a visual cue for a possible high-momentum exhaustion or deep reversal zone, but never a trade signal or advice.

Visuals and Compliance:

All cloud regions use three different, semi-transparent colors for easy reading, and never block price action.

Labels indicate only “Possible Exhaustion,” “Deep Pullback Zone,” and “Balanced/Fair Value”—the language is strictly neutral and descriptive.

All calculations run only on confirmed, historical bars with zero repainting, no future bar lookahead, and no predictive overlays.

How to Use

Add to Chart:

Simply add the indicator to any chart and timeframe.

Configure:

Adjust the EMA, ATR, and RSI settings via the input panel to best fit your instrument and preferred sensitivity.

Choose band multipliers to widen or contract the cloud according to volatility or your system.

Toggle RSI marker/context highlighting as desired.

Interpretation:

Middle Cloud (“Balanced/Fair Value”): Price in this zone suggests mean reversion, equilibrium, or fair pricing for the session’s volatility/trend conditions.

Outer Clouds: If price reaches an outer cloud, pay attention for potential mean-reversion (if trend persists) or exhaustion zones (especially if a diamond appears).

Uptrend: Lower cloud is where larger pullbacks/reversals are often initiated; upper cloud indicates potential trend exhaustion.

Downtrend: Upper and lower clouds are reversed in interpretation.

Diamond Markers: A red diamond atop the upper band signifies RSI overbought; a lime diamond below the lower band shows RSI oversold. These do not recommend trading—only highlight increased likelihood that buyers/sellers may be overextended.

Best Practices:

Do not use the indicator in isolation or as a signal generator. Combine its context with price action confirmation, volume, or other non-repainting tools.

Use labels only for navigation/context, never as actionable advice.

Technical Details

Inputs/Customization: Fully adjustable (EMAs, ATR period, band multipliers, RSI thresholds, label/marker toggles).

Logic: All code processes only historical closed bars and overlays information in real time.

No repaint, strategy, or alerts: No signals, no script-driven trading, and no claims of prediction or guaranteed probability.

House-rule Clean: The script and its visuals are compliant with TradingView’s publishing requirements, both visually and textually.

Summary:

This tool is designed for traders who want to visually frame high-probability reversal, equilibrium, and exhaustion zones adaptively—while keeping price action primary and avoiding visual or conceptual clutter. Use it to better understand where price may statistically find resistance/support or revert, not to automate signals or guarantee outcomes

WJ STS Session SniperA precision-built indicator designed to support the STS (Session Trading System) framework taught by Jay and customized by Willy.

This tool acts as a decision engine, risk module, and session filter, helping you execute session-based scalps with strict discipline and clean rules.

The STS Companion does not replace TV Blast — it enhances it.

This indicator helps you follow the strategy exactly as intended:

• Only trade key session opens

• Only take trades where multi-timeframe momentum aligns

• Only take trades where volume delta confirms direction

• Only take trades when the session is producing a clean impulse

• Use swing-based stop-loss logic

• Automatically calculate the correct micro contract size

• Only take setups when all conditions match your trading plan

⸻

🎯 The Core Principles Behind the Indicator

The STS strategy is built around a simple philosophy:

“Trade only when the market is moving with force, and avoid 99% of chop.”

This companion implements that philosophy with:

⸻

🕒 High-Volume Session Targeting

The indicator highlights and focuses on the first minutes of major global opens:

• Shanghai / Asia Open

• Frankfurt Open

• London Open

• New York (08:20 futures open)

Each session has a defined “trade window” (default 20 minutes) where institutional liquidity and momentum typically enter the market.

This is where the STS edge lives.

⸻

📊 Multi-Timeframe Sentiment Engine (MTF Bias)

The indicator monitors up to four custom timeframes simultaneously and categorizes momentum as:

• Strong Buy

• Strong Sell

• Buy

• Sell

• Mixed

When ALL selected timeframes agree, bars are highlighted for instant direction clarity:

• Blue bars = all bullish

• White bars = all bearish

⸻

🔥 Volume Delta Engine (Aggression Detection)

Tracks real-time buying/selling pressure using:

• Delta EMA

• Volume filters

• High-volume expansion events

High-volume spikes aligned with trend are marked:

• White dot = bullish high-volume impulse

• Gold dot = bearish high-volume impulse

This identifies when large players are stepping in.

⸻

⚡ Breakout-Based Impulse Filter (“Pseudo Blast”)

Uses a breakout and momentum model to identify:

• The first expansion move after a session open

• Directional commitment

• Low-risk, high-RR scalping opportunities

This is the core trigger that aligns with STS-style entries.

⸻

🧮 Structural Stop-Loss + Position Sizing

The indicator automatically calculates:

• Nearest 1-minute swing high/low

• Stop distance in ticks

• Micro contract size based on your dollar risk input

This ensures high consistency and discipline, perfect for:

• TopStep

• Apex

• FundedNext

• Any account with a daily loss limit or tight risk rules

Setup signals only print when risk, stop, and volatility conditions are all safe.

⸻

🟢 When a Valid Setup Appears

The indicator will show:

• A triangle (long/short candidate)

• A label with:

• Stop-loss in ticks

• Recommended micro contract size

This means the system has aligned:

1. Session window

2. MTF bias

3. Volume delta

4. Breakout impulse

5. Proper stop

6. Safe position size

Only then does the STS Companion mark a bar.

⸻

📌 How to Use This Indicator

1. Wait for a major session open

Focus especially on Shanghai, Frankfurt, London, and NY.

2. Check the MTF bias

Blue = all bullish

White = all bearish

Avoid mixed conditions.

3. Confirm volume delta

Look for white/gold high-volume dots aligned with direction.

4. Wait for an impulse breakout

A triangle marks the potential STS entry bar.

5. Use the provided micro size

Position sizing is based on swing stop + your risk per trade.

6. Execute your plan

The indicator supports discipline — it does not override your rules.

⸻

⭐ Designed For

• Gold futures traders (XAUUSD / GC / MGC)

• Session scalpers

• Prop firm traders

• Momentum + breakout scalpers

• Anyone wanting mechanical, rule-based setups

⸻

🔒 Important

This indicator does not auto-trade.

It does not duplicate TV Blast.

It provides a clean, rules-based system to support the STS session methodology with precision and consistency.

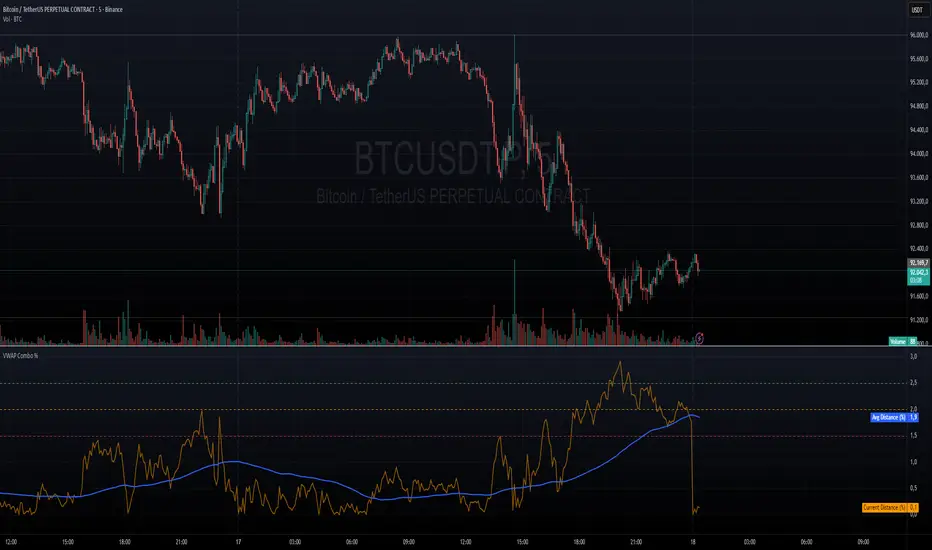

VWAP + VWAP Distance Avg + Alert Lines (%)VWAP Distance & Average Distance Indicator – Detailed Description

The VWAP + VWAP Distance Avg + Alert Lines (%) indicator is designed to measure the distance of the current price from the VWAP (Volume Weighted Average Price), as well as the average distance over a specified period. This tool is particularly useful for traders who use the VWAP as a magnet for price, helping to identify potential trend changes and areas where price may revert toward the VWAP.

Key Features

Current Distance (%)

Calculates the absolute percentage difference between the current price and the VWAP

This line shows how far the price has moved away from the VWAP at any given moment.

Average Distance (%)

Calculates a simple moving average (SMA) of the distance over a specified lookback period.

This provides a reference for typical price deviations from the VWAP, helping traders assess whether the current distance is unusually high or low.

Alert Lines (%)

Allows up to three customizable horizontal alert lines, which can be turned on or off individually.

Each line can be configured with:

Value in percent.

Color.

Line thickness.

These lines serve as visual thresholds, helping traders detect extreme deviations from the VWAP that may precede trend reversals.

Use Case – Detecting Potential Trend Changes

Traders often treat the VWAP as a price magnet, where price tends to revert after significant deviations.

When the current distance exceeds typical average levels or crosses an alert line, it can signal that the price may revert toward the VWAP, potentially indicating a shift in trend or a high-probability mean-reversion scenario.

Disclaimer

This indicator is provided for educational and analytical purposes only. It does not constitute financial advice, and trading decisions are always the sole responsibility of the individual trader. Users should carefully evaluate market conditions and their own risk tolerance before taking any trade.

Better used with VWAP on chart , and be careful around the end of session, for now this works just for session...

still improving on this....

Alpha VWAP Regime🔥 Alpha VWAP Regime — Institutional VWAP Strategy (Closed Source)

Alpha VWAP Regime is a multi-layered VWAP trading system that identifies the active market regime and adapts its signals based on institutional liquidity behavior.

This strategy is closed-source because it uses a proprietary combination of VWAP structures, anchored pivot logic, band deviations, and regime detection filters that are not publicly available.

🧠 How the Strategy Works (Conceptual Explanation)

This strategy does not rely on a single VWAP line.

Instead, it builds a VWAP matrix consisting of:

1) Session VWAP

Defines fair value for the current session.

Used to detect intraday directional bias.

2) Anchored VWAP (AVWAP)

Automatically anchored to swing highs and lows (pivot-based).

Tracks where large players accumulated or distributed positions.

3) VWAP Bands (±1σ and ±2σ)

Used as dynamic volatility envelopes:

±1σ = fair-value zone / no-trade area

±2σ = mean-reversion extremes

4) Market Regime Classification (ADX-based)

The strategy determines which environment the market is in:

Trending Regime: ADX above threshold

Ranging Regime: ADX below threshold

Breakout Regime: Volume-based breakout of AVWAP

Each regime activates a different entry model.

📌 Entry Logic (High-Level Overview)

Trend Mode

Triggered only when ADX confirms a trend.

Entries occur near VWAP or −1σ using price-action confirmation.

Mean Reversion Mode

Activated when the market is ranging.

Entries target the ±2σ deviation bands.

Breakout Mode

Triggered by price crossing AVWAP with above-average volume.

Used to catch institutional continuation moves.

ALL Mode

Combines the three models for a full adaptive system.

📉 Exits & Risk Management

All stops and targets use ATR-based volatility sizing

Trend trades aim for larger targets

Mean-reversion trades aim for smaller snapback moves

Breakouts use wider stops but high R:R

🔍 How to Use the Strategy

Load the script on a clean chart

Choose your preferred regime mode (Trend / MR / Breakout / ALL)

Optionally hide VWAP indicators and display signals only

Use realistic position sizing and commissions

Evaluate performance across multiple assets and timeframes

🔒 Why It Is Closed-Source

The code uses:

A custom anchoring engine

Multi-layered regime filters

Dynamic VWAP matrix

Prop logic for bias scoring

These components were built from scratch and form a unique decision model, so the source is protected.

🇸🇦 الشرح العربي لاستراتيجية Alpha VWAP Regime

Alpha VWAP Regime هي استراتيجية تداول مؤسسية متقدمة تعتمد على تحليل السيولة، وتحديد حالة السوق (Market Regime)، ودمج عدة طبقات من VWAP داخل نموذج واحد متكيف.

الهدف من الاستراتيجية هو التداول في المناطق التي يتواجد فيها المال الذكي، وتجنب التداول في المناطق العشوائية أو منخفضة الجودة.

________________________________________

🧠 كيف تعمل الاستراتيجية؟

الاستراتيجية لا تعتمد على VWAP واحد، بل تستخدم “مصفوفة VWAP” كاملة تتكوّن من:

1) VWAP اليومي (Session VWAP)

يُستخدم لتحديد القيمة العادلة خلال الجلسة، وتحديد الاتجاه اللحظي (Intraday Bias).

________________________________________

2) VWAP المثبّت (Anchored VWAP)

يتم تثبيته تلقائيًا على:

• القمم المهمة (Swing Highs)

• القيعان المهمة (Swing Lows)

ويساعد في تحديد مناطق تمركز المؤسسات، ومناطق الانعكاس أو الاختراقات الحقيقية.

________________________________________

3) نطاقات VWAP (±1σ و ±2σ)

تُستخدم كأغلفة ديناميكية للسيولة والتقلب:

• ±1σ = منطقة القيمة العادلة (Fair-Value Zone)

→ غالبًا منطقة غير مناسبة للتداول (No-Trade Zone)

• ±2σ = مناطق التشبّع الحركي (Extremes)

→ مناسبة لاستراتيجيات الانعكاس (Mean Reversion)

________________________________________

4) تصنيف حالة السوق Market Regimes

الاستراتيجية تستخدم مؤشر ADX لتحديد حالة السوق الحالية:

حالة السوق الوصف

Trending اتجاه واضح وقوي

Ranging تذبذب بدون اتجاه

Breakout اختراق مدعوم بحجم تداول

كل Regime يفعّل نموذج دخول مختلف داخل الاستراتيجية.

________________________________________

🎯 نماذج الدخول داخل الاستراتيجية

1) نموذج الاتجاه (Trend Mode)

يعمل فقط عندما يكون السوق في اتجاه حقيقي.

يعتمد على دخول Pullbacks قرب VWAP أو نطاق −1σ مع تأكيد شموعي.

________________________________________

2) نموذج الانعكاس (Mean Reversion Mode)

يعمل فقط عندما يكون السوق متذبذبًا (Range).

الدخول عند لمس ±2σ بهدف العودة نحو VWAP.

________________________________________

3) نموذج الاختراق (Breakout Mode)

يستخدم اختراقات Anchored VWAP

ولكن بشرط وجود حجم تداول أعلى من المتوسط (Volume Confirmation).

________________________________________

4) وضع الدمج (ALL Mode)

يجمع بين النماذج الثلاثة ويجعل الاستراتيجية متكيفة تلقائيًا مع كل حالات السوق.

________________________________________

📉 الخروج وإدارة المخاطر

تستخدم الاستراتيجية نظامًا ديناميكيًا لإدارة المخاطر:

• وقف الخسارة مبني على ATR

• الأهداف مبنية على طبيعة النموذج

• الصفقات الاتجاهية تستهدف R:R أعلى

• صفقات MR أقصر وأسرع

• صفقات Breakout أوسع ولكن مدعومة بزخم قوي

________________________________________

🧩 كيفية استخدام الاستراتيجية

1. ضع الاستراتيجية على رسم بياني نظيف بدون مؤشرات إضافية

2. اختر نموذج الدخول المناسب من الإعدادات

3. فعّل أو أخفِ خطوط VWAP حسب الحاجة

4. استخدم إعدادات مخاطرة واقعية

5. اختبر الاستراتيجية على عدة أسواق وفريمات

________________________________________

🔒 سبب إغلاق الكود

تم إغلاق الكود لأنها تعتمد على:

• محرك تثبيت AVWAP خاص

• نظام Regime Detection متقدم

• مصفوفة VWAP متعددة الطبقات

• منطق دخول/خروج خاص تم تطويره بالكامل

كل ذلك يتطلب حماية الملكية الفكرية، لذا تم نشرها Closed-Source.

Swing Wicks + Bodies; Stolen from LeviathanSwing Wicks + Bodies — Stolen from Leviathan

This indicator automatically detects swing highs and lows by separating wick swings from body swings, providing a precise view of liquidity zones on the chart.

It draws:

• wick-based swing levels

• body-based swing levels

• dynamic liquidity boxes showing unfilled price zones

• touch counters (T1, T2, T3…)

• optional HTF levels (H1/H4…) for multi-timeframe context

Included features:

• hide filled levels

• keep only the most recent unfilled levels

• full customization (colors, line styles, text size, minimum box height)

• optional “extend until filled” mode

• volume threshold filter

• lookback limitation (history in days)

VIX Spike/Drop TrackerWhat It Does

Core Functionality:

Monitors daily VIX percentage changes and identifies significant spikes (fear increases) and drops (fear decreases)

Backtests historical SPY performance following VIX events across multiple timeframes (1-day, 2-day, 3-day, and 1-week)

Calculates win rates and average returns for each scenario

Provides real-time VIX statistics including percentile rankings, distance from moving average, and momentum

Key Features:

Historical Analysis: Analyzes up to 2,500 bars of historical data to build robust statistical profiles

Dual Event Tracking: Separate statistics for VIX spikes (fear events) and VIX drops (fear subsiding)

Performance Metrics: Shows average SPY returns and win rates at 1, 2, 3, and 5-day intervals

VIX Context: Real-time VIX level, daily change, moving average distance, percentile rank, and 3-day momentum

Smart Predictions: Context-aware signals based on VIX patterns and consecutive spike/drop days

Visual Alerts: Chart annotations and background highlighting for significant events

How to Use It

Setup:

Add the indicator to your chart (works on any timeframe, but analyzes daily data)

Adjust the VIX threshold (default 10%) to define what constitutes a "significant" move

Set the historical lookback period (500 bars = ~2 years of data)

Reading the Statistics Table:

Left side: Statistics for VIX spikes (when fear increases)

Right side: Statistics for VIX drops (when fear decreases)

D1/D2/D3/Wk columns: Average SPY returns 1, 2, 3, and 5 days after the VIX event

Win %: Percentage of time SPY was positive at each interval

n: Sample size (number of historical events analyzed)

Bottom row: Current VIX statistics and market positioning

Interpreting Predictions:

🔴 "FEAR SPIKE - SPY LIKELY DOWN": VIX spiking, historical data shows negative SPY tendency

🟢 "FEAR SUBSIDING - SPY LIKELY UP": VIX dropping, historical data shows positive SPY tendency

🟠 "VIX ELEVATED - MEAN REVERSION DUE": VIX extended above its moving average

🟡 "VIX SUPPRESSED - COMPLACENCY RISK": VIX unusually low, potential volatility expansion ahead

Best Practices

Use this as a statistical context tool, not a standalone trading signal

Combine with your own technical analysis and risk management

Pay attention to win rates alongside average returns for edge assessment

Monitor consecutive spike/drop days for potential mean reversion setups

Higher sample sizes (n) provide more reliable statistics

Customization

Fully customizable colors, threshold levels, table size, and VIX moving average period. Enable/disable chart labels based on your preference for clean charts.

This indicator provides historical statistical context and does not guarantee future performance. Past results do not predict future outcomes.

Financial Stress Conditions Proxy | QuantLapse📘 Financial Stress Conditions Proxy | QuantLapse

Overview:

The Financial Stress Conditions Proxy (FSCP) by QuantLapse is a multi-factor quantitative indicator that measures systemic financial stress across key macro and liquidity benchmarks.

By blending the High-Yield Spread (BAMLH0A0HYM2), Volatility Index (VIX), Secured Overnight Financing Rate (SOFR), and Reverse Repo Operations (RRPONTSYD) into a unified z-score model, this tool visualizes the market’s underlying tension and relief cycles — conditions often associated with risk-off capitulation and market bottoms.

Each component is normalized via a z-score transformation to express how far current readings deviate from historical means, then averaged into a composite “Financial Stress Score.” The result is a dynamic, color-coded column plot that shifts hue as systemic risk compresses or expands.

Purpose

I built this model to track stress inflection points in the global financial system — particularly to identify moments when macro fear, liquidity withdrawal, and volatility compression converge.

These events often precede bottoming phases across risk assets such as equities and crypto.

The indicator serves as a quantitative proxy for the psychological extremes of the market:

Red tones (high stress): systemic strain, deleveraging, or panic phases — potential long-term opportunity zones.

Yellow-green transition: normalization, improving liquidity conditions.

Blue-teal range: stability and low-stress periods — often mid-cycle.

High Stress zones (Quantitative Tightening) -> Red and Orange

Neutral Zones -> Green and Yellow

Low Stress Zone (Quantitative Easing) --> Green to Blue

How It Works

Inputs & Data Sources

BAMLH0A0HYM2 → High-Yield Corporate Bond Spread (credit stress).

VIX → Implied volatility (equity market fear).

SOFR → Funding rate indicator (short-term liquidity).

RRPONTSYD → Reverse repo operations (systemic liquidity absorption).

Normalization Process

Each data stream is smoothed using a user-defined moving average and standard deviation window (default 150 periods).

A z-score is computed:

𝑍=𝑋−Mean/Standard Deviation

The four z-scores are averaged to produce a single composite stress score.

Color Encoding

The composite score is segmented into 16 calibrated stress bands (from +1.6 to −1.6).

Each band corresponds to a color — red at the top for maximum stress, shifting to bright greens and teals as stress subsides.

Colors are assigned dynamically to the plotted columns, creating an intuitive “heat bar” of systemic tension over time.

Interpretation

Rising, bright red columns: liquidity tightening, macro uncertainty, or panic — potential market bottom zones when fear peaks.

Fading yellow → green: stabilization, easing conditions, and early recovery.

Cool blue/teal tones: complacency or extended calm — often late-cycle risk.

Use the FSCP as a macro overlay, not a direct buy/sell trigger.

Its purpose is to provide environmental context — showing when the market is collectively stressed versus when liquidity and confidence return.

Trading Applications

Bottom Detection:

Historically, sustained red/orange conditions have coincided with market capitulation (macro or crypto bottoms).

Watch for color transitions from red → orange → yellow as potential recovery signals.

Risk Management:

Avoid leverage or high exposure when the score is rising rapidly into red zones.

Gradually scale exposure as colors normalize.

Macro Confirmation Tool:

Combine with RSI, breadth indicators, or on-chain data to confirm reversals.

Works well on daily or weekly timeframes for swing and position traders.

Customization

Adjustable lookback periods for mean and standard deviation (default 150).

Works on all markets (equities, crypto, forex) since it sources macroeconomic benchmarks directly.

Can be layered with volatility or liquidity indicators for confirmation.

Why I Built It (originality)

Markets bottom when fear meets exhaustion.

I wanted a tool that quantified that fear in real-time — not by price patterns, but by systemic stress itself.

By merging credit risk, volatility, funding rates, and central bank operations, this model provides a quantitative heartbeat of the financial system — and it visually shows when that heartbeat skips a beat.

In my own trading, I use FSCP to identify macro dislocations and liquidity events that typically precede large recoveries.

It’s not about prediction — it’s about positioning yourself when the system is stretched too far.

Best Practices

Use on higher-timeframe charts (D/W) for context.

Combine with your technical system for entries/exits.

Treat extreme stress as potential accumulation zones, not immediate buy signals.

Allow several sessions of color normalization before confirming reversals.

Disclaimer

This indicator is for educational and research purposes only.

It is not financial advice and does not guarantee future results. Always combine with your own analysis and risk controls before trading decisions.

Summary

The Financial Stress Conditions Proxy translates complex inter-market data into an easy-to-read, color-coded stress bar.

It visually captures the emotional and systemic pulse of global markets — helping traders recognize when panic is peaking and opportunity is quietly forming.

Use it as your quant compass for navigating bottoms in volatile markets.

ATR or % Based Trailing Stop for Delta Exchange (trade_crush)This indicator calculates and visually displays a dynamic trailing stop line on the chart based on either the Average True Range (ATR) or a fixed percentage of the current close price. Designed especially for futures or crypto traders using Delta Exchange, it helps determine where to place trailing stop loss orders to manage risk effectively.

DCA Bot v7 - Cryptosa Nostra 1.0Technical Overview: Adaptive RSI DCA Bot

This is a sophisticated DCA (Dollar Cost Averaging) indicator designed for accumulating assets and managing portfolio distribution. It does not trade on simple RSI crosses. Instead, it combines multi-zone RSI analysis with ATR-based volatility triggers to execute staggered, dynamically-sized trades.

Its core feature is a "learning" engine that adapts its own settings over time. This "brain" can be trained on historical data and then applied to your real-time portfolio holdings via a "Live Override" feature.

Core Logic: How It Works

A trade is only executed when two conditions are met simultaneously:

The RSI Condition: The RSI must be inside one of the four pre-defined zones.

The Price Condition: The price must cross a "trigger line" (the green or red line) that is dynamically calculated based on volatility.

1. The Four RSI Zones

This script uses four distinct zones to determine the intent to trade:

Deep Buy Zone (Default: RSI <= 35 & Downtrend): This is the primary "value" buy signal. It only activates if the RSI is deeply oversold and the price is below the 200-period Trend MA.

Reload Buy Zone (Default: RSI 40-50 & Uptrend): This is a "buy the dip" signal. It looks for minor pullbacks during an established uptrend (price above the 200-period Trend MA).

Profit-Taking Zone (Default: RSI 70-80): Triggers a standard, small sell when the market is overbought.

Euphoria Zone (Default: RSI >= 80): Triggers a larger, more aggressive sell during extreme "blow-off" tops.

2. Dynamic Trade Sizing

The amount to buy or sell is not fixed. It scales dynamically based on how high or low the RSI is:

Buy Sizing: Spends a higher percentage of available cash when RSI is at its lowest (e.g., 35) and a smaller percentage when it's at the top of the reload zone (e.g., 50).

Sell Sizing: Sells a smaller percentage of holdings when RSI just enters the overbought zone (e.g., 70) and a much larger percentage when it's in the euphoria zone (e.g., 80+).

3. The "Adaptive Brain" (ATR Multipliers)

This is the script's learning mechanism. The green/red trigger lines are calculated as: Last Trade Price +/- (ATR * Multiplier).

This "Multiplier" is the brain. It adapts based on trade performance.

After a successful trade (as defined by profit_target_multiplier), the bot gets more confident and reduces the multiplier. This places the next trigger line closer to the price, making it more aggressive.

After a losing trade (as defined by loss_limit_multiplier), the bot gets more cautious and increases the multiplier. This places the next trigger line further away, making it more patient.

How to Use This Indicator

This script is designed to be "trained" on historical data to provide relevant signals for today.

To Train the Brain: In the settings, go to "1. Backtest Settings". Set the "Start Date (For Learning)" to a date in the past (e.g., 6 months or 1 year ago). The script will run a simulation from that date, allowing its Adaptive Multipliers (the "brain") to adjust to the market's volatility.

To See Live Signals: In "2. Live Portfolio Override", check the box "Override Backtest Balance?" and enter your real current coin and USD holdings.

Result: The "Live Status" table (top-right) will now display signals from the trained brain but will calculate the "Potential Buy %" and "Potential Sell %" based on your real portfolio. The "Buy Multi" and "Sell Multi" fields show you the brain's current learned values.

Dashti XAU Liquidity Map ELITE"No Sweep = No Trade

No BOS = No Trade

No Killzone = No Trade

No Volume = No Trade"

Daily ATR vs Move (black & white) + PipsTop of Chart, Mid. Gives the user an idea of what trend is doing and how the current price compares to daily ATR.

Used on this example below to indicate we are within the bottom range for the day, and price has potential to move up without worry of exhaustion.

XAUUSD Recovery for FamilyXAUUSD Recovery for Family is a trend-tracking tool based on a stepped 109-period EMA.

It highlights market direction using automatic color changes and background shading.

How It Works

A modified 109-period EMA is used to detect trend bias

The line only updates in steps after a fixed number of bars (MA Step = 33)

Background color changes when trend direction shifts

Alerts notify the trader when price crosses above or below the trend line

What It Shows

🟢 Green chart background = bullish bias

🔴 Red chart background = bearish bias

📢 Alert signals are generated when the price crosses the stepped EMA

What It Does NOT Do

❌ It does not execute trades automatically

❌ It does not guarantee profit or accuracy

❌ It does not repaint signals

Important Notes

This is a trend visualization tool only

Always combine with proper risk management and confirmation tools

Past performance is not a guarantee of future results

This script is for educational and research purposes

Bollinger Bands Regression Forecast [BigBeluga]🔵 OVERVIEW

The Bollinger Bands Regression Forecast combines volatility envelopes from Bollinger Bands with a linear regression-based projection model .

It visualizes both current and future price zones by extrapolating the Bollinger channel forward in time, giving traders a statistical forecast of probable support and resistance behavior.

🔵 CONCEPTS

Classic Bollinger Bands use a moving average (basis) and standard deviation (deviation) to form dynamic envelopes around price.

This indicator enhances them with linear regression slope detection , allowing it to forecast how the band may expand or contract in the future.

Regression is applied to both the band’s basis and deviation components to predict their trajectory for a user-defined number of Forecast Bars .

The resulting forecast creates a smoothed, funnel-shaped projection that dynamically adapts to volatility.

▲ and ▼ markers highlight potential mean reversion points when price crosses the outer bounds of the bands.

🔵 FEATURES

Forecast Engine : Uses linear regression to project Bollinger Band movement into the future.

Dynamic Channel Width : Adapts standard deviation and slope for realistic volatility modeling.

Auto-Labeled Levels : Displays live upper and lower forecast values for quick reference.

Cross Signals : Marks potential overbought and oversold zones with ▲/▼ signals when price exits the band.

Trend-Adaptive Basis Color : Basis line automatically switches color to represent short-term trend direction.

Customizable Colors and Widths for complete visual control.

🔵 HOW TO USE

Apply the indicator to visualize both current Bollinger structure and its forward projection.

Use ▲/▼ breakout markers to identify short-term reversals or volatility shifts.

When price consistently rides the upper band forecast, the trend is strong and likely continuing.

When regression shows narrowing bands ahead, expect a volatility contraction or consolidation period.

For range traders, outer projected bands can be used as potential mean reversion entry points .

Combine with volume or momentum filters to confirm whether breakouts are genuine or fading.

🔵 CONCLUSION

Bollinger Bands Regression Forecast transforms classic Bollinger analysis into a predictive forecasting model .

By merging volatility dynamics with regression-based extrapolation, it provides traders with a forward-looking visualization of likely price boundaries — revealing not only where volatility is but also where it’s heading next.

2-Stage Dashboard (SQZPRO Wide + EMA)Dashboard for Darvas Box EMA momentum traders, located in the bottom right, mostly for quickly screening if a setup is viable.

- EMAs are 9 & 21

- SQZPRO set to wide squeezes

Long setup:

- Green SQZPRO row

- Green EMA row

Short setup:

- Green SQZPRO row

- Red EMA row