Slope_TKLibrary "Slope_TK"

This library calculate the slope of a serie between two points

The serie can be ta.ema(close,200) for example

The size is the number of bars between the two points for the slope calculation, for example it can be 10

slope_of_ema200 = slope(t a.eam(close, 200) , 10 )

slope( float serie, int size )

MATH

String_Encoder_DecoderLibrary "String_Encoder_Decoder"

String encoder and decoder to use in internal data tranfer in script calculations.

In example, script encode 125 values once and then decode them every candle.

encode(array or values (val1,val2,val3,val4,val5,val6)

encode: encode some values into string

Parameters:

array : of values or values1, value2 (up to 6 values)

(input values must be stringified)

Returns: encoded value

decode(val)

decode: decode into string

Parameters:

val : value to decode, must be stringified

Returns: decoded array of stringified values

fast_utilsLibrary "fast_utils"

This library contains my favourite functions. Will be updated frequently

count_int_digits()

Count int digits in number

Returns: : number of int digits in number

count_float_digits()

Count float digits in number

Returns: : number of float digits in number

stringify()

Convert values in array or matrix into string values

Returns: : array or matrix of string values

arrcompare()

Compare values in arrays

Returns: : bool value

arrdedup()

Remove duplicate values in array

Returns: : array without duplicates

ResInMins()

Converts current resolution in minutes

Returns: : return float number of minuted

MultOfRes(res, mult)

Convert current float TF in minutes to target string TF in "timeframe.period" format.

Parameters:

res : : current resolution in minutes

mult : : Multiple of current TF to be calculated.

Returns: : timeframe format string

fractionLibrary "fraction"

Fraction Creation and Basic Operations.

Cracked a tough problem in making this Polarity Agnostic Decimal without a cheating "abs * sign of input".

it's quite fast, however still test for errors before production use.

>> Big Neon Sign on 1/0 value. <<

Int Array (LOC 0/1)..

To/From Decimal(float)

Comparison ( < / == / >)

Add / Sub / Mult / Div

Invert polarity +/-

String output with 2 formats ..

make(_numerator, _denominator, _val)

Parameters:

_numerator : (int) above the line integer ie: ____ of (___ / bottom )

_denominator : (int) below the line integer ie: ____ of (top / ______ )

_val : (int) OPTIONAL (for no real reason including it) integer to multiply

Returns: array where index 0 is Numerator, 1 is Denominator

add(_fraction, _fraction2)

Perform add operation (left adds right onto )

Parameters:

_fraction : (array) left side Fraction Object

_fraction2 : (array) right side Fraction Object

Returns: array where index 0 is Numerator, 1 is Denominator

subtract(_fraction, _fraction2)

Perform subtract operation (left subtracts right from )

Parameters:

_fraction : (array) left side Fraction Object

_fraction2 : (array) right side Fraction Object

Returns: array where index 0 is Numerator, 1 is Denominator

multiply(_fraction, _fraction2)

Perform multiply operation (left multiplies by right )

Parameters:

_fraction : (array) left side Fraction Object

_fraction2 : (array) right side Fraction Object

Returns: array where index 0 is Numerator, 1 is Denominator

divide(_fraction, _fraction2)

Perform divide operation (left divides by right )

Parameters:

_fraction : (array) left side Fraction Object

_fraction2 : (array) right side Fraction Object

Returns: array where index 0 is Numerator, 1 is Denominator

negative(_fraction)

Perform Negative number inversion ie: (-1/2 => 1/2) or (3/5 => -3/5)

Parameters:

_fraction : (array) Fraction Object to invert to/from negative

Returns: array where index 0 is Numerator, 1 is Denominator

isSmaller(_fraction, _fraction2)

Check if first fraction is smaller

Parameters:

_fraction : (array) left side Fraction Object

_fraction2 : (array) right side Fraction Object

Returns: True if smaller, false if bigger

isLarger(_fraction, _fraction2)

Check if first fraction is larger

Parameters:

_fraction : (array) left side Fraction Object

_fraction2 : (array) right side Fraction Object

Returns: True if smaller, false if bigger

isEqual(_fraction, _fraction2)

Check if first fraction is equal

Parameters:

_fraction : (array) left side Fraction Object

_fraction2 : (array) right side Fraction Object

Returns: True if smaller, false if bigger

fromDec(_input, _epsilon, _iterations)

Convert Decimal to Fraction array

note : this is my own Negative Number Capable (tiny speed loss)

adaptation of the fastest algo out there

Exclusive for Tradingview.

Parameters:

_input : (float) Decimal Input

_epsilon : (int) (OPTIONAL) to precision 0's after dec 0.0000 -> epsilon 0's

_iterations : (int) (OPTIONAL) Maximum iterations Till give up

Returns: array where index 0 is Numerator, 1 is Denominator

toDec()

Convert Fraction to Decimal Output

Returns: Float of fration

toString(_fraction)

Create "A/B" or "A and B/C" String Value of Fraction.

Parameters:

_fraction : (array) Fraction Object to invert to/from negative

Returns: String as (-)? A and B/C format

Encoder DecoderLibrary "EncoderDecoder"

Simple example how to encode some values into float number and then decode it back to original values

f_calctype()

Encode parameter

Returns: encoded value

f_calctype()

Decode parameter

Returns: decoded value

f_srctype()

Encode parameter

Returns: encoded value

f_srctype()

Decode parameter

Returns: decoded value

f_encode(calc_type, src_type, tf, length)

Encodes 4 paramters into float number

Parameters:

calc_type : 1st paramter to encode (its values defined in f_calctype functions) max number of values that can be encoded = 100

src_type : 2nd paramter to encode (its values defined in f_src_type functions) max number of values that can be encoded = 100

tf : 3rd paramter to encode (may be int number with format.price precision length!)

length : 4th paramter to encode (may be any int number)

Returns: float number

f_decode()

Decodes 4 paramters into tuple

Returns: tuple

kNNLibrary "kNN"

Collection of experimental kNN functions. This is a work in progress, an improvement upon my original kNN script:

The script can be recreated with this library. Unlike the original script, that used multiple arrays, this has been reworked with the new Pine Script matrix features.

To make a kNN prediction, the following data should be supplied to the wrapper:

kNN : filter type. Right now either Binary or Percent . Binary works like in the original script: the system stores whether the price has increased (+1) or decreased (-1) since the previous knnStore event (called when either long or short condition is supplied). Percent works the same, but the values stored are the difference of prices in percents. That way larger differences in prices would give higher scores.

k : number k. This is how many nearest neighbors are to be selected (and summed up to get the result).

skew : kNN minimum difference. Normally, the prediction is done with a simple majority of the neighbor votes. If skew is given, then more than a simple majority is needed for a prediction. This also means that there are inputs for which no prediction would be given (if the majority votes are between -skew and +skew). Note that in Percent mode more profitable trades will have higher voting power.

depth : kNN matrix size limit. Originally, the whole available history of trades was used to make a prediction. This not only requires more computational power, but also neglects the fact that the market conditions are changing. This setting restricts the memory matrix to a finite number of past trades.

price : price series

long : long condition. True if the long conditions are met, but filters are not yet applied. For example, in my original script, trades are only made on crossings of fast and slow MAs. So, whenever it is possible to go long, this value is set true. False otherwise.

short : short condition. Same as long , but for short condition.

store : whether the inputs should be stored. Additional filters may be applied to prevent bad trades (for example, trend-based filters), so if you only need to consult kNN without storing the trade, this should be set to false.

feature1 : current value of feature 1. A feature in this case is some kind of data derived from the price. Different features may be used to analyse the price series. For example, oscillator values. Not all of them may be used for kNN prediction. As the current kNN implementation is 2-dimensional, only two features can be used.

feature2 : current value of feature 2.

The wrapper returns a tuple: [ longOK, shortOK ]. This is a pair of filters. When longOK is true, then kNN predicts a long trade may be taken. When shortOK is true, then kNN predicts a short trade may be taken. The kNN filters are returned whenever long or short conditions are met. The trade is supposed to happen when long or short conditions are met and when the kNN filter for the desired direction is true.

Exported functions :

knnStore(knn, p1, p2, src, maxrows)

Store the previous trade; buffer the current one until results are in. Results are binary: up/down

Parameters:

knn : knn matrix

p1 : feature 1 value

p2 : feature 2 value

src : current price

maxrows : limit the matrix size to this number of rows (0 of no limit)

Returns: modified knn matrix

knnStorePercent(knn, p1, p2, src, maxrows)

Store the previous trade; buffer the current one until results are in. Results are in percents

Parameters:

knn : knn matrix

p1 : feature 1 value

p2 : feature 2 value

src : current price

maxrows : limit the matrix size to this number of rows (0 of no limit)

Returns: modified knn matrix

knnGet(distance, result)

Get neighbours by getting k results with the smallest distances

Parameters:

distance : distance array

result : result array

Returns: array slice of k results

knnDistance(knn, p1, p2)

Create a distance array from the two given parameters

Parameters:

knn : knn matrix

p1 : feature 1 value

p2 : feature 2 value

Returns: distance array

knnSum(knn, p1, p2, k)

Make a prediction, finding k nearest neighbours and summing them up

Parameters:

knn : knn matrix

p1 : feature 1 value

p2 : feature 2 value

k : sum k nearest neighbors

Returns: sum of k nearest neighbors

doKNN(kNN, k, skew, depth, price, long, short, store, feature1, feature2)

execute kNN filter

Parameters:

kNN : filter type

k : number k

skew : kNN minimum difference

depth : kNN matrix size limit

price : series

long : long condition

short : short condition

store : store the supplied features (if false, only checks the results without storage)

feature1 : feature 1 value

feature2 : feature 2 value

Returns: filter output

fibo_levelsLibrary "Fibo_levels"

Calculate Fibo levels from any 2 levels. Your need know only 2 price of 2 levels for calculate any level of Fibo: function 'fibo_lvl',

or calculate array of price Fibo levels : function 'fibo_lvls'

fibo_lvl(fibo_lvl1, price1, fibo_lvl2, price2, calc_level)

Parameters:

fibo_lvl1 : First of any level of fibo from 0 to 1 (example 0.236)

price1 : Price for 1th any level (example 2356.1)

fibo_lvl2 : Second of any level of fibo from 0 to 1 (example 0.382)

price2 : Price for 2th any level (example 2497.4)

calc_level : Price for level to calculate (example 0.5)

Returns: return price for calc_level fibo

fibo_lvls(bars, time1, time2, fibo_lvl1, price1, fibo_lvl2, price1)

Parameters:

fibo_lvl1 : First of any level of fibo from 0 to 1 (example 0.236)

price1 : Price for 1th any level (example 2356.1)

fibo_lvl2 : Second of any level of fibo from 0 to 1 (example 0.382)

price1 : Price for 2th any level (example 2497.4)

Returns: array of price for fibo levels : (0.0, 0.118, 0.236, 0.384, 0.5, 0.618, 0.786, 1.0, 1.27,-0.27,1.618,-0.618)

LibIndicadoresUteisLibrary "LibIndicadoresUteis"

Collection of useful indicators. This collection does not do any type of plotting on the graph, as the methods implemented can and should be used to get the return of mathematical formulas, in a way that speeds up the development of new scripts. The current version contains methods for stochastic return, slow stochastic, IFR, leverage calculation for B3 futures market, leverage calculation for B3 stock market, bollinger bands and the range of change.

estocastico(PeriodoEstocastico)

Returns the value of stochastic

Parameters:

PeriodoEstocastico : Period for calculation basis

Returns: Float with the stochastic value of the period

estocasticoLento(PeriodoEstocastico, PeriodoMedia)

Returns the value of slow stochastic

Parameters:

PeriodoEstocastico : Stochastic period for calculation basis

PeriodoMedia : Average period for calculation basis

Returns: Float with the value of the slow stochastic of the period

ifrInvenenado(PeriodoIFR, OrigemIFR)

Returns the value of the RSI/IFR Poisoned of Guima

Parameters:

PeriodoIFR : RSI/IFR period for calculation basis

OrigemIFR : Source of RSI/IFR for calculation basis

Returns: Float with the RSI/IFR value for the period

calculoAlavancagemFuturos(margem, alavancagemMaxima)

Returns the number of contracts to work based on margin

Parameters:

margem : Margin for contract unit

alavancagemMaxima : Maximum number of contracts to work

Returns: Integer with the number of contracts suggested for trading

calculoAlavancagemAcoes(alavancagemMaxima)

Returns the number of batches to work based on the margin

Parameters:

alavancagemMaxima : Maximum number of batches to work

Returns: Integer with the amount of lots suggested for trading

bandasBollinger(periodoBB, origemBB, desvioPadrao)

Returns the value of bollinger bands

Parameters:

periodoBB : Period of bollinger bands for calculation basis

origemBB : Origin of bollinger bands for calculation basis

desvioPadrao : Standard Deviation of bollinger bands for calculation basis

Returns: Two-position array with upper and lower band values respectively

theRoc(periodoROC, origemROC)

Returns the value of Rate Of Change

Parameters:

periodoROC : Period for calculation basis

origemROC : Source of calculation basis

Returns: Float with the value of Rate Of Change

BpaLibrary "Bpa"

TODO: library of Brooks Price Action concepts

isBreakoutBar(atr, high, low, close, open, tail, size)

TODO: check if the bar is a breakout based on the specified conditions

Parameters:

atr : TODO: atr value

high : TODO: high price

low : TODO: low price

close : TODO: close price

open : TODO: open price

tail : TODO: decimal value for a percent that represent the size of the tail of the bar that cant be preceeded to be considered strong close

size : TODO: decimal value for a percent that represents by how much the breakout bar should be bigger than others to be considered one

Returns: TODO: boolean value, true if breakout bar, false otherwise

TradingWolfLibaryLibrary "TradingWolfLibary"

getMA(int, string)

Gets a Moving Average based on type

Parameters:

int : length The MA period

string : maType The type of MA

Returns: A moving average with the given parameters

minStop(float, simple, float, string)

Calculates and returns Minimum stop loss

Parameters:

float : entry price (Close if calculating on the entry candle)

simple : int Calculate how many bars back to look at swings

float : Minimum Stop Loss allowed (Should be x 0.01) if input

string : Direciton of trade either "Long" or "Short"

Returns: Stop Loss Value

intersectLibrary "intersect"

Find Line Intersection X/Y coordinates.

Simple to use, will find intersection if it exists on the segments

if the line segments do not cross on segment, an 'na' value will be returned

if you plot new items with the output coords, they still plot.

avoid this by setting a na(x) condition before plotting new items

get(l1, l2, ( optional _round) )

line intersection coordinates

Parameters:

l1 : (line) first line

l2 : (line) second line

_round : True to make an INT for plotting

if not used, will not round ( overload loophole)

Returns: with x as int if bool is used

na_skip_highestLibrary "na_skip_highest"

Finds the highest historic value over len bars but skip na valued bars (eg, off days). In other words, this will ensure we find the highest value over len bars with a real value, and if there are any na bars in-between, we skip over but the loop will continue. This allows to mimic calculations on markets with off days (eg, weekends).

na_skip_highest(src, len)

Finds the highest historic value over len bars but skip na valued bars (eg, off days). In other words, this will ensure we find the highest value over len bars with a real value, and if there are any na bars in-between, we skip over but the loop will continue. This allows to mimic calculations on markets with off days (eg, weekends).

Parameters:

src : series float source (eg, close)

len : int length, number of recent bars to consider in the window to find the highest value

Returns: highest float highest value found over the len window

KernelFunctionsLibrary "KernelFunctions"

This library provides non-repainting kernel functions for Nadaraya-Watson estimator implementations. This allows for easy substitution/comparison of different kernel functions for one another in indicators. Furthermore, kernels can easily be combined with other kernels to create newer, more customized kernels. Compared to Moving Averages (which are really just simple kernels themselves), these kernel functions are more adaptive and afford the user an unprecedented degree of customization and flexibility.

rationalQuadratic(_src, _lookback, _relativeWeight, _startAtBar)

Rational Quadratic Kernel - An infinite sum of Gaussian Kernels of different length scales.

Parameters:

_src : The source series.

_lookback : The number of bars used for the estimation. This is a sliding value that represents the most recent historical bars.

_relativeWeight : Relative weighting of time frames. Smaller values result in a more stretched-out curve, and larger values will result in a more wiggly curve. As this value approaches zero, the longer time frames will exert more influence on the estimation. As this value approaches infinity, the behavior of the Rational Quadratic Kernel will become identical to the Gaussian kernel.

_startAtBar : Bar index on which to start regression. The first bars of a chart are often highly volatile, and omitting these initial bars often leads to a better overall fit.

Returns: yhat The estimated values according to the Rational Quadratic Kernel.

gaussian(_src, _lookback, _startAtBar)

Gaussian Kernel - A weighted average of the source series. The weights are determined by the Radial Basis Function (RBF).

Parameters:

_src : The source series.

_lookback : The number of bars used for the estimation. This is a sliding value that represents the most recent historical bars.

_startAtBar : Bar index on which to start regression. The first bars of a chart are often highly volatile, and omitting these initial bars often leads to a better overall fit.

Returns: yhat The estimated values according to the Gaussian Kernel.

periodic(_src, _lookback, _period, _startAtBar)

Periodic Kernel - The periodic kernel (derived by David Mackay) allows one to model functions that repeat themselves exactly.

Parameters:

_src : The source series.

_lookback : The number of bars used for the estimation. This is a sliding value that represents the most recent historical bars.

_period : The distance between repititions of the function.

_startAtBar : Bar index on which to start regression. The first bars of a chart are often highly volatile, and omitting these initial bars often leads to a better overall fit.

Returns: yhat The estimated values according to the Periodic Kernel.

locallyPeriodic(_src, _lookback, _period, _startAtBar)

Locally Periodic Kernel - The locally periodic kernel is a periodic function that slowly varies with time. It is the product of the Periodic Kernel and the Gaussian Kernel.

Parameters:

_src : The source series.

_lookback : The number of bars used for the estimation. This is a sliding value that represents the most recent historical bars.

_period : The distance between repititions of the function.

_startAtBar : Bar index on which to start regression. The first bars of a chart are often highly volatile, and omitting these initial bars often leads to a better overall fit.

Returns: yhat The estimated values according to the Locally Periodic Kernel.

ahpuhelperLibrary "ahpuhelper"

Helper Library for Auto Harmonic Patterns UltimateX. It is not meaningful for others. This is supposed to be private library. But, publishing it to make sure that I don't delete accidentally. Some functions may be useful for coders.

insert_open_trades_table_column(showOpenTrades, table_id, column, colors, values, intStatus, harmonicTrailingStartState, lblSizeOpenTrades)

add data to open trades table column

Parameters:

showOpenTrades : flag to show open trades table

table_id : Table Id

column : refers to pattern data

colors : backgroud and text color array

values : cell values

intStatus : status as integer

harmonicTrailingStartState : trailing Start state as per configs

lblSizeOpenTrades : text size

Returns: nextColumn

populate_closed_stats(ClosedStatsPosition, bullishCounts, bearishCounts, bullishRetouchCounts, bearishRetouchCounts, bullishSizeMatrix, bearishSizeMatrix, bullishRR, bearishRR, allPatternLabels, flags, rowMain, rowHeaders)

populate closed stats for harmonic patterns

Parameters:

ClosedStatsPosition : Table position for closed stats

bullishCounts : Matrix containing bullish trade stats

bearishCounts : Matrix containing bearish trade stats

bullishRetouchCounts : Matrix containing bullish trade stats for those which retouched entry

bearishRetouchCounts : Matrix containing bearish trade stats for those which retouched entry

bullishSizeMatrix : Matrix containing data about size of bullish patterns

bearishSizeMatrix : Matrix containing data about size of bearish patterns

bullishRR : Matrix containing Risk Reward data of bullish patterns

bearishRR : Matrix containing Risk Reward data of bearish patterns

allPatternLabels : array containing pattern labels

flags : display flags

rowMain : Pattern header data

rowHeaders : header grouping data

Returns: void

get_rr_details(patternTradeDetails, harmonicTrailingStartState, disableTrail, breakEvenTrail)

calculate and return risk reward based on targets and stops

Parameters:

patternTradeDetails : array containing stop, entry and targets

harmonicTrailingStartState : trailing point

disableTrail : If set, ignores trailing point

breakEvenTrail : If set, trailing does not go beyond breakeven.

Returns: nextColumn

fastlog2Library "fastlog2"

Description:

Returns the approximation of Log2 with the maximal error of: 0.000061011436

Reference:

www.anycodings.com

fastlog2(x)

Returns the approximation of Log2 with the maximal error of: 0.000061011436

Parameters:

x : float

Returns: float, log2 of x

combinLibrary "combin"

Description:

The combin function is a the combination function

as it calculates the number of possible combinations for two given numbers.

This function takes two arguments: the number and the number_chosen.

For example, if the number is 5 and the number chosen is 1,

there are 5 combinations, giving 5 as a result.

Reference:

ideone.com

support.microsoft.com

combin(n, kin)

Returns the number of combinations for a given number of items. Use to determine the total possible number of groups for a given number of items.

Parameters:

n : int, The number of items.

kin : int, The number of items in each combination.

Returns: int.

FibonacciLibrary "Fibonacci"

General Fibonacci functions. Get fib numbers, ratios, etc.

fib_precise(f, precision)

Get the precise Fibonacci ratio, to the specified number of decimal places

Parameters:

f : Fibonacci ratio (string, in form #.###)

precision : Number of decimal places (optional int, dft = 16, max = 32)

Returns: Precise Fibonacci ratio (float)

fib_n(n)

Calculate the Nth number in the Fibonacci sequence

Parameters:

n : Index/number in sequence (int)

Returns: Fibonacci number (int)

TrigLibrary "Trig"

Trigonometric functions

rt_get_angleAlpha(a, b, c, deg)

Get angle α of a right triangle, given the lengths of its sides

Parameters:

a : length of leg a (float)

b : length of leg b (float)

c : length of hypotenuse (float)

deg : flag to return angle in degrees (bool - default = false)

Returns: angle α in radians (or degrees if deg == true)

rt_get_angleAlphaFromLine(x1, y1, x2, y2, l, deg)

Get angle α of a right triangle formed by the given line

Parameters:

x1 : x coordinate 1 (int - optional, required if argument l is not specified)

y1 : y coordinate 1 (float - optional, required if argument l is not specified)

x2 : x coordinate 2 (int - optional, required if argument l is not specified)

y2 : y coordinate 2 (float - optional, required if argument l is not specified)

l : line object (line - optional, required if x1, y1, x2, and y2 agruments are not specified)

deg : flag to return angle in degrees (bool - default = false)

Returns: angle α in radians (or degrees if deg == true)

rt_get_angleBeta(a, b, c, deg)

Get angle β of a right triangle, given the lengths of its sides

Parameters:

a : length of leg a (float)

b : length of leg b (float)

c : length of hypotenuse (float)

deg : flag to return angle in degrees (bool - default = false)

Returns: angle β in radians (or degrees if deg == true)

rt_get_angleBetaFromLine(x1, y1, x2, y2, l, deg)

Get angle β of a right triangle formed by the given line

Parameters:

x1 : x coordinate 1 (int - optional, required if argument l is not specified)

y1 : y coordinate 1 (float - optional, required if argument l is not specified)

x2 : x coordinate 2 (int - optional, required if argument l is not specified)

y2 : y coordinate 2 (float - optional, required if argument l is not specified)

l : line object (line - optional, required if x1, y1, x2, and y2 agruments are not specified)

deg : flag to return angle in degrees (bool - default = false)

Returns: angle β in radians (or degrees if deg == true)

AlgebraLibrary "Algebra"

Algebra functions.

line_fromXy(x1, y1, x2, y2)

Get line slope and y-intercept from coordinates

Parameters:

x1 : x coordinate 1 (int - bar index)

y1 : y coordinate 1 (float - price/value)

x2 : x coordinate 2 (int - bar index)

y2 : y coordinate 2 (float - price/value)

Returns: of line

line_getPrice(x, slope, yInt)

Get line slope and y-intercept from coordinates

Parameters:

x : x coordinate to solve for y (int - bar index)

slope : slope of line (float)

yInt : y-intercept of line (float)

Returns: y (price/value)

L_BetaLibrary "L_Beta"

TODO: add library description here

length()

beta()

simple_beta()

index_selector()

FunctionLAPACKdsyrkLibrary "FunctionLAPACKdsyrk"

subroutine part of LAPACK: Linear Algebra Package,

performs one of the symmetric rank k operations

.

C := alpha*A*A**T + beta*C, or C := alpha*A**T*A + beta*C,

.

where alpha and beta are scalars, C is an n by n symmetric matrix

and A is an n by k matrix in the first case and a k by n matrix

in the second case.

.

reference:

netlib.org

dsyrk(uplo, trans, n, k, alpha, a, lda, beta, c, ldc)

performs one of the symmetric rank k operations

.

C := alpha*A*A**T + beta*C, or C := alpha*A**T*A + beta*C,

.

where alpha and beta are scalars, C is an n by n symmetric matrix

and A is an n by k matrix in the first case and a k by n matrix

in the second case.

.

Parameters:

uplo : string specifies whether the upper or lower triangular part of

the array C is to be referenced as follows:

UPLO = 'U' or 'u' Only the upper triangular part of C is to be referenced.

UPLO = 'L' or 'l' Only the lower triangular part of C is to be referenced.

.

trans : string specifies the operation to be performed as follows:

TRANS = 'N' or 'n' C := alpha*A*A**T + beta*C.

TRANS = 'T' or 't' C := alpha*A**T*A + beta*C.

TRANS = 'C' or 'c' C := alpha*A**T*A + beta*C.

.

n : int specifies the order of the matrix C. N must be at least zero.

k : int On entry with:

TRANS = 'N' or 'n', K specifies the number of columns of the matrix A.

TRANS = 'T' or 't' or 'C' or 'c', K specifies the number of rows of the matrix A.

K must be at least zero.

.

alpha : float scalar.

a : matrix matrix A.

lda : int specifies the first dimension of A.

beta : float scalar.

c : matrix matrix C, is overwritten by the lower triangular part of the updated matrix.

ldc : int specifies the first dimension of C

Returns: void, C is overwritten by the lower triangular part of the updated matrix.

FunctionLAPACKdtrsmLibrary "FunctionLAPACKdtrsm"

subroutine in the LAPACK:linear algebra package, used to solve one of the following matrix equations:

op( A )*X = alpha*B, or X*op( A ) = alpha*B,

where alpha is a scalar, X and B are m by n matrices, A is a unit, or

non-unit, upper or lower triangular matrix and op( A ) is one of

op( A ) = A or op( A ) = A**T.

The matrix X is overwritten on B.

reference:

netlib.org

dtrsm(side, uplo, transa, diag, m, n, alpha, a, lda, b, ldb)

solves one of the matrix equations

op( A )*X = alpha*B, or X*op( A ) = alpha*B,

where alpha is a scalar, X and B are m by n matrices, A is a unit, or

non-unit, upper or lower triangular matrix and op( A ) is one of

op( A ) = A or op( A ) = A**T.

The matrix X is overwritten on B.

Parameters:

side : string , On entry, SIDE specifies whether op( A ) appears on the left or right of X as follows:

SIDE = 'L' or 'l' op( A )*X = alpha*B.

SIDE = 'R' or 'r' X*op( A ) = alpha*B.

uplo : string , specifies whether the matrix A is an upper or lower triangular matrix as follows:

UPLO = 'U' or 'u' A is an upper triangular matrix.

UPLO = 'L' or 'l' A is a lower triangular matrix.

transa : string , specifies the form of op( A ) to be used in the matrix multiplication as follows:

TRANSA = 'N' or 'n' op( A ) = A.

TRANSA = 'T' or 't' op( A ) = A**T.

TRANSA = 'C' or 'c' op( A ) = A**T.

diag : string , specifies whether or not A is unit triangular as follows:

DIAG = 'U' or 'u' A is assumed to be unit triangular.

DIAG = 'N' or 'n' A is not assumed to be unit triangular.

m : int , the number of rows of B. M must be at least zero.

n : int , the number of columns of B. N must be at least zero.

alpha : float , specifies the scalar alpha. When alpha is zero then A is not referenced and B need not be set before entry.

a : matrix, Triangular matrix.

lda : int , specifies the first dimension of A.

b : matrix, right-hand side matrix B, and on exit is overwritten by the solution matrix X.

ldb : int , specifies the first dimension of B.

Returns: void, modifies matrix b.

usage:

dtrsm ('L', 'U', 'N', 'N', 5, 3, 1.0, a, 7, b, 6)

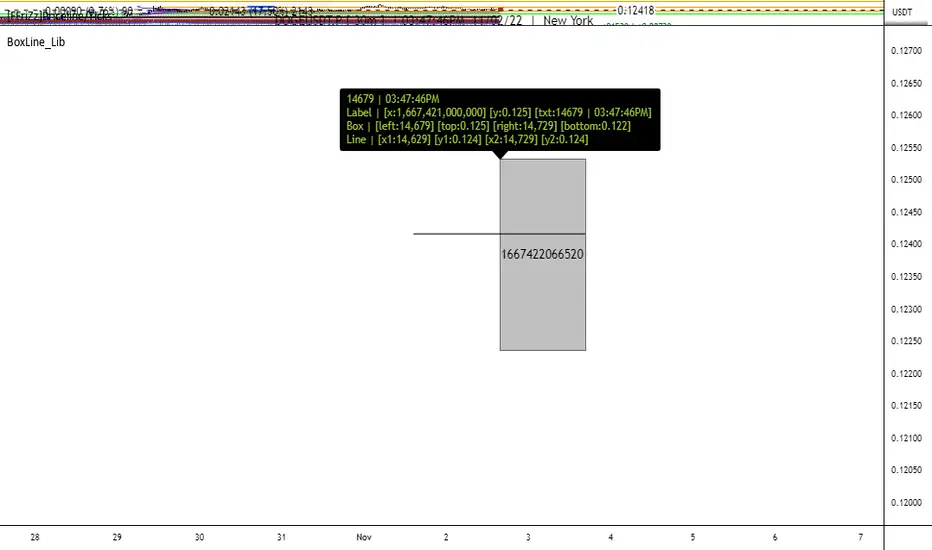

BoxLine_LibLibrary "BoxLine_Lib"

personal Library for line and box built in functions

lineXY(x)

get x1,y1,x2,y2 in a tuple

Parameters:

x : TODO: line

Returns: tuple of x1,y1,x2,y2

line(x)

Create line with only the y1 value(when line == na) or all

when line != na set x1,y1,x2,y2 individually just 1 or all

- use just the line value to set the x2 to current bar or time will set to time

- will auto pick xloc.bar_index or xloc.bar_time if not used

Parameters:

x : (line line,int x1,float y1,int x2,float y2,

string xloc,string extend,color color,string style,int width)

Returns: Line

boxXY(x)

get left,top,right,bottom in a tuple

Parameters:

x : box

Returns: tuple of left,top,right,bottom

box(x)

Create line with only the top,bottom value(when line == na) or all

when box != na set left,top,right,bottom individually just 1 or all

- use just the box value to set the right to current bar or time will set to time

- if right is above a number that a bar_index wouldnt be

Parameters:

x : box box,int left,float top,int right,

float bottom,color border_color, int border_width,

string border_style,string extend,string xloc,

color bgcolor,string text,string text_size, color text_color,

string text_halign,string text_valign,string text_wrap)

Returns: TODO: Box