NY Anchored VWAP and Auto SMANY Anchored VWAP and Auto SMA

This script is a versatile trading indicator for the TradingView platform that combines two powerful components: a New York-anchored Volume-Weighted Average Price (VWAP) and a dynamic Simple Moving Average (SMA). Designed for traders who utilize VWAP for intraday trend analysis, this tool provides a clear visual representation of average price and volatility-adjusted moving averages, generating automated alerts for key crossover signals.

Indicator Components

1. NY Anchored VWAP

The VWAP is a crucial tool that represents the average price of a security adjusted for volume. This version is "anchored" to the start of the New York trading session, resetting at the beginning of each new session. This provides a clean, session-specific anchor point to gauge market sentiment and trend. The VWAP line changes color to reflect its slope:

Green: When the VWAP is trending upwards, indicating a bullish bias.

Red: When the VWAP is trending downwards, indicating a bearish bias.

2. Auto SMA

The Auto SMA is a moving average with a unique twist: its lookback period is not fixed. Instead, it dynamically adjusts based on market volatility. The script measures volatility using the Average True Range (ATR) and a Z-Score calculation.

When volatility is expanding, the SMA's length shortens, making it more sensitive to recent price changes.

When volatility is contracting, the SMA's length lengthens, smoothing out the price action to filter out noise.

This adaptive approach allows the SMA to react appropriately to different market conditions.

Suggested Trading Strategy

This indicator is particularly effective when used on a one-minute chart for identifying high-probability trade entries. The core of the strategy is to trade the crossover between the VWAP and the Auto SMA, with confirmation from a candle close.

The strategy works best when the entry signal aligns with the overall bias of the higher timeframe market structure. For example, if the daily or 4-hour chart is in an uptrend, you would look for bullish signals on the one-minute chart.

Bullish Entry Signal: A potential entry is signaled when the VWAP crosses above the Auto SMA, and is confirmed when the one-minute candle closes above both the VWAP and the SMA. This indicates a potential continuation of the bullish momentum.

Bearish Entry Signal: A potential entry is signaled when the VWAP crosses below the Auto SMA, and is confirmed when the one-minute candle closes below both the VWAP and the SMA. This indicates a potential continuation of the bearish momentum.

The built-in alerts for these crossovers allow you to receive notifications without having to constantly monitor the charts, ensuring you don't miss a potential setup.

ATR

Sentinel 5 — OHL daybreak signals [KedArc Quant]Overview

Sentinel 5 plots the first-bar high/low of each trading session and gives clean, rules-based signals in two ways:

1) OHL Setups at the close of the first bar (Open equals/near High for potential short; Open equals/near Low for potential long).

2) Breakout Signals later in the session when price breaks the first-bar High/Low, with optional body/penetration filters.

Basic workflow

1. Wait for the first session bar to finish.

*If O≈H (optionally by proximity) → short setup. •

*If O≈L → long setup. • If neither happens, optionally allow later breakouts.

2. Optional: Act only on breakouts that penetrate a minimum % of that bar’s range/body.

3. Skip the day automatically if the first bar is abnormally large (marubozu-like / extreme ATR / outsized vs yesterday).

Signals & Markers

Markers on the chart:

▲ O=L (exact) / O near L (proximity) – long setup at first-bar close.

▼ O=H (exact) / O near H (proximity) – short setup at first-bar close.

▲ Breakout Long – later bar breaks above first-bar High meeting your penetration rule.

▼ Breakout Short – later bar breaks below first-bar Low meeting your penetration rule.

Advanced Range Analyzer ProAdvanced Range Analyzer Pro – Adaptive Range Detection & Breakout Forecasting

Overview

Advanced Range Analyzer Pro is a comprehensive trading tool designed to help traders identify consolidations, evaluate their strength, and forecast potential breakout direction. By combining volatility-adjusted thresholds, volume distribution analysis, and historical breakout behavior, the indicator builds an adaptive framework for navigating sideways price action. Instead of treating ranges as noise, this system transforms them into opportunities for mean reversion or breakout trading.

How It Works

The indicator continuously scans price action to identify active range environments. Ranges are defined by volatility compression, repeated boundary interactions, and clustering of volume near equilibrium. Once detected, the indicator assigns a strength score (0–100), which quantifies how well-defined and compressed the consolidation is.

Breakout probabilities are then calculated by factoring in:

Relative time spent near the upper vs. lower range boundaries

Historical breakout tendencies for similar structures

Volume distribution inside the range

Momentum alignment using auxiliary filters (RSI/MACD)

This creates a live probability forecast that updates as price evolves. The tool also supports range memory, allowing traders to analyze the last completed range after a breakout has occurred. A dynamic strength meter is displayed directly above each consolidation range, providing real-time insight into range compression and breakout potential.

Signals and Breakouts

Advanced Range Analyzer Pro includes a structured set of visual tools to highlight actionable conditions:

Range Zones – Gradient-filled boxes highlight active consolidations.

Strength Meter – A live score displayed in the dashboard quantifies compression.

Breakout Labels – Probability percentages show bias toward bullish or bearish continuation.

Breakout Highlights – When a breakout occurs, the range is marked with directional confirmation.

Dashboard Table – Displays current status, strength, live/last range mode, and probabilities.

These elements update in real time, ensuring that traders always see the current state of consolidation and breakout risk.

Interpretation

Range Strength : High scores (70–100) indicate strong consolidations likely to resolve explosively, while low scores suggest weak or choppy ranges prone to false signals.

Breakout Probability : Directional bias greater than 60% suggests meaningful breakout pressure. Equal probabilities indicate balanced compression, favoring mean-reversion strategies.

Market Context : Ranges aligned with higher timeframe trends often resolve in the dominant direction, while counter-trend ranges may lead to reversals or liquidity sweeps.

Volatility Insight : Tight ranges with low ATR imply imminent expansion; wide ranges signal extended consolidation or distribution phases.

Strategy Integration

Advanced Range Analyzer Pro can be applied across multiple trading styles:

Breakout Trading : Enter on probability shifts above 60% with confirmation of volume or momentum.

Mean Reversion : Trade inside ranges with high strength scores by fading boundaries and targeting equilibrium.

Trend Continuation : Focus on ranges that form mid-trend, anticipating continuation after consolidation.

Liquidity Sweeps : Use failed breakouts at boundaries to capture reversals.

Multi-Timeframe : Apply on higher timeframes to frame market context, then execute on lower timeframes.

Advanced Techniques

Combine with volume profiles to identify areas of institutional positioning within ranges.

Track sequences of strong consolidations for trend development or exhaustion signals.

Use breakout probability shifts in conjunction with order flow or momentum indicators to refine entries.

Monitor expanding/contracting range widths to anticipate volatility cycles.

Custom parameters allow fine-tuning sensitivity for different assets (crypto, forex, equities) and trading styles (scalping, intraday, swing).

Inputs and Customization

Range Detection Sensitivity : Controls how strictly ranges are defined.

Strength Score Settings : Adjust weighting of compression, volume, and breakout memory.

Probability Forecasting : Enable/disable directional bias and thresholds.

Gradient & Fill Options : Customize range visualization colors and opacity.

Dashboard Display : Toggle live vs last range, info table size, and position.

Breakout Highlighting : Choose border/zone emphasis on breakout events.

Why Use Advanced Range Analyzer Pro

This indicator provides a data-driven approach to trading consolidation phases, one of the most common yet underutilized market states. By quantifying range strength, mapping probability forecasts, and visually presenting risk zones, it transforms uncertainty into clarity.

Whether you’re trading breakouts, fading ranges, or mapping higher timeframe context, Advanced Range Analyzer Pro delivers a structured, adaptive framework that integrates seamlessly into multiple strategies.

ATR - Daily vs CurrentThis script provides a comprehensive view of the Average True Range (ATR) for both the current trading day and a multi-day lookback, giving traders real-time insight into volatility and potential daily price movement. Key features include:

ATR Table:

- Average ATR: 14-day ATR, representing typical daily volatility.

- Today’s ATR: Current day ATR, showing how much the price has moved so far.

- % of Avg ATR Used: Calculates the percentage of the average ATR that has been realized today, helping assess if a move is near exhaustion.

Possible Daily ATR Range Lines:

- Horizontal lines drawn from today’s open representing ±50% and ±100% of the 14-day ATR, providing a visual guide for potential price extremes.

- Lines are updated once per day and extend from the right to the left, clearly marking possible intraday range limits.

Color-coded for clarity:

- Green = +50% ATR

- Red = -50% ATR

- Lime = +100% ATR

- Maroon = -100% ATR

Usage:

- Useful for day traders and intraday scalpers to track volatility and potential price targets.

- Helps in risk management, setting stops, and estimating realistic intraday moves.

- Provides visual cues for when price has consumed a significant portion of expected daily range.

Note: ATR is a statistical measure; the lines represent possible ranges, not guaranteed targets. Daily market conditions may prevent price from reaching full ATR.

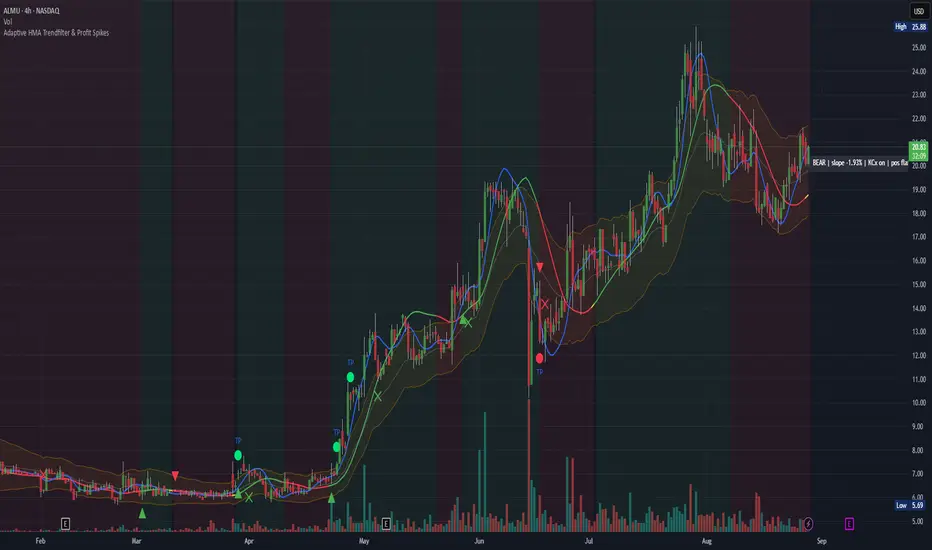

Adaptive HMA Trendfilter & Profit SpikesShort Description

Adaptive trend-following filter using Hull Moving Average (HMA) slope.

Includes optional Keltner Channel entries/exits and dynamic spike-based take-profit markers (ATR/Z-Score).

Optional Fast HMA for early entry visualization (not included in logic).

USER GUIDE:

1) Quick Overview

Trend Filter: Slow HMA defines Bull / Bear / Sideways (via slope & direction).

Entries / Exits:

Entry: Color change of the slow HMA (red→green = Long, green→red = Short), optionally filtered by the Keltner basis.

Exit: Preferably via Keltner Band (Long: Close under Upper Band; Short: Close above Lower Band).

Fallback: exit on opposite HMA color change.

Take-Profit Spikes: Marks abnormal moves (ATR, Z-Score, or both) as discretionary TP signals.

Fast HMA (optional): Purely visual for early entry opportunities; not part of the core trading logic (see §5).

2) Adding & Basic Setup

Add the indicator to your chart.

Open Settings (gear icon) and configure:

HMA: Slow HMA Length = 55, Slope Lookback = 10, Slope Threshold = 0.20%.

Keltner: KC Length = 20, Multiplier = 1.5.

Spike-TP: Mode = ATR+Z, ATR Length = 14, Z Length = 20, Cooldown = 5.

Optionally: enable Fast HMA (e.g., length = 20).

3) Input Parameters – Key Controls

Slow HMA Length: Higher = smoother, fewer but cleaner signals.

Slope Lookback: How far back HMA slope is compared against.

Slope Threshold (%): Minimum slope to avoid “Sideways” regime.

KC Length / Multiplier: Width and reactivity of Keltner Channels.

Exits via KC Bands: Toggle on/off (recommended: on).

Entries only above/below KC Basis: Helps filter out chop.

Spike Mode: Choose ATR, Z, or ATR+Z (stricter, fewer signals).

Spikes only when in position: TP markers show only when you’re in a trade.

4) Entry & Exit Logic

Entries

Long: Slow HMA turns from red → green, and (if filter enabled) Close > KC Basis.

Short: Slow HMA turns from green → red, and (if filter enabled) Close < KC Basis.

Exits

KC Exit (recommended):

Long → crossunder(close, Upper KC) closes trade.

Short → crossover(close, Lower KC).

Fallback Exit: If KC Exits are off → exit on opposite HMA color change.

Spike-TP (Discretionary)

Marks unusually large deviations from HMA.

Use for partial profits or tightening stops.

⚠️ Not auto-traded — only marker/alert.

5) Early Entry Opportunities (Fast HMA Cross – visual only)

The script can optionally display a Fast HMA (e.g., 20) alongside the Slow HMA (e.g., 55).

Bullish early hint: Fast HMA crosses above Slow HMA, or stays above, before the Slow HMA officially turns green.

Bearish early hint: opposite.

⚠️ These signals are not part of the built-in logic — they are purely discretionary:

Advantage: Earlier entries, more profit potential.

Risk: Higher chance of whipsaws.

Practical workflow (early long entry):

Fast HMA crosses above Slow HMA AND Close > KC Basis.

Enter small position with tight stop (under KC Basis or HMA swing).

Once Slow HMA confirms green → add to position or trail stop tighter.

6) Recommended Presets

Crypto (1h/2h):

HMA: 55 / 10 / 0.20–0.30%

KC: 20 / 1.5–1.8

Spikes: ATR+Z, ATR=14, Z=20, Cooldown 5

FX (1h/4h):

HMA: 55 / 8–10 / 0.10–0.25%

KC: 20 / 1.2–1.5

Indices (15m/1h):

HMA: 50–60 / 8–12 / 0.15–0.30%

KC: 20 / 1.3–1.6

Fine-tuning:

Too noisy? → Raise slope threshold or increase HMA length.

Too sluggish? → Lower slope threshold or shorten HMA length.

7) Alerts – Best Practice

Long/Short Entry – get notified when trend color switches & KC filter is valid.

Long/Short Exit – for KC exits or fallback exits.

Long/Short Spike TP – for discretionary profit-taking.

Set via TradingView: Create Alert → Select this indicator → choose condition.

8) Common Pitfalls & Tips

Too many false signals?

Raise slope threshold (more “Sideways” filtering).

Enable KC filter for entries.

Entries too late?

Use Fast HMA cross for early discretionary entries.

Or lower slope threshold slightly.

Spikes too rare/frequent?

More frequent → ATR mode or lower ATR multiplier / Z-threshold.

Rarer but stronger → ATR+Z with higher thresholds.

9) Example Playbook (Long Trade)

Regime: Slow HMA still red, Fast HMA crosses upward (early hint).

Filter: Close > KC Basis.

Early Entry: Small size, stop below KC Basis or recent swing low.

Confirmation: Slow HMA turns green → scale up or trail stop.

Management: Partial profits at Spike-TP marker; full exit at KC upper band break.

ICT AI ATR Signals [TradingFinder]🔵 Introduction

In financial markets, two main factors always have the greatest impact on traders’ decisions: the direction of the trend and the level of price volatility. Although there are various tools to analyze each of these factors, very few indicators can combine them in a coordinated and simultaneous way.

The ICT AI ATR indicator has been designed with this purpose in mind, to provide a unified and comprehensive view of the market instead of relying on multiple scattered indicators.

This indicator is built upon two widely used tools: the Moving Average (MA) and the Average True Range (ATR). The combination of these two indicators allows traders to simultaneously track the trend direction and account for market volatility two elements that always play a decisive role in trading decisions.

In the structure of the indicator, the Moving Average acts as the central line and serves as the backbone of the tool. By calculating the average price over a defined period, the Moving Average filters out excess market noise and provides a clearer picture of the overall price movement.

This helps traders focus on the main trend instead of being distracted by minor and temporary fluctuations. The central line is thus the main reference point for identifying the trend direction.

Alongside this, the ATR is responsible for measuring the real volatility of the market. Unlike many tools that only look at closing price changes, the ATR considers the true range of candlestick movements, giving a more accurate view of market dynamics.

In the ICT AI ATR indicator, this feature is used to draw dynamic bands above and below the Moving Average line. These bands shift with changing market conditions and act like dynamic support and resistance levels, areas where strong price reactions often occur.

This combination allows traders not only to see the dominant market trend through the Moving Average but also to understand volatility and the natural price range via the ATR. For this reason, the ICT AI ATR identifies points that are likely to act as reaction or reversal zones, whether during bounces off the bands or breakouts through them.

With this structure, the trader can at a glance :

Identify the overall market direction using the Moving Average.

Observe volatility and the natural range of price movement through ATR.

Recognize key levels where strong reactions or potential reversals are more likely.

As a result, the ICT AI ATR functions as a combined tool that replaces the need to use several separate indicators, enabling traders to analyze trend, volatility, price bands, and even Fibonacci targets within a single unified framework.

🔵 How to Use

The ICT AI ATR indicator is designed to simplify market analysis through two main components: visual display of bands and signals on the chart itself, and a multi-symbol analytical dashboard capable of monitoring over 20 different assets simultaneously across multiple timeframes.

This dashboard feature allows traders to gain a quick overview of overall market conditions without opening multiple charts or constantly switching timeframes. It updates in real-time, showing active Buy (Long) and Sell signals for each symbol.

As such, the combination of direct chart display and dashboard analytics makes the indicator useful both for detailed analysis of a single symbol and for monitoring multiple markets at once.

🟣 How do ICT AI ATR trading signals work?

Sell Signal (Short) : Triggered when the price pushes below the lower band (Low goes outside the lower band) and then closes back above it. This indicates potential weakness in bullish momentum and suggests possible selling pressure or the start of a downward correction. Traders can use this to spot sell setups or manage long positions.

Buy Signal (Long) : Triggered when the price extends above the upper band (High goes outside the upper band) and then closes back below it. This often signals exhaustion in bearish pressure and the return of buying strength, potentially marking the start of a new upward move.

This signaling logic is based on the actual behavior of price relative to the ATR dynamic bands. Unlike static formulas, signals adapt to changing market conditions, making them more accurate and reliable.

The main advantage of the ICT AI ATR indicator is that traders can benefit from real-time analysis directly on the chart by observing price interactions with the bands and signals while also receiving a multi-market overview through the dashboard. This combination is especially valuable for traders who operate across multiple instruments or markets simultaneously.

🔵 Settings

🟣 Logical settings

Moving Average Type : Select the type of moving average for the central line. Options include EMA, SMA, RMA, WMA, or HMA depending on the trading strategy.

Moving Average Period : Defines the length of the moving average. Shorter periods make the central line more responsive to price changes, while longer periods smooth out the line to show the broader trend.

ATR Period : Determines the number of candles considered for volatility calculation. Shorter periods increase sensitivity, while longer periods provide a more stable view of volatility.

ATR Multiplier : Sets the distance between the upper/lower bands and the central moving average line. Higher values widen the bands, while lower values bring them closer to price.

Smooth Period: Used to smooth data and reduce chart noise. Higher values produce smoother, more consistent indicator lines.

Signal Gap : Defines the minimum number of candles required between two consecutive signals. This prevents back-to-back signals from appearing too frequently and ensures only the more reliable ones are shown.

🟣 Display Settings

Table on Chart : Allows users to choose the position of the signal dashboard either directly on the chart or below it, depending on their layout preference.

Number of Symbols : Enables users to control how many symbols are displayed in the screener table, from 10 to 20, adjustable in increments of 2 symbols for flexible screening depth.

Table Mode : This setting offers two layout styles for the signal table :

Basic : Mode displays symbols in a single column, using more vertical space.

Extended : Mode arranges symbols in pairs side-by-side, optimizing screen space with a more compact view.

Table Size : Lets you adjust the table’s visual size with options such as: auto, tiny, small, normal, large, huge.

Table Position : Sets the screen location of the table. Choose from 9 possible positions, combining vertical (top, middle, bottom) and horizontal (left, center, right) alignments.

🟣 Symbol Settings

Each of the 10 symbol slots comes with a full set of customizable parameters :

Symbol : Define or select the asset (e.g., XAUUSD, BTCUSD, EURUSD, etc.).

Timeframe : Set your desired timeframe for each symbol (e.g., 15, 60, 240, 1D).

🟣 Alert Settings

Alert : Enables alerts for AAS.

Message Frequency : Determines the frequency of alerts. Options include 'All' (every function call), 'Once Per Bar' (first call within the bar), and 'Once Per Bar Close' (final script execution of the real-time bar). Default is 'Once per Bar'.

Show Alert Time by Time Zone : Configures the time zone for alert messages. Default is 'UTC'.

🔵 Conclusion

The ICT AI ATR indicator, by combining three core elements Moving Average for trend detection, ATR for volatility measurement and dynamic bands, and Fibonacci levels for price targets—provides a multi-layered and intelligent tool for market analysis. In addition to showing accurate bands directly on the chart, it also offers a multi-symbol dashboard that allows traders to monitor signals across different assets and timeframes in real time.

The key advantage of this indicator is that it eliminates the need to use several separate tools by integrating trend, volatility, key levels, and trade signals into one unified framework. For this reason, ICT AI ATR is a reliable and effective choice for both short-term traders seeking quick market moves and long-term traders focused on dynamic support and resistance levels.

Płatny skrypt

Better Pivot Points [LuminoAlgo]Overview

The Better Pivot Points indicator is an advanced trend analysis tool that combines Supertrend methodology with automated pivot point identification and zigzag visualization. This indicator helps traders identify significant price turning points and visualize market structure through dynamic pivot labeling and connecting lines.

How It Works

This indicator utilizes a Supertrend-based algorithm to detect meaningful pivot points in price action. Unlike traditional pivot point indicators that rely on fixed time periods, this tool dynamically identifies pivots based on trend changes, providing more relevant and timely signals.

The algorithm tracks trend changes using ATR-based Supertrend crossovers to determine when significant highs and lows have formed. When a trend reversal is detected, the indicator marks the pivot point and draws connecting lines to visualize price flow and market structure progression.

Key Features

• Dynamic Pivot Detection: Automatically identifies high and low pivot points using Supertrend crossovers

• Market Structure Labeling: Labels pivots as HH (Higher High), LH (Lower High), HL (Higher Low), or LL (Lower Low)

• Zigzag Visualization: Connects pivot points with customizable lines to clearly show price flow and market structure

• Color-Coded Analysis: Uses distinct colors to indicate bullish trends (green), bearish trends (red), and neutral conditions (yellow)

• Customizable Parameters: Adjustable ATR period, factor, line width, and line style

Input Settings

• ATR Length: Controls the sensitivity of the Supertrend calculation (default: 21)

• Factor: Multiplier for the ATR-based Supertrend bands (default: 2.0)

• Zigzag Line Width: Customize the thickness of connecting lines (1-4)

• Zigzag Line Style: Choose between Solid, Dashed, or Dotted line styles

What Makes This Original

This indicator combines several analytical concepts into a cohesive tool that differentiates it from standard pivot point indicators:

1. Uses Supertrend crossovers as the trigger for pivot detection rather than traditional high/low lookback periods

2. Automatically categorizes market structure using HH/LH/HL/LL labeling system based on pivot relationships

3. Provides real-time zigzag visualization with intelligent color coding that reflects trend direction

4. Integrates trend direction analysis with structural pivot identification in a single comprehensive tool

The underlying calculations use custom logic for tracking trend states, validating pivot points, and determining appropriate color coding based on market structure analysis.

How to Use

1. Trend Identification: Green lines indicate bullish market structure, red lines show bearish structure, yellow indicates transitional periods

2. Support/Resistance: Pivot points often act as future support and resistance levels for price action

3. Market Structure Analysis: HH and HL patterns suggest uptrends, while LH and LL patterns indicate downtrends

4. Entry/Exit Planning: Use pivot points and trend changes to plan potential trade entries and exits

Important Limitations and Warnings

• This indicator is a technical analysis tool and should not be used as the sole basis for trading decisions

• Pivot points are identified after price moves occur, meaning this indicator has inherent lag and cannot predict future pivots

• False signals can occur during ranging or choppy market conditions where trends are unclear

• Past performance of any indicator does not guarantee future results or trading success

• The indicator works best in clearly trending markets and may produce less reliable signals in sideways price action

• This tool requires interpretation and should be combined with other forms of analysis

• Always use proper risk management and position sizing strategies when trading

Why This Script Is Protected

This indicator uses proprietary algorithms for pivot detection timing, trend state management, and market structure analysis that represent original research and development. The specific logic for pivot validation, color-coding methodology, and structural relationship calculations contains unique approaches that differentiate it from standard pivot point indicators available in the public library.

Disclaimer

This indicator is for educational and analysis purposes only and does not constitute investment advice. Trading involves substantial risk and is not suitable for all investors. Past results are not indicative of future performance. The future is fundamentally unknowable and past results in no way guarantee future performance. Always conduct your own research and consider your risk tolerance before making any trading decisions.

TP/SL Dynamic (FIB,ATR,MULTIPLE,PERCENT)TP/SL Dynamic (FIB, ATR, MULTIPLE, PERCENT)

This indicator provides a flexible framework for managing Take Profit (TP) and Stop Loss (SL) levels using multiple calculation schemes. It is designed for traders who want dynamic or rule-based levels that adapt to volatility, market type, and custom input.

The script supports four TP/SL methodologies:

Pro Standards (Auto-Select): Adapts method based on asset type and volatility.

R Multiples: Risk-based reward multiples from ATR-derived stop distance.

Fibonacci R: Fibonacci extension levels projected from recent pivots.

Percent: Fixed percentage distance from entry, adjusted by volatility.

ATR Multiples: ATR-based calculations with configurable multipliers.

Features:

Up to 3 manual entries, each with configurable time, price, and position size.

Weighted entry price calculation across multiple positions.

Single or multiple TP targets (up to 4) with automatic scaling.

Dynamic ATR option: updates SL/TP levels with live volatility or fixes them at entry.

Pivot-based logic for Fibonacci extensions.

Symbol Locking to prevent mismatches between intended pair and chart symbol.

Table display with optional R-multiples, TP/SL values, and entry details.

Visual chart elements: lines, labels, price-scale markers for SL/TP, and zebra-style info tables.

Entry markers (E1, E2, E3) for clarity.

Alerts for TP and SL triggers (both long and short).

How to Use:

Define entry prices, times, and position sizes (up to 3 entries).

Select a TP method (Pro Standards, R Multiples, Fibonacci R, Percent, or ATR Multiples).

Choose single or multiple TP mode.

Optionally enable Dynamic ATR to update levels in real time.

Check the on-chart table for all calculated levels and alerts.

Author & Credit:

Developed from the ground up by me (no external code used outside The Pine public library).

DEE's Indicator v2 — Daily Range, Averages & Previous High/Low🇺🇸 English

This indicator is designed to help traders analyze market volatility and daily price ranges.

It includes the following features:

• 5-bar analysis: Shows high-low ranges and percentage changes of the last 5 bars.

• Daily Average Range: Calculates daily average ranges based on the last 5 bars.

• Daily AVG Lines: Plots expected top and bottom range levels based on the daily average.

• Previous Day High/Low: Automatically draws lines from the previous day's high and low.

• Timeframe Separators: Adds visual separators between days, months, and years.

• Optional arrows: Displays arrow markers for the last detected bars used in the calculation.

Use cases:

● Intraday traders can quickly measure daily progress compared to the average daily range.

● Swing traders can identify support/resistance levels from previous daily highs and lows.

● Risk managers can monitor when current volatility deviates significantly from the average.

⚠️ Notes:

The script does not generate buy/sell signals; it provides analytical tools only.

All displayed information is for visual/educational purposes and should be combined with your own trading strategy.

👉 Don’t forget to adjust the settings to suit your needs.

If you are using a multi-chart layout with different timeframes and apply this indicator to each chart, the 5-bar data will be calculated separately based on each chart’s TF. However, the “Daily AVG” section will always show the same value for the 1D timeframe.

🇺🇿 O‘zbekcha

Ushbu indikator treyderlarga bozor volatilligi va kundalik narx diapazonlarini tahlil qilishda yordam berish uchun mo‘ljallangan.

Unda quyidagi funksiyalar mavjud:

• 5-bar tahlili: So‘nggi 5 ta bar diapazoni (high–low) va foiz o‘zgarishini ko‘rsatadi.

• Kundalik o‘rtacha diapazon: So‘nggi 5 ta bar asosida o‘rtacha kundalik diapazonni hisoblaydi.

• AVG Lines: Daily AVGning yuqori va pastki diapazon darajalarini chizadi.

• Oldingi kunning High/Low darajalari: Avtomatik ravishda oldingi kunning high va low darajalarini chizadi.

• Vaqt ajratgichlari: Kunlar, oylar va yillar orasiga vizual ajratgich qo‘shadi.

• Ixtiyoriy strelkalar: Hisoblash uchun foydalanilgan so‘nggi barlarda strelka belgilarini ko‘rsatadi.

Qo‘llanilishi:

● Intraday treyderlar kundalik natijani o‘rtacha kundalik diapazon bilan tezda solishtira olishadi.

● Swing treyderlar oldingi kunning high va low darajalaridan qo‘llab-quvvatlash/qarshilik darajalarini aniqlashlari mumkin.

● Risk-menejerlar hozirgi volatillik o‘rtachadan sezilarli darajada og‘ib ketganini kuzatishlari mumkin.

⚠️ Eslatma:

Ushbu indikator sotib olish/sotish signallarini bermaydi; u faqat tahliliy vosita sifatida ishlatiladi.

Ko‘rsatilgan barcha ma’lumotlar vizual/ta’limiy maqsadlarda mo‘ljallangan bo‘lib, o‘z strategiyangiz bilan birgalikda qo‘llanilishi lozim.

👉 Sozlamalarni ehtiyojlaringizga qarab moslashtirishni unutmang.

Agar siz multi-chart rejimida turli timeframelar bilan ishlasangiz va ushbu indikatorni har bir grafikda qo‘llasangiz, 5 ta bar haqidagi ma’lumotlar har bir grafikning o‘z TFiga qarab hisoblanadi. Ammo “Daily AVG” bo‘limida esa faqat 1D timeframe uchun bir xil qiymat ko‘rsatiladi.

🇷🇺 Русский

Этот индикатор предназначен для помощи трейдерам в анализе волатильности рынка и дневных ценовых диапазонов.

Он включает в себя следующие функции:

• Анализ 5 свечей: Показывает диапазон high–low и процентные изменения последних 5 свечей.

• Средний дневной диапазон: Рассчитывает средний дневной диапазон на основе последних 5 свечей.

• Линии среднего диапазона (AVG Lines): Строит ожидаемые верхние и нижние уровни диапазона на основе среднего дневного значения.

• Максимум/минимум предыдущего дня: Автоматически наносит линии с уровнями high и low предыдущего дня.

• Разделители временных интервалов: Добавляет визуальные разделители между днями, месяцами и годами.

• Опциональные стрелки: Показывает стрелки на последних свечах, использованных в расчётах.

Применение:

● Интрадей-трейдеры могут быстро измерять дневное движение по сравнению со средним дневным диапазоном.

● Свинг-трейдеры могут определять уровни поддержки/сопротивления по максимумам и минимумам предыдущего дня.

● Риск-менеджеры могут контролировать ситуации, когда текущая волатильность значительно отклоняется от среднего.

⚠️ Примечания:

Этот индикатор не генерирует сигналы на покупку/продажу; он предоставляет только аналитические инструменты.

Вся отображаемая информация предназначена для визуальных/образовательных целей и должна использоваться совместно с вашей торговой стратегией.

👉 Не забудьте настроить параметры под свои нужды.

Если вы работаете в режиме мульти-графика с разными таймфреймами и применяете этот индикатор на каждом графике, данные по 5 барам будут рассчитываться отдельно для каждого ТФ. Однако в разделе “Daily AVG” всегда отображается одно и то же значение для таймфрейма 1D.

© Dilshod Nurmatov Shuhratovich | deetradesonline | 2025

Custom ATR BandsThis indicator provides a customisable, easy to view band around the price, based on the ATR. The ATR length and multiplier can be adjusted.

Strict VWAP+EMA Trend Aligner with Volume Power - SUBODH BAJPAIAuthor: SUBODH BAJPAI

This indicator combines VWAP, EMA crossover, and Volume Strength filters into a single, easy-to-read system with clear signals and backtest-ready logic.

🔑 Features

• VWAP Tracking → Confirms trend bias (Above = Bullish, Below = Bearish).

• EMA 10/20 Crossovers → Detects momentum shifts (10 > 20 = Long trend).

• Volume Strength Check → Uses both Vol/VolSMA and RVOL thresholds to validate real demand/supply.

• Strict Align Mode → A Long signal triggers only when ALL conditions agree (VWAP, EMA crossover, strong volume).

• ATR-based Stop Loss & Take Profit → Built-in risk management with RR targeting and optional trailing stop.

• Smart Debounce → Prevents noisy/repeated signals by enforcing cooldown bars.

• Backtest Ready → Full strategy version available in Strategy Tester.

🎯 Usage

• Works on any timeframe (intraday → swing).

• Best used on liquid stocks, indices, or futures.

• Look for “LONG” arrows/shapes when all confirmations align.

• Use along with your own support/resistance levels or price action setups.

⚠️ Disclaimer

This script is for educational purposes only.

Not financial advice. Always validate signals with your own strategy and risk management.

Average True Ranges with IBD RSAdvanced ATR Analysis with IBD Relative Strength

This comprehensive indicator combines Average True Range (ATR) analysis with IBD (Investor's Business Daily) Relative Strength calculation, providing both volatility measurement and momentum analysis in one powerful tool.

Key Features:

ATR Analysis:

Standard ATR: Customizable period (default 14) with multiple smoothing options

1.5x ATR: Extended range for wider stop-loss and target calculations

Smoothing Options: Choose between RMA, SMA, EMA, or WMA for ATR calculation

Customizable Colors: Distinct colors for easy visual identification

IBD Relative Strength:

Professional RS Formula: Uses the same calculation method as Investor's Business Daily

Multi-Timeframe Analysis: Compares current price to 3, 6, 9, and 12-month performance

Weighted Calculation: 40% weight on 3-month, 20% each on 6, 9, and 12-month performance

Zero-Based Scale: Values above 0 indicate outperformance, below 0 indicate underperformance

Trading Applications:

Volatility-Based Stops: Use ATR and 1.5x ATR for dynamic stop-loss placement

Position Sizing: ATR helps determine appropriate position size based on volatility

Relative Strength Analysis: IBD RS identifies stocks with superior momentum

Market Timing: High RS values often precede strong price moves

Risk Management: Combine volatility (ATR) with momentum (RS) for comprehensive analysis

Technical Details:

ATR Calculation: True Range smoothed over selected period with chosen method

IBD RS Formula: (40% × 3M) + (20% × 6M) + (20% × 9M) + (20% × 12M) - 100

Display: Separate pane indicator with customizable colors for each component

How to Interpret:

High ATR: Increased volatility, wider stops needed

Low ATR: Reduced volatility, tighter stops possible

Positive IBD RS: Stock outperforming market over measured periods

Negative IBD RS: Stock underperforming market over measured periods

Customizable Parameters:

ATR calculation length

Smoothing method for ATR

Individual colors for ATR, 1.5x ATR, and IBD RS lines

Perfect for swing traders and position traders who want to combine volatility analysis with relative strength momentum in their decision-making process. Particularly useful for stock selection and risk management.

Mutanabby_AI | ATR+ | Trend-Following StrategyThis document presents the Mutanabby_AI | ATR+ Pine Script strategy, a systematic approach designed for trend identification and risk-managed position entry in financial markets. The strategy is engineered for long-only positions and integrates volatility-adjusted components to enhance signal robustness and trade management.

Strategic Design and Methodological Basis

The Mutanabby_AI | ATR+ strategy is constructed upon a foundation of established technical analysis principles, with a focus on objective signal generation and realistic trade execution.

Heikin Ashi for Trend Filtering: The core price data is processed via Heikin Ashi (HA) methodology to mitigate transient market noise and accentuate underlying trend direction. The script offers three distinct HA calculation modes, allowing for comparative analysis and validation:

Manual Calculation: Provides a transparent and deterministic computation of HA values.

ticker.heikinashi(): Utilizes TradingView's built-in function, employing confirmed historical bars to prevent repainting artifacts.

Regular Candles: Allows for direct comparison with standard OHLC price action.

This multi-methodological approach to trend smoothing is critical for robust signal generation.

Adaptive ATR Trailing Stop: A key component is the Average True Range (ATR)-based trailing stop. ATR serves as a dynamic measure of market volatility. The strategy incorporates user-defined parameters (

Key Value and ATR Period) to calibrate the sensitivity of this trailing stop, enabling adaptation to varying market volatility regimes. This mechanism is designed to provide a dynamic exit point, preserving capital and locking in gains as a trend progresses.

EMA Crossover for Signal Generation: Entry and exit signals are derived from the interaction between the Heikin Ashi derived price source and an Exponential Moving Average (EMA). A crossover event between these two components is utilized to objectively identify shifts in momentum, signaling potential long entry or exit points.

Rigorous Stop Loss Implementation: A critical feature for risk mitigation, the strategy includes an optional stop loss. This stop loss can be configured as a percentage or fixed point deviation from the entry price. Importantly, stop loss execution is based on real market prices, not the synthetic Heikin Ashi values. This design choice ensures that risk management is grounded in actual market liquidity and price levels, providing a more accurate representation of potential drawdowns during backtesting and live operation.

Backtesting Protocol: The strategy is configured for realistic backtesting, employing fill_orders_on_standard_ohlc=true to simulate order execution at standard OHLC prices. A configurable Date Filter is included to define specific historical periods for performance evaluation.

Data Visualization and Metrics: The script provides on-chart visual overlays for buy/sell signals, the ATR trailing stop, and the stop loss level. An integrated information table displays real-time strategy parameters, current position status, trend direction, and key price levels, facilitating immediate quantitative assessment.

Applicability

The Mutanabby_AI | ATR+ strategy is particularly suited for:

Cryptocurrency Markets: The inherent volatility of assets such as #Bitcoin and #Ethereum makes the ATR-based trailing stop a relevant tool for dynamic risk management.

Systematic Trend Following: Individuals employing systematic methodologies for trend capture will find the objective signal generation and rule-based execution aligned with their approach.

Pine Script Developers and Quants: The transparent code structure and emphasis on realistic backtesting provide a valuable framework for further analysis, modification, and integration into broader quantitative models.

Automated Trading Systems: The clear, deterministic entry and exit conditions facilitate integration into automated trading environments.

Implementation and Evaluation

To evaluate the Mutanabby_AI | ATR+ strategy, apply the script to your chosen chart on TradingView. Adjust the input parameters (Key Value, ATR Period, Heikin Ashi Method, Stop Loss Settings) to observe performance across various asset classes and timeframes. Comprehensive backtesting is recommended to assess the strategy's historical performance characteristics, including profitability, drawdown, and risk-adjusted returns.

I'd love to hear your thoughts, feedback, and any optimizations you discover! Drop a comment below, give it a like if you find it useful, and share your results.

Average True Range %The ATR% oscillator measures market volatility as a percentage of the closing price, smooths it using a chosen method (RMA, SMA, EMA, or WMA), and compares it to the threshold levels of 0.95% and 1.20%.

Relative Volatility Mass [SciQua]The ⚖️ Relative Volatility Mass (RVM) is a volatility-based tool inspired by the Relative Volatility Index (RVI) .

While the RVI measures the ratio of upward to downward volatility over a period, RVM takes a different approach:

It sums the standard deviation of price changes over a rolling window, separating upward volatility from downward volatility .

The result is a measure of the total “volatility mass” over a user-defined period, rather than an average or normalized ratio.

This makes RVM particularly useful for identifying sustained high-volatility conditions without being diluted by averaging.

────────────────────────────────────────────────────────────

╭────────────╮

How It Works

╰────────────╯

1. Standard Deviation Calculation

• Computes the standard deviation of the chosen `Source` over a `Standard Deviation Length` (`stdDevLen`).

2. Directional Separation

• Volatility on up bars (`chg > 0`) is treated as upward volatility .

• Volatility on down bars (`chg < 0`) is treated as downward volatility .

3. Rolling Sum

• Over a `Sum Length` (`sumLen`), the upward and downward volatilities are summed separately using `math.sum()`.

4. Relative Volatility Mass

• The two sums are added together to get the total volatility mass for the rolling window.

Formula:

RVM = Σ(σ up) + Σ(σ down)

where σ is the standard deviation over `stdDevLen`.

╭────────────╮

Key Features

╰────────────╯

Directional Volatility Tracking – Differentiates between volatility during price advances vs. declines.

Rolling Volatility Mass – Shows the total standard deviation accumulation over a given period.

Optional Smoothing – Multiple MA types, including SMA, EMA, SMMA (RMA), WMA, VWMA.

Bollinger Band Overlay – Available when SMA is selected, with adjustable standard deviation multiplier.

Configurable Source – Apply RVM to `close`, `open`, `hl2`, or any custom source.

╭─────╮

Usage

╰─────╯

Trend Confirmation: High RVM values can confirm strong trending conditions.

Breakout Detection: Spikes in RVM often precede or accompany price breakouts.

Volatility Cycle Analysis: Compare periods of contraction and expansion.

RVM is not bounded like the RVI, so absolute values depend on market volatility and chosen parameters.

Consider normalizing or using smoothing for easier visual comparison.

╭────────────────╮

Example Settings

╰────────────────╯

Short-term volatility detection: `stdDevLen = 5`, `sumLen = 10`

Medium-term trend volatility: `stdDevLen = 14`, `sumLen = 20`

Enable `SMA + Bollinger Bands` to visualize when volatility is unusually high or low relative to recent history.

╭───────────────────╮

Notes & Limitations

╰───────────────────╯

Not a directional signal by itself — use alongside price structure, volume, or other indicators.

Higher `sumLen` will smooth short-term fluctuations but reduce responsiveness.

Because it sums, not averages, values will scale with both volatility and chosen window size.

╭───────╮

Credits

╰───────╯

Based on the Relative Volatility Index concept by Donald Dorsey (1993).

TradingView

SciQua - Joshua Danford

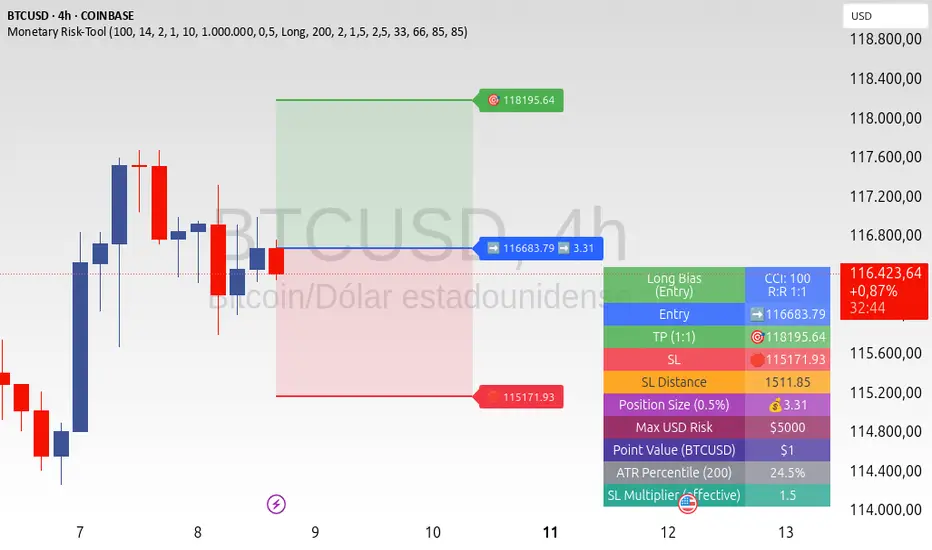

ATR+CCI Monetary Risk Tool - TP/SL⚙️ ATR+CCI Monetary Risk Tool — Volatility-aware TP/SL & Position Sizing

Exact prices (no rounding), ATR-percentile dynamic stops, and risk-budget sizing for consistent execution.

🧠 What this indicator is

A risk-first planning tool. It doesn’t generate orders; it gives you clean, objective levels (Entry, SL, TP) and position size derived from your risk budget. It shows only the latest setup to keep charts readable, and a compact on-chart table summarizing the numbers you actually act on.

✨ What makes it different

Dynamic SL by regime (ATR percentile): Instead of a fixed multiple, the SL multiplier adapts to the current volatility percentile (low / medium / high). That helps avoid tight stops in noisy markets and over-wide stops in quiet markets.

Risk budgeting, not guesswork: Size is computed from Account Balance × Max Risk % divided by SL distance × point value. You risk the same dollars across assets/timeframes.

Precision that matches your instrument: Entry, TP, SL, and SL Distance are displayed as exact prices (no rounding), truncated to syminfo.mintick so they align with broker/exchange precision.

Symbol-aware point value: Uses syminfo.pointvalue so you don’t maintain tick tables.

Non-repaint option: Work from closed bars to keep the plan stable.

🔧 How to use (quick start)

Add to chart and pick your timeframe and symbol.

In settings:

Set Account Balance (USD) and Max Risk per Trade (%).

Choose R:R (1:1 … 1:5).

Pick ATR Period and CCI Period (defaults are sensible).

Keep Dynamic ATR ON to adapt SL by regime.

Keep Use closed-bar values ON to avoid repaint when planning.

Read the labels (Entry/TP/SL) and the table (SL Distance, Position Size, Max USD Risk, ATR Percentile, effective SL Mult).

Combine with your entry trigger (price action, levels, momentum, etc.). This indicator handles risk & targets.

📐 How levels are computed

Bias: CCI ≥ 0 ⇒ long, otherwise short.

ATR Percentile: Percent rank of ATR(atrPeriod) over a lookback window.

Effective SL Mult:

If percentile < Low threshold ⇒ use Low SL Mult (tighter).

If between thresholds ⇒ use Base SL Mult.

If percentile > High threshold ⇒ use High SL Mult (wider).

Stop-Loss: SL = Entry ± ATR × SL_Mult (minus for long, plus for short).

Take-Profit: TP = Entry ± (Entry − SL) × R (R from the R:R dropdown).

Position Size:

USD Risk = Balance × Risk%

Contracts = USD Risk ÷ (|Entry − SL| × PointValue)

For futures, quantity is floored to whole contracts.

Exact prices: Entry/TP/SL and SL Distance are not rounded; they’re truncated to mintick so what you see matches valid price increments.

📊 What you’ll see on chart

Latest Entry (blue), TP (green), SL (red) with labels (optional emojis: ➡️ 🎯 🛑).

Info Table with:

Bias, Entry, TP, SL (exact, truncated to mintick)

SL Distance (exact, truncated)

Position Size (contracts/units)

Max USD Risk

Point Value

ATR Percentile and effective SL Mult

🧪 Practical examples

High-volatility session (e.g., XAUUSD, 1H): ATR percentile is high ⇒ wider SL, smaller size. Reduces churn from normal noise during macro events.

Range-bound market (e.g., EURUSD, 4H): ATR percentile low ⇒ tighter SL, better R:R. Helps you avoid carrying unnecessary risk.

Index swing planning (e.g., ES1!, Daily): Non-repaint levels + risk budgeting = consistent sizing across days/weeks, easier to review and journal.

🧭 Why traders should use it

Consistency: Same dollar risk regardless of instrument or volatility regime.

Clarity: One-trade view forces focus; you see the numbers that matter.

Adaptivity: Stops calibrated to the market’s current behavior, not last month’s.

Discipline: A visible checklist (SL distance, size, USD risk) before you hit buy/sell.

🔧 Input guide (practical defaults)

CCI Period: 100 by default; use as a bias filter, not an entry signal.

ATR Period: 14 by default; raise for smoother, lower for more reactive.

ATR Percentile Lookback: 200 by default (stable regime detection).

Percentile thresholds: 33/66 by default; widen the gap to change how often regimes switch.

SL Mults: Start ~1.5 / 2.0 / 2.5 (low/base/high). Tune by asset.

Risk % per trade: Common pro ranges are 0.25–1.0%; adjust to your risk tolerance.

R:R: Start with 1:2 or 1:3 for balanced skew; adapt to strategy edge.

Closed-bar values: Keep ON for planning/live; turn OFF only for exploration.

💡 Best practices

Combine with your entry logic (structure, momentum, liquidity levels).

Review ATR percentile and effective SL Mult across sessions so you understand regime shifts.

For futures, remember size is floored to whole contracts—safer by design.

Journal trades with the table snapshot to improve risk discipline over time.

⚠️ Notes & limitations

This is not a strategy; it does not place orders or alerts.

No slippage/commissions modeled here; build a strategy() version for backtests that mirror your broker/exchange.

Displayed non-price metrics use two decimals; prices and SL Distance are exact (truncated to mintick).

📎 Disclaimer

For educational purposes only. Not financial advice. Markets involve risk. Test thoroughly before trading live.

ATR%指標概要 / Overview

ATR Percentage (MTF):把 ATR 轉為百分比(ATR%)或保留為絕對值,並在該「波動序列」上套用布林帶。支援多週期(MTF)計算:例如在 5 分圖顯示 4H / D1 的 ATR%。內建白色點狀水平線作為固定門檻(預設 1%)。

ATR Percentage (MTF): Converts ATR to a percentage of price (ATR%) or keeps it as absolute ATR, then applies Bollinger Bands on this volatility series. Supports multi-timeframe (MTF) calculation (e.g., show 4H/D1 ATR% on a 5-min chart). Includes a configurable white dotted horizontal threshold line (default 1%).

⸻

設計目的 / Purpose

• 以 ATR% 衡量相對波動,利於跨品種比較。

Use ATR% for relative volatility to compare across markets.

• 以 布林帶 標示「高/低波動區」,觀察擴張與壓縮。

Use Bollinger Bands on volatility to highlight expansion/squeeze.

• 提供 固定閾值(1%) 作為策略濾網或告警門檻。

Provide a fixed threshold (1%) for filters/alerts.

• 以 MTF 方式,讓低週期策略用高週期波動做濾網。

MTF lets lower-TF strategies filter by higher-TF volatility.

⸻

參數說明 / Inputs

• Use ATR as % of Close:切換 ATR(絕對值)/ ATR%(建議)。

Toggle between absolute ATR and ATR% (recommended).

• ATR Periods:ATR 計算長度(預設 22)。

ATR lookback (default 22).

• Show Bollinger Bands / BB Periods / StdDev:布林帶開關、長度與倍數(預設 20 / 2)。

Bollinger Bands on/off, length, and deviation (default 20 / 2).

• Source Timeframe:計算用週期(如 60、240、D、W;留空/Chart = 跟隨圖表)。

Timeframe used for calculations (e.g., 60, 240, D, W; empty/“Chart” = current).

• Threshold Line (%):白色點線門檻,預設 1.0(即 1%)。

White dotted threshold line, default 1.0 (1%).

提醒:當 非 ATR% 模式時,Threshold 值代表「價格單位」而非百分比。

Note: In non-ATR% mode, the threshold is in price units, not percent.

⸻

訊號解讀 / How to Read

• ATR% > 上軌:波動顯著擴張(趨勢啟動或加速常見)。

ATR% above upper band: significant expansion; often trend ignition/acceleration.

• ATR% < 下軌:波動明顯壓縮(常見於突破前)。

ATR% below lower band: volatility squeeze; often precedes breakouts.

• ATR% 穿越 Threshold(1%):達到固定波動標準,可作策略開關或風控分水嶺。

ATR% crossing the 1% threshold: fixed volatility bar for filters/risk gates.

⸻

內建告警 / Built-in Alerts

• Volatility Breakout (MTF):ATR/ATR% 向上穿越上軌。

Triggers when ATR/ATR% crosses above the upper band.

• Volatility Squeeze (MTF):ATR/ATR% 向下穿越下軌。

Triggers when ATR/ATR% crosses below the lower band.

⸻

使用建議 / Suggested Uses

• 當沖濾網:於 1–5 分圖選擇 4H / D1 作為 Source Timeframe;僅在 ATR% > 1% 且位於中線以上時允許趨勢進場。

Intraday filter: on 1–5m charts, set 4H/D1 as source TF; allow trend entries only when ATR% > 1% and above the midline.

• 突破前偵測:ATR% 長時間貼近下軌 → 留意可能的波動擴張。

Pre-breakout scan: prolonged ATR% near lower band can foreshadow expansion.

• 跨品種比較:用 ATR% 統一指數、外匯、商品的波動刻度。

Cross-asset comparison: ATR% normalizes volatility across indices/FX/commodities.

⸻

已知限制 / Notes

• MTF 對齊:使用 request.security() 對映高週期資料到當前圖表;在歷史回補與即時邊界棒可能略有差異。

MTF alignment: request.security() maps higher-TF data; boundary bars may differ slightly between historical and realtime.

• 百分比分母:ATR% 的分母為同一週期的 close;若需更平滑可改 ATR / SMA(close, N) × 100。

Denominator: ATR% uses same-TF close; for smoother values consider ATR / SMA(close, N) × 100.

• 風險聲明:僅供研究/教育用途,非投資建議,請自行控管風險。

Disclaimer: For research/education only. Not investment advice.

⸻

版本與更新 / Version & Updates

• v1.0:ATR/ATR% + BB(MTF)、1% 白色點線、兩組告警。

v1.0: ATR/ATR% + BB (MTF), 1% white dotted line, two alert conditions.

Mutanabby_AI | Ultimate Algo | Remastered+Overview

The Mutanabby_AI Ultimate Algo Remastered+ represents a sophisticated trend-following system that combines Supertrend analysis with multiple moving average confirmations. This comprehensive indicator is designed specifically for identifying high-probability trend continuation and reversal opportunities across various market conditions.

Core Algorithm Components

**Supertrend Foundation**: The primary signal generation relies on a customizable Supertrend indicator with adjustable sensitivity (1-20 range). This adaptive trend-following tool uses Average True Range calculations to establish dynamic support and resistance levels that respond to market volatility.

**SMA Confirmation Matrix**: Multiple Simple Moving Averages (SMA 4, 5, 9, 13) provide layered confirmation for signal strength. The algorithm distinguishes between regular signals and "Strong" signals based on SMA 4 vs SMA 5 relationship, offering traders different conviction levels for position sizing.

**Trend Ribbon Visualization**: SMA 21 and SMA 34 create a visual trend ribbon that changes color based on their relationship. Green ribbon indicates bullish momentum while red signals bearish conditions, providing immediate visual trend context.

**RSI-Based Candle Coloring**: Advanced 61-tier RSI system colors candles with gradient precision from deep red (RSI ≤20) through purple transitions to bright green (RSI ≥79). This visual enhancement helps traders instantly assess momentum strength and overbought/oversold conditions.

Signal Generation Logic

**Buy Signal Criteria**:

- Price crosses above Supertrend line

- Close price must be above SMA 9 (trend confirmation)

- Signal strength determined by SMA 4 vs SMA 5 relationship

- "Strong Buy" when SMA 4 ≥ SMA 5

- Regular "Buy" when SMA 4 < SMA 5

**Sell Signal Criteria**:

- Price crosses below Supertrend line

- Close price must be below SMA 9 (trend confirmation)

- Signal strength based on SMA relationship

- "Strong Sell" when SMA 4 ≤ SMA 5

- Regular "Sell" when SMA 4 > SMA 5

Advanced Risk Management System

**Automated TP/SL Calculation**: The indicator automatically calculates stop loss and take profit levels using ATR-based measurements. Risk percentage and ATR length are fully customizable, allowing traders to adapt to different market conditions and personal risk tolerance.

**Multiple Take Profit Targets**:

- 1:1 Risk-Reward ratio for conservative profit taking

- 2:1 Risk-Reward for balanced trade management

- 3:1 Risk-Reward for maximum profit potential

**Visual Risk Display**: All risk management levels appear as both labels and optional trend lines on the chart. Customizable line styles (solid, dashed, dotted) and positioning ensure clear visualization without chart clutter.

**Dynamic Level Updates**: Risk levels automatically recalculate with each new signal, maintaining current market relevance throughout position lifecycles.

Visual Enhancement Features

**Customizable Display Options**: Toggle trend ribbon, TP/SL levels, and risk lines independently. Decimal precision adjustments (1-8 decimal places) accommodate different instrument price formats and personal preferences.

**Professional Label System**: Clean, informative labels show entry points, stop losses, and take profit targets with precise price levels. Labels automatically position themselves for optimal chart readability.

**Color-Coded Momentum**: The gradient RSI candle coloring system provides instant visual feedback on momentum strength, helping traders assess market energy and potential reversal zones.

Implementation Strategy

**Timeframe Optimization**: The algorithm performs effectively across multiple timeframes, with higher timeframes (4H, Daily) providing more reliable signals for swing trading. Lower timeframes work well for day trading with appropriate risk adjustments.

**Sensitivity Adjustment**: Lower sensitivity values (1-5) generate fewer but higher-quality signals, ideal for conservative approaches. Higher sensitivity (15-20) increases signal frequency for active trading styles.

**Risk Management Integration**: Use the automated risk calculations as baseline parameters, adjusting risk percentage based on account size and market conditions. The 1:1, 2:1, 3:1 targets enable systematic profit-taking strategies.

Market Application

**Trend Following Excellence**: Primary strength lies in capturing significant trend movements through the Supertrend foundation with SMA confirmation. The dual-layer approach reduces false signals common in single-indicator systems.

**Momentum Assessment**: RSI-based candle coloring provides immediate momentum context, helping traders assess signal strength and potential continuation probability.

**Range Detection**: The trend ribbon helps identify ranging conditions when SMA 21 and SMA 34 converge, alerting traders to potential breakout opportunities.

Performance Optimization

**Signal Quality**: The requirement for both Supertrend crossover AND SMA 9 confirmation significantly improves signal reliability compared to basic trend-following approaches.

**Visual Clarity**: The comprehensive visual system enables rapid market assessment without complex calculations, ideal for traders managing multiple instruments.

**Adaptability**: Extensive customization options allow fine-tuning for specific markets, trading styles, and risk preferences while maintaining the core algorithm integrity.

## Non-Repainting Design

**Educational Note**: This indicator uses standard TradingView functions (Supertrend, SMA, RSI) with normal behavior patterns. Real-time updates on current candles are expected and standard across all technical indicators. Historical signals on closed candles remain fixed and unchanged, ensuring reliable backtesting and analysis.

**Signal Confirmation**: Final signals are confirmed only when candles close, following standard technical analysis principles. The algorithm provides clear distinction between developing signals and confirmed entries.

Technical Specifications

**Supertrend Parameters**: Default sensitivity of 4 with ATR length of 11 provides balanced signal generation. Sensitivity range from 1-20 allows adaptation to different market volatilities and trading preferences.

**Moving Average Configuration**: SMA periods of 8, 9, and 13 create multi-layered trend confirmation, while SMA 21 and 34 form the visual trend ribbon for broader market context.

**Risk Management**: ATR-based calculations with customizable risk percentage ensure dynamic adaptation to market volatility while maintaining consistent risk exposure principles.

Recommended Settings

**Conservative Approach**: Sensitivity 4-5, RSI length 14, higher timeframes (4H, Daily) for swing trading with maximum signal reliability.

**Active Trading**: Sensitivity 6-8, RSI length 8-10, intermediate timeframes (1H) for balanced signal frequency and quality.

**Scalping Setup**: Sensitivity 10-15, RSI length 5-8, lower timeframes (15-30min) with enhanced risk management protocols.

## Conclusion

The Mutanabby_AI Ultimate Algo Remastered+ combines proven trend-following principles with modern visual enhancements and comprehensive risk management. The algorithm's strength lies in its multi-layered confirmation approach and automated risk calculations, providing both novice and experienced traders with clear signals and systematic trade management.

Success with this system requires understanding the relationship between signal strength indicators and adapting sensitivity settings to match current market conditions. The comprehensive visual feedback system enables rapid decision-making while the automated risk management ensures consistent trade parameters.

Practice with different sensitivity settings and timeframes to optimize performance for your specific trading style and risk tolerance. The algorithm's systematic approach provides an excellent framework for disciplined trend-following strategies across various market environments.

Smart Trend Signals [QuantAlgo]🟢 Overview

The Smart Trend Signals indicator is created to address a fundamental challenge in technical analysis: generating timely trend signals while adapting to varying market volatility conditions. The indicator distinguishes itself by employing volatility-adjusted calculations that automatically modify signal sensitivity based on current market conditions, rather than using fixed parameters that perform inconsistently across different market environments. By processing Long and Short signals through separate dynamic calculation engines, each optimized for its respective directional bias, the indicator reduces the common issue of delayed or conflicting signals that plague many traditional trend-following tools. Additionally, the integration of linear regression-based trend confirmation adds another layer of signal validation, helping to filter market noise while maintaining responsiveness to genuine price movements. This adaptive approach makes the indicator practical for both traders and investors across different asset classes and timeframes, from short-term forex/crypto scalping to long-term equity position analysis.

🟢 How It Works

The indicator uses a straightforward calculation process that combines volatility measurement with momentum detection to generate directional signals. The system first calculates Average True Range (ATR) over a user-defined period to measure current market volatility. This ATR value is then multiplied by the Smart Trend Multiplier setting to create dynamic reference levels that expand during volatile periods and contract during calmer market conditions.

For signal generation, the indicator maintains separate calculation paths for Long/Buy and Short/Sell opportunities. Long signals are generated when price moves above a dynamically calculated level below the current price, confirmed by an exponential moving average crossover in the same direction. Short signals work in reverse, triggering when price moves below a calculated level above the current price, also requiring EMA confirmation. This dual-path approach allows each signal type to operate with parameters suited to its directional bias.

🟢 How to Use

Long Signals (Green Labels): Appear as "Long" labels below price bars when the indicator detects upward price momentum above the calculated reference level, confirmed by EMA crossover. These signals identify moments when price action demonstrates bullish characteristics based on the volatility-adjusted calculations.

Short Signals (Red Labels): Display as "Short" labels above price bars when downward price momentum below the reference level is detected and confirmed by EMA crossover. These signals highlight instances where price action exhibits bearish characteristics according to the indicator's mathematical framework.

Customizable Bar Coloring: This feature colors individual price bars to match the current signal direction. When enabled, each bar reflects the indicator's current directional bias, creating a continuous visual representation of trend periods across the chart timeline.

Built-in Alert System: Provides automatic notifications for new signals with detailed exchange and ticker information. The alert system monitors the indicator's calculations continuously and triggers notifications when new long or short signals are generated, allowing traders/investors to track multiple instruments simultaneously.

🟢 Pro Tips for Trading and Investing

→ Parameter Adjustment: Higher Smart Trend Multiplier settings generate fewer signals that may be more selective, while lower settings produce more frequent signals that may include more false positives. Test different settings to find what works for your trading style and market conditions.

→ Timeframe Analysis: Using higher timeframes for general trend direction and lower timeframes for entry timing is a common approach.

→ Risk Management: No indicator eliminates the need for proper risk management. Use appropriate position sizing and stop-loss strategies regardless of signal quality or frequency.

→ Market Conditions: The indicator may perform differently in trending versus ranging markets. Frequent signal changes might indicate choppy conditions. Backtest and paper trade before risking real capital.

TSD Quantum [Moeinudin Montazerfaraj] 🔸 "TSD" stands for **Trend 1-2-3 and Supply & Demand**, which is the foundation of the trading style this indicator is built upon.

🔹 TSD Quantum is a specialized indicator designed exclusively for day traders who trade EURUSD, XAUUSD (Gold), and DAX40 on the 1H, 15M, and 5M timeframes using a Supply & Demand-based strategy.

This indicator is **not suitable for other symbols** and has been tailored specifically for these three assets to ensure high precision and effectiveness.

---

### 🔍 Key Features:

✅ **Trading Checklist Panel**

A built-in checklist helps you track every rule in your trading plan. If even one condition is left unchecked, the system highlights it in red and marks the trade as "Not Allowed." This feature enhances trading discipline.

✅ **Spread & ATR Control Panel**

Supports both auto-calculated and fixed values for spread and ATR. This is especially helpful when placing stop-losses quickly and accurately.

✅ **Inside & Outside Candle Detection**

A dedicated panel highlights whether the last candle is inside or outside. Hovering your mouse over the chart elements automatically colorizes the candles:

🔵 Blue = Outside candle

🔴 Red = Inside candle

Also displays the high/low of the latest outside bar.

✅ **Weekly Trade Stats Panel**

Custom-built for the mentioned three assets. You can enter your trades using either fixed risk or floating risk models.

✅ **Performance Metrics**

Helps you build and adjust a floating risk model—so you don’t have to enter every trade with the same lot size. Improves risk management across multiple trades.

✅ **Base Candles Display**

Grey and white base candles are marked based on supply and demand zones.

✅ **EOT Candles**

Candles with a green dot underneath indicate valid EOT opportunities for potential move-outs.

✅ **RC (Rejection Candle) Detection**

RC candles are automatically detected to alert you of potential traps or weaknesses during Supply/Demand formations.

---

### ⚠️ Disclaimer

This indicator does **not** issue buy/sell signals and **cannot guarantee profit or prevent loss**. It is a **tool for discretionary trading**, not an automated expert advisor.

All decisions must be made by the trader based on their own strategy and risk tolerance.

This is the **latest tested version** of TSD Quantum. All features have been validated and function as intended. Future updates will be provided if needed.

---

🙏 Thank you for reviewing this script. We hope it becomes a valuable addition to your day trading toolkit!

Fibonacci-Based Volume Flow (VFI)Fibonacci-based Volume Flow is an advanced next-generation evolution of LazyBear’s original VFI script that calculates and averages up to 21 Fibonacci-based VFI pairings to create a smoothed composite volume flow signal. This unique and powerful approach reduces noise, adapts to volatility, and provides a clearer view of trend strength and market structure across all timeframes. It also includes dynamic fibonacci guide levels, adaptive lookbacks, EMA crossovers, and structure-aware pivot labeling to help traders identify high-quality reversals, confirm directional bias, and detect divergences with greater precision. It's ideal for traders looking to enhance momentum analysis through volume-based confirmation.

🧠 Key Features🧠

🔹 Multi-VFI Fibonacci Fusion🔹

Blends up to 21 VFI signals (5, 13, 21, 34… up to 610) into smartly paired averages (e.g., 13/34, 55/144) — forming a smoothed composite VFI that’s more adaptive, less noisy, and highly responsive across market conditions.

🔸🔸 Dynamic Lookbacks🔸 🔸

Automatically adjusts histogram high/low tracking based on your chart’s timeframe — no more static tuning. Perfect for scalping fast charts or confirming long-term trends.

🟥🟩 Color-Coded Histogram🟥🟩

Visualizes VFI momentum with gradient coloring.

🧩🧩 Signal Crossovers 🧩🧩

Color-coded crossover lines persistently show bullish or bearish dominance.

Includes three powerful crossover systems:

➖5/13 VFI: Fast, early reversal detection

➖8/21 VFI: Swing-trading sweet spot

➖55/144 VFI: Trend confirmation across long cycles

🏷️ 🏷️Pivot Structure Labels🏷️🏷️

Labels oscillator swings with full structural logic:

➖HH, HL, LH, LL, EQ

➖Displays percent change, price at pivot, oscillator reading

➖Smart coloring detects divergence & trend continuation

📈 📈Dynamic Histogram Guides📈📈

Optional zero and ±50% bands anchor histogram levels based on real histogram extremes, not static thresholds — visually frame momentum shifts with context.

📍 📍Persistent High/Low Pivot Lines📍📍

Track the most significant histogram pivots (not price) across time, with smart labels:

➖Volume flow structure zones

➖Label shows price at pivot, oscillator level, and bars since event

➖Ideal for spotting divergence zones, momentum failures, and trend exhaustion.

🔍 🔍Volatility Table (ATR%)🔍🔍

💡Shows real-time volatility compression or expansion

💡Uses multiple ATR periods (e.g., 14 & 55) for short- and medium-term comparison

💡Helps traders understand whether momentum is likely to continue or stall

🔩🔩Volume-weighted VFI baselines🔩🔩

🟢A daily session-based VWAP of the VFI, which resets each day and highlights intraday volume flow context.

🟠A rolling VWA of VFI, which acts like a VWMA over a fixed window (e.g., 55 bars), smoothing short-term fluctuations and supporting trend/momentum confirmation.

These VWAP-style overlays help traders identify strength vs. weakness relative to volume-weighted baselines — useful for divergence spotting, mean reversion setups, or breakout confirmation.

🧰 🧰Under the Hood: How It Works🧰🧰

🔧 Core VFI Logic

Based on LazyBear’s foundational VFI:

➖Uses log returns of price (HLC3)

➖Filters insignificant moves using volatility-weighted thresholds

➖Normalizes volume via adaptive capping (e.g., 2.5× average)

🌀 Composite Blend System

Each VFI instance is smoothed and then fused via user-selectable pairs. This creates a customizable average VFI representing short, mid, and long-term pressure — one value, many time horizons.

📊 EMA Signal Layer

Crosses trigger persistent color shifts in signal lines, making trend strength clear at a glance.

VFI blend feeds into EMA crossovers. You can toggle visibility for:

➖Fast (5/13)

➖Medium (8/21)

➖Slow (55/144)

🧭 Pivot Framework

Structure logic only compares pivots on same-side polarity:

➖Highs compare to highs above zero

➖Lows compare to lows below zero

This avoids nonsensical comparisons and preserves logical sequences (HH → LH → HL).

🧱 Dynamic Labels

All pivots and persistent levels display:

➖Oscillator value

➖Price value

➖Structure tag (e.g., LH, HL)

➖% change from prior pivot

➖Lookback info

➖Bar age

Unlike traditional VFI:

✅ It blends timeframes with Fibonacci precision

✅ Uses dynamic, volatility-aware logic

✅ Embeds visual structure & divergence intelligence

✅ Enhances entry confidence and exit timing

🔧 This isn’t just an indicator — it’s a volume-informed decision engine.

Ideal For:

🔶Trend-followers wanting cleaner volume-based confirmation

🔶Reversal traders spotting structure + divergence

🔶Scalpers or investors needing adaptable signals

🔶Those who loved LazyBear's VFI

📌 Final Note:

As powerful as Fibonacci Blended Volume Flow is, no single indicator should be used in isolation. For best results, combine it with price action analysis, higher-timeframe context, and complementary tools like trendlines, moving averages, or support/resistance levels. Use it as part of a well-rounded trading approach to confirm setups — not to define them alone.

Fundur - Trend LinesFundur - Trend Lines: Complete Trading Indicator Guide

Indicator Overview

The Fundur - Trend Lines is an advanced multi-layered trend analysis system that combines adaptive trend line technology, momentum analysis, and intelligent signal generation into one comprehensive trading tool. This indicator goes beyond traditional moving averages by utilizing volatility-adjusted trend lines that dynamically adapt to market conditions, providing traders with precise trend strength measurements and actionable trading signals.

What Makes Trend Lines Unique?

The Trend Lines indicator introduces Adaptive Trend Line Technology - a sophisticated methodology that uses Average True Range (ATR) calculations to create trend lines that respond intelligently to market volatility. Unlike static indicators, Trend Lines provides dynamic analysis that adapts its sensitivity based on current market conditions, offering more accurate trend identification and strength assessment.

Core Methodology