ATR Volatility giua64ATR Volatility giua64 – Smart Signal + VIX Filter

📘 Script Explanation (in English)

Title: ATR Volatility giua64 – Smart Signal + VIX Filter

This script analyzes market volatility using the Average True Range (ATR) and compares it to its moving average to determine whether volatility is HIGH, MEDIUM, or LOW.

It includes:

✅ Custom or preset configurations for different asset classes (Forex, Indices, Gold, etc.).

✅ An optional external volatility index input (like the VIX) to refine directional bias.

✅ A directional signal (LONG, SHORT, FLAT) based on ATR strength, direction, and external volatility conditions.

✅ A clean visual table showing key values such as ATR, ATR average, ATR %, VIX level, current range, extended range, and final signal.

This tool is ideal for traders looking to:

Monitor the intensity of price movements

Filter trading strategies based on volatility conditions

Identify momentum acceleration or exhaustion

⚙️ Settings Guide

Here’s a breakdown of the user inputs:

🔹 ATR Settings

Setting Description

ATR Length Number of periods for ATR calculation (default: 14)

ATR Smoothing Type of moving average used (RMA, SMA, EMA, WMA)

ATR Average Length Period for the ATR moving average baseline

🔹 Asset Class Preset

Choose between:

Manual – Define your own point multiplier and thresholds

Forex (Pips) – Auto-set for FX markets (high precision)

Indices (0.1 Points) – For index instruments like DAX or S&P

Gold (USD) – Preset suitable for XAU/USD

If Manual is selected, configure:

Setting Description

Points Multiplier Multiplies raw price ranges into useful units (e.g., 10 for Gold)

Low Volatility Threshold Threshold to define "LOW" volatility

High Volatility Threshold Threshold to define "HIGH" volatility

🔹 Extended Range and VIX

Setting Description

Timeframe for Extended High/Low Used to compare larger price ranges (e.g., Daily or Weekly)

External Volatility Index (VIX) Symbol for a volatility index like "VIX" or "EUVI"

Low VIX Threshold Below this level, VIX is considered "low" (default: 20)

High VIX Threshold Above this level, VIX is considered "high" (default: 30)

🔹 Table Display

Setting Description

Table Position Where the visual table appears on the chart (e.g., bottom_center, top_left)

Show ATR Line on Chart Whether to display the ATR line directly on the chart

✅ Signal Logic Summary

The script determines the final signal based on:

ATR being above or below its average

ATR rising or falling

ATR percentage being significant (>2%)

VIX being high or low

Conditions Signal

ATR rising + high volatility + low VIX LONG

ATR falling + high volatility + high VIX SHORT

ATR flat or low volatility or low %ATR FLAT

ATR

Daily Price RangeThe indicator is designed to analyze an instrument’s volatility based on daily extremes (High-Low) and to compare the current day’s range with the typical (median) range over a selected period. This helps traders assess how much of the "usual" daily movement has already occurred and how much may still be possible during the trading day.

ADR & ATR OverlayADR & ATR Overlay

This indicator will display the following as an overlay on your chart:

ADR

% of ADR

ADR % of Price

ATR

% of ATR

ATR % of Price

Description:

ADR : Average Day Range

% of ADR : Percentage that the current price move has covered its average.

ADR % of Price : The percentage move implied by the average range.

ATR : Average True Range

% of ATR : Percentage that the current price move has covered its average.

ATR % of Price : The percentage move implied by the average true range.

Options:

Time Frame

Length

Smoothing

Enable or Disable each value

Text Color

Background Color

How to use this indicator:

The ADR and ATR can be used to provide information about average price moves to help set targets, stop losses, entries and exits based on the potential average moves.

Example: If the "% of ADR" is reading 100%, then 100% of the asset's average price range has been covered, suggesting that an additional move beyond the range has a lower probability.

Example: "ADR % of Price" provides potential price movement in percentage which can be used to asses R/R for asset.

Example: ADR (D) reading is 100% at market close but ATR (D) is at 70% at close. This suggests that there is a potential move of 30% in Pre/Post market as suggested by averages.

Notes:

These indicators are available as oscillators to place under your chart through trading view but this indicator will place them on the chart in numerical only format.

Please feel free to modify this script if you like but please acknowledge me, I am only a hobby coder so this takes some time & effort.

Precision Trend Shot | JeffreyTimmermansPrecision Trend Shot

The "Precision Trend Shot" Indicator is an advanced technical tool designed to provide a dynamic and adaptive view of market trends. By combining three core components—RSI Oscillator, LSMA ATR, and Adaptable Trend—this indicator delivers precise signals that help traders identify market direction, volatility, and potential trend reversals. The calculated total score, derived from these components, provides a clear, actionable view of market conditions.

Key Features

Multi-Component Analysis: Integrates three key indicators (RSI, LSMA ATR, and Adaptable Trend) for a comprehensive view of market trends.

Dynamic Trend Classification: Categorizes market states as "Bullish" or "Bearish", based on a combined score.

Standard Deviation Bands: Displays standard deviation bands around the score line for enhanced volatility visualization.

Gradient Background Coloring: Visually highlights market phases with gradient colors, aiding quick interpretation.

Customizable Visuals: Offers extensive settings for coloring, background gradients, and signal visibility.

Real-Time Alerts: Generates alerts for significant trend changes or transitions between market states.

Inputs & Settings

RSI Settings:

RSI Source: Default: Close price. Defines the data source for RSI calculation.

RSI Length: Default: 10. Sets the period for calculating RSI.

LSMA ATR Settings:

LSMA Source: Default: Close price. Defines the data source for LSMA calculation.

LSMA Length: Default: 21. Sets the period for calculating the Least Squares Moving Average.

ATR Length: Default: 12. Sets the period for calculating the Average True Range.

Adaptable Trend Settings:

Trend Length: Default: 5. Sets the period for calculating the trend.

Smoothing Length: Default: 5. Controls the smoothing of trend volatility.

Sensitivity: Default: 1.5. Adjusts the sensitivity of trend bands.

Standard Deviation Settings:

Enable Standard Deviation Bands: Default: True. Toggles the display of standard deviation bands.

Standard Deviation Length: Default: 20. Sets the period for standard deviation calculation.

Standard Deviation Multiplier: Default: 2.0. Adjusts the width of the bands.

Smoothing Length: Default: 5. Controls the smoothing of standard deviation bands.

Visual Settings:

Enable Candle Coloring: Default: True. Colors candles based on market state (Bullish or Bearish).

Enable Background Gradient: Default: True. Applies gradient coloring to the background based on trend direction.

Score Line Colors: Customize colors for bullish or bearish score lines.

Calculation Process

RSI Calculation:

Computes the Relative Strength Index (RSI) of the selected source data.

Signals bullish (RSI > 50) or bearish (RSI < 50) conditions.

LSMA ATR Calculation:

Computes LSMA for trend direction and ATR for volatility measurement.

Generates buy and sell signals based on crossover and crossunder of ATR bands.

Adaptable Trend Calculation:

Calculates dynamic trend levels using EMA and standard deviation bands.

Classifies trend states as Bullish or Bearish.

Combined Signal Calculation:

Averages the signals from RSI, LSMA ATR, and Adaptable Trend to generate a total score.

Classifies the market as "Bullish" or "Bearish" based on this score.

Standard Deviation Bands:

Plots standard deviation bands around the combined signal for enhanced volatility analysis.

Gradient Background Coloring:

Colors the chart background based on the identified market state (Bullish or Bearish).

How to Use the Precision Trend Shot Indicator

Identifying Market States:

Bullish Market: Total score > 0, gradient background green.

Bearish Market: Total score < 0, gradient background red.

Confirming Signals:

Use RSI and LSMA ATR signals for early indications.

Use Trend Recon for confirming longer-term trend direction.

Visualizing Volatility:

Standard deviation bands highlight potential reversal zones.

Dynamic Alerts

The Precision Trend Shot Indicator includes a robust alert system for real-time market transitions:

Bullish to Bearish: Market shifts from a bullish to bearish trend.

Bearish to Bullish: Market shifts from a bearish to bullish trend.

Conclusion

The Precision Trend Shot Indicator is an advanced, versatile tool for identifying market trends, visualizing volatility, and generating actionable signals. With customizable settings, dynamic alerts, and clear visual representation, it is an essential addition to any trader’s toolkit.

-Jeffrey

MissedPrice Volume Method[KiomarsRakei]█ Core Concept:

This script detects price zones that are highly likely to be revisited — areas where price moved too quickly to fully fill market activity. Using sharp volume shifts and volatility filters, the script identifies these “missed” levels and generates signals pointing toward them.

Signals are generated before price reaches the zone, allowing you to analyze price behavior both before and after the zone is touched. These zones often act like magnets for price, making them ideal for short-term.

Examples of signals and high hit rate of Missed zones

█ How It Works:

The script monitors 3-candle volume and price behavior to detect moments where volume accelerates abnormally compared to recent averages. When a potential missed zone is found and price hasn’t revisited it yet, a signal is created in advance, pointing to that zone as a likely future target.

█ Features:

Zone Visualization: Dynamic boxes show price targets based on missed volume areas.

Pre-Zone Signals: Alerts fire before price returns, offering early trade setups.

Stat Tracking System: Automatically logs signals, win rate, and average profit.

Live Performance Table: On-chart stats including hit/miss breakdown and late-return analysis.

Works on All Markets: Compatible with any chart that provides volume — crypto, forex, indices, or stocks.

A signal is considered successful when price touches the zone. However, not all zones are guaranteed to be revisited.

█ Key Inputs & Stats Table:

Volume Filters: Control signal sensitivity using min/max relative volume shift.

Zone & Line Settings: Adjust how long the zone stays visible and whether entry lines are drawn.

Custom Colors: Choose colors for buy/sell zones, lines, and visuals.

📊 Table Metrics:

Total Signals: Count of all generated signals.

Win Rate: % of signals where price returned to the zone (hit = touched the zone, regardless of timing).

Bad Signals: Signals that took too long to hit or were never hit.

Bad but Hit: Signals marked bad but eventually touched the zone.

Bad signals are marked in red. These indicate zones that price failed to reach within the expected time window, showing where the script identified a target that remained unfulfilled.

Dumb Money ConceptUse in 1 minute timeframe

1. Strategy setup

Name & sizing: Trades 25% of your account on each signal, assumes 0.04% commission + 2‑tick slippage, starts with a notional 10 million.

Timing: Only makes decisions at each 1‑minute bar close, and processes orders at bar‑close.

2. Optional filters (both default to off)

Volatility filter : when on, requires that yesterday’s ATR (average true range) ≥ your threshold before even placing an entry.

Trend filter : when on, only allows a “long” if yesterday’s close was above its daily MA, or a “short” if below.

You can toggle each filter on/off and adjust ATR period, ATR threshold, and MA length through the inputs at the top.

3. Signal logic (“dumb money” wicks)

At today’s first minute, the script pulls yesterday’s open, high, low, close, ATR and MA—using only completed daily bars so nothing repaints.

It measures the size of yesterday’s upper wick (close→high) vs. lower wick (open→low).

If the upper wick was longer, that sets a long bias (“dumb money” got shaken out at the top). Otherwise it sets a short bias.

4. Calculate where to place orders

On that same first minute of day:

Entry: a limit order at half of yesterday’s range away from today’s open (below the open for longs, above for shorts).

Stop‑loss: one full‑range (×1.0) below today’s open for longs (and above for shorts).

Take‑profit: 1.236× yesterday’s range above today’s open for longs (and below for shorts).

5. Apply filters before sending entry

Before actually placing that limit order, it checks:

Volatility: if enabled, requires yesterday’s ATR ≥ your “Min Daily ATR.”

Trend: if enabled, requires yesterday’s close to lie on the same side of its daily MA as your signal.

If either filter fails, no order is sent.

6. Give the limit order up to 24 hours to fill

The code remembers the bar‑index when the order went live.

If 1440 one‑minute bars pass (≈24 h) without a fill, it automatically cancels the unfilled entry—so stale orders don’t hang around.

7. Once filled, TP/SL manage the trade

As soon as your limit order executes, two opposite orders are placed:

A take‑profit at the 1.236× range level

A stop‑loss at the –1.0× range level

One cancels the other when triggered.

8. No overnight risk

On the very first minute of the next daily bar, any position still open is force‑closed (“Time Exit”)

MACD-V with Volatility Normalisation [DCD]MACD-V with Volatility Normalisation

This indicator is a modified version of the traditional MACD, designed to account for market volatility by normalizing the MACD line using the Average True Range (ATR). It provides a more adaptive approach to identifying momentum shifts and potential trend reversals. This indicator was developed by Alex Spiroglou in this paper:

Spiroglou, Alex, MACD-V: Volatility Normalised Momentum (May 3, 2022).

Features:

Volatility Normalization: The MACD line is adjusted using ATR to standardize its values across different market conditions.

Customizable Parameters: Users can adjust the MACD fast length, slow length, signal line smoothing, and ATR length to suit their trading style.

Histogram Visualization: The histogram highlights the difference between the MACD and signal lines, with customizable colors for positive and negative momentum.

Crossover Signals: Green and red dots indicate bullish and bearish crossovers between the MACD and signal lines.

Background Highlighting: The chart background changes to green when the MACD is above 0 and red when it is below 0, providing a clear visual cue for bullish and bearish conditions.

Horizontal Levels: Dotted horizontal lines are plotted at key levels for better visualization of MACD values.

How to Use:

Look for crossovers between the MACD and signal lines to identify potential buy or sell signals.

Use the histogram to gauge the strength of momentum.

Pay attention to the background color for quick identification of bullish (green) or bearish (red) conditions.

This indicator is ideal for traders who want a more dynamic MACD that adapts to market volatility. Customize the settings to align with your trading strategy and timeframe.

Daily ATR Bonanza: Expected Moves - Tr33man Daily ATR Bonanza: Expected Moves

Overview 🤷♂️

The Daily ATR Bonanza script is a powerful trading tool designed to help traders visualize and understand potential price movements using the Average True Range (ATR). It provides daily and weekly ATR levels, historical statistics, and conditional probability analysis to give traders actionable insights. The script also plots the daily Keltner channel. This script is ideal for traders who want to gauge volatility, identify key levels, and make data-driven decisions.

b]Key Features:

📈 1. Daily and Weekly ATR Levels

🔵ATR Levels: The script calculates and displays ATR-based levels for the day and week. These levels are derived from the previous day's or week's close price and are adjusted using customizable multipliers (0.5x, 1x, and 1.5x by default).

🔵You can choose the number of ATR levels (1, 2, or 3) and adjust the multipliers to suit your trading strategy.

🌐 2. ATR Bands (Keltner Channels)

🔵The script includes an option to display ATR Bands, which are volatility-based envelopes around a moving average. These bands help identify overbought and oversold conditions.

🔵You can adjust the ATR multiplier and the length of the moving average used for the bands.

🧮 3. Historical Statistics and Conditional Probability

🔵 Historical Analysis: The script analyzes historical price movements to calculate the likelihood of closing at certain ATR levels.

🔵 Conditional Probability: This feature shows the probability of the price reaching specific ATR levels given the current market conditions. The conditional matches historical data by an open in the same opening ATR bucket, as well as the current price bucket having been visited in the historical case. Conditional probabilities are just statistics, and do not predict anything.

Data Table: 📚

🔵 Historical Close Probability: The percentage of days the price closed within each ATR level.

🔵 Conditional Close Probability: The likelihood of the price closing within each ATR level today.

❓ What is Conditional Probability? ❓

Conditional probability is a statistical measure that calculates the likelihood of an event occurring given that another event has already occurred. In this script, it is used to determine the probability of the price reaching specific ATR levels based on the current opening range as well as current ATR distance from the previous close.

For example:

If the market opens near the lower end of the first ATR level, the script calculates the likelihood of the price reaching the upper end of the first, second, or third ATR level.

This analysis is based on historical data, making it a powerful tool for understanding potential price movements.

🌟 Understanding the Levels

🔵Daily Levels: These are based on the previous day's close price and ATR. They are updated at the start of each new day.

🔵Weekly Levels: These are based on the previous week's close price and ATR. They are updated at the start of each new week.

🔵ATR Bands: These are dynamic levels that adjust with market volatility.

🔬 Analyze the Statistics (Daily only for now, no weekly yet)

🔵Use the interactive table to understand historical probabilities and conditional probabilities.

🔵Focus on the current opening range and the likelihood of reaching specific levels.

🧠 Make Trading Decisions

🔵Use the ATR levels and bands to identify key support and resistance levels.

🔵Use the conditional probability table to gauge the likelihood of reaching specific targets.

🔵Adjust your strategy based on the historical performance of the market.

Example Use Cases

1. Day Trading

Use the daily ATR levels to set intraday targets and stop-loss levels.

Monitor the conditional probability table to adjust your expectations based on the opening range.

2. Swing Trading

Use the weekly ATR levels to identify longer-term support and resistance levels.

3. Scalping

Use the ATR bands to identify overbought and oversold conditions.

Use the conditional probability table to quickly assess the likelihood of price movements.

Smart Market Matrix Smart Market Matrix

This indicator is designed for intraday, scalping, providing automated detection of price pivots, liquidity traps, and breakout confirmations, along with a context dashboard featuring volatility, trend, and volume.

## Summary Description

### Menu Settings & Their Roles

- **Swing Pivot Strength**: Controls the sensitivity for detecting High/Low pivots.

- **Show Pivot Points**: Toggles the display of HH/LL markers on the chart.

- **VWMA Length for Trap Volume** & **Volume Spike Multiplier**: Identify concentrated volume spikes for liquidity traps.

- **Wick Ratio Threshold** & **Max Body Size Ratio**: Detect candles with disproportionate wicks and small bodies (doji-ish) for traps.

- **ATR Length for Trap**: Measures volatility specific to trap detection.

- **VWMA Length for Breakout Volume**, **ATR Multiplier for Breakout**, **ATR Length for Breakout**, **Min Body/Range Ratio**: Set adaptive breakout thresholds based on volatility and volume.

- **OBV Smooth Length**: Smooths OBV momentum for breakout confirmation.

- **Enable VWAP Filter for Confirmations**: Optionally validate breakouts against the VWAP.

- **Enable Higher-TF Trend Filter** & **Trend Filter Timeframe**: Align breakout signals with the 1h/4h/Daily trend.

- **ADX Length**, **EMA Fast/Slow Length for Context**: Parameters for the context dashboard (Volatility, Trend, Volume).

- **Show Intraday VWAP Line**, **VWAP Line Color/Width**: Display the intraday VWAP line with custom style.

### Signal Interpretation Map

| Signal | Description | Recommended Action |

|--------------------------------|-----------------------------------------------------------|-------------------------------------------|

| 📌 **HH / LL (pivot)** | Market structure (support/resistance) | Note key levels |

| **Bull Trap(green diamond)** | Sweep down + volume spike + wick + rejection | Go long with trend filter

| **Bear Trap(red diamond)** | Sweep up + volume spike + wick + rejection | Go short with trend filter

| 🔵⬆️ **Breakout Confirmed Up** | Close > ATR‑scaled high + volume + OBV↑ | Go long with trend filter |

| 🔵⬇️ **Breakout Confirmed Down** | Close < ATR‑scaled low + volume + OBV↓ | Go short with trend filter |

| 📊 **VWAP Line** | Intraday reference to guide price | Use as dynamic support/resistance |

| ⚡ **Volatility** | ATR ratio High/Med/Low | Adjust position size |

| 📈 **Trend Context** | ADX+EMA Strong/Moderate/Weak | Confirm trend direction |

| 🔍 **Volume Context** | Breakout / Rising / Falling / Calm | Check volume momentum |

*This summary gives you a quick overview of the key settings and how to interpret signals for efficient intraday scalping.*

### Suggested Settings

- **Intraday Scalping (5m–15m)**

- `Swing Pivot Strength = 5`

- `VWMA Length for Trap Volume = 10`, `Volume Spike Multiplier = 1.6`

- `ATR Length for Trap = 7`

- `VWMA Length for Breakout Volume = 12`, `ATR Length for Breakout = 9`, `ATR Multiplier for Breakout = 0.5`

- `Min Body/Range Ratio for Breakout = 0.5`, `OBV Smooth Length = 7`

- `Enable Higher-TF Trend Filter = true` (TF = 60)

- `Show Intraday VWAP Line = true` (Color = orange, Width = 2)

- **Swing Trading (4h–Daily)**

- `Swing Pivot Strength = 10`

- `VWMA Length for Trap Volume = 20`, `Volume Spike Multiplier = 2.0`

- `ATR Length for Trap = 14`

- `VWMA Length for Breakout Volume = 30`, `ATR Length for Breakout = 14`, `ATR Multiplier for Breakout = 0.8`

- `Min Body/Range Ratio for Breakout = 0.7`, `OBV Smooth Length = 14`

- `Enable Higher-TF Trend Filter = true` (TF = D)

- `Show Intraday VWAP Line = false`

*Adjust these values based on the symbol and market volatility for optimal performance.*

[Stop!Loss] ADR Signal ADR Signal - a technical indicator located in a separate window, which displays by default the 80%-level , as well as the 100%-level of the average daily range (ADR) for the last 10 days and compares it with the current intraday range. The indicator helps not only with the use of a mathematical-statistical method to identify a potential reversal at the moment during intraday trading, but can also serves as an effective assistant in risk management.

👉 Basic mechanics of the indicator

Firstly, this indicator tracks the performance of the standard ATR indicator on the daily chart, in other words, ADR (Average Daily Range).

Important ❗️The ATR (Average True Range) indicator was created by J. Welles Wilder Jr. He first introduced ATR in his book "New Concepts in Technical Trading Systems", published in 1978. Wilder developed this indicator to measure market volatility to help traders estimate the range of price movements. This indicator is built into TradingView, more details can be found by link: www.tradingview.com

Like ATR , ADR calculates the average true range for a specified period. In this case, the distance in points from the maximum of each day to its minimum is calculated, after which the arithmetic mean is calculated - this is ADR .

👉 Visualization

ADR Signal is located in a separate window on the chart and has 3 levels:

1) "ADR level" (green line) - the same parameter, the calculations of which are briefly described above. There is 100%-level of ATR on the daily chart (ADR).

2) "Current level" (red line) - this is the current price passage within the day, calculated in points. At the start of a new day, this parameter is reset. Therefore, in the indicator window, this line has sharp drops at the start of a new trading day: "A new trading day - the instrument's power reserve is renewed again".

3) "Signal level" (blue line) - this is an individually customized value that demonstrates a certain part of the ADR parameter.

👉 Inputs

1) - is responsible for the ATR indicator period, the value of which will always be calculated on the daily chart. The default value is "10", that is, ATR is calculated for the last 10 days (not including the current one).

2) - signal level (in %). The default value is "0.8", that is, 80%-level of the ADR parameter (set earlier) is calculated.

👉 Style

1) - by default, this level is colored "blue".

2) - by default, this level is colored "red".

3) - by default, this level is colored "green".

👉 How to use this indicator

Important❗️ The two methods of the use of the ADR Signal indicator described below will be most effective when trading intraday (which is highlighted quite well below), so it is more logical to use the indicator information on time periods H1 and below.

1) Identifying potential reversals during intraday trading:

The ADR Signal indicator can be used as a potential individual reversal strategy.

Important ❗️It should be noted that using it in it without additional confirming analysis tools will be a rather aggressive trading approach. Therefore, it is best to support the entry point in particular with other methods.

In this case, the crossing of the red line (the number of points passed within the current day, that is, from the minimum of the current day to its maximum) and the blue line (color of the Signal level based on the default settings), indicates that the trading instrument has passed 80% (based on the default settings for the "Signal level") of its average distance from the maximum to the minimum over the past 10 days (based on the default settings for the "ADR Length"). Such a situation in the context of the mathematical-statistical approach indicates a probable reversal, since the "power reserve" of this instrument is mostly exhausted, so one can expect with a higher probability, at least, a price stop and possibly a reversal. In case of crossing of the red line and the green one (ADR level), it says again that based on the mathematical-statistical approach, this trading instrument has completely exhausted its intraday "power reserve". In this situation, a stop or reversal of the price will be even more likely.

Of course, using the "Signal level" parameter, one can filter out even more reliable situations for potential price reversals within a day, namely, by specifying, for example, 1.5 in the field of this parameter. Under such conditions, in the case of crossing the red and blue lines (based on the default style settings), to say that the trading instrument has passed 150% of its average distance over the last 10 days (based on the default style settings "ADR length"). In this case, the probability of a stop or reversal of the price increases even more.

2) Use in risk management:

In terms of risk management, this indicator is more applicable to open trades. For example, if one had an open Buy-position (especially if it is an intraday trade) and the price has raised significantly during the day, then the crossing of the red line with the blue line , and especially the red line with the green line , may indicate that the price will most likely stop growing, since the "power reserve" is almost or completely exhausted for this instrument within the current day. In this case, one can, at a minimum, move the trade to breakeven or even partially fix the profit.

We will continue to discuss the methods of using this indicator and strategies based on it here. And we are always waiting for your reactions and feedback on this topic 💬.

Thank you for your support 🚀

RSI Divergence Strategy - AliferCryptoStrategy Overview

The RSI Divergence Strategy is designed to identify potential reversals by detecting regular bullish and bearish divergences between price action and the Relative Strength Index (RSI). It automatically enters positions when a divergence is confirmed and manages risk with configurable stop-loss and take-profit levels.

Key Features

Automatic Divergence Detection: Scans for RSI pivot lows/highs vs. price pivots using user-defined lookback windows and bar ranges.

Dual SL/TP Methods:

- Swing-based: Stops placed a configurable percentage beyond the most recent swing high/low.

- ATR-based: Stops placed at a multiple of Average True Range, with a separate risk/reward multiplier.

Long and Short Entries: Buys on bullish divergences; sells short on bearish divergences.

Fully Customizable: Input groups for RSI, divergence, swing, ATR, and general SL/TP settings.

Visual Plotting: Marks divergences on chart and plots stop-loss (red) and take-profit (green) lines for active trades.

Alerts: Built-in alert conditions for both bullish and bearish RSI divergences.

Detailed Logic

RSI Calculation: Computes RSI of chosen source over a specified period.

Pivot Detection:

- Identifies RSI pivot lows/highs by scanning a lookback window to the left and right.

- Uses ta.barssince to ensure pivots are separated by a minimum/maximum number of bars.

Divergence Confirmation:

- Bullish: Price makes a lower low while RSI makes a higher low.

- Bearish: Price makes a higher high while RSI makes a lower high.

Entry:

- Opens a Long position when bullish divergence is true.

- Opens a Short position when bearish divergence is true.

Stop-Loss & Take-Profit:

- Swing Method: Computes the recent swing high/low then adjusts by a percentage margin.

- ATR Method: Uses the current ATR × multiplier applied to the entry price.

- Take-Profit: Calculated as entry price ± (risk × R/R ratio).

Exit Orders: Uses strategy.exit to place bracket orders (stop + limit) for both long and short positions.

Inputs and Configuration

RSI Settings: Length & price source for the RSI.

Divergence Settings: Pivot lookback parameters and valid bar ranges.

SL/TP Settings: Choice between Swing or ATR method.

Swing Settings: Swing lookback length, margin (%), and risk/reward ratio.

ATR Settings: ATR length, stop multiplier, and risk/reward ratio.

Usage Notes

Adjust the Pivot Lookback and Range values to suit the volatility and timeframe of your market.

Use higher ATR multipliers for wider stops in choppy conditions, or tighten swing margins in trending markets.

Backtest different R/R ratios to find the balance between win rate and reward.

Disclaimer

This script is for educational purposes only and does not constitute financial advice. Trading carries significant risk and you may lose more than your initial investment. Always conduct your own research and consider consulting a professional before making any trading decisions.

ATR & Session & Pivot & Note – MultiTF Utility**ATR & Session & Pivot – MultiTF Utility**

**Description**:This versatile indicator is designed for technical analysis in Forex, Crypto, Gold, and Silver markets. It displays ATR (Average True Range) values across multiple timeframes (Current, 1m, 5m, 15m, 1H, 4H, 1D, 1W) with TP/SL levels, alongside Pivot Point analysis (minor and major), Structure Lines, and Trading Session Boxes.

**Features:**

- **Multi-Timeframe ATR Table:** Shows ATR values for various timeframes with customizable table position (top/middle/bottom, left/center/right) and decimal precision.

- **Custom Text Colors:** Distinct colors for 5m (red), 1H (blue), My ATR (green), and LQ Close (purple).

- **Pivot Points:** Identifies minor pivots (HH, LH, LL, HL) with 9 left and 4 right bars, and major pivots with 18 left and 9 right bars.

- **Structure Lines:** Displays lines connecting pivots with adjustable style and width.

- **Session Boxes:** Highlights New York, London, Tokyo, and Sydney sessions (Tehran timezone +3:30) with customizable background transparency and day-of-week labels.

- **Special Calculations:** Includes My ATR, ATI, SCEP, LQ Close, Min LQ, Max LQ, My CL, and Min Reward.

**How to Use:**

1. Add the indicator to your chart.

2. Customize table position, colors, decimal precision, and enable/disable sessions or pivots via settings.

3. Use ATR values for setting TP/SL levels and leverage pivots and session boxes to identify key market levels.

**Settings:**

- **Table Position & Style:** Adjust table placement and font size.

- **ATR Options:** Enable/disable specific timeframes or special calculations.

- **Sessions:** Toggle visibility of trading sessions and adjust transparency.

- **Pivots:** Enable/disable minor/major pivots and set bar counts.

- **Structure Lines:** Activate lines and customize color, width, and style.

**Ideal For**:Traders seeking a comprehensive tool for ATR analysis, pivot identification, and session-based trading across multiple timeframes.

**Note:** Tailor the settings to align with your trading strategy and market for optimal results.

Daily ATR BandsATR Finder – Volatility Scanner for Smarter Trade Setups

The ATR Finder is a precision tool designed to help traders quickly identify high-volatility assets using the Average True Range (ATR) – a key metric in assessing market momentum and potential breakout zones. By automatically scanning and highlighting tickers or candles with elevated ATR values relative to their recent historical range, this indicator helps you filter for setups that are more likely to experience significant price moves.

Whether you're a day trader seeking intraday momentum or a swing trader looking for setups with strong follow-through potential, the ATR Finder cuts through the noise and visually signals which assets are "on the move." It can be paired with other indicators or price action tools to create a high-conviction trading strategy focused on volatility expansion.

Key Features:

Dynamic ATR Calculation over a user-defined period

Visual Alerts or Color-Coding for above-threshold volatility spikes

Supports Multiple Timeframes for both short- and long-term volatility analysis

Great for spotting breakout opportunities, gap continuations, or trend reversals

Use the ATR Finder to stay ahead of price action and build a watchlist that moves with purpose. Perfect for scalpers, breakout traders, and anyone who respects the power of volatility.

Advanced Momentum Scanner [QuantAlgo]The Advanced Momentum Scanner is a sophisticated technical indicator designed to identify market momentum and trend direction using multiple exponential moving averages (EMAs), momentum metrics, and adaptive visualization techniques. It is particularly valuable for those looking to identify trading and investing opportunities based on trend changes and momentum shifts across any market and timeframe.

🟢 Technical Foundation

The Advanced Momentum Scanner utilizes a multi-layered approach with four different EMA periods to identify market momentum and trend direction:

Ultra-Fast EMA for quick trend changes detection (default: 5)

Fast EMA for short-term trend analysis (default: 10)

Mid EMA for intermediate confirmation (default: 30)

Slow EMA for long-term trend identification (default: 100)

For momentum detection, the indicator implements a Rate of Change (RoC) calculation to measure price momentum over a specified period. It further enhances analysis by incorporating RSI readings for overbought/oversold conditions, volatility measurements through ATR, and optional volume confirmation. When these elements align, the indicator generates trading signals based on the selected sensitivity mode (Conservative, Balanced, or Aggressive).

🟢 Key Features & Signals

1. Multi-Period Trend Identification

The indicator combines multiple EMAs of different lengths to provide comprehensive trend analysis within the same timeframe, displaying the information through color-coded visual elements on the chart.

When an uptrend is detected, chart elements are colored with the bullish theme color (default: green/teal).

Similarly, when a downtrend is detected, chart elements are colored with the bearish theme color (default: red).

During neutral or indecisive periods, chart elements are colored with a neutral gray color, providing clear visual distinction between trending and non-trending market conditions.

This visualization provides immediate insights into underlying trend direction without requiring separate indicators, helping traders and investors quickly identify the market's current state.

2. Trend Strength Information Panel

The trend panel operates in three different sensitivity modes (Conservative, Aggressive, and Balanced), each affecting how the indicator processes and displays market information.

The Conservative mode prioritizes trend sustainability over frequency, showing only strong trend movements with high probability.

The Aggressive mode detects early trend changes, providing more frequent signals but potentially more false positives.

The Balanced mode offers a middle ground with moderate signal frequency and reliability.

Regardless of the selected mode, the panel displays:

Current trend direction (UPTREND, DOWNTREND, or NEUTRAL)

Trend strength percentage (0-100%)

Early detection signals when applicable

The active sensitivity mode

This comprehensive approach helps traders and investors:

→ Assess the strength of current market trends

→ Identify early potential trend changes before full confirmation

→ Make more informed trading and investing decisions based on trend context

3. Customizable Visualization Settings

This indicator offers extensive visual customization options to suit different trading styles and preferences:

Display options:

→ Fully customizable uptrend, downtrend, and neutral colors

→ Color-coded price bars showing trend direction

→ Dynamic gradient bands visualizing potential trend channels

→ Optional background coloring based on trend intensity

→ Adjustable transparency levels for all visual elements

These visualization settings can be fine-tuned through the indicator's interface, allowing traders and investors to create a personalized chart environment that emphasizes the most relevant information for their strategy.

The indicator also features a comprehensive alert system with notifications for:

New trend formations (uptrend, downtrend, neutral)

Early trend change signals

Momentum threshold crossovers

Other significant market conditions

Alerts can be customized and delivered through TradingView's notification system, making it easy to stay informed of important market developments even when you are away from the charts.

🟢 Practical Usage Tips

→ Trend Analysis and Interpretation: The indicator visualizes trend direction and strength directly on the chart through color-coding and the information panel, allowing traders and investors to immediately identify the current market context. This information helps in assessing the potential for continuation or reversal.

→ Signal Generation Strategies: The indicator generates potential trading signals based on trend direction, momentum confirmation, and selected sensitivity mode. Users can choose between Conservative (fewer but more reliable signals), Balanced (moderate approach), or Aggressive (more frequent but potentially less reliable signals).

→ Multi-Period Trend Assessment: Through its layered EMA approach, the indicator enables users to understand trend conditions across different lookback periods within the same timeframe. This helps in identifying the dominant trend and potential turning points.

🟢 Pro Tips

Adjust EMA periods based on your timeframe:

→ Lower values for shorter timeframes and more frequent signals

→ Higher values for higher timeframes and more reliable signals

Fine-tune sensitivity mode based on your trading style:

→ "Conservative" for position trading/long-term investing and fewer false signals

→ "Balanced" for swing trading/medium-term investing with moderate signal frequency

→ "Aggressive" for scalping/day trading and catching early trend changes

Look for confluence between components:

→ Strong trend strength percentage and direction in the information panel

→ Overall market context aligning with the expected direction

Use for multiple trading approaches:

→ Trend following during strong momentum periods

→ Counter-trend trading at band extremes during overextension

→ Early trend change detection with sensitivity adjustments

→ Stop loss placement using dynamic bands

Combine with:

→ Volume indicators for additional confirmation

→ Support/resistance analysis for strategic entry/exit points

→ Multiple timeframe analysis for broader market context

Supertrend Hombrok BotSupertrend Hombrok Bot – Automated Trading Strategy for Dynamic Market Conditions

This trading strategy script has been developed to operate automatically based on detailed market conditions. It combines the popular Supertrend indicator, RSI (Relative Strength Index), Volume, and ATR (Average True Range) to determine the best entry and exit points while maintaining proper risk management.

Key Features:

Supertrend as the Base: Uses the Supertrend indicator to identify the market's trend direction, generating buy signals when the market is in an uptrend and sell signals when in a downtrend.

RSI Filter: The RSI is used to determine overbought and oversold conditions, helping to avoid entries in extreme market conditions. Entries are avoided when RSI > 70 (overbought) and RSI < 30 (oversold), reducing the risk of false movements.

Volume Filter: The strategy checks if the trading volume is above the average multiplied by a user-defined factor. This ensures that only significant movements, with higher liquidity, are considered.

Candle Body Size: The strategy filters only candles with a body large enough relative to the ATR (Average True Range), ensuring that the price movements on the chart have sufficient strength.

Risk Management: The bot is configured to operate with an adjustable Risk/Reward Ratio (R:R). This means that for each trade, both Take Profit (TP) and Stop Loss (SL) are adjusted based on the market's volatility as measured by the ATR.

Automatic Entries and Exits: The script automatically executes entries based on the specified conditions and exits with predefined Stop Loss and Take Profit levels, ensuring risk is controlled for each trade.

How It Works:

Buy Condition: Triggered when the market is in an uptrend (Supertrend), the volume is above the adjusted average, the candle body is strong enough, and the RSI is below the overbought level.

Sell Condition: Triggered when the market is in a downtrend (Supertrend), the volume is above the adjusted average, the candle body is strong enough, and the RSI is above the oversold level.

Alerts:

Buy and Sell Alerts are configured with detailed information, including Stop Loss and Take Profit values, allowing the user to receive notifications when trading conditions are met.

Capital Management:

The capital per trade can be adjusted based on account size and risk profile.

Important Note:

Always test before trading with real capital: While the strategy has been designed based on solid technical analysis methods, always perform tests in real-time market conditions with demo accounts before applying the bot in live trading.

Disclaimer: This script is a tool to assist in the trading process and does not guarantee profit. Past performance is not indicative of future results, and the trader is always responsible for their investment decisions.

Vinicius Setup ATR

Description:

This script is a strategy based on the Supertrend indicator combined with volume analysis, candle strength, and RSI. Its goal is to identify potential entry points for buy and sell trades based on technical criteria, without promising profitability or guaranteed results.

Script Components:

Supertrend: Used as the main trend compass. When the trend is positive (direction = 1), buy signals are considered; when negative (direction = -1), sell signals are considered.

Volume: Entries are only validated if the volume is above the average of the last 20 candles, adjusted with a 1.2 multiplier.

Candle Body: The candle body must be larger than a certain percentage of the ATR, ensuring sufficient strength and volatility.

RSI: Used as a filter to avoid trades in extreme overbought or oversold zones.

Support and Resistance: Identified based on simple pivots (5 periods before and after).

Customizable Parameters:

ATR Length and Multiplier: Controls the sensitivity of the Supertrend.

RSI Period: Adjusts the relative strength filter.

Minimum Volume and Candle Body: Settings to validate entry signals.

Entry Conditions:

Buy: Positive trend + strong candle + high volume + RSI below 70.

Sell: Negative trend + strong candle + high volume + RSI above 30.

Exit Conditions:

The trade is closed upon the appearance of an opposite signal.

Notes:

This is a technical system with no profit guarantees.

It is recommended to test with realistic capital values and parameters suited to your risk management.

The script is not optimized for specific profitability, but rather to support study and the construction of setups with objective criteria.

DEMA Trend Oscillator Strategy📌 Overview

The DEMA Trend Oscillator Strategy is a dynamic trend-following approach based on the Normalized DEMA Oscillator SD.

It adapts in real-time to market volatility with the goal of improving entry accuracy and optimizing risk management.

⚠️ This strategy is provided for educational and research purposes only.

Past performance does not guarantee future results.

🎯 Strategy Objectives

The main goal of this strategy is to respond quickly to sudden price movements and trend reversals,

by combining momentum-based signals with volatility filters.

It is designed to be user-friendly for traders of all experience levels.

✨ Key Features

Normalized DEMA Oscillator: A momentum indicator that normalizes DEMA values on a 0–100 scale, allowing intuitive identification of trend strength

Two-Bar Confirmation Filter: Requires two consecutive bullish or bearish candles to reduce noise and enhance entry reliability

ATR x2 Trailing Stop: In addition to fixed stop-loss levels, a trailing stop based on 2× ATR is used to maximize profits during strong trends

📊 Trading Rules

Long Entry:

Normalized DEMA > 55 (strong upward momentum)

Candle low is above the upper SD band

Two consecutive bullish candles appear

Short Entry:

Normalized DEMA < 45 (downward momentum)

Candle high is below the lower SD band

Two consecutive bearish candles appear

Exit Conditions:

Take-profit at a risk-reward ratio of 1.5

Stop-loss triggered if price breaks below (long) or above (short) the SD band

Trailing stop activated based on 2× ATR to secure and extend profits

💰 Risk Management Parameters

Symbol & Timeframe: Any (AUDUSD 5M example)

Account size (virtual): $3000

Commission: 0.4PIPS(0.0004)

Slippage: 2 pips

Risk per trade: 5%

Number of trades (backtest):534

All parameters can be adjusted based on broker specifications and individual trading profiles.

⚙️ Trading Parameters & Considerations

Indicator: Normalized DEMA Oscillator SD

Parameter settings:

DEMA Period (len_dema): 40

Base Length: 20

Long Threshold: 55

Short Threshold: 45

Risk-Reward Ratio: 1.5

ATR Multiplier for Trailing Stop: 2.0

🖼 Visual Support

The chart displays the following visual elements:

Upper and lower SD bands (±2 standard deviations)

Entry signals shown as directional arrows

🔧 Strategy Improvements & Uniqueness

This strategy is inspired by “Normalized DEMA Oscillator SD” by QuantEdgeB,

but introduces enhancements such as a two-bar confirmation filter and an ATR-based trailing stop.

Compared to conventional trend-following strategies, it offers superior noise filtering and profit optimization.

✅ Summary

The DEMA Trend Oscillator Strategy is a responsive and practical trend-following method

that combines momentum detection with adaptive risk management.

Its visual clarity and logical structure make it a powerful and repeatable tool

for traders seeking consistent performance in trending markets.

⚠️ Always apply appropriate risk management. This strategy is based on historical data and does not guarantee future results.

RSI-MACD Momentum Fusion Indicator(RMFI)📈 RSI-MACD Momentum Fusion Indicator (RMFI)

The RMFI combines the strengths of two RSI variants with a dynamically adaptive MACD module into a powerful momentum oscillator ranging from 0 to 100. The goal is to unify converging momentum information from different perspectives into a clear, weighted overall signal.

🔧 Core Features

RSI 1: Classic Wilder RSI, sensitive to short-term momentum.

RSI 2: Modified RSI based on normalized price movement ranges (Range Momentum).

MACD (3 Modes):

Standardized (min/max-based)

Fully adaptive (Z-score normalization)

50% adaptive (hybrid weighting of both approaches)

Dynamic MACD mode selection (optional): Automatic switching of MACD normalization based on volatility levels (ATR-based).

Signal Line: Smoothed average of all components to visualize momentum trends and crossovers.

🎯 Visualization

Clear separation of overbought (>70) and oversold (<30) zones with color highlighting.

Different colors based on the dynamic MACD mode – visually indicates how strongly the market adapts to volatility.

⚙️ Recommended Use

Ideal for trend following, divergence confirmation (with external divergence logic), and momentum reversals.

Particularly effective in volatile markets, as the MACD component adaptively responds to instability.

© champtrades

Intraday Uncertainty [PhenLabs]📊 Intraday Uncertainty

Version: PineScript™ v6

📌 Description

The Intraday Uncertainty indicator offers traders a visual representation of market certainty/uncertainty during trading sessions. By comparing each price bar’s range to the Average True Range (ATR), it provides an intuitive way to gauge market conviction through a color gradient system.

This tool helps traders identify periods of high certainty (potentially trending markets) versus high uncertainty (potentially choppy or volatile markets) without complex calculations or multiple indicators. The color-coded bars create an immediate visual cue to support decision-making in varying market conditions.

🚀 Points of Innovation

Automated range-to-ATR ratio calculation that adapts to changing market volatility

Dynamic color gradient system that visually distinguishes between certain and uncertain price action

Customizable gradient clamping to fine-tune sensitivity to market conditions

Integrated dashboard that provides clear interpretation guidance

Position-flexible legend that accommodates different chart layouts

Highly optimized for performance with minimal calculation overhead

🔧 Core Components

ATR Calculation: Measures market volatility using a configurable lookback period

Range-to-ATR Ratio: Compares current bar’s high-low range against average volatility

Gradient Mapping System: Converts numerical uncertainty values into an intuitive color scale

Dashboard Legend: Provides clear interpretation guidance with customizable positioning

🔥 Key Features

Bar Coloring: Instantly identifies market certainty levels through intuitive color gradients

Customizable ATR Period: Adjust sensitivity to historical volatility based on trading style

Gradient Clamping: Fine-tune the color sensitivity using the Range/ATR multiplier

Color Customization: Personalize the color scheme to match your chart aesthetics

Informative Dashboard: Quickly interpret color meanings with the optional on-chart legend

Flexible Display Options: Customize dashboard position and text size for your chart layout

🎨 Visualization

Color Gradient: Bars colored on a spectrum from green (high certainty) to red (high uncertainty)

Dashboard Legend: Optional on-chart guide explaining the color interpretation

Color Intensity: Stronger colors indicate more extreme certainty/uncertainty levels

At-a-glance Interpretation: Quickly identify market conviction without analyzing numbers

📖 Usage Guidelines

Calculation Settings

ATR Period

Default: 14

Range: 1+

Description: Controls the lookback period for ATR calculation. Lower values increase sensitivity to recent volatility, while higher values provide more stability.

Gradient Clamp (Range/ATR Multiplier)

Default: 2.0

Range: 0.1+

Description: Sets the maximum Range/ATR ratio for gradient scaling. Ranges above this value display the end color (high uncertainty).

Color Settings

Gradient Start Color (High Certainty)

Default: Green

Description: Color representing high market certainty (low Range/ATR ratio)

Gradient End Color (Low Certainty)

Default: Red

Description: Color representing low market certainty (high Range/ATR ratio)

Dashboard Settings

Show Dashboard Legend

Default: True

Description: Toggles the visibility of the on-chart interpretation guide

Dashboard Position

Options: top_right, top_left, bottom_right, bottom_left, middle_right, middle_left

Default: bottom_right

Description: Controls the placement of the dashboard on your chart

Dashboard Text Size

Options: tiny, small, normal, large, huge

Default: normal

Description: Adjusts the text size of the dashboard for readability

✅ Best Use Cases

Identifying potential trend shifts when certainty levels change dramatically

Confirming trend strength through consistent certainty levels

Detecting choppy/sideways markets with persistent high uncertainty

Filtering trading signals from other indicators based on certainty levels

Gauging market conviction behind price breakouts or pullbacks

Optimizing entry/exit timing based on certainty/uncertainty transitions

⚠️ Limitations

Does not predict future price direction, only measures current bar certainty

May provide false signals during news events or unexpected volatility spikes

Requires context within the broader market environment for optimal interpretation

Color interpretation is relative rather than absolute across different securities

ATR-based calculation means sensitivity varies across different timeframes

💡 What Makes This Unique

Simplicity: Single visual indicator that doesn’t require multiple technical tools

Adaptability: Automatically adjusts to changing market volatility conditions

Contextual Analysis: Provides market conviction context beyond just price movement

Intuitive Design: Color-based system that requires minimal learning curve

Efficiency: Lightweight calculation that doesn’t impact chart performance

🔬 How It Works

1. ATR Calculation:

Calculates the Average True Range using the specified period

Establishes a baseline for normal market volatility

2. Range Analysis:

Measures each bar’s high-low range

Compares this range to the current ATR value to create a ratio

3. Gradient Mapping:

Converts the Range/ATR ratio to a normalized value between 0 and 1

Maps this value onto a color gradient between the start and end colors

Applies the resulting color to the price bar

4. Dashboard Creation:

Constructs an information panel on the last visible bar

Populates it with color samples and interpretation guidance

💡 Note:

This indicator works best when used in conjunction with other technical analysis tools rather than in isolation. The certainty/uncertainty measure provides context for your trading decisions but should not be the sole basis for entries and exits. Consider using higher certainty periods for trend-following strategies and exercise caution during periods of high uncertainty.

Rogue ORB PRORogue ORB Pro is a precision-engineered Opening Range Breakout (ORB) indicator built for active intraday traders who need real signals, not noise.

This tool identifies high-probability breakout entries from the opening range, enhanced with optional ATR-based stop loss levels, deviation targets, cooldown filters, and a relative volume gate to filter weak setups.

🔍 Key Features:

Opening Range High/Low: Drawn from a user-defined time window and locked for the day

Deviations: Automatically plots target zones above and below the OR range (e.g. 1, 2 deviations)

Pre-Market Levels: Automatically draws pre market high and low lines at the end of pre market session

Buy/Sell Signals: Triggered on breakout of the OR High/Low with configurable breakout logic (touch or close)

ATR Stop Loss Line: Dynamically drawn at a fixed ATR distance from breakout candle, with optional SL label

Cooldown Period: Prevents back-to-back signals by enforcing a user-defined bar delay between entries, can help with overtrading

Volume Filter: Optional relative volume filter that requires breakout candles to exceed a custom volume threshold

VWAP Overlay: Visual VWAP for directional bias and confluence

FSH ATR MTF MonitorThe FSH ATR MTF Monitor tracks the Average True Range (ATR) and current range across six customizable timeframes, displaying the results in a table. When a timeframe’s range exceeds its ATR, the range value turns yellow, signaling heightened volatility. This multi-timeframe tool helps traders assess market conditions and plan entries or exits.

Key Features:

- Monitors ATR and range for up to six timeframes simultaneously.

- Customizable ATR length and timeframe inputs.

- Highlights ranges exceeding ATR in yellow for quick identification.

- Table display with toggle option for flexibility.

How to Use:

1. Add the indicator to your chart.

2. Adjust the ATR length and timeframes in the inputs as needed.

3. Watch for yellow range values to spot volatility spikes across timeframes.

4. Toggle the table off if not needed.

Ideal for scalpers, swing traders, or anyone analyzing volatility across multiple timeframes.

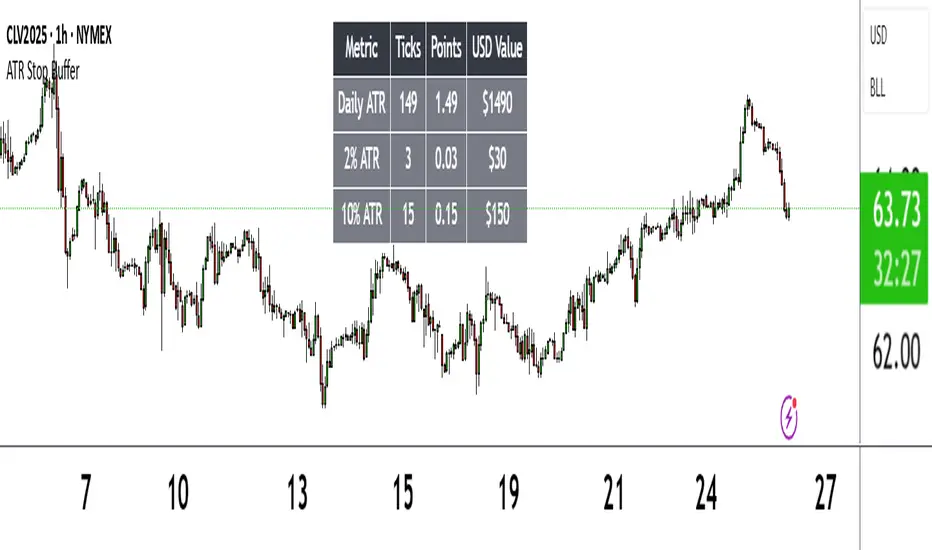

ATR Stop BufferThe ATR Stop Buffer indicator calculates the Daily Average True Range (ATR) and converts it into ticks based on the symbol's minimum price movement. It then displays the full ATR, 2% of ATR, and 10% of ATR in a clean table format, rounded up for simplicity. This tool is ideal for traders who want to set volatility-based stop-loss levels or buffers for their trades.

Key Features:

- Uses a 14-period Daily ATR for robust volatility measurement.

- Converts ATR into ticks for precise application across different instruments.

- Table display with toggle option for flexibility.

- Perfect for risk management and trade planning.

How to Use:

1. Add the indicator to your chart.

2. Use the table values to adjust your stop-loss distances (e.g., 2% ATR for tight stops, 10% ATR for wider buffers).

3. Toggle the table off if you only need the values occasionally.

Note: Works best on instruments with defined tick sizes (e.g., futures, forex, stocks).

Adaptive Fibonacci Pullback System -FibonacciFluxAdaptive Fibonacci Pullback System (AFPS) - FibonacciFlux

This work is licensed under a Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA 4.0). Original concepts by FibonacciFlux.

Abstract

The Adaptive Fibonacci Pullback System (AFPS) presents a sophisticated, institutional-grade algorithmic strategy engineered for high-probability trend pullback entries. Developed by FibonacciFlux, AFPS uniquely integrates a proprietary Multi-Fibonacci Supertrend engine (0.618, 1.618, 2.618 ratios) for harmonic volatility assessment, an Adaptive Moving Average (AMA) Channel providing dynamic market context, and a synergistic Multi-Timeframe (MTF) filter suite (RSI, MACD, Volume). This strategy transcends simple indicator combinations through its strict, multi-stage confluence validation logic. Historical simulations suggest that specific MTF filter configurations can yield exceptional performance metrics, potentially achieving Profit Factors exceeding 2.6 , indicative of institutional-level potential, while maintaining controlled risk under realistic trading parameters (managed equity risk, commission, slippage).

4 hourly MTF filtering

1. Introduction: Elevating Pullback Trading with Adaptive Confluence

Traditional pullback strategies often struggle with noise, false signals, and adapting to changing market dynamics. AFPS addresses these challenges by introducing a novel framework grounded in Fibonacci principles and adaptive logic. Instead of relying on static levels or single confirmations, AFPS seeks high-probability pullback entries within established trends by validating signals through a rigorous confluence of:

Harmonic Volatility Context: Understanding the trend's stability and potential turning points using the unique Multi-Fibonacci Supertrend.

Adaptive Market Structure: Assessing the prevailing trend regime via the AMA Channel.

Multi-Dimensional Confirmation: Filtering signals with lower-timeframe Momentum (RSI), Trend Alignment (MACD), and Market Conviction (Volume) using the MTF suite.

The objective is to achieve superior signal quality and adaptability, moving beyond conventional pullback methodologies.

2. Core Methodology: Synergistic Integration

AFPS's effectiveness stems from the engineered synergy between its core components:

2.1. Multi-Fibonacci Supertrend Engine: Utilizes specific Fibonacci ratios (0.618, 1.618, 2.618) applied to ATR, creating a multi-layered volatility envelope potentially resonant with market harmonics. The averaged and EMA-smoothed result (`smoothed_supertrend`) provides a robust, dynamic trend baseline and context filter.

// Key Components: Multi-Fibonacci Supertrend & Smoothing

average_supertrend = (supertrend1 + supertrend2 + supertrend3) / 3

smoothed_supertrend = ta.ema(average_supertrend, st_smooth_length)

2.2. Adaptive Moving Average (AMA) Channel: Provides dynamic market context. The `ama_midline` serves as a key filter in the entry logic, confirming the broader trend bias relative to adaptive price action. Extended Fibonacci levels derived from the channel width offer potential dynamic S/R zones.

// Key Component: AMA Midline

ama_midline = (ama_high_band + ama_low_band) / 2

2.3. Multi-Timeframe (MTF) Filter Suite: An optional but powerful validation layer (RSI, MACD, Volume) assessed on a lower timeframe. Acts as a **validation cascade** – signals must pass all enabled filters simultaneously.

2.4. High-Confluence Entry Logic: The core innovation. A pullback entry requires a specific sequence and validation:

Price interaction with `average_supertrend` and recovery above/below `smoothed_supertrend`.

Price confirmation relative to the `ama_midline`.

Simultaneous validation by all enabled MTF filters.

// Simplified Long Entry Logic Example (incorporates key elements)

long_entry_condition = enable_long_positions and

(low < average_supertrend and close > smoothed_supertrend) and // Pullback & Recovery

(close > ama_midline and close > ama_midline) and // AMA Confirmation

(rsi_filter_long_ok and macd_filter_long_ok and volume_filter_ok) // MTF Validation

This strict, multi-stage confluence significantly elevates signal quality compared to simpler pullback approaches.

1hourly filtering

3. Realistic Implementation and Performance Potential

AFPS is designed for practical application, incorporating realistic defaults and highlighting performance potential with crucial context:

3.1. Realistic Default Strategy Settings:

The script includes responsible default parameters:

strategy('Adaptive Fibonacci Pullback System - FibonacciFlux', shorttitle = "AFPS", ...,

initial_capital = 10000, // Accessible capital

default_qty_type = strategy.percent_of_equity, // Equity-based risk

default_qty_value = 4, // Default 4% equity risk per initial trade

commission_type = strategy.commission.percent,

commission_value = 0.03, // Realistic commission

slippage = 2, // Realistic slippage

pyramiding = 2 // Limited pyramiding allowed

)

Note: The default 4% risk (`default_qty_value = 4`) requires careful user assessment and adjustment based on individual risk tolerance.

3.2. Historical Performance Insights & Institutional Potential:

Backtesting provides insights into historical behavior under specific conditions (always specify Asset/Timeframe/Dates when sharing results):

Default Performance Example: With defaults, historical tests might show characteristics like Overall PF ~1.38, Max DD ~1.16%, with potential Long/Short performance variance (e.g., Long PF 1.6+, Short PF < 1).

Optimized MTF Filter Performance: Crucially, historical simulations demonstrate that meticulous configuration of the MTF filters (particularly RSI and potentially others depending on market) can significantly enhance performance. Under specific, optimized MTF filter settings combined with appropriate risk management (e.g., 7.5% risk), historical tests have indicated the potential to achieve **Profit Factors exceeding 2.6**, alongside controlled drawdowns (e.g., ~1.32%). This level of performance, if consistently achievable (which requires ongoing adaptation), aligns with metrics often sought in institutional trading environments.

Disclaimer Reminder: These results are strictly historical simulations. Past performance does not guarantee future results. Achieving high performance requires careful parameter tuning, adaptation to changing markets, and robust risk management.

3.3. Emphasizing Risk Management:

Effective use of AFPS mandates active risk management. Utilize the built-in Stop Loss, Take Profit, and Trailing Stop features. The `pyramiding = 2` setting requires particularly diligent oversight. Do not rely solely on default settings.

4. Conclusion: Advancing Trend Pullback Strategies

The Adaptive Fibonacci Pullback System (AFPS) offers a sophisticated, theoretically grounded, and highly adaptable framework for identifying and executing high-probability trend pullback trades. Its unique blend of Fibonacci resonance, adaptive context, and multi-dimensional MTF filtering represents a significant advancement over conventional methods. While requiring thoughtful implementation and risk management, AFPS provides discerning traders with a powerful tool potentially capable of achieving institutional-level performance characteristics under optimized conditions.

Acknowledgments

Developed by FibonacciFlux. Inspired by principles of Fibonacci analysis, adaptive averaging, and multi-timeframe confirmation techniques explored within the trading community.

Disclaimer

Trading involves substantial risk. AFPS is an analytical tool, not a guarantee of profit. Past performance is not indicative of future results. Market conditions change. Users are solely responsible for their decisions and risk management. Thorough testing is essential. Deploy at your own considered risk.