Bender Filtered MA Cloud with Buy Sell SignalsBender MA Cloud is a powerful indicator that uses two moving averages filtered by standard deviation to create a "cloud" on the chart. The upper and lower bounds of the cloud could be key levels of support and resistance, and the indicator plots lines on the chart that reflects the average price of the stock over a specified period of time. The standard deviation is used to filter out noise and identify significant trends. Bender MA Cloud also generates signals based on the direction changes of the fast moving average, crosses of the cloud, and breaches of the cloud boundaries. This indicator is a useful tool for traders who want to make informed decisions based on reliable market trends and anticipate potential trade opportunities. (Video Demo Coming Soon)

Configurable Indicator Signals

Signal on :

Pullbacks

A pullback begins when the fast MA1 line changes direction and moves opposite to the cloud. The pullback is confirmed when the fast MA1 line returns to the direction of the cloud on the close of the bar. These signals can be fine-tuned using the invalidation settings below.

Breaches

A breach is signaled when the price closes beyond the slow MA2 line in the opposite direction of the cloud. These signals can be optimized using the invalidation settings.

Crosses

A cross is signaled by a change in the direction of the cloud. The strength of the cross can be evaluated using the settings below..

Signal Filters

Confirmed pullbacks allowed after a cross

The number of confirmed pullbacks allowed after a cross can be set using this option. If the number of confirmed pullbacks since the last cross exceeds the specified value, the pullback signal will be invalidated.

Allowed Number of bars in Pullback

The pullback signal is considered invalid if the specified number of bars form within the pullback without a reversal occurring. This limits the number of bars allowed in the pullback.

Invalidate Pullback if price breaches the slow MA2

The pullback signal is considered invalid if the price crosses the slow MA2 during the pullback. This indicates that the trend may be reversing and the signal is no longer reliable.

Require Strong Cloud During Pullback

This option allows you to invalidate the pullback signal if the cloud is not considered strong using the ATR strength threshold. This can help to ensure that the signal is reliable and accurate..

Require Strong Cross. _ look-back bars.

This option allows you to invalidate the cross signal if the cloud is not considered strong over a specified number of look-back bars. The strength of the cloud is measured using the ATR strength threshold, and the signal will be invalidated if the cloud is not considered strong. This can help to ensure that the signal is reliable and accurate..

Strength Threshold ATR Length

This option allows you to specify the ATR length that should be used to gauge the strength of the cloud. Keep in mind that the ATR is a dynamic measure, so if there is a spike in the ATR, the cloud strength calculations will also change. This can affect the reliability and accuracy of the signals generated by the indicator.

Cloud Size Must Be _ times the size of the Threshold ATR to be considered strong

This option allows you to specify the minimum size that the cloud must be relative to the Threshold ATR in order to be considered strong. If the distance between the fast MA1 and the slow MA2 is less than the specified value multiplied by the Threshold ATR, the cloud is considered weak. For example, if the cloud size is not at least 2 times the ATR, it will be considered weak.

This indicator is also incorporated into the Bender Bot strategy script and can be used to autonomously manage strategies based on signals and confluences identified by the indicator. When used as a standalone indicator, the features below will not affect the indicators functionality.

Bender Bot Strategy Confluence

Require Signal Confluence before opening any position

This option requires that all of the signal conditions are met before opening any position. If all conditions are satisfied, the signal will remain "Long" or "Short" until it is invalidated.

Require MA Cloud Directional Confluence before opening any position

This option requires that the direction of the cloud (either "Long" or "Short") is in agreement before opening any position. The direction of the cloud changes on crosses.

Close Position if Pullback is started

This option closes the position if a pullback is started and causes the fast MA1 line to change direction and oppose the open position.

Please feel free to contact me if there are any questions

Wyszukaj w skryptach "bot"

Bender Money Flow Index MTF with Buy & Sell SignalsMFI = Money Flow Index

MTF = Multi Timeframe

The Money Flow Index (MFI) is a technical indicator that can generate sentiment insight or pressure using both price and volume data.

Configurable Indicator Signals

Signal on MFI line directional changes

Invalidate Signal if not in a overbought or oversold pressure zone

Invalidate signal if MFI line is not in confluence with the moving average

Invalidate signal after a defined number of bars in the opposing direction

Please Note:

This indicator is also embedded in the Bender Bot strategy script. Signals and confluence identified by this indicator can be used to autonomously mange strategies. The below features will not have any effect on this indicator's functionality when used as a stand alone indicator.

Bender Bot Strategy Confluence

Require any signal and MFI directional confluence before opening any trade

Require any signal and MFI and Moving average to be in confluence before opening any trade

Require any signal to be in directional confluence with the full MFI signal

Please feel free to contact me with any questions or concerns.

[ADOL_]EasyTradingENG) EasyTrading Indicator(ET)

Introduce)

This is the result of long research and trial and error. This indicator is an indicator that marks the signal on the chart.

Short-term, mid-term, and long-term points are analyzed, and signals leading to long-term trends are marked with a background color.

Indicates oversold and overbought, and modified Ichimoku equilibrium. Indicates the criteria for the new TD.

It is the latest version of the signal indicator that complements the limitations of existing indicators.

Noise cancellation is the key to overcoming limitations.

Alerts are included in the signal notation, allowing integration with bots that utilize alerts.

So that even beginners can use it easily, we exclude miscellaneous functions and focus only on whether it is long or short.

principle)

Principle of Moving Average: Various moving averages (SMA, EMA, WMA, HMA, RMA, SWMA, VWMA) can be used. Simply using only moving averages cannot overcome the existing problems.

The problems that arise from existing signal indicators include structural problems in which entry and exit do not appear properly due to lagging and delay of indicators, and frequent overuse of RBIs.

In order to compensate for these limitations, BNF's disparate rate trading method was referred to. I did not use the existing moving average as it is, but I optimized the formula by reflecting my experience, so the existing moving average

It is characterized by the fact that it cannot be implemented according to the signal of the indicator.

The principle of oversold and overbought: implemented using RSI.

Short-term signal: The principle of the TD indicator has been utilized and modified. The setup principle of the TD indicator,

which compares the current candlestick and the four previous candlesticks and indicates numbers from 1 to 9, was modified by applying it to the moving average.

Intermediate Signal: Moving averages and Ichimoku balance have been modified. We applied the breakthrough of clouds (positive and negative) created in Ichimok balance.

Long-term signal: The principle of moving averages was used.

comparison with existing indicators)

Compared to Supertrends:

The top is the ET indicator, and the bottom is the supertrend indicator. Supertrend is set to 14,3, which is commonly used.

Looking at the background color representing the long-term signal of ET while the super trend repeatedly displays buy and sell and sees loss of intervals

ET does not see section loss as no signal appears in the middle after one entry.

The same goes for other sports.

Compared to the moving average (sma):

Even when compared to the golden cross and dead cross conditions that break through the moving average line, the moving average line accumulates losses due to frequent entries and exits in the section that moves sideways.

ET, which compensates for the limitations, continues the trend without noise.

Comparison with Ichimoku:

ET has less noise than entering a trade using Ichimoku's red cloud and green cloud.

Necessity)

In order to work with the bot, the key is to accurately implement the hitting point and remove noise. It is a basic approach to trading even if it is not linked to a bot.

In the setting of most indicators, if you increase the period, you can see the long-term trend, but the entry point is delayed, and if you decrease the period, the entry point becomes frequent and enters a place where you shouldn't enter.

ET catches the entry point and noise removal, and helps you approach the entry point correctly even if you don't trade often.

Catching the two rabbits was the most difficult. how many years...

chart)

Notation of background color:

Long-term signals are displayed in the background color so that trends can be grasped at a glance.

Long term signal:

It is indicated by an arrow on the chart.

Mid term signal:

The decline is indicated by a black gradient on the candle and a red circle above the candle.

The rise is indicated by a white gradient on the candle and a green circle below the candle.

short-term signal:

On the chart, the candlesticks are numbered from 1 to 9.

Oversold/Overbought:

Oversold conditions are indicated by yellow diamonds (◆).

Overbought is indicated by a blue diamond (◆).

Determine the TP on the first oversold or overbought bar. Split profit start.

timeframes and alerts)

It can be applied to all time frames, and the standard time at the center is 1h.

You can adjust the dot while viewing the 15-minute bar and the 1-hour bar together.

multi time frame. It is recommended to observe multiple times at the same time using the split screen.

Note)

This indicator is not a guarantee of absolute returns, and you are solely responsible for any trading decisions you make.

How to use)

It is set to be used by invited users only.

If you receive an invitation, tap Add indicator to favorites at the bottom of the indicator.

If you go to the chart screen and press the indicator at the top, there is a Favorites tab on the left tab.

Add an indicator by clicking on the indicator name in the Favorites tab (or Invite Only).

If a study error occurs when adding an indicator even though permission has been granted

You may be able to fix the problem by turning off all charts and restarting.

KOR) EasyTrading 지표(ET)

소개)

이것은 오랜 연구와 시행착오의 결과물입니다. 해당 지표는 차트에 시그널을 표기해주는 지표입니다.

단기, 중기, 장기 타점을 분석하며, 장기트렌드를 이끄는 시그널은 배경색으로 표기됩니다.

과매도와 과매수를 표시하며, 변형된 일목균형을 표시합니다. 새로운 TD의 기준을 표시합니다.

기존의 지표들이 가지는 한계를 보완한 시그널 지표의 가장 최신 버전입니다.

한계를 극복하는데는 노이즈 제거가 핵심이라고 볼 수 있습니다.

시그널 표기에는 얼러트가 포함되어, 얼러트를 활용하는 봇과 연동이 가능합니다.

초보자도 쉽게 활용할 수 있도록 잡다한 기능은 빼고, 롱이냐 숏이냐에만 집중합니다.

원리)

이동평균선의 원리 : 여러가지 이동평균선(SMA, EMA, WMA, HMA, RMA, SWMA, VWMA) 을 활용할 수 있습니다. 단순히 이동평균선만 활용하는 것으로는 기존의 문제점을 뛰어넘을 수 없습니다.

기존의 시그널 지표에서 발생하는 문제점은, 기본적으로 지표가 가지는 후행성과 지연으로 인해, 진입과 청산의 자리가 제대로 나오지 않는 구조적인 문제, 잦은 타점 남발 등이 있습니다.

이러한 한계를 보완하기 위해서 BNF의 괴리율 매매법을 참고하였습니다. 기존의 이평선을 그대로 쓰는 것이 아니라 저의 경험을 반영해 수식을 최적화하였기 때문에 기존의 이평선으로는

해당 지표의 시그널을 따라 구현할 수 없다는 것이 특징입니다.

과매도, 과매수의 원리 : RSI를 활용하여 구현하였습니다.

단기시그널 : TD 지표의 원리를 활용 및 변형하였습니다. 현재 캔들과 4개이전의 캔들을 비교해 1~9까지 숫자로 표기하는 TD 지표의 setup 원리를 이평선에 적용하여 변형하였습니다.

중기시그널 : 이평선 및 일목균형을 변형하였습니다. 일목균형에서 만들어지는 구름(양운과 음운)의 돌파를 응용하였습니다.

장기시그널 : 이평선의 원리를 활용하였습니다.

기존의 지표들과 비교)

슈퍼트렌드와 비교 :

상단은 ET지표, 하단은 슈퍼트렌드 지표입니다. 슈퍼트렌드는 일반적으로 많이 쓰는 14,3 으로 세팅하였습니다.

슈퍼트렌드가 buy와 sell을 반복적으로 띄우며 구간손실을 보는동안, ET의 장기시그널을 나타내는 배경색을 보면

ET는 한번의 진입후 중간에 시그널이 출현하지 않으면서 구간손실을 보지 않고 있습니다.

다른 종목에서도 마찬가지입니다.

이동평균선(sma)과 비교 :

이동평균선을 돌파하는 골든크로스와 데드크로스 조건과 비교해도 횡보하는 구간에서 이동평균선은 잦은 진입과 청산으로 손실을 누적하지만

한계를 보완한 ET는 노이즈 없이 추세를 이어나갑니다.

일목균형과 비교 :

일목균형의 양운과 음운을 활용하여 타점을 진입하는 것보다 노이즈가 적습니다.

필요성)

봇과 연동하기 위해서는 타점을 정확하게 구현하는 것과 노이즈의 제거가 핵심입니다. 봇과 연동하지 않더라도 매매의 기본적인 접근입니다.

대부분의 지표의 설정에서 기간을 늘리면 장기추세를 볼 수 있으나 진입점이 늦어지고, 기간을 줄이면 진입점이 잦아 들어가지 말아야 할 곳에 들어가게 됩니다.

ET는 진입점과 노이즈 제거 두마리 토끼를 잡아, 자주 매매하지 않더라도 바르게 진입점에 접근할 수 있도록 도와줍니다.

두마리 토끼를 잡는 것이 가장 어려웠습니다. 몇년의 시간..

차트로 설명)

배경색의 표기 :

장기시그널을 배경색으로 표기하여 트렌드를 한눈에 파악할 수 있도록 하였습니다.

장기시그널 :

차트상에서 화살표로 표기됩니다.

중기 시그널 :

하락은 캔들의 검정색 그라데이션과 캔들 위 빨간색 원으로 표시됩니다.

상승은 캔들의 하얀색 그라데이션과 캔들 아래 초록색 원으로 표시됩니다.

단기시그널 :

차트상에서 캔들에 1~9까지 숫자로 표시됩니다.

과매도/과매수 :

과매도는 노란색 다이아몬드(◆)로 표시됩니다.

과매수는 파란색 다이아몬드(◆)로 표시됩니다.

과매도, 과매수가 처음 발생하는 봉에서 TP를 결정합니다. 분할익절 시작.

타임프레임 및 얼러트)

모든 시간프레임에 적용 가능하며, 중심이 되는 기준시간은 1h 입니다.

15분봉과 1시간봉을 같이 보면서 타점을 조절할 수 있습니다.

멀티타임프레임. 화면분할을 활용하여 여러 시간을 동시에 관찰하는 것을 추천합니다.

참고사항)

해당지표는 절대수익을 보장하는 지표가 아니며, 귀하가 내리는 모든 거래 결정은 전적으로 귀하의 책임입니다.

사용방법 )

초대된 사용자만 사용할 수 있도록 설정이 되어있습니다.

초대를 받을 경우, 지표 하단의 즐겨찾기에 인디케이터 넣기를 누릅니다.

차트화면으로가서 상단에 지표를 눌러 왼쪽탭에 보면 즐겨찾기 탭이 있습니다.

즐겨찾기 탭 (또는, 인바이트 온리) 에서 지표이름을 눌러서 지표를 추가합니다.

권한이 부여됐음에도 지표추가시 study error가 발생할 경우

차트를 모두 끄고 재시작함으로써 문제점을 해결할 수 있습니다.

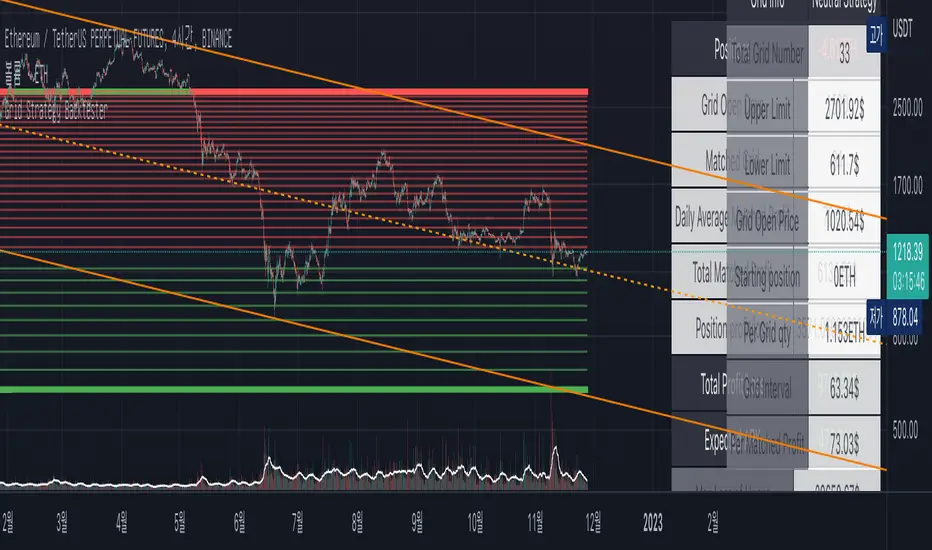

Grid Strategy Back Tester (Long/Short/Neutral)Preface

I'd like to send a thank you to @xxattaxx-DisDev.

The 'Line' Code, which was the most difficult to plan the Grid Indicator, was solved through the 'Grid Bot Simulator' script of @xxattaxx-DisDev.

A brief description of the indicators

These indicators are designed for backtesting of grid trading that can be opened on various exchanges.

Grid trading is a method of selling at particular intervals as prices rise and fall for gird interval price range.

This indicator is actually designed to see what the Long / Short / Neutral grid has achieved and how much it has achieved over a given period of time.

How to use

1. Lower Limit and Upper Limit are required when putting indicators on the chart.

After that, choose the 'Time' when to open the grid.

Also, select Long / Short / Neutral direction if necessary.

2. Statistics Table

Matched Grid shows how many grid pairs were engaged during the backtesting period.

The Daily Average Matching Profit is calculated based on the number of these closed grids.

Total Matching Profit is calculated as Matching Grid * Per Matching Profit.

Position Profit/Loss shows the benefits and losses from your current position.

Total Profit/Loss is sum of Total Matching Profit and Position Profit/Loss.

The Expanded APY shows the benefits of running the strategy on these terms for a year.

Max Loss of Upper is the maximum loss assumed to be directly at the top of the grid range.

BEP days (Upper) show how many days of maintenance relative to Average Matching Profit can result in greater profit than maximum loss if the grid continues to move within range.

(In the case of Long Strategy, it appears to be 'Min Profit', which shows minimal benefit if it reaches the top.)

Max Loss of Lower and BEP days (Lower) shows the opposite.

(In the case of Short Strategy, it is also referred to as 'Min Profit', which shows minimal benefit if it reaches the bottom.)

3. Grid Info

Total Grid Number, Upper Limit, and Lower Limit show the values you set in INPUT.

Grid Open Price shows the price for the period you decide to open.

Starting Position shows the number of positions that were initially held in the case of a Long / Short Strategy.

(0 for Neutral Strategy)

Per Grid qty shows how many positions are allocated to one grid

Grid Interval shows the spacing of each grid.

Per Matched Profit shows how much profit is generated when a single grid is matched.

Caution

Backtesting results for these indicators may vary depending on the time frame.

Therefore, I recommend that you use it only to compare Profit/Loss over time.

*In addition, there is a problem that all lines in the grid are not implemented, but it is independent of the backtest results.

--------------------------------------

서문

지표를 기획함에 있어서 가장 어려웠던 line 코드를 @xxattaxx-DisDev의 'Grid Bot Simulator' 스크립트를 통해 해결할 수 있었습니다.

이에 감사의 말씀을 드립니다.

해당 지표에 대한 간단한 설명

해당 지표는 다양한 거래소에서 오픈할 수 있는 그리드 매매에 대한 백테스팅을 위해 만들어졌습니다.

그리드매매는, 특정 가격 구간에 대해 가격이 오르고 내림에 따라 일정 간격에 맞춰 매매를 하는 방식입니다.

이 지표는 실질적으로 롱/숏/중립 그리드가 어떠한 성과를, 특정 기간동안 얼마나 냈는지를 확인하고자 만들어졌습니다.

사용방법

1. 인풋

지표를 차트위에 넣을 때, Lower Limit과 Upper Limit이 필요합니다.

그 후 그리드를 언제부터 오픈할 것인지를 선택하세요.

또, 필요하다면 Long / Short / Neutral의 방향을 선택하세요.

2. 그리드 통계

Matched Grid는, 백테스팅 기간동안 체결된 그리드 쌍이 몇개인지를 보여줍니다.

이 체결된 그리드의 갯수를 바탕으로 Daily Average Matched Profit이 계산됩니다.

Total Matched Profit은, Matched Grid * Per Matched Profit으로 계산됩니다.

Position Profit/Loss는, 현재 갖고 있는 포지션으로 인한 이익과 손실을 보여줍니다.

Total Matched Profit과 Position Profit/Loss를 합친 금액이 Total Profit/Loss가 됩니다.

Expcted APY는, 이러한 조건으로 전략을 1년동안 운영했을 때의 이익을 보여줍니다.

Max Loss of Upper는, 그리드 범위의 최상단에 바로 도달했을 경우를 가정한 최대 손실입니다.

BEP days(Upper)는, 그리드가 범위 내에서 계속 움직일 경우, Average Matched Profit을 기준으로 며칠동안 유지되어야 최대손실보다 더 큰 이익이 발생할 수 있는지를 보여줍니다.

(Long Strategy의 경우, ‘Min Profit’이라고 나타나는데, 최상단에 도달했을 경우 최소한의 이익을 보여줍니다)

Max Loss of Lower는 그 반대의 경우를 보여줍니다.

(Short Strategy의 경우, 역시 ‘Min Profit’이라고 나타나는데, 최하단에 도착했을 경우 최소한의 이익을 보여줍니다)

3. 그리드 정보

그리드 갯수, Upper Limt, Lower Limt은 자신이 설정한 값을 보여줍니다.

Grid Open Price는, 자신이 오픈하기로 정했던 기간의 가격을 보여줍니다.

Starting Position은, 롱/숏 그리드의 경우에 처음에 들고 시작했던 포지션의 갯수를 보여줍니다.

Neutral Strategy의 경우 0입니다.

Per Grid qty는, 하나의 그리드에 얼마만큼의 포지션이 배분되었는지를 보여주며

Grid Interval은 각 그리드의 간격을 보여줍니다.

또, Per Matched Profit은 하나의 그리드가 체결될 때 얼마만큼의 이익이 발생하는 지를 보여줍니다.

이러한 지표에 대한 역테스트 결과는 시간 프레임에 따라 달라질 수 있습니다.

따라서 시간 경과에 따른 손익을 비교할 때만 사용하는 것이 좋습니다.

*추가로, 그리드의 라인이 모두 구현되지 않는 문제가 있지만, 백테스팅 결과와는 무관합니다.

ATR Trend Run - Signals Alerts SL and TP by Tech Store OnThe script uses several ATR formulas for entering/exiting trades, support/resistance lines to take TP1 (take profit 1) and another ATR formula for TP2 (take profit 2). Everything is fully configurable to your preference, and you can back-test it via TradingView. You can also configure the indicator for signals during US trading sessions (with or without power hour), as well as taking profits/stop-loss session time(s), as well as to close a position at the end of the trading session no matter what. Also, you can turn all of that off, so there are no trading session/end of day limits and each trade will run until it either hits SL, TP1, TP1 > back to entry, TP2. Note: indicator is set to skip consecutive/opposite signals, while you currently have a trade open > if you hit a trend – ride it to the end!

For example: If you will be day trading SPY and you wish to close your positions no matter what right before the market closes (3:45PM ET > 15min before closes): Make sure to checkbox “Intraday – Close Position Before Market Closes” in the strategy/indicator Settings, so that you are alerted soon before the market closes, if you wish to continue holding the position – leave this checkbox unchecked.

SL: SL is set to be slightly above/below the signal candle, which is best suited for this strategy.

Strategy Take Profit Approach

While the initial position open and SL hit is always based on a closed candle bar (can’t do otherwise, as otherwise you will have 10s of fake signal alerts), there are 2 ways on trading this strategy in terms of TP1 and TP1 taken > back to Entry, which is based off Alert type.

You can switch this as you like within the indicator settings, “Checked: TP1 taken > back to Entry per Price Touch | Unchecked: per Candle Close”.

Candle Close vs Price Touch: with the Default method - Candle Close for an alert for TP1 or if price comes back to Entry after TP1 is taken will only be triggered once candle bar fully closes crossing the area, while Price Touch will alert when price touches the area before candle bar closes.

For example: your trade is running well, you grab TP1 and the price reverses and hits your trade Entry area. With Price Touch – you are immediately alerted to close your trade with no loss and with TP1 profit. With Candle Close - you will receive an alert only once candle bar fully closes on top of the Entry crossing it backwards, meaning it may lower your TP1 profit or even completely reverse the trade into loss in case it will be a huge candle bar for any reason. However, it may touch the Entry area, looking like the price is reversing, but then continue per initial trade direction, sometimes becoming a trend. So, while Price Touch seem like a more conservative approach, Candle Close can give you much bigger profits if you catch a trend, but you can always change it via the Settings.

Note: TradingView back-testing engine does not have a feature to open/close orders IMMEDIATELY via Price Touch trigger, but only when the candle closes after price touches the scripted area/line/etc., so you for the most accurate results, test your strategy out via Candle Close setting. Otherwise, decide yourself. I personally like more Candle Close since I can test it out via back-testing with the most accurate results.

TP2 is set per Candle Close as often the ATR trailing stop line will be hit and bounced off, so it’s best to wait until candle actually breaks it/closes through it.

Note: If you will be observing the strategy LIVE, during LIVE candle bar movement – it will look weird, like it’s placing an order after order during any trigger – this seem like a TradingView bug, but is only observational, once the candle bar is closed and you refresh TradingView it will all look correct.

Back-Testing

If you wish to do some back-testing, just modify the strategy/indicator Settings:

-----1) STRATEGY: This is for back-testing/experimenting with the script inputs.

----------a. You can setup a start date (date, month, year) from which it will start opening back-test trades, select a position size and select TP1 size, the idea here is to close half (or whatever you choose) portion of the trade once you hit your TP1, then to either close at small profit or to catch a trend and close the second portion of the position long way ahead from Entry, otherwise it will alert you to close the position at TP2, if price comes back to Entry, at reversal signal or at the end of US trading session if the option for it is checked. If you wish to close the whole position at TP1, just enter the same amount for TP1 to match backtest position size. Otherwise you can experiment with TP1 sizing – try it out!

-----2) Feel free to experiment with ATR settings and with S&R Left/Right bars, you may be amazed how results will differ and find some really cool combinations!

-----3) Make sure you select/de-select “Intraday – Close Position Before Market Closes” setting depending on what you are back-testing and on which conditions

-----4) Note: If you wish to do some deep back-testing (1+ years), use the “Deep Backtesting” feature within Strategy Tester on the TradingView as otherwise it may show wrong results or even fail to compute the results

Add the alerts

-----Right-click anywhere on the TradingView chart

-----Click on Add alert

-----Condition: ATR Trend Run - Signals Alerts SL and TP, by Tech Store On

----------o Right underneath the condition click on the drop-down menu and select “alert() function calls only”

-----Expiration time: Whatever you wish

-----Alert actions: Whatever notifications you wish

-----Alert name: DO NOT TOUCH THIS

-----Hit “Create”

-----Note: If you change ANY Settings within the indicator – you must DELETE the current alert and create a new one per steps above, otherwise it will continue triggering alerts per old Settings!

- Note: If you add the alert while the script is currently “In Position” it will not know that. So either wait when there will be no position open at all or close your position partially if the bot opens it twice bigger or so in case per script the bot will think it is already in position.

Note: Because of the slippage and the order processing time between TradingView, AutoView and the Broker (it’s usually about a second or so), it is suggested to not use a timeframe lower than 1min. The script is working really well with 1M/3M/5M/H1/H4 timeframes per my back-testing, but feel free to explore via Strategy Back-testing what’s best for the instrument you wish to trade.

If you wish to try this out for a week or so – please reach out and I will give you access.

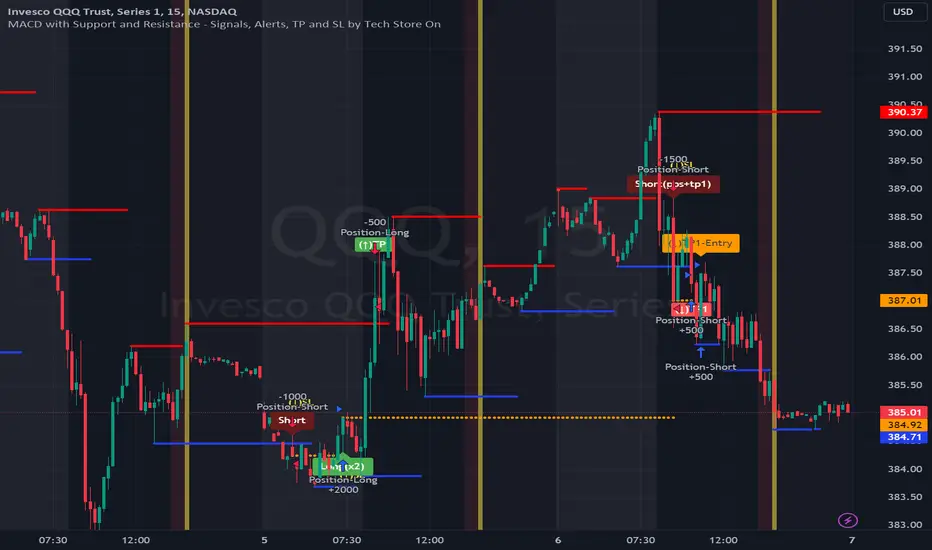

MACD with Support and Resistance - Signals, Alerts, TP and SLMACD with Support and Resistance - Signals Alerts SL and TP by Tech Store On

The script uses MACD for entering/exiting trades and support/resistance lines to take TP1 (take profit 1). Both MACD and support/resistance lines are fully configurable to your preference, and you can back-test it via TradingView. Once TP1 is taken, you can either set the indicator to close the trade at the end of the US trading session day (4PM ET) or you can continue taking partial profits where you wish or just wait until reversal signal alert.

For example: If you will be day trading SPY and you wish to close your positions no matter what right before the market closes (3:45PM ET > 15min before closes): Make sure to checkbox “Intraday – Close Position Before Market Closes” in the strategy/indicator Settings, so that you are alerted soon before the market closes, if you wish to continue holding the position – leave this checkbox unchecked.

SL: SL is set to be slightly above/below the MACD signal candle, which is best suited for this strategy from manual backtesting.

Strategy Take Profit Approach

While the initial position open and SL hit is always based on a closed candle bar (can’t do otherwise, as otherwise you will have 10s of fake signal alerts), there are 2 ways on trading this strategy in terms of TP1 / TP1 taken > back to Entry, which is based off Alert type.

You can switch this as you like within the indicator settings, “Checked: TP1/TP1 taken > back to Entry per Price Touch | Unchecked: per Candle Close”.

Candle Close vs Price Touch: with the Default method - Candle Close for an alert for TP1 or if price comes back to Entry after TP1 is taken will only be triggered once candle bar fully closes crossing the area, while Price Touch will alert when price touches the area before candle bar closes.

For example: your trade is running well, you grab TP1 and the price reverses and hits your trade Entry area. With Price Touch – you are immediately alerted to close your trade with no loss and with TP1 profit. With Candle Close - you will receive an alert only once candle bar fully closes on top of the Entry crossing it backwards, meaning it may lower your TP1 profit or even completely reverse the trade into loss in case it will be a huge candle bar for any reason. However, it may touch the Entry area, looking like the price is reversing, but then continue per initial trade direction, sometimes becoming a trend. So, while Price Touch seem like a more conservative approach, Candle Close can give you much bigger profits if you catch a trend, but you can always change it via the Settings.

Note: TradingView back-testing engine does not have a feature to open/close orders IMMEDIATELY via Price Touch trigger, but only when the candle closes after price touches the scripted area/line/etc., so you for the most accurate results, test your strategy out via Candle Close setting. Otherwise, decide yourself. I personally like more Candle Close since I can test it out via back-testing with the most accurate results.

Note: If you will be observing the strategy LIVE, during LIVE candle bar movement – it will look weird, like it’s placing an order after order during any trigger – this seem like a TradingView bug, but is only observational, once the candle bar is closed and you refresh TradingView it will all look correct.

Back-Testing

If you wish to do some back-testing, just modify the strategy/indicator Settings:

-----1) STRATEGY: This is for back-testing/experimenting with the script inputs.

----------a. You can setup a start date (date, month, year) from which it will start opening back-test trades, select a position size and select TP1 size, the idea here is to close half (or whatever you choose) portion of the trade once you hit your TP1, then to either close at small profit or to catch a trend and close the second portion of the position long way ahead from Entry, otherwise it will alert you to close the position if price comes back to Entry, at reversal signal or at the end of US trading session if the option for it is checked. If you wish to close the whole position at TP1, just enter the same amount for TP1 to match backtest position size. Otherwise you can experiment with TP1 sizing – try it out!

-----2) Feel free to experiment with MACD settings and with S&R Left/Right bars, you may be amazed how results will differ and find some really cool combinations!

-----3) Make sure you select/de-select “Intraday – Close Position Before Market Closes” setting depending on what you are back-testing and on which conditions

-----4) Note: If you wish to do some deep back-testing (1+ years), use the “Deep Backtesting” feature within Strategy Tester on the TradingView as otherwise it may show wrong results or even fail to compute the results

Add the alerts

-----Right-click anywhere on the TradingView chart

-----Click on Add alert

-----Condition: MACD with Support and Resistance - Signals

----------o Right underneath the condition click on the drop-down menu and select “alert() function calls only”

-----Expiration time: Whatever you wish

-----Alert actions: Whatever notifications you wish

-----Alert name: DO NOT TOUCH THIS

-----Hit “Create”

-----Note: If you change ANY Settings within the indicator – you must DELETE the current alert and create a new one per steps above, otherwise it will continue triggering alerts per old Settings!

- Note: If you add the alert while the script is currently “In Position” it will not know that. So either wait when there will be no position open at all or close your position partially if the bot opens it twice bigger or so in case per script the bot will think it is already in position.

Note: Because of the slippage and the order processing time between TradingView, AutoView and the Broker (it’s usually about a second or so), it is suggested to not use a timeframe lower than 1min. The script is working really well with 15M/H1 timeframes per my back-testing, but feel free to explore via Strategy Back-testing what’s best for the instrument you wish to trade.

PineHelperLibrary "PineHelper"

This library provides various functions to reduce your time.

recent_opentrade_entry_bar_index()

get a recent opentrade entry bar_index

Returns: (int) bar_index

recent_closedtrade_entry_bar_index()

get a recent closedtrade entry bar_index

Returns: (int) bar_index

recent_closedtrade_exit_bar_index()

get a recent closedtrade exit bar_index

Returns: (int) bar_index

all_opnetrades_roi()

get all aopentrades roi

Returns: (float) roi

bars_since_recent_opentrade_entry()

get bars since recent opentrade entry

Returns: (int) number of bars

bars_since_recent_closedtrade_entry()

get bars since recent closedtrade entry

Returns: (int) number of bars

bars_since_recent_closedtrade_exit()

get bars since recent closedtrade exit

Returns: (int) number of bars

recent_opentrade_entry_id()

get recent opentrade entry ID

Returns: (string) entry ID

recent_closedtrade_entry_id()

get recent closedtrade entry ID

Returns: (string) entry ID

recent_closedtrade_exit_id()

get recent closedtrade exit ID

Returns: (string) exit ID

recent_opentrade_entry_price()

get recent opentrade entry price

Returns: (float) price

recent_closedtrade_entry_price()

get recent closedtrade entry price

Returns: (float) price

recent_closedtrade_exit_price()

get recent closedtrade exit price

Returns: (float) price

recent_opentrade_entry_time()

get recent opentrade entry time

Returns: (int) time

recent_closedtrade_entry_time()

get recent closedtrade entry time

Returns: (int) time

recent_closedtrade_exit_time()

get recent closedtrade exit time

Returns: (int) time

time_since_recent_opentrade_entry()

get time since recent opentrade entry

Returns: (int) time

time_since_recent_closedtrade_entry()

get time since recent closedtrade entry

Returns: (int) time

time_since_recent_closedtrade_exit()

get time since recent closedtrade exit

Returns: (int) time

recent_opentrade_size()

get recent opentrade size

Returns: (float) size

recent_closedtrade_size()

get recent closedtrade size

Returns: (float) size

all_opentrades_size()

get all opentrades size

Returns: (float) size

recent_opentrade_profit()

get recent opentrade profit

Returns: (float) profit

all_opentrades_profit()

get all opentrades profit

Returns: (float) profit

recent_closedtrade_profit()

get recent closedtrade profit

Returns: (float) profit

recent_opentrade_max_runup()

get recent opentrade max runup

Returns: (float) runup

recent_closedtrade_max_runup()

get recent closedtrade max runup

Returns: (float) runup

recent_opentrade_max_drawdown()

get recent opentrade maxdrawdown

Returns: (float) mdd

recent_closedtrade_max_drawdown()

get recent closedtrade maxdrawdown

Returns: (float) mdd

max_open_trades_drawdown()

get max open trades drawdown

Returns: (float) mdd

recent_opentrade_commission()

get recent opentrade commission

Returns: (float) commission

recent_closedtrade_commission()

get recent closedtrade commission

Returns: (float) commission

qty_by_percent_of_equity(percent)

get qty by percent of equtiy

Parameters:

percent : (series float) percent that you want to set

Returns: (float) quantity

qty_by_percent_of_position_size(percent)

get size by percent of position size

Parameters:

percent : (series float) percent that you want to set

Returns: (float) size

is_day_change()

get bool change of day

Returns: (bool) day is change or not

is_in_trade()

get bool using number of bars

Returns: (bool) allowedToTrade

discord_message(name, message)

get json format discord message

Parameters:

name : (string) name of bot

message : (string) message that you want to send

Returns: (string) json format string

telegram_message(chat_id, message)

get json format telegram message

Parameters:

chat_id : (string) chatId of bot

message : (string) message that you want to send

Returns: (string) json format string

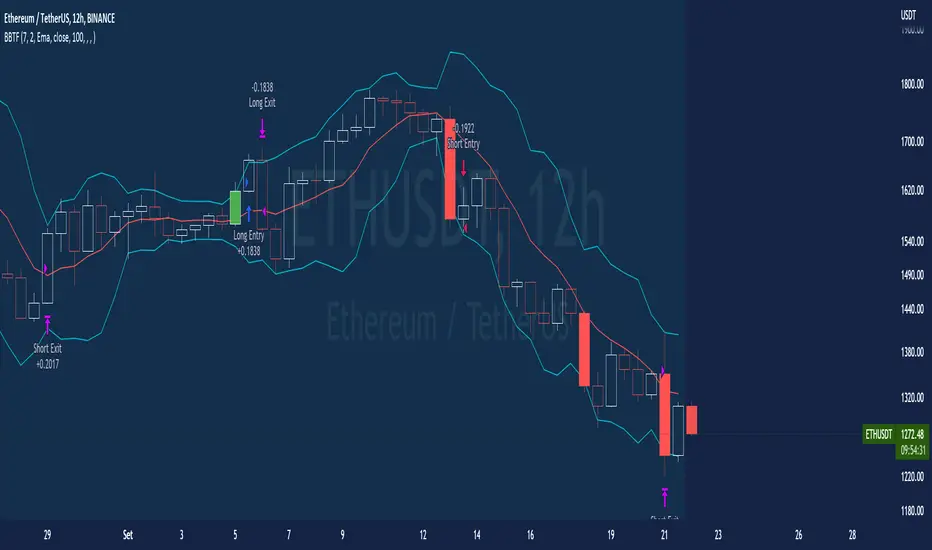

BT-Bollinger Bands - Trend FollowingEsse script foi criado para estudo de Backtest.

O script usa as Bandas de Bollinger para indicar o início de uma tendência, a entrada é configurada quando o preço abre abaixo e fecha acima da banda superior ou para venda quando o preço abre acima e fecha abaixo da banda inferior.

Não há um stop fixo e nem alvo fixo a saída se dá quando o preço toca a média da banda.

Você pode usar uma média móvel como filtro combinado com a estratégia.

O Script também pode ser usado com algum serviço de bot como 3commas.io , basta colocar as mensagens de entrada e saída para o bot.

Autor : Credsonb - Nick: M4TR1X_BR

Neste gráfico estou usando as seguintes configurações:

Bandas Bollinger: 7

Desvio Padrão: 1.5

Time Frame: 12hs

Ticker: ETH

This script was created for Backtest study.

script uses Bollinger Bands to indicate the start of a trend, entry is set when price opens below and closes above the upper band or for short when price opens above and closes below the lower band.

There is no fixed stop and no fixed target, the exit occurs when the price touches the average of the band.

You can use a moving average as a filter combined with the strategy.

The Script can also be used with some bot service like 3commas. io , just put the input and output messages to the bot.

Author : Credsonb - Nick: M4TR1X_BR

Full Volatility Statistics and Forecast

This is a tool designed to translate the data from the expected volatility of different assets, such as for example VIX, which measures the volatility of SP500 index.

Once get the data from the volatility asset we want to measure(for this test I have used VIX), we are going to translate it the required timeframe expected move by dividing the initial value into :

252 = if we want to use the daily timeframe, since there are ~252 aproximative daily trading days

52 = if we want to use the weekly timeframe, since there 52 trading weeks in a year

12 = if we want to use the monthly timeframe, since there are 12 months in a year

For this example I have used 252 with the daily timeframe.

In this scenario, we can see that we had 5711 total cnadles which we analysed, and in this case, we had 942 crosses, where the daily movement ended up either above or below the channel made from the opening daily candle value + expected movement from the volatility, giving as a total of 16.5% of occurances that volatility was higher than expected, and in 83.5% of the times, we can see that the price stayed within our channel.

At the same time, we can see that we had 6 max losses in a row ( OUT) AND 95 max wins in a row (IN), and at the same time in those moments when the volatility crosses happen we had a 0.51% avg movements when the top crossed happened, and 0.67% avg movements when the bot happened.

Lastly on the second part of the panel, we had E which means the expected movement of today, for example it has 61.056$ , so lets say price opened on 4083, our top is 4083 + 61 and our bot is 4083 - 61 ( giving us the daily channel). At continuation we can see that overall the avg bull candle os 0.714% and avg bear candle was 0.805% .

I hope this tool will help you with your future analysis and trades !

If you have any questions please let me know !

BT-SAR Ema, Squeeze, Volatility

Esse script foi criado para estudo de Backtest.

Ele usa o SAR PARABÓLICO como indicador de sinal de entrada, você também pode combinar 3 indicadores para filtrar as entradas: Média Móvel, Squeeze Momentum e Volatility Oscilator .

Existe duas entradas, quando o SAR Parabólico vira ou pelo Breakout (usando o último preço) do SAR Parabólico antes dele virar.

As Os filtros podem ser usados de forma combinada ou individual.

O Script também pode ser usado com algum serviço de bot como 3commas.io, basta colocar as mensagens de entrada e saída para o bot.

This script was created for Backtest study.

It uses PARABOLIC SAR as input signal indicator, you can also combine 3 indicators to filter inputs: Moving Average, Squeeze Momentum and Volatility Oscillator .

There are two entries, when the Parabolic SAR turns or by Breakout (using the last price) of the Parabolic SAR before it turns.

The Filters can be used in combination or individually.

The Script can also be used with some bot service like 3commas.io, just put the input and output messages to the bot.

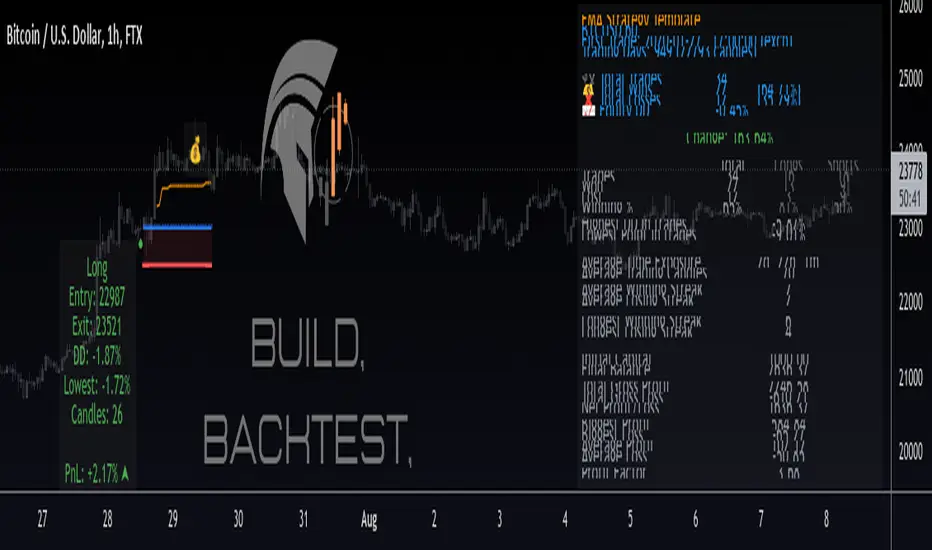

Protervus Trading ToolkitHi Traders! Welcome to Protervus Trading Toolkit (PTT) , a comprehensive set of tools to help you building, backtesting, and even automating your strategy.

Important : the data and screenshots I publish are solely for presentation and explanation purposes and must not be intended as recommendations or guarantees. Please consider eventual backtesting results seen here as almost-random. My goal is not to provide ready-made strategies, signals, or infallible methods, but rather indicators and tools to help you focus on your own research and build a reliable trading plan based on discipline.

BUILD, BACKTEST, AUTOMATE

The first step is to link a chained indicator which will send Entry signals and, optionally, Exit signals: to integrate your own triggers with this toolkit, check out my tutorial and use this code as a template.

Then, in the Trading Settings you can set the Trading Mode (Full - Long and Short, Long only, or Short only) as well as Starting Capital, Drawdown Limit, Risk per Trade, Fees, and the date range in which trading will be enabled and backtested.

Go further by tweaking your strategy with built-in Take Profit and Stop Loss conditions, and keep it under control thanks to the Statistics Panel.

Trades will be shown on the chart, including TP\SL levels (according to the ones you enable) and per-trade statistics:

Tip: point the cursor over TP or SL icon to open the tooltip, showing additional details about the trade.

BUILT-IN CONDITIONS

Note: all conditions already account for fees.

Take Profit \ Stop Loss percentage

Take Profit or Stop at Loss when a fixed percentage is reached.

Limit \ Hard Stop: the trade will be considered closed when that specific price is reached - otherwise, the candle closing price will be used.

Trailing Take Profit

Trail the price and close the trade in profit when it reverses for the chosen percentage.

Engage and Disengage: activate trailing when the price is above the entry price for the chosen percentage, and de-activate it if price goes past the disengage percentage.

Safety TP: close the trade at Break-Even if the price sharply reverses from engaged area to BE level. A specific Alert is available in order to create a separate trigger with immediate effect.

Note: using TP Safety with an Engage % of zero might result in many early exits, so it is recommended to add some margin to Engage % to avoid that.

Exit \ Stop on Opposite Signal

Close the trade when another, contrary signal is received (e.g. close a Long position when a signal to go Short is received).

Exit \ Stop after X candles

Close the trade after X candles, as soon as the condition is met (e.g. for Take Profit condition, it will close the trade after X candles as soon as the trade is in profit).

Bind to TP \ SL: only validate the condition if the current PnL is above (TakeProfit cond.) or below (Stop Loss cond.) the specified percentage.

ATR Stop

Classic ATR Stop Loss.

Trailing ATR

Chase the price by the defined ratio and close the position when the candle closes past the ATR line.

Bind to TP \ SL: only validate the condition if the current PnL is above (TakeProfit cond.) or below (Stop Loss cond.) the specified percentage.

External Signal (sent from your indicator)

Close the position basing on your own triggers, defined in the chained indicator.

- Bind to TP \ SL: only validate the condition if the current PnL is above (TakeProfit cond.) or below (Stop Loss cond.) the specified percentage.

PANEL CUSTOMIZATION AND ADDITIONAL OPTIONS

A strategy name can be assigned in the settings and will show it at the top of the Statistics Panel, so you can better identify and label your tests and live instances.

The panel can be customized in terms of colors, text size and height. It can be also "split" in modular panels that will appear at the bottom of the chart.

It is also possible to show \ hide prices and live data labels as well as position and Break-Even levels. In some cases you will need to limit the display of those plots in order to avoid PineScript calculation issues.

If you limited the plots but you are checking very old trades, you can enable the Legacy position tracker to see basic markers for positions (position is active, and profit \ loss marker).

In the case you will be sending webhook alerts to a trading bot , "Position Alert Failover" will come in aid to prevent situations where the initial trade closing alert is either not sent or missed: it will keep sending the position closing signal for X candles.

PLUGINS

Thanks to the modular nature of PTT, plugins will eventually be available to provide additional features and extend functionalities even further. Make sure to keep an eye on updates.

CREATING ALERTS

To create alerts you must first select the PTT indicator from the "Condition" drop-down menu, then the whole list of available alerts will appear. When creating alerts, please make sure to set "Once Per Bar Close" for the normal conditions, and "Once Per Bar" for safety conditions (Limit and Hard Stop simulation, Trailing TP Safety Trigger).

Besides positions opening and closing alerts, you also have the option to add extra alerts for when a position is open or not open (e.g. Active Long position, No Long Position) - that might come handy when dealing with trading bots and automation tools. Also, as mentioned earlier, you have the chance to create a special alert as failover in order to repeat the closing alert.

TIPS AND RECOMMENDATIONS

Set Visual Order > Bring to front for PTT to avoid other indicators or candles covering up labels.

If you receive errors like "Referencing too many candles" or "Too many drawings", use the " Limit to last candles " function in the Settings panel to lower the number of candles.

If the Statistics Panel or labels are not appearing, and no errors are shown (red circled exclamation mark next to indicator's name), try changing any value in the settings to trigger a new calculation.

The Lowest Point in Trades refers to the maximum movement against your position. However, if the price never goes negative against the Entry level, it will be calculated from the Break-Even level.

Differently from TradingView's Strategy Tester, PTT calculates DrawDown from the Equity line (the starting balance).

Remember that Backtests only show past results, and although very useful to understand if your strategy makes sense, the market can completely change at any moment and ruin your dreams: make sure to avoid over-fitting (using very specific values) in your settings and to prefer more generic values in order to factor broader market situations.

After many successful backtests of your newly created strategy, let it run live without actually trading it for some time (paper trading), and see if it remains valid.

You can use multiple Conditions as safeguard. For example, main Stop condition can be Trailing ATR and secondary Stop condition can be Stop Loss % with Hard Stop, so you will be protected in case of sudden big price moves.

Smart Money BusterAfter daytrading for a while i came into conclusion that price action trading is the most successful way to trade for me and this project was for me to simplify my way of trading at the beginning. Eventually it got big and turned into a very useful helper indicator for me to setup on different pairs for alerts and only look at the charts to decide for entry when the alerts come from 120 different pairs that i set it up. Since i always looked at indicators for a way to make my job simpler and give me more time to do more important things for me rather than drawing lines on different pairs eveyday i think it got to a point where it works to my liking and making me gain time, thus more money.

This indicator uses smart money concepts like Market Structure, Order Blocks, Quassimodo Levels, Structure Breaks, Pumps and Dumps, Imbalances(In the works will be added in first update) to help trader catch what the whales are thinking and how to enter in the right time for swing trading, catching bottoms and tops.

Here are some of the features as of release:

Detects Market Structure and draws zig-zag lines and keeps note of pivot points.

Detects Order blocks and draws boxes when the conditions met

Detects the quassimodo levels and changes the color of the box to signal double confluence meaning stronger signal

Draws structure break lines

Setting to set structure break percentage before drawing boxes to get the boxes drawn if you want to be more 'sure' about the Order Block Levels.

Setting to change depth and backstep values for zigzags to be able to let you fit the system for different time frames.

Setting to set MSB trigger point between High and Low, Close and Open or hl2 values.

Setting to set Signal Triggering Range between Start, Middle and End meaning eg. if you set it to Middle it will wait for MSB trigger point to hit the middle of the box before giving you a signal.

Setting for changing HH-LL pivot points lookback count, 5 as default. Increasing this value will make you compare your pivot points with more data, really useful in lower time frames where will be a lot of zig-zags and highs and lows giving you a method to avoid false signals. Recommended to keep it lower values on 30 min and higher and increase it in lower Timeframes according to market volatility.

Setting to add a Box limit where the box of order block will be set invalid after certain candles and it still didn't trigger. Default value of 0 means it's disabled.

Setting to set Candle volatility percentage value to avoid big candles getting opposite signals on fast pump or dump schemes and bust those market makers schemes. Gotta say this came out really handy in crypto markets :)

As an end you can set alerts for 'Buy' , ' Sell ', ' Buy and Sell' together or if you wish you can connect it to bots via webhook as an entry. Although haven't connected to any bots myself as i think the best method of trading is human and machine working together. Since we have the creativity and out of the box thinking and machines have the ability to brute force calculation and huge bandwith that we don't currently have. At least until Elon Musk turns is into a cyborg, which i am not very eager about.

Planned Features:

- Add ability to detect imbalances(fair value gaps) to add third confluence to detect dragon fruit entries. This will make the system work with triple confluence.

- Add more settings so humans can command the ai better.

- Maybe a strategy version after i write my own dynamic take profit algorithm to give system ability make quantitative decisions based on current position profit levels.

- Although i think i fixed almost all the important bugs if there ever comes up one bugs will take priority for updates.

- And some things i may decide to add later. I will keep working on this project since it works well for me.

And like always, happy trading.

KISS BOT (Keep It Simple BOT)A very simple script that can be used for Futures and Options Trading - for stocks, crypto, forex etc.

The script includes usage of following public scripts:

1. Super Trend

2. Linear Regression

3. Exponential Moving Average

Concept, we are using three EMA, with source High, Low, and Close. We want to buy or sell when there is a crossover of third EMA (fastest) over first and second respectively.

E.g. the default values are EMA 13 High, EMA 13 Low and EMA 5 Close, we will get Buy signal when EMA 5 crosses over EMA 13 High and we will get Sell signal when EMA 5 crosses under EMA 13 Low.

Super Trend settings are made for Looking for Buy or Looking Sell, so that we focus on the trend. Trend is your friend.

Buy Trigger Line and Sell Trigger Line are just indication of using Trigger Line, buy is when EMA 5 crosses EMA 13 Low and Sell When EMA 5 Crosses EMA 13 High

The Tunnel or Band highlighted is the no trade zone for us and we do not want to trade side ways market.

Inside Bars are shown in Yellow, these candles do not qualify for any trade decision.

Outside Bars are shown in Pink, these candles do not qualify for any trade decision

Density & Step Grid Strategies BacktesterThis contains several signals for backtesting strategies only in binance futures assets.

HOW IT WORKS

Grid trading is a trading strategy where an investor creates a so-called "price grid". The basic idea of the strategy is to repeatedly buy at the pre-specified price and then wait for the price to rise above that level and then sell the position (and vice versa with shorting or hedging). We introduce 2 grids trading algorithms "Step" and "Density" .

FEATURES

Grid size: This algorithm has a max of 20 orders.

Take profit: The trader can increase or decrease the distance between the grids from the User Interface panel, is the the distance from average price.

Management: The algorithm distributes the capital for all orders depending on the amount fator, for example 1.1% of amount factor adds 10% over the previus order.

Stop Loss: The algorithm place the stopn using distance from the last lower / upper grid depending on the position side.

USES

Indispensable research and backtesting tool for those using bots for their investments. The algorithm produces a backtesting of the strategy for past history. It is used by professional traders to understand if this strategy has been profitable on a market and what parameters to use for bots using this strategy, only binance futures assets supported.

If you would like to develop your own algorithm with customized conditions based on a grid strategy, please contact us.

If you need help in using this tool, please contact us without hesitation.

Percentage Range IndicatorThe Percentage Range Indicator is useful for assessing the volatility of pairs for percentage-based grid bots. The higher the percentage range for a given time period, the more trades a grid bot is likely to generate in that period. Conversely, a grid bot can be optimised by using grids that are less than the Percentage Range Indicator value.

I have been using the Percentage Range Indicator based on the one hour time period and 168 periods of smoothing (seven days based on one-hour periods).

Enjoy.

TTP AF Sim ProThis indicator helps you visualise, practice, manage and automatically add funds to DCA deals that are in negative.

Multiple factors factors are relevant when trying to exit a bad deal:

How much funds are invested

What's the current average position price

How far the price has already dropped from that average

Is the price bouncing significantly and frequently to the upside providing multiple opportunities to exit or is it still a free-falling knife dumping heavy?

What are your TP % expectations

This indicator allows you to enter all these parameters visualising them all together in a single chart. The chart will show you based on all this information how much funds you would have required to exit in profit and rescue the deal in green. It will also flag if the exit strategy would have failed by plotting a red label indicating all the times where the TP wouldn't have been reached.

The exit strategies

In this pro version you have access to edit all settings and the added ability to use an external indicator as source:

Custom external indicator as source

Relative Strength Index (RSI)

Commodity Channel Index (CCI)

Money Flow Index (MFI)

Bollinger Bands (BB)

Automated Add Funds-alert

With this indicator you can also add funds to the deals automatically:

Every time the conditions are true an alert is sent

Add Bot ID and Email Token for the deals

Select automatically calculated volume or your own custom

Tweak your exit strategy to your liking and add your Bot ID and Email Token to automatically add funds to your open deals.

TTP AF SimThis indicator helps you visualise, practice, manage and automatically add funds to DCA deals that are in negative.

Multiple factors factors are relevant when trying to exit a bad deal:

How much funds are invested

What's the current average position price

How far the price has already dropped from that average

Is the price bouncing significantly and frequently to the upside providing multiple opportunities to exit or is it still a free-falling knife dumping heavy?

What are your TP % expectations

This indicator allows you to enter all these parameters visualising them all together in a single chart. The chart will show you based on all this information how much funds you would have required to exit in profit and rescue the deal in green. It will also flag if the exit strategy would have failed by plotting a red label indicating all the times where the TP wouldn't have been reached.

The exit strategies

In this basic version you have access to well tested and pre-defined conditions with the following indicators:

Relative Strength Index (RSI)

Commodity Channel Index (CCI)

Money Flow Index (MFI)

Bollinger Bands (BB)

Automated Add Funds-alert

With this indicator you can also add funds to the deals automatically:

Every time the conditions are true an alert is sent

Add Bot ID and Email Token for the deals

Select automatically calculated volume or your own custom

Select exit strategy and add your Bot ID and Email Token to automatically add funds to your open deals.

3RSI 3CCI BB 5orders DCA strategy+This strategy is just an attempt to find the indicator values for the trading bot service that I use (link in profile). Due to the use of the “request.security” function in the code, the indicators can be redrawn, but this is not important in history. The strategy used only 5 orders for the "DCA" - bot, located at the same distance in the price overlap range. I only use this strategy when trading in pairs against bitcoin.

Эта стратегия – просто попытка подобрать значения индикаторов для сервиса торговых ботов, который я использую (ссылка в профиле). Из-за использования в коде функции «request.security» возможна перерисовка индикаторов, но на истории это не важно. В стратегии использовано всего 5 ордеров для «DCA» - бота, находящихся на одинаковом расстоянии в диапазоне перекрытия цены. Я использую данную стратегию только при торговле в парах к биткоину.

Premium ScalperThe strategy works with a combination of a number of different factors, including:

- Volume

- Moving averages

- Volatility

- RSI

This strategy generates long and short signals based on volume movements, moving averages and RSI. By combining other algorithms, low volatility periods can be filtered out.

The best results can be achieved by pairing the indicator with a bot through 3Commas and using a diversification strategy. This way you spread your risk over different pairs and you therefore also have a great chance of taking big moves.

The strategy results we display are results WITHOUT leverage. It is therefore also possible to only long on spot with this strategy, but for optimal results a trading bot link is required.

The settings we have used for these results are an order size of 100% with a 0.08% commission size.

Side note: This indicator does NOT use repainting!

We offer the possibility to try the indicator for free for 7 days.

Scalping Trading System ALERT Crypto and StocksThis is the alert version of the strategy with the same name.

Indicators

SImple Moving Average

Exponential Moving Average

Keltner Channels

MACD Histogram

Stochastics

Rules for entry

long= Close of the candle bigger than both moving averages and close of the candle is between the top and bot levels from Keltner . At the same time the macd histogram is negative and stochastic is below 50.

short= Close of the candle smaller than both moving averages and close of the candle is between the top and bot levels from Keltner . At the same time the macd histogram is positive and stochastic is above 50.

Rules for exit

We exit when we meet an opposite reverse order.

This strategy has no risk management inside, so use it with caution !

CDC Action Zone - 3Commas AlertCDC Action Zone, The well know indicator using EMA 12 and EMA 26.

When EMA 12 crosses EMA 26 will be a signal to trade.

You can change EMA that you want from settings.

This indicator work with 3Commas - Crypto DCA Bot . (Tradingview custom signal)

You can get a "BOT ID" and "Email token" from 3Commas when you create a bot.

Add into text box in indicator's settings.

After that create alert in Tradingview

Check webhook and using Url below for send signals to 3Commas bot.

3commas.io

This indicator will alert 40 Symbols at one time. (Tradingview set max symbols at 40)

If you want to alert more than 40 symbols, you can change symbols from settings and create new alert.

DiscordWebhookFunctionLibrary "DiscordWebhookFunction"

discordMarkdown(_str, _italic, _bold, _code, _strike, _under) Convert string to markdown formatting User can combine any function at the same time.

Parameters:

_str : String input

_italic : Italic

_bold : Bold

_code : Code markdown

_strike : Strikethrough

_under : Underline

Returns: string Markdown formatted string.

discordWebhookJSON(_username, _avatarImgUrl, _contentText, _bodyTitle, _descText, _bodyUrl, _embedCol, _timestamp, _authorName, _authorUrl, _authorIconUrl, _footerText, _footerIconUrl, _thumbImgUrl, _imageUrl) Convert data to JSON format for Discord Webhook Integration.

Parameters:

_username : Override bot (webhook) username string / name,

_avatarImgUrl : Override bot (webhook) avatar by image URL,

_contentText : Main content page message,

_bodyTitle : Custom Webhook's embed message body title,

_descText : Webhook's embed message body description,

_bodyUrl : Webhook's embed body direct link URL,

_embedCol : Webhook's embed color,

_timestamp : Timestamp,

_authorName : Webhook's embed author name / title,

_authorUrl : Webhook's embed author direct link URL,

_authorIconUrl : Webhook's embed author icon by image URL,

_footerText : Webhook's embed footer text / title,

_footerIconUrl : Webhook's embed footer icon by image URL,

_thumbImgUrl : Webhook's embed thumbnail image URL,

_imageUrl : Webhook's embed body image URL.

Returns: string Single-line JSON format

3C Sim SignalThis indicator offers the same deal start conditions available on Backtest script but now as an external signal so you can not only backtest but also set up alerts.

You can use the backtest script to backtest this indicator as an external signal and then once happy with the backtest results send directly tradingview alerts to your own bots on any exchange.

It supports most of the deal start conditions currently available for DCA bots on binance.com for example:

- TV technical ratings: buy, sell, strong buy, strong sell.

- RSI

- MFI

- CCI

- Ultimate Oscilator

- QFL

- min volume filter

Once added to the chart it will plot one when the deal start condition is true and zero when is not.

The conditions can be used in long or short strategy mode.

The biggest advantage compared to using it separately from the DSC already available in the backtest script is that because this is a separated study it will perform faster than the backtest and it resolves repainting issues. This two aspects make these indicator better suited for real time trading while still being able to connect to the backtest as an external indicator therefore still backtestable.

Now you can backtest symbols on any exchange and once your strategy is ready you then can send alerts directly to your bots.