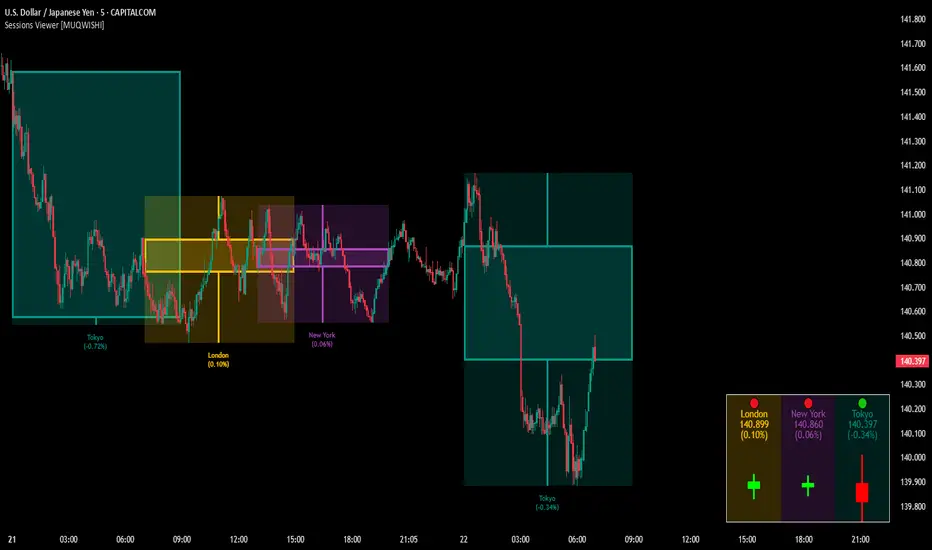

Market Sessions & Viewer Panel [By MUQWISHI]▋ INTRODUCTION :

The “Market Sessions & Viewer Panel” is a clean and intuitive visual indicator tool that highlights up to four trading sessions directly on the chart. Each session is fully customizable with its name, session time, and color. It also generates a panel that provides a quick-glance summary of each session’s candle/bar shape, helping traders gain insight into the volatility across all trading sessions.

_______________________

▋ OVERVIEW:

_______________________

▋ CREDIT:

This indicator utilizes the “ Timezone — Library ”. A huge thanks to @n00btraders for effort and well-organized work.

_______________________

▋ SESSION PANEL:

The Session Panel allows traders to visually compare session volatility using a candlestick/bar pattern.

Each bar represents the price action during a session and includes the session status, session name, closing price, change(%) from open, and a tooltip that reveals detailed OHLC and volume when hovered over.

Chart Type:

It offers two styles Bar or Candle to display based on traders’ preference

Sorting:

Allowing to arrange session candles/bars based on…

—Left to Right: The most recently opened on the left, moving backward in time to the right.

—Right to Left: The most recently opened on the right, moving backward in time to the left.

—Default: Arrange sessions in the user-defined input order.

_______________________

▋ CHART VISUALIZATION:

The chart visualization highlights each trading session using color-coded backgrounds in two selectable drawing styles that span their respective active timeframes. Each session block provides session’s name, close price, and change from open.

Chart Type: Candle

Chart Type: Box

Extra Drawing Feature:

This feature may not exist in other indicators within the same category, it extends the session block drawing to the projected end of the session. This's done through estimation based on historical data; however, it doesn’t function fully on seconds-based timeframes due to drawing limitations.

_______________________

▋ INDICATOR SETTINGS:

Section(1): Sessions

(1) Universal Timezone.

(2) Each Session: Enable/Disable, Name, Color, and Time.

Section(2): Session Panel

(1) Show/Hide Session Panel.

(2) Chart Type: Candle/Bar.

(3) Bar’s Up/Down color.

(4) Width and Height of the bar.

(5) Location of Session Panel on chat.

(6) Sort: Left to Right (most recent session is placed on the left), Right to Left (most recent session is placed on the right), and Default (as input arrangement).

Section(3): Chart Visualization

(1) Show/Hide Chart Block Visualization.

(2) Draw Shape: Box/Candle.

(3) Border Style and Size.

(4) Label Styling includes location, size, and some essential selectable infos.

Please let me know if you have any questions

Wskaźnik Pine Script®