Futures Playbook: VWAP + OR + Cross-Asset TellsFutures Playbook: VWAP + OR + Cross-Asset Tells (with Trade Messages + Coach Panel)

This all-in-one futures trading toolkit combines Opening Range (OR) levels, VWAP, and cross-asset signals to help traders quickly read intraday structure, manage execution, and filter noise.

Core Features

• Opening Range (OR):

• Customizable OR window with High/Low and Midpoint.

• Automatic shading of the OR zone.

• VWAP & Bands:

• Built-in or session-anchored VWAP.

• Optional standard deviation bands for context.

• Cross-Asset Tells:

• Live reads on US 10Y yield, DXY, Crude, and Gold.

• Regime detection: rates risk, USD strength, energy softness, and real-rate easing.

• Confirmations:

• Volume vs. moving average filter.

• Cumulative delta with smoothing.

• ATR-based chop filter to avoid low-quality trends.

Trade Messages + Coach Panel

• Trade Messages (labels): Automatic on-chart prompts for OR completion, VWAP reclaim/loss, long/short setups, and EU close flows.

• Coach Panel (table): Real-time dashboard with regime context, directional bias, execution notes, risk reminders, and key levels (ORH, ORL, VWAP).

Alerts

• OR breakout (long/short with confirmations).

• VWAP reclaim or loss.

• 10Y yield crossing risk threshold.

Use Case

Designed for futures traders and scalpers who rely on VWAP + OR dynamics and need cross-asset confirmation before committing to trades. Great for structuring entries, managing risk, and filtering market noise throughout the session.

Średnia Cena Ważona Wolumenem (VWAP)

VWAP Bands by PKTELUGUTRADERThe VWAP bands are like moving-average bands, but instead of being based on a simple or exponential moving average, they are calculated around the Volume Weighted Average Price (VWAP).

UPDATED LINE COLORS

Hybrid Trend MAHybrid Trend MA (Pine Script v6)

This indicator combines Exponential Moving Averages (EMA) and Arnaud Legoux Moving Averages (ALMA) into a single hybrid trend-following tool. It is designed to help traders visualize medium- and long-term trend directions while also capturing smoother short-term signals.

Key Features:

EMA Trend Structure

Three EMAs are plotted (lengths: 38, 62, 200).

Each EMA line changes color depending on whether it is rising or falling relative to the others:

Red → Strong uptrend alignment.

Lime → Strong downtrend alignment.

Aqua → Neutral or transition.

The indicator also fills the space between EMA zones with silver shading to highlight trend channels.

ALMA Trend Confirmation

Two ALMA curves are plotted (lengths: 13, 50).

Similar rising/falling logic is applied to color them:

Red → Bullish alignment and rising.

Green → Bearish alignment and falling.

Cyan → Neutral or uncertain trend.

A cross marker is plotted whenever the fast and slow ALMA lines cross, which may serve as an entry/exit confirmation.

Customizable Smoothing

The smoothe setting controls how many bars are checked to confirm whether an EMA or ALMA is rising/falling, helping reduce noise.

How to Use:

Trend Identification: The EMA set shows the larger market structure. When all EMAs align in direction and color, the trend is stronger.

Entry & Exit Confirmation: The ALMA cross signals can be used to refine entries and exits within the broader EMA trend.

Dynamic Visuals: Colored EMAs + ALMAs make it easy to distinguish bullish, bearish, and ranging conditions at a glance.

[Shoshi] Liquidity SuiteChatGPT řekl:

Přemýšlení po dobu 24s

Liquidity Suite

A powerful, modular toolkit for liquidity-based trading — now with level merging, per-TF/global label offsets, and a master Liquidity toggle.

• Highs/Lows from Custom, 4H, D, W, M, Y

• Previous/Current candle anchoring (wick-anchored)

• Per-TF horizontal offsets + a global right-edge offset for tidy columns

• Optional “Merging levels” with % tolerance (e.g., 0.03%) — clusters nearby levels into one label (Y / pM / …) using the highest-TF color

• Custom line style/width/color and label mode (name/price/both), auto visibility by chart TF

• Buyside/Sellside inducements and FVG/Voids (visible count cap)

• NEW: Global “Show Liquidity” switch — instantly hides and clears all liquidity graphics regardless of other settings

• Asia, London, NY, Custom sessions

• Top/Mid/Bottom + open markers/labels

• Horizontal zones and optional vertical markers (Start/Start+End), extendable lines/background

• Killzones/Day/Week/Month opens

• Optional vertical shading; configurable line + label

• Daily/Weekly/Monthly VWAP with styles Line/Step/Area/Circles/Cross

• Right-edge labels (name/price/both), theme-aware colors

• Dark/White theme

• Separate configs per session/VWAP, per-TF level offsets, and merge tolerance

• Optimized for performance with object limits (lines/labels/boxes)

• Clean, uncluttered visuals for focused execution

Dynamic EMA x VWAP AlertsDynamic EMA × VWAP Alerts generates buy and sell signals only when an EMA crossover happens in a meaningful VWAP (or standard deviation band) context. By combining classic EMA logic with flexible VWAP anchors (Daily, Weekly, Rolling) and optional advanced filters (ATR, Relative Volume, Deviation, Distance, Time Windows) to trim noise further, the script creates location-aware, filterable alerts rather than “everywhere” crosses. The value for trading and originality here lies in the integration of one or multiple anchors, band gating, combinator logic, and advanced regime filters. It’s designed for use across multiple instruments and timeframes, where EMA/VWAP context is relevant. It can run quietly in the background while you focus on price action and your own S/R levels.

What it does (quick take)

Detects EMA crossovers (double or optional triple) and evaluates them in VWAP context.

Plots Buy/Sell markers only when all chosen conditions are met.

Clean UX: keep all or parts of the engine visible or hide everything and let alerts run based on the silent engine behind your own S/R levels in an uncluttered, practical chart, as illustrated below.

Engine illustration: All selected engines visible

Practical use case: Same snapshot sequence as above but all selected engines invisible

Swing examples (beyond intraday)

Signals-only (clean value view):

Signals + your own S/R lines:

EMA selection (choose your playbook)

Defaults: Fast 9, Medium 21 (common intraday combo).

Modes: Double Cross — Fast vs Medium.

Triple Cross (optional) — adds a Slow EMA trend filter (enable Slow > 0).

Ranges: you can set each EMA 0–200 (0 = hidden/off)

Visuals are optional; you can display or hide each EMA line

EMA cross footprints (optional): Helps you assess trend continuation or change.

Use your own strategy: switch to 9/50, 20/50, 50/200, or whatever EMA set you trust for your instrument/timeframe.

VWAP Selection (the context engine)

Daily VWAP – resets each chart day (00:00–23:59). Typical fit: scalpers and fast intraday decision points.

Weekly VWAP – resets at the start of the calendar week. Typical fit: intraday with higher-timeframe context (aligns day trades with weekly bias).

Rolling VWAP – an adjustable VWMA-based rolling anchor (not session-reset), used as a flexible context reference Typical fit: multi-day swings when you want a flexible anchor that adapts across sessions.

Standard deviation bands (σ ±1/±2/±3) available for each anchor and help you express the “how far from fair value” idea.

Why VWAP matters: it’s a running, volume-weighted anchor where strong moves relative to VWAP and its bands help frame mean-reversion vs. trend-continuation risk. Evaluating crosses relative to VWAP/±σ reduces “everywhere” noise and helps frame potential setups.

How alerts are decided

An alert triggers only when:

Your selected EMA crossover occurs, and

Your chosen VWAP gate(s) and any filters pass. (Computed on bar close to avoid mid-bar noise)

Signals and alerts do not repaint; alerts evaluate and fire once per bar close.

Alert gates (Single / AND / OR)

Select one VWAP source or combine two (e.g., Daily + Weekly) with Single, AND, or OR logic.

Choose gate levels from VWAP or standard deviation bands (±σ). Typical long logic: price at/under VWAP or −σ. Typical short logic: price at/over VWAP or +σ.

Practical recipes:

Trend-follow: Daily AND Weekly at/above VWAP → confirms strength on two anchors.

Mean-reversion probe: Daily OR Rolling at −1σ → allows earlier fades with flexibility.

Advanced filtering: Suitable for advanced/Quant traders

During the research and development of this indicator, the EMA/VWAP cross logic was tested on historical S&P500 Futures data to explore patterns on multiple timeframes. These selected filtering indicators below showed correlation between certain market conditions and chosen indicator thresholds, helping reduce noise and lower-quality alerts. Results were research-oriented and are not predictive of future performance.

Therefore, I have built these indicator filters that run silently in the background. They let you trim noise by requiring alerts to appear only in market regimes you define. Each one constrains alert conditions; using them together helps tailor alerts to your strategy—but overly strict settings may filter out most or all alerts.

Relative Volume (RVOL): compares current volume to a baseline; ensures alerts arrive with participation instead of thin tape.

Deviation Threshold (%): controls how close the cross must be to the VWAP/σ level; tight = anchored signals, loose = more activity.

ATR Gate (+ Relative regime): keeps alerts inside a volatility regime; avoids both dead tape and chaotic spikes.

Distance Guard: requires price to be at least X ticks/% away from VWAP; useful to avoid premature signals near fair value.

Note: It’s not recommended to activate all of them at once or change the values aggressively. Unless you’ve done deeper backtesting or machine learning calibration, you can easily filter out everything. Use small thresholds at first, then adjust to your instrument once you see how each filter changes alert frequency and quality. Advanced/quant users can fine-tune freely.

Case example:

Unfiltered: Timeframe 15 min, EMA Selection 9/21, VWAP gates Rolling (250 bars) OR Weekly

Filtered: Same setup as above + activated filters:

RVOL: 100 bars, Min. RVOL 0.4

Deviation threshold (%): 0.3

ATR Length: 14

Min ATR (%): 0.05

Relative regime: Base length 2000, Min Ratio 0.85, Max Ratio 2

Under the hood

This indicator leans on TradingView built-ins (e.g., EMA, VWMA, ATR, alertcondition) to maximize speed, stability, and compatibility while we implement the custom logic (VWAP anchors, band gating, combinator gates, advanced filters, time windows). Built-ins were easy to work with and reduced edge-case bugs and kept the visuals responsive, while the design gives fine-tuning and clean visuals—so both discretionary traders and quant-minded users can shape the alerts to their strategy and workflow.

Disclaimer

The tools, scripts, and indicators presented here are provided for educational and informational purposes only. They are not financial advice and should not be interpreted as investment recommendations, trading signals, or a solicitation to buy or sell any financial instrument.

All forms of trading and investing involve risk. The past performance of any security, strategy, or market condition does not guarantee future outcomes. Users are solely responsible for their own trading and investment decisions, including evaluating their financial situation, objectives, and risk tolerance.

By using this indicator, you acknowledge that you do so at your own risk. The author accepts no liability for any direct or indirect loss or damage—including, without limitation, loss of profits—that may arise from the use of, or reliance upon, this tool.

Volume Pressure Arrows[Blk0ut]Volume Pressure Arrows are an innovative (I think) market pressure tool designed to cut through noise and provide traders with a realistic, but quick insight into buying vs selling pressure and which has real control. Rather than relying on any single classic indicator, this script blends five complementary measures of price–volume dynamics—Cumulative Volume Delta (CVD), VWAP distance, OBV slope, ATR expansion, and the DMI ratio—into a unified “pressure score.”

Each component is normalized, weighted, and combined into a single metric that can be read at a glance through intuitive up and down arrows plotted directly on the chart. By transforming multiple complex data streams into a single aggregated signal, Volume Pressure Arrows help traders answer some of the hardest questions we can face: is the current move backed by conviction? is there true momentum? Is price action about to reverse?

Why It’s Different

Traditional oscillators often create conflicting signals, forcing traders to guess which one to trust. This indicator integrates five perspectives on volume and momentum pressure into a single framework, balancing raw flow (CVD), relative positioning (VWAP), trend conviction (OBV slope), volatility expansion (ATR), and directional bias (DMI). The result is a weighted, probability-minded score capped between -100 and +100 for consistency and clarity.

Important note : Inspiration for the use of directly plotted arrows came from dgtrd "https://www.tradingview.com/u/dgtrd/" and their brilliant work on LazyBear's Squeeze Indicator "https://www.tradingview.com/script/Dsr7B2xE-Squeeze-Momentum-Indicator-LazyBear-vX-by-DGT/"

How to Read It

Bullish Arrows appear below the candles when the pressure score pushes above the neutral threshold, signaling meaningful buyer dominance.

Bearish Arrows appear above the candles when pressure drops below the negative threshold, indicating strong selling pressure.

Neutral Arrows (smaller, faded) mark conditions where pressure exists but is not decisive—useful for spotting early rotations or fading momentum.

Color Gradients dynamically adjust with score intensity, making stronger signals visually brighter and weaker ones softer.

How to Use It Effectively

This tool is best applied as a confirmation and timing layer. It is not meant to replace your core strategy, but to validate whether momentum pressure supports your trade thesis.

Combine with trendlines, chart patterns, or breakouts to gauge conviction.

Use bullish or bearish arrows as filters, only take trades when price action aligns with strong directional pressure.

Watch neutral arrows near key levels; they often foreshadow balance breaking into directional moves.

Adjust the weightings to emphasize the components that matter most to your style (e.g., more weight on CVD for scalpers, or ATR expansion for volatility traders).

As with any indicator, this is not a magic ball and does not guarantee success. But it does allow you to increase the probability odds to your favor if you align it with your edge. Happy trading!

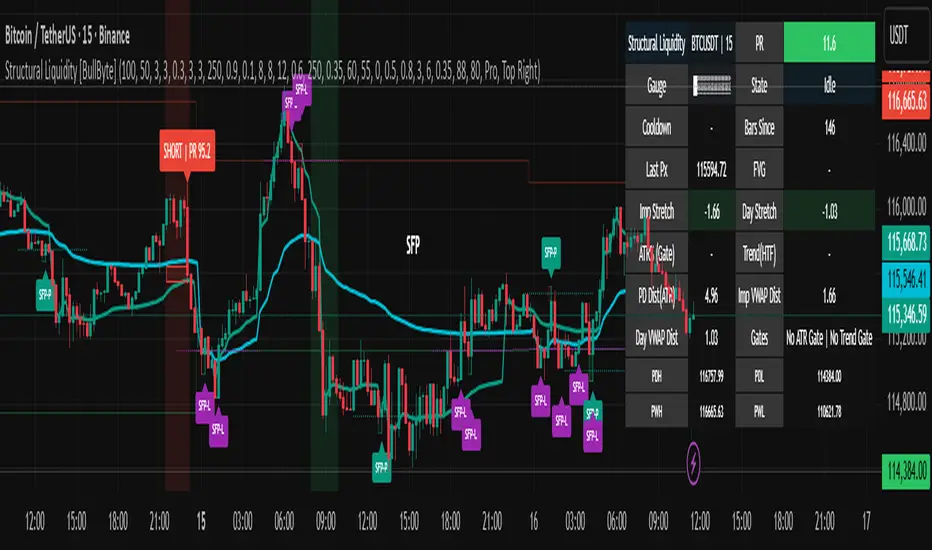

Structural Liquidity Signals [BullByte]Structural Liquidity Signals (SFP, FVG, BOS, AVWAP)

Short description

Detects liquidity sweeps (SFPs) at pivots and PD/W levels, highlights the latest FVG, tracks AVWAP stretch, arms percentile extremes, and triggers after confirmed micro BOS.

Full description

What this tool does

Structural Liquidity Signals shows where price likely tapped liquidity (stop clusters), then waits for structure to actually change before it prints a trigger. It spots:

Liquidity sweeps (SFPs) at recent pivots and at prior day/week highs/lows.

The latest Fair Value Gap (FVG) that often “pulls” price or serves as a reaction zone.

How far price is stretched from two VWAP anchors (one from the latest impulse, one from today’s session), scaled by ATR so it adapts to volatility.

A “percentile” extreme of an internal score. At extremes the script “arms” a setup; it only triggers after a small break of structure (BOS) on a closed bar.

Originality and design rationale, why it’s not “just a mashup”

This is not a mashup for its own sake. It’s a purpose-built flow that links where liquidity is likely to rest with how structure actually changes:

- Liquidity location: We focus on areas where stops commonly cluster—recent pivots and prior day/week highs/lows—then detect sweeps (SFPs) when price wicks beyond and closes back inside.

- Displacement context: We track the last Fair Value Gap (FVG) to account for recent inefficiency that often acts as a magnet or reaction zone.

- Stretch measurement: We anchor VWAP to the latest N-bar impulse and to the Daily session, then normalize stretch by ATR to assess dislocation consistently across assets/timeframes.

- Composite exhaustion: We combine stretch, wick skew, and volume surprise, then bend the result with a tanh transform so extremes are bounded and comparable.

- Dynamic extremes and discipline: Rather than triggering on every sweep, we “arm” at statistical extremes via percent-rank and only fire after a confirmed micro Break of Structure (BOS). This separates “interesting” from “actionable.”

Key concepts

SFP (liquidity sweep): A candle briefly trades beyond a level (where stops sit) and closes back inside. We detect these at:

Pivots (recent swing highs/lows confirmed by “left/right” bars).

Prior Day/Week High/Low (PDH/PDL/PWH/PWL).

FVG (Fair Value Gap): A small 3‑bar gap (bar2 high vs bar1 low, or vice versa). The latest gap often acts like a magnet or reaction zone. We track the most recent Up/Down gap and whether price is inside it.

AVWAP stretch: Distance from an Anchored VWAP divided by ATR (volatility). We use:

Impulse AVWAP: resets on each new N‑bar high/low.

Daily AVWAP: resets each new session.

PR (Percentile Rank): Where the current internal score sits versus its own recent history (0..100). We arm shorts at high PR, longs at low PR.

Micro BOS: A small break of the recent high (for longs) or low (for shorts). This is the “go/no‑go” confirmation.

How the parts work together

Find likely liquidity grabs (SFPs) at pivots and PD/W levels.

Add context from the latest FVG and AVWAP stretch (how far price is from “fair”).

Build a bounded score (so different markets/timeframes are comparable) and compute its percentile (PR).

Arm at extremes (high PR → short candidate; low PR → long candidate).

Only print a trigger after a micro BOS, on a closed bar, with spacing/cooldown rules.

What you see on the chart (legend)

Lines:

Teal line = Impulse AVWAP (resets on new N‑bar extreme).

Aqua line = Daily AVWAP (resets each session).

PDH/PDL/PWH/PWL = prior day/week levels (toggle on/off).

Zones:

Greenish box = latest Up FVG; Reddish box = latest Down FVG.

The shading/border changes after price trades back through it.

SFP labels:

SFP‑P = SFP at Pivot (dotted line marks that pivot’s price).

SFP‑L = SFP at Level (at PDH/PDL/PWH/PWL).

Throttle: To reduce clutter, SFPs are rate‑limited per direction.

Triggers:

Triangle up = long trigger after BOS; triangle down = short trigger after BOS.

Optional badge shows direction and PR at the moment of trigger.

Optional Trigger Zone is an ATR‑sized box around the trigger bar’s close (for visualization only).

Background:

Light green/red shading = a long/short setup is “armed” (not a trigger).

Dashboard (Mini/Pro) — what each item means

PR: Percentile of the internal score (0..100). Near 0 = bullish extreme, near 100 = bearish extreme.

Gauge: Text bar that mirrors PR.

State: Idle, Armed Long (with a countdown), or Armed Short.

Cooldown: Bars remaining before a new setup can arm after a trigger.

Bars Since / Last Px: How long since last trigger and its price.

FVG: Whether price is in the latest Up/Down FVG.

Imp/Day VWAP Dist, PD Dist(ATR): Distance from those references in ATR units.

ATR% (Gate), Trend(HTF): Status of optional regime filters (volatility/trend).

How to use it (step‑by‑step)

Keep the Safety toggles ON (default): triggers/visuals on bar‑close, optional confirmed HTF for trend slope.

Choose timeframe:

Intraday (5m–1h) or Swing (1h–4h). On very fast/thin charts, enable Performance mode and raise spacing/cooldown.

Watch the dashboard:

When PR reaches an extreme and an SFP context is present, the background shades (armed).

Wait for the trigger triangle:

It prints only after a micro BOS on a closed bar and after spacing/cooldown checks.

Use the Trigger Zone box as a visual reference only:

This script never tells you to buy/sell. Apply your own plan for entry, stop, and sizing.

Example:

Bullish: Sweep under PDL (SFP‑L) and reclaim; PR in lower tail arms long; BOS up confirms → long trigger on bar close (ATR-sized trigger zone shown).

Bearish: Sweep above PDH/pivot (SFP‑L/P) and reject; PR in upper tail arms short; BOS down confirms → short trigger on bar close (ATR-sized trigger zone shown).

Settings guide (with “when to adjust”)

Safety & Stability (defaults ON)

Confirm triggers at bar close, Draw visuals at bar close: Keep ON for clean, stable prints.

Use confirmed HTF values: Applies to HTF trend slope only; keeps it from changing until the HTF bar closes.

Performance mode: Turn ON if your chart is busy or laggy.

Core & Context

ATR Length: Bigger = smoother distances; smaller = more reactive.

Impulse AVWAP Anchor: Larger = fewer resets; smaller = resets more often.

Show Daily AVWAP: ON if you want session context.

Use last FVG in logic: ON to include FVG context in arming/score.

Show PDH/PDL/PWH/PWL: ON to see prior day/week levels that often attract sweeps.

Liquidity & Microstructure

Pivot Left/Right: Higher values = stronger/rarer pivots.

Min Wick Ratio (0..1): Higher = only more pronounced SFP wicks qualify.

BOS length: Larger = stricter BOS; smaller = quicker confirmations.

Signal persistence: Keeps SFP context alive for a few bars to avoid flicker.

Signal Gating

Percent‑Rank Lookback: Larger = more stable extremes; smaller = more reactive extremes.

Arm thresholds (qHi/qLo): Move closer to 0.5 to see more arms; move toward 0/1 to see fewer arms.

TTL, Cooldown, Min bars and Min ATR distance: Space out triggers so you’re not reacting to minor noise.

Regime Filters (optional)

ATR percentile gate: Only allow triggers when volatility is at/above a set percentile.

HTF trend gate: Only allow longs when the HTF slope is up (and shorts when it’s down), above a minimum slope.

Visuals & UX

Only show “important” SFPs: Filters pivot SFPs by Volume Z and |Impulse stretch|.

Trigger badges/history and Max badge count: Control label clutter.

Compact labels: Toggle SFP‑P/L vs full names.

Dashboard mode and position; Dark theme.

Reading PR (the built‑in “oscillator”)

PR ~ 0–10: Potential bullish extreme (long side can arm).

PR ~ 90–100: Potential bearish extreme (short side can arm).

Important: “Armed” ≠ “Enter.” A trigger still needs a micro BOS on a closed bar and spacing/cooldown to pass.

Repainting, confirmations, and HTF notes

By default, prints wait for the bar to close; this reduces repaint‑like effects.

Pivot SFPs only appear after the pivot confirms (after the chosen “right” bars).

PD/W levels come from the prior completed candles and do not change intraday.

If you enable confirmed HTF values, the HTF slope will not change until its higher‑timeframe bar completes (safer but slightly delayed).

Performance tips

If labels/zones clutter or the chart lags:

Turn ON Performance mode.

Hide FVG or the Trigger Zone.

Reduce badge history or turn badge history off.

If price scaling looks compressed:

Keep optional “score”/“PR” plots OFF (they overlay price and can affect scaling).

Alerts (neutral)

Structural Liquidity: LONG TRIGGER

Structural Liquidity: SHORT TRIGGER

These fire when a trigger condition is met on a confirmed bar (with defaults).

Limitations and risk

Not every sweep/extreme reverses; false triggers occur, especially on thin markets and low timeframes.

This indicator does not provide entries, exits, or position sizing—use your own plan and risk control.

Educational/informational only; no financial advice.

License and credits

© BullByte - MPL 2.0. Open‑source for learning and research.

Built from repeated observations of how liquidity runs, imbalance (FVG), and distance from “fair” (AVWAPs) combine, and how a small BOS often marks the moment structure actually shifts.

Goat VWAPMulti TF Vwap used by Goat in most of his trades.

Used for TP/SL; support/resistance.

Goat used it most on high TF like daily.

VWAP Fade RTHSame as

Except this version only updates during CME Regular Trading Hours

9:30 AM NY/EST -4 PM NY/EST

VWAP FadeVWAP fade indicator simple parameters for how it works and the logic behind VWAP fade

You can try other products but recommended for Copper/Silver futures due to how they tend to do the VWAP fade

Identify VWAP retest:

Price moves back into VWAP after trending away.

Fail condition:

Candle touches VWAP but fails to close across it (stays on trend side).

Signal:

Short if price came from below and fails to close above VWAP.

Long if price came from above and fails to close below VWAP.

Confirm with volume spike (optional filter).

AVWAP (ATR-Weighted VWAP) IndicatorAVWAP (Average True Range Weighted Average Price), you typically combine two core indicators:

1. VWAP (Volume Weighted Average Price)

This is the base indicator that calculates the average price weighted by volume over a session or specified period.

VWAP serves as the core reference price level around which volatility adjustments are made for AVWAP.

2. ATR (Average True Range)

ATR measures market volatility, representing the average price range over a set period.

ATR is used to create volatility bands or buffers around the VWAP, adjusting levels to reflect prevailing market volatility.

How These Indicators Work Together for AVWAP:

Use VWAP to establish your average price line weighted by volume.

Calculate ATR to understand the average price movement range.

Apply ATR as multipliers to VWAP to create upper and lower volatility-adjusted bands (e.g., VWAP ± 1 × ATR), which form the AVWAP bands.

These bands help identify volatility-aware support/resistance and stop-loss placement zones.

So to make things easier I have built a custom AVWAP indicator to be used

How to use my custom indicator:

The central blue line is the VWAP.

The red and green bands above and below VWAP are AVWAP bands set at VWAP ± 1.5 × ATR by default.

Adjust the ATR length and multiplier inputs to suit the timeframe and volatility preferences.

Use the bands as dynamic support/resistance and for setting stop loss zones based on volatility.

Monthly VWAPDescription

This indicator identifies potential mean reversion opportunities by tracking price deviations from monthly VWAP with dynamic volatility-adjusted thresholds.

Core Logic:

The indicator monitors when price moves significantly away from monthly VWAP and looks for potential reversal opportunities. It uses ATR-based dynamic thresholds that adapt to current market volatility, combined with volume confirmation to filter out weak signals.

Key Features:

Adaptive Thresholds: ATR-based bands that adjust to market volatility

Volume Confirmation: Requires average volume spike to validate signals

Monthly Reset: VWAP anchors reset each month for fresh reference levels

Visual Clarity: Color-coded deviation line with background highlights for active signals

Info Panel: Shows days from anchor and current price context vs fair value

Signal Generation:

Buy Signal: Price below monthly VWAP by threshold amount with elevated volume

Sell Signal: Price above monthly VWAP by threshold amount with elevated volume

Neutral: Price within threshold range or insufficient volume

Best Used For:

Mean reversion strategies in ranging markets

Identifying potential oversold/overbought conditions

Understanding price position relative to monthly fair value

Option Selling Indicator

* ✅ Bullish Trend → Background turns Green (favorable for Put Selling)

* ❌ Bearish Trend → Background turns Red (favorable for Call Selling)

* ⚪ Sideways / Weak Trend → Background turns White (avoid trades or use range strategies)

📊 How to Use:

1. Apply the indicator on Index Futures or Stocks where Options are actively traded.

2. Use the **background color** as a visual guide:

* Green → Consider **Put Selling** opportunities.

* Red → Consider **Call Selling** opportunities.

* Grey → Market is sideways → **Avoid trades** or use strangle/straddle strategies.

3. Confirm signals with **VWAP levels** for better entries.

Weekly VwapsThe Weekly Vwaps indicator lets you plot weekly Volume-Weighted Average Price (VWAP) lines for up to six months of your choosing, with years ranging from 2020 to 2050. It’s a focused tool pulled straight from the weekly VWAP section of the Advanced VWAP Calendar indicator, keeping all the same controls and look but expanded to handle more months. You can use it alongside the original indicator if you need extra weekly VWAPs (up to 30 lines total) or run it on its own for a clean, dedicated setup.

How It Works: Six Month Groups: Pick any six months (e.g., Jan 2020, Sep 2025, or Jul 2040) and enable up to five weekly VWAPs per month (W1–W5), starting from Monday midnight.

Default Setup: Loads with September 2025 VWAPs turned on, with other months (August–April 2025) off but ready to enable. All default to 2025.

Customization: Toggle all weeks in a month or pick specific ones. Adjust label sizes (tiny to huge) and line widths (1–5). Colors are teal, fuchsia, red, green, and yellow/orange for weeks 1–5, with clear labels like “W1 Sep 2025 123.45”.

Label Control: A “Show All Labels” switch lets you hide labels to keep your chart tidy.

Intraday Only: Works on intraday timeframes (e.g., 5-minute, 1-hour) for accurate VWAPs.

Why Use It: Add to Advanced VWAP Calendar: If the original’s two-month limit isn’t enough, this adds six more months of weekly VWAPs for deeper analysis.

Standalone Option: Perfect if you only want weekly VWAPs without other features, with flexibility to pick any months and years.

User-Friendly: Ready to go with September 2025 enabled, easy to tweak for past or future data.

Get Started: Add it to your TradingView chart, and September 2025 VWAPs will show up instantly. Adjust months, years, or toggles in the settings to focus on what you need. Test it on intraday charts and use the label toggle to manage clutter. Great for traders wanting precise, customizable weekly VWAPs!

FuTech : Preferential Price📌 First Ever Indicator : FuTech : Preferential Price

💡 What if you could instantly know the Preferential Price — as if the company announced a preferential issue in today’s meeting surprisingly?

Normally, you’d be stuck with tedious valuation spreadsheets and SEBI formula checks 🧮📑…

✨ But not anymore — this tool does the hard work for you!

With just one click, it auto-calculates the Preferential Issue Floor Price under SEBI ICDR Regulations, 2018 - Regulation 164 (as amended), directly from your chart symbol.

✅ How it works ?

📅 Relevant Date = 30 days prior to either:

• Today’s date (default mode)

• Or your chosen EGM date (user input)

📊 For the Relevant Date, the indicator automatically computes:

• VWAP (90 trading days preceding Relevant Date)

• VWAP (10 trading days preceding Relevant Date)

🔎 As per SEBI Reg.164, the higher of these two VWAPs is selected as the Minimum Issue Price (Preferential Price).

💰 Price is neatly formatted in Indian style (e.g. ₹1,00,000).

✅ Key Features:

⚡ Auto-calculates from chart symbol — no manual entry.

🎛️ Option to input EGM date for accurate floor price compliance.

🎨 Fully customizable: text color, size, background, position.

🪄 Clean display → shows only the final Preferential Price (Reg.164).

📌 Usage:

This indicator is built for analysts, fund managers, and corporate professionals dealing with Preferential Allotment pricing compliance.

It ensures quick visibility of the floor price under SEBI ICDR rules, directly on your chart.

⚠️ Disclaimer:

📌 The calculated Preferential Price is an approximation based on SEBI ICDR Reg.164 methodology.

📊 Actual price determined by the company / merchant banker may vary slightly (±5) due to rounding, data source differences, or timing adjustments.

📅 Ensure to verify with official exchange data and SEBI filings before relying on these numbers.

📝 This tool is meant for analytical and educational purposes only, not a substitute for regulatory or professional advice.

Multi Rolling VWAP Indicator - RVWAPThe Rolling VWAP (RVWAP) Indicator calculates a volume-weighted average price over a user-defined lookback period, providing a smoother alternative to traditional VWAP without session resets. Ideal for intraday and swing traders, it helps identify dynamic support/resistance levels and market trends across any timeframe.

Features:

Customizable Lookback: Adjust the rolling window (default: 14 bars) to suit your trading style.

Dynamic Coloring: RVWAP line changes color based on price position—green (above), red (below), or yellow (equal).

Standard Deviation Bands: Optional upper/lower bands (toggleable) highlight volatility and potential reversal zones.

Visual Clarity: Semi-transparent band fill for easy trend analysis.

Usage:

Add the indicator to your chart, tweak the lookback period and band settings, and use it to spot trend direction, support/resistance, or mean-reversion opportunities. Perfect for stocks, forex, crypto, and more.

EMA/VWAP SuiteEMA/VWAP Suite

Overview

The EMA/VWAP Suite is a versatile and customizable Pine Script indicator designed for traders who want to combine Exponential Moving Averages (EMAs) and Volume Weighted Average Prices (VWAPs) in a single, powerful tool. It overlays up to eight EMAs and six VWAPs (three anchored, three rolling) on the chart, each with percentage difference labels to show how far the current price is from these key levels. This indicator is perfect for technical analysis, supporting strategies like trend following, mean reversion, and VWAP-based trading.

By default, the indicator displays eight EMAs and a session-anchored VWAP (AVWAP 1, in fuchsia) with their respective percentage difference labels, keeping the chart clean yet informative. Other VWAPs and their bands are disabled by default but can be enabled and customized as needed. The suite is designed to minimize clutter while providing maximum flexibility for traders.

Features

- Eight Customizable EMAs: Plot up to eight EMAs with user-defined lengths (default: 3, 9, 19, 38, 50, 65, 100, 200), each with a unique color for easy identification.

- EMA Percentage Difference Labels: Show the percentage difference between the current price and each EMA, displayed only for visible EMAs when enabled.

- Three Anchored VWAPs: Plot VWAPs anchored to the start of a session, week, or month, with customizable source, offset, and band multipliers. AVWAP 1 (session-anchored, fuchsia) is enabled by default.

- Three Rolling VWAPs: Plot VWAPs calculated over fixed periods (default: 20, 50, 100), with customizable source, offset, and band multipliers.

- VWAP Bands: Optional upper and lower bands for each VWAP, based on standard deviation with user-defined multipliers.

- VWAP Percentage Difference Labels: Display the percentage difference between the current price and each VWAP, shown only for visible VWAPs. Enabled by default to show the AVWAP 1 label.

- Customizable Colors: Each VWAP has a user-defined color via input settings, with labels matching the VWAP line colors (e.g., AVWAP 1 defaults to fuchsia).

Flexible Display Options: Toggle individual EMAs, VWAPs, bands, and labels on or off to reduce chart clutter.

Settings

The indicator is organized into intuitive setting groups:

EMA Settings

Show EMA 1–8 : Toggle each EMA on or off (default: all enabled).

EMA 1–8 Length : Set the period for each EMA (default: 3, 9, 19, 38, 50, 65, 100, 200).

Show EMA % Difference Labels : Enable/disable percentage difference labels for all EMAs (default: enabled).

EMA Label Font Size (8–20) : Adjust the font size for EMA labels (default: 10, mapped to “tiny”).

Anchored VWAP 1–3 Settings

Show AVWAP 1–3 : Toggle each anchored VWAP on or off (default: AVWAP 1 enabled, others disabled).

AVWAP 1–3 Color : Set the color for each VWAP line and its label (default: fuchsia for AVWAP 1, purple for AVWAP 2, teal for AVWAP 3).

AVWAP 1–3 Anchor : Choose the anchor period (“Session,” “Week,” “Month”; default: Session for AVWAP 1, Week for AVWAP 2, Month for AVWAP 3).

AVWAP 1–3 Source : Select the price source (default: hlc3).

AVWAP 1–3 Offset : Set the horizontal offset for the VWAP line (default: 0).

Show AVWAP 1–3 Bands : Toggle upper/lower bands (default: disabled).

AVWAP 1–3 Band Multiplier : Adjust the standard deviation multiplier for bands (default: 1.0).

Rolling VWAP 1–3 Settings

Show RVWAP 1–3 : Toggle each rolling VWAP on or off (default: disabled).

RVWAP 1–3 Color : Set the color for each VWAP line and its label (default: navy for RVWAP 1, maroon for RVWAP 2, fuchsia for RVWAP 3).

RVWAP 1–3 Period Length : Set the period for the rolling VWAP (default: 20, 50, 100).

RVWAP 1–3 Source : Select the price source (default: hlc3).

RVWAP 1–3 Offset : Set the horizontal offset (default: 0).

Show RVWAP 1–3 Bands : Toggle upper/lower bands (default: disabled).

RVWAP 1–3 Band Multiplier : Adjust the standard deviation multiplier for bands (default: 1.0).

VWAP Label Settings

Show VWAP % Difference Labels : Enable/disable percentage difference labels for all VWAPs (default: enabled, showing AVWAP 1 label).

VWAP Label Font Size (8–20) : Adjust the font size for VWAP labels (default: 10, mapped to “tiny”).

How It Works

EMAs : Calculated using ta.ema(close, length) for each user-defined period. Percentage differences are computed as ((close - ema) / close) * 100 and displayed as labels for visible EMAs when show_ema_labels is enabled.

Anchored VWAPs : Calculated using ta.vwap(source, anchor, 1), where the anchor is determined by the selected timeframe (Session, Week, or Month). Bands are computed using the standard deviation from ta.vwap.

Rolling VWAPs : Calculated using ta.vwap(source, length), with bands based on ta.stdev(source, length).

Labels : Updated on each new bar (ta.barssince(ta.change(time) != 0) == 0) to show percentage differences. Labels are only displayed for visible EMAs/VWAPs to avoid clutter.

Color Matching: VWAP labels use the same color as their corresponding VWAP lines, set via input settings (e.g., avwap1_color for AVWAP 1).

Example Use Cases

- Trend Following: Use longer EMAs (e.g., 100, 200) to identify trends and shorter EMAs (e.g., 3, 9) for entry/exit signals.

- Mean Reversion: Monitor percentage difference labels to spot overbought/oversold conditions relative to EMAs or VWAPs.

- VWAP Trading: Use the default session-anchored AVWAP 1 for intraday trading, adding weekly/monthly VWAPs or rolling VWAPs for broader context.

- Intraday Analysis: Leverage the session-anchored AVWAP 1 (enabled by default) for day trading, with bands as support/resistance zones.

Cumulative VWAPThis indicator plots the cumulative VWAP from the first bar loaded on the chart. Unlike the traditional daily VWAP that resets at the start of each trading session, this version continuously aggregates price and volume over the full visible chart history.

(Fixed-Range) Anchored VWAPThis "Fixed-Range Anchored VWAP" indicator allows traders full control over where the VWAP calculation begins and ends. VWAP combines both price and volume to reflect the true average price paid, often serving as a benchmark for gauging value, sentiment, and trend strength.

With this tool, traders can anchor VWAP to any candle, optionally define an end point, or keep it running forward with a single toggle. Up to three bands can be added around VWAP, either as standard deviations or percentage offsets.

How to Use

The indicator is particularly useful for analyzing VWAP around significant events, like earnings announcements or sharp price swings, to identify support, resistance, and mean-reversion opportunities.

Add the indicator and select a candle to set the Anchor.

Choose an End point or enable Cancel End for an open-ended VWAP.

Pick Std Dev or Percent for band mode.

Turn on up to three bands, adjust multipliers, and set fill colors.

Use VWAP and its bands to evaluate extensions, trend context, and fair value zones.

Anchored VWAP Pro - Multi-Timeframe Analysis ToolProfessional anchored VWAP indicator featuring multiple key anchor points for comprehensive price analysis. Displays volume-weighted average prices from critical market moments including NY market open, daily highs/lows, session start, and previous day reference levels.

Key Features:

NY Open VWAP (9:30 AM ET anchor)

High of Day (HOD) and Low of Day (LOD) VWAPs with dynamic anchoring

Start-of-Day VWAP (18:00 ET session anchor)

Previous Day VWAP for reference and support/resistance analysis

Customizable line colors, widths, and styles (solid/dashed/dotted)

Clean visibility controls for each VWAP line

Optimized for forex and futures markets with proper session timing

Historical line preservation with configurable display periods

Usage:

Ideal for identifying key support/resistance levels, mean reversion opportunities, and institutional price levels. The multiple anchor points provide context for both intraday and swing trading strategies.

Settings:

Full customization of visibility, colors, line weights, and styles through organized input groups. Toggle individual VWAPs on/off based on your trading strategy requirements.

Market Application:

Designed for 24-hour markets including forex, indices, and commodities. Particularly effective on major currency pairs and index futures during active trading sessions.

VWAP Price ChannelVWAP Price Channel cuts the crust off of a traditional price channel (Donchian Channel) by anchoring VWAPs at the highs and lows. By doing this, the flat levels, characteristic of traditional Donchian Channels, are no more!

Author's Note: This indicator is formed with no inherent use, and serves solely as a thought experiment.

> Concept

I would be hesitant to call this a "predictive" indicator, however the behavior of it would suggest it could be considered at least partially predictive

Essentially, the Anchored VWAPs creates something from otherwise nothing.

While the DC upper or lower values are staying flat, the VWAPs improvise based on price and volume to project a level that may be a better representation of where future highs or lows may settle.

Visually, this looks like we have cut off the corners of the Donchian Channel.

Note: Notice how we are calculating values before the corners are realized.

> Implementation

While this is only a concept indicator, The specific application I've gone with for this, is a sort of supertrend-ish display (A Trend Flipping Trailing Stop Loss).

The script uses basic logic to create a trend direction, and then displays the Anchored VWAPs as a form of trailing stop loss.

While "In Trend", the script fills in the area between the VWAP and Price in the direction of trend.

When new highs or lows are made while in trend, the opposite VWAP will start to generate at the new highs or lows. These happen on every new high or low, so they are not indicating the trend shift, but could be interpreted as breakout levels for the current trend direction in order for continuation.

Note: All values are drawn live, but when using higher timeframes, there is a natural calculation discrepancy when using live data vs. historical.

> Technicals

In this script, I'm simply detecting new highs or lows from the DC and using those as the anchor frequency on the built-in VWAP function.

So each time a new high or low is made based on DC, the VWAP function re-anchors to the high or low of the candle.

Past that, I have implemented some logic in order to account for a common occurrence I faced during development.

Frequently, the price would outpace the anchored VWAP, so we would end up with the VWAP being further from price than the actual DC upper or lower.

Due to this, what I have ended up with was a third value which, rather than switching between raw VWAP values and DC values, it adjusts the value based on the change in the VWAP value.

This can be simply thought of as a "Start + Change" type of setup.

By doing this, I can use the change values from the actual anchored VWAP, and under normal conditions, this will also be the true VWAP value.

However, situationally, I am able to update the start value which we're applying the VWAP change to.

In other words, when these situations happen, the VWAP change is added to the new (closer to price) DC value.

The specific trend logic being used is nothing fancy at all, we are simply checking if a new high or low is created and setting the trend in that direction.

This is in line with some traditional DC Strategies.

To those who made it here,

Just remember:

The chart may be ugly, but it's the fastest analysis of the data you can get.

Nicer displays often come at the hidden cost of latency.

You have to shoot your shot to make it.

Choose 2: Fast, Clean, Useful

Enjoy!

VWMA MACD Trend Grinder Buy/Sell SignalsDescription:

This indicator combines a VWMA-based MACD with volume and trend filters to reduce false buy and sell signals.

It is designed to give more reliable entry and exit points in trending markets while avoiding low-volume noise.

Features:

1. VWMA MACD:

- MACD is calculated using Volume-Weighted Moving Averages (VWMA) instead of standard EMAs.

- Histogram shows the difference between MACD and its signal line.

2. Volume Filter:

- Signals are only triggered when current volume exceeds a multiple of its moving average.

- Reduces false signals in low-volume periods.

3. Trend Filter:

- Only triggers buy signals when price is above a long-term VWMA (uptrend).

- Only triggers sell signals when price is below the long-term VWMA (downtrend).

- Helps avoid counter-trend trades.

4. Plots:

- MACD (blue), Signal (orange), Histogram (green/red)

- Trend VWMA (purple)

- Buy and Sell arrows in the indicator pane (green/red)

5. Alerts:

- Configurable alerts for buy and sell signals filtered by volume and trend.

Inputs:

- Fast Length: VWMA period for the fast MACD line (default 12)

- Slow Length: VWMA period for the slow MACD line (default 26)

- Signal Length: EMA period for the MACD signal line (default 9)

- Volume MA Length: Length for volume moving average filter (default 20)

- Volume Threshold Multiplier: Multiplier for volume filter (default 1.2)

- Trend VWMA Length: Period for long-term trend VWMA (default 50)

- Price Source: Close, HL2, HLC3, OHLC4

Usage:

- Use as a confirmation tool along with other analysis techniques.

- Buy when the green triangle appears (MACD crossover, above trend VWMA, sufficient volume).

- Sell when the red triangle appears (MACD crossunder, below trend VWMA, sufficient volume).

- Trend VWMA helps visually confirm the market trend.