BBPCTIndicator tracks percentage distance between current price and its historical deviations, to produce premium and discount zones, suggest mean reversions,cooldowns and pullbacks

Script so far is traditional,simple, and straight forward ,tinkered it real quick on friend request after failing to find properly done and intuitive work on Bollinger Bands % in pine library

It might or might not be re-published as open source or study protected script , really depends on how future updates goes,how much work will be put in and how unique end result will be.

//Input Options in first release

Option to switch between small (6) variety of filters

(This time no non-traditional filters to avoid overwhelming and confusing users ,current list still yields good diversity for changing indicators behavior and pinpointing best suited filtering direction, in future current types will be swapped with more advanced ones and consolidated into three options tailored for different market conditions - trending,ranging, and balanced(?) - jack of all trades master of none.)

Option to toggle basic warnings about possible reversals,option for colored bars(candles) and/or arrow plots

OB/OS levels can be adjusted via inputs

Note: Current default compiling will lack traditional values as i ditched them and set to personal preference, set to 100 0 for traditional look

Sigma can be changed in inputs,length obviously can be changed too

Source can be changed

//Upcoming updates

Polishment- algorithmic change for cores logic

Attempt to build logic to differentiate pullbacks from reversals

More complex reversal recognition and their confirmations

Proper color coding

//Screencaps

Dont use comment section for asking access , got two warnings already from tradingview moderators because people flood the comment section and apparently its offence from my end to not provide directions for access.

If u are willing to test indicator and actually deliver feedback,ideas, params - Dm(direct message) and we add u ,expiration timer will be set in place to clean up in case no feedback is delivered.

P.S its not likely i will add more people to testing after people count reach 40-50 or script becomes older than week

Odchylenie standardowe (Zmienność)

StDev Based Trendlines - JDAs a second alternatively based trendline script this is the Standard Deviation vesrion.

This script draws trendlines from the pivot points in the price chart.

The angle of the trendlines is determined by (a percentage of) the Standard Deviation.

The angle follows the change in price, compared to the StDev at the moment where the pivot point is detected

The StDev percentage determines if the trendline follows the rate of change of the StDev or a fraction ( value < 100) or a multiple ( value > 100) of that

JD.

#NotTradingAdvice #DYOR

Disclaimer.

I AM NOT A FINANCIAL ADVISOR.

THESE IDEAS ARE NOT ADVICE AND ARE FOR EDUCATION PURPOSES ONLY.

ALWAYS DO YOUR OWN RESEARCH!

VWAP Standard Deviation Multi-Time FrameVWAP Standard Deviation Multi-Time Frame indicator shows VWAP , 1 standard deviation price from the VWAP, 2 standard deviation price from the VWAP and 3 standard deviation price from the VWAP

These lines are value regions and usually act as great support and resistance .

For best results allow the VWAP to develop in the beginning of the time frame, for almost about 20% of the total time period

For example, in a daily time frame, wait for about 4hrs for VWAP to develop before using the VWAP and Standard devaitions of VWAP as support and resistance zones

Change the values in timeframe input to use it for intraday, swing and long term trades.

Possible values are based on standard timeframe values 5,15,D,W,M, 12M etc

Trend Analysis IndicatorThe Trend Analysis Indicator was created by Adam White (Stocks & Commodities V. 10:8 (358-360)) and this is not to be confused with the Trend Analysis Index which was also created by Adam White. The stock is trending when it is above the signal and loses steam when it falls below the signal. Generally you should buy when it is above it's signal and sell when it goes below the signal.

Let me know if you would like me to write more scripts!

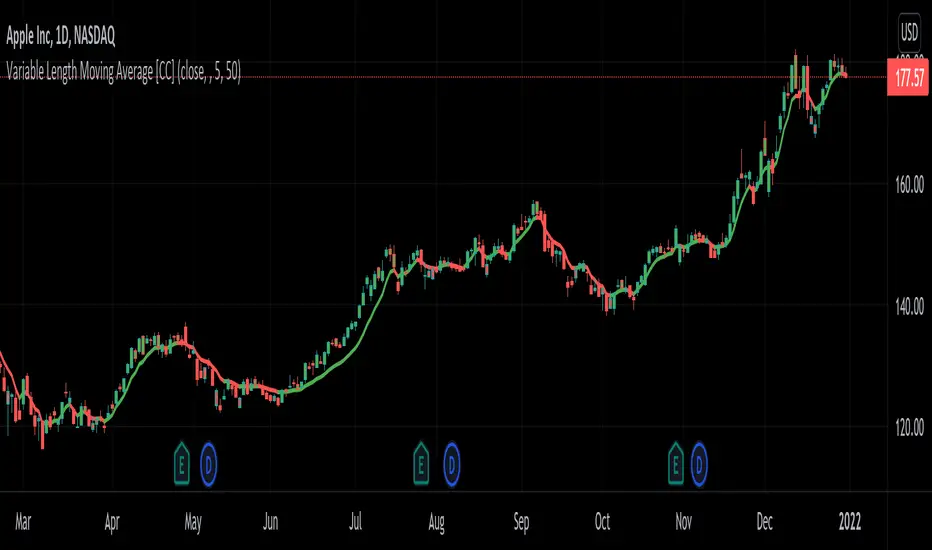

Variable Length Moving AverageThe Variable Length Moving Average was created by George R. Arrington Ph.D. (Stocks & Commodities V. 9:6 (219-223)) and I'm really loving this indicator. It is a great moving average that hugs the price very closely and it is fully adjustable to your needs. It detects signals extremely well and I have color coded the moving average line to make it very easy to interpret.

This is not to be confused with the Variable Moving Average created by Tushar S. Chande and as of now I haven't seen any other script for this moving average out there yet.

Please let me know if you would like me to write any other scripts for indicators you would like to see!

McMillan Volatility Bands w/ Buy & Sell Signals [optstrategist]BACKGROUND

McMillan Volatility Bands are an alternative approach to John Bollinger's "Bollinger Band" study and developed by world-renowned options trader and author Lawrence G. McMillan. Given his background in options trading, it was natural for Lawrence to approach any volatility-based study in the same manner options are priced --using Black-Scholes model. This model of pricing assumes a financial asset's volatility should be measured in percentage change rather than absolute value change.

OVERVIEW

The McMillan Volatility Bands indicator for TradingView will plot the 3 and 4-standard deviation bands around a 20-day moving average. This is how Larry has always used this system. The user can, however, change the standard deviation value as well as the moving average length to their preferred setting. This indicator can be used on any asset and on any timeframe.

Furthermore, the indicator will plot buy and sell signals based on a trading system used by Larry in his flagship newsletter publication The Daily Strategist. The system gives a signal when price closes outside the 4-sigma band and then closes back within the 3-sigma band. That 'signal bar' will be colored red or green for a sell or buy signal setup, respectively.

Finally, an arrow will be plotted on the chart where the system would actually enter the trade. This is determined when price trades a little beyond the extreme of the 'signal bar'. The level by which price has to go beyond the 'signal bar' is an input parameter and can be adjusted by the user. We've chosen the default value of 0.34. This means, the indicator will not give a buy or sell entry until the price moves: 1/3 x beyond the extreme signal bar. This is to prevent getting whipsawed by some setups that never really move in your favor. We've found it successfully removes the less-valuable trade setups.

PARAMETERS

ma_length => length of the moving average that the volatility bands work off of

outside_sigma => standard deviation of outer volatility band

inside_sigma => standard deviation of inner volatility band

entry_trigger_cushion => this refers to the percentage of the signal bar's range. The default value is 0.34. This means price will need to move 1/3 (~34%) of the signal bar's range beyond the high (for a buy) or low (for a sell) of the signal bar to trigger a buy/sell entry. This entry plots the arrow on the chart. We have found requiring this extra move in price eliminates many of the less-desirable signals at the expense of entering the better signals a little later.

WANT TO PURCHASE OR NEED MORE INFORMATION ON McMILLAN VOLATILITY BANDS?

Visit the link below to see purchasing options as well as screenshots of the indicator and how we trade it at McMillan Analysis Corp.

Corrected Moving AverageThis moving average was originally developed by professor Andreas Uhl in 2005 (The paper in German: www.buero-uhl.de). Here is the guy himself: wavelab.at

The strength of the CMA is that the current value of the time series must exceed the current volatility-dependent threshold, so that the filter increases or falls, avoiding false signals in weak phases.

The straight line of CMA can be used for a ranging market identification

[e2] Bitcoin Halving Key & AvwapThis indicator shows a Key Level Support & Resistance level and VWAP that reset on your choice of the Bitcoin's halving date.

Optional Key Calculation Mode:

- Start with first (2012) or second (2016) halving date.

- Start with first and reset on the second (Halving to halving mode)

- Start with every next halving simultaneously (Halving + halving mode)

Labels show the Market Capitalization, total minted Bitcoins and Bitcoin's close price on the halving's date.

A maximum of 5 bands calculated using a factor of the anchored VWAP's standard deviation can be displayed.

Note

- The script is designed for Bitcoin markets only.

- Estimated 3rd halving, script will be updated when next halving occurs.

[e2] EDS Key & AvwapThis indicator shows a Key Level Support & Resistance level and VWAP that resets on your choice of the stock's Earnings , Dividends or Splits release date.

A maximum of 8 bands calculated using a factor of the anchored VWAP's standard deviation can be displayed.

Note

The script is designed for stock-trading only.

Credits

Inspired by timwest , LazyBear 's Earnings S/R Levels and MichelT 's Earnings, Splits, Dividends scripts.

SMU STDEV Candles This script creates a STDEV in a candle format so you can see the Change in a candle format and compare it with the actual price candle.

Is very similar to SMU RSI and SMU ROC. The interesting part is to see the full effect of traditional indicators in a candle format rather than a simple plot format. Very interesting view in SPX. There is a very big clue in the chart as STDEV changed since 2008. Can you figure it out?

Also, try this in lower time frame and you will be amazed how Algo kills volatility after each upside or downside. Fascinating

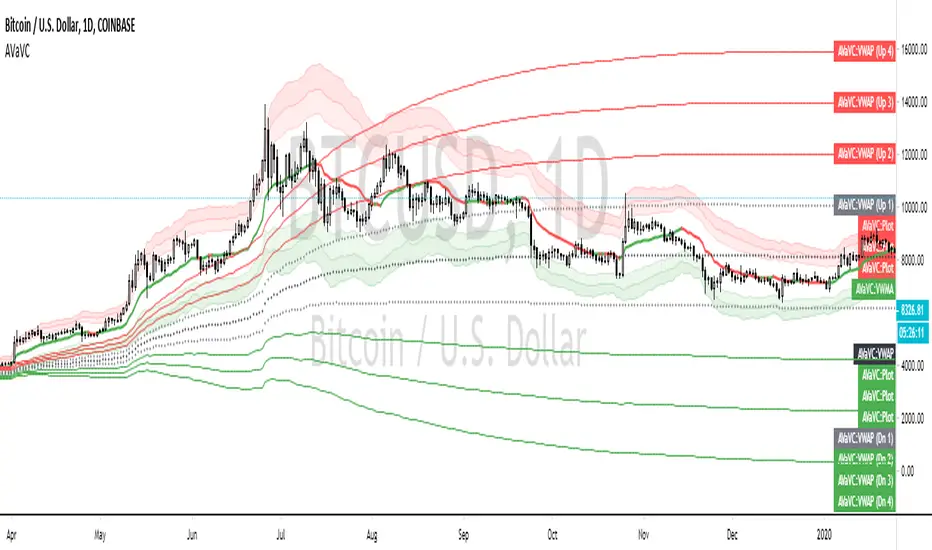

Anchored VWAP w/ Stdev and VWMA CloudThis is a fun little project that allows you to anchor the Volume Weighed Average Price (VWAP) to a specific day and plot up to 4 standard deviations up or down.

I've also added a Volume Weighted Moving Average (VWMA) plot and accompanying cloud to more easily visualize how volume-based momentum affects trends.

Typically, you'll see price respecting the VWMA Cloud and can expect price bounces off of the VWAP standard deviations.

When setting the initial anchor point, it's best to select a day with high volume and volatility.

This idea is not 100% original, but I couldn't find 1) a public script combining the ideas and 2) the correct plotting of the standard deviation via accumulation.

Happy Trading!

FAQ

Why is your script Protected?

Users like to take my open-source code and charge to use it without my permission.

How do I use this to trade?

Add it to your chart and see what stacks up with your current setup. I trade Forex, so what looks bad on my charts might look golden on yours.

How long have you been doing this?

I've been coding for about 8 years and actively trading for 2 years. My degree is in Robotics Engineering and I became obsessed with investing at 22.

How do you trade?

Hurst + SNR + MESA MAMA + ATR + LSTM + Pure Grid. You can't completely code this setup using Pinescript, but if you learn C++ or Python you're there!

Are your returns good?

I average 0.68% every weekday or 22.65% monthly, using the method above.

Can you build my indicator or strategy?

Absolutely! If it hasn't been done before and it improves our community, then consider it done.

But can you build an indicator or strategy for me and only me?

Citing the house rules, I cannot solicit for any purpose. So saying "PM me" would be a grievous violation of said rules, obviously.

Functions Allowing Series As Length - PineCoders FAQ█ WARNING

Improvements to the following Pine built-ins have deprecated the vast majority of this publication's functions, as the built-ins now accept "series int" `length` arguments:

ta.wma()

ta.linreg()

ta.variance()

ta.stdev()

ta.correlation()

NOTE

For an EMA function that allows a "series int" argument for `length`, please see `ema2()` in the ta library by TradingView .

█ ORIGINAL DESCRIPTION

Pinescript requires many of its built-in functions to use a simple int as their period length, which entails the period length cannot vary during the script's execution. These functions allow using a series int or series float for their period length, which means it can vary on each bar.

The functions shared in this script include:

Rolling sum: Sum(src,p)

Simple moving average: Sma(src,p)

Rolling variance: Variance(src,p)

Rolling standard deviation: Stdev(src,p)

Rolling covariance: Covariance(x,y,p)

Rolling correlation: Correlation(x,y,p)

If p is a float then it is rounded to the nearest int .

How to Use the Script

Most of the functions in the script are dependent on the Sma function. The Correlation function uses the Covariance and Stdev functions. Be sure you include all the required functions in your script.

Make sure the series you use as the length argument is greater than 0, else the functions will return na . When using a series as length argument, the following error might appear:

Pine cannot determine the referencing length of a series. Try using max_bars_back in the study or strategy function.

This can be frequent if you use barssince(condition) where condition is a relatively rare event. You can fix it by including max_bars_back=5000 in your study declaration statement as follows:

study("Title",overlay=true,max_bars_back=5000)

Example

The chart shows the Sma , Stdev , Covariance and Correlation functions. The Sma uses the closing price as input and bars as period length where:

bars = barssince(change(security(syminfo.tickerid,"D",close ,lookahead=true)))

The Stdev uses the closing price as input and bars + 9 as period length. The Covariance and Correlation use the closing price as x and bar_index as y , with bars + 9 as period length.

Look first. Then leap.

TD Moon Cycle Standard Deviation Z Score AlertsHas alerts for the TD 9 function, also the black is Z score and blue is STD Dev

Also the moon functionality of Ichimoonku is built into this as well because sometimes I just want to see the cycles of moon with TD9 ; see that script (Ichimoonku) for more info on moon functionality.

Much love

Enjoy

GL HF

xoxo

Snoop

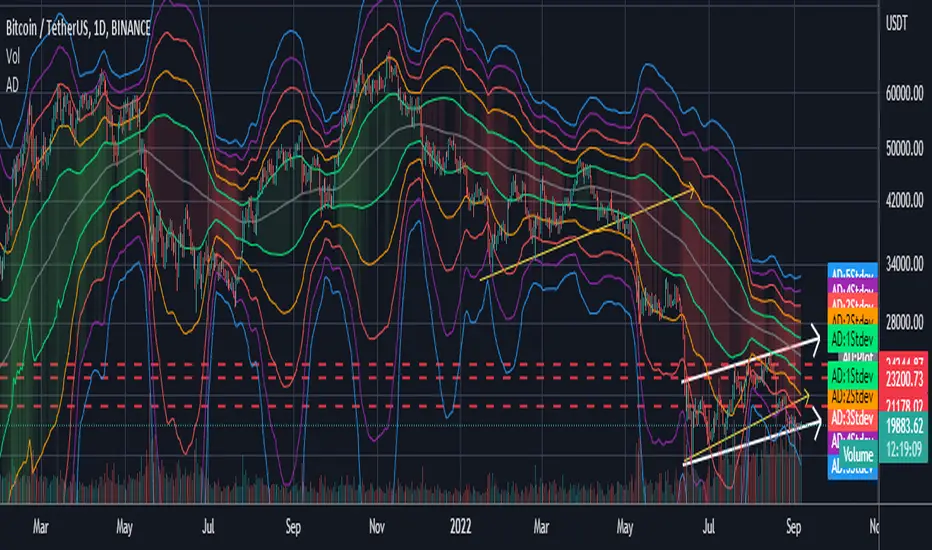

AEONDRIFT {Expected Ranges}Expected Ranges base on AEONDRIFT implementation of Standard Deviation bands.

Note: In no way is this intended as a financial/investment/trading advice. You are responsible for your own investment/trade decisions.

Please PM me for access information.

Function : Bollinger Bands and BBW Squeeze DetectorThis script shows Bollinger Bands function and want to detect Bollinger Band Width Squeeze with a successful, different perspective .

Bollinger Bands : You can specify the Bollinger Bands periods as mutable variables .

Bollinger Band Width Squeeze : First the Bollinger bands width was calculated.The width was then divided into levels using the money flow index.

Thus, the bollinger takes into account the available volume averages when calculating the band width mfi (Money Flow Index).

After this modelling, we can limit and color the lower limit and upper limits just as Relative Strength Index.

We can even put warnings on oversold areas if desired. Let's not forget that we are working with width rather than price.

By design, squeeze areas are defined directly above the Bollinger Bands with coloration. I think it is very practical and looks stylish.

I tried and found it quite successful and wanted to share it with users.

I came up with many ideas when I wrote this system, and I will share them very soon . I hope it will be useful to users and give new ideas.

Best regards.

Standard Deviation - Sum Of The Squares Minus Square Of The SumsIntroduction

The standard deviation measure the dispersion of a data set, in short this metric will tell you if your data is on average closer or farther away from the mean. Its one of the most important tools in statistics and living without it is pretty much impossible, without it you can forget about Bollinger-bands, CCI, and even the LSMA (ouch this hurt) .

Now i don't want to extend myself about the standard deviation since that would require a huge post but i want to show you how to calculate the standard deviation from the stdev pinescript function.

Sum Of The Squares Minus Square Of The Sums

Any metric calculated from a moving average can be classified as "running", this mean that the metric constantly update itself and is not constant, this is why it is better to say "running standard deviation" but its okay. If we use the standard calculation for the standard deviation which would be sqrt(sma(pow(close - sma,2))) we might get something totally different from the stdev function :

In white the pine stdev function and in red the standard calculation of both period 4, its clear that both are not the same, one might try to use the Bessel's correction but that won't do either, this is because most technical analysis tools will calculate the square root of the "Sum Of The Squares Minus Square Of The Sums" method to estimate the standard deviation

Another way is to use :

a = sqrt(sma(pow(close,2),length) - pow(sma(close,length),2))

By returning the difference we might still see some errors :

Nothing relevant of course.

Conclusion

Some of you might already be aware of this but a reminder is always good since it can be confusing to make what can be considered the good standard deviation formula and then have something totally different from the pine function, i hope this post will be useful and that you learned something from it.

Thanks for reading :)

AEONDRIFT with FG & DFG {EMA} indicatorsAEONDRIFT with {EMA} implementation of FUSIONGAPS (FG) and DIFFERENTIAL FUSIONGAPS (DFG) derived indicators.

~JuniAiko

(=^~^=)v~

Check out the other analytical tools that I had published.

AEONDRIFT:

Self-Adjusting RSIThis indicator was originally developed by David Sepiashvili (Stocks & Commodities V. 24:2 (February, 2006): The Self-Adjusting RSI ).

The author presented a technique to adjust the traditional RSI overbought and oversold thresholds so as to ensure that 70-80% of RSI values lie between the two thresholds.

He used two algorithms for adjusting:

Standard Deviation-based

Simple Moving Average-based

Easy and straightforward. But this is not a true way.

Source code on request