Combo Backtest 123 Reversal & Chande Momentum Oscillator This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots Chande Momentum Oscillator. This indicator was

developed by Tushar Chande. A scientist, an inventor, and a respected

trading system developer, Mr. Chande developed the CMO to capture what

he calls "pure momentum". For more definitive information on the CMO and

other indicators we recommend the book The New Technical Trader by Tushar

Chande and Stanley Kroll.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change,

etc. It is most closely related to Welles Wilder`s RSI, yet it differs

in several ways:

- It uses data for both up days and down days in the numerator, thereby

directly measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term

extreme movements in price are not hidden. Once calculated, smoothing

can be applied to the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to

clearly see changes in net momentum using the 0 level. The bounded scale

also allows you to conveniently compare values across different securities.

WARNING:

- For purpose educate only

- This script to change bars colors

Wyszukaj w skryptach "momentum"

Noro's Squeeze Momentum Strategy v1.0This strategy uses 3 different indicators:

1) Squeeze Momentum Indicator (by LazyBear)

2) Color of a candle as filter of signals

3) Candle body size as filter of signals (EMA Body)

Strategy

If Squeeze Momentum Indicator is indicated uptrend both at the same time by a candle red and at the same time more than a third of a body of an average candle - to open long (and to close short)

If Squeeze Momentum Indicator is indicated downtrend both at the same time by a candle green and at the same time more than a third of a body of an average candle - to open short (and to close long)

Relative Momentum Index Backtest The Relative Momentum Index (RMI) was developed by Roger Altman. Impressed

with the Relative Strength Index's sensitivity to the number of look-back

periods, yet frustrated with it's inconsistent oscillation between defined

overbought and oversold levels, Mr. Altman added a momentum component to the RSI.

As mentioned, the RMI is a variation of the RSI indicator. Instead of counting

up and down days from close to close as the RSI does, the RMI counts up and down

days from the close relative to the close x-days ago where x is not necessarily

1 as required by the RSI). So as the name of the indicator reflects, "momentum" is

substituted for "strength".

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

CMO (Chande Momentum Oscillator) Strategy Backtest This indicator plots Chande Momentum Oscillator. This indicator was

developed by Tushar Chande. A scientist, an inventor, and a respected

trading system developer, Mr. Chande developed the CMO to capture what

he calls "pure momentum". For more definitive information on the CMO and

other indicators we recommend the book The New Technical Trader by Tushar

Chande and Stanley Kroll.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change,

etc. It is most closely related to Welles Wilder`s RSI, yet it differs

in several ways:

- It uses data for both up days and down days in the numerator, thereby

directly measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term

extreme movements in price are not hidden. Once calculated, smoothing

can be applied to the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to

clearly see changes in net momentum using the 0 level. The bounded scale

also allows you to conveniently compare values across different securities.

Session Opening Range Breakout (ORBO)This strategy automates a classic Opening Range Breakout (ORBO) approach: it builds a price range for the first minutes after the market opens, then looks for strong breakouts above or below that range to catch early directional moves.

Concept

The idea behind ORBO is simple:

The first minutes after the session open are often highly informative.

Price forms an “opening range” that acts as a mini support/resistance zone.

A clean breakout beyond this zone can lead to high-momentum moves.

This script turns that logic into a fully backtestable strategy in TradingView.

How the strategy works

Opening Range Session

Default session: 09:30–09:50 (exchange time)

During this window, the script tracks:

orHigh → highest high within the session

orLow → lowest low within the session

This forms your Opening Range for the day.

Breakout Logic (after the window ends)

Once the defined session ends:

Long Entry:

If the close crosses above the Opening Range High (orHigh),

→ strategy.entry("OR Long", strategy.long) is triggered.

Short Entry:

If the close crosses below the Opening Range Low (orLow),

→ strategy.entry("OR Short", strategy.short) is triggered.

Only one opening range per day is considered, which keeps the logic clean and easy to interpret.

Daily Reset

At the start of a new trading day, the script resets:

orHigh := na

orLow := na

A fresh Opening Range is then built using the next session’s 09:30–09:50 candles.

This ensures entries are always based on today’s structure, not yesterday’s.

Visuals & Inputs

Inputs:

Opening range session → default: "0930-0950"

Show OR levels → toggle visibility of OR High / Low lines

Fill range body → optional shaded zone between OR High and OR Low

Chart visuals:

A green line marks the Opening Range High.

A red line marks the Opening Range Low.

Optional yellow fill highlights the entire OR zone.

Background shading during the session shows when the range is currently being built.

These visuals make it easy to see:

Where the OR sits relative to current price

How clean / noisy the breakout was

How often price respects or rejects the opening zone

Backtesting & Optimization

Because this is written as a strategy():

You can use TradingView’s Strategy Tester to view:

Win rate

Net profit

Drawdown

Profit factor

Equity curve

Ideas to experiment with:

Change the session window (e.g., 09:15–09:45, 10:00–10:30)

Apply to different:

Markets: indices, FX, crypto, stocks

Timeframes: 1m / 5m / 15m

Add your own:

Stop Loss & Take Profit levels

Time filters (only trade certain days / times)

Volatility filters (e.g., ATR, range size thresholds)

Higher-timeframe trend filter (e.g., only take longs above 200 EMA)

Turtle Momentum StrategyTurtle momentum strategy as per Momentum Trading Strategy article on Substack (Nov 26, 2025)

QQQ Momentum Regime Rider (EMA + VWAP + ADX + Vol Pullback)My strategy catches intraday momentum, has a phenomenal return of 18% annually

Confirmed Momentum QQQ (RSI/MACD Filter)Gemini and Myself,

How This Targets a Higher Win Rate

The key to the win rate increase is the RSI 20/80 filter.

Long Signal: A long entry is now only taken if the trend is up (SMA cross), the MACD is bullish, and the RSI is not overbought (below 80). By only entering when momentum is not yet exhausted, you increase the chance that the price can travel far enough to hit your 4.0 point Take Profit.

Wider SL: The wider Stop Loss of 2.5 points reduces the chance of being stopped out prematurely by routine market movements (whipsaws), which is the number one killer of win rates in high-frequency trading.

After applying these changes, you will need to run the Strategy Tester again to see the new win rate and the new total number of trades.

Would you like me to help you interpret the new Strategy Tester results once you apply these settings?

Zero Lag + Momentum Bias StrategyZero Lag + Momentum Bias Strategy (MTF + Strong MBI + R:R + Partial TP + Alerts)

DNSE VN301!, ADX Momentum StrategyDiscover the tailored Pine Script for trading VN30F1M Futures Contracts intraday.

This strategy applies the Statistical Method (IQR) to break down the components of the ADX, calculating the threshold of "normal" momentum fluctuations in price to identify potential breakouts for entry and exit signals. The script automatically closes all positions by 14:30 to avoid overnight holdings.

www.tradingview.com

Settings & Backtest Results:

- Chart: 30-minute timeframe

- Initial capital: VND 100 million

- Position size: 4 contracts per trade (includes trading fees, excludes tax)

- Backtest period: Sep-2021 to Sep-2025

- Return: over 270% (with 5 ticks slippage)

- Trades executed: 1,000+

- Win rate: ~40%

- Profit factor: 1.2

Default Script Settings:

Calculates the acceleration of changes in the +DI and -DI components of the ADX, using IQR to define "normal" momentum fluctuations (adjustable via Lookback period).

Calculates the difference between each bar’s Open and Close prices, using IQR to define "normal" gaps (adjustable via Lookback period).

Entry & Exit Conditions:

Entry Long: Change in +DI or -DI > Avg IQR Value AND Close Price > Previous Close

Exit Long: (all 4 conditions must be met)

- Change in +DI or -DI > Avg IQR Value

- RSI < Previous RSI

- Close–Open Gap > Avg IQR Gap

- Close Price < Previous Close

Entry Short: Change in +DI or -DI > Avg IQR Value AND Close Price < Previous Close

Exit Short: (all 4 conditions must be met)

- Change in +DI or -DI > Avg IQR Value

- RSI > Previous RSI

- Close–Open Gap > Avg IQR Gap

- Close Price > Previous Close

Disclaimers:

Trading futures contracts carries a high degree of risk, and price movements can be highly volatile. This script is intended as a reference tool only. It should be used by individuals who fully understand futures trading, have assessed their own risk tolerance, and are knowledgeable about the strategy’s logic.

All investment decisions are the sole responsibility of the user. DNSE bears no liability for any potential losses incurred from applying this strategy in real trading. Past performance does not guarantee future results. Please contact us directly if you have specific questions about this script.

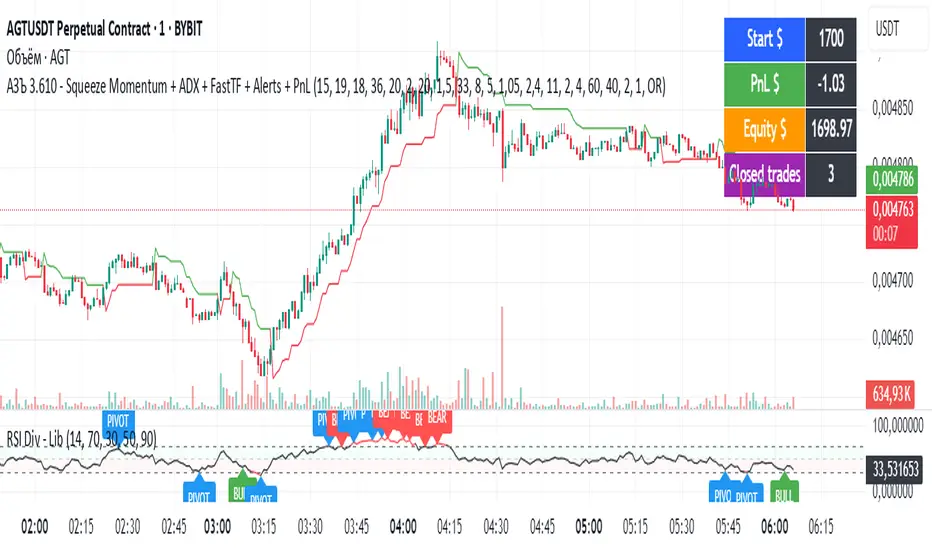

АЗЪ 3.610 - Squeeze Momentum + ADX + FastTF + Alerts + PnLStrata genius squeeze momentum + tester + adx +fast tf

Kaufman Trend Strategy# ✅ Kaufman Trend Strategy – Full Description (Script Publishing Version)

**Kaufman Trend Strategy** is a dynamic trend-following strategy based on Kaufman Filter theory.

It detects real-time trend momentum, reduces noise, and aims to enhance entry accuracy while optimizing risk.

⚠️ _For educational and research purposes only. Past performance does not guarantee future results._

---

## 🎯 Strategy Objective

- Smooth price noise using Kaufman Filter smoothing

- Detect the strength and direction of trends with a normalized oscillator

- Manage profits using multi-stage take-profits and adaptive ATR stop-loss logic

---

## ✨ Key Features

- **Kaufman Filter Trend Detection**

Extracts directional signal using a state space model.

- **Multi-Stage Profit-Taking**

Automatically takes partial profits based on color changes and zero-cross events.

- **ATR-Based Volatility Stops**

Stops adjust based on swing highs/lows and current market volatility.

---

## 📊 Entry & Exit Logic

**Long Entry**

- `trend_strength ≥ 60`

- Green trend signal

- Price above the Kaufman average

**Short Entry**

- `trend_strength ≤ -60`

- Red trend signal

- Price below the Kaufman average

**Exit (Long/Short)**

- Blue trend color → TP1 (50%)

- Oscillator crosses 0 → TP2 (25%)

- Trend weakens → Final exit (25%)

- ATR + swing-based stop loss

---

## 💰 Risk Management

- Initial capital: `$3,000`

- Order size: `$100` per trade (realistic, low-risk sizing)

- Commission: `0.002%`

- Slippage: `2 ticks`

- Pyramiding: `1` max position

- Estimated risk/trade: `~0.1–0.5%` of equity

> ⚠️ _No trade risks more than 5% of equity. This strategy follows TradingView script publishing rules._

---

## ⚙️ Default Parameters

- **1st Take Profit**: 50%

- **2nd Take Profit**: 25%

- **Final Exit**: 25%

- **ATR Period**: 14

- **Swing Lookback**: 10

- **Entry Threshold**: ±60

- **Exit Threshold**: ±40

---

## 📅 Backtest Summary

- **Symbol**: USD/JPY

- **Timeframe**: 1H

- **Date Range**: Jan 3, 2022 – Jun 4, 2025

- **Trades**: 924

- **Win Rate**: 41.67%

- **Profit Factor**: 1.108

- **Net Profit**: +$1,659.29 (+54.56%)

- **Max Drawdown**: -$1,419.73 (-31.87%)

---

## ✅ Summary

This strategy uses Kaufman filtering to detect market direction with reduced lag and increased smoothness.

It’s built with visual clarity and strong trade management, making it practical for both beginners and advanced users.

---

## 📌 Disclaimer

This script is for educational and informational purposes only and should not be considered financial advice.

Use with proper risk controls and always test in a demo environment before live trading.

4 Bar Momentum Reversal strategy█ STRATEGY DESCRIPTION

The "4 Bar Momentum Reversal Strategy" is a mean-reversion strategy designed to identify price reversals following a sustained downward move. It enters a long position when a reversal condition is met and exits when the price shows strength by exceeding the previous bar's high. This strategy is optimized for indices and stocks on the daily timeframe.

█ WHAT IS THE REFERENCE CLOSE?

The Reference Close is the closing price from X bars ago, where X is determined by the Lookback period. Think of it as a moving benchmark that helps the strategy assess whether prices are trending upwards or downwards relative to past performance. For example, if the Lookback is set to 4, the Reference Close is the closing price 4 bars ago (`close `).

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The close price has been lower than the Reference Close for at least `Buy Threshold` consecutive bars. This indicates a sustained downward move, suggesting a potential reversal.

The signal occurs within the specified time window (between `Start Time` and `End Time`).

2. EXIT CONDITION

A Sell Signal is generated when the current closing price exceeds the high of the previous bar (`close > high `). This indicates that the price has shown strength, potentially confirming the reversal and prompting the strategy to exit the position.

█ ADDITIONAL SETTINGS

Buy Threshold: The number of consecutive bearish bars needed to trigger a Buy Signal. Default is 4.

Lookback: The number of bars ago used to calculate the Reference Close. Default is 4.

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed for trending markets with frequent reversals.

It performs best in volatile conditions where price movements are significant.

Backtesting results should be analysed to optimize the Buy Threshold and Lookback parameters for specific instruments.

The Most Powerful TQQQ EMA Crossover Trend Trading StrategyTQQQ EMA Crossover Strategy Indicator

Meta Title: TQQQ EMA Crossover Strategy - Enhance Your Trading with Effective Signals

Meta Description: Discover the TQQQ EMA Crossover Strategy, designed to optimize trading decisions with fast and slow EMA crossovers. Learn how to effectively use this powerful indicator for better trading results.

Key Features

The TQQQ EMA Crossover Strategy is a powerful trading tool that utilizes Exponential Moving Averages (EMAs) to identify potential entry and exit points in the market. Key features of this indicator include:

**Fast and Slow EMAs:** The strategy incorporates two EMAs, allowing traders to capture short-term trends while filtering out market noise.

**Entry and Exit Signals:** Automated signals for entering and exiting trades based on EMA crossovers, enhancing decision-making efficiency.

**Customizable Parameters:** Users can adjust the lengths of the EMAs, as well as take profit and stop loss multipliers, tailoring the strategy to their trading style.

**Visual Indicators:** Clear visual plots of the EMAs and exit points on the chart for easy interpretation.

How It Works

The TQQQ EMA Crossover Strategy operates by calculating two EMAs: a fast EMA (default length of 20) and a slow EMA (default length of 50). The core concept is based on the crossover of these two moving averages:

- When the fast EMA crosses above the slow EMA, it generates a *buy signal*, indicating a potential upward trend.

- Conversely, when the fast EMA crosses below the slow EMA, it produces a *sell signal*, suggesting a potential downward trend.

This method allows traders to capitalize on momentum shifts in the market, providing timely signals for trade execution.

Trading Ideas and Insights

Traders can leverage the TQQQ EMA Crossover Strategy in various market conditions. Here are some insights:

**Scalping Opportunities:** The strategy is particularly effective for scalping in volatile markets, allowing traders to make quick profits on small price movements.

**Swing Trading:** Longer-term traders can use this strategy to identify significant trend reversals and capitalize on larger price swings.

**Risk Management:** By incorporating customizable stop loss and take profit levels, traders can manage their risk effectively while maximizing potential returns.

How Multiple Indicators Work Together

While this strategy primarily relies on EMAs, it can be enhanced by integrating additional indicators such as:

- **Relative Strength Index (RSI):** To confirm overbought or oversold conditions before entering trades.

- **Volume Indicators:** To validate breakout signals, ensuring that price movements are supported by sufficient trading volume.

Combining these indicators provides a more comprehensive view of market dynamics, increasing the reliability of trade signals generated by the EMA crossover.

Unique Aspects

What sets this indicator apart is its simplicity combined with effectiveness. The reliance on EMAs allows for smoother signals compared to traditional moving averages, reducing false signals often associated with choppy price action. Additionally, the ability to customize parameters ensures that traders can adapt the strategy to fit their unique trading styles and risk tolerance.

How to Use

To effectively utilize the TQQQ EMA Crossover Strategy:

1. **Add the Indicator:** Load the script onto your TradingView chart.

2. **Set Parameters:** Adjust the fast and slow EMA lengths according to your trading preferences.

3. **Monitor Signals:** Watch for crossover points; enter trades based on buy/sell signals generated by the indicator.

4. **Implement Risk Management:** Set your stop loss and take profit levels using the provided multipliers.

Regularly review your trading performance and adjust parameters as necessary to optimize results.

Customization

The TQQQ EMA Crossover Strategy allows for extensive customization:

- **EMA Lengths:** Change the default lengths of both fast and slow EMAs to suit different time frames or market conditions.

- **Take Profit/Stop Loss Multipliers:** Adjust these values to align with your risk management strategy. For instance, increasing the take profit multiplier may yield larger gains but could also increase exposure to market fluctuations.

This flexibility makes it suitable for various trading styles, from aggressive scalpers to conservative swing traders.

Conclusion

The TQQQ EMA Crossover Strategy is an effective tool for traders seeking an edge in their trading endeavors. By utilizing fast and slow EMAs, this indicator provides clear entry and exit signals while allowing for customization to fit individual trading strategies. Whether you are a scalper looking for quick profits or a swing trader aiming for larger moves, this indicator offers valuable insights into market trends.

Incorporate it into your TradingView toolkit today and elevate your trading performance!

Elliott's Quadratic Momentum - Strategy [presentTrading]█ Introduction and How It Is Different

The "Elliott's Quadratic Momentum - Strategy" is a unique and innovative approach in the realm of technical trading. This strategy is a fusion of multiple SuperTrend indicators combined with an Elliott Wave-like pattern analysis, offering a comprehensive and dynamic trading tool. It stands apart from conventional strategies by incorporating multiple layers of trend analysis, thereby providing a more robust and nuanced view of market movements.

*Although the script doesn't explicitly analyze Elliott Wave patterns, it employs a wave-like approach by considering multiple SuperTrend indicators. Elliott Wave theory is based on the premise that markets move in predictable wave patterns. While this script doesn't identify specific Elliott Wave structures like impulsive and corrective waves, the sequential checking of trend conditions across multiple SuperTrend indicators mimics a wave-like progression.

BTC 8hr Long/Short Performance

Local Detail

█ Strategy, How It Works: Detailed Explanation

The core of this strategy lies in its multi-tiered approach:

1. Multiple SuperTrend Indicators:

The strategy employs four different SuperTrend indicators, each with unique ATR lengths and multipliers. These indicators offer various perspectives on market trends, ranging from short to long-term views.

By analyzing the convergence of these indicators, the strategy can pinpoint robust entry signals for both long and short positions.

2. Elliott Wave-like Pattern Recognition:

While not directly applying Elliott Wave theory, the strategy takes inspiration from its pattern recognition approach. It looks for alignments in market movements that resemble the characteristic waves of Elliott's theory.

This pattern recognition aids in confirming the signals provided by the SuperTrend indicators, adding an extra layer of validation to the trading signals.

3. Comprehensive Market Analysis:

By combining multiple indicators and pattern analysis, the strategy offers a holistic view of the market. This allows for capturing potential trend reversals and significant market moves early.

█ Trade Direction

The strategy is designed with flexibility in mind, allowing traders to select their preferred trading direction – Long, Short, or Both. This adaptability is key for traders looking to tailor their approach to different market conditions or personal trading styles. The strategy automatically adjusts its logic based on the chosen direction, ensuring that traders are always aligned with their strategic objectives.

█ Usage

To utilize the "Elliott's Quadratic Momentum - Strategy" effectively:

Traders should first determine their trading direction and adjust the SuperTrend settings according to their market analysis and risk appetite.

The strategy is versatile and can be applied across various time frames and asset classes, making it suitable for a wide range of trading scenarios.

It's particularly effective in trending markets, where the alignment of multiple SuperTrend indicators can provide strong trade signals.

█ Default Settings

Trading Direction: Configurable (Long, Short, Both)

SuperTrend Settings:

SuperTrend 1: ATR Length 7, Multiplier 4.0

SuperTrend 2: ATR Length 14, Multiplier 3.618

SuperTrend 3: ATR Length 21, Multiplier 3.5

SuperTrend 4: ATR Length 28, Multiplier 3.382

Additional Settings: Gradient effect for trend visualization, customizable color schemes for upward and downward trends.

FTR, WMA, OBV & RSI StrategyThis Pine Script code is a trading strategy that uses several indicators such as Fisher Transform (FTR), On-Balance Volume (OBV), Relative Strength Index (RSI), and a Weighted Moving Average (WMA). The strategy generates buy and sell signals based on the conditions of these indicators.

The Fisher Transform function is a technical indicator that uses past prices to determine whether the current market is bullish or bearish. The Fisher Transform function takes in four multipliers and a length parameter. The four multipliers are used to calculate four Fisher Transform values, and these values are used in combination to determine if the market is bullish or bearish.

The Weighted Moving Average (WMA) is a technical indicator that smooths out the price data by giving more weight to the most recent prices.

The Relative Strength Index (RSI) is a momentum indicator that measures the strength of a security's price action. The RSI ranges from 0 to 100 and is typically used to identify overbought or oversold conditions in the market.

The On-Balance Volume (OBV) is a technical indicator that uses volume to predict changes in the stock price. OBV values are calculated by adding volume on up days and subtracting volume on down days.

The strategy uses the Fisher Transform values to generate buy and sell signals when all four Fisher Transform values change color. It also uses the WMA to determine if the trend is bullish or bearish, the OBV to confirm the trend, and the RSI to filter out false signals.

The red and green triangular arrows attempt to indicate that the trend is bullish or bearish and should not be traded against in the opposite direction. This helps with my FOMO :)

All comments welcome!

The script should not be relied upon alone, there are no stop loss or take profit filters. The best results have been back-tested using Tradingview on the 45m - 3 hour timeframes.

Simple Momentum and Trend, Fixed PnL Strategy for SPY 1D [SR]This strategy uses an ATR rule to assess momentum and a TSI rule to assess bullish or bearishness

It has a fixed stop at 50 points, and fixed take profit at 300 pips

It provides a very satisfyingly smooth equity line with a max drawdown below 5% and realized profit over 200%

This is the initial version as I work out optimizations and add plots to the chart based on the strategy's actions.

I would love to get the community's feedback and help as I'm new. Not sure how to limit the date range of the backtest to make it more realistic. I'm also not certain how to plot it best.

Crypto momentum strategyThis strategy is based on LazyBear's Squeeze Momentum indicator. It analyzes when the trend in the momentum is shifting, locating the peaks and the valleys, and takes those as sell and buy signals respectively. This is a long strategy, so it also takes into consideration the 50 period Exponential Moving Average to identify upward trends. If the closing price of the candle is above the 50EMA, and the slope of the 50EMA is trending upwards, then the buy signal is executed. If these conditions are not met, the buy signal is ignored.

This strategy works well with crypto trading on the day/week charts.

It has a profit ratio of 4:1 on average, and roughly half of the trades are profitable.

Equal-Length EMA/SMA Crossover Momentum StrategyOverview:

This momentum and trend-following strategy captures the majority of any trending move, and works well on high timeframes.

It uses an equal-period EMA and SMA crossover to detect trend acceleration/deceleration, since an EMA places a greater weight and significance on the most recent data.

This version is optimized for longs, and designed to cut your losses quickly and let your winners run.

To reduce noise and optimize entries, we combined this with an overall trend bias for further confluence.

How it works:

Signals are determined by the crossover of an EMA and SMA of the same length, e.g. EMA-50 and SMA-50.

The overall trend bias is determined using a slower SMA golden/death cross, e.g. SMA-50 and SMA-100.

The signal is stronger when it occurs in confluence with the overall trend bias, e.g. when EMA-50 crosses over SMA-50, while above the SMA-100. This is analogous to only opening long positions in a bull market.

Signal description:

Trend Buy: EMA crosses above SMA, and overall trend bias is bullish. Buying is in confluence with the overall trend bias.

Risky Buy: EMA crosses above SMA, and overall trend bias is bearish. Buying is early, more risky, and not in confluence with the overall trend bias.

Late Buy: SMA crosses above BIAS_SLOW. This gives further confirmation of bullish trend, but signal comes later.

Sell: EMA crosses under SMA.

Strategy entry and exit conditions:

This version enters a Long when "TREND BUY" is signalled.

This version has Sell/Shorts disabled because UP ONLY.

Long entry: Strategy enters Long when EMA is above SMA, while overall trend bias is bullish.

Long exit: Close long when EMA crosses under SMA.

Chande Momentum Strat (Crossover)This is a Chande Momentum strategy that buys and sells when the line crosses the buy and sell lines. Different signal then the other Chande Momentum strategy. In my opinion they both work better at different time frames and possibly commodities.

Squeeze Momentum StrategyJust turned LazyBears' Squeeze Momentum Indicator into a strategy. You can understand how it works and pay credit to LazyBear here: uk (dot) tradingview (dot) com/v/nqQ1DT5a/

Best results seem to be on the 4h chart. Added LazyBear's Volume Weighted Moving Average indicator, which can be used (select in strategy properties) to more selectively long or short if desired. Defaults to using 100% of your initial strategy equity (just my preference), and this cannot be changed without recoding the strategy, but should be easy to do if desired. Added leverage, trade risk, backdate time window and trade type selector inputs.

Happy trading!

Not financial advice.

Combo Backtest 123 Reversal & Dynamic Momentum Index This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots Dynamic Momentum Index indicator. The Dynamic Momentum

Index (DMI) was developed by Tushar Chande and Stanley Kroll. The indicator

is covered in detail in their book The New Technical Trader.

The DMI is identical to Welles Wilder`s Relative Strength Index except the

number of periods is variable rather than fixed. The variability of the time

periods used in the DMI is controlled by the recent volatility of prices.

The more volatile the prices, the more sensitive the DMI is to price changes.

In other words, the DMI will use more time periods during quiet markets, and

less during active markets. The maximum time periods the DMI can reach is 30

and the minimum is 3. This calculation method is similar to the Variable

Moving Average, also developed by Tushar Chande.

The advantage of using a variable length time period when calculating the RSI

is that it overcomes the negative effects of smoothing, which often obscure short-term moves.

The volatility index used in controlling the time periods in the DMI is based

on a calculation using a five period standard deviation and a ten period average

of the standard deviation.

WARNING:

- For purpose educate only

- This script to change bars colors.

simple momentumIt's a simple momentum script:

- go long if A positive closes in a row, exit after B negative closes

- go short if C negative closes in a row, exit after D positive closes