Interval — full-screen verticals + H/L + metrics (robust v6)Specify the start date of the analysis and the end date of the analysis, after which 2 vertical lines will appear, the extremes in this period will be marked, and the percentage of deviations will be shown. Next, you can switch assets and see how they behave over the same time interval.

Cykle

Wickless Heikin Ashi B/S [CHE]Wickless Heikin Ashi B/S \

Purpose.

Wickless Heikin Ashi B/S \ is built to surface only the cleanest momentum turns: it prints a Buy (B) when a bullish Heikin-Ashi candle forms with virtually no lower wick, and a Sell (S) when a bearish Heikin-Ashi candle forms with no upper wick. Optional Lock mode turns these into one-shot signals that hold the regime (bull or bear) until the opposite side appears. The tool can also project dashed horizontal lines from each signal’s price level to help you manage entries, stops, and partial take-profits visually.

How it works.

The indicator computes standard Heikin-Ashi values from your chart’s OHLC. A bar qualifies as bullish if its HA close is at or above its HA open; bearish if below. Then the wick on the relevant side is compared to the bar’s HA range. If that wick is smaller than your selected percentage threshold (plus a tiny tick epsilon to avoid rounding noise), the raw condition is considered “wickless.” Only one side can fire; on the rare occasion both raw conditions would overlap, the bar is ignored to prevent false dual triggers. When Lock is enabled, the first valid signal sets the active regime (background shaded light green for bull, light red for bear) and suppresses further same-side triggers until the opposite side appears, which helps reduce overtrading in chop.

Why wickless?

A missing wick on the “wrong” side of a Heikin-Ashi candle is a strong hint of persistent directional pressure. In practice, this filters out hesitation bars and many mid-bar flips. Traders who prefer entering only when momentum is decisive will find wickless bars useful for timing entries within an established bias.

Visuals you get.

When a valid buy appears, a small triangle “B” is plotted below the bar and a green dashed line can extend to the right from the signal’s HA open price. For sells, a triangle “S” above the bar and a red dashed line do the same. These lines act like immediate, price-anchored references for stop placement and profit scaling; you can shift the anchor left by a chosen number of bars if you prefer the line to start a little earlier for visual alignment.

How to trade it

Establish context first.

Pick a timeframe that matches your style: intraday index or crypto traders often use 5–60 minutes; swing traders might prefer 2–4 hours or daily. The tool is agnostic, but the cleanest results occur when the market is already trending or attempting a fresh breakout.

Entry.

When a B prints, the simplest rule is to enter long at or just after bar close. A conservative variation is to require price to take out the high of the signal bar in the next bar(s). For S, invert the logic: enter short on or after close, or only if price breaks the signal bar’s low.

Stop-loss.

Place the stop beyond the opposite extreme of the signal HA bar (for B: under the HA low; for S: above the HA high). If you prefer a static reference, use the dashed line level (signal HA open) or an ATR buffer (e.g., 1.0–1.5× ATR(14)). The goal is to give the trade enough room that normal noise does not immediately knock you out, while staying small enough to keep the risk contained.

Take-profit and management.

Two pragmatic approaches work well:

R-multiple scaling. Define your initial risk (distance from entry to stop). Scale out at 1R, 2R, and let a runner go toward 3R+ if structure holds.

Trailing logic. Trail behind a short moving average (e.g., EMA 20) or progressive swing points. Many traders also exit on the opposite signal when Lock flips, especially on faster timeframes.

Position sizing.

Keep risk per trade modest and consistent (e.g., 0.25–1% of account). The indicator improves timing; it does not replace risk control.

Settings guidance

Max lower wick for Bull (%) / Max upper wick for Bear (%).

These control how strict “wickless” must be. Tighter values (0.3–1.0%) yield fewer but cleaner signals and are great for strong trends or low-noise instruments. Looser values (1.5–3.0%) catch more setups in volatile markets but admit more noise. If you notice too many borderline bars triggering during high-volatility sessions, increase these thresholds slightly.

Lock (one-shot until opposite).

Keep Lock ON when you want one decisive signal per leg, reducing noise and signal clusters. Turn it OFF only if your plan intentionally scales into trends with multiple entries.

Extended lines & anchor offset.

Leave lines ON to maintain a visual memory of the last trigger levels. These often behave like near-term support/resistance. The offset simply lets you start that line one or more bars earlier if you prefer the look; it does not change the math.

Colors.

Use distinct bull/bear line colors you can read easily on your theme. The default lime/red scheme is chosen for clarity.

Practical examples

Momentum continuation (long).

Price is above your baseline (e.g., EMA 200). A B prints with a tight lower wick filter. Enter on close; stop under the signal HA low. Price pushes up in the next bars; you scale at 1R, trail the rest with EMA 20, and finally exit when a distant S appears or your trail is hit.

Breakout confirmation (short).

Following a range, price breaks down and prints an S with no upper wick. Enter short as the bar closes or on a subsequent break of the signal bar’s low. If the next bar immediately rejects and prints a bullish HA bar, your stop above the signal HA high limits damage. Otherwise, ride the move, harvesting partials as the red dashed line remains unviolated.

Alerts and automation

Set alerts to “Once Per Bar Close” for stability.

Bull ONE-SHOT fires when a valid buy prints (and Lock allows it).

Bear ONE-SHOT fires for sells analogously.

With Lock enabled, you avoid multiple pings in the same direction during a single leg—useful for webhooks or mobile notifications.

Reliability and limitations

The script calculates from completed bars and does not use higher-timeframe look-ahead or repainting tricks. Heikin-Ashi smoothing can lag turns slightly, which is expected and part of the design. In narrow ranges or whipsaw conditions, signals naturally thin out; if you must trade ranges, either tighten the wick filters and keep Lock ON, or add a trend/volatility filter (e.g., trade B only above EMA 200; S only below). Remember: this is an indicator, not a strategy. If you want exact statistics, port the triggers into a strategy and backtest with your chosen entry, stop, and exit rules.

Final notes

Wickless Heikin Ashi B/S \ is a precision timing tool: it waits for decisive, wickless HA bars, provides optional regime locking to reduce noise, and leaves clear price anchors on your chart for disciplined management. Use it with a simple framework—trend bias, fixed risk, and a straightforward exit plan—and it will keep your execution consistent without cluttering the screen or your decision-making.

Disclaimer: This indicator is for educational use and trade assistance only. It is not financial advice. You alone are responsible for your risk and results.

Enhance your trading precision and confidence with Wickless Heikin Ashi B/S ! 🚀

Happy trading

Chervolino

Vertical Lines @ Hour & :45vertical lines at hour and 45 past each hour

when manipulation is most likely to happen

Smart Algogn2 [ChartPrime]Smart Algo indicator with buy/sell signals, optimized for crypto intraday trading.

MEMEC - Meme Coin Market Cap [Da_Prof]For this indicator, the meme coin market cap of the top meme coins are added together to get an estimate of the total meme coin market cap back to the first meme coin, DOGE. Meme.C does this natively on TradingView, but its data only goes back to 19 May 2025. For the indicator, MEME.C supersedes the addition of all the individual meme coins (i.e., from 19 May 2025 to present). The start of MEME.C is labeled on the chart by default, but can be removed by deselecting the label in the settings.

After the creation of DOGE, but before data is available for Meme.C, the highest market cap meme coins are added together to estimate the meme coin market cap. The meme coins used by default are DOGE, SHIB, PEPE, BONK, FLOKI, PENGU, TRUMP, SPX6900, FARTCOIN, WIF, M, BRETT, B, MOG, APE, TURBO, DOG, and POPCAT. Users can select if they wish to disregard any or all of these coins. As of the creation of the indicator, DOGE, SHIB, and PEPE have CRYPTOCAP symbols on TradingView. Therefore, the true market cap of these coins is integrated into this indicator. The other meme coin market caps are estimated using price and the circulating supply as of 09/16/2025. I make no claims as to the indicator's exact accuracy. In fact, it isn't exactly accurate since I utilized the circulating supply on the day it was created, so for meme coins that have a changing supply, the market cap will be at least slightly inaccurate. Use this indicator at your own risk.

To use the indicator, it is best to plot overlayed on the CRYPTOCAP:DOGE chart. You can decide whether or not to hide the DOGE market cap.

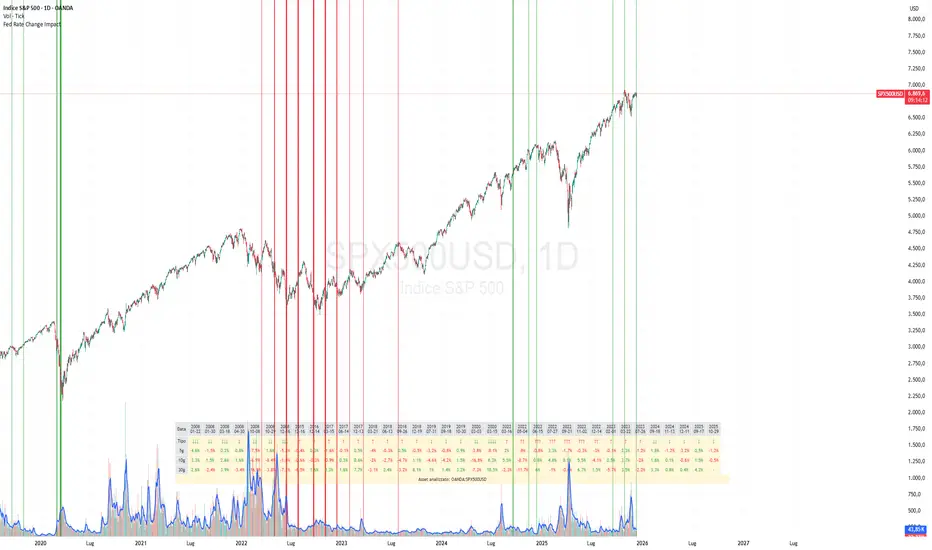

Fed Rate Change Impact📊 Fed Rate Change Impact — Macro Event-Driven Indicator

Fed Rate Change Impact is an advanced indicator designed to analyze the impact of Federal Reserve interest rate changes on financial markets. It integrates event-driven logic with dynamic visualization, percentage diagnostics, and multi-asset selection, offering a clear and customizable view of post-event effects.

🔍 Key Features 📅 Preloaded Fed Events : Includes over 30 historical rate cut (↓) and hike (↑) dates from 2008 to 2024.

📈 Post-Event Analysis : Calculates the percentage change of the selected asset 5, 10, and 30 days after each event.

📌 Vertical Chart Lines : Visually highlights each event directly on the chart, with dynamic coloring (red for hikes, green for cuts).

📋 Diagnostic Table : Displays real-time impact for each event, with color-coded values and a compact layout.

🧠 Interactive Filter: Choose to display only hikes, only cuts, or both.

🧭 Flexible Asset Selection : Analyze the current chart asset, pick from a predefined list, or manually input any ticker via input.symbol().

🎯 Contextual Highlighting : The table highlights the analyzed asset if it matches the active chart symbol.

⚙️ Customizable Parameters lookahead5, lookahead10, lookahead30: Define the time horizon for measuring post-event impact.

eventFilter : Choose which type of events to display.

presetAsset / customAsset : Select or input the asset to analyze.

🧪 Recommended Use Cases Macroeconomic analysis on indices, commodities, crypto, and forex

Studying delayed effects of rate changes on sensitive assets

Building event-driven strategies or diagnostic overlays

Visual backtesting and cross-asset comparison

🧠 Technical Notes The indicator is compatible with overlay=true and works best on Daily timeframe.

The table automatically adapts to the number of events and includes visual padding for improved readability.

All calculations are performed in real time and require no external data.

Emas cryptosmart## General Summary

The Emas cryptosmart indicator is a technical analysis tool designed to provide a clear and comprehensive view of the market trend. It combines a long-term Hull Moving Average (HMA) to establish the overall trend with a faster, more responsive Triple Hull Moving Average (THMA) to identify short-term momentum.

Its primary feature is the dynamic candle coloring, which offers immediate visual cues about price direction, simplifying trading decisions.

## Indicator Components

This indicator is composed of two main lines:

Hull 200 (HMA): The Long-Term Trend Anchor

This line (dynamic lime/red by default) acts as a filter for the main market trend. Due to its 200-period setting, it moves smoothly and establishes the general context.

Uptrend: When the Hull 200 is rising (lime color), it indicates the macro trend is bullish.

Downtrend: When it is falling (red color), the macro trend is bearish.

THMA 55: The Short-Term Momentum Line

This line (dynamic aqua/orange by default) is a Triple Hull Moving Average. It is extremely fast and sensitive to recent price changes, designed to capture immediate momentum.

This is the key line for the candle coloring and for identifying potential entry or exit points.

## How to Interpret It

The primary strategy is to use the Hull 200 to define the direction for your trades and the THMA 55 to fine-tune your timing.

Candle Coloring (Main Signal):

Bullish Candles (default: aqua): When the price closes above the THMA 55, the candles turn to a bullish color. This signals that immediate momentum is positive and can be considered a buy signal or confirmation to stay in a long position.

Bearish Candles (default: orange): When the price closes below the THMA 55, the candles turn to a bearish color. This indicates that immediate momentum is negative, suggesting a potential sell or an exit from a long position.

Confluence Strategy:

The highest-probability signals occur when both moving averages are aligned.

Strong Buy Example: Look for a situation where the Hull 200 is rising (lime color) and wait for the candles to turn bullish as the price crosses above the THMA 55.

Strong Sell Example: Look for a situation where the Hull 200 is falling (red color) and wait for the candles to turn bearish as the price crosses below the THMA 55.

## Key Features

Visual Clarity: Automatic candle coloring eliminates the need to constantly interpret crosses, allowing for a quick read of the market's state.

Dual Perspective: Offers a balanced view by combining a slow trend indicator with a fast momentum indicator.

Reduced Lag: The use of Hull variants minimizes the delay typical of conventional moving averages (SMAs/EMAs).

Fully Customizable: All colors, for both the lines and the candles, can be adjusted in the settings menu to fit your visual style.

oscillator fast cryptosmart (Bands on Scale)The oscillator fast cryptosmart is a high-sensitivity momentum indicator designed to generate signals more rapidly than many traditional oscillators, such as the MACD. It is engineered to detect potential price breakouts by analyzing short-term market cycles.

At its core, the indicator uses a Detrended Price Oscillator (DPO) to remove the longer-term trend from price action, allowing it to focus purely on the underlying momentum cycles. It then calculates dynamic volatility bands around this oscillator line.

Signals are generated when momentum breaks out from a normal range, providing traders with an early warning of a potential acceleration in price.

How to Interpret the Signals:

Buy Signal (Green Vertical Line): A buy signal is generated when the oscillator's main line (yellow) crosses above its upper statistical band. This indicates a sharp surge in positive momentum, suggesting a potential upward move is beginning.

Sell Signal (Red Vertical Line): A sell signal is generated when the oscillator's main line crosses below its lower statistical band. This indicates a significant increase in negative momentum, suggesting a potential downward move is starting.

By focusing on momentum breakouts rather than lagging moving average crossovers, the oscillator fast cryptosmart aims to provide an edge in identifying opportunities in fast-moving markets.

oi + funding oscillator cryptosmartThe oi + funding oscillator cryptosmart is an advanced momentum tool designed to gauge sentiment in the crypto derivatives market. It combines Open Interest (OI) changes with Funding Rates, normalizes them into a single oscillator using a z-score, and identifies potential market extremes.

This provides traders with a powerful visual guide to spot when the market is over-leveraged (overheated) or when a significant deleveraging event has occurred (oversold), signaling potential reversals.

How It Works

Combined Data: The indicator tracks the rate of change in Open Interest and the value of Funding Rates.

Oscillator: It blends these two data points into a single, smoothed oscillator line that moves above and below a zero line.

Extreme Zones:

Overheated (Red Zone): When the oscillator enters the upper critical zone, it suggests excessive greed and high leverage, increasing the risk of a sharp correction (long squeeze). A cross below this level generates a potential sell signal.

Oversold (Green Zone): When the oscillator enters the lower critical zone, it indicates panic, liquidations, and a potential market bottom. A cross above this level generates a potential buy signal.

Trading Strategy & Timeframes

This oscillator is designed to be versatile, but its effectiveness can vary depending on the timeframe.

Optimal Timeframes (1H and 4H): The indicator has shown its highest effectiveness on the 1-hour and 4-hour charts. These timeframes are ideal for capturing significant shifts in market sentiment reflected in OI and funding data, filtering out short-term noise while still providing timely reversal signals.

Lower Timeframes (e.g., 1-min, 5-min, 15-min): On shorter timeframes, the oscillator is still a highly effective tool, but it is best used as a confluence factor within a broader trading system. Due to the increased noise on these charts, it is not recommended to use its signals in isolation. Instead, use it as a final argument for entry. For example, if your primary scalping strategy gives you a buy signal, you can check if the oscillator is also exiting the oversold (green) zone to add a powerful layer of confirmation to your trade.

Fixed Asset TurnoverFixed Asset Turnover (FAT) measures how efficiently a company uses its fixed assets (Property, Plant & Equipment – PPE) to generate revenue. It shows how many times the company “turns over” its fixed assets in a period relative to revenue.

High FAT: Assets are used efficiently; the company generates more revenue per unit of fixed assets.

Low FAT: Fixed assets are underutilized; the company may have invested too much in assets that don’t produce sufficient revenue.

Formula:

Fixed Asset Turnover=Total Revenue/Average Net Fixed Assets

What it tells you:

Indicates asset efficiency in generating sales.

Useful to compare companies within the same industry (because asset intensity varies by sector).

Helps identify whether a company is over-invested in fixed assets or underutilizing them.

How to use it:

Trend Analysis:

Track FAT over time for the same company to see if asset utilization is improving.

Benchmarking:

Compare FAT against competitors or industry averages.

Investment Decisions:

Higher FAT usually suggests more efficient operations, but context matters (e.g., heavy-capital industries naturally have lower FAT).

Front Contract Roll Detector (TV-mapped 1!)This script looks at the security.instrument and finds the current best matching price for the current instrument on a front loaded contract.

This is very useful for detecting when TradingView rolls over contracts and an alert can be put in place for this.

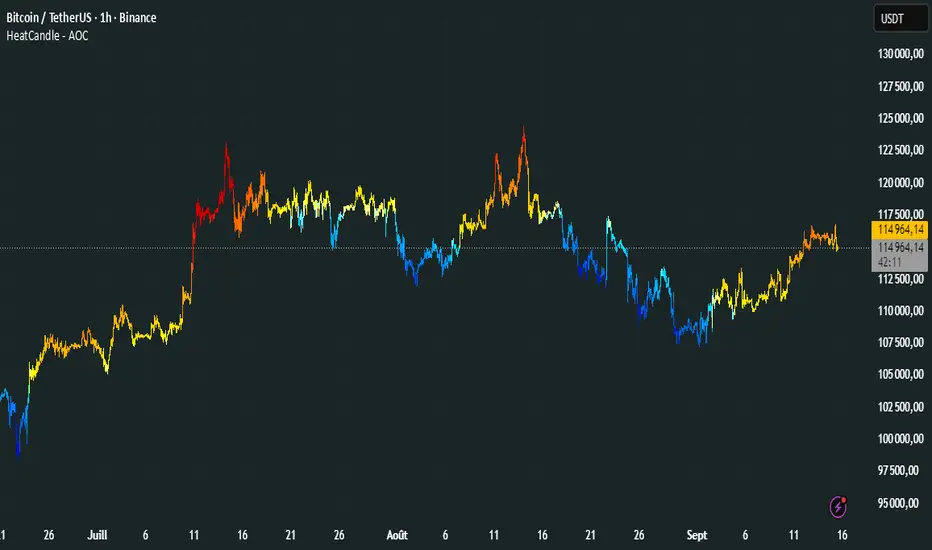

HeatCandleHeatCandle - AOC Indicator

✨ Features

📊 Heat-Map Candles: Colors candles based on the price’s deviation from a Triangular Moving Average (TMA), creating a heat-map effect to visualize price zones.

📏 Zone-Based Coloring: Assigns colors to 20 distinct zones (Z0 to Z19) based on the percentage distance from the TMA, with customizable thresholds.

⚙️ Timeframe-Specific Zones: Tailored zone thresholds for 1-minute, 5-minute, 15-minute, 30-minute, 1-hour, and 4-hour timeframes for precise analysis.

🎨 Customizable Visuals: Gradient color scheme from deep blue (oversold) to red (overbought) for intuitive price movement interpretation.

🛠️ Adjustable Parameters: Configure TMA length and threshold multiplier to fine-tune sensitivity.

🛠️ How to Use

Add to Chart: Apply the "HeatCandle - AOC" indicator on TradingView.

Configure Inputs:

TMA Length: Set the period for the Triangular Moving Average (default: 150).

Threshold Multiplier: Adjust the multiplier to scale zone sensitivity (default: 1.0).

Analyze: Observe colored candles on the chart, where colors indicate the price’s deviation from the TMA:

Dark blue (Z0) indicates strong oversold conditions.

Red (Z19) signals strong overbought conditions.

Track Trends: Use the color zones to identify potential reversals, breakouts, or trend strength based on price distance from the TMA.

🎯 Why Use It?

Visual Clarity: The heat-map candle coloring simplifies identifying overbought/oversold conditions at a glance.

Timeframe Flexibility: Zone thresholds adapt to the selected timeframe, ensuring relevance across short and long-term trading.

Customizable Sensitivity: Adjust TMA length and multiplier to match your trading style or market conditions.

Versatile Analysis: Ideal for scalping, swing trading, or trend analysis when combined with other indicators.

📝 Notes

Ensure sufficient historical data for accurate TMA calculations, especially with longer lengths.

The indicator is most effective on volatile markets where price deviations are significant.

Pair with momentum indicators (e.g., RSI, MACD) or support/resistance levels for enhanced trading strategies.

Happy trading! 🚀📈

Gold H4 First Hour Scalping IndicatorUpdated V4

This Indicator shows how much on an average gold moved in first 4 hour. Then The possible direction in the next h4

AWSA "Level Indicator with ATR" isn't a single, defined indicator but typically refers to a trading strategy or indicator that uses the Average True Range (ATR) to create dynamic levels on a price chart, such as support, resistance, or stop-loss levels. The ATR is a volatility indicator that measures market volatility; when high, it suggests the market has large price swings, and when low, small price swings. By using the ATR value with a multiplier, traders can set price levels that adapt to changing market volatility, providing more objective and dynamic trading signals than fixed-price levels.

Period Separator + Future LinesDescription

This indicator draws vertical separator lines for each selected timeframe (e.g., daily or hourly) and also projects additional separator lines into the future.

It helps traders visually divide the chart into consistent time periods and see upcoming period boundaries in advance.

Features

- Draws vertical lines at the start of each chosen period (daily by default).

- Extends several separator lines into the future so you can anticipate upcoming sessions.

- Fully customizable: color, style (solid/dashed/dotted), line width, and timeframe can be adjusted from the settings.

- Lines are plotted without distorting auto-scaling, so the chart view remains clean.

Use Case

Ideal for intraday and swing traders who want clear visual time markers and the ability to prepare for upcoming trading sessions.

Bitcoin Cycles IndicatorTrack Bitcoin's cyclical price patterns across multiple timeframes with this cycle analysis tool. The indicator automatically identifies cycle lows and highs, marking them with clear visual labels that show cycle day counts and failed cycle detection.

Key Features:

Multi-Time frame Support - Optimized settings for Daily, Weekly, Monthly, and Custom time frames

Cycle Tracking - Identifies and labels cycle lows (green) and highs (red) with day counts

Failed Cycle Detection - Highlights when cycles break below previous lows

Customizable Settings - Adjust cycle lengths, colors, and display options for each timeframe

Info Box - Real-time cycle information display with current cycle day count

Projection Boxes - Visual cycle length projections for better analysis

Perfect for Bitcoin traders and analysts who want to understand market cycles and timing. Works best on Daily charts for short-term cycles and Weekly/Monthly charts for longer-term analysis.

SCTR - AbsoluteIndicator for showing Absolute Value of SCTR - StockCharts Technical Rank.

Uses the calculations from Stock Charts based on the following:

Long-Term Indicators (weighting)

--------------------------------

* Percent above/below 200-day EMA (30%)

* 125-Day Rate-of-Change (30%)

Medium-Term Indicators (weighting)

----------------------------------

* Percent above/below 50-day EMA (15%)

* 20-day Rate-of-Change (15%)

Short-Term Indicators (weighting)

---------------------------------

* 3-day slope of PPO(12,26,9) Histogram/3 (5%)

* 14-day RSI (5%)

First H4 Window Box with PanelThis indicator will explain in detail about the characterstics of first hour open in Gold

Weinstein Stage Analyzer — Table Only (more padding)What it does

This indicator applies Stan Weinstein’s Stage Analysis (Stages 1–4) and presents the result in a clean, compact table only—no lines, labels, or overlays. It shows:

• Previous Stage

• Current Stage (with Early / Mature / Late tag)

• Duration (how long price has been in the current stage, in HTF bars)

• Sentiment (Bullish / Bearish / Balanced / Cautious, derived from stage & maturity)

Timeframe-aware logic

• Weekly charts: classic 30-period MA (Weinstein’s original 30-week concept).

• Daily & Intraday: computed on Daily 150 as a practical daily translation of the 30-week idea.

• Monthly: ~7-period MA (~30 weeks ≈ 7 months).

The stage classification itself is evaluated on this HTF context and then displayed on your active chart.

EMA/SMA toggle

Choose EMA (default) or SMA for the trend line used in stage detection.

How stages are decided (practical rules)

• Stage 2 (Advance): MA rising with price above an upper band.

• Stage 4 (Decline): MA falling with price below a lower band.

• Flat MA zones become Stage 1 (Base) or Stage 3 (Top) depending on the prior trend.

“Maturity” tags (Early/Mature/Late) come from run length and extension beyond the band.

Inputs you can tweak

• MA Type: EMA / SMA

• Price Band (±%) and Slope Threshold to tighten/loosen stage flips

• Maturity thresholds: min/max bars & late-extension %

Notes

• Duration is for the entire current stage (e.g., total time in Stage 4), not just the maturity slice.

• A Top Padding Rows input is included to nudge the table lower if it overlaps your OHLC readout.

Disclaimer

For educational use only. Not financial advice. Always confirm with your own analysis, risk management, and market context.

NX - ICT PD ArraysThis Pine Script indicator identifies and visualizes Fair Value Gaps (FVGs) and Order Blocks (OBs) based on refined price action logic.

FVGs are highlighted when price leaves an imbalance between candles, while Order Blocks are detected using ICT methodology—marking the last opposing candle before a displacement move.

The script dynamically tracks and updates these zones, halting box extension once price interacts with them. Customizable colors and lookback settings allow traders to tailor the display to their strategy.

RSI HIGHs and LOWs MarkerThis indicator marks significant RSI (14) pivot points directly on the price chart.

Red markers above candles highlight confirmed RSI highs where the RSI value exceeded 75 (overbought zone).

Green markers below candles highlight confirmed RSI lows where the RSI value dropped below 25 (oversold zone).

These signals help traders quickly identify potential reversal zones and overextended market conditions without having to monitor the RSI window separately.

First Window Box + Asia Open HourFirst Window Box + Asia Open Hour is an indicator which marks the High and Low of the Asia Open First hour along with the range marking of First Four Hour and its lenght comparing to the length of last 10 days first four hour range.