Smoothed Waddah ATR~~~All Credit to LAZY BEAR for posting the original Script which is an old MT4 indicator.~~~~

No this system does not repaint... if it does let me know. Either the code is wrong or you are using a repainting chart such as renko candles.

*PURPOSE*

This Is an "Enhanced or Smoothed" version of the script that captures the heiken-ashi closing price as its main calculation variable. While using normal bar or line charts. Enhancements integrate trade filters to reduce false signals.

*WHAT TYPE OF TRADING STRATEGY IS THIS?*

This is a Long Only, Trend Trading System. Is intended to be applied to Charts/Timeframes that produce sustainable trends for which ever asset you are trading.

*NOTE OF ADVICE REGARDING SETTINGS*

Settings can be tweaked but I have found that best results come with the given settings. If a chart is too choppy to trade this indicator successfully, it is advised not to change the settings but either find a different timeframe or different asset to apply this strategy to.

TLDR

Indicator measures the change of the MacD (difference between MAC D of given EMA's) and compares it to the difference between the Upper and Lower Bollinger bands. Green bar over trigger line= entry. Red bar over trigger line = close.

*SETTINGS AND INPUTS*

-MacD of HeikenAshi chart (will always be of the Heikenashi chart even when applied to different chart type)

sensitivity = input(150, title='Sensitivity') =range should be (125-175)multiplier so that MacD can be compared to BB

fastLength = input(20, title='MacD FastEMA Length')

slowLength = input(40, title='MacD SlowEMA Length')

-Bollinger Band of currently used price chart type

channelLength = input(20, title='BB Channel Length')

mult = input(1.5, title='BB Stdev Multiplier')

-14 Period RSI Trade Filter (set to 0 to Disable)

RSI14filter = input(40, title='RSI Value trade filter') =only gives entry when RSI is higher than given value

*ABSTRACT & CONCEPT*

TLDR - Indicator measures the change of the MacD (difference between MAC D of given EMA's) and compares it to the difference between the Upper and Lower Bollinger bands. Green bar over trigger line= entry. Red bar over trigger line = close.

Indicator plots -

Bars are the change in the MAC D and the indicator line is the difference in the BB.

When Bars are higher than the indicator line then it is considered a trend "Explosion"

Green Bars are Trend Explosion to the upside, Red Bars are Trend explosion to the downside.

GENERAL DETAIL-

the core calculation is measuring the change in MacD of current candle compared to the MacD of two previous candles.

This value is multiplied by the sensitivy so it can be compared to the change in Bollinger Band Width.

if the MACD change is positive then you get a green/lime bar for that value. If the MacDchange is negative you get a red/orange bar for that value.

and are determined by whether the actual change is increasing in that direction or decreasing. (bars getting taller or bars getting shorter)

Entry signal for long is A positive change in MACD difference (Green bar) that is greater than the change of the bollinger band (orange signal line) AND if the RSI value is above your filter.

Close signal or Trend Stop Warning Signal is given when a Negative MacD Difference (red bar) is greater than the change of the bollinger band (orange Line)

*CONSIDERATIONS AND THOUGHTS*

I have over 150 iterations of this indicator and this is the most consistent and best version of settings and filters I was able to generate. I built this indicator specifically for 3 charts. SPY monthly, QQQ monthly, BTC 3 Day. However this indicator works well on any long term bullish chart. (tech stocks are great) .

Trend trading systems are intended to be homerun hitting, plunge protecting indicators that allow for long legs and expanding volatility. This indicator does this as the trigger line is Dynamic with the expansion and contraction of the bollinger band.

I do not take every signal specifically not the close signals. Instead they more like warnings in ultra bullish environments.

If i had to pair this indicator with any other filter than the RSI, it would be a long term moving average i.e. the 50 week or equivalent for your chart. signals above rising moving averages means that you are trading with an upward trending market.

Hope this helps. Happy trades.

-SnarkyPuppy

Wyszukaj w skryptach "bands"

Z-Score Strategy Backtest The author of this indicator is Veronique Valcu. The z-score (z) for a data

item x measures the distance (in standard deviations StdDev) and direction

of the item from its mean (U):

z = (x-StdDev) / U

A value of zero indicates that the data item x is equal to the mean U, while

positive or negative values show that the data item is above (x>U) or below

(x Values of +2 and -2 show that the data item is two standard deviations

above or below the chosen mean, respectively, and over 95.5% of all data

items are contained within these two horizontal references (see Figure 1).

We substitute x with the closing price C, the mean U with simple moving

average (SMA) of n periods (n), and StdDev with the standard deviation of

closing prices for n periods, the above formula becomes:

Z_score = (C - SMA(n)) / StdDev(C,n)

The z-score indicator is not new, but its use can be seen as a supplement to

Bollinger bands. It offers a simple way to assess the position of the price

vis-a-vis its resistance and support levels expressed by the Bollinger Bands.

In addition, crossings of z-score averages may signal the start or the end of

a tradable trend. Traders may take a step further and look for stronger signals

by identifying common crossing points of z-score, its average, and average of average.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

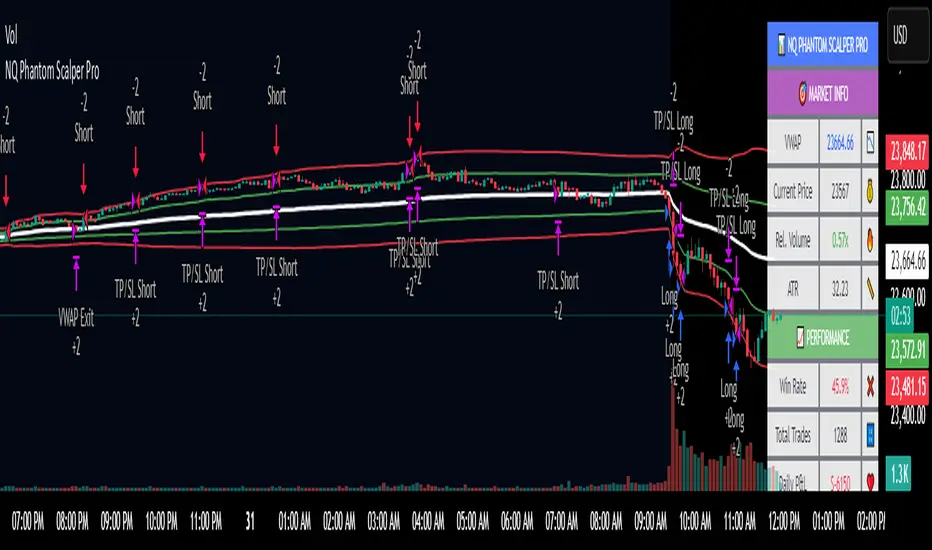

NQ Phantom Scalper Pro# 👻 NQ Phantom Scalper Pro

**Advanced VWAP Mean Reversion Strategy with Volume Confirmation**

## 🎯 Strategy Overview

The NQ Phantom Scalper Pro is a sophisticated mean reversion strategy designed specifically for Nasdaq 100 (NQ) futures scalping. This strategy combines Volume Weighted Average Price (VWAP) bands with intelligent volume spike detection to identify high-probability reversal opportunities during optimal market hours.

## 🔧 Key Features

### VWAP Band System

- **Dynamic VWAP Bands**: Automatically adjusting standard deviation bands based on intraday volatility

- **Multiple Band Levels**: Configurable Band #1 (entry trigger) and Band #2 (profit target reference)

- **Flexible Anchoring**: Choose from Session, Week, Month, Quarter, or Year-based VWAP calculations

### Volume Intelligence

- **Volume Spike Detection**: Only triggers entries when volume exceeds SMA by configurable multiplier

- **Relative Volume Display**: Real-time volume strength indicator in info panel

- **Optional Volume Filter**: Can be disabled for testing alternative setups

### Advanced Time Management

- **12-Hour Format**: User-friendly time inputs (9 AM - 4 PM default)

- **Lunch Filter**: Automatically avoids low-liquidity lunch period (12-2 PM)

- **Visual Time Zones**: Color-coded background for active/inactive periods

- **Market Hours Focus**: Optimized for peak NQ trading sessions

### Smart Risk Management

- **ATR-Based Stops**: Volatility-adjusted stop losses using Average True Range

- **Dual Exit Strategy**: VWAP mean reversion + fixed profit targets

- **Adjustable Risk-Reward**: Configurable target ratio to opposite VWAP band

- **Position Sizing**: Percentage-based equity allocation

### Optional Trend Filter

- **EMA Trend Alignment**: Optional trend filter to avoid counter-trend trades

- **Configurable Period**: Adjustable EMA length for trend determination

- **Toggle Functionality**: Enable/disable based on market conditions

## 📊 How It Works

### Entry Logic

**Long Entries**: Triggered when price touches lower VWAP band + volume spike during active hours

**Short Entries**: Triggered when price touches upper VWAP band + volume spike during active hours

### Exit Strategy

1. **VWAP Mean Reversion**: Early exit when price returns to VWAP center line

2. **Profit Target**: Fixed target based on percentage to opposite VWAP band

3. **Stop Loss**: ATR-based protective stop

### Visual Elements

- **VWAP Center Line**: Blue line showing volume-weighted fair value

- **Green Bands**: Entry trigger levels (Band #1)

- **Red Bands**: Extended levels for target reference (Band #2)

- **Orange EMA**: Trend filter line (when enabled)

- **Background Colors**: Yellow (lunch), Gray (after hours), Clear (active trading)

- **Info Panel**: Real-time metrics display

## ⚙️ Recommended Settings

### Timeframes

- **Primary**: 1-5 minute charts for scalping

- **Validation**: Test on 15-minute for swing applications

### Market Conditions

- **Best Performance**: Ranging/choppy markets with good volume

- **Trend Markets**: Enable trend filter to avoid counter-trend trades

- **High Volatility**: Increase ATR multiplier for stops

### Session Optimization

- **Pre-Market**: Generally avoided (low volume)

- **Morning Session**: 9:30 AM - 12:00 PM (high activity)

- **Lunch Period**: 12:00 PM - 2:00 PM (filtered by default)

- **Afternoon Session**: 2:00 PM - 4:00 PM (good volume)

- **After Hours**: Generally avoided (wide spreads)

## ⚠️ Risk Disclaimer

This strategy is for educational purposes only and does not constitute financial advice. Past performance does not guarantee future results. Trading futures involves substantial risk of loss and is not suitable for all investors. Users should:

- Thoroughly backtest on historical data

- Start with small position sizes

- Understand the risks of leveraged trading

- Consider transaction costs and slippage

- Never risk more than you can afford to lose

## 📈 Performance Tips

1. **Volume Threshold**: Adjust volume multiplier based on average NQ volume patterns

2. **Band Sensitivity**: Modify band multipliers for different volatility regimes

3. **Time Filters**: Customize trading hours based on your timezone and preferences

4. **Trend Alignment**: Use trend filter during strong directional markets

5. **Risk Management**: Always maintain consistent position sizing and risk parameters

**Version**: 6.0 Compatible

**Asset**: Optimized for NASDAQ 100 Futures (NQ)

**Style**: Mean Reversion Scalping

**Frequency**: High-Frequency Trading Ready

Ticker Pulse Meter + Fear EKG StrategyDescription

The Ticker Pulse Meter + Fear EKG Strategy is a technical analysis tool designed to identify potential entry and exit points for long positions based on price action relative to historical ranges. It combines two proprietary indicators: the Ticker Pulse Meter (TPM), which measures price positioning within short- and long-term ranges, and the Fear EKG, a VIX-inspired oscillator that detects extreme market conditions. The strategy is non-repainting, ensuring signals are generated only on confirmed bars to avoid false positives. Visual enhancements, such as optional moving averages and Bollinger Bands, provide additional context but are not core to the strategy's logic. This script is suitable for traders seeking a systematic approach to capturing momentum and mean-reversion opportunities.

How It Works

The strategy evaluates price action using two key metrics:

Ticker Pulse Meter (TPM): Measures the current price's position within short- and long-term price ranges to identify momentum or overextension.

Fear EKG: Detects extreme selling pressure (akin to "irrational selling") by analyzing price behavior relative to historical lows, inspired by volatility-based oscillators.

Entry signals are generated when specific conditions align, indicating potential buying opportunities. Exits are triggered based on predefined thresholds or partial position closures to manage risk. The strategy supports customizable lookback periods, thresholds, and exit percentages, allowing flexibility across different markets and timeframes. Visual cues, such as entry/exit dots and a position table, enhance usability, while optional overlays like moving averages and Bollinger Bands provide additional chart context.

Calculation Overview

Price Range Calculations:

Short-Term Range: Uses the lowest low (min_price_short) and highest high (max_price_short) over a user-defined short lookback period (lookback_short, default 50 bars).

Long-Term Range: Uses the lowest low (min_price_long) and highest high (max_price_long) over a user-defined long lookback period (lookback_long, default 200 bars).

Percentage Metrics:

pct_above_short: Percentage of the current close above the short-term range.

pct_above_long: Percentage of the current close above the long-term range.

Combined metrics (pct_above_long_above_short, pct_below_long_below_short) normalize price action for signal generation.

Signal Generation:

Long Entry (TPM): Triggered when pct_above_long_above_short crosses above a user-defined threshold (entryThresholdhigh, default 20) and pct_below_long_below_short is below a low threshold (entryThresholdlow, default 40).

Long Entry (Fear EKG): Triggered when pct_below_long_below_short crosses under an extreme threshold (orangeEntryThreshold, default 95), indicating potential oversold conditions.

Long Exit: Triggered when pct_above_long_above_short crosses under a profit-taking level (profitTake, default 95). Partial exits are supported via a user-defined percentage (exitAmt, default 50%).

Non-Repainting Logic: Signals are calculated using data from the previous bar ( ) and only plotted on confirmed bars (barstate.isconfirmed), ensuring reliability.

Visual Enhancements:

Optional moving averages (SMA, EMA, WMA, VWMA, or SMMA) and Bollinger Bands can be enabled for trend context.

A position table displays real-time metrics, including open positions, Fear EKG, and Ticker Pulse values.

Background highlights mark periods of high selling pressure.

Entry Rules

Long Entry:

TPM Signal: Occurs when the price shows strength relative to both short- and long-term ranges, as defined by pct_above_long_above_short crossing above entryThresholdhigh and pct_below_long_below_short below entryThresholdlow.

Fear EKG Signal: Triggered by extreme selling pressure, when pct_below_long_below_short crosses under orangeEntryThreshold. This signal is optional and can be toggled via enable_yellow_signals.

Entries are executed only on confirmed bars to prevent repainting.

Exit Rules

Long Exit: Triggered when pct_above_long_above_short crosses under profitTake.

Partial exits are supported, with the strategy closing a user-defined percentage of the position (exitAmt) up to four times per position (exit_count limit).

Exits can be disabled or adjusted via enable_short_signal and exitPercentage settings.

Inputs

Backtest Start Date: Defines the start of the backtesting period (default: Jan 1, 2017).

Lookback Periods: Short (lookback_short, default 50) and long (lookback_long, default 200) periods for range calculations.

Resolution: Timeframe for price data (default: Daily).

Entry/Exit Thresholds:

entryThresholdhigh (default 20): Threshold for TPM entry.

entryThresholdlow (default 40): Secondary condition for TPM entry.

orangeEntryThreshold (default 95): Threshold for Fear EKG entry.

profitTake (default 95): Exit threshold.

exitAmt (default 50%): Percentage of position to exit.

Visual Options: Toggle for moving averages and Bollinger Bands, with customizable types and lengths.

Notes

The strategy is designed to work across various timeframes and assets, with data sourced from user-selected resolutions (i_res).

Alerts are included for long entry and exit signals, facilitating integration with TradingView's alert system.

The script avoids repainting by using confirmed bar data and shifted calculations ( ).

Visual elements (e.g., SMA, Bollinger Bands) are inspired by standard Pine Script practices and are optional, not integral to the core logic.

Usage

Apply the script to a chart, adjust input settings to suit your trading style, and use the visual cues (entry/exit dots, position table) to monitor signals. Enable alerts for real-time notifications.

Designed to work best on Daily timeframe.

Anomalous Holonomy Field Theory🌌 Anomalous Holonomy Field Theory (AHFT) - Revolutionary Quantum Market Analysis

Where Theoretical Physics Meets Trading Reality

A Groundbreaking Synthesis of Differential Geometry, Quantum Field Theory, and Market Dynamics

🔬 THEORETICAL FOUNDATION - THE MATHEMATICS OF MARKET REALITY

The Anomalous Holonomy Field Theory represents an unprecedented fusion of advanced mathematical physics with practical market analysis. This isn't merely another indicator repackaging old concepts - it's a fundamentally new lens through which to view and understand market structure .

1. HOLONOMY GROUPS (Differential Geometry)

In differential geometry, holonomy measures how vectors change when parallel transported around closed loops in curved space. Applied to markets:

Mathematical Formula:

H = P exp(∮_C A_μ dx^μ)

Where:

P = Path ordering operator

A_μ = Market connection (price-volume gauge field)

C = Closed price path

Market Implementation:

The holonomy calculation measures how price "remembers" its journey through market space. When price returns to a previous level, the holonomy captures what has changed in the market's internal geometry. This reveals:

Hidden curvature in the market manifold

Topological obstructions to arbitrage

Geometric phase accumulated during price cycles

2. ANOMALY DETECTION (Quantum Field Theory)

Drawing from the Adler-Bell-Jackiw anomaly in quantum field theory:

Mathematical Formula:

∂_μ j^μ = (e²/16π²)F_μν F̃^μν

Where:

j^μ = Market current (order flow)

F_μν = Field strength tensor (volatility structure)

F̃^μν = Dual field strength

Market Application:

Anomalies represent symmetry breaking in market structure - moments when normal patterns fail and extraordinary opportunities arise. The system detects:

Spontaneous symmetry breaking (trend reversals)

Vacuum fluctuations (volatility clusters)

Non-perturbative effects (market crashes/melt-ups)

3. GAUGE THEORY (Theoretical Physics)

Markets exhibit gauge invariance - the fundamental physics remains unchanged under certain transformations:

Mathematical Formula:

A'_μ = A_μ + ∂_μΛ

This ensures our signals are gauge-invariant observables , immune to arbitrary market "coordinate changes" like gaps or reference point shifts.

4. TOPOLOGICAL DATA ANALYSIS

Using persistent homology and Morse theory:

Mathematical Formula:

β_k = dim(H_k(X))

Where β_k are the Betti numbers describing topological features that persist across scales.

🎯 REVOLUTIONARY SIGNAL CONFIGURATION

Signal Sensitivity (0.5-12.0, default 2.5)

Controls the responsiveness of holonomy field calculations to market conditions. This parameter directly affects the threshold for detecting quantum phase transitions in price action.

Optimization by Timeframe:

Scalping (1-5min): 1.5-3.0 for rapid signal generation

Day Trading (15min-1H): 2.5-5.0 for balanced sensitivity

Swing Trading (4H-1D): 5.0-8.0 for high-quality signals only

Score Amplifier (10-200, default 50)

Scales the raw holonomy field strength to produce meaningful signal values. Higher values amplify weak signals in low-volatility environments.

Signal Confirmation Toggle

When enabled, enforces additional technical filters (EMA and RSI alignment) to reduce false positives. Essential for conservative strategies.

Minimum Bars Between Signals (1-20, default 5)

Prevents overtrading by enforcing quantum decoherence time between signals. Higher values reduce whipsaws in choppy markets.

👑 ELITE EXECUTION SYSTEM

Execution Modes:

Conservative Mode:

Stricter signal criteria

Higher quality thresholds

Ideal for stable market conditions

Adaptive Mode:

Self-adjusting parameters

Balances signal frequency with quality

Recommended for most traders

Aggressive Mode:

Maximum signal sensitivity

Captures rapid market moves

Best for experienced traders in volatile conditions

Dynamic Position Sizing:

When enabled, the system scales position size based on:

Holonomy field strength

Current volatility regime

Recent performance metrics

Advanced Exit Management:

Implements trailing stops based on ATR and signal strength, with mode-specific multipliers for optimal profit capture.

🧠 ADAPTIVE INTELLIGENCE ENGINE

Self-Learning System:

The strategy analyzes recent trade outcomes and adjusts:

Risk multipliers based on win/loss ratios

Signal weights according to performance

Market regime detection for environmental adaptation

Learning Speed (0.05-0.3):

Controls adaptation rate. Higher values = faster learning but potentially unstable. Lower values = stable but slower adaptation.

Performance Window (20-100 trades):

Number of recent trades analyzed for adaptation. Longer windows provide stability, shorter windows increase responsiveness.

🎨 REVOLUTIONARY VISUAL SYSTEM

1. Holonomy Field Visualization

What it shows: Multi-layer quantum field bands representing market resonance zones

How to interpret:

Blue/Purple bands = Primary holonomy field (strongest resonance)

Band width = Field strength and volatility

Price within bands = Normal quantum state

Price breaking bands = Quantum phase transition

Trading application: Trade reversals at band extremes, breakouts on band violations with strong signals.

2. Quantum Portals

What they show: Entry signals with recursive depth patterns indicating momentum strength

How to interpret:

Upward triangles with portals = Long entry signals

Downward triangles with portals = Short entry signals

Portal depth = Signal strength and expected momentum

Color intensity = Probability of success

Trading application: Enter on portal appearance, with size proportional to portal depth.

3. Field Resonance Bands

What they show: Fibonacci-based harmonic price zones where quantum resonance occurs

How to interpret:

Dotted circles = Minor resonance levels

Solid circles = Major resonance levels

Color coding = Resonance strength

Trading application: Use as dynamic support/resistance, expect reactions at resonance zones.

4. Anomaly Detection Grid

What it shows: Fractal-based support/resistance with anomaly strength calculations

How to interpret:

Triple-layer lines = Major fractal levels with high anomaly probability

Labels show: Period (H8-H55), Price, and Anomaly strength (φ)

⚡ symbol = Extreme anomaly detected

● symbol = Strong anomaly

○ symbol = Normal conditions

Trading application: Expect major moves when price approaches high anomaly levels. Use for precise entry/exit timing.

5. Phase Space Flow

What it shows: Background heatmap revealing market topology and energy

How to interpret:

Dark background = Low market energy, range-bound

Purple glow = Building energy, trend developing

Bright intensity = High energy, strong directional move

Trading application: Trade aggressively in bright phases, reduce activity in dark phases.

📊 PROFESSIONAL DASHBOARD METRICS

Holonomy Field Strength (-100 to +100)

What it measures: The Wilson loop integral around price paths

>70: Strong positive curvature (bullish vortex)

<-70: Strong negative curvature (bearish collapse)

Near 0: Flat connection (range-bound)

Anomaly Level (0-100%)

What it measures: Quantum vacuum expectation deviation

>70%: Major anomaly (phase transition imminent)

30-70%: Moderate anomaly (elevated volatility)

<30%: Normal quantum fluctuations

Quantum State (-1, 0, +1)

What it measures: Market wave function collapse

+1: Bullish eigenstate |↑⟩

0: Superposition (uncertain)

-1: Bearish eigenstate |↓⟩

Signal Quality Ratings

LEGENDARY: All quantum fields aligned, maximum probability

EXCEPTIONAL: Strong holonomy with anomaly confirmation

STRONG: Good field strength, moderate anomaly

MODERATE: Decent signals, some uncertainty

WEAK: Minimal edge, high quantum noise

Performance Metrics

Win Rate: Rolling performance with emoji indicators

Daily P&L: Real-time profit tracking

Adaptive Risk: Current risk multiplier status

Market Regime: Bull/Bear classification

🏆 WHY THIS CHANGES EVERYTHING

Traditional technical analysis operates on 100-year-old principles - moving averages, support/resistance, and pattern recognition. These work because many traders use them, creating self-fulfilling prophecies.

AHFT transcends this limitation by analyzing markets through the lens of fundamental physics:

Markets have geometry - The holonomy calculations reveal this hidden structure

Price has memory - The geometric phase captures path-dependent effects

Anomalies are predictable - Quantum field theory identifies symmetry breaking

Everything is connected - Gauge theory unifies disparate market phenomena

This isn't just a new indicator - it's a new way of thinking about markets . Just as Einstein's relativity revolutionized physics beyond Newton's mechanics, AHFT revolutionizes technical analysis beyond traditional methods.

🔧 OPTIMAL SETTINGS FOR MNQ 10-MINUTE

For the Micro E-mini Nasdaq-100 on 10-minute timeframe:

Signal Sensitivity: 2.5-3.5

Score Amplifier: 50-70

Execution Mode: Adaptive

Min Bars Between: 3-5

Theme: Quantum Nebula or Dark Matter

💭 THE JOURNEY - FROM IMPOSSIBLE THEORY TO TRADING REALITY

Creating AHFT was a mathematical odyssey that pushed the boundaries of what's possible in Pine Script. The journey began with a seemingly impossible question: Could the profound mathematical structures of theoretical physics be translated into practical trading tools?

The Theoretical Challenge:

Months were spent diving deep into differential geometry textbooks, studying the works of Chern, Simons, and Witten. The mathematics of holonomy groups and gauge theory had never been applied to financial markets. Translating abstract mathematical concepts like parallel transport and fiber bundles into discrete price calculations required novel approaches and countless failed attempts.

The Computational Nightmare:

Pine Script wasn't designed for quantum field theory calculations. Implementing the Wilson loop integral, managing complex array structures for anomaly detection, and maintaining computational efficiency while calculating geometric phases pushed the language to its limits. There were moments when the entire project seemed impossible - the script would timeout, produce nonsensical results, or simply refuse to compile.

The Breakthrough Moments:

After countless sleepless nights and thousands of lines of code, breakthrough came through elegant simplifications. The realization that market anomalies follow patterns similar to quantum vacuum fluctuations led to the revolutionary anomaly detection system. The discovery that price paths exhibit holonomic memory unlocked the geometric phase calculations.

The Visual Revolution:

Creating visualizations that could represent 4-dimensional quantum fields on a 2D chart required innovative approaches. The multi-layer holonomy field, recursive quantum portals, and phase space flow representations went through dozens of iterations before achieving the perfect balance of beauty and functionality.

The Balancing Act:

Perhaps the greatest challenge was maintaining mathematical rigor while ensuring practical trading utility. Every formula had to be both theoretically sound and computationally efficient. Every visual had to be both aesthetically pleasing and information-rich.

The result is more than a strategy - it's a synthesis of pure mathematics and market reality that reveals the hidden order within apparent chaos.

📚 INTEGRATED DOCUMENTATION

Once applied to your chart, AHFT includes comprehensive tooltips on every input parameter. The source code contains detailed explanations of the mathematical theory, practical applications, and optimization guidelines. This published description provides the overview - the indicator itself is a complete educational resource.

⚠️ RISK DISCLAIMER

While AHFT employs advanced mathematical models derived from theoretical physics, markets remain inherently unpredictable. No mathematical model, regardless of sophistication, can guarantee future results. This strategy uses realistic commission ($0.62 per contract) and slippage (1 tick) in all calculations. Past performance does not guarantee future results. Always use appropriate risk management and never risk more than you can afford to lose.

🌟 CONCLUSION

The Anomalous Holonomy Field Theory represents a quantum leap in technical analysis - literally. By applying the profound insights of differential geometry, quantum field theory, and gauge theory to market analysis, AHFT reveals structure and opportunities invisible to traditional methods.

From the holonomy calculations that capture market memory to the anomaly detection that identifies phase transitions, from the adaptive intelligence that learns and evolves to the stunning visualizations that make the invisible visible, every component works in mathematical harmony.

This is more than a trading strategy. It's a new lens through which to view market reality.

Trade with the precision of physics. Trade with the power of mathematics. Trade with AHFT.

I hope this serves as a good replacement for Quantum Edge Pro - Adaptive AI until I'm able to fix it.

— Dskyz, Trade with insight. Trade with anticipation.

Gradient Trend Filter STRATEGY [ChartPrime/PineIndicators]This strategy is based on the Gradient Trend Filter indicator developed by ChartPrime. Full credit for the concept and indicator goes to ChartPrime.

The Gradient Trend Filter Strategy is designed to execute trades based on the trend analysis and filtering system provided by the Gradient Trend Filter indicator. It integrates a noise-filtered trend detection system with a color-gradient visualization, helping traders identify trend strength, momentum shifts, and potential reversals.

How the Gradient Trend Filter Strategy Works

1. Noise Filtering for Smoother Trends

To reduce false signals caused by market noise, the strategy applies a three-stage smoothing function to the source price. This function ensures that trend shifts are detected more accurately, minimizing unnecessary trade entries and exits.

The filter is based on an Exponential Moving Average (EMA)-style smoothing technique.

It processes price data in three successive passes, refining the trend signal before generating trade entries.

This filtering technique helps eliminate minor fluctuations and highlights the true underlying trend.

2. Multi-Layered Trend Bands & Color-Based Trend Visualization

The Gradient Trend Filter constructs multiple trend bands around the filtered trend line, acting as dynamic support and resistance zones.

The mid-line changes color based on the trend direction:

Green for uptrends

Red for downtrends

A gradient cloud is formed around the trend line, dynamically shifting colors to provide early warning signals of trend reversals.

The outer bands function as potential support and resistance, helping traders determine stop-loss and take-profit zones.

Visualization elements used in this strategy:

Trend Filter Line → Changes color between green (bullish) and red (bearish).

Trend Cloud → Dynamically adjusts color based on trend strength.

Orange Markers → Appear when a trend shift is confirmed.

Trade Entry & Exit Conditions

This strategy automatically enters trades based on confirmed trend shifts detected by the Gradient Trend Filter.

1. Trade Entry Rules

Long Entry:

A bullish trend shift is detected (trend direction changes to green).

The filtered trend value crosses above zero, confirming upward momentum.

The strategy enters a long position.

Short Entry:

A bearish trend shift is detected (trend direction changes to red).

The filtered trend value crosses below zero, confirming downward momentum.

The strategy enters a short position.

2. Trade Exit Rules

Closing a Long Position:

If a bearish trend shift occurs, the strategy closes the long position.

Closing a Short Position:

If a bullish trend shift occurs, the strategy closes the short position.

The trend shift markers (orange diamonds) act as a confirmation signal, reinforcing the validity of trade entries and exits.

Customization Options

This strategy allows traders to adjust key parameters for flexibility in different market conditions:

Trade Direction: Choose between Long Only, Short Only, or Long & Short .

Trend Length: Modify the length of the smoothing function to adapt to different timeframes.

Line Width & Colors: Customize the visual appearance of trend lines and cloud colors.

Performance Table: Enable or disable the equity performance table that tracks historical trade results.

Performance Tracking & Reporting

A built-in performance table is included to monitor monthly and yearly trading performance.

The table calculates monthly percentage returns, displaying them in a structured format.

Color-coded values highlight profitable months (blue) and losing months (red).

Tracks yearly cumulative performance to assess long-term strategy effectiveness.

Traders can use this feature to evaluate historical performance trends and optimize their strategy settings accordingly.

How to Use This Strategy

Identify Trend Strength & Reversals:

Use the trend line and cloud color changes to assess trend strength and detect potential reversals.

Monitor Momentum Shifts:

Pay attention to gradient cloud color shifts, as they often appear before the trend line changes color.

This can indicate early momentum weakening or strengthening.

Act on Trend Shift Markers:

Use orange diamonds as confirmation signals for trend shifts and trade entry/exit points.

Utilize Cloud Bands as Support/Resistance:

The outer bands of the cloud serve as dynamic support and resistance, helping with stop-loss and take-profit placement.

Considerations & Limitations

Trend Lag: Since the strategy applies a smoothing function, entries may be slightly delayed compared to raw price action.

Volatile Market Conditions: In high-volatility markets, trend shifts may occur more frequently, leading to higher trade frequency.

Optimized for Trend Trading: This strategy is best suited for trending markets and may produce false signals in sideways (ranging) conditions.

Conclusion

The Gradient Trend Filter Strategy is a trend-following system based on the Gradient Trend Filter indicator by ChartPrime. It integrates noise filtering, trend visualization, and gradient-based color shifts to help traders identify strong market trends and potential reversals.

By combining trend filtering with a multi-layered cloud system, the strategy provides clear trade signals while minimizing noise. Traders can use this strategy for long-term trend trading, momentum shifts, and support/resistance-based decision-making.

This strategy is a fully automated system that allows traders to execute long, short, or both directions, with customizable settings to adapt to different market conditions.

Credit for the original concept and indicator goes to ChartPrime.

Advanced Gold Scalping Strategy with RSI Divergence# Advanced Gold Scalping Strategy with RSI Divergence

## Overview

This Pine Script implements an advanced scalping strategy for gold (XAUUSD) trading, primarily designed for the 1-minute timeframe. The strategy utilizes the Relative Strength Index (RSI) indicator along with its moving average to identify potential trade setups based on divergences between price action and RSI movements.

## Key Components

### 1. RSI Calculation

- Uses a customizable RSI length (default: 60)

- Allows selection of the source for RSI calculation (default: close price)

### 2. Moving Average of RSI

- Supports multiple MA types: SMA, EMA, SMMA (RMA), WMA, VWMA, and Bollinger Bands

- Customizable MA length (default: 3)

- Option to display Bollinger Bands with adjustable standard deviation multiplier

### 3. Divergence Detection

- Implements both bullish and bearish divergence identification

- Uses pivot high and pivot low points to detect divergences

- Allows for customization of lookback periods and range for divergence detection

### 4. Entry Conditions

- Long Entry: Bullish divergence when RSI is below 40

- Short Entry: Bearish divergence when RSI is above 60

### 5. Trade Management

- Stop Loss: Customizable, default set to 11 pips

- Take Profit: Customizable, default set to 33 pips

### 6. Visualization

- Plots RSI line and its moving average

- Displays horizontal lines at 30, 50, and 70 RSI levels

- Shows Bollinger Bands when selected

- Highlights divergences with "Bull" and "Bear" labels on the chart

## Input Parameters

- RSI Length: Adjusts the period for RSI calculation

- RSI Source: Selects the price source for RSI (close, open, high, low, hl2, hlc3, ohlc4)

- MA Type: Chooses the type of moving average applied to RSI

- MA Length: Sets the period for the moving average

- BB StdDev: Adjusts the standard deviation multiplier for Bollinger Bands

- Show Divergence: Toggles the display of divergence labels

- Stop Loss: Sets the stop loss distance in pips

- Take Profit: Sets the take profit distance in pips

## Strategy Logic

1. **RSI Calculation**:

- Computes RSI using the specified length and source

- Calculates the chosen type of moving average on the RSI

2. **Divergence Detection**:

- Identifies pivot points in both price and RSI

- Checks for higher lows in RSI with lower lows in price (bullish divergence)

- Checks for lower highs in RSI with higher highs in price (bearish divergence)

3. **Trade Entry**:

- Enters a long position when a bullish divergence is detected and RSI is below 40

- Enters a short position when a bearish divergence is detected and RSI is above 60

4. **Position Management**:

- Places a stop loss order at the entry price ± stop loss pips (depending on the direction)

- Sets a take profit order at the entry price ± take profit pips (depending on the direction)

5. **Visualization**:

- Plots the RSI and its moving average

- Draws horizontal lines for overbought/oversold levels

- Displays Bollinger Bands if selected

- Shows divergence labels on the chart for identified setups

## Usage Instructions

1. Apply the script to a 1-minute XAUUSD (Gold) chart in TradingView

2. Adjust the input parameters as needed:

- Increase RSI Length for less frequent but potentially more reliable signals

- Modify MA Type and Length to change the sensitivity of the RSI moving average

- Adjust Stop Loss and Take Profit levels based on current market volatility

3. Monitor the chart for Bull (long) and Bear (short) labels indicating potential trade setups

4. Use in conjunction with other analysis and risk management techniques

## Considerations

- This strategy is designed for short-term scalping and may not be suitable for all market conditions

- Always backtest and forward test the strategy before using it with real capital

- The effectiveness of divergence-based strategies can vary depending on market trends and volatility

- Consider using additional confirmation signals or filters to improve the strategy's performance

Remember to adapt the strategy parameters to your risk tolerance and trading style, and always practice proper risk management.

BBSR Extreme Strategy [nachodog]The Bollinger Bands Stochastic RSI Extreme Strategy is a comprehensive trading approach designed for use on the TradingView platform, employing a combination of Bollinger Bands and the Stochastic RSI to identify potential entry and exit points in the market. This strategy is converted into Pine Script version 5 and is specifically tailored as a strategy rather than a mere study, allowing traders to simulate and backtest their trades within the TradingView environment.

Strategy Overview:

Bollinger Bands serve as the primary tool for volatility and price level analysis. By calculating the standard deviation of price movements around a simple moving average (SMA), this strategy identifies the upper and lower bounds of price fluctuations, helping traders spot potential reversal points.

Stochastic RSI is used to gauge the momentum by comparing the closing price's position relative to its price range over a certain period. This indicator helps in determining overbought or oversold conditions, providing insights into potential bullish or bearish momentum.

Entry Signals:

Bullish Entry: The strategy signals a long entry when the price moves from below to above the lower Bollinger Band, coupled with a Stochastic RSI indicating an exit from oversold conditions. This suggests an uptrend initiation, prompting a buy order.

Bearish Entry: Conversely, a short entry is signaled when the price drops from above to below the upper Bollinger Band while the Stochastic RSI moves from overbought territory. This condition indicates a potential downtrend, triggering a sell order.

Exit Criteria:

Stop Loss: A key feature of this strategy is the inclusion of a user-defined stop loss percentage, which helps manage risk by specifying the maximum allowable loss per trade.

Bearish Exit for Long Positions: Long positions are exited either when a bearish signal is detected or when the price crosses below the lower Bollinger Band, suggesting a reversal or weakening of the bullish trend.

Bullish Exit for Short Positions: Short positions are closed upon a bullish signal or when the price crosses above the upper Bollinger Band, indicating a potential reversal or diminishing bearish momentum.

Strategy Benefits:

The strategy provides a structured framework for entering and exiting trades, leveraging the strengths of both Bollinger Bands and Stochastic RSI.

It includes parameters for customization, such as the stop loss percentage, allowing traders to align the strategy with their risk tolerance and trading objectives.

The ability to backtest and simulate trades on TradingView enhances its utility, offering insights into the strategy's performance under historical market conditions.

Overall, the Bollinger Bands Stochastic RSI Extreme Strategy is designed for traders who seek to capitalize on trend reversals and momentum shifts, with built-in risk management features to safeguard against significant losses.

HYE Trend Hunter [Strategy]*** Stratejinin Türkçe ve İngilizce açıklaması aşağıya eklenmiştir.

HYE Trend Hunter

In this strategy, two of the most basic data (price and volume) necessary for detecting trends as early as possible and entering the trade on time are used. In this context, the approaches of some classical and new generation indicators using price and volume have been taken into account.

The strategy is prepared to generate buy signals only. The following steps were followed to generate the buy and exit signals.

1-) First of all, the two most basic data of the strategy, “slow leading line” and “fast leading line” need to be calculated. For this, we use the formula of the “senkou span A” line of the indicator known as the Ichimoku Cloud. We also need to calculate lines known as tenkan sen and kijun sen in ichimoku because they are used in the calculation of this formula.

The high and low values of the candles are taken into account when calculating the Tenkansen, Kijunsen and Senkou Span A lines in the Ichimoku cloud. In this strategy, the highest and lowest values of the periodic VWAP are taken into account when calculating the "slow leading line" and "fast leading line". (The periodic vwap formula was coded and made available by @neolao on tradingviev). Also, in the ichimoku cloud, while the Senkou Span A line is plotted 26 periods into the future, we consider the values of the fast and slow leading lines in the last candle in this strategy.

ORIGINAL ICHIMOKU SPAN A FORMULA

Tenkansen = (Highest high of the last 9 candles + Lowest low of the last 9 candles) / 2

Kijunsen = (Highest high of the last 26 candles + Lowest low of the last 26 candles) / 2

Senkou Span A = Tenkansen + Kijunsen / 2

HYE TREND HUNTER SPAN A FORMULA*

Tenkansen = (Highest VWAP of the last 9 candles + Lowest VWAP of the last 9 candles) / 2

Kijunsen = (Highest VWAP of the last 26 candles + Lowest VWAP of the last 26 candles) / 2

Senkou Span A = Tenkansen + Kijunsen / 2

* We use the original ichimoku values 9 and 26 for the slow line, and 5 and 13 for the fast line. These settings can be changed from the strategy settings.

2-) At this stage, we have 2 lines that we obtained by using the formula of the ichimoku cloud, one of the most classical trend indicators, and by including the volume-weighted average price.

a-) Fast Leading Line (5-13)

b-) Slow Leading Line (9-26)

For the calculation we will do soon, we get a new value by taking the average of these two lines. Using this value, which is the average of the fast and slow leading lines, we plot the Bollinger Bands indicator, which is known as one of the most classic volatility indicators of technical analysis. Thus, we are trying to understand whether there is a volatility change in the market, which may mean the presence of a trend start. We will use this data in the calculation of buy-sell signals.

In the classical Bollinger Bands calculation, the standard deviation is calculated by applying a multiplier at the rate determined by the user (2 is used in the original settings) to the moving average calculated with the “closing price”, and this value is added or subtracted from the moving average and upper band and lower band lines are drawn.

In the HYE Trend Hunter Strategy, instead of the moving average calculated with the closing price in the Bollinger Band calculation, we consider the average of the fast and slow leading lines calculated in the 1st step and draw the Bollinger upper and lower bands accordingly. We use the values of 2 and 20 as the standard deviation and period, as in the original settings. These settings can also be changed from the strategy settings.

3-) At this stage, we have fast and slow leading lines trying to understand the trend direction using VWAP, and Bollinger lower and upper bands calculated by the average of these lines.

In this step, we will use another tool that will help us understand whether the invested market (forex, crypto, stocks) is gaining momentum in volume. The Time Segmented Volume indicator was created by the Worden Brothers Inc. and coded by @liw0 and @vitelot on tradingview. The TSV indicator segments the price and volume of an investment instrument according to certain time periods and makes calculations on comparing these price and volume data to reveal the buying and selling periods.

To trade in the buy direction on the HYE Trend Hunter Strategy, we look for the TSV indicator to be above 0 and above its exponential moving average value. TSV period and exponential moving average period settings (13 and 7) can also be changed in the strategy settings.

BUY SIGNAL

1-) Fast Leading Line value should be higher than the Fast Leading Line value in the previous candle.

2-) Slow Leading Line value should be higher than the Slow Leading Line value in the previous candle.

3-) Candle Closing value must be higher than the Upper Bollinger Band.

4-) TSV value must be greater than 0.

5-) TSV value must be greater than TSVEMA value.

EXIT SIGNAL

1-) Fast Leading Line value should be lower than the Fast Leading Line value in the previous candle.

2-) Slow Leading Line value should be lower than the Slow Leading Line value in the previous candle.

TIPS AND WARNINGS

1-) The standard settings of the strategy work better in higher timeframes (4-hour, daily, etc.). For lower timeframes, you should change the strategy settings and find the best value for yourself.

2-) All lines (fast and slow leading lines and Bollinger bands) except TSV are displayed on the strategy. For a simpler view, you can hide these lines in the strategy settings.

3-) You can see the color changes of the fast and slow leading lines as well as you can specify a single color for these lines in the strategy settings.

4-) It is an strategy for educational and experimental purposes. It cannot be considered as investment advice. You should be careful and make your own risk assessment when opening real market trades using this strategy.

_______________________________________________

HYE Trend Avcısı

Bu stratejide, trendlerin olabildiğince erken tespit edilebilmesi ve zamanında işleme girilebilmesi için gerekli olan en temel iki veriden (fiyat ve hacim) yararlanılmaktadır. Bu kapsamda, fiyat ve hacim kullanan bazı klasik ve yeni nesil indikatörlerin yaklaşımları dikkate alınmıştır.

Strateji yalnızca alış yönlü sinyaller üretecek şekilde hazırlanmıştır. Alış ve çıkış sinyallerinin üretilmesi için aşağıdaki adımlar izlenmiştir.

1-) Öncelikle, stratejinin en temel iki verisi olan “yavaş öncü çizgi” ve “hızlı öncü çizgi” hesaplamasının yapılması gerekiyor. Bunun için de Ichimoku Bulutu olarak bilinen indikatörün “senkou span A” çizgisinin formülünü kullanıyoruz. Bu formülün hesaplamasında kullanılmaları nedeniyle ichimoku’da tenkan sen ve kijun sen olarak bilinen çizgileri de hesaplamamız gerekiyor.

Ichimoku bulutunda Tenkansen, Kijunsen ve Senkou Span A çizgileri hesaplanırken mumların yüksek ve düşük değerleri dikkate alınıyor. Bu stratejide ise “yavaş öncü çizgi” ve “hızlı öncü çizgi” hesaplanırken periyodik VWAP’ın en yüksek ve en düşük değerleri dikkate alınıyor. (Periyodik vwap formülü, tradingviev’de @neolao tarafından kodlanmış ve kullanıma açılmış). Ayrıca, ichimoku bulutunda Senkou Span A çizgisi geleceğe yönelik çizilirken (26 mum ileriye dönük) biz bu stratejide öncü çizgilerin son mumdaki değerlerini dikkate alıyoruz.

ORJİNAL ICHIMOKU SPAN A FORMÜLÜ

Tenkansen = (Son 9 mumun en yüksek değeri + Son 9 mumun en düşük değeri) / 2

Kijunsen = (Son 26 mumun en yüksek değeri + Son 26 mumun en düşük değeri) / 2

Senkou Span A = Tenkansen + Kijunsen / 2

HYE TREND HUNTER SPAN A FORMÜLÜ*

Tenkansen = (Son 9 mumun en yüksek VWAP değeri + Son 9 mumun en düşük VWAP değeri) / 2

Kijunsen = (Son 26 mumun en yüksek VWAP değeri + Son 26 mumun en düşük VWAP değeri) / 2

Senkou Span A = Tenkansen + Kijunsen / 2

* Yavaş çizgi için orijinal ichimoku değerleri olan 9 ve 26’yı kullanırken, hızlı çizgi için 5 ve 13’ü kullanıyoruz. Bu ayarlar, strateji ayarlarından değiştirilebiliyor.

2-) Bu aşamada, elimizde en klasik trend indikatörlerinden birisi olan ichimoku bulutunun formülünden faydalanarak, işin içinde hacim ağırlıklı ortalama fiyatı da sokmak suretiyle elde ettiğimiz 2 çizgimiz var.

a-) Hızlı Öncü Çizgi (5-13)

b-) Yavaş Öncü Çizgi (9-26)

Birazdan yapacağımız hesaplama için bu iki çizginin de ortalamasını alarak yeni bir değer elde ediyoruz. Hızlı ve yavaş öncü çizgilerin ortalaması olan bu değeri kullanarak, teknik analizin en klasik volatilite indikatörlerinden birisi olarak bilinen Bollinger Bantları indikatörünü çizdiriyoruz. Böylelikle piyasada bir trend başlangıcının varlığı anlamına gelebilecek volatilite değişikliği var mı yok mu anlamaya çalışıyoruz. Bu veriyi al-sat sinyallerinin hesaplamasında kullanacağız.

Klasik Bollinger Bantları hesaplamasında, “kapanış fiyatıyla” hesaplanan hareketli ortalamaya, kullanıcı olarak belirlenen oranda (orijinal ayarlarında 2 kullanılır) bir çarpan uygulanarak standart sapma hesaplanıyor ve bu değer hareketli ortalamaya eklenip çıkartılarak üst bant ve alt bant çizgileri çiziliyor.

HYE Trend Avcısı stratejisinde, Bollinger Bandı hesaplamasında kapanış fiyatıyla hesaplanan hareketli ortalama yerine, 1. adımda hesapladığımız hızlı ve yavaş öncü çizgilerin ortalamasını dikkate alıyoruz ve buna göre bollinger üst ve alt bantlarını çizdiriyoruz. Standart sapma ve periyot olarak yine orijinal ayarlarında olduğu gibi 2 ve 20 değerlerini kullanıyoruz. Bu ayarlar da strateji ayarlarından değiştirilebiliyor.

3-) Bu aşamada, elimizde VWAP kullanarak trend yönünü anlamaya çalışan hızlı ve yavaş öncü çizgilerimiz ile bu çizgilerin ortalaması ile hesaplanan bollinger alt ve üst bantlarımız var.

Bu adımda, yatırım yapılan piyasanın (forex, kripto, hisse senedi) hacimsel olarak ivme kazanıp kazanmadığını anlamamıza yarayacak bir araç daha kullanacağız. Time Segmented Volume indikatörü, Worden Kardeşler şirketi tarafından oluşturulmuş ve tradingview’de @liw0 ve @vitelot tarafından kodlanarak kullanıma açılmış. TSV indikatörü, bir yatırım aracının fiyatını ve hacmini belirli zaman aralıklarına göre bölümlere ayırarak, bu fiyat ve hacim verilerini, alış ve satış dönemlerini ortaya çıkarmak için karşılaştırmak üzerine hesaplamalar yapar.

HYE Trend Avcısı stratejisinde alış yönünde işlem yapmak için, TSV indikatörünün 0’ın üzerinde olmasını ve kendi üstel hareketli ortalama değerinin üzerinde olmasını arıyoruz. TSV periyodu ve üstel hareketli ortalama periyodu ayarları da (13 ve 7) strateji ayarlarından değiştirilebiliyor.

ALIŞ SİNYALİ

1-) Hızlı Öncü Çizgi değeri bir önceki mumdaki Hızlı Öncü Çizgi değerinden yüksek olmalı.

2-) Yavaş Öncü Çizgi değeri bir önceki mumdaki Yavaş Öncü Çizgi değerinden yüksek olmalı.

3-) Kapanış Değeri, Üst Bollinger Bandı değerinden yüksek olmalı.

4-) TSV değeri 0’dan büyük olmalı.

5-) TSV değeri TSVEMA değerinden büyük olmalı.

ÇIKIŞ SİNYALİ

1-) Hızlı Öncü Çizgi değeri bir önceki mumdaki Hızlı Öncü Çizgi değerinden düşük olmalı.

2-) Yavaş Öncü Çizgi değeri bir önceki mumdaki Yavaş Öncü Çizgi değerinden düşük olmalı.

İPUÇLARI VE UYARILAR

1-) Stratejinin standart ayarları, yüksek zaman dilimlerinde (4 saatlik, günlük vs.) daha iyi çalışıyor. Düşük zaman dilimleri için strateji ayarlarını değiştirmeli ve kendiniz için en iyi değeri bulmalısınız.

2-) Stratejide tüm çizgiler (hızlı ve yavaş öncü çizgiler ile bollinger bantları) -TSV dışında- açık olarak gelmektedir. Daha sade bir görüntü için bu çizgilerin görünürlüğünü strateji ayarlarından gizleyebilirsiniz.

3-) Hızlı ve yavaş öncü çizgilerin renk değişimlerini görebileceğiniz gibi bu çizgiler için tek bir renk olarak da strateji ayarlarında belirleme yapabilirsiniz.

4-) Eğitim ve deneysel amaçlı bir stratejidir. Yatırım tavsiyesi olarak değerlendirilemez. Bu stratejiyi kullanarak gerçek piyasa işlem açarken dikkatli olmalı ve kendi risk değerlendirmenizi yapmalısınız.

888 BOT #backtest█ 888 BOT #backtest (open source)

This is an Expert Advisor 'EA' or Automated trading script for ‘longs’ and ‘shorts’, which uses only a Take Profit or, in the worst case, a Stop Loss to close the trade.

It's a much improved version of the previous ‘Repanocha’. It doesn`t use 'Trailing Stop' or 'security()' functions (although using a security function doesn`t mean that the script repaints) and all signals are confirmed, therefore the script doesn`t repaint in alert mode and is accurate in backtest mode.

Apart from the previous indicators, some more and other functions have been added for Stop-Loss, re-entry and leverage.

It uses 8 indicators, (many of you already know what they are, but in case there is someone new), these are the following:

1. Jurik Moving Average

It's a moving average created by Mark Jurik for professionals which eliminates the 'lag' or delay of the signal. It's better than other moving averages like EMA , DEMA , AMA or T3.

There are two ways to decrease noise using JMA . Increasing the 'LENGTH' parameter will cause JMA to move more slowly and therefore reduce noise at the expense of adding 'lag'

The 'JMA LENGTH', 'PHASE' and 'POWER' parameters offer a way to select the optimal balance between 'lag' and over boost.

Green: Bullish , Red: Bearish .

2. Range filter

Created by Donovan Wall, its function is to filter or eliminate noise and to better determine the price trend in the short term.

First, a uniform average price range 'SAMPLING PERIOD' is calculated for the filter base and multiplied by a specific quantity 'RANGE MULTIPLIER'.

The filter is then calculated by adjusting price movements that do not exceed the specified range.

Finally, the target ranges are plotted to show the prices that will trigger the filter movement.

Green: Bullish , Red: Bearish .

3. Average Directional Index ( ADX Classic) and ( ADX Masanakamura)

It's an indicator designed by Welles Wilder to measure the strength and direction of the market trend. The price movement is strong when the ADX has a positive slope and is above a certain minimum level 'ADX THRESHOLD' and for a given period 'ADX LENGTH'.

The green color of the bars indicates that the trend is bullish and that the ADX is above the level established by the threshold.

The red color of the bars indicates that the trend is down and that the ADX is above the threshold level.

The orange color of the bars indicates that the price is not strong and will surely lateralize.

You can choose between the classic option and the one created by a certain 'Masanakamura'. The main difference between the two is that in the first it uses RMA () and in the second SMA () in its calculation.

4. Parabolic SAR

This indicator, also created by Welles Wilder, places points that help define a trend. The Parabolic SAR can follow the price above or below, the peculiarity that it offers is that when the price touches the indicator, it jumps to the other side of the price (if the Parabolic SAR was below the price it jumps up and vice versa) to a distance predetermined by the indicator. At this time the indicator continues to follow the price, reducing the distance with each candle until it is finally touched again by the price and the process starts again. This procedure explains the name of the indicator: the Parabolic SAR follows the price generating a characteristic parabolic shape, when the price touches it, stops and turns ( SAR is the acronym for 'stop and reverse'), giving rise to a new cycle. When the points are below the price, the trend is up, while the points above the price indicate a downward trend.

5. RSI with Volume

This indicator was created by LazyBear from the popular RSI .

The RSI is an oscillator-type indicator used in technical analysis and also created by Welles Wilder that shows the strength of the price by comparing individual movements up or down in successive closing prices.

LazyBear added a volume parameter that makes it more accurate to the market movement.

A good way to use RSI is by considering the 50 'RSI CENTER LINE' centerline. When the oscillator is above, the trend is bullish and when it is below, the trend is bearish .

6. Moving Average Convergence Divergence ( MACD ) and ( MAC-Z )

It was created by Gerald Appel. Subsequently, the histogram was added to anticipate the crossing of MA. Broadly speaking, we can say that the MACD is an oscillator consisting of two moving averages that rotate around the zero line. The MACD line is the difference between a short moving average 'MACD FAST MA LENGTH' and a long moving average 'MACD SLOW MA LENGTH'. It's an indicator that allows us to have a reference on the trend of the asset on which it is operating, thus generating market entry and exit signals.

We can talk about a bull market when the MACD histogram is above the zero line, along with the signal line, while we are talking about a bear market when the MACD histogram is below the zero line.

There is the option of using the MAC-Z indicator created by LazyBear, which according to its author is more effective, by using the parameter VWAP ( volume weighted average price ) 'Z-VWAP LENGTH' together with a standard deviation 'STDEV LENGTH' in its calculation.

7. Volume Condition

Volume indicates the number of participants in this war between bulls and bears, the more volume the more likely the price will move in favor of the trend. A low trading volume indicates a lower number of participants and interest in the instrument in question. Low volumes may reveal weakness behind a price movement.

With this condition, those signals whose volume is less than the volume SMA for a period 'SMA VOLUME LENGTH' multiplied by a factor 'VOLUME FACTOR' are filtered. In addition, it determines the leverage used, the more volume , the more participants, the more probability that the price will move in our favor, that is, we can use more leverage. The leverage in this script is determined by how many times the volume is above the SMA line.

The maximum leverage is 8.

8. Bollinger Bands

This indicator was created by John Bollinger and consists of three bands that are drawn superimposed on the price evolution graph.

The central band is a moving average, normally a simple moving average calculated with 20 periods is used. ('BB LENGTH' Number of periods of the moving average)

The upper band is calculated by adding the value of the simple moving average X times the standard deviation of the moving average. ('BB MULTIPLIER' Number of times the standard deviation of the moving average)

The lower band is calculated by subtracting the simple moving average X times the standard deviation of the moving average.

the band between the upper and lower bands contains, statistically, almost 90% of the possible price variations, which means that any movement of the price outside the bands has special relevance.

In practical terms, Bollinger bands behave as if they were an elastic band so that, if the price touches them, it has a high probability of bouncing.

Sometimes, after the entry order is filled, the price is returned to the opposite side. If price touch the Bollinger band in the same previous conditions, another order is filled in the same direction of the position to improve the average entry price, (% MINIMUM BETTER PRICE ': Minimum price for the re-entry to be executed and that is better than the price of the previous position in a given %) in this way we give the trade a chance that the Take Profit is executed before. The downside is that the position is doubled in size. 'ACTIVATE DIVIDE TP': Divide the size of the TP in half. More probability of the trade closing but less profit.

█ STOP LOSS and RISK MANAGEMENT.

A good risk management is what can make your equity go up or be liquidated.

The % risk is the percentage of our capital that we are willing to lose by operation. This is recommended to be between 1-5%.

% Risk: (% Stop Loss x % Equity per trade x Leverage) / 100

First the strategy is calculated with Stop Loss, then the risk per operation is determined and from there, the amount per operation is calculated and not vice versa.

In this script you can use a normal Stop Loss or one according to the ATR. Also activate the option to trigger it earlier if the risk percentage is reached. '% RISK ALLOWED'

'STOP LOSS CONFIRMED': The Stop Loss is only activated if the closing of the previous bar is in the loss limit condition. It's useful to prevent the SL from triggering when they do a ‘pump’ to sweep Stops and then return the price to the previous state.

█ BACKTEST

The objective of the Backtest is to evaluate the effectiveness of our strategy. A good Backtest is determined by some parameters such as:

- RECOVERY FACTOR: It consists of dividing the 'net profit' by the 'drawdown’. An excellent trading system has a recovery factor of 10 or more; that is, it generates 10 times more net profit than drawdown.

- PROFIT FACTOR: The ‘Profit Factor’ is another popular measure of system performance. It's as simple as dividing what win trades earn by what loser trades lose. If the strategy is profitable then by definition the 'Profit Factor' is going to be greater than 1. Strategies that are not profitable produce profit factors less than one. A good system has a profit factor of 2 or more. The good thing about the ‘Profit Factor’ is that it tells us what we are going to earn for each dollar we lose. A profit factor of 2.5 tells us that for every dollar we lose operating we will earn 2.5.

- SHARPE: (Return system - Return without risk) / Deviation of returns.

When the variations of gains and losses are very high, the deviation is very high and that leads to a very poor ‘Sharpe’ ratio. If the operations are very close to the average (little deviation) the result is a fairly high 'Sharpe' ratio. If a strategy has a 'Sharpe' ratio greater than 1 it is a good strategy. If it has a 'Sharpe' ratio greater than 2, it is excellent. If it has a ‘Sharpe’ ratio less than 1 then we don't know if it is good or bad, we have to look at other parameters.

- MATHEMATICAL EXPECTATION: (% winning trades X average profit) + (% losing trades X average loss).

To earn money with a Trading system, it is not necessary to win all the operations, what is really important is the final result of the operation. A Trading system has to have positive mathematical expectation as is the case with this script: ME = (0.87 x 30.74$) - (0.13 x 56.16$) = (26.74 - 7.30) = 19.44$ > 0

The game of roulette, for example, has negative mathematical expectation for the player, it can have positive winning streaks, but in the long term, if you continue playing you will end up losing, and casinos know this very well.

PARAMETERS

'BACKTEST DAYS': Number of days back of historical data for the calculation of the Backtest.

'ENTRY TYPE': For '% EQUITY' if you have $ 10,000 of capital and select 7.5%, for example, your entry would be $ 750 without leverage. If you select CONTRACTS for the 'BTCUSDT' pair, for example, it would be the amount in 'Bitcoins' and if you select 'CASH' it would be the amount in $ dollars.

'QUANTITY (LEVERAGE 1X)': The amount for an entry with X1 leverage according to the previous section.

'MAXIMUM LEVERAGE': It's the maximum allowed multiplier of the quantity entered in the previous section according to the volume condition.

The settings are for Bitcoin at Binance Futures (BTC: USDTPERP) in 15 minutes.

For other pairs and other timeframes, the settings have to be adjusted again. And within a month, the settings will be different because we all know the market and the trend are changing.

Configurable BB+RSI+Aroon strategy backtest for binary optionsI wanted to share this strategy that I use myself for binary options trading. After trading binary options for several years I have learned that every single day is unique... assets behave differently every single day. So, when I start the day I want to know which is the optimum combination of parameters in my indicators that will give me the signals I want during the day and I get that by doing a quick backtest of the parameters combination in a specific asset that same day. When trading Binary Options I usually do 3 or 4 trades max per day and, yes, there are moments in which even with the right backtest data the signals fail (I strongly believe that there is no strategy that guarantees 100% success in any type of trade, and this one here is not an exception - but has worked well with some assets). So, here is my contribution to improve your productivity by automating a bit that backtesting part.

How this script works?

It is a simple price crossunder / crossover Bollinger Bands (BB) with a confirmation from RSI overbought / oversold signals and a fast Aroon. You will see the BB plotted with its confirmations:

(1) a blue circle that plots in the chart when the price is coming back inside the channel (within the Bollinger Bands)

(2) an orange square that plots in the chart when the RSI is coming back from the overbought or oversold areas

(3) a triangle that could be red or green depending on the Aroon confirmation: Red if Aroon Down is crossing down Aroon Up or green if vice versa.

The strategy will call for long (Call) if:

(1) the price is crossing over the lower band of the Bollinger Bands, coming back inside the channel

(2) Aroon Up is crossing or has crossed above Aroon Down

(3) RSI is crossing over the oversold limit

Consequently, the strategy will call for a short (Put) if:

(1) the price is crossing down the upper band of the Bollinger Bands, coming back inside the channel

(2) Aroon Down is crossing or has crossed below Aroon Up

(3) RSI is crossing under the overbought limit

You can configure:

1. Aroon length (keep it as fast as possible: 3, 4 or 5 are recommended values)

2. The point where Aroon Up and Aroon Down cross to make the signal valid (50 is by default. It could also be 25 or 75)

3. The RSI length

4. RSI Overbought and Oversold limits (they do not need to be symmetric: you can use 29 and 93, for example)

5. Bollinger Bands length and standard deviation

6. Number of bars to keep your option open. Depending on the timeframe used, this will determine the time you will keep your binary option open. If you are in a 1 min chart and keep this parameter in 3, then you will need to configure your binary option to expire in 3 minutes.

How to evaluate your backtest?

In Binary Options you only need the success rate, so what I do is that when I am manually updating the parameters I keep my strategy tester window open checking the winning trades vs losing trades ratio ("Percent Profitable"). I personally will only keep an asset monitored looking for signals that day if the Percent Profitable on the backtest of the same day is above 80%.

Regarding the code: it is open, public and free. No need to ask for permission if you want to copy+paste and use it in whole or parts.

Happy pip hunting!

-marco

hullma percentage linesWhat you see is a hullMA (user defined length) with 4 percentage bands attached to it.

The bands percentage and hullMA length can be adjusted to see how the trading strategy performs.

I implemented only long trades with a crossover from one of the lower bands, when it crosses over a high band

it exits the trade.

Improvement coulde be:

-more percentage bands

-short trades

-trades between bands

Enjoy:)

Hazel nut BB Strategy, volume base- lite versionHazel nut BB Strategy, volume base — lite version

Having knowledge and information in financial markets is only useful when a trader operates with a well-defined trading strategy. Trading strategies assist in capital management, profit-taking, and reducing potential losses.

This strategy is built upon the core principle of supply and demand dynamics. Alongside this foundation, one of the widely used technical tools — the Bollinger Bands — is employed to structure a framework for profit management and risk control.

In this strategy, the interaction of these tools is explained in detail. A key point to note is that for calculating buy and sell volumes, a lower timeframe function is used. When applied with a tick-level resolution, this provides the most precise measurement of buyer/seller flows. However, this comes with a limitation of reduced historical depth. Users should be aware of this trade-off: if precise tick-level data is required, shorter timeframes should be considered to extend historical coverage .

The strategy offers multiple configuration options. Nevertheless, it should be treated strictly as a supportive tool rather than a standalone trading system. Decisions must integrate personal analysis and other instruments. For example, in highly volatile assets with narrow ranges, it is recommended to adjust profit-taking and stop-loss percentages to smaller values.

◉ Volume Settings

• Buyer and seller volume (up/down volume) are requested from a lower timeframe, with an option to override the automatic resolution.

• A global lookback period is applied to calculate moving averages and cumulative sums of buy/sell/delta volumes.

• Ratios of buyers/sellers to total volume are derived both on the current bar and across the lookback window.

◉ Bollinger Band

• Bands are computed using configurable moving averages (SMA, EMA, RMA, WMA, VWMA).

• Inputs allow control of length, standard deviation multiplier, and offset.

• The basis, upper, and lower bands are plotted, with a shaded background between them.

◉ Progress & Proximity

• Relative position of the price to the Bollinger basis is expressed as percentages (qPlus/qMinus).

• “Near band” conditions are triggered when price progress toward the upper or lower band exceeds a user-defined threshold (%).

• A signed score (sScore) represents how far the close has moved above or below the basis relative to band width.

◉ Info Table

• Optional compact table summarizing:

• - Upper/lower band margins

• - Buyer/seller volumes with moving averages

• - Delta and cumulative delta

• - Buyer/seller ratios per bar and across the window

• - Money flow values (buy/sell/delta × price) for bar-level and summed periods

• The table is neutral-colored and resizable for different chart layouts.

◉ Zone Event Gate

• Tracks entry into and exit from “near band” zones.

• Arming logic: a side is armed when price enters a band proximity zone.

• Trigger logic: on exit, a trade event is generated if cumulative buyer or seller volume dominates over a configurable window.

◉ Trading Logic

• Orders are placed only on zone-exit events, conditional on volume dominance.

• Position sizing is defined as a fixed percentage of strategy equity.

• Long entries occur when leaving the lower zone with buyer dominance; short entries occur when leaving the upper zone with seller dominance.

◉ Exit Rules

• Open positions are managed by a strict priority sequence:

• 1. Stop-loss (% of entry price)

• 2. Take-profit (% of entry price)

• 3. Opposite-side event (zone exit with dominance in the other direction)

• Stop-loss and take-profit levels are configurable

◉ Notes

• This lite version is intended to demonstrate the interaction of Bollinger Bands and volume-based dominance logic.

• It provides a framework to observe how price reacts at band boundaries under varying buy/sell pressure, and how zone exits can be systematically converted into entry/exit signals.

When configuring this strategy, it is essential to carefully review the settings within the Strategy Tester. Ensure that the chosen parameters and historical data options are correctly aligned with the intended use. Accurate back testing depends on applying proper configurations for historical reference. The figure below illustrates sample result and configuration type.

Penguin Volatility State StrategyThe Penguin Volatility State Strategy is a comprehensive technical analysis framework designed to identify the underlying "state" or "regime" of the market. Instead of just providing simple buy or sell signals, its primary goal is to classify the market into one of four distinct states by combining trend, momentum, and volatility analysis.

The core idea is to trade only when these three elements align, focusing on periods of volatility expansion (a "squeeze breakout") that occur in the direction of a confirmed trend and are supported by strong momentum.

Key Components

The strategy is built upon two main engines

The Volatility Engine (Bollinger Bands vs. Keltner Channels)

This engine detects periods of rapidly increasing volatility. It measures the percentage difference (diff) between the upper bands of Bollinger Bands (which are based on standard deviation) and Keltner Channels (based on Average True Range). During a volatility "squeeze," both bands are close. When price breaks out, the Bollinger Band expands much faster than the Keltner Channel, causing the diff value to become positive. A positive diff signals a volatility breakout, which is the moment the strategy becomes active.

The Trend & Momentum Engine (Multi-EMA System)

This engine determines the market's direction and strength. It uses:

A Fast EMA (e.g., 12-period) and a Slow EMA (e.g., 26-period): The crossover of these two moving averages defines the primary, underlying trend (similar to a MACD).

An Ultra-Fast EMA (e.g., 2-period of ohlc4): This is used to measure the immediate, short-term momentum of the price.

The Four Market States

By combining the Trend and Momentum engines, the strategy categorizes the market into four visually distinct states, represented by the chart's background color. This is the most crucial aspect of the system.

💚 Green State: Strong Bullish

The primary trend is UP (Fast EMA > Slow EMA) AND the immediate momentum is STRONG (Price > Fast EMA).