Backtesting on Non-Standard Charts: Caution! - PineCoders FAQMuch confusion exists in the TradingView community about backtesting on non-standard charts. This script tries to shed some light on the subject in the hope that traders make better use of those chart types.

Non-standard charts are:

Heikin Ashi (HA)

Renko

Kagi

Point & Figure

Range

These chart types are called non-standard because they all transform market prices into synthetic views of price action. Some focus on price movement and disregard time. Others like HA use the same division of bars into fixed time intervals but calculate artificial open, high, low and close (OHLC) values.

Non-standard chart types can provide traders with alternative ways of interpreting price action, but they are not designed to test strategies or run automated traded systems where results depend on the ability to enter and exit trades at precise price levels at specific times, whether orders are issued manually or algorithmically. Ironically, the same characteristics that make non-standard chart types interesting from an analytical point of view also make them ill-suited to trade execution. Why? Because of the dislocation that a synthetic view of price action creates between its non-standard chart prices and real market prices at any given point in time. Switching from a non-standard chart price point into the market always entails a translation of time/price dimensions that results in uncertainty—and uncertainty concerning the level or the time at which orders are executed is detrimental to all strategies.

The delta between the chart’s price when an order is issued (which is assumed to be the expected price) and the price at which that order is filled is called slippage . When working from normal chart types, slippage can be caused by one or more of the following conditions:

• Time delay between order submission and execution. During this delay the market may move normally or be subject to large orders from other traders that will cause large moves of the bid/ask levels.

• Lack of bids for a market sell or lack of asks for a market buy at the current price level.

• Spread taken by middlemen in the order execution process.

• Any other event that changes the expected fill price.

When a market order is submitted, matching engines attempt to fill at the best possible price at the exchange. TradingView strategies usually fill market orders at the opening price of the next candle. A non-standard chart type can produce misleading results because the open of the next candle may or may not correspond to the real market price at that time. This creates artificial and often beneficial slippage that would not exist on standard charts.

Consider an HA chart. The open for each candle is the average of the previous HA bar’s open and close prices. The open of the HA candle is a synthetic value, but the real market open at the time the new HA candle begins on the chart is the unrelated, regular open at the chart interval. The HA open will often be lower on long entries and higher on short entries, resulting in unrealistically advantageous fills.

Another example is a Renko chart. A Renko chart is a type of chart that only measures price movement. The purpose of a Renko chart is to cluster price action into regular intervals, which consequently removes the time element. Because Trading View does not provide tick data as a price source, it relies on chart interval close values to construct Renko bricks. As a consequence, a new brick is constructed only when the interval close penetrates one or more brick thresholds. When a new brick starts on the chart, it is because the previous interval’s close was above or below the next brick threshold. The open price of the next brick will likely not represent the current price at the time this new brick begins, so correctly simulating an order is impossible.

Some traders have argued with us that backtesting and trading off HA charts and other non-standard charts is useful, and so we have written this script to show traders what happens when order fills from backtesting on non-standard charts are compared to real-world fills at market prices.

Let’s review how TV backtesting works. TV backtesting uses a broker emulator to execute orders. When an order is executed by the broker emulator on historical bars, the price used for the fill is either the close of the order’s submission bar or, more often, the open of the next. The broker emulator only has access to the chart’s prices, and so it uses those prices to fill orders. When backtesting is run on a non-standard chart type, orders are filled at non-standard prices, and so backtesting results are non-standard—i.e., as unrealistic as the prices appearing on non-standard charts. This is not a bug; where else is the broker emulator going to fetch prices than from the chart?

This script is a strategy that you can run on either standard or non-standard chart types. It is meant to help traders understand the differences between backtests run on both types of charts. For every backtest, a label at the end of the chart shows two global net profit results for the strategy:

• The net profits (in currency) calculated by TV backtesting with orders filled at the chart’s prices.

• The net profits (in currency) calculated from the same orders, but filled at market prices (fetched through security() calls from the underlying real market prices) instead of the chart’s prices.

If you run the script on a non-standard chart, the top result in the label will be the result you would normally get from the TV backtesting results window. The bottom result will show you a more realistic result because it is calculated from real market fills.

If you run the script on a normal chart type (bars, candles, hollow candles, line, area or baseline) you will see the same result for both net profit numbers since both are run on the same real market prices. You will sometimes see slight discrepancies due to occasional differences between chart prices and the corresponding information fetched through security() calls.

Features

• Results shown in the Data Window (third icon from the top right of your chart) are:

— Cumulative results

— For each order execution bar on the chart, the chart and market previous and current fills, and the trade results calculated from both chart and market fills.

• You can choose between 2 different strategies, both elementary.

• You can use HA prices for the calculations determining entry/exit conditions. You can use this to see how a strategy calculated from HA values can run on a normal chart. You will notice that such strategies will not produce the same results as the real market results generated from HA charts. This is due to the different environment backtesting is running on where for example, position sizes for entries on the same bar will be calculated differently because HA and standard chart close prices differ.

• You can choose repainting/non-repainting signals.

• You can show MAs, entry/exit markers and market fill levels.

• You can show candles built from the underlying market prices.

• You can color the background for occurrences where an order is filled at a different real market price than the chart’s price.

Notes

• On some non-standard chart types you will not obtain any results. This is sometimes due to how certain types of non-standard types work, and sometimes because the script will not emit orders if no underlying market information is detected.

• The script illustrates how those who want to use HA values to calculate conditions can do so from a standard chart. They will then be getting orders emitted on HA conditions but filled at more realistic prices because their strategy can run on a standard chart.

• On some non-standard chart types you will see market results surpass chart results. While this may seem interesting, our way of looking at it is that it points to how unreliable non-standard chart backtesting is, and why it should be avoided.

• In order not to extend an already long description, we do not discuss the particulars of executing orders on the realtime bar when using non-standard charts. Unless you understand the minute details of what’s going on in the realtime bar on a particular non-standard chart type, we recommend staying away from this.

• Some traders ask us: Why does TradingView allow backtesting on non-standard chart types if it produces unrealistic results? That’s somewhat like asking a hammer manufacturer why it makes hammers if hammers can hurt you. We believe it’s a trader’s responsibility to understand the tools he is using.

Takeaways

• Non-standard charts are not bad per se, but they can be badly used.

• TV backtesting on non-standard charts is not broken and doesn’t require fixing. Traders asking for a fix are in dire need of learning more about trading. We recommend they stop trading until they understand why.

• Stay away from—even better, report—any vendor presenting you with strategies running on non-standard charts and implying they are showing reliable results.

• If you don’t understand everything we discussed, don’t use non-standard charts at all.

• Study carefully how non-standard charts are built and the inevitable compromises used in calculating them so you can understand their limitations.

Thanks to @allanster and @mortdiggiddy for their help in editing this description.

Look first. Then leap.

Wyszukaj w skryptach "backtesting"

Simple APF Strategy Backtesting [The Quant Science]Simple backtesting strategy for the quantitative indicator Autocorrelation Price Forecasting. This is a Buy & Sell strategy that operates exclusively with long orders. It opens long positions and generates profit based on the future price forecast provided by the indicator. It's particularly suitable for trend-following trading strategies or directional markets with an established trend.

Main functions

1. Cycle Detection: Utilize autocorrelation to identify repetitive market behaviors and cycles.

2. Forecasting for Backtesting: Simulate trades and assess the profitability of various strategies based on future price predictions.

Logic

The strategy works as follow:

Entry Condition: Go long if the hypothetical gain exceeds the threshold gain (configurable by user interface).

Position Management: Sets a take-profit level based on the future price.

Position Sizing: Automatically calculates the order size as a percentage of the equity.

No Stop-Loss: this strategy doesn't includes any stop loss.

Example Use Case

A trader analyzes a dayli period using 7 historical bars for autocorrelation.

Sets a threshold gain of 20 points using a 5% of the equity for each trade.

Evaluates the effectiveness of a long-only strategy in this period to assess its profitability and risk-adjusted performance.

User Interface

Length: Set the length of the data used in the autocorrelation price forecasting model.

Thresold Gain: Minimum value to be considered for opening trades based on future price forecast.

Order Size: percentage size of the equity used for each single trade.

Strategy Limit

This strategy does not use a stop loss. If the price continues to drop and the future price forecast is incorrect, the trader may incur a loss or have their capital locked in the losing trade.

Disclaimer!

This is a simple template. Use the code as a starting point rather than a finished solution. The script does not include important parameters, so use it solely for educational purposes or as a boilerplate.

High Low Cloud Strategy BacktestingHigh Low Cloud Strategy Backtesting: this is a breakout and reversal previous trend strategy

A. Indicator: row 6 to row 17

1. Fast Cloud

Upper line = ema of High with 60 periods

Lower line = ema of Low with 60 periods

1. Slow Cloud

Upper line = ema of High with 240 periods

Lower line = ema of Low with 240 periods

B. Strategy Backtesting

1. Chart IDC, Time frame: M30

2. Long condition: row 20 to row 34

a. Entry =

* Upper line of Fast Cloud below Lower line of Slow Cloud

* Price crossover Upper line of Slow Cloud

b. Stoploss =

* Price crossunder bottom of 240 periods (~ bottom of 5 days)

c. Takeprofit =

* Lower line of Fast Cloud above Upper line of Slow Cloud

* Price crossunder Lower line of Fast Cloud

3. Short condition: row 37 to row 49

a. Entry =

* Lower line of Fast Cloud above Upper line of Slow Cloud

* Price crossunder Lower line of Slow Cloud

b. Stoploss =

* Price crossover peak of 240 periods (~ bottom of 5 days)

c. Takeprofit =

* Upper line of Fast Cloud below Lower line of Slow Cloud

* Price crossover Upper line of Fast Cloud

Grid Bot BacktestingBinance, Bybit, Bitget, and other cross-exchange (grid) trading bot backtesting.

Auto bound: Automatically setting upper and lower price bounds.

Manual: Setting upper and lower price bounds manually.

The graph below represents the overall asset changes (initial investment amount + current position profit + grid profit).

Try using backtesting when setting up a grid bot on the exchange!

바이낸스, 바이비트, 비트겟 등 교차거래(그리드) 봇 백테스팅

Auto bound : 자동으로 상,하단 가격 설정

Manual : 직접 상,하단 가격 설정

아래 그래프는 총 자산 변화입니다.(초기투자금액 + 현재 포지션 수익 + 그리드 수익)

거래소에서 그리드 봇 설정할 때 백테스팅 유용하게 써보세요!

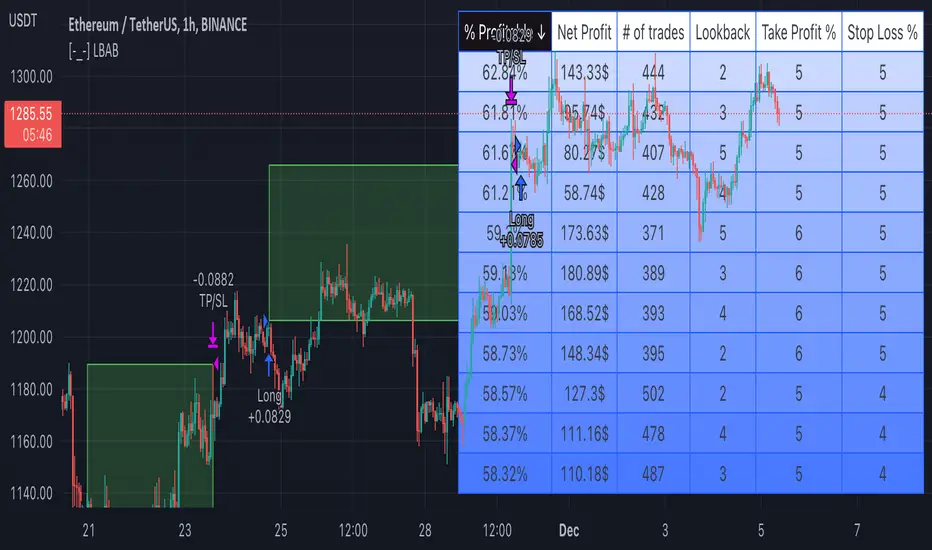

[-_-] Level Breakout, Auto Backtesting StrategyDescription:

A Long only strategy based on breakout from a certain level formed by High price. It has auto-backtesting capabilities (you set ranges for the three main parameters: Lookback, TP and SL; the strategy then goes through different combinations of those parameters and displays a table with results that you can sort by Percentage of profitable trades AND/OR Net profit AND/OR Number of trades). So you can, for example, sort only by Net profit to find combination of parameters that gives highest net profit, or sort by Net profit and Percentage profitable to find a combination of parameters that gives the best balance between profitability and profit. The auto-backtesting also takes into account the commission which is set in % in the inputs (make sure to set the same value in properties of the strategy so that auto-backtesting and real backtesting results match).

NOTE: auto-backtesting only find the best combinations and displays them in a table, you will then need to manually set the Lookback, TP and SL inputs for real backtesting to match.

Parameters:

- Lookback -> # of bars for filtering signals; recommended range from 2 to 5

- TP (%) -> take profit; recommended range from 5 to 10

- SL (%) -> stop loss; recommended range from 1 to 5

- Commission (%) -> commission per trade

- Min/Max Lookback -> lookback range for auto-backtesting

- Min/Max TP -> take profit range for auto-backtesting

- Min/Max SL -> stop loss range for auto-backtesting

- Percentage profitable -> sort by percentage of profitable trades

- Net profit -> sort by net profit

- Number of trades -> sort by number of trades

Strategy Backtesting Template [MYN]A few people have been asking me to share my backtesting template. Currently I use this as my starting point for validating existing strategies and developing new ones.

Features:

Trading Date Range

Trade Direction

4 progressive take profits with target percents and percentage of position to take profit on (Thanks adolgo)

Variable percentage Stop Loss

Automatic ProfitView Alert Syntax builder for Longs and Shorts

ADX checkbox to automatically add conditional logic to your strategy

Rainbow Strategy BacktestingRainbow Strategy Backtesting base on "Rainbow Moving Average" Strategy as below:

1.Rainbow Moving Average setup

- Source: source of 1st MA

- Type: SMA/EMA

- Period: period of 1st MA

- Displacement: period of 2nd MA to 7th MA with source is previous MA

2.Trend Define

- Up Trend: Main MA moving at the top of Rainbow

- Down Trend: Main MA moving at the bottom of Rainbow

- Sideway: Main MA moving between the top and the bottom of Rainbow

3.Signal

- Buy Signal: When Rainbow change to Up Trend.

- Sell Signal: When Rainbow change to Down Trend.

- Exit: When Rainbow change to Sideway.

4.RSI Filter

- "Enable": Only signals have 1st RSI moving between Overbought and Oversold and 2nd RSI moving outside Middle Channel are accepted.

- The filter may help trader avoid bull trap, bear trap and choppy market.

5.Backtesting Infomation

- Ticker: BTCUSDT

- Timeframe: H1

- Rainbow parameter:

+ Source: hlc3

+ Type: SMA

+ Period: 12

+ Displacement: 3

- RSI Filter parameter:

+ Enable

+ 1st RSI filter: period 12, overbought 65, oversold 35

+ 2nd RSI filter: period 9, upper middle 56, lower middle 44

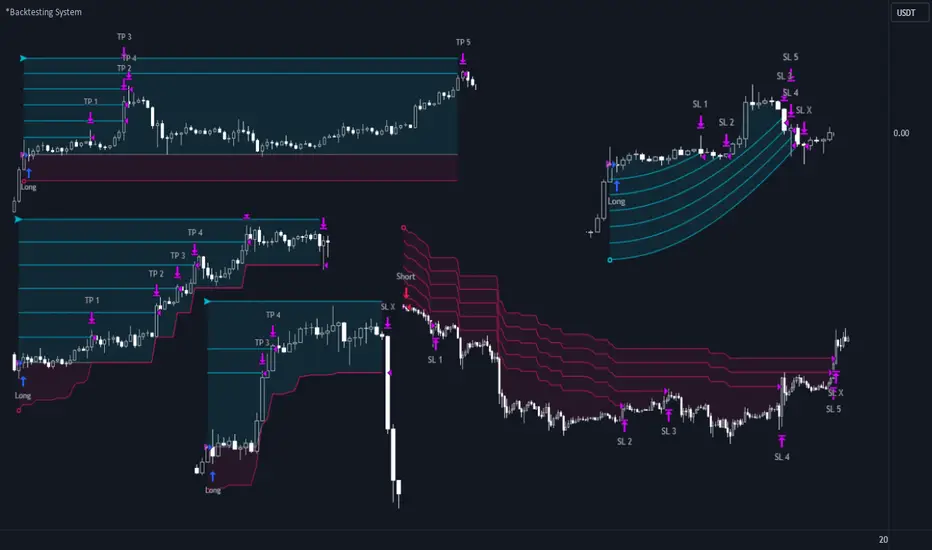

*Backtesting System ⚉ OVERVIEW ⚉

One of the best Systems for Backtesting your Strategies.

Incredibly flexible, simple, fast and feature-rich system — will solve most of your queries without much effort.

Many systems for setting StopLoss, TakeProfit, Risk Management and advanced Filters.

All you need to do is plug in your indicator and start Backtesting .

I intentionally left the option to use my System on Full Power before you load your indicator into it.

The system uses the built-in simple and popular moving average crossover signal for this purpose. (EMA 50 & 200).

Also Highly Recommend that you Fully use ALL of the features of this system so that you understand how they work before you ask questions.

Also tried to leave TIPS for each feature everywhere, read Tips, activate them and see how they work.

But before you use this system, I Recommend you to read the following description in Full.

—————— How to connect your indicator in 2 steps:

Adapt your indicator by adding only 2 lines of code and then connect it to this Backtesting System.

Step 1 — Create your connector, For doing so:

• 1 — Find or create in your indicator where are the conditions printing the Long-Buy and Short-Sell signals.

• 2 — Create an additional plot as below

I'm giving an example with a Two moving averages cross.

Please replicate the same methodology for your indicator wether it's a MACD, RSI , Pivots, or whatever indicator with Clear Buy and Sell conditions.

//@version=5

indicator('Moving Average Cross', overlay = true)

MA200 = ta.𝚎𝚖𝚊(close, 200)

MA50 = ta.𝚎𝚖𝚊(close, 50)

// Generate Buy and Sell conditions

buy = ta.crossover (MA200, MA50)

sell = ta.crossunder (MA200, MA50)

plot(MA200, color=color.green)

plot(MA50 , color=color.red )

bgcolor(color = buy ? color.green : sell ? color.red : na, title='SIGNALS')

// ———————————————— SIGNAL FOR SYSTEM ————————————————

Signal = buy ? +1 : sell ? -1 : 0

plot(Signal, title='🔌Connector🔌', display = display.none)

// —————— 🔥 The Backtesting System expects the value to be exactly +1 for the 𝚋𝚞𝚕𝚕𝚒𝚜𝚑 signal, and -1 for the 𝚋𝚎𝚊𝚛𝚒𝚜𝚑 signal

Basically, I identified my Buy & Sell conditions in the code and added this at the bottom of my indicator code

Now you can connect your indicator to the Backtesting System using the Step 2

Step 2 — Connect the connector

• 1 — Add your updated indicator to a TradingView chart and Add the Backtesting System as well to the SAME chart

• 2 — Open the Backtesting System settings and in the External Source field select your 🔌Connector🔌 (which comes from your indicator)

_______________________________

⚉ MAIN SETTINGS ⚉

‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

𝐄𝐱𝐭𝐞𝐫𝐧𝐚𝐥 𝐒𝐨𝐮𝐫𝐜𝐞 — Select your indicator. Add your indicator by following the 2 steps described above and select it in the menu. To familiarize yourself with the system until you select your indicator, you will have an in-built strategy of crossing the two moving EMA's of 50 and 200.

Long Deals — Enable/Disable Long Deals.

Short Deals — Enable/Disable Short Deals.

Wait End Deal — Enable/Disable waiting for a trade to close at Stop Loss/Take Profit. Until the trade closes on the Stop Loss or Take Profit, no new trade will open.

Reverse Deals — To force the opening of a trade in the opposite direction.

ReEntry Deal — Automatically open the same new deal after the deal is closed.

ReOpen Deal — Reopen the trade if the same signal is received. For example, if you are already in the long and a new signal is received in the long, the trade will reopen. * Does not work if Wait End Deal is enabled.

𝐓𝐚𝐤𝐞 𝐏𝐫𝐨𝐟𝐢𝐭:

None — Disables take profit. Useful if you only want to use dynamic stoplosses such as MA, Fast-Trailing, ATR Trail.

FIXED % — Fixed take profit in percent.

FIXED $ — Fixed Take in Money.

ATR — Fixed Take based on ATR.

R:R — Fixed Take based on the size of your stop loss. For example, if your stop is 10% and R:R=1, then the Take would be 10%. R:R=3 Take would be 30%, etc.

HH / LL — Fixed Take based on the previous maximum/minimum (extremum).

𝐒𝐭𝐨𝐩 𝐋𝐨𝐬𝐬:

None — Disables Stop Loss. Useful if you want to work without a stop loss. *Be careful if Wait End Deal is enabled, the trade may not close for a long time until it reaches the Take.

FIXED % — Fixed Stop in percent.

FIXED $ — Fixed Stop in Money.

TRAILING — Dynamic Trailing Stop like on the stock exchanges.

FAST TRAIL — Dynamic Fast Trailing Stop moves immediately in profit and stays in place if the price stands still or the price moves in loss.

ATR — Fixed Stop based on the ATR.

ATR TRAIL — Dynamic Trailing Stop based on the ATR.

LO / HI — A Fixed Stop based on the last Maximum/Minimum extemum. Allows you to place a stop just behind or above the low/high candle.

MA — Dynamic Stop based on selected Moving Average. * You will have 8 types of MA (EMA, SMA, HMA, etc.) to choose from, but you can easily add dozens of other MAs, which makes this type of stop incredibly flexible.

Add % — If true, then with the "𝗦𝘁𝗼𝗽 %" parameter you can add percentages to any of the current SL. Can be especially useful when using Stop - 𝗔𝗧𝗥 or 𝗠𝗔 or 𝗟𝗢/𝗛𝗜. For example with 𝗟𝗢/𝗛𝗜 to put a stop for the last High/Low and add 0.5% additional Stoploss.

Fixed R:R — If the stop loss is Dynamic (Trailing or MA) then if R:R true can also be made Dynamic * Use it carefully, the function is experimental.

_________________________________________

⚉ TAKE PROFIT LEVELS ⚉

‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

A unique method of constructing intermediate Take Profit Levels will allow you to select up to 5 intermediate Take Profit Levels and one intermediate Stop Loss.

Intermediate Take Profit Levels are perfectly calculated into 5 equal parts in the form of levels from the entry point to the final Take Profit target.

All you need to do is to choose the necessary levels for fixing and how much you want to fix at each level as a percentage. For example, TP 3 will always be exactly between the entry point and the Take Profit target. And the value of TP 3 = 50 will close 50% of the amount of the remaining size of the position.

Note: all intermediate SL/TP are closed from the remaining position amount and not from the initial position size, as TV does by default.

SL 0 Position — works in the same way as TP 1-5 but it's Stop. With this parameter you can set the position where the intermediate stop will be set.

Breakeven on TP — When activated, it allows you to put the stop loss at Breakeven after the selected TP is reached. For this function to work as it should - you need to activate an intermediate Take. For example, if TP 3 is activated and Breakeven on TP = 3, then after the price reaches this level, the Stop loss will go to Breakeven.

* This function will not work with Dynamic Stoplosses, because it simply does not make sense.

CoolDown # Bars — When activated, allows you to add a delay before a new trade is opened. A new trade after CoolDown will not be opened until # bars pass and a new signal appears.

_____________________________

⚉ TIME FILTERS ⚉

‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

Powerful time filter code that allows you to filter data based on specific time zones, dates, and session days. This code is ideal for those who need to analyze data from different time zones and weed out irrelevant data.

With Time Filter, you can easily set the starting and ending time zones by which you want to filter the data.

You can also set a start and end date for your data and choose which days of the week to include in the analysis. In addition, you can specify start and end times for a specific session, allowing you to focus your analysis on specific time periods.

_________________________________

⚉ SIGNAL FILTERS ⚉

‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

Signal Filters — allows you to easily customize and optimize your trading strategies based on 10 filters.

Each filter is designed to help you weed out inaccurate signals to minimize your risks.

Let's take a look at their features:

__________________________________

⚉ RISK MANAGEMENT ⚉

‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

Risk management tools that allow you to set the maximum number of losing trades in a row, a limit on the number of trades per day or week and other filters.

Loss Streak — Set Max number of consecutive loss trades.

Win Streak — Max Winning Streak Length.

Row Loss InDay — Max of consecutive days with a loss in a row.

DrawDown % — Max DrawDown (in % of strategy equity).

InDay Loss % — Set Max Intraday Loss.

Daily Trades — Limit the number of MAX trades per day.

Weekly Trades — Limit the number of MAX trades per week.

* 🡅 I would Not Recommend using these functions without understanding how they work.

Order Size — Position Size

• NONE — Use the default position size settings in Tab "Properties".

• EQUITY — The amount of the allowed position as a percentage of the initial capital.

• Use Net Profit — On/Off the use of profit in the following trades. *Only works if the type is EQUITY.

• SIZE — The size of the allowed position in monetary terms.

• Contracts — The size of the allowed position in the contracts. 1 Сontract = Сurrent price.

________________

⚉ NOTES ⚉

‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

It is important to note that I have never worked with Backtesting and the functions associated with them before.

It took me about a month of slow work to build this system.

I want to say Big Thanks:

• The PineScripters🌲 group, the guys suggested how to implement some features. Especially @allanster

• Thanks to all those people who share their developments for free on TV and not only.

• I also thank myself for not giving up and finishing the project, and not trying to monetize the system by selling it. * Although I really want the money :)

I tried hard to make it as fast and convenient as possible for everyone who will use my code.

That's why I didn't use any libraries and dozens of heavy functions, and I managed to fit in 8+-functions for the whole code.

Absolutely every block of code I tried to make full-fledged modular, that it was easy to import/edit for myself (you).

I have abused the Ternary Pine operator a little (a lot) so that the code was as compact as possible.

Nevertheless, I tried very hard to keep my code very understandable even for beginners.

At last I managed to write 500 lines of code, making it one of the fastest and most feature-rich systems out there.

I hope everyone enjoys my work.

Put comments and write likes.

Backtesting ModuleDo you often find yourself creating new 'strategy()' scripts for each trading system? Are you unable to focus on generating new systems due to fatigue and time loss incurred in the process? Here's a potential solution: the 'Backtesting Module' :)

INTRODUCTION

Every trading system is based on four basic conditions: long entry, long exit, short entry and short exit (which are typically defined as boolean series in Pine Script).

If you can define the conditions generated by your trading system as a series of integers, it becomes possible to use these variables in different scripts in efficient ways. (Pine Script is a convenient language that allows you to use the integer output of one indicator as a source in another.)

The 'Backtesting Module' is a dynamic strategy script designed to adapt to your signals. It boasts two notable features:

⮞ It produces a backtest report using the entry and exit variables you define.

⮞ It not only serves for system testing but also to combine independent signals into a single system. (This functionality enables to create complex strategies and report on their success!)

The module tests Golden and Death cross signals by default, when you enter your own conditions the default signals will be neutralized. The methodology is described below.

PREPARATION

There are three simple steps to connect your own indicator to the Module.

STEP 1

Firstly, you must define entry and exit variables in your own script. Let's elucidate it with a straightforward example. Consider a system generating long and short signals based on the intersections of two moving averages. Consequently, our conditions would be as follows:

// Signals

long = ta.crossover(ta.sma(close, 14), ta.sma(close, 28))

short = ta.crossunder(ta.sma(close, 14), ta.sma(close, 28))

Now, the question is: How can we convert boolean variables into integer variables? The answer is conditional ternary block, defined as follows:

// Entry & Exit

long_entry = long ? 1 : 0

long_exit = short ? 1 : 0

short_entry = short ? 1 : 0

short_exit = long ? 1 : 0

The mechanics of the Entry & Exit variables are simple. The variable takes on a value of 1 when your trading system generates the signal and if your system does not produce any signal, variable returns 0. In this example, you see how exit signals can be generated in a trading system that only contains entry signals. If you have a system with original exit signals, you can also use them directly. (Please mind the NOTES section below).

STEP 2

To utilize the Entry & Exit variables as source in another script, they must be plotted on the chart. Therefore, the final detail to include in the script containing your trading system would be as follows:

// Plot The Output

plot(long_entry, "Long Entry", display=display.data_window, editable=false)

plot(long_exit, "Long Exit", display=display.data_window, editable=false)

plot(short_entry, "Short Entry", display=display.data_window, editable=false)

plot(short_exit, "Short Exit", display=display.data_window, editable=false)

STEP 3

Now, we are ready to test the system! Load the Backtesting Module indicator onto the chart along with your trading system/indicator. Then set the outputs of your system (Long Entry, Long Exit, Short Entry, Short Exit) as source in the module. That's it.

FEATURES & ORIGINALITY

⮞ Primarily, this script has been created to provide you with an easy and practical method when testing your trading system.

⮞ I thought it might be nice to visualize a few useful results. The Backtesting Module provides insights into the outcomes of both long and short trades by computing the number of trades and the success percentage.

⮞ Through the 'Trade' parameter, users can specify the market direction in which the indicator is permitted to initiate positions.

⮞ Users have the flexibility to define the date range for the test.

⮞ There are optional features allowing users to plot entry prices on the chart and customize bar colors.

⮞ The report and the test date range are presented in a table on the chart screen. The entry price can be monitored in the data window.

⮞ Note that results are based on realized returns, and the open trade is not included in the displayed results. (The only exception is the 'Unrealized PNL' result in the table.)

STRATEGY SETTINGS

The default parameters are as follows:

⮞ Initial Balance : 10000 (in units of currency)

⮞ Quantity : 10% of equity

⮞ Commission : 0.04%

⮞ Slippage : 0

⮞ Dataset : All bars in the chart

For a realistic backtest result, you should size trades to only risk sustainable amounts of equity. Do not risk more than 5-10% on a trade. And ALWAYS configure your commission and slippage parameters according to pessimistic scenarios!

NOTES

⮞ This script is intended solely for development purposes. And it'll will be available for all the indicators I publish.

⮞ In this version of the module, all order types are designed as market orders. The exit size is the sum of the entry size.

⮞ As your trading conditions grow more intricate, you might need to define the outputs of your system in alternative ways. The method outlined in this description is tailored for straightforward signal structures.

⮞ Additionally, depending on the structure of your trading system, the backtest module may require further development. This encompasses stop-loss, take-profit, specific exit orders, quantity, margin and risk management calculations. I am considering releasing improvements that consider these options in future versions.

⮞ An example of how complex trading signals can be generated is the OTT Collection. If you're interested in seeing how the signals are constructed, you can use the link below.

THANKS

Special thanks to PineCoders for their valuable moderation efforts.

I hope this will be a useful example for the TradingView community...

DISCLAIMER

This is just an indicator, nothing more. It is provided for informational and educational purposes exclusively. The utilization of this script does not constitute professional or financial advice. The user solely bears the responsibility for risks associated with script usage. Do not forget to manage your risk. And trade as safely as possible. Best of luck!

Vortex Ocillator - backtestingbacktesting strategy for the vortex oscilator indicator, slightly modified on this version so that the buy and sell signals work with the backtesting and are consistant

original idea i posted by accident

the script with alerts

not intended to be financial advice, strategy is for made for testing

Biffy

Backtesting Period Selector | ComponentDescription

It's nice to quickly be able to set the backtesting period when writing strategies.

To make this process faster I wrote a simple 'component'.

So this is not a strategy but rather code you can plug-into your strategy and use

if you need that specific functionality.

Then it's just a matter of selecting which dates you want to backtest.

You can also chose to color the background to visually show the testing period.

Unfortunately, the background color is fixed at 'blue' for now.

Ps. I like the idea of writing small components to be pluged into other strategies

I'll try to develop this idea a bit further and see how small pieces of code can

easily provide specific functionality to assist and make deving strategies a bit less 'Pineful'.

Usage

First copy the instructed part of the component code over to your strategy.

Next, use the testPeriod() function to limit strategies to the specified backtesting period.

Example usage:

if testPeriod()

strategy.entry("LE", strategy.long)

Todo / Improvements

There are many ways to improve this component and I'm not a very good coder so this is a very crude solutions.

Anyway, here are some things which would be nice to improve:

1. Enable color selection so that the user can choose the background color of his own liking.

2. Improve naming of variables.

3. Test for ilogical choices, such as test period start being at a later date, than test period stop.

4. Account for time zones.

As always, any feedback, corrections or thoughts are very much welcome!

/pbergden

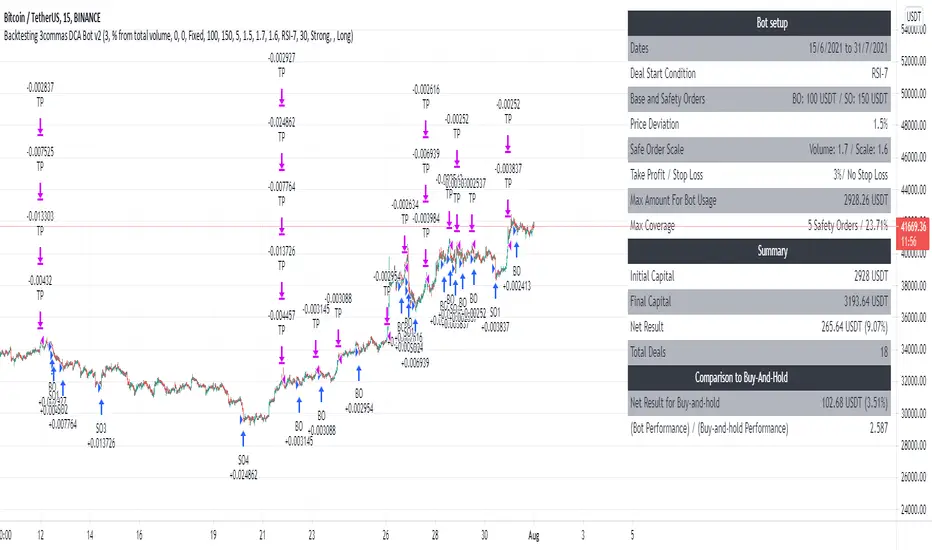

Backtesting 3commas DCA Bot v2Updating previously published simulated 3commas DCA logic with a sexier insert and more meaningful default parameters.

RSI MACD with conditional MA indicator backtestingbacktesting for the RSI MACD with conditional MA indicator:

BullBear with Volume-Percentile TP - Strategy [presentTrading] Happy New Year, everyone! I hope we have a fantastic year ahead.

It's been a while since I published an open script, but it's time to return.

This strategy introduces an indicator called Bull Bear Power, combined with an advanced take-profit system, which is the main innovative and educational aspect of this script. I hope all of you find some useful insights here. Welcome to engage in meaningful exchanges. This is a versatile tool suitable for both novice and experienced traders.

█ Introduction and How it is Different

Unlike traditional strategies that rely solely on price or volume indicators, this approach combines Bull Bear Power (BBP) with volume percentile analysis to identify optimal entry and exit points. It features a dynamic take-profit mechanism based on ATR (Average True Range) multipliers adjusted by volume and percentile factors, ensuring adaptability to diverse market conditions. This multifaceted strategy not only improves signal accuracy but also optimizes risk management, distinguishing it from conventional trading methods.

BTCUSD 6hr performance

Disable the visualization of Bull Bear Power (BBP) to clearly view the Z-Score.

█ Strategy, How it Works: Detailed Explanation

The BBP Strategy with Volume-Percentile TP utilizes several interconnected components to analyze market data and generate trading signals. Here's an overview with essential equations:

🔶 Core Indicators and Calculations

1. Exponential Moving Average (EMA):

- **Purpose:** Smoothens price data to identify trends.

- **Formula:**

EMA_t = (Close_t * (2 / (lengthInput + 1))) + (EMA_(t-1) * (1 - (2 / (lengthInput + 1))))

- Usage: Baseline for Bull and Bear Power.

2. Bull and Bear Power:

- Bull Power: `BullPower = High_t - EMA_t`

- Bear Power: `BearPower = Low_t - EMA_t`

- BBP:** `BBP = BullPower + BearPower`

- Interpretation: Positive BBP indicates bullish strength, negative indicates bearish.

3. Z-Score Calculation:

- Purpose: Normalizes BBP to assess deviation from the mean.

- Formula:

Z-Score = (BBP_t - bbp_mean) / bbp_std

- Components:

- `bbp_mean` = SMA of BBP over `zLength` periods.

- `bbp_std` = Standard deviation of BBP over `zLength` periods.

- Usage: Identifies overbought or oversold conditions based on thresholds.

🔶 Volume Analysis

1. Volume Moving Average (`vol_sma`):

vol_sma = (Volume_1 + Volume_2 + ... + Volume_vol_period) / vol_period

2. Volume Multiplier (`vol_mult`):

vol_mult = Current Volume / vol_sma

- Thresholds:

- High Volume: `vol_mult > 2.0`

- Medium Volume: `1.5 < vol_mult ≤ 2.0`

- Low Volume: `1.0 < vol_mult ≤ 1.5`

🔶 Percentile Analysis

1. Percentile Calculation (`calcPercentile`):

Percentile = (Number of values ≤ Current Value / perc_period) * 100

2. Thresholds:

- High Percentile: >90%

- Medium Percentile: >80%

- Low Percentile: >70%

🔶 Dynamic Take-Profit Mechanism

1. ATR-Based Targets:

TP1 Price = Entry Price ± (ATR * atrMult1 * TP_Factor)

TP2 Price = Entry Price ± (ATR * atrMult2 * TP_Factor)

TP3 Price = Entry Price ± (ATR * atrMult3 * TP_Factor)

- ATR Calculation:

ATR_t = (True Range_1 + True Range_2 + ... + True Range_baseAtrLength) / baseAtrLength

2. Adjustment Factors:

TP_Factor = (vol_score + price_score) / 2

- **vol_score** and **price_score** are based on current volume and price percentiles.

Local performance

🔶 Entry and Exit Logic

1. Long Entry: If Z-Score crosses above 1.618, then Enter Long.

2. Short Entry: If Z-Score crosses below -1.618, then Enter Short.

3. Exiting Positions:

If Long and Z-Score crosses below 0:

Exit Long

If Short and Z-Score crosses above 0:

Exit Short

4. Take-Profit Execution:

- Set multiple exit orders at dynamically calculated TP levels based on ATR and adjusted by `TP_Factor`.

█ Trade Direction

The strategy determines trade direction using the Z-Score from the BBP indicator:

- Long Positions:

- Condition: Z-Score crosses above 1.618.

- Short Positions:

- Condition: Z-Score crosses below -1.618.

- Exiting Trades:

- Long Exit: Z-Score drops below 0.

- Short Exit: Z-Score rises above 0.

This approach aligns trades with prevailing market trends, increasing the likelihood of successful outcomes.

█ Usage

Implementing the BBP Strategy with Volume-Percentile TP in TradingView involves:

1. Adding the Strategy:

- Copy the Pine Script code.

- Paste it into TradingView's Pine Editor.

- Save and apply the strategy to your chart.

2. Configuring Settings:

- Adjust parameters like EMA length, Z-Score thresholds, ATR multipliers, volume periods, and percentile settings to match your trading preferences and asset behavior.

3. Backtesting:

- Use TradingView’s backtesting tools to evaluate historical performance.

- Analyze metrics such as profit factor, drawdown, and win rate.

4. Optimization:

- Fine-tune parameters based on backtesting results.

- Test across different assets and timeframes to enhance adaptability.

5. Deployment:

- Apply the strategy in a live trading environment.

- Continuously monitor and adjust settings as market conditions change.

█ Default Settings

The BBP Strategy with Volume-Percentile TP includes default parameters designed for balanced performance across various markets. Understanding these settings and their impact is essential for optimizing strategy performance:

Bull Bear Power Settings:

- EMA Length (`lengthInput`): 21

- **Effect:** Balances sensitivity and trend identification; shorter lengths respond quicker but may generate false signals.

- Z-Score Length (`zLength`): 252

- **Effect:** Long period for stable mean and standard deviation, reducing false signals but less responsive to recent changes.

- Z-Score Threshold (`zThreshold`): 1.618

- **Effect:** Higher threshold filters out weaker signals, focusing on significant market moves.

Take Profit Settings:

- Use Take Profit (`useTP`): Enabled (`true`)

- **Effect:** Activates dynamic profit-taking, enhancing profitability and risk management.

- ATR Period (`baseAtrLength`): 20

- **Effect:** Shorter period for sensitive volatility measurement, allowing tighter profit targets.

- ATR Multipliers:

- **Effect:** Define conservative to aggressive profit targets based on volatility.

- Position Sizes:

- **Effect:** Diversifies profit-taking across multiple levels, balancing risk and reward.

Volume Analysis Settings:

- Volume MA Period (`vol_period`): 100

- **Effect:** Longer period for stable volume average, reducing the impact of short-term spikes.

- Volume Multipliers:

- **Effect:** Determines volume conditions affecting take-profit adjustments.

- Volume Factors:

- **Effect:** Adjusts ATR multipliers based on volume strength.

Percentile Analysis Settings:

- Percentile Period (`perc_period`): 100

- **Effect:** Balances historical context with responsiveness to recent data.

- Percentile Thresholds:

- **Effect:** Defines price and volume percentile levels influencing take-profit adjustments.

- Percentile Factors:

- **Effect:** Modulates ATR multipliers based on price percentile strength.

Impact on Performance:

- EMA Length: Shorter EMAs increase sensitivity but may cause more false signals; longer EMAs provide stability but react slower to market changes.

- Z-Score Parameters:*Longer Z-Score periods create more stable signals, while higher thresholds reduce trade frequency but increase signal reliability.

- ATR Multipliers and Position Sizes: Higher multipliers allow for larger profit targets with increased risk, while diversified position sizes help in securing profits at multiple levels.

- Volume and Percentile Settings: These adjustments ensure that take-profit targets adapt to current market conditions, enhancing flexibility and performance across different volatility environments.

- Commission and Slippage: Accurate settings prevent overestimation of profitability and ensure the strategy remains viable after accounting for trading costs.

Conclusion

The BBP Strategy with Volume-Percentile TP offers a robust framework by combining BBP indicators with volume and percentile analyses. Its dynamic take-profit mechanism, tailored through ATR adjustments, ensures that traders can effectively capture profits while managing risks in varying market conditions.

Bollinger Pair TradeNYSE:MA-1.6*NYSE:V

Revision: 1

Author: @ozdemirtrading

Revision 2 Considerations :

- Simplify and clean up plotting

Disclaimer: This strategy is currently working on the 5M chart. Change the length input to accommodate your needs.

For the backtesting of more than 3 months, you may need to upgrade your membership.

Description:

The general idea of the strategy is very straightforward: it takes positions according to the lower and upper Bollinger bands.

But I am mainly using this strategy for pair trading stocks. Do not forget that you will get better results if you trade with cointegrated pairs.

Bollinger band: Moving average & standard deviation are calculated based on 20 bars on the 1H chart (approx 240 bars on a 5m chart). X-day moving averages (20 days as default) are also used in the background in some of the exit strategy choices.

You can define position entry levels as the multipliers of standard deviation (for exp: mult2 as 2 * standard deviation).

There are 4 choices for the exit strategy:

SMA: Exit when touches simple moving average (SMA)

SKP: Skip SMA and do not stop if moving towards 20D SMA, and exit if it touches the other side of the band

SKPXDSMA: Skip SMA if moving towards 20D SMA, and exit if it touches 20D SMA

NoExit: Exit if it touches the upper & lower band only.

Options:

- Strategy hard stop: if trade loss reaches a point defined as a percent of the initial capital. Stop taking new positions. (not recommended for pair trade)

- Loss per trade: close position if the loss is at a defined level but keeps watching for new positions.

- Enable expected profit for trade (expected profit is calculated as the distance to SMA) (recommended for pair trade)

- Enable VIX threshold for the following options: (recommended for volatile periods)

- Stop trading if VIX for the previous day closes above the threshold

- Reverse active trade direction if VIX for the previous day is above the threshold

- Take reverse positions (assuming the Bollinger band is going to expand) for all trades

Backtesting:

Close positions after a defined interval: mark this if you want the close the final trade for backtesting purposes. Unmark it to get live signals.

Use custom interval: Backtest specific time periods.

Other Options:

- Use EMA: use an exponential moving average for the calculations instead of simple moving average

- Not against XDSMA: do not take a position against 20D SMA (if X is selected as 20) (recommended for pairs with a clear trend)

- Not in XDSMA 1 DEV: do not take a position in 20D SMA 1*standart deviation band (recommended if you need to decrease # of trades and increase profit for trade)

- Not in XDSMA 2 DEV: do not take a position in 20D SMA 2*standart deviation band

Session management:

- Not in session: Session start and end times can be defined here. If you do not want to trade in certain time intervals, mark that session.(helps to reduce slippage and get more realistic backtest results)

Simple and Profitable Scalping Strategy (ForexSignals TV)Strategy is based on the "SIMPLE and PROFITABLE Forex Scalping Strategy" taken from YouTube channel ForexSignals TV.

See video for a detailed explaination of the whole strategy.

I'm not entirely happy with the performance of this strategy yet however I do believe it has potential as the concept makes a lot of sense.

I'm open to any ideas people have on how it could be improved.

Strategy incorporates the following features:

Risk management:

Configurable X% loss per stop (default to 1%)

Configurable R:R ratio

Trade entry:

Based on stratgey conditions outlined below

Trade exit:

Based on stratgey conditions outlined below

Backtesting:

Configurable backtesting range by date

Trade drawings:

Each entry condition indicator can be turned on and off

TP/SL boxes drawn for all trades. Can be turned on and off

Trade exit information labels. Can be turned on and off

NOTE: Trade drawings will only be applicable when using overlay strategies

Debugging:

Includes section with useful debugging techniques

Strategy conditions

Trade entry:

LONG

C1: On higher timeframe trend EMAs, Fast EMA must be above Slow EMA

C2: On higher timeframe trend EMAs, price must be above Fast EMA

C3: On current timeframe entry EMAs, Fast EMA must be above Medium EMA and Medium EMA must be above Slow EMA

C4: On current timeframe entry EMAs, all 3 EMA lines must have fanned out in upward direction for previous X candles (configurable)

C5: On current timeframe entry EMAs, previous candle must have closed above and not touched any EMA lines

C6: On current timeframe entry EMAs, current candle must have pulled back to touch the EMA line(s)

C7: Price must break through the high of the last X candles (plus price buffer) to trigger entry (stop order entry)

SHORT

C1: On higher timeframe trend EMAs, Fast EMA must be below Slow EMA

C2: On higher timeframe trend EMAs, price must be below Fast EMA

C3: On current timeframe entry EMAs, Fast EMA must be below Medium EMA and Medium EMA must be below Slow EMA

C4: On current timeframe entry EMAs, all 3 EMA lines must have fanned out in downward direction for previous X candles (configurable)

C5: On current timeframe entry EMAs, previous candle must have closed above and not touched any EMA lines

C6: On current timeframe entry EMAs, current candle must have pulled back to touch the EMA line(s)

C7: Price must break through the low of the last X candles (plus price buffer) to trigger entry (stop order entry)

Trade entry:

Calculated position size based on risk tolerance

Entry price is a stop order set just above (buffer configurable) the recent swing high/low (long/short)

Trade exit:

Stop Loss is set just below (buffer configurable) trigger candle's low/high (long/short)

Take Profit calculated from Stop Loss using R:R ratio

Credits

"SIMPLE and PROFITABLE Forex Scalping Strategy" taken from YouTube channel ForexSignals TV

SSL + Wave Trend StrategyStrategy incorporates the following features:

Risk management:

Configurable X% loss per stop loss

Configurable R:R ratio

Trade entry:

Based on strategy conditions below

Trade exit:

Based on strategy conditions below

Backtesting:

Configurable backtesting range by date

Trade drawings:

Each entry condition indicator can be turned on and off

TP/SL boxes drawn for all trades. Can be turned on and off

Trade exit information labels. Can be turned on and off

NOTE: Trade drawings will only be applicable when using overlay strategies

Alerting:

Alerts on LONG and SHORT trade entries

Debugging:

Includes section with useful debugging techniques

Strategy conditions

Trade entry:

LONG

C1: SSL Hybrid baseline is BLUE

C2: SSL Channel crosses up (green above red)

C3: Wave Trend crosses up (represented by pink candle body)

C4: Entry candle height is not greater than configured threshold

C5: Entry candle is inside Keltner Channel (wicks or body depending on configuration)

C6: Take Profit target does not touch EMA (represents resistance)

SHORT

C1: SSL Hybrid baseline is RED

C2: SSL Channel crosses down (red above green)

C3: Wave Trend crosses down (represented by orange candle body)

C4: Entry candle height is not greater than configured threshold

C5: Entry candle is inside Keltner Channel (wicks or body depending on configuration)

C6: Take Profit target does not touch EMA (represents support)

Trade exit:

Stop Loss: Size configurable with NNFX ATR multiplier

Take Profit: Calculated from Stop Loss using R:R ratio

Credits

Strategy is based on the YouTube video "This Unique Strategy Made 47% Profit in 2.5 Months " by TradeSmart.

It combines the following indicators to determine trade entry/exit conditions:

Wave Trend: Indicator: WaveTrend Oscillator by @LazyBear

SSL Channel: SSL channel by @ErwinBeckers

SSL Hybrid: SSL Hybrid by @Mihkel00

Keltner Channels: Keltner Channels Bands by @ceyhun

Candle Height: Candle Height in Percentage - Columns by @FreeReveller

NNFX ATR: NNFX ATR by @sueun123

Risk Management Strategy TemplateThis strategy is intended to be used as a base template for building new strategies.

It incorporates the following features:

Risk management:

Configurable X% loss per stop loss

Configurable R:R ratio

Trade entry:

Calculated position size based on risk tolerance

Trade exit:

Stop Loss currently configurable ATR multiplier but can be replaced based on strategy

Take Profit calculated from Stop Loss using R:R ratio

Backtesting:

Configurable backtesting range by date

Trade drawings:

TP/SL boxes drawn for all trades. Can be turned on and off

Trade exit information labels. Can be turned on and off

NOTE: Trade drawings will only be applicable when using overlay strategies

Debugging:

Includes section with useful debugging techniques

Strategy conditions

Trade entry:

LONG

C1: Price is above EMA line

C2: RSI is crossing out of oversold area

SHORT

C1: Price is below EMA line

C2: RSI is crossing out of overbought area

Trade exit:

Stop Loss: Stop Loss ATR multiplier is hit

Take Profit: R:R multiplier * Stop Loss is hit

The idea is to use RSI to catch pullbacks within the main trend.

Note that this strategy is intended to be a simple base strategy for building upon. It was not designed to be traded in its current form.

Grid Spot Trading Algorithm V2 - The Quant ScienceGrid Spot Trading Algorithm V2 is the last grid trading algorithm made by our developer team.

Grid Spot Trading Algorithm V2 is a fixed 10-level grid trading algorithm. The grid is divided into an accumulation area (red) and a selling area (green).

In the accumulation area, the algorithm will place new buy orders, selling the long positions on the top of the grid.

BUYING AND SELLING LOGIC

The algorithm places up to 5 limit orders on the accumulation section of the grid, each time the price cross through the middle grid. Each single order uses 20% of the equity.

Positions are closed at the top of the grid by default, with the algorithm closing all orders at the first sell level. The exit level can be adjusted using the user interface, from the first level up to the fifth level above.

CONFIGURING THE ALGORITHM

1) Add it to the chart: Add the script to the current chart that you want to analyze.

2) Select the top of the grid: Confirm a price level with the mouse on which to fix the top of the grid.

3) Select the bottom of the grid: Confirm a price level with the mouse on which to fix the bottom of the grid.

4) Wait for the automatic creation of the grid.

USING THE ALGORITHM

Once the grid configuration process is completed, the algorithm will generate automatic backtesting.

You can add a stop loss that destroys the grid by setting the destruction price and activating the feature from the user interface. When the stop loss is activated, you can view it on the chart.

Custom Triple Moving Average Strategy | Auto BacktestingCreate your own MA Strategy set of up to three moving averages!

Auto Backtesting.

Cloud between MA1 and MA2.

Many different MA types to choose from.

Totally Custom!

Happy Trading, and algorithm analysis!

Gold Friday Anomaly StrategyThis script implements the " Gold Friday Anomaly Strategy ," a well-known historical trading strategy that leverages the gold market's behavior from Thursday evening to Friday close. It is a backtesting-focused strategy designed to assess the historical performance of this pattern. Traders use this anomaly as it captures a recurring market tendency observed over the years.

What It Does:

Entry Condition: The strategy enters a long position at the beginning of the Friday trading session (Thursday evening close) within the defined backtesting period.

Exit Condition: Friday evening close.

Backtesting Controls: Allows users to set custom backtesting periods to evaluate strategy performance over specific date ranges.

Key Features:

Custom Backtest Periods: Easily configurable inputs to set the start and end date of the backtesting range.

Fixed Slippage and Commission Settings: Ensures realistic simulation of trading conditions.

Process Orders on Close: Backtesting is optimized by processing orders at the bar's close.

Important Notes:

Backtesting Only: This script is intended purely for backtesting purposes. Past performance is not indicative of future results.

Live Trading Recommendations: For live trading, it is highly recommended to use limit orders instead of market orders, especially during evening sessions, as market order slippage can be significant.

Default Settings:

Entry size: 10% of equity per trade.

Slippage: 1 tick.

Commission: 0.05% per trade.

FreedX Grid Backtest█ FreedX Grid Backtest is an open-source tool that offers accurate GRID calculations for GRID trading strategies. This advanced tool allows users to backtest GRID trading parameters with precision, accurately reflecting exchange functionalities. We are committed to enhancing trading strategies through precise backtesting solutions and address the issue of unreliable backtesting practices observed on GRID trading strategies. FreedX Grid Backtest is designed for optimal calculation speed and plotting efficiency, ensuring users to achieve fastest calculations during their analysis.

█ GRID TRADING STRATEGY SETTINGS

The core of the FreedX Grid Backtest tool lies in its ability to simulate grid trading strategies. Grid trading involves placing orders at regular intervals within a predefined price range, creating a grid of orders that capitalize on market volatility.

Features:

⚙️ Backtest Range:

→ Purpose: Allows users to specify the backtesting range of GRID strategy. Closes all positions at the end of this range.

→ How to Use: Drag the dates to fit the desired backtesting range.

⚙️ Investment & Compounding:

→ Purpose: Allows users to specify the total investment amount and select between fixed and compound investment strategies. Compounding adjusts trade quantities based on performance, enhancing the grid strategy's adaptability to market changes.

→ How to Use: Set the desired investment amount and choose between "Fixed" or "Compound" for the investment method.

⚙️ Leverage & Grid Levels:

→ Purpose: Leverage amplifies the investment amount, increasing potential returns (and risks). Users can define the number of grid levels, which determines how the investment is distributed across the grid.

→ How to Use: Input the desired leverage and number of grids. The tool automatically calculates the distribution of funds across each grid level.

⚙️ Distribution Type & Mode:

→ Purpose: Users can select the distribution type (Arithmetic or Geometric) to set how grid levels are determined. The mode (Neutral, Long, Short) dictates the direction of trades within the grid.

→ How to Use: Choose the distribution type and mode based on the desired trading strategy and market outlook.

⚙️ Enable LONG/SHORT Grids exclusively:

█ MANUAL LEVELS AND STOP TRIGGERS

Beyond automated settings, the tool offers manual adjustments for traders seeking finer control over their grid strategies.

Features:

⚙️ Manual Level Adjustment:

→ Purpose: Enables traders to manually set the top, reference, and bottom levels of the grid, offering precision control over the trading range.

→ How to Use: Activate manual levels and adjust the top, reference, and bottom levels as needed to define the grid's scope.

⚙️ Stop Triggers:

→ Purpose: Provides an option to set upper and lower price limits, acting as stop triggers to close or terminate trades. This feature safeguards investments against significant market movements outside the anticipated range.

→ How to Use: Enable stop triggers and specify the upper and lower limits. The tool will automatically manage positions based on these parameters.

---

This guide gives you a quick and clear overview of the FreedX Grid Backtest tool, explaining how you can use this cutting-edge tool to improve your trading strategies.

Why is it ok to backtest on TradingView from now on!TradingView backtester has bad reputation. For a good reason - it was producing wrong results, and it was clear at first sight how bad they were.

But this has changed. Along with many other improvements in its PineScript coding capabilities, TradingView fixed important bug, which was the main reason for miscalculations. TradingView didn't really speak out about this fix, so let me try :)

Have a look at this short code of a swing trading strategy (PLEASE DON'T FOCUS ON BACKTEST RESULTS ATTACHED HERE - THEY DO NOT MATTER). Sometimes entry condition happens together with closing condition for the already ongoing trade. Example: the condition to close Long entry is the same as a condition to enter Short. And when these two aligned, not only a Long was closed and Short was entered (as intended), but also a second Short was entered, too!!! What's even worse, that second short was not controlled with closing conditions inside strategy.exit() function and it very often lead to losses exceeding whatever was declared in "loss=" parameter. This could not have worked well...

But HOORAY!!! - it has been fixed and won't happen anymore. So together with other improvements - TradingView's backtester and PineScript is now ok to work with on standard candlesticks :)

Yep, no need to code strategies and backtest them on other platforms anymore.

----------------

Having said the above, there are still some pitfalls remaining, which you need to be aware of and avoid:

Don't backtest on HeikenAshi, Renko, Kagi candlesticks. They were not invented with backtesting in mind. There are still using wrong price levels for entries and therefore producing always too good backtesting results. Only standard candlesticks are reliable to backtest on.

Don't use Trailing Stop in your code. TradingView operates only on closed candlesticks, not on tick data and because of that, backtester will always assume price has first reached its favourable extreme (so 'high' when you are in Long trade and 'low' when you are in Short trade) before it starts to pull back. Which is rarely the truth in reality. Therefore strategies using Trailing Stop are also producing too good backtesting results. It is especially well visible on higher timeframe strategies - for some reason your strategy manages to make gains on those huge, fat candlesticks :) But that's not reality.

"when=" inside strategy.exit() does not work as you would intuitively expect. If you want to have logical condition to close your trade (for example - crossover(rsi(close,14),20)) you need to place it inside strategy.close() function. And leave StopLoss + TakeProfit conditions inside strategy.exit() function. Just as in attached code.

If you're working with pyramiding, add "process_orders_on_close=ANY" to your strategy() script header. Default setting ("=FIFO") will first close the trade, which was opened first, not the one which was hit by Stop-Loss condidtion.

----------------

That's it, I guess :) If you are noticing other issues with backtester and would like to share, let everyone know in comments. If the issue is indeed a bug, there is a chance TradingView dev team will hear your voice and take it into account when working on other improvements. Just like they heard about the bug I described above.

P.S. I know for a fact that more improvements in the backtesting area are coming. Some will change the game even for non-coding traders. If you want to be notified quickly and with my comment - gimme "follow".