Institutional Volume Profile# Institutional Volume Profile (IVP) - Advanced Volume Analysis Indicator

## Overview

The Institutional Volume Profile (IVP) is a sophisticated technical analysis tool that combines traditional volume profile analysis with institutional volume detection algorithms. This indicator helps traders identify key price levels where significant institutional activity has occurred, providing insights into market structure and potential support/resistance zones.

## Key Features

### 🎯 Volume Profile Analysis

- **Point of Control (POC)**: Identifies the price level with the highest volume activity

- **Value Area**: Highlights the price range containing a specified percentage (default 70%) of total volume

- **Multi-Row Distribution**: Displays volume distribution across 10-50 price levels for detailed analysis

- **Customizable Period**: Analyze volume profiles over 10-500 bars

### 🏛️ Institutional Volume Detection

- **Pocket Pivot Volume (PPV)**: Detects bullish institutional buying when up-volume exceeds recent down-volume peaks

- **Pivot Negative Volume (PNV)**: Identifies bearish institutional selling when down-volume exceeds recent up-volume peaks

- **Accumulation Detection**: Spots potential accumulation phases with high volume and narrow price ranges

- **Distribution Analysis**: Identifies distribution patterns with high volume but minimal price movement

### 🎨 Visual Customization Options

- **Multiple Color Schemes**: Heat Map, Institutional, Monochrome, and Rainbow themes

- **Bar Styles**: Solid, Gradient, Outlined, and 3D Effect rendering

- **Volume Intensity Display**: Visual intensity based on volume magnitude

- **Flexible Positioning**: Left or right side profile placement

- **Current Price Highlighting**: Real-time price level indication

### 📊 Advanced Visual Features

- **Volume Labels**: Display volume amounts at key price levels

- **Gradient Effects**: Multi-step gradient rendering for enhanced visibility

- **3D Styling**: Shadow effects for professional appearance

- **Opacity Control**: Adjustable transparency (10-100%)

- **Border Customization**: Configurable border width and styling

## How It Works

### Volume Distribution Algorithm

The indicator analyzes each bar within the specified period and distributes its volume proportionally across the price levels it touches. This creates an accurate representation of where trading activity has been concentrated.

### Institutional Detection Logic

- **PPV Trigger**: Current up-bar volume > highest down-volume in lookback period + above volume MA

- **PNV Trigger**: Current down-bar volume > highest up-volume in lookback period + above volume MA

- **Accumulation**: High volume + narrow range + bullish close

- **Distribution**: Very high volume + minimal price movement

### Value Area Calculation

Starting from the POC, the algorithm expands both upward and downward, adding volume until reaching the specified percentage of total volume (default 70%).

## Configuration Parameters

### Profile Settings

- **Profile Period**: 10-500 bars (default: 50)

- **Number of Rows**: 10-50 levels (default: 24)

- **Profile Width**: 10-100% of screen (default: 30%)

- **Value Area %**: 50-90% (default: 70%)

### Institutional Analysis

- **PPV Lookback Days**: 5-20 periods (default: 10)

- **Volume MA Length**: 10-200 periods (default: 50)

- **Institutional Threshold**: 1.0-2.0x multiplier (default: 1.2)

### Visual Controls

- **Bar Style**: Solid, Gradient, Outlined, 3D Effect

- **Color Scheme**: Heat Map, Institutional, Monochrome, Rainbow

- **Profile Position**: Left or Right side

- **Opacity**: 10-100%

- **Show Labels**: Volume amount display toggle

## Interpretation Guide

### Volume Profile Elements

- **Thick Horizontal Bars**: High volume nodes (strong support/resistance)

- **Thin Horizontal Bars**: Low volume nodes (weak levels)

- **White Line (POC)**: Strongest support/resistance level

- **Blue Highlighted Area**: Value Area (fair value zone)

### Institutional Signals

- **Blue Triangles (PPV)**: Bullish institutional buying detected

- **Orange Triangles (PNV)**: Bearish institutional selling detected

- **Color-Coded Bars**: Different colors indicate institutional activity types

### Color Scheme Meanings

- **Heat Map**: Red (high volume) → Orange → Yellow → Gray (low volume)

- **Institutional**: Blue (PPV), Orange (PNV), Aqua (Accumulation), Yellow (Distribution)

- **Monochrome**: Grayscale intensity based on volume

- **Rainbow**: Color-coded by price level position

## Trading Applications

### Support and Resistance

- POC acts as dynamic support/resistance

- High volume nodes indicate strong price levels

- Low volume areas suggest potential breakout zones

### Institutional Activity

- PPV above Value Area: Strong bullish signal

- PNV below Value Area: Strong bearish signal

- Accumulation patterns: Potential upward breakouts

- Distribution patterns: Potential downward pressure

### Market Structure Analysis

- Value Area defines fair value range

- Profile shape indicates market sentiment

- Volume gaps suggest potential price targets

## Alert Conditions

- PPV Detection at current price level

- PNV Detection at current price level

- PPV above Value Area (strong bullish)

- PNV below Value Area (strong bearish)

## Best Practices

1. Use multiple timeframes for confirmation

2. Combine with price action analysis

3. Pay attention to volume context (above/below average)

4. Monitor institutional signals near key levels

5. Consider overall market conditions

## Technical Notes

- Maximum 500 boxes and 100 labels for optimal performance

- Real-time calculations update on each bar close

- Historical analysis uses complete bar data

- Compatible with all TradingView chart types and timeframes

---

*This indicator is designed for educational and informational purposes. Always combine with other analysis methods and risk management strategies.*

Wyszukaj w skryptach "algo"

DisplayUtilitiesLibrary "DisplayUtilities"

Display utilities for color management and visual presentation

get_direction_color(direction, up_excessive, up_normal, neutral, down_normal, down_excessive)

Get candle color based on direction and color scheme

Parameters:

direction (int) : Direction value (-2, -1, 0, 1, 2)

up_excessive (color) : Color for +2 direction

up_normal (color) : Color for +1 direction

neutral (color) : Color for 0 direction

down_normal (color) : Color for -1 direction

down_excessive (color) : Color for -2 direction

Returns: Appropriate color for the direction

get_candle_paint_directions(paint_opt, body_dir, bar_dir, breakout_dir, combined_dir)

Get candle directions for different painting algorithms

Parameters:

paint_opt (string) : Painting option algorithm

body_dir (int) : Body direction

bar_dir (int) : Bar direction

breakout_dir (int) : Breakout direction

combined_dir (int) : Combined direction

Returns:

get_bias_paint_directions(paint_bias, unified_dir)

Get paint directions based on bias filter

Parameters:

paint_bias (string) : Paint bias option ("All", "Bull Bias", "Bear Bias")

unified_dir (int) : Unified direction

Returns: Directions for two plotcandle series

get_transparency_levels(sf_filtered, fade_option, fade_opacity)

Calculate transparency levels for strength factor filtering

Parameters:

sf_filtered (bool) : Is strength factor filtered

fade_option (string) : Fade option ("Disabled", "Fade Candle", "Do Not Fade Wick", "Do Not Fade Wick and Border")

fade_opacity (int) : Fade opacity percentage

Returns:

get_strength_factor_filter(filter_option, individual_filters)

Generate strength factor filter conditions

Parameters:

filter_option (string) : Filter option string

individual_filters (map) : Map of individual filter conditions

Returns: Boolean filter result

get_signal_bar_condition(signal_option, individual_filters)

Generate signal bar conditions (inverted filters)

Parameters:

signal_option (string) : Signal bar option string

individual_filters (map) : Map of individual filter conditions

Returns: Boolean signal bar result

get_zscore_signal_condition(z_signal_option, z_filters)

Get Z-score signal bar conditions

Parameters:

z_signal_option (string) : Z-score signal option

z_filters (map) : Map of Z-score filters

Returns: Boolean Z-score signal condition

get_standard_colors()

Create a standard color scheme for directions

Returns: Standard color set

apply_zscore_modification(original_dir, z_filtered)

Modify directions for Z-score excess display

Parameters:

original_dir (int) : Original direction

z_filtered (bool) : Is Z-score filtered (shows excess)

Returns: Modified direction (doubled if excess detected)

get_default_fade_colors()

Get default fade colors for strength factor overlay

Returns: Default colors for TV overlay

should_paint_candles(paint_algo)

Check if paint algorithm should show candles

Parameters:

paint_algo (string) : Paint algorithm option

Returns: True if algorithm should display candles

get_signal_bar_char(signal_type, is_bullish)

Get signal bar character based on signal type

Parameters:

signal_type (string) : Signal type ("strength_factor" or "zscore")

is_bullish (bool) : Direction is bullish

Returns: Character and location for plotchar

get_signal_bar_color(signal_type, is_bullish)

Get signal bar colors

Parameters:

signal_type (string) : Signal type ("strength_factor" or "zscore")

is_bullish (bool) : Direction is bullish

Returns: Signal bar color

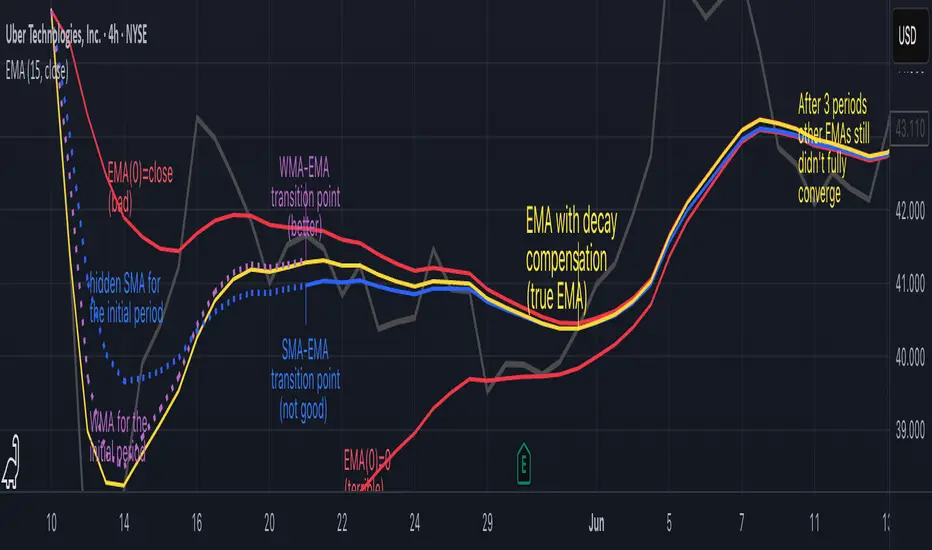

Why EMA Isn't What You Think It IsMany new traders adopt the Exponential Moving Average (EMA) believing it's simply a "better Simple Moving Average (SMA)". This common misconception leads to fundamental misunderstandings about how EMA works and when to use it.

EMA and SMA differ at their core. SMA use a window of finite number of data points, giving equal weight to each data point in the calculation period. This makes SMA a Finite Impulse Response (FIR) filter in signal processing terms. Remember that FIR means that "all that we need is the 'period' number of data points" to calculate the filter value. Anything beyond the given period is not relevant to FIR filters – much like how a security camera with 14-day storage automatically overwrites older footage, making last month's activity completely invisible regardless of how important it might have been.

EMA, however, is an Infinite Impulse Response (IIR) filter. It uses ALL historical data, with each past price having a diminishing - but never zero - influence on the calculated value. This creates an EMA response that extends infinitely into the past—not just for the last N periods. IIR filters cannot be precise if we give them only a 'period' number of data to work on - they will be off-target significantly due to lack of context, like trying to understand Game of Thrones by watching only the final season and wondering why everyone's so upset about that dragon lady going full pyromaniac.

If we only consider a number of data points equal to the EMA's period, we are capturing no more than 86.5% of the total weight of the EMA calculation. Relying on he period window alone (the warm-up period) will provide only 1 - (1 / e^2) weights, which is approximately 1−0.1353 = 0.8647 = 86.5%. That's like claiming you've read a book when you've skipped the first few chapters – technically, you got most of it, but you probably miss some crucial early context.

▶️ What is period in EMA used for?

What does a period parameter really mean for EMA? When we select a 15-period EMA, we're not selecting a window of 15 data points as with an SMA. Instead, we are using that number to calculate a decay factor (α) that determines how quickly older data loses influence in EMA result. Every trader knows EMA calculation: α = 1 / (1+period) – or at least every trader claims to know this while secretly checking the formula when they need it.

Thinking in terms of "period" seriously restricts EMA. The α parameter can be - should be! - any value between 0.0 and 1.0, offering infinite tuning possibilities of the indicator. When we limit ourselves to whole-number periods that we use in FIR indicators, we can only access a small subset of possible IIR calculations – it's like having access to the entire RGB color spectrum with 16.7 million possible colors but stubbornly sticking to the 8 basic crayons in a child's first art set because the coloring book only mentioned those by name.

For example:

Period 10 → alpha = 0.1818

Period 11 → alpha = 0.1667

What about wanting an alpha of 0.17, which might yield superior returns in your strategy that uses EMA? No whole-number period can provide this! Direct α parameterization offers more precision, much like how an analog tuner lets you find the perfect radio frequency while digital presets force you to choose only from predetermined stations, potentially missing the clearest signal sitting right between channels.

Sidenote: the choice of α = 1 / (1+period) is just a convention from 1970s, probably started by J. Welles Wilder, who popularized the use of the 14-day EMA. It was designed to create an approximate equivalence between EMA and SMA over the same number of periods, even thought SMA needs a period window (as it is FIR filter) and EMA doesn't. In reality, the decay factor α in EMA should be allowed any valye between 0.0 and 1.0, not just some discrete values derived from an integer-based period! Algorithmic systems should find the best α decay for EMA directly, allowing the system to fine-tune at will and not through conversion of integer period to float α decay – though this might put a few traditionalist traders into early retirement. Well, to prevent that, most traditionalist implementations of EMA only use period and no alpha at all. Heaven forbid we disturb people who print their charts on paper, draw trendlines with rulers, and insist the market "feels different" since computers do algotrading!

▶️ Calculating EMAs Efficiently

The standard textbook formula for EMA is:

EMA = CurrentPrice × alpha + PreviousEMA × (1 - alpha)

But did you know that a more efficient version exists, once you apply a tiny bit of high school algebra:

EMA = alpha × (CurrentPrice - PreviousEMA) + PreviousEMA

The first one requires three operations: 2 multiplications + 1 addition. The second one also requires three ops: 1 multiplication + 1 addition + 1 subtraction.

That's pathetic, you say? Not worth implementing? In most computational models, multiplications cost much more than additions/subtractions – much like how ordering dessert costs more than asking for a water refill at restaurants.

Relative CPU cost of float operations :

Addition/Subtraction: ~1 cycle

Multiplication: ~5 cycles (depending on precision and architecture)

Now you see the difference? 2 * 5 + 1 = 11 against 5 + 1 + 1 = 7. That is ≈ 36.36% efficiency gain just by swapping formulas around! And making your high school math teacher proud enough to finally put your test on the refrigerator.

▶️ The Warmup Problem: how to start the EMA sequence right

How do we calculate the first EMA value when there's no previous EMA available? Let's see some possible options used throughout the history:

Start with zero : EMA(0) = 0. This creates stupidly large distortion until enough bars pass for the horrible effect to diminish – like starting a trading account with zero balance but backdating a year of missed trades, then watching your balance struggle to climb out of a phantom debt for months.

Start with first price : EMA(0) = first price. This is better than starting with zero, but still causes initial distortion that will be extra-bad if the first price is an outlier – like forming your entire opinion of a stock based solely on its IPO day price, then wondering why your model is tanking for weeks afterward.

Use SMA for warmup : This is the tradition from the pencil-and-paper era of technical analysis – when calculators were luxury items and "algorithmic trading" meant your broker had neat handwriting. We first calculate an SMA over the initial period, then kickstart the EMA with this average value. It's widely used due to tradition, not merit, creating a mathematical Frankenstein that uses an FIR filter (SMA) during the initial period before abruptly switching to an IIR filter (EMA). This methodology is so aesthetically offensive (abrupt kink on the transition from SMA to EMA) that charting platforms hide these early values entirely, pretending EMA simply doesn't exist until the warmup period passes – the technical analysis equivalent of sweeping dust under the rug.

Use WMA for warmup : This one was never popular because it is harder to calculate with a pencil - compared to using simple SMA for warmup. Weighted Moving Average provides a much better approximation of a starting value as its linear descending profile is much closer to the EMA's decay profile.

These methods all share one problem: they produce inaccurate initial values that traders often hide or discard, much like how hedge funds conveniently report awesome performance "since strategy inception" only after their disastrous first quarter has been surgically removed from the track record.

▶️ A Better Way to start EMA: Decaying compensation

Think of it this way: An ideal EMA uses an infinite history of prices, but we only have data starting from a specific point. This creates a problem - our EMA starts with an incorrect assumption that all previous prices were all zero, all close, or all average – like trying to write someone's biography but only having information about their life since last Tuesday.

But there is a better way. It requires more than high school math comprehension and is more computationally intensive, but is mathematically correct and numerically stable. This approach involves compensating calculated EMA values for the "phantom data" that would have existed before our first price point.

Here's how phantom data compensation works:

We start our normal EMA calculation:

EMA_today = EMA_yesterday + α × (Price_today - EMA_yesterday)

But we add a correction factor that adjusts for the missing history:

Correction = 1 at the start

Correction = Correction × (1-α) after each calculation

We then apply this correction:

True_EMA = Raw_EMA / (1-Correction)

This correction factor starts at 1 (full compensation effect) and gets exponentially smaller with each new price bar. After enough data points, the correction becomes so small (i.e., below 0.0000000001) that we can stop applying it as it is no longer relevant.

Let's see how this works in practice:

For the first price bar:

Raw_EMA = 0

Correction = 1

True_EMA = Price (since 0 ÷ (1-1) is undefined, we use the first price)

For the second price bar:

Raw_EMA = α × (Price_2 - 0) + 0 = α × Price_2

Correction = 1 × (1-α) = (1-α)

True_EMA = α × Price_2 ÷ (1-(1-α)) = Price_2

For the third price bar:

Raw_EMA updates using the standard formula

Correction = (1-α) × (1-α) = (1-α)²

True_EMA = Raw_EMA ÷ (1-(1-α)²)

With each new price, the correction factor shrinks exponentially. After about -log₁₀(1e-10)/log₁₀(1-α) bars, the correction becomes negligible, and our EMA calculation matches what we would get if we had infinite historical data.

This approach provides accurate EMA values from the very first calculation. There's no need to use SMA for warmup or discard early values before output converges - EMA is mathematically correct from first value, ready to party without the awkward warmup phase.

Here is Pine Script 6 implementation of EMA that can take alpha parameter directly (or period if desired), returns valid values from the start, is resilient to dirty input values, uses decaying compensator instead of SMA, and uses the least amount of computational cycles possible.

// Enhanced EMA function with proper initialization and efficient calculation

ema(series float source, simple int period=0, simple float alpha=0)=>

// Input validation - one of alpha or period must be provided

if alpha<=0 and period<=0

runtime.error("Alpha or period must be provided")

// Calculate alpha from period if alpha not directly specified

float a = alpha > 0 ? alpha : 2.0 / math.max(period, 1)

// Initialize variables for EMA calculation

var float ema = na // Stores raw EMA value

var float result = na // Stores final corrected EMA

var float e = 1.0 // Decay compensation factor

var bool warmup = true // Flag for warmup phase

if not na(source)

if na(ema)

// First value case - initialize EMA to zero

// (we'll correct this immediately with the compensation)

ema := 0

result := source

else

// Standard EMA calculation (optimized formula)

ema := a * (source - ema) + ema

if warmup

// During warmup phase, apply decay compensation

e *= (1-a) // Update decay factor

float c = 1.0 / (1.0 - e) // Calculate correction multiplier

result := c * ema // Apply correction

// Stop warmup phase when correction becomes negligible

if e <= 1e-10

warmup := false

else

// After warmup, EMA operates without correction

result := ema

result // Return the properly compensated EMA value

▶️ CONCLUSION

EMA isn't just a "better SMA"—it is a fundamentally different tool, like how a submarine differs from a sailboat – both float, but the similarities end there. EMA responds to inputs differently, weighs historical data differently, and requires different initialization techniques.

By understanding these differences, traders can make more informed decisions about when and how to use EMA in trading strategies. And as EMA is embedded in so many other complex and compound indicators and strategies, if system uses tainted and inferior EMA calculatiomn, it is doing a disservice to all derivative indicators too – like building a skyscraper on a foundation of Jell-O.

The next time you add an EMA to your chart, remember: you're not just looking at a "faster moving average." You're using an INFINITE IMPULSE RESPONSE filter that carries the echo of all previous price actions, properly weighted to help make better trading decisions.

EMA done right might significantly improve the quality of all signals, strategies, and trades that rely on EMA somewhere deep in its algorithmic bowels – proving once again that math skills are indeed useful after high school, no matter what your guidance counselor told you.

Smarter Money Concepts - OBs [PhenLabs]📊 Smarter Money Concepts - OBs

Version: PineScript™ v6

📌 Description

Smarter Money Concepts - OBs (Order Blocks) is an advanced technical analysis tool designed to identify and visualize institutional order zones on your charts. Order blocks represent significant areas of liquidity where smart money has entered positions before major moves. By tracking these zones, traders can anticipate potential reversals, continuations, and key reaction points in price action.

This indicator incorporates volume filtering technology to identify only the most significant order blocks, eliminating low-quality signals and focusing on areas where institutional participation is likely present. The combination of price structure analysis and volume confirmation provides traders with high-probability zones that may attract future price action for tests, rejections, or breakouts.

🚀 Points of Innovation

Volume-Filtered Block Detection : Identifies only order blocks formed with significant volume, focusing on areas with institutional participation

Advanced Break of Structure Logic : Uses sophisticated price action analysis to detect legitimate market structure breaks preceding order blocks

Dynamic Block Management : Intelligently tracks, extends, and removes order blocks based on price interaction and time-based expiration

Structure Recognition System : Employs technical analysis algorithms to find significant swing points for accurate order block identification

Dual Directional Tracking : Simultaneously monitors both bullish and bearish order blocks for comprehensive market structure analysis

🔧 Core Components

Order Block Detection : Identifies institutional entry zones by analyzing price action before significant breaks of structure, capturing where smart money has likely positioned before moves.

Volume Filtering Algorithm : Calculates relative volume compared to a moving average to qualify only order blocks formed with significant market participation, eliminating noise.

Structure Break Recognition : Uses price action analysis to detect legitimate breaks of market structure, ensuring order blocks are identified only at significant market turning points.

Dynamic Block Management : Continuously monitors price interaction with existing blocks, extending, maintaining, or removing them based on current market behavior.

🔥 Key Features

Volume-Based Filtering : Filter out insignificant blocks by requiring a minimum volume threshold, focusing only on zones with likely institutional activity

Visual Block Highlighting : Color-coded boxes clearly mark bullish and bearish order blocks with customizable appearance

Flexible Mitigation Options : Choose between “Wick” or “Close” methods for determining when a block has been tested or mitigated

Scan Range Adjustment : Customize how far back the indicator looks for structure points to adapt to different market conditions and timeframes

Break Source Selection : Configure which price component (close, open, high, low) is used to determine structure breaks for precise block identification

🎨 Visualization

Bullish Order Blocks : Blue-colored rectangles highlighting zones where bullish institutional orders were likely placed before upward moves, representing potential support areas.

Bearish Order Blocks : Red-colored rectangles highlighting zones where bearish institutional orders were likely placed before downward moves, representing potential resistance areas.

Block Extension : Order blocks extend to the right of the chart, providing clear visualization of these significant zones as price continues to develop.

📖 Usage Guidelines

Order Block Settings

Scan Range : Default: 25. Defines how many bars the indicator scans to determine significant structure points for order block identification.

Bull Break Price Source : Default: Close. Determines which price component is used to detect bullish breaks of structure.

Bear Break Price Source : Default: Close. Determines which price component is used to detect bearish breaks of structure.

Visual Settings

Bullish Blocks Color : Default: Blue with 85% transparency. Controls the appearance of bullish order blocks.

Bearish Blocks Color : Default: Red with 85% transparency. Controls the appearance of bearish order blocks.

General Options

Block Mitigation Method : Default: Wick, Options: Wick, Close. Determines how block mitigation is calculated - “Wick” uses high/low values while “Close” uses close values for more conservative mitigation criteria.

Remove Filled Blocks : Default: Disabled. When enabled, order blocks are removed once they’ve been mitigated by price action.

Volume Filter

Volume Filter Enabled : Default: Enabled. When activated, only shows order blocks formed with significant volume relative to recent average.

Volume SMA Period : Default: 15, Range: 1-50. Number of periods used to calculate the average volume baseline.

Min. Volume Ratio : Default: 1.5, Range: 0.5-10.0. Minimum volume ratio compared to average required to display an order block; higher values filter out more blocks.

✅ Best Use Cases

Identifying high-probability support and resistance zones for trade entries and exits

Finding optimal stop-loss placement behind significant order blocks

Detecting potential reversal areas where price may react after extended moves

Confirming breakout trades when price clears major order blocks

Building a comprehensive market structure map for medium to long-term trading decisions

Pinpointing areas where smart money may have positioned before major market moves

⚠️ Limitations

Most effective on higher timeframes (1H and above) where institutional activity is more clearly defined

Can generate multiple signals in choppy market conditions, requiring additional filtering

Volume filtering relies on accurate volume data, which may be less reliable for some securities

Recent market structure changes may invalidate older order blocks not yet automatically removed

Block identification is based on historical price action and may not predict future behavior with certainty

💡 What Makes This Unique

Volume Intelligence : Unlike basic order block indicators, this script incorporates volume analysis to identify only the most significant institutional zones, focusing on quality over quantity.

Structural Precision : Uses sophisticated break of structure algorithms to identify true market turning points, going beyond simple price pattern recognition.

Dynamic Block Management : Implements automatic block tracking, extension, and cleanup to maintain a clean and relevant chart display without manual intervention.

Institutional Focus : Designed specifically to highlight areas where smart money has likely positioned, helping retail traders align with institutional perspectives rather than retail noise.

🔬 How It Works

1. Structure Identification Process :

The indicator continuously scans price action to identify significant swing points and structure levels within the specified range, establishing a foundation for order block recognition.

2. Break Detection :

When price breaks an established structure level (crossing below a significant low for bearish breaks or above a significant high for bullish breaks), the indicator marks this as a potential zone for order block formation.

3. Volume Qualification :

For each potential order block, the algorithm calculates the relative volume compared to the configured period average. Only blocks formed with volume exceeding the minimum ratio threshold are displayed.

4. Block Creation and Management :

Valid order blocks are created, tracked, and managed as price continues to develop. Blocks extend to the right of the chart until they are either mitigated by price action or expire after the designated timeframe.

5. Continuous Monitoring :

The indicator constantly evaluates price interaction with existing blocks, determining when blocks have been tested, mitigated, or invalidated, and updates the visual representation accordingly.

💡 Note:

Order Blocks represent areas where institutional traders have likely established positions and may defend these zones during future price visits. For optimal results, use this indicator in conjunction with other confluent factors such as key support/resistance levels, trendlines, or additional confirmation indicators. The most reliable signals typically occur on higher timeframes where institutional activity is most prominent. Start with the default settings and adjust parameters gradually to match your specific trading instrument and style.

Adaptive Kalman Trend Filter (Zeiierman)█ Overview

The Adaptive Kalman Trend Filter indicator is an advanced trend-following tool designed to help traders accurately identify market trends. Utilizing the Kalman Filter—a statistical algorithm rooted in control theory and signal processing—this indicator adapts to changing market conditions, smoothing price data to filter out noise. By focusing on state vector-based calculations, it dynamically adjusts trend and range measurements, making it an excellent tool for both trend-following and range-based trading strategies. The indicator's adaptive nature is enhanced by options for volatility adjustment and three unique Kalman filter models, each tailored for different market conditions.

█ How It Works

The Kalman Filter works by maintaining a model of the market state through matrices that represent state variables, error covariances, and measurement uncertainties. Here’s how each component plays a role in calculating the indicator’s trend:

⚪ State Vector (X): The state vector is a two-dimensional array where each element represents a market property. The first element is an estimate of the true price, while the second element represents the rate of change or trend in that price. This vector is updated iteratively with each new price, maintaining an ongoing estimate of both price and trend direction.

⚪ Covariance Matrix (P): The covariance matrix represents the uncertainty in the state vector’s estimates. It continuously adapts to changing conditions, representing how much error we expect in our trend and price estimates. Lower covariance values suggest higher confidence in the estimates, while higher values indicate less certainty, often due to market volatility.

⚪ Process Noise (Q): The process noise matrix (Q) is used to account for uncertainties in price movements that aren’t explained by historical trends. By allowing some degree of randomness, it enables the Kalman Filter to remain responsive to new data without overreacting to minor fluctuations. This noise is particularly useful in smoothing out price movements in highly volatile markets.

⚪ Measurement Noise (R): Measurement noise is an external input representing the reliability of each new price observation. In this indicator, it is represented by the setting Measurement Noise and determines how much weight is given to each new price point. Higher measurement noise makes the indicator less reactive to recent prices, smoothing the trend further.

⚪ Update Equations:

Prediction: The state vector and covariance matrix are first projected forward using a state transition matrix (F), which includes market estimates based on past data. This gives a “predicted” state before the next actual price is known.

Kalman Gain Calculation: The Kalman gain is calculated by comparing the predicted state with the actual price, balancing between the covariance matrix and measurement noise. This gain determines how much of the observed price should influence the state vector.

Correction: The observed price is then compared to the predicted price, and the state vector is updated using this Kalman gain. The updated covariance matrix reflects any adjustment in uncertainty based on the latest data.

█ Three Kalman Filter Models

Standard Model: Assumes that market fluctuations follow a linear progression without external adjustments. It is best suited for stable markets.

Volume Adjusted Model: Adjusts the filter sensitivity based on trading volume. High-volume periods result in stronger trends, making this model suitable for volume-driven assets.

Parkinson Adjusted Model: Uses the Parkinson estimator, accounting for volatility through high-low price ranges, making it effective in markets with high intraday fluctuations.

These models enable traders to choose a filter that aligns with current market conditions, enhancing trend accuracy and responsiveness.

█ Trend Strength

The Trend Strength provides a visual representation of the current trend's strength as a percentage based on oscillator calculations from the Kalman filter. This table divides trend strength into color-coded segments, helping traders quickly assess whether the market is strongly trending or nearing a reversal point. A high trend strength percentage indicates a robust trend, while a low percentage suggests weakening momentum or consolidation.

█ Trend Range

The Trend Range section evaluates the market's directional movement over a specified lookback period, highlighting areas where price oscillations indicate a trend. This calculation assesses how prices vary within the range, offering an indication of trend stability or the likelihood of reversals. By adjusting the trend range setting, traders can fine-tune the indicator’s sensitivity to longer or shorter trends.

█ Sigma Bands

The Sigma Bands in the indicator are based on statistical standard deviations (sigma levels), which act as dynamic support and resistance zones. These bands are calculated using the Kalman Filter's trend estimates and adjusted for volatility (if enabled). The bands expand and contract according to market volatility, providing a unique visualization of price boundaries. In high-volatility periods, the bands widen, offering better protection against false breakouts. During low volatility, the bands narrow, closely tracking price movements. Traders can use these sigma bands to spot potential entry and exit points, aiming for reversion trades or trend continuation setups.

Trend Based

Volatility Based

█ How to Use

Trend Following:

When the Kalman Filter is green, it signals a bullish trend, and when it’s red, it indicates a bearish trend. The Sigma Cloud provides additional insights into trend strength. In a strong bullish trend, the cloud remains below the Kalman Filter line, while in a strong bearish trend, the cloud stays above it. Expansion and contraction of the Sigma Cloud indicate market momentum changes. Rapid expansion suggests an impulsive move, which could either signal the continuation of the trend or be an early sign of a possible trend reversal.

Mean Reversion: Watch for prices touching the upper or lower sigma bands, which often act as dynamic support and resistance.

Volatility Breakouts: Enable volatility-adjusted sigma bands. During high volatility, watch for price movements that extend beyond the bands as potential breakout signals.

Trend Continuation: When the Kalman Filter line aligns with a high trend strength, it signals a continuation in that direction.

█ Settings

Measurement Noise: Adjusts how sensitive the indicator is to price changes. Higher values smooth out fluctuations but delay reaction, while lower values increase sensitivity to short-term changes.

Kalman Filter Model: Choose between the standard, volume-adjusted, and Parkinson-adjusted models based on market conditions.

Band Sigma: Sets the standard deviation used for calculating the sigma bands, directly affecting the width of the dynamic support and resistance.

Volatility Adjusted Bands: Enables bands to dynamically adapt to volatility, increasing their effectiveness in fluctuating markets.

Trend Strength: Defines the lookback period for trend strength calculation. Shorter periods result in more responsive trend strength readings, while longer periods smooth out the calculation.

Trend Range: Specifies the lookback period for the trend range, affecting the assessment of trend stability over time.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

RSI (Kernel Optimized) | Flux Charts💎 GENERAL OVERVIEW

Introducing our new KDE Optimized RSI Indicator! This indicator adds a new aspect to the well-known RSI indicator, with the help of the KDE (Kernel Density Estimation) algorithm, estimates the probability of a candlestick will be a pivot or not. For more information about the process, please check the "HOW DOES IT WORK ?" section.

Features of the new KDE Optimized RSI Indicator :

A New Approach To Pivot Detection

Customizable KDE Algorithm

Realtime RSI & KDE Dashboard

Alerts For Possible Pivots

Customizable Visuals

❓ HOW TO INTERPRET THE KDE %

The KDE % is a critical metric that reflects how closely the current RSI aligns with the KDE (Kernel Density Estimation) array. In simple terms, it represents the likelihood that the current candlestick is forming a pivot point based on historical data patterns. a low percentage suggests a lower probability of the current candlestick being a pivot point. In these cases, price action is less likely to reverse, and existing trends may continue. At moderate levels, the possibility of a pivot increases, indicating potential trend shifts or consolidations.Traders should start monitoring closely for confirmation signals. An even higher KDE % suggests a strong likelihood that the current candlestick could form a pivot point, which could lead to a reversal or significant price movement. These points often align with overbought or oversold conditions in traditional RSI analysis, making them key moments for potential trade entry or exit.

📌 HOW DOES IT WORK ?

The RSI (Relative Strength Index) is a widely used oscillator among traders. It outputs a value between 0 - 100 and gives a glimpse about the current momentum of the price action. This indicator then calculates the RSI for each candlesticks, and saves them into an array if the candlestick is a pivot. The low & high pivot RSIs' are inserted into two different arrays. Then the a KDE array is calculated for both of the low & high pivot RSI arrays. Explaining the KDE might be too much for this write-up, but for a brief explanation, here are the steps :

1. Define the necessary options for the KDE function. These are : Bandwidth & Nº Steps, Array Range (Array Max - Array Min)

2. After that, create a density range array. The array has (steps * 2 - 1) elements and they are calculated by (arrMin + i * stepCount), i being the index.

3. Then, define a kernel function. This indicator has 3 different kernel distribution modes : Uniform, Gaussian and Sigmoid

4. Then, define a temporary value for the current element of KDE array.

5. For each element E in the pivot RSI array, add "kernel(densityRange.get(i) - E, 1.0 / bandwidth)" to the temporary value.

6. Add 1.0 / arrSize * to the KDE array.

Then the prefix sum array of the KDE array is calculated. For each candlestick, the index closest to it's RSI value in the KDE array is found using binary search. Then for the low pivot KDE calculation, the sum of KDE values from found index to max index is calculated. For the high pivot KDE, the sum of 0 to found index is used. Then if high or low KDE value is greater than the activation threshold determined in the settings, a bearish or bullish arrow is plotted after bar confirmation respectively. The arrows are drawn as long as the KDE value of current candlestick is greater than the threshold. When the KDE value is out of the threshold, a less transparent arrow is drawn, indicating a possible pivot point.

🚩 UNIQUENESS

This indicator combines RSI & KDE Algorithm to get a foresight of possible pivot points. Pivot points are important entry, confirmation and exit points for traders. But to their nature, they can be only detected after more candlesticks are rendered after them. The purpose of this indicator is to alert the traders of possible pivot points using KDE algorithm right away when they are confirmed. The indicator also has a dashboard for realtime view of the current RSI & Bullish or Bearish KDE value. You can fully customize the KDE algorithm and set up alerts for pivot detection.

⚙️ SETTINGS

1. RSI Settings

RSI Length -> The amount of bars taken into account for RSI calculation.

Source -> The source value for RSI calculation.

2. Pivots

Pivot Lengths -> Pivot lengths for both high & low pivots. For example, if this value is set to 21; 21 bars before AND 21 bars after a candlestick must be higher for a candlestick to be a low pivot.

3. KDE

Activation Threshold -> This setting determines the amount of arrows shown. Higher options will result in more arrows being rendered.

Kernel -> The kernel function as explained in the upper section.

Bandwidth -> The bandwidth variable as explained in the upper section. The smoothness of the KDE function is tied to this setting.

Nº Bins -> The Nº Steps variable as explained in the upper section. It determines the precision of the KDE algorithm.

Multiple Naked LevelsPURPOSE OF THE INDICATOR

This indicator autogenerates and displays naked levels and gaps of multiple types collected into one simple and easy to use indicator.

VALUE PROPOSITION OF THE INDICATOR AND HOW IT IS ORIGINAL AND USEFUL

1) CONVENIENCE : The purpose of this indicator is to offer traders with one coherent and robust indicator providing useful, valuable, and often used levels - in one place.

2) CLUSTERS OF CONFLUENCES : With this indicator it is easy to identify levels and zones on the chart with multiple confluences increasing the likelihood of a potential reversal zone.

THE TYPES OF LEVELS AND GAPS INCLUDED IN THE INDICATOR

The types of levels include the following:

1) PIVOT levels (Daily/Weekly/Monthly) depicted in the chart as: dnPIV, wnPIV, mnPIV.

2) POC (Point of Control) levels (Daily/Weekly/Monthly) depicted in the chart as: dnPoC, wnPoC, mnPoC.

3) VAH/VAL STD 1 levels (Value Area High/Low with 1 std) (Daily/Weekly/Monthly) depicted in the chart as: dnVAH1/dnVAL1, wnVAH1/wnVAL1, mnVAH1/mnVAL1

4) VAH/VAL STD 2 levels (Value Area High/Low with 2 std) (Daily/Weekly/Monthly) depicted in the chart as: dnVAH2/dnVAL2, wnVAH2/wnVAL2, mnVAH1/mnVAL2

5) FAIR VALUE GAPS (Daily/Weekly/Monthly) depicted in the chart as: dnFVG, wnFVG, mnFVG.

6) CME GAPS (Daily) depicted in the chart as: dnCME.

7) EQUILIBRIUM levels (Daily/Weekly/Monthly) depicted in the chart as dnEQ, wnEQ, mnEQ.

HOW-TO ACTIVATE LEVEL TYPES AND TIMEFRAMES AND HOW-TO USE THE INDICATOR

You can simply choose which of the levels to be activated and displayed by clicking on the desired radio button in the settings menu.

You can locate the settings menu by clicking into the Object Tree window, left-click on the Multiple Naked Levels and select Settings.

You will then get a menu of different level types and timeframes. Click the checkboxes for the level types and timeframes that you want to display on the chart.

You can then go into the chart and check out which naked levels that have appeared. You can then use those levels as part of your technical analysis.

The levels displayed on the chart can serve as additional confluences or as part of your overall technical analysis and indicators.

In order to back-test the impact of the different naked levels you can also enable tapped levels to be depicted on the chart. Do this by toggling the 'Show tapped levels' checkbox.

Keep in mind however that Trading View can not shom more than 500 lines and text boxes so the indocator will not be able to give you the complete history back to the start for long duration assets.

In order to clean up the charts a little bit there are two additional settings that can be used in the Settings menu:

- Selecting the price range (%) from the current price to be included in the chart. The default is 25%. That means that all levels below or above 20% will not be displayed. You can set this level yourself from 0 up to 100%.

- Selecting the minimum gap size to include on the chart. The default is 1%. That means that all gaps/ranges below 1% in price difference will not be displayed on the chart. You can set the minimum gap size yourself.

BASIC DESCRIPTION OF THE INNER WORKINGS OF THE INDICTATOR

The way the indicator works is that it calculates and identifies all levels from the list of levels type and timeframes above. The indicator then adds this level to a list of untapped levels.

Then for each bar after, it checks if the level has been tapped. If the level has been tapped or a gap/range completely filled, this level is removed from the list so that the levels displayed in the end are only naked/untapped levels.

Below is a descrition of each of the level types and how it is caluclated (algorithm):

PIVOT

Daily, Weekly and Monthly levels in trading refer to significant price points that traders monitor within the context of a single trading day. These levels can provide insights into market behavior and help traders make informed decisions regarding entry and exit points.

Traders often use D/W/M levels to set entry and exit points for trades. For example, entering long positions near support (daily close) or selling near resistance (daily close).

Daily levels are used to set stop-loss orders. Placing stops just below the daily close for long positions or above the daily close for short positions can help manage risk.

The relationship between price movement and daily levels provides insights into market sentiment. For instance, if the price fails to break above the daily high, it may signify bearish sentiment, while a strong breakout can indicate bullish sentiment.

The way these levels are calculated in this indicator is based on finding pivots in the chart on D/W/M timeframe. The level is then set to previous D/W/M close = current D/W/M open.

In addition, when price is going up previous D/W/M open must be smaller than previous D/W/M close and current D/W/M close must be smaller than the current D/W/M open. When price is going down the opposite.

POINT OF CONTROL

The Point of Control (POC) is a key concept in volume profile analysis, which is commonly used in trading.

It represents the price level at which the highest volume of trading occurred during a specific period.

The POC is derived from the volume traded at various price levels over a defined time frame. In this indicator the timeframes are Daily, Weekly, and Montly.

It identifies the price level where the most trades took place, indicating strong interest and activity from traders at that price.

The POC often acts as a significant support or resistance level. If the price approaches the POC from above, it may act as a support level, while if approached from below, it can serve as a resistance level. Traders monitor the POC to gauge potential reversals or breakouts.

The way the POC is calculated in this indicator is by an approximation by analysing intrabars for the respective timeperiod (D/W/M), assigning the volume for each intrabar into the price-bins that the intrabar covers and finally identifying the bin with the highest aggregated volume.

The POC is the price in the middle of this bin.

The indicator uses a sample space for intrabars on the Daily timeframe of 15 minutes, 35 minutes for the Weekly timeframe, and 140 minutes for the Monthly timeframe.

The indicator has predefined the size of the bins to 0.2% of the price at the range low. That implies that the precision of the calulated POC og VAH/VAL is within 0.2%.

This reduction of precision is a tradeoff for performance and speed of the indicator.

This also implies that the bigger the difference from range high prices to range low prices the more bins the algorithm will iterate over. This is typically the case when calculating the monthly volume profile levels and especially high volatility assets such as alt coins.

Sometimes the number of iterations becomes too big for Trading View to handle. In these cases the bin size will be increased even more to reduce the number of iterations.

In such cases the bin size might increase by a factor of 2-3 decreasing the accuracy of the Volume Profile levels.

Anyway, since these Volume Profile levels are approximations and since precision is traded for performance the user should consider the Volume profile levels(POC, VAH, VAL) as zones rather than pin point accurate levels.

VALUE AREA HIGH/LOW STD1/STD2

The Value Area High (VAH) and Value Area Low (VAL) are important concepts in volume profile analysis, helping traders understand price levels where the majority of trading activity occurs for a given period.

The Value Area High/Low is the upper/lower boundary of the value area, representing the highest price level at which a certain percentage of the total trading volume occurred within a specified period.

The VAH/VAL indicates the price point above/below which the majority of trading activity is considered less valuable. It can serve as a potential resistance/support level, as prices above/below this level may experience selling/buying pressure from traders who view the price as overvalued/undervalued

In this indicator the timeframes are Daily, Weekly, and Monthly. This indicator provides two boundaries that can be selected in the menu.

The first boundary is 70% of the total volume (=1 standard deviation from mean). The second boundary is 95% of the total volume (=2 standard deviation from mean).

The way VAH/VAL is calculated is based on the same algorithm as for the POC.

However instead of identifying the bin with the highest volume, we start from range low and sum up the volume for each bin until the aggregated volume = 30%/70% for VAL1/VAH1 and aggregated volume = 5%/95% for VAL2/VAH2.

Then we simply set the VAL/VAH equal to the low of the respective bin.

FAIR VALUE GAPS

Fair Value Gaps (FVG) is a concept primarily used in technical analysis and price action trading, particularly within the context of futures and forex markets. They refer to areas on a price chart where there is a noticeable lack of trading activity, often highlighted by a significant price movement away from a previous level without trading occurring in between.

FVGs represent price levels where the market has moved significantly without any meaningful trading occurring. This can be seen as a "gap" on the price chart, where the price jumps from one level to another, often due to a rapid market reaction to news, events, or other factors.

These gaps typically appear when prices rise or fall quickly, creating a space on the chart where no transactions have taken place. For example, if a stock opens sharply higher and there are no trades at the prices in between the two levels, it creates a gap. The areas within these gaps can be areas of liquidity that the market may return to “fill” later on.

FVGs highlight inefficiencies in pricing and can indicate areas where the market may correct itself. When the market moves rapidly, it may leave behind price levels that traders eventually revisit to establish fair value.

Traders often watch for these gaps as potential reversal or continuation points. Many traders believe that price will eventually “fill” the gap, meaning it will return to those price levels, providing potential entry or exit points.

This indicator calculate FVGs on three different timeframes, Daily, Weekly and Montly.

In this indicator the FVGs are identified by looking for a three-candle pattern on a chart, signalling a discrete imbalance in order volume that prompts a quick price adjustment. These gaps reflect moments where the market sentiment strongly leans towards buying or selling yet lacks the opposite orders to maintain price stability.

The indicator sets the gap to the difference from the high of the first bar to the low of the third bar when price is moving up or from the low of the first bar to the high of the third bar when price is moving down.

CME GAPS (BTC only)

CME gaps refer to price discrepancies that can occur in charts for futures contracts traded on the Chicago Mercantile Exchange (CME). These gaps typically arise from the fact that many futures markets, including those on the CME, operate nearly 24 hours a day but may have significant price movements during periods when the market is closed.

CME gaps occur when there is a difference between the closing price of a futures contract on one trading day and the opening price on the following trading day. This difference can create a "gap" on the price chart.

Opening Gaps: These usually happen when the market opens significantly higher or lower than the previous day's close, often influenced by news, economic data releases, or other market events occurring during non-trading hours.

Gaps can result from reactions to major announcements or developments, such as earnings reports, geopolitical events, or changes in economic indicators, leading to rapid price movements.

The importance of CME Gaps in Trading is the potential for Filling Gaps: Many traders believe that prices often "fill" gaps, meaning that prices may return to the gap area to establish fair value.

This can create potential trading opportunities based on the expectation of gap filling. Gaps can act as significant support or resistance levels. Traders monitor these levels to identify potential reversal points in price action.

The way the gap is identified in this indicator is by checking if current open is higher than previous bar close when price is moving up or if current open is lower than previous day close when price is moving down.

EQUILIBRIUM

Equilibrium in finance and trading refers to a state where supply and demand in a market balance each other, resulting in stable prices. It is a key concept in various economic and trading contexts. Here’s a concise description:

Market Equilibrium occurs when the quantity of a good or service supplied equals the quantity demanded at a specific price level. At this point, there is no inherent pressure for the price to change, as buyers and sellers are in agreement.

Equilibrium Price is the price at which the market is in equilibrium. It reflects the point where the supply curve intersects the demand curve on a graph. At the equilibrium price, the market clears, meaning there are no surplus goods or shortages.

In this indicator the equilibrium level is calculated simply by finding the midpoint of the Daily, Weekly, and Montly candles respectively.

NOTES

1) Performance. The algorithms are quite resource intensive and the time it takes the indicator to calculate all the levels could be 5 seconds or more, depending on the number of bars in the chart and especially if Montly Volume Profile levels are selected (POC, VAH or VAL).

2) Levels displayed vs the selected chart timeframe. On a timeframe smaller than the daily TF - both Daily, Weekly, and Monthly levels will be displayed. On a timeframe bigger than the daily TF but smaller than the weekly TF - the Weekly and Monthly levels will be display but not the Daily levels. On a timeframe bigger than the weekly TF but smaller than the monthly TF - only the Monthly levels will be displayed. Not Daily and Weekly.

CREDITS

The core algorithm for calculating the POC levels is based on the indicator "Naked Intrabar POC" developed by rumpypumpydumpy (https:www.tradingview.com/u/rumpypumpydumpy/).

The "Naked intrabar POC" indicator calculates the POC on the current chart timeframe.

This indicator (Multiple Naked Levels) adds two new features:

1) It calculates the POC on three specific timeframes, the Daily, Weekly, and Monthly timeframes - not only the current chart timeframe.

2) It adds functionaly by calculating the VAL and VAH of the volume profile on the Daily, Weekly, Monthly timeframes .

ICT Power Of Three | Flux Charts💎 GENERAL OVERVIEW

Introducing our new ICT Power Of Three Indicator! This indicator is built around the ICT's "Power Of Three" strategy. This strategy makes use of these 3 key smart money concepts : Accumulation, Manipulation and Distribution. Each step is explained in detail within this write-up. For more information about the process, check the "HOW DOES IT WORK" section.

Features of the new ICT Power Of Three Indicator :

Implementation of ICT's Power Of Three Strategy

Different Algorithm Modes

Customizable Execution Settings

Customizable Backtesting Dashboard

Alerts for Buy, Sell, TP & SL Signals

📌 HOW DOES IT WORK ?

The "Power Of Three" comes from these three keywords "Accumulation, Manipulation and Distribution". Here is a brief explanation of each keyword :

Accumulation -> Accumulation phase is when the smart money accumulate their positions in a fixed range. This phase indicates price stability, generally meaning that the price constantly switches between up & down trend between a low and a high pivot point. When the indicator detects an accumulation zone, the Power Of Three strategy begins.

Manipulation -> When the smart money needs to increase their position sizes, they need retail traders' positions for liquidity. So, they manipulate the market into the opposite direction of their intended direction. This will result in retail traders opening positions the way that the smart money intended them to do, creating liquidity. After this step, the real move that the smart money intended begins.

Distribution -> This is when the real intention of the smart money comes into action. With the new liquidity thanks to the manipulation phase, the smart money add their positions towards the opposite direction of the retail mindset. The purpose of this indicator is to detect the accumulation and manipulation phases, and help the trader move towards the same direction as the smart money for their trades.

Detection Methods Of The Indicator :

Accumulation -> The indicator detects accumulation zones as explained step-by-step :

1. Draw two lines from the lowest point and the highest point of the latest X bars.

2. If the (high line - low line) is lower than Average True Range (ATR) * accumulationConstant

3. After the condition is validated, an accumulation zone is detected. The accumulation zone will be invalidated and manipulation phase will begin when the range is broken.

Manipulation -> If the accumulation range is broken, check if the current bar closes / wicks above the (high line + ATR * manipulationConstant) or below the (low line - ATR * manipulationConstant). If the condition is met, the indicator detects a manipulation zone.

Distribution -> The purpose of this indicator is to try to foresee the distribution zone, so instead of a detection, after the manipulation zone is detected the indicator automatically create a "shadow" distribution zone towards the opposite direction of the freshly detected manipulation zone. This shadow distribution zone comes with a take-profit and stop-loss layout, customizable by the trader in the settings.

The X bars, accumulationConstant and manipulationConstant are subject to change with the "Algorithm Mode" setting. Read the "Settings" section for more information.

This indicator follows these steps and inform you step by step by plotting them in your chart.

🚩UNIQUENESS

This indicator is an all-in-one suite for the ICT's Power Of Three concept. It's capable of plotting the strategy, giving signals, a backtesting dashboard and alerts feature. Different and customizable algorithm modes will help the trader fine-tune the indicator for the asset they are currently trading. The backtesting dashboard allows you to see how your settings perform in the current ticker. You can also set up alerts to get informed when the strategy is executable for different tickers.

⚙️SETTINGS

1. General Configuration

Algorithm Mode -> The indicator offers 3 different detection algorithm modes according to your needs. Here is the explanation of each mode.

a) Small Manipulation

This mode has the default bar length for the accumulation detection, but a lower manipulation constant, meaning that slighter imbalances in the price action can be detected as manipulation. This setting can be useful on tickers that have lower liquidity, thus can be manipulated easier.

b) Big Manipulation

This mode has the default bar length for the accumulation detection, but a higher manipulation constant, meaning that heavier imbalances on the price action are required in order to detect manipulation zones. This setting can be useful on tickers that have higher liquidity, thus can be manipulated harder.

c) Short Accumulation

This mode has a ~70% lower bar length requirement for accumulation zone detection, and the default manipulation constant. This setting can be useful on tickers that are highly volatile and do not enter accumulation phases too often.

Breakout Method -> If "Close" is selected, bar close price will be taken into calculation when Accumulation & Manipulation zone invalidation. If "Wick" is selected, a wick will be enough to validate the corresponding zone.

2. TP / SL

TP / SL Method -> If "Fixed" is selected, you can adjust the TP / SL ratios from the settings below. If "Dynamic" is selected, the TP / SL zones will be auto-determined by the algorithm.

Risk -> The risk you're willing to take if "Dynamic" TP / SL Method is selected. Higher risk usually means a better winrate at the cost of losing more if the strategy fails. This setting is has a crucial effect on the performance of the indicator, as different tickers may have different volatility so the indicator may have increased performance when this setting is correctly adjusted.

3. Visuals

Show Zones -> Enables / Disables rendering of Accumulation (yellow) and Manipulation (red) zones.

ICT Concept [TradingFinder] Order Block | FVG | Liquidity Sweeps🔵 Introduction

The "ICT" style is one of the subsets of "Price Action" technical analysis. ICT is a method created by "Michael Huddleston", a professional forex trader and experienced mentor. The acronym ICT stands for "Inner Circle Trader".

The main objective of the ICT trading strategy is to combine "Price Action" and the concept of "Smart Money" to identify optimal entry points into trades. However, finding suitable entry points is not the only strength of this approach. With the ICT style, traders can better understand price behavior and adapt their trading approach to market structure accordingly.

Numerous concepts are discussed in this style, but the key practical concepts for trading in financial markets include "Order Block," "Liquidity," and "FVG".

🔵 How to Use

🟣Order Block

Order blocks are a specific type of "Supply and Demand" zones formed when a series of orders are placed in a block. These orders could be created by banks or other major players. Banks typically execute large orders in blocks during their trading sessions. If they were to enter the market directly with a small quantity, significant price movements would occur before the orders are fully executed, resulting in less profit. To avoid this, they divide their orders into smaller, manageable positions. Traders should look for "buy" opportunities in "demand order blocks" areas and "sell" opportunities in "supply order blocks".

🟣Liquidity

These levels are where traders aim to exit their trades. "Market Makers" or smart money usually collects or distributes their trading positions near levels where many retail traders have placed their "Stop Loss" orders. When the liquidity resulting from these losses is collected, the price often reverses direction.

A "Stop Hunt" is a move designed to neutralize liquidity generated by triggered stop losses. Banks often use significant news events to trigger stop hunts and acquire the liquidity released in the market. If, for example, they intend to execute heavy buy orders, they encourage others to sell through stop hunts.

As a result, if there is liquidity in the market before reaching the order block region, the credibility of that order block is higher. Conversely, if liquidity is near the order block, meaning the price reaches the order block before reaching the liquidity area, the credibility of that order block is lower.

🟣FVG (Fair Value Gap)

To identify the "Fair Value Gap" on the chart, one must analyze candle by candle. Focus on candles with large bodies, examining one candle and the one before it. The candles before and after this central candle should have long shadows, and their bodies should not overlap with the body of the central candle. The distance between the shadows of the first and third candles is called the FVG range.

These zone function in two ways :

•Supply and Demand zone: In this case, the price reacts to these zone, and its trend reverses.

•Liquidity zone: In this scenario, the price "fills" the zone and then reaches the order block.

Important Note: In most cases, FVG zone with very small width act as supply and demand zone, while zone with a significant width act as liquidity zone, absorbing the price.

🔵 Setting

🟣Order Block

Refine Order Block : When the option for refining order blocks is Off, the supply and demand zones encompass the entire length of the order block (from Low to High) in their standard state and remain unaltered. On the option for refining order blocks triggers the improvement of supply and demand zones using the error correction algorithm.

Refine Type : The enhancement of order blocks via the error correction algorithm can be executed through two methods: Defensive and Aggressive. In the Aggressive approach, the widest possible range is taken into account for order blocks.

Show High Levels : If major high levels are to be displayed, set the option for showing high level to Yes.

Show Low Levels : If major low levels are to be displayed, set the option for showing low level to Yes.

Show Last Support : If showing the last support is desired, set the option for showing last support to Yes.

Show Last Resistance : If showing the last resistance is desired, set the option for showing last resistance to Yes.

🟣 FVG

FVG Filter : When FVG filtering is activated, the number of FVG areas undergoes filtration based on the specified algorithm.

FVG Filter Types :

1. Very Aggressive : Apart from the initial condition, an additional condition is introduced. For an upward FVG, the maximum price of the last candle should exceed the maximum price of the middle candle. Similarly, for a downward FVG, the minimum price of the last candle should be lower than the minimum price of the middle candle. This mode eliminates a minimal number of FVGs.

2. Aggressive : In addition to the conditions of the Very Aggressive mode, this mode considers the size of the middle candle; it should not be small. Consequently, a larger number of FVGs are eliminated in this mode.

3. Defensive : Alongside the conditions of the Very Aggressive mode, this mode takes into account the size of the middle candle, which should be relatively large with the majority of it comprising the body. Furthermore, to identify upward FVGs, the second and third candles must be positive, whereas for downward FVGs, the second and third candles must be negative. This mode filters out a considerable number of FVGs, retaining only those of suitable quality.

4. Very Defensive : In addition to the conditions of the Defensive mode, the first and third candles should not be very small-bodied doji candles. This mode filters out the majority of FVGs, leaving only the highest quality ones. Show Demand FVG: Enables the display of demand-related boxes, which can be toggled between off and on. Show Supply FVG: Enables the display of supply-related boxes along the path, which can also be toggled between off and on.

🟣 Liquidity

Statics Liquidity Line Sensitivity : A value ranging from 0 to 0.4. Increasing this value reduces the sensitivity of the "Statics Liquidity Line Detection" function and increases the number of identified lines. The default value is 0.3.

Dynamics Liquidity Line Sensitivity : A value ranging from 0.4 to 1.95. Increasing this value enhances the sensitivity of the "Dynamics Liquidity Line Detection" function and decreases the number of identified lines. The default value is 1.

Statics Period Pivot : Default value is set to 8. By adjusting this value, you can specify the period for static liquidity line pivots.

Dynamics Period Pivot : Default value is set to 3. By adjusting this value, you can specify the period for dynamic liquidity line pivots.

You can activate or deactivate liquidity lines as necessary using the buttons labeled "Show Statics High Liquidity Line," "Show Statics Low Liquidity Line," "Show Dynamics High Liquidity Line," and "Show Dynamics Low Liquidity Line".

Double AI Super Trend Trading - Strategy [PresentTrading]█ Introduction and How It is Different

The Double AI Super Trend Trading Strategy is a cutting-edge approach that leverages the power of not one, but two AI algorithms, in tandem with the SuperTrend technical indicator. The strategy aims to provide traders with enhanced precision in market entry and exit points. It is designed to adapt to market conditions dynamically, offering the flexibility to trade in both bullish and bearish markets.

*The KNN part is mainly referred from @Zeiierman.

BTCUSD 8hr performance

ETHUSD 8hr performance

█ Strategy, How It Works: Detailed Explanation

1. SuperTrend Calculation

The SuperTrend is a popular indicator that captures market trends through a combination of the Volume-Weighted Moving Average (VWMA) and the Average True Range (ATR). This strategy utilizes two sets of SuperTrend calculations with varying lengths and factors to capture both short-term and long-term market trends.

2. KNN Algorithm

The strategy employs k-Nearest Neighbors (KNN) algorithms, which are supervised machine learning models. Two sets of KNN algorithms are used, each focused on different lengths of historical data and number of neighbors. The KNN algorithms classify the current SuperTrend data point as bullish or bearish based on the weighted sum of the labels of the k closest historical data points.

3. Signal Generation

Based on the KNN classifications and the SuperTrend indicator, the strategy generates signals for the start of a new trend and the continuation of an existing trend.

4. Trading Logic

The strategy uses these signals to enter long or short positions. It also incorporates dynamic trailing stops for exit conditions.

Local picture

█ Trade Direction

The strategy allows traders to specify their trading direction: long, short, or both. This enables the strategy to be versatile and adapt to various market conditions.

█ Usage

ToolTips: Comprehensive tooltips are provided for each parameter to guide the user through the customization process.

Inputs: Traders can customize numerous parameters including the number of neighbors in KNN, ATR multiplier, and types of moving averages.

Plotting: The strategy also provides visual cues on the chart to indicate bullish or bearish trends.

Order Execution: Based on the generated signals, the strategy will execute buy or sell orders automatically.

█ Default Settings

The default settings are configured to offer a balanced approach suitable for most scenarios:

Initial Capital: $10,000

Default Quantity Type: 10% of equity

Commission: 0.1%

Slippage: 1

Currency: USD

These settings can be modified to suit various trading styles and asset classes.

Fibonacci Structure & Trend Channel (Expo)█ Overview

The Fibonacci Structure & Trend Channel (Expo) is designed to identify trend direction and potential reversal levels and offer insights into price structure based on Fibonacci ratios. The algorithm plots a Fibonacci channel, making it easier for traders to identify potential retracement points. Additionally, the Fibonacci market structure is plotted to enhance traders' understanding of the underlying order flow.

█ How to Use

Identify Trends

Use the plotted Fibonacci Trend Line to identify the direction of the market trend. A green line typically signifies a bullish trend, while a red line signifies a bearish trend.

Retracement Levels

The plotted Fibonacci levels can act as potential support or resistance levels. Look for price action signs at these levels for entry or exit points.

Channel Trading

If you enable the Fibonacci channel, the upper and lower bounds can act as overbought or oversold levels.

Market Structure

The plotted Fibonacci market structure serves as a valuable tool for dissecting the underlying order flow and gauging the strength or weakness of a trend. By analyzing these structures, traders can identify key levels where supply and demand intersect, which often act as pivotal points for trend reversals or accelerations. This visual representation simplifies complex market dynamics. Whether you're looking to catch a new trend early or seeking confirmation for a potential reversal, understanding the market structure plotted by the Fibonacci ratios can provide actionable insights for various trading strategies.

Use the Table

The information table can provide quick insights into the current trend and when it started.

█ Settings

The Fibonacci settings allow traders to specify the Fibonacci retracement levels that will be used to calculate the trend and its channel.

The Fibonacci Structure Trend Channel structure settings enable traders to fine-tune how the indicator identifies and plots the underlying price structure.

-----------------

Disclaimer