Targets For Many Indicators [LuxAlgo]The Targets For Many Indicators is a useful utility tool able to display targets for many built-in indicators as well as external indicators. Targets can be set for specific user-set conditions between two series of values, with the script being able to display targets for two different user-set conditions.

Alerts are included for the occurrence of a new target as well as for reached targets.

🔶 USAGE

Targets can help users determine the price limit where the price might start deviating from an indication given by one or multiple indicators. In the context of trading, targets can help secure profits/reduce losses of a trade, as such this tool can be useful to evaluate/determine user take profits/stop losses.

Due to these essentially being horizontal levels, they can also serve as potential support/resistances, with breakouts potentially confirming new trends.

In the above example, we set targets 3 ATR's away from the closing price when the price crosses over the script built-in SuperTrend indicator using ATR period 10 and factor 3. Using "Long Position Target" allows setting a target above the price, disabling this setting will place targets below the price.

Users might be interested in obtaining new targets once one is reached, this can be done by enabling "New Target When Reached" in the target logic setting section, resulting in more frequent targets.

Lastly, users can restrict new target creation until current ones are reached. This can result in fewer and longer-term targets, with a higher reach rate.

🔹 Dashboard

A dashboard is displayed on the top right of the chart, displaying the amount, reach rate of targets 1/2, and total amount.

This dashboard can be useful to evaluate the selected target distances relative to the selected conditions, with a higher reach rate suggesting the distance of the targets from the price allows them to be reached.

🔶 DETAILS

🔹 Indicators

Besides 'External' sources, each source can be set at 1 of the following Build-In Indicators :

ACCDIST : Accumulation/distribution index

ATR : Average True Range

BB (Middle, Upper or Lower): Bollinger Bands

CCI : Commodity Channel Index

CMO : Chande Momentum Oscillator

COG : Center Of Gravity

DC (High, Mid or Low): Donchian Channels

DEMA : Double Exponential Moving Average

EMA : Exponentially weighted Moving Average

HMA : Hull Moving Average

III : Intraday Intensity Index

KC (Middle, Upper or Lower): Keltner Channels

LINREG : Linear regression curve

MACD (macd, signal or histogram): Moving Average Convergence/Divergence

MEDIAN : median of the series

MFI : Money Flow Index

MODE : the mode of the series

MOM : Momentum

NVI : Negative Volume Index

OBV : On Balance Volume

PVI : Positive Volume Index

PVT : Price-Volume Trend

RMA : Relative Moving Average

ROC : Rate Of Change

RSI : Relative Strength Index

SMA : Simple Moving Average

STOCH : Stochastic

Supertrend

TEMA : Triple EMA or Triple Exponential Moving Average

VWAP : Volume Weighted Average Price

VWMA : Volume-Weighted Moving Average

WAD : Williams Accumulation/Distribution

WMA : Weighted Moving Average

WVAD : Williams Variable Accumulation/Distribution

%R : Williams %R

Each indicator is provided with a link to the Reference Manual or to the Build-In Indicators page.

The latter contains more information about each indicator.

Note that when "Show Source Values" is enabled, only values that can be logically found around the price will be shown. For example, Supertrend , SMA , EMA , BB , ... will be made visible. Values like RSI , OBV , %R , ... will not be visible since they will deviate too much from the price.

🔹 Interaction with settings

This publication contains input fields, where you can enter the necessary inputs per indicator.

Some indicators need only 1 value, others 2 or 3.

When several input values are needed, you need to separate them with a comma.

You can use 0 to 4 spaces between without a problem. Even an extra comma doesn't give issues.

The red colored help text will guide you further along (Only when Target is enabled)

Some examples that work without issues:

Some examples that work with issues:

As mentioned, the errors won't be visible when the concerning target is disabled

🔶 SETTINGS

Show Target Labels: Display target labels on the chart.

Candle Coloring: Apply candle coloring based on the most recent active target.

Target 1 and Target 2 use the same settings below:

Enable Target: Display the targets on the chart.

Long Position Target: Display targets above the price a user selected condition is true. If disabled will display the targets below the price.

New Target Condition: Conditional operator used to compare "Source A" and "Source B", options include CrossOver, CrossUnder, Cross, and Equal.

🔹 Sources

Source A: Source A input series, can be an indicator or external source.

External: External source if 'External" is selected in "Source A".

Settings: Settings of the selected indicator in "Source A", entered settings of indicators requiring multiple ones must be comma separated, for example, "10, 3".

Source B: Source B input series, can be an indicator or external source.

External: External source if 'External" is selected in "Source B".

Settings: Settings of the selected indicator in "Source B", entered settings of indicators requiring multiple ones must be comma separated, for example, "10, 3".

Source B Value: User-defined numerical value if "value" is selected in "Source B".

Show Source Values: Display "Source A" and "Source B" on the chart.

🔹 Logic

Wait Until Reached: When enabled will not create a new target until an existing one is reached.

New Target When Reached: Will create a new target when an existing one is reached.

Evaluate Wicks: Will use high/low prices to determine if a target is reached. Unselecting this setting will use the closing price.

Target Distance From Price: Controls the distance of a target from the price. Can be determined in currencies/points, percentages, ATR multiples, ticks, or using multiple of external values.

External Distance Value: External distance value when "External Value" is selected in "Target Distance From Price".

Wyszukaj w skryptach "accumulation"

SADROCThe "Smoothed Accumulation/Distribution Rate of Change" (SADROC) indicator draws inspiration from the Chaikin Oscillator's use of accumulation and distribution, formatted in a manner just like the MACD (Moving Average Convergence Divergence) indicator. My goal was to create something with greater speed and accuracy than the classic MACD

Here's a breakdown of its key elements:

Inputs: Users can customize the indicator by specifying the fast length, slow length, and signal length to fit their preferences.

Calculations: The indicator calculates cumulative volume and then computes the Accumulation/Distribution (AD) value based on price and volume data. The SADROC is calculated as the Rate of Change of the exponential moving averages of the price. The difference between these two values is further smoothed to generate the final SADROC value.

Plotting: The indicator plots the SADROC line and a signal line on the chart. Additionally, it includes a histogram that visually represents the difference between SADROC and the signal line.

Grid Spot Trading Algorithm V2 - The Quant ScienceGrid Spot Trading Algorithm V2 is the last grid trading algorithm made by our developer team.

Grid Spot Trading Algorithm V2 is a fixed 10-level grid trading algorithm. The grid is divided into an accumulation area (red) and a selling area (green).

In the accumulation area, the algorithm will place new buy orders, selling the long positions on the top of the grid.

BUYING AND SELLING LOGIC

The algorithm places up to 5 limit orders on the accumulation section of the grid, each time the price cross through the middle grid. Each single order uses 20% of the equity.

Positions are closed at the top of the grid by default, with the algorithm closing all orders at the first sell level. The exit level can be adjusted using the user interface, from the first level up to the fifth level above.

CONFIGURING THE ALGORITHM

1) Add it to the chart: Add the script to the current chart that you want to analyze.

2) Select the top of the grid: Confirm a price level with the mouse on which to fix the top of the grid.

3) Select the bottom of the grid: Confirm a price level with the mouse on which to fix the bottom of the grid.

4) Wait for the automatic creation of the grid.

USING THE ALGORITHM

Once the grid configuration process is completed, the algorithm will generate automatic backtesting.

You can add a stop loss that destroys the grid by setting the destruction price and activating the feature from the user interface. When the stop loss is activated, you can view it on the chart.

VolumeIndicatorsLibrary "VolumeIndicators"

This is a library of 'Volume Indicators'.

It aims to facilitate the grouping of this category of indicators, and also offer the customized supply of the source, not being restricted to just the closing price.

Indicators:

1. Volume Moving Average (VMA):

Moving average of volume. Identify trends in trading volume.

2. Money Flow Index (MFI): Measures volume pressure in a range of 0 to 100.

Calculates the ratio of volume when the price goes up and when the price goes down

3. On-Balance Volume (OBV):

Identify divergences between trading volume and an asset's price.

Sum of trading volume when the price rises and subtracts volume when the price falls.

4. Accumulation/Distribution (A/D):

Identifies buying and selling pressure by tracking the flow of money into and out of an asset based on volume patterns.

5. Chaikin Money Flow (CMF):

A variation of A/D that takes into account the daily price variation and weighs trading volume accordingly.

6. Volume Oscillator (VO):

Identify divergences between trading volume and an asset's price. Ratio of change of volume, from a fast period in relation to a long period.

7. Positive Volume Index (PVI):

Identify the upward strength of an asset. Volume when price rises divided by total volume.

8. Negative Volume Index (NVI):

Identify the downward strength of an asset. Volume when price falls divided by total volume.

9. Price-Volume Trend (PVT):

Identify the strength of an asset's price trend based on its trading volume. Cumulative change in price with volume factor

vma(length, maType, almaOffset, almaSigma, lsmaOffSet)

@description Volume Moving Average (VMA)

Parameters:

length : (int) Length for moving average

maType : (int) Type of moving average for smoothing

almaOffset : (float) Offset for Arnauld Legoux Moving Average

almaSigma : (float) Sigma for Arnauld Legoux Moving Average

lsmaOffSet : (float) Offset for Least Squares Moving Average

Returns: (float) Moving average of Volume

mfi(source, length)

@description MFI (Money Flow Index).

Uses both price and volume to measure buying and selling pressure in an asset.

Parameters:

source : (float) Source of series (close, high, low, etc.)

length

Returns: (float) Money Flow series

obv(source)

@description On Balance Volume (OBV)

Same as ta.obv(), but with customized type of source

Parameters:

source : (float) Series

Returns: (float) OBV

ad()

@description Accumulation/Distribution (A/D)

Returns: (float) Accumulation/Distribution (A/D) series

cmf(length)

@description CMF (Chaikin Money Flow).

Measures the flow of money into or out of an asset over time, using a combination of price and volume, and is used to identify the strength and direction of a trend.

Parameters:

length

Returns: (float) Chaikin Money Flow series

vo(shortLen, longLen, maType, almaOffset, almaSigma, lsmaOffSet)

@description Volume Oscillator (VO)

Parameters:

shortLen : (int) Fast period for volume

longLen : (int) Slow period for volume

maType : (int) Type of moving average for smoothing

almaOffset

almaSigma

lsmaOffSet

Returns: (float) Volume oscillator

pvi(source)

@description Positive Volume Index (PVI)

Same as ta.pvi(), but with customized type of source

Parameters:

source : (float) Series

Returns: (float) PVI

nvi(source)

@description Negative Volume Index (NVI)

Same as ta.nvi(), but with customized type of source

Parameters:

source : (float) Series

Returns: (float) PVI

pvt(source)

@description Price-Volume Trend (PVT)

Same as ta.pvt(), but with customized type of source

Parameters:

source : (float) Series

Returns: (float) PVI

Chaikin Money Flow - LibraryLibrary "Chaikin Money Flow"

cmf()

Developed by Marc Chaikin, Chaikin Money Flow measures the amount of Money Flow Volume over a specific period.

Money Flow Volume forms the basis for the Accumulation Distribution Line. Instead of a cumulative total of

Money Flow Volume, Chaikin Money Flow simply sums Money Flow Volume for a specific look-back period, typically

20 or 21 days. The resulting indicator fluctuates above/below the zero line just like an oscillator. Chartists

weigh the balance of buying or selling pressure with the absolute level of Chaikin Money Flow. Chartists can

also look for crosses above or below the zero line to identify changes on money flow.

The Accumulation Distribution Line was developed by Marc Chaikin to measure the cumulative flow of money into and

out of an index or security. The Accumulation/Distribution Line can be compared to the OBV (On Balance Volume),

which adds or subtracts volume depending on the closing price. Marc Chaikin chose a different approach, instead

of relying on the closing price, he used CLV (Close Location Value).

Crypto Force IndexIntroduction

The Crypto Force Index (CFI) indicator helps us understand the current strength and weakness of the price. It is very useful when used on high timeframes for investment purposes and not for short term trading.

To determine the strength and weakness of the price, a level grid based on the RSI indicator is used.

Based on the RSI value, red circles (oversold condition) and green circles (overbought condition) appear under the price candles. The more intense the color of the circles, the more that the current price is in an overbought or oversold condition.

The signal levels are all configurable to adapt the indicator across multiple instruments and markets.

The default configuration have been designed to obtain more accurate signals on Ethereum and Bitcoin, using the weekly timeframe.

Why Crypto Force Index?

The Crypto Force Index (CFI) is the consequence of my study of investments based on the accumulation plan. I wanted to demonstrate that I am improving the returns of the classic DCA ( dollar cost averaging ) and VA ( value averaging ).

After finding my own model of an accumulation plan, I decided to create the Crypto Force Index to help me visually enter the market.

The formulas of the indicator are very simple, but my studies confirm the power of this tool.

How are the signals to be interpreted?

The Crypto Force Index helps us to highlight the overbought and oversold areas, with the use of circles under the price of candles and with a thermometer inserted at the base of the graph, where all the phases of strength and weakness are highlighted.

As soon as the red circles start to appear on the chart, that may be a good time to enter LONG to the market and start accumulating. If the circles are green, we can consider decreasing the current exposure by selling part of your portfolio, or decide to stay flat.

I personally use these signals on the weekly timeframe, to decide to feed my accumulation plan at the beginning of each month.

I hope it can be of help to you! Please help me improve the Crypto Force Index! :)

Co-relation and St-deviation Strategy - BNB/USDT 15minThis indicator based on statistical analysis. it uses standard deviation and its co-relation to price action to generate signals. and following indicators has been used to calculate standard deviation and its co-relation values. finally it is capable to identify market changes in bottoms to pic most suitable points.

1. Parabolic SAR (parabolic stop and reverse)

2. Supertrend

3. Relative strength index (RSI)

4. Money flow index (MFI)

5. Balance of Power

6. Chande Momentum Oscillator

7. Center of Gravity (COG)

8. Directional Movement Index (DMI)

9. Stochastic

10. Symmetrically weighted moving average with fixed length

11. True strength index (TSI)

12. Williams %R

13. Accumulation/distribution index

14. Intraday Intensity Index

15. Negative Volume Index

16. Positive Volume Index

17. On Balance Volume

18. Price-Volume Trend

19. True range

20. Volume-weighted average price

21. Williams Accumulation/Distribution

22. Williams Variable Accumulation/Distribution

23. Simple Moving Average

24. Exponential Moving Average

25. CCI (commodity channel index)

26. Chop Zone

27. Ease of Movement

28. Detrended Price Oscillator

29. Advance Decline Line

30. Bull Bear Power

Indicators Combination Framework v3 IND [DTU]Hello All,

This script is a framework to analyze and see the results by combine selected indicators for (long, short, longexit, shortexit) conditions.

I was designed this for beginners and users to facilitate to see effects of the technical indicators combinations on the chart WITH NO CODE

You can improve your strategies according the results of this system by connecting the framework to a strategy framework/template such as Pinecoder, Benson, daveatt or custom.

This is enhanced version of my previous indicator "Indicators & Conditions Test Framework "

Currently there are 93 indicators (23 newly added) connected over library. You can also import an External Indicator or add Custom indicator (In the source)

It is possible to change it from Indicator to strategy (simple one) by just remarking strategy parts in the source code and see real time profit of your combinations

Feel free to change or use it in your source

Special thanks goes to Pine wizards: Trading view (built-in Indicators), @Rodrigo, @midtownsk8rguy, @Lazybear, @Daveatt and others for their open source codes and contributions

SIMPLE USAGE

1. SETTING: Show Alerts= True (To see your entries and Exists)

2. Define your Indicators (ex: INDICATOR1: ema(close,14), INDICATOR2: ema(close,21), INDICATOR3: ema(close,200)

3. Define Your Combinations for long & Short Conditions

a. For Long: (INDICATOR1 crossover INDICATOR2) AND (INDICATOR3 < close)

b. For Short: (INDICATOR1 crossunder INDICATOR2) AND (INDICATOR3 > close)

4. Select Strategy/template (Import strategy to chart) that you export your signals from the list

5. Analyze the best profit by changing Indicators values

SOME INDICATORS DETAILS

Each Indicator includes:

- Factorization : Converting the selected indicator to Double, triple Quadruple such as EMA to DEMA, TEMA QEMA

- Log : Simple or log10 can be used for calculation on function entries

- Plot Type : You can overlay the indicator on the chart (such ema) or you can use stochastic/Percentrank approach to display in the variable hlines range

- Extended Parametes : You can use default parameters or you can use extended (P1,P2) parameters regarding to indicator type and your choice

- Color : You can define indicator color and line properties

- Smooth : you can enable swma smooth

- indicators : you can select one of the 93 function like ema(),rsi().. to define your indicator

- Source : you can select from already defined indicators (IND1-4), External Indicator (EXT), Custom Indicator (CUST), and other sources (close, open...)

CONDITION DETAILS

- There are are 4 type of conditions, long entry, short entry, long exit, short exit.

- Each condition are built up from 4 combinations that joined with "AND" & "OR" operators

- You can see the results by enabling show alerts check box

- If you only wants to enter long entry and long exit, just fill these conditions

- If "close on opposite" checkbox selected on settings, long entry will be closed on short entry and vice versa

COMBINATIONS DETAILS

- There are 4 combinations that joined with "AND" & "OR" operators for each condition

- combinations are built up from compare 1st entry with 2nd one by using operator

- 1st and 2nd entries includes already defined indicators (IND1-5), External Indicator (EXT), Custom Indicator (CUST), and other sources (close, open...)

- Operators are comparison values such as >,<, crossover,...

- 2nd entry include "VALUE" parameter that will use to compare 1st indicator with value area

- If 2nd indicator selected different than "VALUE", value are will mean previous value of the selection. (ex: value area= 2, 2nd entry=close, means close )

- Selecting "NONE" for the 1st entry will disable calculation of current and following combinations

JOINS DETAILS

- Each combination will join wiht the following one with the JOIN (AND, OR) operator (if the following one is not equal "NONE")

CUSTOM INDICATOR

- Custom Indicator defines harcoded in the source code.

- You can call it with "CUST" in the Indicator definition source or combination entries source

- You can change or implement your custom indicator by updating the source code

EXTERNAL INDICATOR

- You can import an external indicator by selecting it from the ext source.

- External Indicator should be already imported to the chart and it have an plot function to output its signal

EXPORTING SIGNAL

- You can export your result to an already defined strategy template such as Pine coders, Benson, Daveatt Strategy templates

- Or you can define your custom export for other future strategy templates

ALERTS

- By enabling show alerts checkbox, you can see long entry exits on the bottom, and short entry exits aon the top of the chart

ADDITIONAL INFO

- You can see all off the inputs descriptions in the tooltips. (You can also see the previous version for details)

- Availability to set start, end dates

- Minimize repainting by using security function options (Secure, Semi Secure, Repaint)

- Availability of use timeframes

-

Version 3 INDICATORS LIST (More to be added):

▼▼▼ OVERLAY INDICATORS ▼▼▼

alma(src,len,offset=0.85,sigma=6).-------Arnaud Legoux Moving Average

ama(src,len,fast=14,slow=100).-----------Adjusted Moving Average

accdist().-------------------------------Accumulation/distribution index.

cma(src,len).----------------------------Corrective Moving average

dema(src,len).---------------------------Double EMA (Same as EMA with 2 factor)

ema(src,len).----------------------------Exponential Moving Average

gmma(src,len).---------------------------Geometric Mean Moving Average

highest(src,len).------------------------Highest value for a given number of bars back.

hl2ma(src,len).--------------------------higest lowest moving average

hma(src,len).----------------------------Hull Moving Average.

lagAdapt(src,len,perclen=5,fperc=50).----Ehlers Adaptive Laguerre filter

lagAdaptV(src,len,perclen=5,fperc=50).---Ehlers Adaptive Laguerre filter variation

laguerre(src,len).-----------------------Ehlers Laguerre filter

lesrcp(src,len).-------------------------lowest exponential esrcpanding moving line

lexp(src,len).---------------------------lowest exponential expanding moving line

linreg(src,len,loffset=1).---------------Linear regression

lowest(src,len).-------------------------Lovest value for a given number of bars back.

mcginley(src, len.-----------------------McGinley Dynamic adjusts for market speed shifts, which sets it apart from other moving averages, in addition to providing clear moving average lines

percntl(src,len).------------------------percentile nearest rank. Calculates percentile using method of Nearest Rank.

percntli(src,len).-----------------------percentile linear interpolation. Calculates percentile using method of linear interpolation between the two nearest ranks.

previous(src,len).-----------------------Previous n (len) value of the source

pivothigh(src,BarsLeft=len,BarsRight=2).-Previous pivot high. src=src, BarsLeft=len, BarsRight=p1=2

pivotlow(src,BarsLeft=len,BarsRight=2).--Previous pivot low. src=src, BarsLeft=len, BarsRight=p1=2

rema(src,len).---------------------------Range EMA (REMA)

rma(src,len).----------------------------Moving average used in RSI. It is the exponentially weighted moving average with alpha = 1 / length.

sar(start=len, inc=0.02, max=0.02).------Parabolic SAR (parabolic stop and reverse) is a method to find potential reversals in the market price direction of traded goods.start=len, inc=p1, max=p2. ex: sar(0.02, 0.02, 0.02)

sma(src,len).----------------------------Smoothed Moving Average

smma(src,len).---------------------------Smoothed Moving Average

super2(src,len).-------------------------Ehlers super smoother, 2 pole

super3(src,len).-------------------------Ehlers super smoother, 3 pole

supertrend(src,len,period=3).------------Supertrend indicator

swma(src,len).---------------------------Sine-Weighted Moving Average

tema(src,len).---------------------------Triple EMA (Same as EMA with 3 factor)

tma(src,len).----------------------------Triangular Moving Average

vida(src,len).---------------------------Variable Index Dynamic Average

vwma(src,len).---------------------------Volume Weigted Moving Average

volstop(src,len,atrfactor=2).------------Volatility Stop is a technical indicator that is used by traders to help place effective stop-losses. atrfactor=p1

wma(src,len).----------------------------Weigted Moving Average

vwap(src_).------------------------------Volume Weighted Average Price (VWAP) is used to measure the average price weighted by volume

▼▼▼ NON OVERLAY INDICATORS ▼▼

adx(dilen=len, adxlen=14, adxtype=0).----adx. The Average Directional Index (ADX) is a used to determine the strength of a trend. len=>dilen, p1=adxlen (default=14), p2=adxtype 0:ADX, 1:+DI, 2:-DI (def:0)

angle(src,len).--------------------------angle of the series (Use its Input as another indicator output)

aroon(len,dir=0).------------------------aroon indicator. Aroons major function is to identify new trends as they happen.p1 = dir: 0=mid (default), 1=upper, 2=lower

atr(src,len).----------------------------average true range. RMA of true range.

awesome(fast=len=5,slow=34,type=0).------Awesome Oscilator is an indicator used to measure market momentum. defaults : fast=len= 5, p1=slow=34, p2=type: 0=Awesome, 1=difference

bbr(src,len,mult=1).---------------------bollinger %%

bbw(src,len,mult=2).---------------------Bollinger Bands Width. The Bollinger Band Width is the difference between the upper and the lower Bollinger Bands divided by the middle band.

cci(src,len).----------------------------commodity channel index

cctbbo(src,len).-------------------------CCT Bollinger Band Oscilator

change(src,len).-------------------------A.K.A. Momentum. Difference between current value and previous, source - source . is most commonly referred to as a rate and measures the acceleration of the price and/or volume of a security

cmf(len=20).-----------------------------Chaikin Money Flow Indicator used to measure Money Flow Volume over a set period of time. Default use is len=20

cmo(src,len).----------------------------Chande Momentum Oscillator. Calculates the difference between the sum of recent gains and the sum of recent losses and then divides the result by the sum of all price movement over the same period.

cog(src,len).----------------------------The cog (center of gravity) is an indicator based on statistics and the Fibonacci golden ratio.

copcurve(src,len).-----------------------Coppock Curve. was originally developed by Edwin Sedge Coppock (Barrons Magazine, October 1962).

correl(src,len).-------------------------Correlation coefficient. Describes the degree to which two series tend to deviate from their ta.sma values.

count(src,len).--------------------------green avg - red avg

cti(src,len).----------------------------Ehler s Correlation Trend Indicator by

dev(src,len).----------------------------ta.dev() Measure of difference between the series and its ta.sma

dpo(len).--------------------------------Detrended Price OScilator is used to remove trend from price.

efi(len).--------------------------------Elders Force Index (EFI) measures the power behind a price movement using price and volume.

eom(len=14,div=10000).-------------------Ease of Movement.It is designed to measure the relationship between price and volume.p1 = div: 10000= (default)

falling(src,len).------------------------ta.falling() Test if the `source` series is now falling for `length` bars long. (Use its Input as another indicator output)

fisher(len).-----------------------------Fisher Transform is a technical indicator that converts price to Gaussian normal distribution and signals when prices move significantly by referencing recent price data

histvol(len).----------------------------Historical volatility is a statistical measure used to analyze the general dispersion of security or market index returns for a specified period of time.

kcr(src,len,mult=2).---------------------Keltner Channels Range

kcw(src,len,mult=2).---------------------ta.kcw(). Keltner Channels Width. The Keltner Channels Width is the difference between the upper and the lower Keltner Channels divided by the middle channel.

klinger(type=len).-----------------------Klinger oscillator aims to identify money flow’s long-term trend. type=len: 0:Oscilator 1:signal

macd(src,len).---------------------------MACD (Moving Average Convergence/Divergence)

mfi(src,len).----------------------------Money Flow Index s a tool used for measuring buying and selling pressure

msi(len=10).-----------------------------Mass Index (def=10) is used to examine the differences between high and low stock prices over a specific period of time

nvi().-----------------------------------Negative Volume Index

obv().-----------------------------------On Balance Volume

pvi().-----------------------------------Positive Volume Index

pvt().-----------------------------------Price Volume Trend

ranges(src,upper=len, lower=-5).---------ranges of the source. src=src, upper=len, v1:lower=upper . returns: -1 source=upper otherwise 0

rising(src,len).-------------------------ta.rising() Test if the `source` series is now rising for `length` bars long. (Use its Input as another indicator output)

roc(src,len).----------------------------Rate of Change

rsi(src,len).----------------------------Relative strength Index

rvi(src,len).----------------------------The Relative Volatility Index (RVI) is calculated much like the RSI, although it uses high and low price standard deviation instead of the RSI’s method of absolute change in price.

smi_osc(src,len,fast=5, slow=34).--------smi Oscillator

smi_sig(src,len,fast=5, slow=34).--------smi Signal

stc(src,len,fast=23,slow=50).------------Schaff Trend Cycle (STC) detects up and down trends long before the MACD. Code imported from

stdev(src,len).--------------------------Standart deviation

trix(src,len) .--------------------------the rate of change of a triple exponentially smoothed moving average.

tsi(src,len).----------------------------The True Strength Index indicator is a momentum oscillator designed to detect, confirm or visualize the strength of a trend.

ultimateOsc(len.-------------------------Ultimate Oscillator indicator (UO) indicator is a technical analysis tool used to measure momentum across three varying timeframes

variance(src,len).-----------------------ta.variance(). Variance is the expectation of the squared deviation of a series from its mean (ta.sma), and it informally measures how far a set of numbers are spread out from their mean.

willprc(src,len).------------------------Williams %R

wad().-----------------------------------Williams Accumulation/Distribution.

wvad().----------------------------------Williams Variable Accumulation/Distribution.

HISTORY

v3.01

ADD: 23 new indicators added to indicators list from the library. Current Total number of Indicators are 93. (to be continued to adding)

ADD: 2 more Parameters (P1,P2) for indicator calculation added. Par:(Use Defaults) uses only indicator(Source, Length) with library's default parameters. Par:(Use Extra Parameters P1,P2) use indicator(Source,Length,p1,p2) with additional parameters if indicator needs.

ADD: log calculation (simple, log10) option added on indicator function entries

ADD: New Output Signals added for compatibility on exporting condition signals to different Strategy templates.

ADD: Alerts Added according to conditions results

UPD: Indicator source inputs now display with indicators descriptions

UPD: Most off the source code rearranged and some functions moved to the new library. Now system work like a little bit frontend/backend

UPD: Performance improvement made on factorization and other source code

UPD: Input GUI rearranged

UPD: Tooltips corrected

REM: Extended indicators removed

UPD: IND1-IND4 added to indicator data source. Now it is possible to create new indicators with the previously defined indicators value. ex: IND1=ema(close,14) and IND2=rsi(IND1,20) means IND2=rsi(ema(close,14),20)

UPD: Custom Indicator (CUST) added to indicator data source and Combination Indicator source.

UPD: Volume added to indicator data source and Combination Indicator source.

REM: Custom indicators removed and only one custom indicator left

REM: Plot Type "Org. Range (-1,1)" removed

UPD: angle, rising, falling type operators moved to indicator library

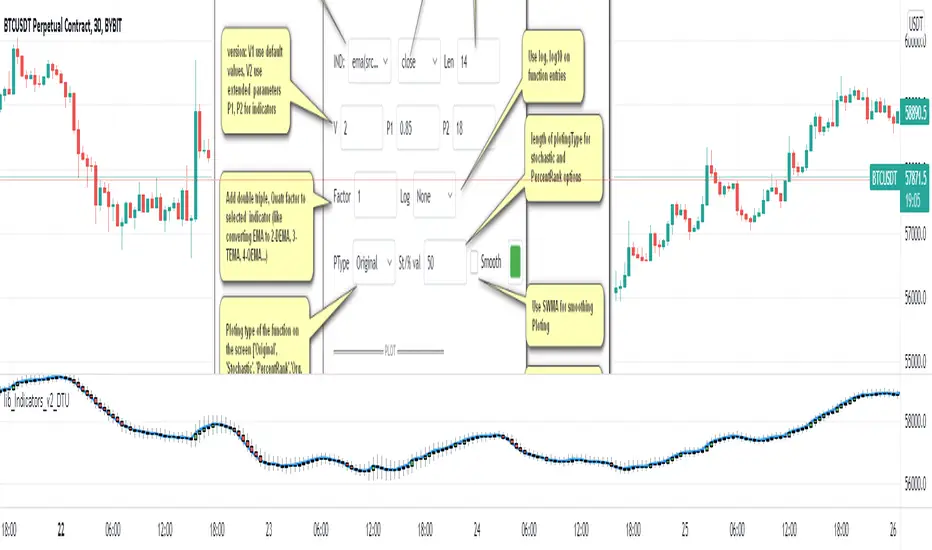

Indicator Functions with Factor and HeikinAshiHello all,

This indicator returns below selected indicators values with entered parameters.

Also you can add factorization, functions candles, function HeikinAshi and more to the plot.

VERSION:

Version 1: returns series only source and Length with already defined default values

Version 2: returns series with source, Length, p1 and p2 parameters according to the indicator definition (ex: )

PARAMETERS p1 p2

for defining multi arguments (See indicators list) indicator input value usable with verison=V2 selected.. ex: for alma( src , len ,offset=0.85,sigma=6), set source=source, len=length, p1=0.85 an p2=6

FACTOR:

Add double triple, Quadruple factors to selected indicator (like converting EMA to 2-DEMA, 3-TEMA, 4-QEMA...)

1-Original

2-Double

3-Triple

4-Quadruple

LOG

Log: Use log, log10 on function entries

PLOTTING:

PType: Plotting type of the function on the screen

Original :use original values

Org. Range (-1,1): usable for indicators between range -1 and 1

Stochastic: Convert indicator values by using stochastic calculation between -1 & 1. (use AT/% length to better view)

PercentRank: Convert indicator values by using Percent Rank calculation between -1 & 1. (use AT/% length to better view)

ST/%: length for plotting Type for stochastic and Percent Rank options

Smooth: Use SWMA for smoothing the function

DISPLAY TYPES

Plot Candles: Display the selected indicator as candle by implementing values

Plot Ind: Display result of indicator with selected source

HeikinAshi: Display Selected indicator candles with Heikin Ashi calculation

INDICATOR LIST:

hide = 'DONT DISPLAY', //Dont display & calculate the indicator. (For my framework usage)

alma = 'alma( src , len ,offset=0.85,sigma=6)', // Arnaud Legoux Moving Average

ama = 'ama( src , len ,fast=14,slow=100)', //Adjusted Moving Average

acdst = 'accdist()', // Accumulation/distribution index.

cma = 'cma( src , len )', //Corrective Moving average

dema = 'dema( src , len )', // Double EMA (Same as EMA with 2 factor)

ema = 'ema( src , len )', // Exponential Moving Average

gmma = 'gmma( src , len )', //Geometric Mean Moving Average

hghst = 'highest( src , len )', //Highest value for a given number of bars back.

hl2ma = 'hl2ma( src , len )', //higest lowest moving average

hma = 'hma( src , len )', // Hull Moving Average .

lgAdt = 'lagAdapt( src , len ,perclen=5,fperc=50)', //Ehler's Adaptive Laguerre filter

lgAdV = 'lagAdaptV( src , len ,perclen=5,fperc=50)', //Ehler's Adaptive Laguerre filter variation

lguer = 'laguerre( src , len )', //Ehler's Laguerre filter

lsrcp = 'lesrcp( src , len )', //lowest exponential esrcpanding moving line

lexp = 'lexp( src , len )', //lowest exponential expanding moving line

linrg = 'linreg( src , len ,loffset=1)', // Linear regression

lowst = 'lowest( src , len )', //Lovest value for a given number of bars back.

pcnl = 'percntl( src , len )', //percentile nearest rank. Calculates percentile using method of Nearest Rank.

pcnli = 'percntli( src , len )', //percentile linear interpolation. Calculates percentile using method of linear interpolation between the two nearest ranks.

rema = 'rema( src , len )', //Range EMA (REMA)

rma = 'rma( src , len )', //Moving average used in RSI . It is the exponentially weighted moving average with alpha = 1 / length.

sma = 'sma( src , len )', // Smoothed Moving Average

smma = 'smma( src , len )', // Smoothed Moving Average

supr2 = 'super2( src , len )', //Ehler's super smoother, 2 pole

supr3 = 'super3( src , len )', //Ehler's super smoother, 3 pole

strnd = 'supertrend( src , len ,period=3)', //Supertrend indicator

swma = 'swma( src , len )', //Sine-Weighted Moving Average

tema = 'tema( src , len )', // Triple EMA (Same as EMA with 3 factor)

tma = 'tma( src , len )', //Triangular Moving Average

vida = 'vida( src , len )', // Variable Index Dynamic Average

vwma = 'vwma( src , len )', // Volume Weigted Moving Average

wma = 'wma( src , len )', //Weigted Moving Average

angle = 'angle( src , len )', //angle of the series (Use its Input as another indicator output)

atr = 'atr( src , len )', // average true range . RMA of true range.

bbr = 'bbr( src , len ,mult=1)', // bollinger %%

bbw = 'bbw( src , len ,mult=2)', // Bollinger Bands Width . The Bollinger Band Width is the difference between the upper and the lower Bollinger Bands divided by the middle band.

cci = 'cci( src , len )', // commodity channel index

cctbb = 'cctbbo( src , len )', // CCT Bollinger Band Oscilator

chng = 'change( src , len )', //Difference between current value and previous, source - source.

cmo = 'cmo( src , len )', // Chande Momentum Oscillator . Calculates the difference between the sum of recent gains and the sum of recent losses and then divides the result by the sum of all price movement over the same period.

cog = 'cog( src , len )', //The cog (center of gravity ) is an indicator based on statistics and the Fibonacci golden ratio.

cpcrv = 'copcurve( src , len )', // Coppock Curve. was originally developed by Edwin "Sedge" Coppock (Barron's Magazine, October 1962).

corrl = 'correl( src , len )', // Correlation coefficient . Describes the degree to which two series tend to deviate from their ta. sma values.

count = 'count( src , len )', //green avg - red avg

dev = 'dev( src , len )', //ta.dev() Measure of difference between the series and it's ta. sma

fall = 'falling( src , len )', //ta.falling() Test if the `source` series is now falling for `length` bars long. (Use its Input as another indicator output)

kcr = 'kcr( src , len ,mult=2)', // Keltner Channels Range

kcw = 'kcw( src , len ,mult=2)', //ta.kcw(). Keltner Channels Width. The Keltner Channels Width is the difference between the upper and the lower Keltner Channels divided by the middle channel.

macd = 'macd( src , len )', // macd

mfi = 'mfi( src , len )', // Money Flow Index

nvi = 'nvi()', // Negative Volume Index

obv = 'obv()', // On Balance Volume

pvi = 'pvi()', // Positive Volume Index

pvt = 'pvt()', // Price Volume Trend

rise = 'rising( src , len )', //ta.rising() Test if the `source` series is now rising for `length` bars long. (Use its Input as another indicator output)

roc = 'roc( src , len )', // Rate of Change

rsi = 'rsi( src , len )', // Relative strength Index

smosc = 'smi_osc( src , len ,fast=5, slow=34)', //smi Oscillator

smsig = 'smi_sig( src , len ,fast=5, slow=34)', //smi Signal

stdev = 'stdev( src , len )', //Standart deviation

trix = 'trix( src , len )' , //the rate of change of a triple exponentially smoothed moving average .

tsi = 'tsi( src , len )', //True Strength Index

vari = 'variance( src , len )', //ta.variance(). Variance is the expectation of the squared deviation of a series from its mean (ta. sma ), and it informally measures how far a set of numbers are spread out from their mean.

wilpc = 'willprc( src , len )', // Williams %R

wad = 'wad()', // Williams Accumulation/Distribution .

wvad = 'wvad()' //Williams Variable Accumulation/Distribution

I will update the indicator list when I will update the library

Thanks to tradingview, @RodrigoKazuma for their open source indicators

lib_Indicators_v2_DTULibrary "lib_Indicators_v2_DTU"

This library functions returns included Moving averages, indicators with factorization, functions candles, function heikinashi and more.

Created it to feed as backend of my indicator/strategy "Indicators & Combinations Framework Advanced v2 " that will be released ASAP.

This is replacement of my previous indicator (lib_indicators_DT)

I will add an indicator example which will use this indicator named as "lib_indicators_v2_DTU example" to help the usage of this library

Additionally library will be updated with more indicators in the future

NOTES:

Indicator functions returns only one series :-(

plotcandle function returns candle series

INDICATOR LIST:

hide = 'DONT DISPLAY', //Dont display & calculate the indicator. (For my framework usage)

alma = 'alma(src,len,offset=0.85,sigma=6)', //Arnaud Legoux Moving Average

ama = 'ama(src,len,fast=14,slow=100)', //Adjusted Moving Average

acdst = 'accdist()', //Accumulation/distribution index.

cma = 'cma(src,len)', //Corrective Moving average

dema = 'dema(src,len)', //Double EMA (Same as EMA with 2 factor)

ema = 'ema(src,len)', //Exponential Moving Average

gmma = 'gmma(src,len)', //Geometric Mean Moving Average

hghst = 'highest(src,len)', //Highest value for a given number of bars back.

hl2ma = 'hl2ma(src,len)', //higest lowest moving average

hma = 'hma(src,len)', //Hull Moving Average.

lgAdt = 'lagAdapt(src,len,perclen=5,fperc=50)', //Ehler's Adaptive Laguerre filter

lgAdV = 'lagAdaptV(src,len,perclen=5,fperc=50)', //Ehler's Adaptive Laguerre filter variation

lguer = 'laguerre(src,len)', //Ehler's Laguerre filter

lsrcp = 'lesrcp(src,len)', //lowest exponential esrcpanding moving line

lexp = 'lexp(src,len)', //lowest exponential expanding moving line

linrg = 'linreg(src,len,loffset=1)', //Linear regression

lowst = 'lowest(src,len)', //Lovest value for a given number of bars back.

pcnl = 'percntl(src,len)', //percentile nearest rank. Calculates percentile using method of Nearest Rank.

pcnli = 'percntli(src,len)', //percentile linear interpolation. Calculates percentile using method of linear interpolation between the two nearest ranks.

rema = 'rema(src,len)', //Range EMA (REMA)

rma = 'rma(src,len)', //Moving average used in RSI. It is the exponentially weighted moving average with alpha = 1 / length.

sma = 'sma(src,len)', //Smoothed Moving Average

smma = 'smma(src,len)', //Smoothed Moving Average

supr2 = 'super2(src,len)', //Ehler's super smoother, 2 pole

supr3 = 'super3(src,len)', //Ehler's super smoother, 3 pole

strnd = 'supertrend(src,len,period=3)', //Supertrend indicator

swma = 'swma(src,len)', //Sine-Weighted Moving Average

tema = 'tema(src,len)', //Triple EMA (Same as EMA with 3 factor)

tma = 'tma(src,len)', //Triangular Moving Average

vida = 'vida(src,len)', //Variable Index Dynamic Average

vwma = 'vwma(src,len)', //Volume Weigted Moving Average

wma = 'wma(src,len)', //Weigted Moving Average

angle = 'angle(src,len)', //angle of the series (Use its Input as another indicator output)

atr = 'atr(src,len)', //average true range. RMA of true range.

bbr = 'bbr(src,len,mult=1)', //bollinger %%

bbw = 'bbw(src,len,mult=2)', //Bollinger Bands Width. The Bollinger Band Width is the difference between the upper and the lower Bollinger Bands divided by the middle band.

cci = 'cci(src,len)', //commodity channel index

cctbb = 'cctbbo(src,len)', //CCT Bollinger Band Oscilator

chng = 'change(src,len)', //Difference between current value and previous, source - source .

cmo = 'cmo(src,len)', //Chande Momentum Oscillator. Calculates the difference between the sum of recent gains and the sum of recent losses and then divides the result by the sum of all price movement over the same period.

cog = 'cog(src,len)', //The cog (center of gravity) is an indicator based on statistics and the Fibonacci golden ratio.

cpcrv = 'copcurve(src,len)', //Coppock Curve. was originally developed by Edwin "Sedge" Coppock (Barron's Magazine, October 1962).

corrl = 'correl(src,len)', //Correlation coefficient. Describes the degree to which two series tend to deviate from their ta.sma values.

count = 'count(src,len)', //green avg - red avg

dev = 'dev(src,len)', //ta.dev() Measure of difference between the series and it's ta.sma

fall = 'falling(src,len)', //ta.falling() Test if the `source` series is now falling for `length` bars long. (Use its Input as another indicator output)

kcr = 'kcr(src,len,mult=2)', //Keltner Channels Range

kcw = 'kcw(src,len,mult=2)', //ta.kcw(). Keltner Channels Width. The Keltner Channels Width is the difference between the upper and the lower Keltner Channels divided by the middle channel.

macd = 'macd(src,len)', //macd

mfi = 'mfi(src,len)', //Money Flow Index

nvi = 'nvi()', //Negative Volume Index

obv = 'obv()', //On Balance Volume

pvi = 'pvi()', //Positive Volume Index

pvt = 'pvt()', //Price Volume Trend

rise = 'rising(src,len)', //ta.rising() Test if the `source` series is now rising for `length` bars long. (Use its Input as another indicator output)

roc = 'roc(src,len)', //Rate of Change

rsi = 'rsi(src,len)', //Relative strength Index

smosc = 'smi_osc(src,len,fast=5, slow=34)', //smi Oscillator

smsig = 'smi_sig(src,len,fast=5, slow=34)', //smi Signal

stdev = 'stdev(src,len)', //Standart deviation

trix = 'trix(src,len)' , //the rate of change of a triple exponentially smoothed moving average.

tsi = 'tsi(src,len)', //True Strength Index

vari = 'variance(src,len)', //ta.variance(). Variance is the expectation of the squared deviation of a series from its mean (ta.sma), and it informally measures how far a set of numbers are spread out from their mean.

wilpc = 'willprc(src,len)', //Williams %R

wad = 'wad()', //Williams Accumulation/Distribution.

wvad = 'wvad()' //Williams Variable Accumulation/Distribution.

}

f_func(string, float, simple, float, float, float, simple) f_func Return selected indicator value with different parameters. New version. Use extra parameters for available indicators

Parameters:

string : FuncType_ indicator from the indicator list

float : src_ close, open, high, low,hl2, hlc3, ohlc4 or any

simple : int length_ indicator length

float : p1 extra parameter-1. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p2 extra parameter-2. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p3 extra parameter-3. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

simple : int version_ indicator version for backward compatibility. V1:dont use extra parameters p1,p2,p3 and use default values. V2: use extra parameters for available indicators

Returns: float Return calculated indicator value

fn_heikin(float, float, float, float) fn_heikin Return given src data (open, high,low,close) as heikin ashi candle values

Parameters:

float : o_ open value

float : h_ high value

float : l_ low value

float : c_ close value

Returns: float heikin ashi open, high,low,close vlues that will be used with plotcandle

fn_plotFunction(float, string, simple, bool) fn_plotFunction Return input src data with different plotting options

Parameters:

float : src_ indicator src_data or any other series.....

string : plotingType Ploting type of the function on the screen

simple : int stochlen_ length for plotingType for stochastic and PercentRank options

bool : plotSWMA Use SWMA for smoothing Ploting

Returns: float

fn_funcPlotV2(string, float, simple, float, float, float, simple, string, simple, bool, bool) fn_funcPlotV2 Return selected indicator value with different parameters. New version. Use extra parameters fora available indicators

Parameters:

string : FuncType_ indicator from the indicator list

float : src_data_ close, open, high, low,hl2, hlc3, ohlc4 or any

simple : int length_ indicator length

float : p1 extra parameter-1. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p2 extra parameter-2. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p3 extra parameter-3. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

simple : int version_ indicator version for backward compatibility. V1:dont use extra parameters p1,p2,p3 and use default values. V2: use extra parameters for available indicators

string : plotingType Ploting type of the function on the screen

simple : int stochlen_ length for plotingType for stochastic and PercentRank options

bool : plotSWMA Use SWMA for smoothing Ploting

bool : log_ Use log on function entries

Returns: float Return calculated indicator value

fn_factor(string, float, simple, float, float, float, simple, simple, string, simple, bool, bool) fn_factor Return selected indicator's factorization with given arguments

Parameters:

string : FuncType_ indicator from the indicator list

float : src_data_ close, open, high, low,hl2, hlc3, ohlc4 or any

simple : int length_ indicator length

float : p1 parameter-1. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p2 parameter-2. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p3 parameter-3. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

simple : int version_ indicator version for backward compatibility. V1:dont use extra parameters p1,p2,p3 and use default values. V2: use extra parameters for available indicators

simple : int fact_ Add double triple, Quatr factor to selected indicator (like converting EMA to 2-DEMA, 3-TEMA, 4-QEMA...)

string : plotingType Ploting type of the function on the screen

simple : int stochlen_ length for plotingType for stochastic and PercentRank options

bool : plotSWMA Use SWMA for smoothing Ploting

bool : log_ Use log on function entries

Returns: float Return result of the function

fn_plotCandles(string, simple, float, float, float, simple, string, simple, bool, bool, bool) fn_plotCandles Return selected indicator's candle values with different parameters also heikinashi is available

Parameters:

string : FuncType_ indicator from the indicator list

simple : int length_ indicator length

float : p1 parameter-1. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p2 parameter-2. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p3 parameter-3. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

simple : int version_ indicator version for backward compatibility. V1:dont use extra parameters p1,p2,p3 and use default values. V2: use extra parameters for available indicators

string : plotingType Ploting type of the function on the screen

simple : int stochlen_ length for plotingType for stochastic and PercentRank options

bool : plotSWMA Use SWMA for smoothing Ploting

bool : log_ Use log on function entries

bool : plotheikin_ Use Heikin Ashi on Plot

Returns: float

SMA Squeeze Oscillator█ OVERVIEW

SMA Squeeze Oscillator is a momentum oscillator based on the relationship between multiple SMA moving averages. It combines volatility compression analysis (Squeeze), wave-style momentum structure, trend filtering, breakout signals, and divergence detection.

The indicator is designed to identify periods of market compression (low volatility), which are often followed by dynamic price moves. Additionally, it visualizes momentum and trend structure in a clean and readable way, without using a classic histogram.

█ CONCEPT

The core of the indicator is built on three SMA moving averages with different lengths. The distance between them (spread) is compared to ATR, which allows the detection of volatility compression (Squeeze).

- When the SMA spread is smaller than ATR × multiplier, the market is considered to be in Squeeze

- When the spread expands beyond this threshold, the market exits the Squeeze – often signaling the beginning of an impulse

Momentum is calculated from the relationship between the faster SMA and the slower SMAs, then smoothed. Instead of a traditional histogram, the indicator displays continuous momentum waves above and below the zero line, making changes in momentum structure easier to read.

An optional SMA trend filter can be used to limit signals to the direction of the current trend.

█ FEATURES

Calculations

- three SMA moving averages

- ATR as a volatility measure

- Squeeze detection based on SMA spread

- wave-based momentum oscillator with smoothing

- optional SMA trend filter

Visualization

- momentum waves above / below the zero line

- bullish / bearish trend fills

- separate fill and color for Squeeze phases

- thick zero line reflecting current trend

- wave-style candle coloring based on momentum

- first wave markers after exiting Squeeze

- bullish and bearish divergence visualization

Signals

- momentum zero-line cross (Bull / Bear Cross)

- first momentum wave after Squeeze

- classic bullish and bearish divergences

Alerts

- Bull Cross

- Bear Cross

- First Bullish after Squeeze

- First Bearish after Squeeze

- Bullish Divergence

- Bearish Divergence

█ HOW TO USE

Adding the indicator

Paste the code into Pine Editor or search for “SMA Squeeze Oscillator” on TradingView.

Main settings

- SMA 1 / 2 / 3 – lengths of SMAs used for Squeeze and momentum

- ATR Length / Multiplier – Squeeze detection sensitivity

- ATR Multiplier = 0 → the indicator does not display Squeeze zones

- Momentum Smoothing – smoothing of momentum waves

- Enable SMA Filter – trend filter

- the current trend is reflected by the zero-line color

- price below SMA → bearish trend

- price above SMA → bullish trend

- when enabled, it filters Bull / Bear Cross and First Bullish / Bearish after Squeeze signals, allowing only those aligned with the trend

- Enable candle coloring – wave-style candle coloring

- Enable Divergence – divergence detection

█ APPLICATION

Squeeze & Breakout

Squeeze phases indicate low volatility and energy accumulation. A breakout from Squeeze often leads to a strong directional move.

The SMA filter is not required – instead, users may apply:

- a more advanced trend filter

- structural confirmation (level break, correction completion)

- additional price-action tools

Momentum trading

The direction and slope of momentum waves help assess impulse strength and loss of momentum.

A momentum reversal can act as an early signal of a correction or potential trend change, often before it becomes visible on price.

Divergences

The indicator detects classic bullish and bearish divergences.

Important notes:

- divergences appear with a delay equal to the pivot length required for detection, by default, this delay is two candles

- divergences forming on small momentum waves or inside a Squeeze are often misleading and should be treated with caution

█ NOTES

- the indicator works best when used in market context

- Squeeze reflects volatility, not direction

- it is not a standalone trading system

[SMC] Binet Nexus Alpha : Institutional Liquidity & Order BlocksBINET™ NEXUS ALPHA : The Institutional SMC Terminal

Overview

The BINET™ NEXUS ALPHA is a professional-grade execution terminal designed to bridge the gap between retail "Smart Money Concepts" and actual institutional data. Built on the proprietary BINET™ Core v17.5 engine, this terminal prioritizes Price Action Narrative over lagging signals.

Unlike basic SMC indicators that clutter charts with unverified boxes, the Nexus Alpha uses an Institutional Confluence Engine to filter out retail "stop-run" noise and identify high-conviction zones where big money is actually positioning.

The Narrative Engine (Visual Intelligence)

The terminal replaces abstract lines with a high-visibility geometric narrative designed for rapid scanning on 4K/high-res monitors:

█ (Solid Blue Block): Institutional Vol Spike. Represents a "Foundation Surge" where volume significantly exceeds retail averages.

◆ (Gold Diamond): Liquidity Hunt. Direct identification of price tapping into resting Order Blocks (OB) or Fair Value Gaps (FVG).

● (Blue Circle): Macro Accumulation. Alerts you to long-term institutional position building.

▲/▼ (Triangles): Market Structure Breaks. Real-time Break of Structure (BOS) tracking.

The Command HUD (Mission Control)

The terminal features a real-time Hierarchical HUD that audits every trade before you enter:

Signal Quality (Sync Score): A 0-100% confluence rating. 85%+ represents "Elite Institutional Sync."

Stop Advisor & Risk Meter: Calculates the highest-volume liquidity bin for stop placement and warns you if the Max Stop Distance (%) is exceeded.

Market Health Engine: Automatically detects the current regime (Scalp, Swing, or Position) to adjust your execution strategy.

Success Probability: A rolling trajectory of the system's performance, showing whether recent win-rates are trending up (▲) or down (▼).

Institutional Workflow

Filter: Check the Trade Bias (Long/Short) on the HUD.

Confirm: Wait for the Sync Score to cross your threshold (Default 65%).

Audit: Verify that the Risk Meter is not in "High Exposure" mode.

Execute: Target the provided TP1/TP2 levels projected on the chart.

Technical Specifications

Language: Pine Script® v6

Logic: Smart Money Concepts (SMC) + Volume Delta Analysis

Core: BINET™ v17.5 Concurrency Engine

Founder's Note

The BINET™ NEXUS ALPHA was designed for traders who demand institutional-grade transparency. It is the final piece of the BINET Suite, designed to be used alongside the Macro Sector Rotation and Trend Matrix tools for a complete Top-Down to Bottom-Up trading workflow.

Minervini Ultimate +VCPMinervini Ultimate Suite (SEPA Dashboard)

This indicator implements Mark Minervini's "Trend Template" criteria combined with a Volatility Contraction Pattern (VCP) detector and a custom Relative Strength rating. It is designed to help traders visualize the technical health of a stock based on stage analysis concepts.

This indicator serves as a complete Control System (Dashboard) for Mark Minervini's SEPA trading strategy. Instead of manually checking five different metrics on every chart, this indicator performs the mathematical calculations and presents the "bottom line" in a single, organized table.

1. What This Indicator Does

The goal is to ensure you never enter a trade blindly. It verifies the stock against Minervini's strict requirements:

Trend: Is the stock in a healthy Stage 2 Uptrend?

Relative Strength: Is it stronger than the general market?

Buy Risk: Is it the right time to buy, or is the price extended?

Pressure: Are institutions accumulating or distributing?

VCP: Is there a breakout opportunity (volatility contraction) right now?

2. Key Benefits

Time-Saving: Instead of drawing lines and calculating percentages manually, you get immediate visual feedback (Green/Red).

Discipline: The indicator will flag "Extended" (Red) if you attempt to buy a stock that has run up too much, saving you from late entries and unnecessary losses.

Precision Timing: The VCP feature (Blue Dots) helps you identify the "calm before the storm"—the exact moment volatility contracts, which often precedes a major breakout.

3. Indicator Parameters & Features

A. Minervini Pressure (Buying vs. Selling)

What it checks: Money flow over the last 20 days.

Calculation: Sums up volume on "Up Days" (Green) versus volume on "Down Days" (Red).

Meaning:

🟢 Buying: More money is entering than leaving. A sign of institutional accumulation.

🔴 Selling: Selling pressure dominates. The price may be rising, but without strong volume backing.

B. Buy Risk (Price Extension)

What it checks: The distance of the current price from the 50-Day Moving Average. Minervini strictly warns against "chasing" stocks.

Signals:

🟢 Low Risk: Price is within 0% – 15% of the 50MA. This is the ideal "Buy Zone".

🟡 Caution: Price is 15% – 25% away. Buy with increased caution.

🔴 Extended: Price is >25% from the MA. Do not buy. The probability of a pullback is high.

⚪ Broken: Price is below the 50MA. The short-term trend is damaged.

C. TPR - Trend Template (Trend Power Rating)

What it checks: Is the stock in a Stage 2 Uptrend?

Strict Rules (All must be true for a PASS):

Price > 50MA > 150MA > 200MA.

The 200MA is trending UP (positive slope).

Price is near the 52-Week High (within 25%).

Price is above the 52-Week Low (at least 25%).

Meaning:

🟢 PASSED: Technically healthy and ready to move.

🔴 FAILED: The trend structure is broken (e.g., MAs are entangled).

D. RPR Score (Relative Performance Rating)

What it checks: How strong the stock is compared to the general market (S&P 500 / SPY).

Calculation: Weighted performance over 3, 6, 9, and 12 months vs. the SPY. The score ranges from 1 to 99.

Meaning:

🟢 80-99: Market Leader. These are the stocks Minervini targets.

🟡 70-80: Good, but not elite.

⚪ Below 70: Laggard (weaker than the market).

E. VCP Action (Volatility Contraction Pattern)

What it checks: Monitors price tightness. It calculates the range between the highest close and lowest close over the last 5 days.

Meaning:

🔵 SQUEEZE (Blue Text + Blue Dot on Chart): The price range has contracted to less than 2.5%.

Why it matters: When a stock stops moving wildly and trades in a tight range ("Flat Line"), it indicates supply has dried up. A high-volume breakout often follows immediately.

Momentum Trend & Ignition DashboardDescription

Rationale & Originality Traders often struggle with chart clutter, needing separate indicators for Moving Averages, Volume anomalies, and Fundamental stats (like 52-week highs or Float). This script solves this problem by creating a unified "Momentum Dashboard." It is not just a collection of averages; it is a purpose-built tool for Breakout and Trend Following strategies (such as CAN SLIM or VCP).

The uniqueness of this script lies in its "Confluence Logic": it allows a trader to instantly validate a setup by checking three pillars simultaneously without changing tabs:

Trend: Are the key MAs (20, 50, 100, 200) stacked correctly?

Ignition: Is there a "Power Play" (Big Price Move + Heavy Volume) occurring right now?

Stats: Is the stock near its 52-week high, and does it have a supportive Up/Down Volume Ratio?

How It Works (Detailed Calculations)

1. Custom Trend Ribbon (4x MA Mix):

The script plots 4 independent Moving Averages.

Innovation: Unlike standard inputs, each MA can be individually toggled between SMA (Simple) or EMA (Exponential). This allows traders to mix "Fast" trend lines (e.g., 10 or 20 EMA) with "Slow" institutional lines (e.g., 50 or 200 SMA) in one overlay.

2. "Purple Dot" Ignition Detection:

This features a custom detection algorithm for "Ignition Bars."

Logic: It compares the current candle's Close to the previous Close. If the move exceeds a user-defined threshold (default 5%) AND the Volume exceeds a fixed liquidity threshold (default 500k), a Purple Dot is plotted.

This filters out "low volume drift" and highlights true institutional participation.

3. Relative Volume (RVol) Engine:

Calculates the ratio of Current Volume to the 50-period SMA of Volume.

Visuals: If the ratio exceeds the user threshold (e.g., 1.5x average), the dashboard highlights the data, and optionally the chart bars, alerting the trader to unusual activity.

4. Statistical Dashboard (Data Panel):

Using request.security, the panel fetches daily timeframe data regardless of the chart view.

52-Week & 13-Week H/L: Calculates the percentage distance from these key levels to gauge overhead supply.

U/D Ratio: Calculates the sum of volume on "Up Days" vs. "Down Days" over 50 periods. A value > 1.0 suggests institutional accumulation.

Float %: (Stocks Only) Fetches financial data to show the percentage of shares available for trading.

How to Use This Script

This script is designed for Trend Following and Breakout Trading:

The Setup: Use the Data Panel to find stocks with a U/D Ratio > 1.0 and price within 15% of the 52-Week High.

The Trend: Ensure price is above the MA 2 (set to 50 SMA) and MA 4 (set to 200 SMA) to confirm a Stage 2 uptrend.

The Trigger: Watch for the Purple Dot.

If a Purple Dot appears as price breaks out of a consolidation (base), it confirms institutional buying.

Use the RVol panel to confirm that volume is at least 1.5x normal levels.

Risk Management: Use the MA 1 (set to 20 EMA) as a trailing stop-loss during strong trends.

Settings & Configuration

MAs: Fully adjustable Length and Type (SMA/EMA).

Big Move (Purple Dot): Adjust the % Move based on asset volatility (e.g., use 3% for Large Caps, 10% for Crypto).

Table: The data panel is fully dynamic. You can toggle specific rows (like Float or SMA distance) On/Off to save screen space, and position it anywhere on the chart.

Credits & References

The concept of Relative Volume (RVol) and U/D Ratio is derived from standard Volume Analysis used by William O'Neil.

The "Big Move" combined with Volume thresholds is based on standard Volume Spread Analysis (VSA) concepts regarding "Effort vs. Result."

Financial data fetch (Float) utilizes TradingView's built-in financial() library.

Options Gamma Flip Zones [BackQuant]Options Gamma Flip Zones

A market-structure style “gamma flip” mapper that builds adaptive strike-like zones, scores how price interacts with them, then promotes the strongest candidates into confirmed flip zones. Designed to highlight pinning, failed breaks, and rotational behavior without needing live options chain data.

What this indicator does

This script identifies price levels that behave like “strike magnets” during conditions that resemble options pinning, then draws dynamic zones around those levels.

Instead of assuming every round number matters, it:

Creates a strike ladder (auto or manual step).

Applies a regime filter that looks for “pin-friendly” market conditions.

Tracks and scores repeated interactions with the level.

Upgrades a zone from candidate to confirmed when enough evidence accumulates.

Invalidates zones when price achieves sustained acceptance away from them.

The output is a set of shaded boxes (zones) centered on strike-like levels, with text readouts that show the current state of each zone.

Key concept: “Gamma proxy”

A true gamma flip requires options positioning data. This indicator does not use options chain gamma.

Instead, it uses a proxy approach:

When markets have elevated volatility relative to their recent baseline AND trend strength is weak, price often behaves “sticky” around key levels.

In those conditions, repeated touches and failed escapes around a level behave similarly to pinning around strikes.

So this tool is best read as:

“Where would a strike-like magnet likely exist right now, based on price behavior and regime conditions?”

How zones are created

Zones only start forming when the script detects a pin-friendly regime.

1) Strike Ladder (level selection)

Auto Strike Step selects a step size based on current price magnitude (bigger price, bigger step).

Manual Strike Step lets you force a fixed increment.

The current “active level” is the nearest rounded level to price.

Major Level Every optionally marks major ladder levels (multiples of step).

2) Band construction (zone thickness)

Each zone is a symmetric band around the level, using one of two modes:

ATR mode scales thickness with volatility.

Percent mode scales thickness as a fraction of price.

This matters because “pin behavior” is not a single tick. It’s a region where price repeatedly probes and rejects.

Regime filter (when the script is allowed to believe in pinning)

A zone is only eligible to form and strengthen when Pin Regime is active. Pin Regime is a conjunction of:

1) IV proxy (ATR z-score)

Uses ATR as a volatility proxy.

Converts ATR% into a z-score relative to a long lookback.

IV Proxy Threshold controls how elevated volatility must be before the script considers pinning likely.

2) Weak trend requirement

The script also requires price action to be non-trending:

EMA spread must be small (fast vs slow EMA not diverging strongly).

ADX must be below a ceiling, confirming weak directional trend strength.

Interpretation:

High “IV proxy” + weak trend is where pin-like behavior is most common.

If trend is strong, zones are less meaningful because price is more likely to accept away from levels.

Flip confirmation logic (what upgrades a zone)

A zone is not “confirmed” just because price is near it once. The script builds conviction via evidence accumulation.

Evidence types:

Touches : price comes close to the level within tolerance.

Failed escapes : price pushes outside the band but closes back inside (rejection).

Acceptance run : consecutive closes outside the band, suggesting price is accepting away from the zone.

Protections:

Touch Cooldown prevents counting the same micro-chop as multiple touches.

Acceptance Bars defines what “real acceptance” means, so the zone does not get invalidated by one noisy bar.

A zone becomes confirmed when:

Touches meet the “evidence” requirement.

Failed escapes meet the “rejection” requirement.

The regime filter still says the market is pin-friendly.

That is important, it avoids promoting levels that only worked briefly in a trending tape.

Zone scoring and lifecycle

Each zone maintains a score that evolves over time. Think of score as “how much this level has recently behaved like a magnet.”

Score dynamics:

Decay per bar : score fades over time if price stops respecting the zone.

+ per touch : repeated proximity increases score.

+ per failed escape : rejections add stronger reinforcement.

- per acceptance bar : sustained trading outside reduces score.

Min score to draw : prevents clutter from weak, low-confidence zones.

Invalidation:

If the score becomes very weak AND price achieves sustained acceptance away from the zone, the zone is deleted.

This keeps the chart clean and ensures zones represent current market behavior, not ancient levels.

How to read the plot on chart

1) Zone fill and border

Each zone is drawn as a box extended to the right.

Fill opacity adapts to zone strength, strong zones are visually more prominent.

Border color encodes the current directional context and special events.

2) Bullish vs bearish coloring

A zone is colored bullish when price is currently trading above the zone’s mid-level.

A zone is colored bearish when price is currently trading below it.

This is not a trade signal by itself, it is a state cue for “which side is in control around the level.”

3) Failed escape highlighting

If price attempts to break above the band and fails, the border temporarily highlights as a failed up escape.

If price attempts to break below the band and fails, the border temporarily highlights as a failed down escape.

These are the moments where pin behavior is most visible:

Break attempt.

Immediate rejection.

Return to the band.

4) Midline (optional)

The zone midline is the strike-like level itself.

It is dotted to distinguish it from price structure lines.

5) Optional strike ladder overlay

When enabled, the script draws major and minor ladder lines near current price.

Major levels are thicker and less transparent.

This is a visualization aid for “where the algorithm is rounding,” not a prediction tool.

On-chart text readout (what the box text means)

Each box prints a compact state summary, designed for fast scanning:

Γ CANDIDATE means the zone is being tracked but not yet validated.

Γ FLIP (PROXY) means the zone has met confirmation requirements.

BULL/BEAR indicates which side price is on relative to the mid-level.

L prints the level value.

T is touch count, repeated proximity events.

F is fail count, rejected escape attempts.

IVz is the volatility proxy z-score at the moment.

ADX is the trend strength context.

Practical use cases

1) Pinning and range trading context

Confirmed zones often act like gravity wells in sideways or rotational regimes.

When price repeatedly fails to escape, fading outer edges can be reasonable context for mean reversion workflows.

2) Breakout validation

If price achieves acceptance outside the band for multiple bars, that is stronger breakout context than a single wick.

Zones that invalidate cleanly can mark transitions from pinning to directional move.

3) Time your “do nothing” periods

When Pin Regime is active and a zone is confirmed, the tape often becomes sticky and inefficient for trend chasing.

This helps avoid taking trend entries into a pin environment.

Alerts

Standalone alertconditions are included:

Zone Confirmed : a candidate becomes confirmed.

Zone Touch : price touches an active zone within tolerance.

Zone Invalidated : the zone loses relevance and is removed.

Tuning guidelines

Sensitivity vs quality

Lower Touches Needed and Failed Escapes Needed creates more zones faster, but with lower quality.

Higher values create fewer zones, but the ones that remain are more behaviorally “proven.”

Band width

ATR mode adapts to volatility and is typically safer across assets.

Percent mode is consistent visually but can feel too tight in high vol or too wide in low vol if not tuned.

Regime thresholds

If you want fewer zones, raise IV proxy threshold and tighten weak-trend filters.

If you want more zones, lower IV proxy threshold and loosen weak-trend filters.

Limitations

This is a proxy model, not live options gamma.

In strong trends, pinning assumptions can break, the regime filter is there to reduce that risk, but not eliminate it.

Auto strike step is designed for typical market ranges, manual step is recommended for niche tick sizes or custom markets.

Disclaimer

Educational and informational only, not financial advice.

Not a complete trading system.