[e2] Drawing Library :: Horizontal Ray█ OVERVIEW

Library "e2hray"

A drawing library that contains the hray() function, which draws a horizontal ray/s with an initial point determined by a specified condition. It plots a ray until it reached the price. The function let you control the visibility of historical levels and setup the alerts.

█ HORIZONTAL RAY FUNCTION

hray(condition, level, color, extend, hist_lines, alert_message, alert_delay, style, hist_style, width, hist_width)

Parameters:

condition : Boolean condition that defines the initial point of a ray

level : Ray price level.

color : Ray color.

extend : (optional) Default value true, current ray levels extend to the right, if false - up to the current bar.

hist_lines : (optional) Default value true, shows historical ray levels that were revisited, default is dashed lines. To avoid alert problems set to 'false' before creating alerts.

alert_message : (optional) Default value string(na), if declared, enables alerts that fire when price revisits a line, using the text specified

alert_delay : (optional) Default value int(0), number of bars to validate the level. Alerts won't trigger if the ray is broken during the 'delay'.

style : (optional) Default value 'line.style_solid'. Ray line style.

hist_style : (optional) Default value 'line.style_dashed'. Historical ray line style.

width : (optional) Default value int(1), ray width in pixels.

hist_width : (optional) Default value int(1), historical ray width in pixels.

Returns: void

█ EXAMPLES

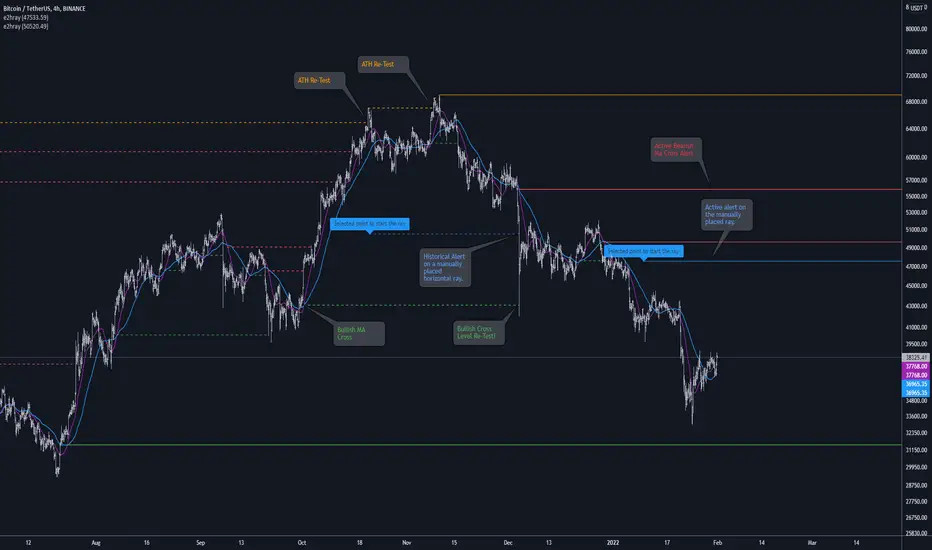

• Example 1. Single horizontal ray from the dynamic input.

//@version=5

indicator("hray() example :: Dynamic input ray", overlay = true)

import e2e4mfck/e2hray/1 as e2draw

inputTime = input.time(timestamp("20 Jul 2021 00:00 +0300"), "Date", confirm = true)

inputPrice = input.price(54, 'Price Level', confirm = true)

e2draw.hray(time == inputTime, inputPrice, color.blue, alert_message = 'Ray level re-test!')

var label mark = label.new(inputTime, inputPrice, 'Selected point to start the ray', xloc.bar_time)

• Example 2. Multiple horizontal rays on the moving averages cross.

//@version=5

indicator("hray() example :: MA Cross", overlay = true)

import e2e4mfck/e2hray/1 as e2draw

float sma1 = ta.sma(close, 20)

float sma2 = ta.sma(close, 50)

bullishCross = ta.crossover( sma1, sma2)

bearishCross = ta.crossunder(sma1, sma2)

plot(sma1, 'sma1', color.purple)

plot(sma2, 'sma2', color.blue)

// 1a. We can use 2 function calls to distinguish long and short sides.

e2draw.hray(bullishCross, sma1, color.green, alert_message = 'Bullish Cross Level Broken!', alert_delay = 10)

e2draw.hray(bearishCross, sma2, color.red, alert_message = 'Bearish Cross Level Broken!', alert_delay = 10)

// 1b. Or a single call for both.

// e2draw.hray(bullishCross or bearishCross, sma1, bullishCross ? color.green : color.red)

• Example 3. Horizontal ray at the all time highs with an alert.

//@version=5

indicator("hray() example :: ATH", overlay = true)

import e2e4mfck/e2hray/1 as e2draw

var float ath = 0, ath := math.max(high, ath)

bool newAth = ta.change(ath)

e2draw.hray(nz(newAth ), high , color.orange, alert_message = 'All Time Highs Tested!', alert_delay = 10)

Wyszukaj w skryptach "VAR+计量模型+黄金期货"

Moving Average Multitool CrossoverAs per request, this is a moving average crossover version of my original moving average multitool script .

It allows you to easily access and switch between different types of moving averages, without having to continuously add and remove different moving averages from your chart. This should make backtesting moving average crossovers much, much more easier. It also has the option to show buy and sell signals for the crossovers of the chosen moving averages.

It contains the following moving averages:

Exponential Moving Average (EMA)

Simple Moving Average (SMA)

Weighted Moving Average (WMA)

Double Exponential Moving Average (DEMA)

Triple Exponential Moving Average (TEMA)

Triangular Moving Average (TMA)

Volume-Weighted Moving Average (VWMA)

Smoothed Moving Average (SMMA)

Hull Moving Average (HMA)

Least Squares Moving Average (LSMA)

Kijun-Sen line from the Ichimoku Kinko-Hyo system (Kijun)

McGinley Dynamic (MD)

Rolling Moving Average (RMA)

Jurik Moving Average (JMA)

Arnaud Legoux Moving Average (ALMA)

Vector Autoregression Moving Average (VAR)

Welles Wilder Moving Average (WWMA)

Sine Weighted Moving Average (SWMA)

Leo Moving Average (LMA)

Variable Index Dynamic Average (VIDYA)

Fractal Adaptive Moving Average (FRAMA)

Variable Moving Average (VAR)

Geometric Mean Moving Average (GMMA)

Corrective Moving Average (CMA)

Moving Median (MM)

Quick Moving Average (QMA)

Kaufman's Adaptive Moving Average (KAMA)

Volatility-Adjusted Moving Average (VAMA)

Modular Filter (MF)

benchLibrary "bench"

A simple banchmark library to analyse script performance and bottlenecks.

Very useful if you are developing an overly complex application in Pine Script, or trying to optimise a library / function / algorithm...

Supports artificial looping benchmarks (of fast functions)

Supports integrated linear benchmarks (of expensive scripts)

One important thing to note is that the Pine Script compiler will completely ignore any calculations that do not eventually produce chart output. Therefore, if you are performing an artificial benchmark you will need to use the bench.reference(value) function to ensure the calculations are executed.

Please check the examples towards the bottom of the script.

Quick Reference

(Be warned this uses non-standard space characters to get the line indentation to work in the description!)

```

// Looping benchmark style

benchmark = bench.new(samples = 500, loops = 5000)

data = array.new_int()

if bench.start(benchmark)

while bench.loop(benchmark)

array.unshift(data, timenow)

bench.mark(benchmark)

while bench.loop(benchmark)

array.unshift(data, timenow)

bench.mark(benchmark)

while bench.loop(benchmark)

array.unshift(data, timenow)

bench.stop(benchmark)

bench.reference(array.get(data, 0))

bench.report(benchmark, '1x array.unshift()')

// Linear benchmark style

benchmark = bench.new()

data = array.new_int()

bench.start(benchmark)

for i = 0 to 1000

array.unshift(data, timenow)

bench.mark(benchmark)

for i = 0 to 1000

array.unshift(data, timenow)

bench.stop(benchmark)

bench.reference(array.get(data, 0))

bench.report(benchmark,'1000x array.unshift()')

```

Detailed Interface

new(samples, loops) Initialises a new benchmark array

Parameters:

samples : int, the number of bars in which to collect samples

loops : int, the number of loops to execute within each sample

Returns: int , the benchmark array

active(benchmark) Determing if the benchmarks state is active

Parameters:

benchmark : int , the benchmark array

Returns: bool, true only if the state is active

start(benchmark) Start recording a benchmark from this point

Parameters:

benchmark : int , the benchmark array

Returns: bool, true only if the benchmark is unfinished

loop(benchmark) Returns true until call count exceeds bench.new(loop) variable

Parameters:

benchmark : int , the benchmark array

Returns: bool, true while looping

reference(number, string) Add a compiler reference to the chart so the calculations don't get optimised away

Parameters:

number : float, a numeric value to reference

string : string, a string value to reference

mark(benchmark, number, string) Marks the end of one recorded interval and the start of the next

Parameters:

benchmark : int , the benchmark array

number : float, a numeric value to reference

string : string, a string value to reference

stop(benchmark, number, string) Stop the benchmark, ending the final interval

Parameters:

benchmark : int , the benchmark array

number : float, a numeric value to reference

string : string, a string value to reference

report(Prints, benchmark, title, text_size, position)

Parameters:

Prints : the benchmarks results to the screen

benchmark : int , the benchmark array

title : string, add a custom title to the report

text_size : string, the text size of the log console (global size vars)

position : string, the position of the log console (global position vars)

unittest_bench(case) Cache module unit tests, for inclusion in parent script test suite. Usage: bench.unittest_bench(__ASSERTS)

Parameters:

case : string , the current test case and array of previous unit tests (__ASSERTS)

unittest(verbose) Run the bench module unit tests as a stand alone. Usage: bench.unittest()

Parameters:

verbose : bool, optionally disable the full report to only display failures

logLibrary "log"

Logging library for easily displaying debug, info, warn, error and critical messages.

No real need to explain why you might want to use this library! I'm sure you've all experienced the frustration of trying to understand the data state of your scripts... so, enjoy! More on it's way...

(Don't forget to check the helpers in the script and the useful tips below)

Some Useful Tips

By default the log console persists between bars (for history) and bars and ticks (for realtime).

Sometimes it is useful to clear the log after each candle or tick (assuming we are using the above helpers):

```

log_print(clear = true) // starts afresh on every bar and tick (excludes historical bars but good realtime tick analysis)

log_print(clear = barstate.isnew) // clears the log at the start of each bar (again, excludes historical but good realtime candle analysis)

```

It is also useful to be able to selectively understand the state of data at specific points or times within a script:

```

if log.once()

debug('useful variable', my_var) // this log only gets written once, upon first execution of this statement

if log.only(5)

debug3(a, b, c) // these variables are only logged the first five times this statement is executed

log_print(clear = false) // clear must be false and you should not write other logs on every bar, or the above will be lost

```

Final tip. If you want to view ONLY log entries of a particular level, then negate the constant:

```

log_print(level = -LOG_DEBUG)

```

Detailed Interface

once() Restrict execution to only happen once. Usage: if assert.once()\n happens_once()

Returns: bool, true on first execution within scope, false subsequently

only(repeat) Restrict execution to happen a set number of times. Usage: if assert.only(5)\n happens_five_times()

Parameters:

repeat : int, the number of times to return true

Returns: bool, true for the set number of times within scope, false subsequently

init() Initialises the log array

Returns: string , tuple based array to contain all pending log entries (__LOG)

clear(msgs) Clears the log array

Parameters:

msgs : string , the current collection of unfiltered and unprocessed logs (__LOG)

trace(msgs, msg) Writes a trace message to the log console

Parameters:

msgs : string , the current collection of unfiltered and unprocessed logs (__LOG)

msg : string, the trace message to write to the log

debug(msgs, msg) Writes a debug message to the log console

Parameters:

msgs : string , the current collection of unfiltered and unprocessed logs (__LOG)

msg : string, the debug message to write to the log

info(msgs, msg) Writes an info message to the log console

Parameters:

msgs : string , the current collection of unfiltered and unprocessed logs (__LOG)

msg : string, the info message to write to the log

warn(msgs, msg) Writes a warning message to the log console

Parameters:

msgs : string , the current collection of unfiltered and unprocessed logs (__LOG)

msg : string, the warn message to write to the log

error(msgs, msg) Writes an error message to the log console

Parameters:

msgs : string , the current collection of unfiltered and unprocessed logs (__LOG)

msg : string, the error message to write to the log

fatal(msgs, msg) Writes a critical message to the log console

Parameters:

msgs : string , the current collection of unfiltered and unprocessed logs (__LOG)

msg : string, the fatal message to write to the log

log(msgs, level, msg) Write a log message to the log console with a custom level

Parameters:

msgs : string , the current collection of unfiltered and unprocessed logs (__LOG)

level : ing, the logging level to assign to the message

msg : string, the log message to write to the log

severity(msgs) Checks the unprocessed log messages and returns the highest present level

Parameters:

msgs : string , the current collection of unfiltered and unprocessed logs (__LOG)

Returns: int, the highest level found within the unfiltered logs

print(msgs, level, clear, rows, text_size, position) Prints all log messages to the screen

Parameters:

msgs : string , the current collection of unfiltered and unprocessed logs (__LOG)

level : int, the minimum required log level of each message to be displayed

clear : bool, clear the printed log console after each render (useful with realtime when set to barstate.isconfirmed)

rows : int, the number of rows to display in the log console

text_size : string, the text size of the log console (global size vars)

position : string, the position of the log console (global position vars)

unittest_log(case) Log module unit tests, for inclusion in parent script test suite. Usage: log.unittest_log(__ASSERTS)

Parameters:

case : string , the current test case and array of previous unit tests (__ASSERTS)

unittest(verbose) Run the log module unit tests as a stand alone. Usage: log.unittest()

Parameters:

verbose : bool, optionally disable the full report to only display failures

CreateAndShowZigzagLibrary "CreateAndShowZigzag"

Functions in this library creates/updates zigzag array and shows the zigzag

getZigzag(zigzag, prd, max_array_size) calculates zigzag using period

Parameters:

zigzag : is the float array for the zigzag (should be defined like "var zigzag = array.new_float(0)"). each zigzag points contains 2 element: 1. price level of the zz point 2. bar_index of the zz point

prd : is the length to calculate zigzag waves by highest(prd)/lowest(prd)

max_array_size : is the maximum number of elements in zigzag, keep in mind each zigzag point contains 2 elements, so for example if it's 10 then zigzag has 10/2 => 5 zigzag points

Returns: dir that is the current direction of the zigzag

showZigzag(zigzag, oldzigzag, dir, upcol, dncol) this function shows zigzag

Parameters:

zigzag : is the float array for the zigzag (should be defined like "var zigzag = array.new_float(0)"). each zigzag points contains 2 element: 1. price level of the zz point 2. bar_index of the zz point

oldzigzag : is the float array for the zigzag, you get copy the zigzag array to oldzigzag by "oldzigzag = array.copy(zigzay)" before calling get_zigzag() function

dir : is the direction of the zigzag wave

upcol : is the color of the line if zigzag direction is up

dncol : is the color of the line if zigzag direction is down

Returns: null

Profit Maximizer StrategyFirst I would like to thank to @KivancOzbilgic for developing this indicator.

All the credit goes to him.

I just created a strategy, in order to try to find the perfect parameters, timeframe and currency for it.

I will provide below the same description like he has in the publish of profit maximizer

Profit Maximizer - PMax combines the powerful sides of MOST (Moving Average Trend Changer) and SuperTrend (ATR price detection) in one indicator.

Backtest and optimization results of PMax are far better when compared to its ancestors MOST and SuperTrend. It reduces the number of false signals in sideways and give more reliable trade signals.

PMax is easy to determine the trend and can be used in any type of markets and instruments. It does not repaint.

The first parameter in the PMax indicator set by the three parameters is the period/length of ATR.

The second Parameter is the Multiplier of ATR which would be useful to set the value of distance from the built in Moving Average.

I personally think the most important parameter is the Moving Average Length and type.

PMax will be much sensitive to trend movements if Moving Average Length is smaller. And vice versa, will be less sensitive when it is longer.

As the period increases it will become less sensitive to little trends and price actions.

In this way, your choice of period, will be closely related to which of the sort of trends you are interested in.

We are under the effect of the uptrend in cases where the Moving Average is above PMax;

conversely under the influence of a downward trend, when the Moving Average is below PMax.

Built in Moving Average type defaultly set as EMA but users can choose from 8 different Moving Average types like:

SMA : Simple Moving Average

EMA : Exponential Movin Average

WMA : Weighted Moving Average

TMA : Triangular Moving Average

VAR : Variable Index Dynamic Moving Average aka VIDYA

WWMA : Welles Wilder's Moving Average

ZLEMA : Zero Lag Exponential Moving Average

TSF : True Strength Force

Tip: In sideways VAR would be a good choice

You can use PMax default alarms and Buy Sell signals like:

1-

BUY when Moving Average crosses above PMax

SELL when Moving Average crosses under PMax

2-

BUY when prices jumps over PMax line.

SELL when prices go under PMax line.

PMax Explorer STRATEGY & SCREENERProfit Maximizer - PMax Explorer STRATEGY & SCREENER screens the BUY and SELL signals (trend reversals) for 20 user defined different tickers in Tradingview charts.

Simply input the name of the ticker in Tradingview that you want to screen.

Terminology explanation:

Confirmed Reversal: PMax reversal that happened in the last bar and cannot be repainted.

Potential Reversal: PMax reversal that might happen in the current bar but can also not happen depending upon the timeframe closing price.

Downtrend: Tickers that are currently in the sell zone

Uptrend: Tickers that are currently in the buy zone

Screener has also got a built in PMax indicator which users can confirm the reversals on graphs.

Screener explores the 20 tickers in current graph's time frame and also in desired parameters of the SuperTrend indicator.

Also you can optimize the parameters manually with the built in STRATEGY version.

PMax indicator :

Profit Maximizer - PMax is a brand new indicator developed by me.

It's a combination of two trailing stop loss indicators;

One is Anıl Özekşi's MOST (Moving Stop Loss) Indicator

and the other one is well known ATR based SuperTrend

Profit Maximizer - PMax tries to solve this problem. PMax combines the powerful sides of MOST (Moving Average Trend Changer) and SuperTrend (ATR price detection) in one indicator.

Backtest and optimization results of PMax are far better when compared to its ancestors MOST and SuperTrend. It reduces the number of false signals in sideways and give more reliable trade signals.

PMax is easy to determine the trend and can be used in any type of markets and instruments. It does not repaint.

The first parameter in the PMax indicator set by the three parameters is the period/length of ATR.

The second Parameter is the Multiplier of ATR which would be useful to set the value of distance from the built in Moving Average.

I personally think the most important parameter is the Moving Average Length and type.

PMax will be much sensitive to trend movements if Moving Average Length is smaller. And vice versa, will be less sensitive when it is longer.

As the period increases it will become less sensitive to little trends and price actions.

In this way, your choice of period, will be closely related to which of the sort of trends you are interested in.

We are under the effect of the uptrend in cases where the Moving Average is above PMax;

conversely under the influence of a downward trend, when the Moving Average is below PMax.

Built in Moving Average type defaultly set as EMA but users can choose from 8 different Moving Average types like:

SMA : Simple Moving Average

EMA : Exponential Movin Average

WMA : Weighted Moving Average

TMA : Triangular Moving Average

VAR : Variable Index Dynamic Moving Average aka VIDYA

WWMA : Welles Wilder's Moving Average

ZLEMA : Zero Lag Exponential Moving Average

TSF : True Strength Force

Tip: In sideways VAR would be a good choice

You can use PMax default alarms and Buy Sell signals like:

1-

BUY when Moving Average crosses above PMax

SELL when Moving Average crosses under PMax

2-

BUY when prices jumps over PMax line.

SELL when prices go under PMax line.

Profit Maximizer PMaxPMax is a brand new indicator developed by KivancOzbilgic in earlier 2020.

It's a combination of two trailing stop loss indicators;

One is Anıl Özekşi's MOST (Moving Stop Loss) Indicator

and the other one is well known ATR based SuperTrend.

Both MOST and SuperTrend Indicators are very good at trend following systems but conversely their performance is not bright in sideways market conditions like most of the other indicators.

Profit Maximizer - PMax tries to solve this problem. PMax combines the powerful sides of MOST (Moving Average Trend Changer) and SuperTrend (ATR price detection) in one indicator.

Backtest and optimization results of PMax are far better when compared to its ancestors MOST and SuperTrend. It reduces the number of false signals in sideways and give more reliable trade signals.

PMax is easy to determine the trend and can be used in any type of markets and instruments. It does not repaint.

The first parameter in the PMax indicator set by the three parameters is the period/length of ATR.

The second Parameter is the Multiplier of ATR which would be useful to set the value of distance from the built in Moving Average.

I personally think the most important parameter is the Moving Average Length and type.

PMax will be much sensitive to trend movements if Moving Average Length is smaller. And vice versa, will be less sensitive when it is longer.

As the period increases it will become less sensitive to little trends and price actions.

In this way, your choice of period, will be closely related to which of the sort of trends you are interested in.

We are under the effect of the uptrend in cases where the Moving Average is above PMax;

conversely under the influence of a downward trend, when the Moving Average is below PMax.

Built in Moving Average type defaultly set as EMA but users can choose from 8 different Moving Average types like:

SMA : Simple Moving Average

EMA : Exponential Movin Average

WMA : Weighted Moving Average

TMA : Triangular Moving Average

VAR : Variable Index Dynamic Moving Average aka VIDYA

WWMA : Welles Wilder's Moving Average

ZLEMA : Zero Lag Exponential Moving Average

TSF : True Strength Force

Tip: In sideways VAR would be a good choice

You can use PMax default alarms and Buy Sell signals like:

1-

BUY when Moving Average crosses above PMax

SELL when Moving Average crosses under PMax

2-

BUY when prices jumps over PMax line.

SELL when prices go under PMax line.

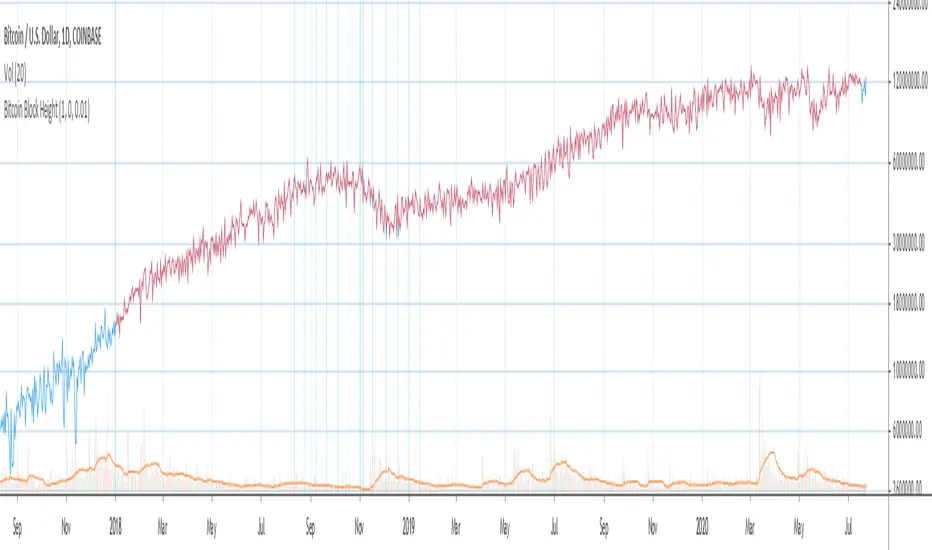

Bitcoin Block Height (Total Blocks)Bitcoin Block Height by RagingRocketBull 2020

Version 1.0

Differences between versions are listed below:

ver 1.0: compare QUANDL Difficulty vs Blockchain Difficulty sources, get total error estimate

ver 2.0: compare QUANDL Hash Rate vs Blockchain Hash Rate sources, get total error estimate

ver 3.0: Total Blocks estimate using different methods

--------------------------------

This indicator estimates Bitcoin Block Height (Total Blocks) using Difficulty and Hash Rate in the most accurate way possible, since

QUANDL doesn't provide a direct source for Bitcoin Block Height (neither QUANDL:BCHAIN, nor QUANDL:BITCOINWATCH/MINING).

Bitcoin Block Height can be used in other calculations, for instance, to estimate the next date of Bitcoin Halving.

Using this indicator I demonstrate:

- that QUANDL data is not accurate and differ from Blockchain source data (industry standard), but still can be used in calculations

- how to plot a series of data points from an external csv source and compare it with another source

- how to accurately estimate Bitcoin Block Height

Features:

- compare QUANDL Difficulty source (EOD, D1) with external Blockchain Difficulty csv source (EOD, D1, embedded)

- show/hide Quandl/Blockchain Difficulty curves

- show/hide Blockchain Difficulty candles

- show/hide differences (aqua vertical lines)

- show/hide time gaps (green vertical lines)

- count source differences within data range only or for the whole history

- multiply both sources by alpha to match before comparing

- floor/round both matched sources when comparing

- Blockchain Difficulty offset to align sequences, bars > 0

- count time gaps and missing bars (as result of time gaps)

WARNING:

- This indicator hits the max 1000 vars limit, adding more plots/vars/data points is not possible

- Both QUANDL/Blockchain provide daily EOD data and must be plotted on a daily D1 chart otherwise results will be incorrect

- current chart must not have any time gaps inside the range (time gaps outside the range don't affect the calculation). Time gaps check is provided.

Otherwise hardcoded Blockchain series will be shifted forward on gaps and the whole sequence become truncated at the end => data comparison/total blocks estimate will be incorrect

Examples of valid charts that can run this indicator: COINBASE:BTCUSD,D1 (has 8 time gaps, 34 missing bars outside the range), QUANDL:BCHAIN/DIFF,D1 (has no gaps)

Usage:

- Description of output plot values from left to right:

- c_shifted - 4x blockchain plotcandles ohlc, green/black (default na)

- diff - QUANDL Difficulty

- c_shifted - Blockchain Difficulty with offset

- QUANDL Difficulty multiplied by alpha and rounded

- Blockchain Difficulty multiplied by alpha and rounded

- is_different, bool - cur bar's source values are different (1) or not (0)

- count, number of differences

- bars, total number of bars/data points in the range

- QUANDL daily blocks

- Blockchain daily blocks

- QUANDL total blocks

- Blockchain total blocks

- total_error - difference between total_blocks estimated using both sources as of cur bar, blocks

- number_of_gaps - number of time gaps on a chart

- missing_bars - number of missing bars as result of time gaps on a chart

- Color coding:

- Blue - QUANDL data

- Red - Blockchain data

- Black - Is Different

- Aqua - number of differences

- Green - number of time gaps

- by default the indicator will show lots of vertical aqua lines, 138 differences, 928 bars, total error -370 blocks

- to compare the best match of the 2 sources shift Blockchain source 1 bar into the future by setting Blockchain Difficulty offset = 1, leave alpha = 0.01 =>

this results in no vertical aqua lines, 0 differences, total_error = 0 blocks

if you move the mouse inside the range some bars will show total_error = 1 blocks => total_error <= 1 blocks

- now uncheck Round Difficulty Values flag => some filled aqua areas, 218 differences.

- now set alpha = 1 (use raw source values) instead of 0.01 => lots of filled aqua areas, 871 differences.

although there are many differences this still doesn't affect the total_blocks estimate provided Difficulty offset = 1

Methodology:

To estimate Bitcoin Block Height we need 3 steps, each step has its own version:

- Step 1: Compare QUANDL Difficulty vs Blockchain Difficulty sources and estimate error based on differences

- Step 2: Compare QUANDL Hash Rate vs Blockchain Hash Rate sources and estimate error based on differences

- Step 3: Estimate Bitcoin Block Height (Total Blocks) using different methods in the most accurate way possible

QUANDL doesn't provide block time data, but we can calculate it using the Hash Rate approximation formula:

estimated Hash rate/sec H = 2^32 * D / T, where D - Difficulty, T - block time, sec

1. block time (T) can be derived from the formula, since we already know Difficulty (D) and Hash Rate (H) from QUANDL

2. using block time (T) we can estimate daily blocks as daily time / block time

3. block height (total blocks) = cumulative sum of daily blocks of all bars on the chart (that's why having no gaps is important)

Notes:

- This code uses Pinescript v3 compatibility framework

- hash rate is in THash/s, although QUANDL falsely states in description GHash/s! THash = 1000 GHash

- you can't read files, can only embed/hardcode raw data in script

- both QUANDL and Blockchain sources have no gaps

- QUANDL and Blockchain series are different in the following ways:

- all QUANDL data is already shifted 1 bar into the future, i.e. prev day's value is shown as cur day's value => Blockchain data must be shifted 1 bar forward to match

- all QUANDL diff data > 1 bn (10^12) are truncated and have last 1-2 digits as zeros, unlike Blockchain data => must multiply both values by 0.01 and floor/round the results

- QUANDL sometimes rounds, other times truncates those 1-2 last zero digits to get the 3rd last digit => must use both floor/round

- you can only shift sequences forward into the future (right), not back into the past (left) using positive offset => only Blockchain source can be shifted

- since total_blocks is already a cumulative sum of all prev values on each bar, total_error must be simple delta, can't be also int(cum()) or incremental

- all Blockchain values and total_error are na outside the range - move you mouse cursor on the last bar/inside the range to see them

TLDR, ver 1.0 Conclusion:

QUANDL/Blockchain Difficulty source differences don't affect total blocks estimate, total error <= 1 block with avg 150 blocks/day is negligible

Both QUANDL/Blockchain Difficulty sources are equally valid and can be used in calculations. QUANDL is a relatively good stand in for Blockchain industry standard data.

Links:

QUANDL difficulty source: www.quandl.com

QUANDL hash rate source: www.quandl.com

Blockchain difficulty source (export data as csv): www.blockchain.com

Support and Resistance levels from Options DataINTRODUCTION

This script is designed to visualize key support and resistance levels derived from options data on TradingView charts. It overlays lines, labels, and boxes to highlight levels such as Put Walls (gamma support), Call Walls (gamma resistance), Gamma Flip points, Vanna levels, and more.

These levels are intended to help traders identify potential areas of price magnetism, reversal, or breakout based on options market dynamics. All calculations and visualizations are based on user-provided data pasted into the input field, as Pine Script cannot directly fetch external options data due to platform limitations (explained below).

For convenience, my website allows users to interact with a bot that will generate the string for up to 30 tickers at once getting nearly real-time data on demand (data is cached for 15min). With the output string pasted into this indicator, it's a bliss to shuffle through your portfolio and see those levels for each ticker.

The script is open-source under TradingView's terms, allowing users to study, modify, and improve it. It draws inspiration from common options-derived metrics like gamma exposure and vanna, which are widely discussed in financial literature. No external code is copied without rights; all logic is original or based on standard mathematical formulas.

How the Options Levels Are Calculated

The levels displayed by this script are not computed within Pine Script itself—instead, they rely on pre-calculated values provided by the user (via a pasted data string). These values are derived from options chain data fetched from financial APIs (e.g., using libraries like yfinance in Python). Here's a step-by-step overview of how these levels are generally calculated externally before being input into the script:

Fetching Options Data:

Historical and current options chain data for a ticker (e.g., strikes, open interest, volume, implied volatility, expirations) is retrieved for near-term expirations (e.g., up to 90 days).

Current stock price is obtained from recent history.

Gamma Support (Put Wall) and Resistance (Call Wall):

Gamma Calculation: For each option, gamma (the rate of change of delta) is computed using the Black-Scholes formula:

gamma = N'(d1) / (S * sigma * sqrt(T))

where S is the stock price, K is the strike, T is time to expiration (in years), sigma is implied volatility, r is the risk-free rate (e.g., 0.0445), and N'(d1) is the normal probability density function.

Weighted gamma is multiplied by open interest and aggregated by strike.

The Put Wall is the strike below the current price with the highest weighted gamma from puts (acting as support).

The Call Wall is the strike above the current price with the highest weighted gamma from calls (acting as resistance).

Short-term versions focus on strikes closer to the money (e.g., within 10-15% of the price).

Gamma Flip Level:

Net dealer gamma exposure (GEX) is calculated across all strikes:

GEX = sum (gamma * OI * 100 * S^2 * sign * decay)

where sign is +1 for calls/-1 for puts, and decay is 1 / sqrt(T).

The flip point is the price where net GEX changes sign (from positive to negative or vice versa), interpolated between strikes.

Vanna Levels:

Vanna (sensitivity of delta to volatility) is calculated:

vanna = -N'(d1) * d2 / sigma

where d2 = d1 - sigma * sqrt(T).

Weighted by open interest, the highest positive and negative vanna strikes are identified.

Other Levels:

S1/R1: Significant strikes with high combined open interest and volume (80% OI + 20% volume), below/above price for support/resistance.

Implied Move: ATM implied volatility scaled by S * sigma * sqrt(d/365) (e.g., for 7 days).

Call/Put Ratio: Total call contracts divided by put contracts (OI + volume).

IV Percentage: Average ATM implied volatility.

Options Activity Level: Average contracts per unique strike, binned into levels (0-4).

Stop Loss: Dynamically set below the lowest support (e.g., Put Wall, Gamma Flip), adjusted by IV (tighter in low IV).

Fib Target: 1.618 extension from Put Wall to Call Wall range.

Previous day levels are stored for comparison (e.g., to detect Call Wall movement >2.5% for alerts).

Effect as Support and Resistance in Technical Trading

Options levels like gamma walls influence price action due to market maker hedging:

Put Wall (Gamma Support): High put gamma below price creates a "magnet" effect—market makers buy stock as price falls, providing support. Traders might look for bounces here as entry points for longs.

Call Wall (Gamma Resistance): High call gamma above price leads to selling pressure from hedging, acting as resistance. Rejections here could signal trims, sells or even shorts.

Gamma Flip: Where gamma exposure flips sign, often a volatility pivot—crossing it can accelerate moves (bullish above, bearish below).

Vanna Levels: Positive/negative vanna indicate volatility sensitivity; crosses may signal regime shifts.

Implied Move: Shows expected range; prices outside suggest overextension.

S1/R1 and Fib Target: Volume/OI clusters act as classic S/R; Fib extensions project upside targets post-breakout.

In trading, these are not guarantees—combine with TA (e.g., volume, trends). High activity levels imply stronger effects; low CP ratio suggests bearish sentiment. Alerts trigger on proximities/crosses for awareness, not advice.

Limitations of the TradingView Platform for Data Pulling

TradingView's Pine Script is sandboxed for security and performance:

No direct internet access or API calls (e.g., can't fetch yfinance data in-script).

Limited to chart data/symbol info; no real-time options chains.

Inputs are static per load; updates require manual pasting.

Caching isn't persistent across sessions.

This prevents dynamic data pulling, ensuring scripts remain lightweight but requiring external tools for fresh data.

Creative Solution for On-Demand Data Pulling

To overcome these limitations, users can use external tools or scripts (e.g., Python-based) to fetch and compute levels on demand. The tool processes tickers, generates a formatted string (e.g., "TICKER:level1,level2,...;TIMESTAMP:unix;"), and users paste it into the script's input. This keeps data fresh without violating platform rules, as computation happens off-platform. For example, run a local script to query APIs and output the string—adaptable for any ticker.

Script Functionality Breakdown

Inputs: Custom data string (parsed for levels/timestamp); toggles for short-term/previous/Vanna/stop loss; style options (colors, transparency).

Parsing: Extracts levels for the chart symbol; gets timestamp for "updated ago" display.

Drawing: Lines/labels for levels; boxes for gamma zones/implied move; clears old elements on updates.

Info Panel: Top-right summary with metrics (CP ratio, IV, distances, activity); emojis for quick status.

Alerts: Conditions for proximities, crosses, bounces (e.g., 0.5% bounce from Put Wall).

Performance: Uses vars for persistence; efficient for real-time.

This script is educational—test thoroughly. Not financial advice; past performance isn't indicative of future results. Feedback welcome via TradingView comments.

BTC/USD 3分バイナリー予測【完全修正版v7.2】## BTC/USD 3-Minute Binary Prediction Indicator v7.2 Documentation

### Overview

This indicator predicts whether BTCUSD price will move ±$25 or more within 3 minutes using a 5-layer filter system and pattern recognition. Designed for 30-second timeframe analysis with statistical tracking.

### ⚠️ Critical Warnings

- **This is a prediction tool, NOT a profit guarantee**

- **30-second timeframe ONLY** (Will not function correctly on other timeframes)

- **BTCUSD pair ONLY**

- **Past performance does not guarantee future results**

- **Test thoroughly in demo before live trading**

- **You can lose your entire investment**

### Core Components

#### 1. Five-Layer Filter System

```

Layer 1: Trend Alignment (25 points) - EMA configuration analysis

Layer 2: Indicator Confluence (25 points) - RSI + MACD confirmation

Layer 3: Volume Analysis (20 points) - Abnormal volume detection

Layer 4: Key Levels (15 points) - Support/Resistance proximity

Layer 5: Momentum (15 points) - Price acceleration measurement

```

#### 2. Pattern Recognition Engine

- Double Top/Bottom formations

- Triangle patterns (Symmetrical, Ascending, Descending)

- Channel patterns

- Candlestick patterns (Engulfing, Hammer, Hanging Man)

#### 3. Performance Tracking

- Overall win rate

- Hourly performance

- Daily performance

- Real-time statistics

### Input Parameters

#### Basic Settings

- `Range Width ($)`: Target price movement (Default: $50 = ±$25)

- `Minimum Confidence (%)`: Required confidence for entry (Default: 75%)

- `Max Daily Trades`: Overtrading prevention (Default: 5)

#### Filter Settings

- `Trend Filter`: EMA alignment validation

- `Volume Confirmation`: Volume spike detection

- `S/R Filter`: Key level analysis

- `Momentum Alignment`: Directional strength confirmation

#### Display Settings

- `Minimal Mode`: Reduced visual elements for experienced users

- `Pattern Display`: Visual pattern overlays

- `EMA Lines`: Moving average visualization

### Usage Instructions

#### Setup Process

1. Open BTCUSD chart on TradingView

2. **Set timeframe to 30 seconds** (CRITICAL)

3. Add indicator to chart

4. Adjust parameters if needed

#### Reading Signals

**Decision Panel (Left Side)**

- `HIGH`: Predicts +$25 move in 3 minutes

- `LOW`: Predicts -$25 move in 3 minutes

- `WAIT`: Conditions building, no entry yet

- `STAY`: No trade opportunity

**F-Score Interpretation**

- 65+ points: Direction suggestion (light color)

- 80+ points: Strong signal (solid color)

- Entry ready: Exclamation mark (!)

**Statistics Panel (Right Side)**

- Win rate: Percentage of successful predictions

- 1H Stats: Last hour performance

- Daily Stats: Today's results

#### Entry Execution

1. Wait for `HIGH!` or `LOW!` in decision panel

2. Large arrow appears on chart (▲ for HIGH, ▼ for LOW)

3. Enter at **next candle open**

4. Result evaluated after 3 minutes (6 candles)

### Algorithm Logic

#### Early Entry System (v7.2 Feature)

The indicator uses predictive analysis starting at F-Score 65 instead of waiting for 80:

- Faster signal generation

- Reduced opportunity loss

- Slightly lower win rate trade-off

#### Confidence Calculation

```

Base confidence: 50%

+ Filter score bonus

+ Pattern recognition bonus

+ Volatility adjustment

- Risk factors

= Final confidence (50-95%)

```

### Technical Specifications

#### Multi-Timeframe Analysis

- Primary: 30-second chart

- Secondary: 1-minute data

- Reference: 5-minute trend

#### Data Processing

- Real-time tick analysis

- No repainting (signals are final)

- Historical verification system

### Limitations & Known Issues

1. **Spread/Commission Not Included**: Actual profits will be lower

2. **30-Second Noise**: High false signal risk on ultra-short timeframe

3. **Network Latency**: Execution delays not accounted for

4. **Market Conditions**: Performance varies with volatility

5. **Algorithm Trading**: Cannot compete with HFT systems

### Performance Metrics

- Target Win Rate: 83% (aspirational)

- Evaluation Period: 3 minutes

- Risk per trade: Fixed ±$25

- Maximum daily exposure: 5 trades

### Troubleshooting Guide

**No signals appearing?**

- Check F-Score (needs 65+)

- Verify 30-second timeframe

- Ensure BTCUSD pair selected

**Low win rate?**

- Only trade 75%+ confidence signals

- Respect daily trade limit

- Avoid news events

**Pattern shows "-"?**

- Normal when no clear pattern exists

- Not all market conditions produce patterns

### Code Modification Notes

Written in Pine Script v6. Key considerations for modifications:

- Global variables use `var` for persistence

- Drawing objects require manual management

- Bar counting varies by timeframe

- Pattern detection runs on confirmed bars only

### Risk Disclosure

**IMPORTANT**: Trading cryptocurrencies involves substantial risk of loss and is not suitable for all investors. The high degree of leverage can work against you as well as for you. Before deciding to trade, you should carefully consider your investment objectives, level of experience, and risk appetite. The possibility exists that you could sustain a loss of some or all of your initial investment and therefore you should not invest money that you cannot afford to lose.

### Support & Updates

- Report issues in TradingView comments

- Check for updates regularly

- Version 7.2 is current release

- Community feedback welcome

### Legal Notice

This indicator is provided for educational and research purposes only. It should not be construed as investment advice. The authors and distributors of this indicator accept no liability for losses incurred through its use. Always consult with a qualified financial advisor before making investment decisions.

---

*Version: 7.2*

*License: Mozilla Public License 2.0*

*Author: *

*Last Updated: 2024*

**FINAL WARNING: This indicator cannot predict the future. Use at your own risk. Start with demo trading. Never trade with money you cannot afford to lose.**

Pivot Points. High & Lows By Reversal PercentageLibrary "Pivot Points. High & Lows By Reversal Percentage" by Jal9000

This Pine Script library provides a robust function for identifying and tracking pivot points (reversal points) in price data, suitable for integration into custom trading indicators and strategies.

🛠️ Main Features:

- ✅ Identifies pivot highs and lows based on configurable price movement thresholds.

- ✅ Lightweight. No candle backtracing used. Much less computation heavy.

- ✅ Supports multiple calls (with different values) within a single script.

- ✅ Compatible with request.security for multi-timeframe analysis.

- ✅ Returns both confirmed and temporary pivots for flexible integration.

- ✅ Pinescript V5 and V6 compliant code.

Purpose:

The pivots library enables Pine Script developers to easily add pivot point detection to their scripts. It identifies significant price reversals by evaluating price movements against a minimum range threshold ( min_range_pct ) and confirming reversals based on a percentage ( reversal_pct ) of the prior trend’s magnitude. The library supports multiple simultaneous calls with different settings, making it ideal for multi-timeframe strategies.

How It Works:

The library’s f_calculatePivot function tracks price movements to detect pivot points:

Minimum Range Threshold : A potential pivot is considered if the price moves beyond the min_range_pct percentage of the current high (for a high pivot) or low (for a low pivot), ensuring sufficient movement.

Reversal Confirmation : A pivot is confirmed if the price reverses from the potential pivot by at least the reversal_pct percentage of the distance between the last confirmed pivot and the current potential pivot, measuring the retracement relative to the prior trend’s magnitude.

The function alternates between tracking highs (in an uptrend) and lows (in a downtrend), updating the trend when a pivot is confirmed.

State management uses an array of pivot_state objects, allowing independent calculations for different timeframes and min_range_pct values within the same script.

## Technical Reference

Functions:

f_calculatePivot(series float _high, series float _low, float _min_range_pct, float _reversal_pct) →

- Parameters:

_high : The high price series (e.g., high or math.max(open, close) ).

_low : The low price series (e.g., low or math.min(open, close) ).

_min_range_pct : The minimum percentage price movement to consider a potential pivot.

_reversal_pct : The percentage of the prior trend’s distance required to confirm a pivot.

- Returns:

A tuple containing:

isNewPivot : Boolean indicating if a new pivot was confirmed.

last_confirmed_pivot : The most recent confirmed pivot (type pivot ).

temp_pivot : The current temporary pivot (type pivot ).

Pivot type:

idx (series int) : Bar index of the pivot.

typ (series int) : Type of pivot ( PIVOT_HIGH or PIVOT_LOW ).

prc (series float) : Price of the pivot.

tme (series int) : Timestamp of the pivot.

Constants (internal):

TREND_LONG , TREND_SHORT : Trend direction indicators (1, -1).

PIVOT_HIGH , PIVOT_LOW : Pivot type indicators (1, -1).

✨ Example of Use:

//@version=5

indicator("Pivot Example", overlay=true)

import jal9000/pivots/1 as pivots

// Inputs

min_range_pct = input.float(20.0, 'Min Range %')

reversal_pct = input.float(30.0, 'Reversal %')

ignore_wick = input.bool(true, 'Ignore wick')

h = ignore_wick ? math.max(open, close) : high

l = ignore_wick ? math.min(open, close) : low

// Call the function with high, low, and input parameters

= pivots.f_calculatePivot(h, l, min_range_pct, reversal_pct)

// Variable to store previous confirmed pivot outside the function

var pivots.pivot prev_confirmed_pivot = na

// Draw the line if a new pivot is confirmed and previous pivot exists

if is_new_pivot

if not na(prev_confirmed_pivot) and not na(new_confirmed_pivot)

line.new(x1 = prev_confirmed_pivot.idx, y1 = prev_confirmed_pivot.prc, x2 = new_confirmed_pivot.idx, y2 = new_confirmed_pivot.prc, color = color.blue, width = 1)

prev_confirmed_pivot := new_confirmed_pivot

## Release Notes

v1

- Initial release of the pivots library with f_calculatePivot function for detecting pivot points and supporting multiple configurations and timeframes.

v2

- Code is Pinescript V6 ready. Remains identified as V5, but changing the version number is the only thing that is required to be v6.

Trapped Traders [ScorsoneEnterprises]This indicator identifies and visualizes trapped traders - market participants caught on the wrong side of price movements with significant volume imbalances. By analyzing volume delta at specific price levels, it reveals where traders are likely experiencing unrealized losses and may be forced to exit their positions.

The point of this tool is to identify where the liquidity in a trend may be.

var lowerTimeframe = switch

useCustomTimeframeInput => lowerTimeframeInput

timeframe.isseconds => "1S"

timeframe.isintraday => "1"

timeframe.isdaily => "5"

=> "60"

= ta.requestVolumeDelta(lowerTimeframe)

price_quantity = map.new()

is_red_candle = close < open

is_green_candle = close > open

for i=0 to lkb-1 by 1

current_vol = price_quantity.get(close)

new_vol = na(current_vol) ? lastVolume : current_vol + lastVolume

price_quantity.put(close, new_vol)

if is_green_candle and new_vol < 0

price_quantity.put(close, new_vol)

else if is_red_candle and new_vol > 0

price_quantity.put(close, new_vol)

We see in this snippet, the lastVolume variable is the most recent volume delta we can receive from the lower timeframe, we keep updating the price level we're keeping track of with that lastVolume from the lower timeframe.

This is the bulk of the concept as this level and size gives us the idea of how many traders were on the wrong side of the trend, and acting as liquidity for the profitable entries. The more, the stronger.

There are 3 ways to visualize this. A basic label, that will display the size and if positive or negative next to the bar, a gradient line that goes 10 bars to the future to be used as a support or resistance line that includes the quantity, and a bubble chart with the quantity. The larger the quantity, the bigger the bubble.

We see in this example on NYMEX:CL1! that there are lines plotted throughout this price action that price interacts with in meaningful way. There are consistently many levels for us.

Here on CME_MINI:ES1! we see the labels on the chart, and the size set to large. It is the same concept just another way to view it.

This chart of CME_MINI:RTY1! shows the bubble chart visualization. It is a way to view it that is pretty non invasive on the chart.

Every timeframe is supported including daily, weekly, and monthly.

The included settings are the display style, like mentioned above. If the user would like to see the volume numbers on the chart. The text size along with the transparency percentage. Following that is the settings for which lower timeframe to calculate the volume delta on. Finally, if you would like to see your inputs in the status line.

No indicator is 100% accurate, use "Trapped Traders" along with your own discretion.

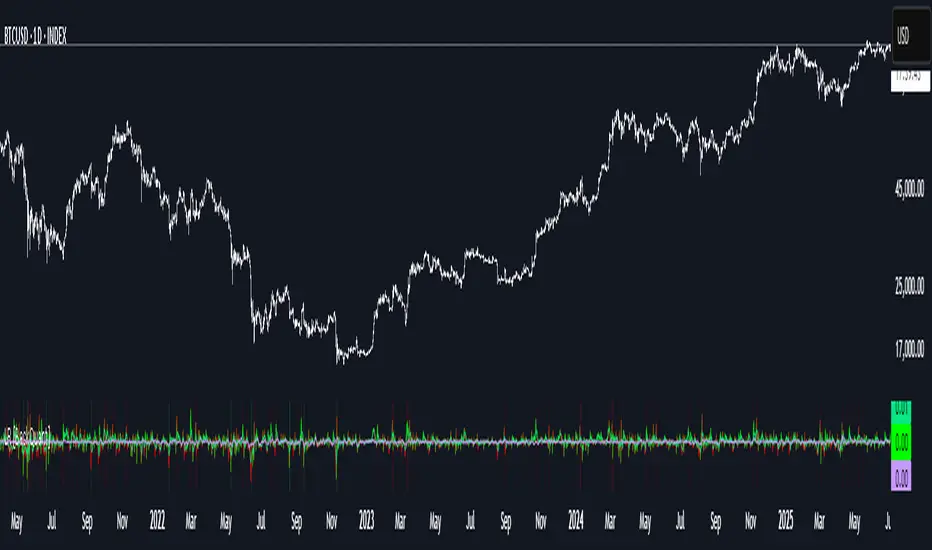

Markov Chain [3D] | FractalystWhat exactly is a Markov Chain?

This indicator uses a Markov Chain model to analyze, quantify, and visualize the transitions between market regimes (Bull, Bear, Neutral) on your chart. It dynamically detects these regimes in real-time, calculates transition probabilities, and displays them as animated 3D spheres and arrows, giving traders intuitive insight into current and future market conditions.

How does a Markov Chain work, and how should I read this spheres-and-arrows diagram?

Think of three weather modes: Sunny, Rainy, Cloudy.

Each sphere is one mode. The loop on a sphere means “stay the same next step” (e.g., Sunny again tomorrow).

The arrows leaving a sphere show where things usually go next if they change (e.g., Sunny moving to Cloudy).

Some paths matter more than others. A more prominent loop means the current mode tends to persist. A more prominent outgoing arrow means a change to that destination is the usual next step.

Direction isn’t symmetric: moving Sunny→Cloudy can behave differently than Cloudy→Sunny.

Now relabel the spheres to markets: Bull, Bear, Neutral.

Spheres: market regimes (uptrend, downtrend, range).

Self‑loop: tendency for the current regime to continue on the next bar.

Arrows: the most common next regime if a switch happens.

How to read: Start at the sphere that matches current bar state. If the loop stands out, expect continuation. If one outgoing path stands out, that switch is the typical next step. Opposite directions can differ (Bear→Neutral doesn’t have to match Neutral→Bear).

What states and transitions are shown?

The three market states visualized are:

Bullish (Bull): Upward or strong-market regime.

Bearish (Bear): Downward or weak-market regime.

Neutral: Sideways or range-bound regime.

Bidirectional animated arrows and probability labels show how likely the market is to move from one regime to another (e.g., Bull → Bear or Neutral → Bull).

How does the regime detection system work?

You can use either built-in price returns (based on adaptive Z-score normalization) or supply three custom indicators (such as volume, oscillators, etc.).

Values are statistically normalized (Z-scored) over a configurable lookback period.

The normalized outputs are classified into Bull, Bear, or Neutral zones.

If using three indicators, their regime signals are averaged and smoothed for robustness.

How are transition probabilities calculated?

On every confirmed bar, the algorithm tracks the sequence of detected market states, then builds a rolling window of transitions.

The code maintains a transition count matrix for all regime pairs (e.g., Bull → Bear).

Transition probabilities are extracted for each possible state change using Laplace smoothing for numerical stability, and frequently updated in real-time.

What is unique about the visualization?

3D animated spheres represent each regime and change visually when active.

Animated, bidirectional arrows reveal transition probabilities and allow you to see both dominant and less likely regime flows.

Particles (moving dots) animate along the arrows, enhancing the perception of regime flow direction and speed.

All elements dynamically update with each new price bar, providing a live market map in an intuitive, engaging format.

Can I use custom indicators for regime classification?

Yes! Enable the "Custom Indicators" switch and select any three chart series as inputs. These will be normalized and combined (each with equal weight), broadening the regime classification beyond just price-based movement.

What does the “Lookback Period” control?

Lookback Period (default: 100) sets how much historical data builds the probability matrix. Shorter periods adapt faster to regime changes but may be noisier. Longer periods are more stable but slower to adapt.

How is this different from a Hidden Markov Model (HMM)?

It sets the window for both regime detection and probability calculations. Lower values make the system more reactive, but potentially noisier. Higher values smooth estimates and make the system more robust.

How is this Markov Chain different from a Hidden Markov Model (HMM)?

Markov Chain (as here): All market regimes (Bull, Bear, Neutral) are directly observable on the chart. The transition matrix is built from actual detected regimes, keeping the model simple and interpretable.

Hidden Markov Model: The actual regimes are unobservable ("hidden") and must be inferred from market output or indicator "emissions" using statistical learning algorithms. HMMs are more complex, can capture more subtle structure, but are harder to visualize and require additional machine learning steps for training.

A standard Markov Chain models transitions between observable states using a simple transition matrix, while a Hidden Markov Model assumes the true states are hidden (latent) and must be inferred from observable “emissions” like price or volume data. In practical terms, a Markov Chain is transparent and easier to implement and interpret; an HMM is more expressive but requires statistical inference to estimate hidden states from data.

Markov Chain: states are observable; you directly count or estimate transition probabilities between visible states. This makes it simpler, faster, and easier to validate and tune.

HMM: states are hidden; you only observe emissions generated by those latent states. Learning involves machine learning/statistical algorithms (commonly Baum–Welch/EM for training and Viterbi for decoding) to infer both the transition dynamics and the most likely hidden state sequence from data.

How does the indicator avoid “repainting” or look-ahead bias?

All regime changes and matrix updates happen only on confirmed (closed) bars, so no future data is leaked, ensuring reliable real-time operation.

Are there practical tuning tips?

Tune the Lookback Period for your asset/timeframe: shorter for fast markets, longer for stability.

Use custom indicators if your asset has unique regime drivers.

Watch for rapid changes in transition probabilities as early warning of a possible regime shift.

Who is this indicator for?

Quants and quantitative researchers exploring probabilistic market modeling, especially those interested in regime-switching dynamics and Markov models.

Programmers and system developers who need a probabilistic regime filter for systematic and algorithmic backtesting:

The Markov Chain indicator is ideally suited for programmatic integration via its bias output (1 = Bull, 0 = Neutral, -1 = Bear).

Although the visualization is engaging, the core output is designed for automated, rules-based workflows—not for discretionary/manual trading decisions.

Developers can connect the indicator’s output directly to their Pine Script logic (using input.source()), allowing rapid and robust backtesting of regime-based strategies.

It acts as a plug-and-play regime filter: simply plug the bias output into your entry/exit logic, and you have a scientifically robust, probabilistically-derived signal for filtering, timing, position sizing, or risk regimes.

The MC's output is intentionally "trinary" (1/0/-1), focusing on clear regime states for unambiguous decision-making in code. If you require nuanced, multi-probability or soft-label state vectors, consider expanding the indicator or stacking it with a probability-weighted logic layer in your scripting.

Because it avoids subjectivity, this approach is optimal for systematic quants, algo developers building backtested, repeatable strategies based on probabilistic regime analysis.

What's the mathematical foundation behind this?

The mathematical foundation behind this Markov Chain indicator—and probabilistic regime detection in finance—draws from two principal models: the (standard) Markov Chain and the Hidden Markov Model (HMM).

How to use this indicator programmatically?

The Markov Chain indicator automatically exports a bias value (+1 for Bullish, -1 for Bearish, 0 for Neutral) as a plot visible in the Data Window. This allows you to integrate its regime signal into your own scripts and strategies for backtesting, automation, or live trading.

Step-by-Step Integration with Pine Script (input.source)

Add the Markov Chain indicator to your chart.

This must be done first, since your custom script will "pull" the bias signal from the indicator's plot.

In your strategy, create an input using input.source()

Example:

//@version=5

strategy("MC Bias Strategy Example")

mcBias = input.source(close, "MC Bias Source")

After saving, go to your script’s settings. For the “MC Bias Source” input, select the plot/output of the Markov Chain indicator (typically its bias plot).

Use the bias in your trading logic

Example (long only on Bull, flat otherwise):

if mcBias == 1

strategy.entry("Long", strategy.long)

else

strategy.close("Long")

For more advanced workflows, combine mcBias with additional filters or trailing stops.

How does this work behind-the-scenes?

TradingView’s input.source() lets you use any plot from another indicator as a real-time, “live” data feed in your own script (source).

The selected bias signal is available to your Pine code as a variable, enabling logical decisions based on regime (trend-following, mean-reversion, etc.).

This enables powerful strategy modularity : decouple regime detection from entry/exit logic, allowing fast experimentation without rewriting core signal code.

Integrating 45+ Indicators with Your Markov Chain — How & Why

The Enhanced Custom Indicators Export script exports a massive suite of over 45 technical indicators—ranging from classic momentum (RSI, MACD, Stochastic, etc.) to trend, volume, volatility, and oscillator tools—all pre-calculated, centered/scaled, and available as plots.

// Enhanced Custom Indicators Export - 45 Technical Indicators

// Comprehensive technical analysis suite for advanced market regime detection

//@version=6

indicator('Enhanced Custom Indicators Export | Fractalyst', shorttitle='Enhanced CI Export', overlay=false, scale=scale.right, max_labels_count=500, max_lines_count=500)

// |----- Input Parameters -----| //

momentum_group = "Momentum Indicators"

trend_group = "Trend Indicators"

volume_group = "Volume Indicators"

volatility_group = "Volatility Indicators"

oscillator_group = "Oscillator Indicators"

display_group = "Display Settings"

// Common lengths

length_14 = input.int(14, "Standard Length (14)", minval=1, maxval=100, group=momentum_group)

length_20 = input.int(20, "Medium Length (20)", minval=1, maxval=200, group=trend_group)

length_50 = input.int(50, "Long Length (50)", minval=1, maxval=200, group=trend_group)

// Display options

show_table = input.bool(true, "Show Values Table", group=display_group)

table_size = input.string("Small", "Table Size", options= , group=display_group)

// |----- MOMENTUM INDICATORS (15 indicators) -----| //

// 1. RSI (Relative Strength Index)

rsi_14 = ta.rsi(close, length_14)

rsi_centered = rsi_14 - 50

// 2. Stochastic Oscillator

stoch_k = ta.stoch(close, high, low, length_14)

stoch_d = ta.sma(stoch_k, 3)

stoch_centered = stoch_k - 50

// 3. Williams %R

williams_r = ta.stoch(close, high, low, length_14) - 100

// 4. MACD (Moving Average Convergence Divergence)

= ta.macd(close, 12, 26, 9)

// 5. Momentum (Rate of Change)

momentum = ta.mom(close, length_14)

momentum_pct = (momentum / close ) * 100

// 6. Rate of Change (ROC)

roc = ta.roc(close, length_14)

// 7. Commodity Channel Index (CCI)

cci = ta.cci(close, length_20)

// 8. Money Flow Index (MFI)

mfi = ta.mfi(close, length_14)

mfi_centered = mfi - 50

// 9. Awesome Oscillator (AO)

ao = ta.sma(hl2, 5) - ta.sma(hl2, 34)

// 10. Accelerator Oscillator (AC)

ac = ao - ta.sma(ao, 5)

// 11. Chande Momentum Oscillator (CMO)

cmo = ta.cmo(close, length_14)

// 12. Detrended Price Oscillator (DPO)

dpo = close - ta.sma(close, length_20)

// 13. Price Oscillator (PPO)

ppo = ta.sma(close, 12) - ta.sma(close, 26)

ppo_pct = (ppo / ta.sma(close, 26)) * 100

// 14. TRIX

trix_ema1 = ta.ema(close, length_14)

trix_ema2 = ta.ema(trix_ema1, length_14)

trix_ema3 = ta.ema(trix_ema2, length_14)

trix = ta.roc(trix_ema3, 1) * 10000

// 15. Klinger Oscillator

klinger = ta.ema(volume * (high + low + close) / 3, 34) - ta.ema(volume * (high + low + close) / 3, 55)

// 16. Fisher Transform

fisher_hl2 = 0.5 * (hl2 - ta.lowest(hl2, 10)) / (ta.highest(hl2, 10) - ta.lowest(hl2, 10)) - 0.25

fisher = 0.5 * math.log((1 + fisher_hl2) / (1 - fisher_hl2))

// 17. Stochastic RSI

stoch_rsi = ta.stoch(rsi_14, rsi_14, rsi_14, length_14)

stoch_rsi_centered = stoch_rsi - 50

// 18. Relative Vigor Index (RVI)

rvi_num = ta.swma(close - open)

rvi_den = ta.swma(high - low)

rvi = rvi_den != 0 ? rvi_num / rvi_den : 0

// 19. Balance of Power (BOP)

bop = (close - open) / (high - low)

// |----- TREND INDICATORS (10 indicators) -----| //

// 20. Simple Moving Average Momentum

sma_20 = ta.sma(close, length_20)

sma_momentum = ((close - sma_20) / sma_20) * 100

// 21. Exponential Moving Average Momentum

ema_20 = ta.ema(close, length_20)

ema_momentum = ((close - ema_20) / ema_20) * 100

// 22. Parabolic SAR

sar = ta.sar(0.02, 0.02, 0.2)

sar_trend = close > sar ? 1 : -1

// 23. Linear Regression Slope

lr_slope = ta.linreg(close, length_20, 0) - ta.linreg(close, length_20, 1)

// 24. Moving Average Convergence (MAC)

mac = ta.sma(close, 10) - ta.sma(close, 30)

// 25. Trend Intensity Index (TII)

tii_sum = 0.0

for i = 1 to length_20

tii_sum += close > close ? 1 : 0

tii = (tii_sum / length_20) * 100

// 26. Ichimoku Cloud Components

ichimoku_tenkan = (ta.highest(high, 9) + ta.lowest(low, 9)) / 2

ichimoku_kijun = (ta.highest(high, 26) + ta.lowest(low, 26)) / 2

ichimoku_signal = ichimoku_tenkan > ichimoku_kijun ? 1 : -1

// 27. MESA Adaptive Moving Average (MAMA)

mama_alpha = 2.0 / (length_20 + 1)

mama = ta.ema(close, length_20)

mama_momentum = ((close - mama) / mama) * 100

// 28. Zero Lag Exponential Moving Average (ZLEMA)

zlema_lag = math.round((length_20 - 1) / 2)

zlema_data = close + (close - close )

zlema = ta.ema(zlema_data, length_20)

zlema_momentum = ((close - zlema) / zlema) * 100

// |----- VOLUME INDICATORS (6 indicators) -----| //

// 29. On-Balance Volume (OBV)

obv = ta.obv

// 30. Volume Rate of Change (VROC)

vroc = ta.roc(volume, length_14)

// 31. Price Volume Trend (PVT)

pvt = ta.pvt

// 32. Negative Volume Index (NVI)

nvi = 0.0

nvi := volume < volume ? nvi + ((close - close ) / close ) * nvi : nvi

// 33. Positive Volume Index (PVI)

pvi = 0.0

pvi := volume > volume ? pvi + ((close - close ) / close ) * pvi : pvi

// 34. Volume Oscillator

vol_osc = ta.sma(volume, 5) - ta.sma(volume, 10)

// 35. Ease of Movement (EOM)

eom_distance = high - low

eom_box_height = volume / 1000000

eom = eom_box_height != 0 ? eom_distance / eom_box_height : 0

eom_sma = ta.sma(eom, length_14)

// 36. Force Index

force_index = volume * (close - close )

force_index_sma = ta.sma(force_index, length_14)

// |----- VOLATILITY INDICATORS (10 indicators) -----| //

// 37. Average True Range (ATR)

atr = ta.atr(length_14)

atr_pct = (atr / close) * 100

// 38. Bollinger Bands Position

bb_basis = ta.sma(close, length_20)

bb_dev = 2.0 * ta.stdev(close, length_20)

bb_upper = bb_basis + bb_dev

bb_lower = bb_basis - bb_dev

bb_position = bb_dev != 0 ? (close - bb_basis) / bb_dev : 0

bb_width = bb_dev != 0 ? (bb_upper - bb_lower) / bb_basis * 100 : 0

// 39. Keltner Channels Position

kc_basis = ta.ema(close, length_20)

kc_range = ta.ema(ta.tr, length_20)

kc_upper = kc_basis + (2.0 * kc_range)

kc_lower = kc_basis - (2.0 * kc_range)

kc_position = kc_range != 0 ? (close - kc_basis) / kc_range : 0

// 40. Donchian Channels Position

dc_upper = ta.highest(high, length_20)

dc_lower = ta.lowest(low, length_20)

dc_basis = (dc_upper + dc_lower) / 2

dc_position = (dc_upper - dc_lower) != 0 ? (close - dc_basis) / (dc_upper - dc_lower) : 0

// 41. Standard Deviation

std_dev = ta.stdev(close, length_20)

std_dev_pct = (std_dev / close) * 100

// 42. Relative Volatility Index (RVI)

rvi_up = ta.stdev(close > close ? close : 0, length_14)

rvi_down = ta.stdev(close < close ? close : 0, length_14)

rvi_total = rvi_up + rvi_down

rvi_volatility = rvi_total != 0 ? (rvi_up / rvi_total) * 100 : 50

// 43. Historical Volatility

hv_returns = math.log(close / close )

hv = ta.stdev(hv_returns, length_20) * math.sqrt(252) * 100

// 44. Garman-Klass Volatility

gk_vol = math.log(high/low) * math.log(high/low) - (2*math.log(2)-1) * math.log(close/open) * math.log(close/open)

gk_volatility = math.sqrt(ta.sma(gk_vol, length_20)) * 100

// 45. Parkinson Volatility

park_vol = math.log(high/low) * math.log(high/low)

parkinson = math.sqrt(ta.sma(park_vol, length_20) / (4 * math.log(2))) * 100

// 46. Rogers-Satchell Volatility

rs_vol = math.log(high/close) * math.log(high/open) + math.log(low/close) * math.log(low/open)

rogers_satchell = math.sqrt(ta.sma(rs_vol, length_20)) * 100

// |----- OSCILLATOR INDICATORS (5 indicators) -----| //

// 47. Elder Ray Index

elder_bull = high - ta.ema(close, 13)

elder_bear = low - ta.ema(close, 13)

elder_power = elder_bull + elder_bear

// 48. Schaff Trend Cycle (STC)

stc_macd = ta.ema(close, 23) - ta.ema(close, 50)

stc_k = ta.stoch(stc_macd, stc_macd, stc_macd, 10)

stc_d = ta.ema(stc_k, 3)

stc = ta.stoch(stc_d, stc_d, stc_d, 10)

// 49. Coppock Curve

coppock_roc1 = ta.roc(close, 14)

coppock_roc2 = ta.roc(close, 11)

coppock = ta.wma(coppock_roc1 + coppock_roc2, 10)

// 50. Know Sure Thing (KST)

kst_roc1 = ta.roc(close, 10)

kst_roc2 = ta.roc(close, 15)

kst_roc3 = ta.roc(close, 20)

kst_roc4 = ta.roc(close, 30)

kst = ta.sma(kst_roc1, 10) + 2*ta.sma(kst_roc2, 10) + 3*ta.sma(kst_roc3, 10) + 4*ta.sma(kst_roc4, 15)

// 51. Percentage Price Oscillator (PPO)

ppo_line = ((ta.ema(close, 12) - ta.ema(close, 26)) / ta.ema(close, 26)) * 100

ppo_signal = ta.ema(ppo_line, 9)

ppo_histogram = ppo_line - ppo_signal

// |----- PLOT MAIN INDICATORS -----| //

// Plot key momentum indicators

plot(rsi_centered, title="01_RSI_Centered", color=color.purple, linewidth=1)

plot(stoch_centered, title="02_Stoch_Centered", color=color.blue, linewidth=1)

plot(williams_r, title="03_Williams_R", color=color.red, linewidth=1)

plot(macd_histogram, title="04_MACD_Histogram", color=color.orange, linewidth=1)

plot(cci, title="05_CCI", color=color.green, linewidth=1)

// Plot trend indicators

plot(sma_momentum, title="06_SMA_Momentum", color=color.navy, linewidth=1)

plot(ema_momentum, title="07_EMA_Momentum", color=color.maroon, linewidth=1)

plot(sar_trend, title="08_SAR_Trend", color=color.teal, linewidth=1)

plot(lr_slope, title="09_LR_Slope", color=color.lime, linewidth=1)

plot(mac, title="10_MAC", color=color.fuchsia, linewidth=1)

// Plot volatility indicators

plot(atr_pct, title="11_ATR_Pct", color=color.yellow, linewidth=1)

plot(bb_position, title="12_BB_Position", color=color.aqua, linewidth=1)

plot(kc_position, title="13_KC_Position", color=color.olive, linewidth=1)

plot(std_dev_pct, title="14_StdDev_Pct", color=color.silver, linewidth=1)

plot(bb_width, title="15_BB_Width", color=color.gray, linewidth=1)

// Plot volume indicators

plot(vroc, title="16_VROC", color=color.blue, linewidth=1)

plot(eom_sma, title="17_EOM", color=color.red, linewidth=1)

plot(vol_osc, title="18_Vol_Osc", color=color.green, linewidth=1)

plot(force_index_sma, title="19_Force_Index", color=color.orange, linewidth=1)

plot(obv, title="20_OBV", color=color.purple, linewidth=1)

// Plot additional oscillators

plot(ao, title="21_Awesome_Osc", color=color.navy, linewidth=1)

plot(cmo, title="22_CMO", color=color.maroon, linewidth=1)

plot(dpo, title="23_DPO", color=color.teal, linewidth=1)

plot(trix, title="24_TRIX", color=color.lime, linewidth=1)

plot(fisher, title="25_Fisher", color=color.fuchsia, linewidth=1)

// Plot more momentum indicators

plot(mfi_centered, title="26_MFI_Centered", color=color.yellow, linewidth=1)

plot(ac, title="27_AC", color=color.aqua, linewidth=1)

plot(ppo_pct, title="28_PPO_Pct", color=color.olive, linewidth=1)

plot(stoch_rsi_centered, title="29_StochRSI_Centered", color=color.silver, linewidth=1)

plot(klinger, title="30_Klinger", color=color.gray, linewidth=1)

// Plot trend continuation

plot(tii, title="31_TII", color=color.blue, linewidth=1)

plot(ichimoku_signal, title="32_Ichimoku_Signal", color=color.red, linewidth=1)

plot(mama_momentum, title="33_MAMA_Momentum", color=color.green, linewidth=1)

plot(zlema_momentum, title="34_ZLEMA_Momentum", color=color.orange, linewidth=1)

plot(bop, title="35_BOP", color=color.purple, linewidth=1)

// Plot volume continuation

plot(nvi, title="36_NVI", color=color.navy, linewidth=1)

plot(pvi, title="37_PVI", color=color.maroon, linewidth=1)

plot(momentum_pct, title="38_Momentum_Pct", color=color.teal, linewidth=1)

plot(roc, title="39_ROC", color=color.lime, linewidth=1)

plot(rvi, title="40_RVI", color=color.fuchsia, linewidth=1)

// Plot volatility continuation

plot(dc_position, title="41_DC_Position", color=color.yellow, linewidth=1)

plot(rvi_volatility, title="42_RVI_Volatility", color=color.aqua, linewidth=1)

plot(hv, title="43_Historical_Vol", color=color.olive, linewidth=1)

plot(gk_volatility, title="44_GK_Volatility", color=color.silver, linewidth=1)

plot(parkinson, title="45_Parkinson_Vol", color=color.gray, linewidth=1)

// Plot final oscillators

plot(rogers_satchell, title="46_RS_Volatility", color=color.blue, linewidth=1)

plot(elder_power, title="47_Elder_Power", color=color.red, linewidth=1)

plot(stc, title="48_STC", color=color.green, linewidth=1)

plot(coppock, title="49_Coppock", color=color.orange, linewidth=1)

plot(kst, title="50_KST", color=color.purple, linewidth=1)

// Plot final indicators

plot(ppo_histogram, title="51_PPO_Histogram", color=color.navy, linewidth=1)

plot(pvt, title="52_PVT", color=color.maroon, linewidth=1)

// |----- Reference Lines -----| //

hline(0, "Zero Line", color=color.gray, linestyle=hline.style_dashed, linewidth=1)

hline(50, "Midline", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

hline(-50, "Lower Midline", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

hline(25, "Upper Threshold", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

hline(-25, "Lower Threshold", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

// |----- Enhanced Information Table -----| //

if show_table and barstate.islast

table_position = position.top_right

table_text_size = table_size == "Tiny" ? size.tiny : table_size == "Small" ? size.small : size.normal

var table info_table = table.new(table_position, 3, 18, bgcolor=color.new(color.white, 85), border_width=1, border_color=color.gray)

// Headers

table.cell(info_table, 0, 0, 'Category', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.blue, 70))

table.cell(info_table, 1, 0, 'Indicator', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.blue, 70))

table.cell(info_table, 2, 0, 'Value', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.blue, 70))

// Key Momentum Indicators

table.cell(info_table, 0, 1, 'MOMENTUM', text_color=color.purple, text_size=table_text_size, bgcolor=color.new(color.purple, 90))

table.cell(info_table, 1, 1, 'RSI Centered', text_color=color.purple, text_size=table_text_size)

table.cell(info_table, 2, 1, str.tostring(rsi_centered, '0.00'), text_color=color.purple, text_size=table_text_size)

table.cell(info_table, 0, 2, '', text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 1, 2, 'Stoch Centered', text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 2, 2, str.tostring(stoch_centered, '0.00'), text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 0, 3, '', text_color=color.red, text_size=table_text_size)