MTF Signal XpertMTF Signal Xpert – Detailed Description

Overview:

MTF Signal Xpert is a proprietary, open‑source trading signal indicator that fuses multiple technical analysis methods into one cohesive strategy. Developed after rigorous backtesting and extensive research, this advanced tool is designed to deliver clear BUY and SELL signals by analyzing trend, momentum, and volatility across various timeframes. Its integrated approach not only enhances signal reliability but also incorporates dynamic risk management, helping traders protect their capital while navigating complex market conditions.

Detailed Explanation of How It Works:

Trend Detection via Moving Averages

Dual Moving Averages:

MTF Signal Xpert computes two moving averages—a fast MA and a slow MA—with the flexibility to choose from Simple (SMA), Exponential (EMA), or Hull (HMA) methods. This dual-MA system helps identify the prevailing market trend by contrasting short-term momentum with longer-term trends.

Crossover Logic:

A BUY signal is initiated when the fast MA crosses above the slow MA, coupled with the condition that the current price is above the lower Bollinger Band. This suggests that the market may be emerging from a lower price region. Conversely, a SELL signal is generated when the fast MA crosses below the slow MA and the price is below the upper Bollinger Band, indicating potential bearish pressure.

Recent Crossover Confirmation:

To ensure that signals reflect current market dynamics, the script tracks the number of bars since the moving average crossover event. Only crossovers that occur within a user-defined “candle confirmation” period are considered, which helps filter out outdated signals and improves overall signal accuracy.

Volatility and Price Extremes with Bollinger Bands

Calculation of Bands:

Bollinger Bands are calculated using a 20‑period simple moving average as the central basis, with the upper and lower bands derived from a standard deviation multiplier. This creates dynamic boundaries that adjust according to recent market volatility.

Signal Reinforcement:

For BUY signals, the condition that the price is above the lower Bollinger Band suggests an undervalued market condition, while for SELL signals, the price falling below the upper Bollinger Band reinforces the bearish bias. This volatility context adds depth to the moving average crossover signals.

Momentum Confirmation Using Multiple Oscillators

RSI (Relative Strength Index):

The RSI is computed over 14 periods to determine if the market is in an overbought or oversold state. Only readings within an optimal range (defined by user inputs) validate the signal, ensuring that entries are made during balanced conditions.

MACD (Moving Average Convergence Divergence):

The MACD line is compared with its signal line to assess momentum. A bullish scenario is confirmed when the MACD line is above the signal line, while a bearish scenario is indicated when it is below, thus adding another layer of confirmation.

Awesome Oscillator (AO):

The AO measures the difference between short-term and long-term simple moving averages of the median price. Positive AO values support BUY signals, while negative values back SELL signals, offering additional momentum insight.

ADX (Average Directional Index):

The ADX quantifies trend strength. MTF Signal Xpert only considers signals when the ADX value exceeds a specified threshold, ensuring that trades are taken in strongly trending markets.

Optional Stochastic Oscillator:

An optional stochastic oscillator filter can be enabled to further refine signals. It checks for overbought conditions (supporting SELL signals) or oversold conditions (supporting BUY signals), thus reducing ambiguity.

Multi-Timeframe Verification

Higher Timeframe Filter:

To align short-term signals with broader market trends, the script calculates an EMA on a higher timeframe as specified by the user. This multi-timeframe approach helps ensure that signals on the primary chart are consistent with the overall trend, thereby reducing false signals.

Dynamic Risk Management with ATR

ATR-Based Calculations:

The Average True Range (ATR) is used to measure current market volatility. This value is multiplied by a user-defined factor to dynamically determine stop loss (SL) and take profit (TP) levels, adapting to changing market conditions.

Visual SL/TP Markers:

The calculated SL and TP levels are plotted on the chart as distinct colored dots, enabling traders to quickly identify recommended exit points.

Optional Trailing Stop:

An optional trailing stop feature is available, which adjusts the stop loss as the trade moves favorably, helping to lock in profits while protecting against sudden reversals.

Risk/Reward Ratio Calculation:

MTF Signal Xpert computes a risk/reward ratio based on the dynamic SL and TP levels. This quantitative measure allows traders to assess whether the potential reward justifies the risk associated with a trade.

Condition Weighting and Signal Scoring

Binary Condition Checks:

Each technical condition—ranging from moving average crossovers, Bollinger Band positioning, and RSI range to MACD, AO, ADX, and volume filters—is assigned a binary score (1 if met, 0 if not).

Cumulative Scoring:

These individual scores are summed to generate cumulative bullish and bearish scores, quantifying the overall strength of the signal and providing traders with an objective measure of its viability.

Detailed Signal Explanation:

A comprehensive explanation string is generated, outlining which conditions contributed to the current BUY or SELL signal. This explanation is displayed on an on‑chart dashboard, offering transparency and clarity into the signal generation process.

On-Chart Visualizations and Debug Information

Chart Elements:

The indicator plots all key components—moving averages, Bollinger Bands, SL and TP markers—directly on the chart, providing a clear visual framework for understanding market conditions.

Combined Dashboard:

A dedicated dashboard displays key metrics such as RSI, ADX, and the bullish/bearish scores, alongside a detailed explanation of the current signal. This consolidated view allows traders to quickly grasp the underlying logic.

Debug Table (Optional):

For advanced users, an optional debug table is available. This table breaks down each individual condition, indicating which criteria were met or not met, thus aiding in further analysis and strategy refinement.

Mashup Justification and Originality

MTF Signal Xpert is more than just an aggregation of existing indicators—it is an original synthesis designed to address real-world trading complexities. Here’s how its components work together:

Integrated Trend, Volatility, and Momentum Analysis:

By combining moving averages, Bollinger Bands, and multiple oscillators (RSI, MACD, AO, ADX, and an optional stochastic), the indicator captures diverse market dynamics. Each component reinforces the others, reducing noise and filtering out false signals.

Multi-Timeframe Analysis:

The inclusion of a higher timeframe filter aligns short-term signals with longer-term trends, enhancing overall reliability and reducing the potential for contradictory signals.

Adaptive Risk Management:

Dynamic stop loss and take profit levels, determined using ATR, ensure that the risk management strategy adapts to current market conditions. The optional trailing stop further refines this approach, protecting profits as the market evolves.

Quantitative Signal Scoring:

The condition weighting system provides an objective measure of signal strength, giving traders clear insight into how each technical component contributes to the final decision.

How to Use MTF Signal Xpert:

Input Customization:

Adjust the moving average type and period settings, ATR multipliers, and oscillator thresholds to align with your trading style and the specific market conditions.

Enable or disable the optional stochastic oscillator and trailing stop based on your preference.

Interpreting the Signals:

When a BUY or SELL signal appears, refer to the on‑chart dashboard, which displays key metrics (e.g., RSI, ADX, bullish/bearish scores) along with a detailed breakdown of the conditions that triggered the signal.

Review the SL and TP markers on the chart to understand the associated risk/reward setup.

Risk Management:

Use the dynamically calculated stop loss and take profit levels as guidelines for setting your exit points.

Evaluate the provided risk/reward ratio to ensure that the potential reward justifies the risk before entering a trade.

Debugging and Verification:

Advanced users can enable the debug table to see a condition-by-condition breakdown of the signal generation process, helping refine the strategy and deepen understanding of market dynamics.

Disclaimer:

MTF Signal Xpert is intended for educational and analytical purposes only. Although it is based on robust technical analysis methods and has undergone extensive backtesting, past performance is not indicative of future results. Traders should employ proper risk management and adjust the settings to suit their financial circumstances and risk tolerance.

MTF Signal Xpert represents a comprehensive, original approach to trading signal generation. By blending trend detection, volatility assessment, momentum analysis, multi-timeframe alignment, and adaptive risk management into one integrated system, it provides traders with actionable signals and the transparency needed to understand the logic behind them.

Wyszukaj w skryptach "Trailing stop"

Blackflag FTS (1H Trailing) + MSB-OB FibThis indicator combines a 1-hour trailing stop system with multi-timeframe Fibonacci retracement levels and ZigZag structure detection to assist traders in identifying trend direction and potential reversal zones.

Features:

✅ 1-Hour Trailing Stop: Uses an ATR-based trailing stop mechanism to track trend direction and dynamic support/resistance.

✅ Multi-Timeframe Approach: The trailing stop is calculated on the 1-hour timeframe, while the ZigZag and Fibonacci retracement levels are based on the 15-minute chart.

✅ ZigZag Structure Detection: Helps filter market swings and trend reversals dynamically.

✅ Fibonacci Levels (0.5 & 0.786): Key retracement levels to watch for price reactions.

✅ Alerts for Key Levels: Get notified when the price crosses important levels (1H trailing stop, Fib 0.5, Fib 0.786).

How It Works:

The trailing stop adapts dynamically based on ATR values and determines trend direction.

ZigZag detection filters out minor price movements to highlight major swing points.

Fibonacci levels are calculated based on ZigZag swings, helping traders spot potential reversal zones.

This tool is useful for trend-following traders, breakout traders, and Fibonacci-based strategies.

Let me know if you'd like any modifications! 🚀

Quantitative Breakout Bands (AIBitcoinTrend)Quantitative Breakout Bands (AIBitcoinTrend) is an advanced indicator designed to adapt to dynamic market conditions by utilizing a Kalman filter for real-time data analysis and trend detection. This innovative tool empowers traders to identify price breakouts, evaluate trends, and refine their trading strategies with precision.

👽 What Are Quantitative Breakout Bands, and Why Are They Unique?

Quantitative Breakout Bands combine advanced filtering techniques (Kalman Filters) with statistical measures such as mean absolute error (MAE) to create adaptive price bands. These bands adjust to market conditions dynamically, providing insights into volatility, trend strength, and breakout opportunities.

What sets this indicator apart is its ability to incorporate both position (price) and velocity (rate of price change) into its calculations, making it highly responsive yet smooth. This dual consideration ensures traders get reliable signals without excessive lag or noise.

👽 The Math Behind the Indicator

👾 Kalman Filter Estimation:

At the core of the indicator is the Kalman Filter, a recursive algorithm used to predict the next state of a system based on past observations. It incorporates two primary elements:

State Prediction: The indicator predicts future price (position) and velocity based on previous values.

Error Covariance Adjustment: The process and measurement noise parameters refine the prediction's accuracy by balancing smoothness and responsiveness.

👾 Breakout Bands Calculation:

The breakout bands are derived from the mean absolute error (MAE) of price deviations relative to the filtered trendline:

float upperBand = kalmanPrice + bandMultiplier * mae

float lowerBand = kalmanPrice - bandMultiplier * mae

The multiplier allows traders to adjust the sensitivity of the bands to market volatility.

👾 Slope-Based Trend Detection:

A weighted slope calculation measures the gradient of the filtered price over a configurable window. This slope determines whether the market is trending bullish, bearish, or neutral.

👾 Trailing Stop Mechanism:

The trailing stop employs the Average True Range (ATR) to calculate dynamic stop levels. This ensures positions are protected during volatile moves while minimizing premature exits.

👽 How It Adapts to Price Movements

Dynamic Noise Calibration: By adjusting process and measurement noise inputs, the indicator balances smoothness (to reduce noise) with responsiveness (to adapt to sharp price changes).

Trend Responsiveness: The Kalman Filter ensures that trend changes are quickly identified, while the slope calculation adds confirmation.

Volatility Sensitivity: The MAE-based bands expand and contract in response to changes in market volatility, making them ideal for breakout detection.

👽 How Traders Can Use the Indicator

👾 Breakout Detection:

Bullish Breakouts: When the price moves above the upper band, it signals a potential upward breakout.

Bearish Breakouts: When the price moves below the lower band, it signals a potential downward breakout.

The trailing stop feature offers a dynamic way to lock in profits or minimize losses during trending moves.

👾 Trend Confirmation:

The color-coded Kalman line and slope provide visual cues:

Bullish Trend: Positive slope, green line.

Bearish Trend: Negative slope, red line.

👽 Why It’s Useful for Traders

Dynamic and Adaptive: The indicator adjusts to changing market conditions, ensuring relevance across timeframes and asset classes.

Noise Reduction: The Kalman Filter smooths price data, eliminating false signals caused by short-term noise.

Comprehensive Insights: By combining breakout detection, trend analysis, and risk management, it offers a holistic trading tool.

👽 Indicator Settings

Process Noise (Position & Velocity): Adjusts filter responsiveness to price changes.

Measurement Noise: Defines expected price noise for smoother trend detection.

Slope Window: Configures the lookback for slope calculation.

Lookback Period for MAE: Defines the sensitivity of the bands to volatility.

Band Multiplier: Controls the band width.

ATR Multiplier: Adjusts the sensitivity of the trailing stop.

Line Width: Customizes the appearance of the trailing stop line.

Disclaimer: This indicator is designed for educational purposes and does not constitute financial advice. Please consult a qualified financial advisor before making investment decisions.

ka66: Candle Range MarkThis is a simple trailing stop loss tool using bar ranges, to be used with some discretion and understanding of basic price action.

Given a configurable percentage value, e.g. 25%:

A bullish bar (close > open) will be marked at the lower 25%

A bearish bar (close < open) will be marked at the upper 25%

The idea is to move your stop loss after each completed bar in the direction of the trade, at the configured percentage value.

If you have an inside bar, or something very close to it, or a doji-type bar, don't trail that, because there is no clarity of what the bar means, we can only wait.

The chart shows an example use, with trailing at 10% of the bar, from the initial stop loss after entry, trailing till we get stopped out. Some things to note:

Because this example focuses on a short trade, we ignore the bullish candles, and keep our trailing stop at the last bearish candle.

We ignore doji-esque candles and inside bars, where the body is in the range of the prior candle. Some definitions of inside bars include the wicks as well. I don't have a strong opinion, and this example is just for illustration. Furthermore, the inside bar will likely be the opposite of the swing bars (e.g. bullish bar in a range of bearish bars), so our stop remains unchanged.

One could use this semi-systematic approach in scalping on any timeframe, for example to maximise gains, adjusting the bar percentage as needed.

ATT Model with Buy/Sell SignalsIndicator Summary

This indicator is based on the ATT (Arithmetic Time Theory) model, using specific turning points derived from the ATT sequence (3, 11, 17, 29, 41, 47, 53, 59) to identify potential market reversals. It also integrates the RSI (Relative Strength Index) to confirm overbought and oversold conditions, triggering buy and sell signals when conditions align with the ATT sequence and RSI level.

Turning Points: Detected based on the ATT sequence applied to bar count. This suggests high-probability areas where the market could turn.

RSI Filter: Adds strength to the signals by ensuring buy signals occur when RSI is oversold (<30) and sell signals when RSI is overbought (>70).

Max Signals Per Session: Limits signals to two per session to reduce over-trading.

Entry Criteria

Buy Signal: Enter a buy trade if:

The indicator displays a green "BUY" marker.

RSI is below the oversold level (default <30), suggesting a potential upward reversal.

Sell Signal: Enter a sell trade if:

The indicator displays a red "SELL" marker.

RSI is above the overbought level (default >70), indicating a potential downward reversal.

Exit Criteria

Take Profit (TP):

Define TP as a fixed percentage or point value based on the asset's volatility. For example, set TP at 1.5-2x the risk, or a predefined point target (like 50-100 points).

Alternatively, exit the position when price approaches a key support/resistance level or the next significant swing high/low.

Stop Loss (SL):

Place the SL below the recent low (for buys) or above the recent high (for sells).

Set a fixed SL in points or percentage based on the asset’s average movement range, like an ATR-based stop, or limit it to a specific risk amount per trade (1-2% of account).

Trailing into Profit

Use a trailing strategy to lock in profits and let winning trades run further. Two main options:

ATR Trailing Stop:

Set the trailing stop based on the ATR (Average True Range), adjusting every time a new candle closes. This can help in volatile markets by keeping the stop at a consistent distance based on recent price movement.

Break-Even and Partial Profits:

When the price moves in your favor by a set amount (e.g., 1:1 risk/reward), move SL to the entry (break-even).

Take partial profit at intermediate levels (e.g., 50% at 1:1 RR) and trail the remainder.

Risk Management for Prop Firm Evaluation

Prop firms often have strict rules on daily loss limits, max drawdowns, and minimum profit targets. Here’s how to align your strategy with these:

Limit Risk per Trade:

Keep risk per trade to a conservative level (e.g., 1% or lower of your account balance). This allows for more room in case of a drawdown and aligns with most prop firm requirements.

Daily Loss Limits:

Set a daily stop-loss that ensures you don’t exceed the firm’s rules. For example, if the daily limit is 5%, stop trading once you reach a 3-4% drawdown.

Avoid Over-Trading:

Stick to the max signals per session rule (one or two trades). Taking only high-probability setups reduces emotional and reactive trades, preserving capital.

Stick to a Profit Target:

Aim to meet the evaluation’s profit goal efficiently but avoid risky or oversized trades to reach it faster.

Avoid Major Economic Events:

News events can disrupt technical setups. Avoid trading around significant releases (like FOMC or NFP) to reduce the chance of sudden losses due to high volatility.

Summary

Using this strategy with discipline, a structured entry/exit approach, and tight risk management can maximize your chances of passing a prop firm evaluation. The ATT model’s turning points, combined with the RSI, provide an edge by highlighting reversal zones, while limiting trades to 1-2 per session helps maintain controlled risk.

Bullish B's - RSI Divergence StrategyThis indicator strategy is an RSI (Relative Strength Index) divergence trading tool designed to identify high-probability entry and exit points based on trend shifts. It utilizes both regular and hidden RSI divergence patterns to spot potential reversals, with signals for both bullish and bearish conditions.

Key Features

Divergence Detection:

Bullish Divergence: Signals when RSI indicates momentum strengthening at a lower price level, suggesting a reversal to the upside.

Bearish Divergence: Signals when RSI shows weakening momentum at a higher price level, indicating a potential downside reversal.

Hidden Divergences: Looks for hidden bullish and bearish divergences, which signal trend continuation points where price action aligns with the prevailing trend.

Volume-Adjusted Entry Signals:

The strategy enters long trades when RSI shows bullish or hidden bullish divergence, indicating an upward momentum shift.

An optional volume filter ensures that only high-volume, high-conviction trades trigger a signal.

Exit Signals:

Exits long positions when RSI reaches a customizable overbought level, typically indicating a potential reversal or profit-taking opportunity.

Also closes positions if bearish divergence signals appear after a bullish setup, providing protection against trend reversals.

Trailing Stop-Loss:

Uses a trailing stop mechanism based on ATR (Average True Range) or a percentage threshold to lock in profits as the price moves in favor of the trade.

Alerts and Custom Notifications:

Integrated with TradingView alerts to notify the user when entry and exit conditions are met, supporting timely decision-making without constant monitoring.

Customizable Parameters:

Users can adjust the RSI period, pivot lookback range, overbought level, trailing stop type (ATR or percentage), and divergence range to fit their trading style.

Ideal Usage

This strategy is well-suited for trend traders and swing traders looking to capture reversals and trend continuations on medium to long timeframes. The divergence signals, paired with trailing stops and volume validation, make it adaptable for multiple asset classes, including stocks, forex, and crypto.

Summary

With its focus on RSI divergence, trailing stop-loss management, and volume filtering, this strategy aims to identify and capture trend changes with minimized risk. This allows traders to efficiently capture profitable moves and manage open positions with precision.

This Strategy BEST works with GLD!

Simple RSI stock Strategy [1D] The "Simple RSI Stock Strategy " is designed to long-term traders. Strategy uses a daily time frame to capitalize on signals generated by the Relative Strength Index (RSI) and the Simple Moving Average (SMA). This strategy is suitable for low-leverage trading environments and focuses on identifying potential buy opportunities when the market is oversold, while incorporating strong risk management with both dynamic and static Stop Loss mechanisms.

This strategy is recommended for use with a relatively small amount of capital and is best applied by diversifying across multiple stocks in a strong uptrend, particularly in the S&P 500 stock market. It is specifically designed for equities, and may not perform well in other markets such as commodities, forex, or cryptocurrencies, where different market dynamics and volatility patterns apply.

Indicators Used in the Strategy:

1. RSI (Relative Strength Index):

- The RSI is a momentum oscillator used to identify overbought and oversold conditions in the market.

- This strategy enters long positions when the RSI drops below the oversold level (default: 30), indicating a potential buying opportunity.

- It focuses on oversold conditions but uses a filter (SMA 200) to ensure trades are only made in the context of an overall uptrend.

2. SMA 200 (Simple Moving Average):

- The 200-period SMA serves as a trend filter, ensuring that trades are only executed when the price is above the SMA, signaling a bullish market.

- This filter helps to avoid entering trades in a downtrend, thereby reducing the risk of holding positions in a declining market.

3. ATR (Average True Range):

- The ATR is used to measure market volatility and is instrumental in setting the Stop Loss.

- By multiplying the ATR value by a custom multiplier (default: 1.5), the strategy dynamically adjusts the Stop Loss level based on market volatility, allowing for flexibility in risk management.

How the Strategy Works:

Entry Signals:

The strategy opens long positions when RSI indicates that the market is oversold (below 30), and the price is above the 200-period SMA. This ensures that the strategy buys into potential market bottoms within the context of a long-term uptrend.

Take Profit Levels:

The strategy defines three distinct Take Profit (TP) levels:

TP 1: A 5% from the entry price.

TP 2: A 10% from the entry price.

TP 3: A 15% from the entry price.

As each TP level is reached, the strategy closes portions of the position to secure profits: 33% of the position is closed at TP 1, 66% at TP 2, and 100% at TP 3.

Visualizing Target Points:

The strategy provides visual feedback by plotting plotshapes at each Take Profit level (TP 1, TP 2, TP 3). This allows traders to easily see the target profit levels on the chart, making it easier to monitor and manage positions as they approach key profit-taking areas.

Stop Loss Mechanism:

The strategy uses a dual Stop Loss system to effectively manage risk:

ATR Trailing Stop: This dynamic Stop Loss adjusts based on the ATR value and trails the price as the position moves in the trader’s favor. If a price reversal occurs and the market begins to trend downward, the trailing stop closes the position, locking in gains or minimizing losses.

Basic Stop Loss: Additionally, a fixed Stop Loss is set at 25%, limiting potential losses. This basic Stop Loss serves as a safeguard, automatically closing the position if the price drops 25% from the entry point. This higher Stop Loss is designed specifically for low-leverage trading, allowing more room for market fluctuations without prematurely closing positions.

to determine the level of stop loss and target point I used a piece of code by RafaelZioni, here is the script from which a piece of code was taken

Together, these mechanisms ensure that the strategy dynamically manages risk while offering robust protection against significant losses in case of sharp market downturns.

The position size has been estimated by me at 75% of the total capital. For optimal capital allocation, a recommended value based on the Kelly Criterion, which is calculated to be 59.13% of the total capital per trade, can also be considered.

Enjoy !

Advanced Position Management [Mr_Rakun]Advanced Position Management

This Pine Script code is for a strategy titled "Advanced Position Management," aimed at effective trade execution and management using multiple take profit levels, trailing stop loss, and dynamic position sizing.

Take Profit Levels: It defines up to three take profit (TP) levels, allowing partial position exits at different price thresholds. The take profit levels and their respective quantities are adjustable using inputs.

Stop Loss and Trailing Stop: The script implements an initial stop loss based on a percentage from the entry price. Additionally, it features a trailing stop that moves based on either a percentage or previous TP levels, dynamically adjusting to maximize gains while protecting profits.

Position Size: The position size is customizable and based on USD value, allowing the trader to manage risk more effectively.

Advantages:

Flexibility: Multiple take profit levels and a dynamic stop loss system allow traders to lock in profits while keeping the position open for further gains.

Risk Management: The initial stop loss and trailing stop help to limit losses and protect profits as the trade moves in the desired direction.

Automation: Once the strategy is deployed, it automatically handles entry, exit, and stop management, reducing the need for constant monitoring.

------ TR ------

Gelişmiş Pozisyon Yönetimi

Bu Pine Script kodu, Gelişmiş Pozisyon Yönetimi için kendi stratejilerinize kolayca entegre edeceğiniz bir risk yönetimidir. Çoklu kâr al seviyeleri, takip eden stop-loss ve dinamik pozisyon büyüklüğü kullanarak işlem yürütme ve yönetiminde etkilidir.

Gelişmiş Pozisyon Yönetimi

Kâr Alma Seviyeleri;

Kod, pozisyonların farklı fiyat seviyelerinde kısmi kapatılmasını sağlayan üç farklı kâr alma (TP) seviyesini tanımlar. Bu kâr alma seviyeleri ve ilgili miktarları, girişlerle ayarlanabilir.

Stop Loss ve Takip Eden Stop;

Koda, giriş fiyatından bir yüzdeye dayalı olarak başlangıçta stop-loss uygulanır. Ayrıca, fiyat hareketine göre kendini ayarlayan takip eden bir stop-loss sistemi bulunur. Ayrıca TP seviyelerini takip eden stop loss özelliğide vardır.

Avantajları:

Esneklik;

Çoklu kâr alma seviyeleri ve dinamik stop-loss sistemi, trader'ların kazançlarını kilitleyip aynı zamanda pozisyonu açık tutmalarına olanak tanır.

Risk Yönetimi;

Başlangıç stop-loss ve takip eden stop, zararı sınırlamaya ve kazançları korumaya yardımcı olur.

Otomasyon;

Strateji bir kez devreye alındığında, giriş, çıkış ve stop yönetimi otomatik olarak gerçekleştirilir, bu da sürekli takip ihtiyacını azaltır.

Mean Reversion Cloud (Ornstein-Uhlenbeck) // AlgoFyreThe Mean Reversion Cloud (Ornstein-Uhlenbeck) indicator detects mean-reversion opportunities by applying the Ornstein-Uhlenbeck process. It calculates a dynamic mean using an Exponential Weighted Moving Average, surrounded by volatility bands, signaling potential buy/sell points when prices deviate.

TABLE OF CONTENTS

🔶 ORIGINALITY

🔸Adaptive Mean Calculation

🔸Volatility-Based Cloud

🔸Speed of Reversion (θ)

🔶 FUNCTIONALITY

🔸Dynamic Mean and Volatility Bands

🞘 How it works

🞘 How to calculate

🞘 Code extract

🔸Visualization via Table and Plotshapes

🞘 Table Overview

🞘 Plotshapes Explanation

🞘 Code extract

🔶 INSTRUCTIONS

🔸Step-by-Step Guidelines

🞘 Setting Up the Indicator

🞘 Understanding What to Look For on the Chart

🞘 Possible Entry Signals

🞘 Possible Take Profit Strategies

🞘 Possible Stop-Loss Levels

🞘 Additional Tips

🔸Customize settings

🔶 CONCLUSION

▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅

🔶 ORIGINALITY The Mean Reversion Cloud (Ornstein-Uhlenbeck) is a unique indicator that applies the Ornstein-Uhlenbeck stochastic process to identify mean-reverting behavior in asset prices. Unlike traditional moving average-based indicators, this model uses an Exponentially Weighted Moving Average (EWMA) to calculate the long-term mean, dynamically adjusting to recent price movements while still considering all historical data. It also incorporates volatility bands, providing a "cloud" that visually highlights overbought or oversold conditions. By calculating the speed of mean reversion (θ) through the autocorrelation of log returns, this indicator offers traders a more nuanced and mathematically robust tool for identifying mean-reversion opportunities. These innovations make it especially useful for markets that exhibit range-bound characteristics, offering timely buy and sell signals based on statistical deviations from the mean.

🔸Adaptive Mean Calculation Traditional MA indicators use fixed lengths, which can lead to lagging signals or over-sensitivity in volatile markets. The Mean Reversion Cloud uses an Exponentially Weighted Moving Average (EWMA), which adapts to price movements by dynamically adjusting its calculation, offering a more responsive mean.

🔸Volatility-Based Cloud Unlike simple moving averages that only plot a single line, the Mean Reversion Cloud surrounds the dynamic mean with volatility bands. These bands, based on standard deviations, provide traders with a visual cue of when prices are statistically likely to revert, highlighting potential reversal zones.

🔸Speed of Reversion (θ) The indicator goes beyond price averages by calculating the speed at which the price reverts to the mean (θ), using the autocorrelation of log returns. This gives traders an additional tool for estimating the likelihood and timing of mean reversion, making the signals more reliable in practice.

🔶 FUNCTIONALITY The Mean Reversion Cloud (Ornstein-Uhlenbeck) indicator is designed to detect potential mean-reversion opportunities in asset prices by applying the Ornstein-Uhlenbeck stochastic process. It calculates a dynamic mean through the Exponentially Weighted Moving Average (EWMA) and plots volatility bands based on the standard deviation of the asset's price over a specified period. These bands create a "cloud" that represents expected price fluctuations, helping traders to identify overbought or oversold conditions. By calculating the speed of reversion (θ) from the autocorrelation of log returns, the indicator offers a more refined way of assessing how quickly prices may revert to the mean. Additionally, the inclusion of volatility provides a comprehensive view of market conditions, allowing for more accurate buy and sell signals.

Let's dive into the details:

🔸Dynamic Mean and Volatility Bands The dynamic mean (μ) is calculated using the EWMA, giving more weight to recent prices but considering all historical data. This process closely resembles the Ornstein-Uhlenbeck (OU) process, which models the tendency of a stochastic variable (such as price) to revert to its mean over time. Volatility bands are plotted around the mean using standard deviation, forming the "cloud" that signals overbought or oversold conditions. The cloud adapts dynamically to price fluctuations and market volatility, making it a versatile tool for mean-reversion strategies. 🞘 How it works Step one: Calculate the dynamic mean (μ) The Ornstein-Uhlenbeck process describes how a variable, such as an asset's price, tends to revert to a long-term mean while subject to random fluctuations. In this indicator, the EWMA is used to compute the dynamic mean (μ), mimicking the mean-reverting behavior of the OU process. Use the EWMA formula to compute a weighted mean that adjusts to recent price movements. Assign exponentially decreasing weights to older data while giving more emphasis to current prices. Step two: Plot volatility bands Calculate the standard deviation of the price over a user-defined period to determine market volatility. Position the upper and lower bands around the mean by adding and subtracting a multiple of the standard deviation. 🞘 How to calculate Exponential Weighted Moving Average (EWMA)

The EWMA dynamically adjusts to recent price movements:

mu_t = lambda * mu_{t-1} + (1 - lambda) * P_t

Where mu_t is the mean at time t, lambda is the decay factor, and P_t is the price at time t. The higher the decay factor, the more weight is given to recent data.

Autocorrelation (ρ) and Standard Deviation (σ)

To measure mean reversion speed and volatility: rho = correlation(log(close), log(close ), length) Where rho is the autocorrelation of log returns over a specified period.

To calculate volatility:

sigma = stdev(close, length)

Where sigma is the standard deviation of the asset's closing price over a specified length.

Upper and Lower Bands

The upper and lower bands are calculated as follows:

upper_band = mu + (threshold * sigma)

lower_band = mu - (threshold * sigma)

Where threshold is a multiplier for the standard deviation, usually set to 2. These bands represent the range within which the price is expected to fluctuate, based on current volatility and the mean.

🞘 Code extract // Calculate Returns

returns = math.log(close / close )

// Calculate Long-Term Mean (μ) using EWMA over the entire dataset

var float ewma_mu = na // Initialize ewma_mu as 'na'

ewma_mu := na(ewma_mu ) ? close : decay_factor * ewma_mu + (1 - decay_factor) * close

mu = ewma_mu

// Calculate Autocorrelation at Lag 1

rho1 = ta.correlation(returns, returns , corr_length)

// Ensure rho1 is within valid range to avoid errors

rho1 := na(rho1) or rho1 <= 0 ? 0.0001 : rho1

// Calculate Speed of Mean Reversion (θ)

theta = -math.log(rho1)

// Calculate Volatility (σ)

sigma = ta.stdev(close, corr_length)

// Calculate Upper and Lower Bands

upper_band = mu + threshold * sigma

lower_band = mu - threshold * sigma

🔸Visualization via Table and Plotshapes

The table shows key statistics such as the current value of the dynamic mean (μ), the number of times the price has crossed the upper or lower bands, and the consecutive number of bars that the price has remained in an overbought or oversold state.

Plotshapes (diamonds) are used to signal buy and sell opportunities. A green diamond below the price suggests a buy signal when the price crosses below the lower band, and a red diamond above the price indicates a sell signal when the price crosses above the upper band.

The table and plotshapes provide a comprehensive visualization, combining both statistical and actionable information to aid decision-making.

🞘 Code extract // Reset consecutive_bars when price crosses the mean

var consecutive_bars = 0

if (close < mu and close >= mu) or (close > mu and close <= mu)

consecutive_bars := 0

else if math.abs(deviation) > 0

consecutive_bars := math.min(consecutive_bars + 1, dev_length)

transparency = math.max(0, math.min(100, 100 - (consecutive_bars * 100 / dev_length)))

🔶 INSTRUCTIONS

The Mean Reversion Cloud (Ornstein-Uhlenbeck) indicator can be set up by adding it to your TradingView chart and configuring parameters such as the decay factor, autocorrelation length, and volatility threshold to suit current market conditions. Look for price crossovers and deviations from the calculated mean for potential entry signals. Use the upper and lower bands as dynamic support/resistance levels for setting take profit and stop-loss orders. Combining this indicator with additional trend-following or momentum-based indicators can improve signal accuracy. Adjust settings for better mean-reversion detection and risk management.

🔸Step-by-Step Guidelines

🞘 Setting Up the Indicator

Adding the Indicator to the Chart:

Go to your TradingView chart.

Click on the "Indicators" button at the top.

Search for "Mean Reversion Cloud (Ornstein-Uhlenbeck)" in the indicators list.

Click on the indicator to add it to your chart.

Configuring the Indicator:

Open the indicator settings by clicking on the gear icon next to its name on the chart.

Decay Factor: Adjust the decay factor (λ) to control the responsiveness of the mean calculation. A higher value prioritizes recent data.

Autocorrelation Length: Set the autocorrelation length (θ) for calculating the speed of mean reversion. Longer lengths consider more historical data.

Threshold: Define the number of standard deviations for the upper and lower bands to determine how far price must deviate to trigger a signal.

Chart Setup:

Select the appropriate timeframe (e.g., 1-hour, daily) based on your trading strategy.

Consider using other indicators such as RSI or MACD to confirm buy and sell signals.

🞘 Understanding What to Look For on the Chart

Indicator Behavior:

Observe how the price interacts with the dynamic mean and volatility bands. The price staying within the bands suggests mean-reverting behavior, while crossing the bands signals potential entry points.

The indicator calculates overbought/oversold conditions based on deviation from the mean, highlighted by color-coded cloud areas on the chart.

Crossovers and Deviation:

Look for crossovers between the price and the mean (μ) or the bands. A bullish crossover occurs when the price crosses below the lower band, signaling a potential buying opportunity.

A bearish crossover occurs when the price crosses above the upper band, suggesting a potential sell signal.

Deviations from the mean indicate market extremes. A large deviation indicates that the price is far from the mean, suggesting a potential reversal.

Slope and Direction:

Pay attention to the slope of the mean (μ). A rising slope suggests bullish market conditions, while a declining slope signals a bearish market.

The steepness of the slope can indicate the strength of the mean-reversion trend.

🞘 Possible Entry Signals

Bullish Entry:

Crossover Entry: Enter a long position when the price crosses below the lower band with a positive deviation from the mean.

Confirmation Entry: Use additional indicators like RSI (above 50) or increasing volume to confirm the bullish signal.

Bearish Entry:

Crossover Entry: Enter a short position when the price crosses above the upper band with a negative deviation from the mean.

Confirmation Entry: Look for RSI (below 50) or decreasing volume to confirm the bearish signal.

Deviation Confirmation:

Enter trades when the deviation from the mean is significant, indicating that the price has strayed far from its expected value and is likely to revert.

🞘 Possible Take Profit Strategies

Static Take Profit Levels:

Set predefined take profit levels based on historical volatility, using the upper and lower bands as guides.

Place take profit orders near recent support/resistance levels, ensuring you're capitalizing on the mean-reversion behavior.

Trailing Stop Loss:

Use a trailing stop based on a percentage of the price deviation from the mean to lock in profits as the trend progresses.

Adjust the trailing stop dynamically along the calculated bands to protect profits as the price returns to the mean.

Deviation-Based Exits:

Exit when the deviation from the mean starts to decrease, signaling that the price is returning to its equilibrium.

🞘 Possible Stop-Loss Levels

Initial Stop Loss:

Place an initial stop loss outside the lower band (for long positions) or above the upper band (for short positions) to protect against excessive deviations.

Use a volatility-based buffer to avoid getting stopped out during normal price fluctuations.

Dynamic Stop Loss:

Move the stop loss closer to the mean as the price converges back towards equilibrium, reducing risk.

Adjust the stop loss dynamically along the bands to account for sudden market movements.

🞘 Additional Tips

Combine with Other Indicators:

Enhance your strategy by combining the Mean Reversion Cloud with momentum indicators like MACD, RSI, or Bollinger Bands to confirm market conditions.

Backtesting and Practice:

Backtest the indicator on historical data to understand how it performs in various market environments.

Practice using the indicator on a demo account before implementing it in live trading.

Market Awareness:

Keep an eye on market news and events that might cause extreme price movements. The indicator reacts to price data and might not account for news-driven events that can cause large deviations.

🔸Customize settings 🞘 Decay Factor (λ): Defines the weight assigned to recent price data in the calculation of the mean. A value closer to 1 places more emphasis on recent prices, while lower values create a smoother, more lagging mean.

🞘 Autocorrelation Length (θ): Sets the period for calculating the speed of mean reversion and volatility. Longer lengths capture more historical data, providing smoother calculations, while shorter lengths make the indicator more responsive.

🞘 Threshold (σ): Specifies the number of standard deviations used to create the upper and lower bands. Higher thresholds widen the bands, producing fewer signals, while lower thresholds tighten the bands for more frequent signals.

🞘 Max Gradient Length (γ): Determines the maximum number of consecutive bars for calculating the deviation gradient. This setting impacts the transparency of the plotted bands based on the length of deviation from the mean.

🔶 CONCLUSION

The Mean Reversion Cloud (Ornstein-Uhlenbeck) indicator offers a sophisticated approach to identifying mean-reversion opportunities by applying the Ornstein-Uhlenbeck stochastic process. This dynamic indicator calculates a responsive mean using an Exponentially Weighted Moving Average (EWMA) and plots volatility-based bands to highlight overbought and oversold conditions. By incorporating advanced statistical measures like autocorrelation and standard deviation, traders can better assess market extremes and potential reversals. The indicator’s ability to adapt to price behavior makes it a versatile tool for traders focused on both short-term price deviations and longer-term mean-reversion strategies. With its unique blend of statistical rigor and visual clarity, the Mean Reversion Cloud provides an invaluable tool for understanding and capitalizing on market inefficiencies.

Intramarket Difference Index StrategyHi Traders !!

The IDI Strategy:

In layman’s terms this strategy compares two indicators across markets and exploits their differences.

note: it is best the two markets are correlated as then we know we are trading a short to long term deviation from both markets' general trend with the assumption both markets will trend again sometime in the future thereby exhausting our trading opportunity.

📍 Import Notes:

This Strategy calculates trade position size independently (i.e. risk per trade is controlled in the user inputs tab), this means that the ‘Order size’ input in the ‘Properties’ tab will have no effect on the strategy. Why ? because this allows us to define custom position size algorithms which we can use to improve our risk management and equity growth over time. Here we have the option to have fixed quantity or fixed percentage of equity ATR (Average True Range) based stops in addition to the turtle trading position size algorithm.

‘Pyramiding’ does not work for this strategy’, similar to the order size input togeling this input will have no effect on the strategy as the strategy explicitly defines the maximum order size to be 1.

This strategy is not perfect, and as of writing of this post I have not traded this algo.

Always take your time to backtests and debug the strategy.

🔷 The IDI Strategy:

By default this strategy pulls data from your current TV chart and then compares it to the base market, be default BINANCE:BTCUSD . The strategy pulls SMA and RSI data from either market (we call this the difference data), standardizes the data (solving the different unit problem across markets) such that it is comparable and then differentiates the data, calling the result of this transformation and difference the Intramarket Difference (ID). The formula for the the ID is

ID = market1_diff_data - market2_diff_data (1)

Where

market(i)_diff_data = diff_data / ATR(j)_market(i)^0.5,

where i = {1, 2} and j = the natural numbers excluding 0

Formula (1) interpretation is the following

When ID > 0: this means the current market outperforms the base market

When ID = 0: Markets are at long run equilibrium

When ID < 0: this means the current market underperforms the base market

To form the strategy we define one of two strategy type’s which are Trend and Mean Revesion respectively.

🔸 Trend Case:

Given the ‘‘Strategy Type’’ is equal to TREND we define a threshold for which if the ID crosses over we go long and if the ID crosses under the negative of the threshold we go short.

The motivating idea is that the ID is an indicator of the two symbols being out of sync, and given we know volatility clustering, momentum and mean reversion of anomalies to be a stylised fact of financial data we can construct a trading premise. Let's first talk more about this premise.

For some markets (cryptocurrency markets - synthetic symbols in TV) the stylised fact of momentum is true, this means that higher momentum is followed by higher momentum, and given we know momentum to be a vector quantity (with magnitude and direction) this momentum can be both positive and negative i.e. when the ID crosses above some threshold we make an assumption it will continue in that direction for some time before executing back to its long run equilibrium of 0 which is a reasonable assumption to make if the market are correlated. For example for the BTCUSD - ETHUSD pair, if the ID > +threshold (inputs for MA and RSI based ID thresholds are found under the ‘‘INTRAMARKET DIFFERENCE INDEX’’ group’), ETHUSD outperforms BTCUSD, we assume the momentum to continue so we go long ETHUSD.

In the standard case we would exit the market when the IDI returns to its long run equilibrium of 0 (for the positive case the ID may return to 0 because ETH’s difference data may have decreased or BTC’s difference data may have increased). However in this strategy we will not define this as our exit condition, why ?

This is because we want to ‘‘let our winners run’’, to achieve this we define a trailing Donchian Channel stop loss (along with a fixed ATR based stop as our volatility proxy). If we were too use the 0 exit the strategy may print a buy signal (ID > +threshold in the simple case, market regimes may be used), return to 0 and then print another buy signal, and this process can loop may times, this high trade frequency means we fail capture the entire market move lowering our profit, furthermore on lower time frames this high trade frequencies mean we pay more transaction costs (due to price slippage, commission and big-ask spread) which means less profit.

By capturing the sum of many momentum moves we are essentially following the trend hence the trend following strategy type.

Here we also print the IDI (with default strategy settings with the MA difference type), we can see that by letting our winners run we may catch many valid momentum moves, that results in a larger final pnl that if we would otherwise exit based on the equilibrium condition(Valid trades are denoted by solid green and red arrows respectively and all other valid trades which occur within the original signal are light green and red small arrows).

another example...

Note: if you would like to plot the IDI separately copy and paste the following code in a new Pine Script indicator template.

indicator("IDI")

// INTRAMARKET INDEX

var string g_idi = "intramarket diffirence index"

ui_index_1 = input.symbol("BINANCE:BTCUSD", title = "Base market", group = g_idi)

// ui_index_2 = input.symbol("BINANCE:ETHUSD", title = "Quote Market", group = g_idi)

type = input.string("MA", title = "Differrencing Series", options = , group = g_idi)

ui_ma_lkb = input.int(24, title = "lookback of ma and volatility scaling constant", group = g_idi)

ui_rsi_lkb = input.int(14, title = "Lookback of RSI", group = g_idi)

ui_atr_lkb = input.int(300, title = "ATR lookback - Normalising value", group = g_idi)

ui_ma_threshold = input.float(5, title = "Threshold of Upward/Downward Trend (MA)", group = g_idi)

ui_rsi_threshold = input.float(20, title = "Threshold of Upward/Downward Trend (RSI)", group = g_idi)

//>>+----------------------------------------------------------------+}

// CUSTOM FUNCTIONS |

//<<+----------------------------------------------------------------+{

// construct UDT (User defined type) containing the IDI (Intramarket Difference Index) source values

// UDT will hold many variables / functions grouped under the UDT

type functions

float Close // close price

float ma // ma of symbol

float rsi // rsi of the asset

float atr // atr of the asset

// the security data

getUDTdata(symbol, malookback, rsilookback, atrlookback) =>

indexHighTF = barstate.isrealtime ? 1 : 0

= request.security(symbol, timeframe = timeframe.period,

expression = [close , // Instentiate UDT variables

ta.sma(close, malookback) ,

ta.rsi(close, rsilookback) ,

ta.atr(atrlookback) ])

data = functions.new(close_, ma_, rsi_, atr_)

data

// Intramerket Difference Index

idi(type, symbol1, malookback, rsilookback, atrlookback, mathreshold, rsithreshold) =>

threshold = float(na)

index1 = getUDTdata(symbol1, malookback, rsilookback, atrlookback)

index2 = getUDTdata(syminfo.tickerid, malookback, rsilookback, atrlookback)

// declare difference variables for both base and quote symbols, conditional on which difference type is selected

var diffindex1 = 0.0, var diffindex2 = 0.0,

// declare Intramarket Difference Index based on series type, note

// if > 0, index 2 outpreforms index 1, buy index 2 (momentum based) until equalibrium

// if < 0, index 2 underpreforms index 1, sell index 1 (momentum based) until equalibrium

// for idi to be valid both series must be stationary and normalised so both series hae he same scale

intramarket_difference = 0.0

if type == "MA"

threshold := mathreshold

diffindex1 := (index1.Close - index1.ma) / math.pow(index1.atr*malookback, 0.5)

diffindex2 := (index2.Close - index2.ma) / math.pow(index2.atr*malookback, 0.5)

intramarket_difference := diffindex2 - diffindex1

else if type == "RSI"

threshold := rsilookback

diffindex1 := index1.rsi

diffindex2 := index2.rsi

intramarket_difference := diffindex2 - diffindex1

//>>+----------------------------------------------------------------+}

// STRATEGY FUNCTIONS CALLS |

//<<+----------------------------------------------------------------+{

// plot the intramarket difference

= idi(type,

ui_index_1,

ui_ma_lkb,

ui_rsi_lkb,

ui_atr_lkb,

ui_ma_threshold,

ui_rsi_threshold)

//>>+----------------------------------------------------------------+}

plot(intramarket_difference, color = color.orange)

hline(type == "MA" ? ui_ma_threshold : ui_rsi_threshold, color = color.green)

hline(type == "MA" ? -ui_ma_threshold : -ui_rsi_threshold, color = color.red)

hline(0)

Note it is possible that after printing a buy the strategy then prints many sell signals before returning to a buy, which again has the same implication (less profit. Potentially because we exit early only for price to continue upwards hence missing the larger "trend"). The image below showcases this cenario and again, by allowing our winner to run we may capture more profit (theoretically).

This should be clear...

🔸 Mean Reversion Case:

We stated prior that mean reversion of anomalies is an standerdies fact of financial data, how can we exploit this ?

We exploit this by normalizing the ID by applying the Ehlers fisher transformation. The transformed data is then assumed to be approximately normally distributed. To form the strategy we employ the same logic as for the z score, if the FT normalized ID > 2.5 (< -2.5) we buy (short). Our exit conditions remain unchanged (fixed ATR stop and trailing Donchian Trailing stop)

🔷 Position Sizing:

If ‘‘Fixed Risk From Initial Balance’’ is toggled true this means we risk a fixed percentage of our initial balance, if false we risk a fixed percentage of our equity (current balance).

Note we also employ a volatility adjusted position sizing formula, the turtle training method which is defined as follows.

Turtle position size = (1/ r * ATR * DV) * C

Where,

r = risk factor coefficient (default is 20)

ATR(j) = risk proxy, over j times steps

DV = Dollar Volatility, where DV = (1/Asset Price) * Capital at Risk

🔷 Risk Management:

Correct money management means we can limit risk and increase reward (theoretically). Here we employ

Max loss and gain per day

Max loss per trade

Max number of consecutive losing trades until trade skip

To read more see the tooltips (info circle).

🔷 Take Profit:

By defualt the script uses a Donchain Channel as a trailing stop and take profit, In addition to this the script defines a fixed ATR stop losses (by defualt, this covers cases where the DC range may be to wide making a fixed ATR stop usefull), ATR take profits however are defined but optional.

ATR SL and TP defined for all trades

🔷 Hurst Regime (Regime Filter):

The Hurst Exponent (H) aims to segment the market into three different states, Trending (H > 0.5), Random Geometric Brownian Motion (H = 0.5) and Mean Reverting / Contrarian (H < 0.5). In my interpretation this can be used as a trend filter that eliminates market noise.

We utilize the trending and mean reverting based states, as extra conditions required for valid trades for both strategy types respectively, in the process increasing our trade entry quality.

🔷 Example model Architecture:

Here is an example of one configuration of this strategy, combining all aspects discussed in this post.

Future Updates

- Automation integration (next update)

ATR (Average True Range) mit relative/absolute Zahlen GERMAN:

Schnelle Zusammenfassung:

Dieses Skript basiert auf dem ATR-Indikator und wurde so angepasst, dass sowohl relative (%) als auch absolute Zahlen angezeigt werden. Es bietet eine Darstellung des ATR in absoluten und prozentualen Werten sowie multipliziert mit den Faktoren x2, x2.5 und x3. Diese Darstellung erleichtert die Festlegung von Stop-Kursen, insbesondere für Trailing Stops und Trailing Abstände.

Periode:

Die Periode ist einstellbar und definiert die Länge der Berechnung des ATR (Standardwert: 14).

Glättung: Es stehen verschiedene Methoden zur Auswahl, um die Daten zu glätten (RMA, SMA, EMA, WMA).

Berechnungen:

ATR (Absolute Zahl): Berechnung der durchschnittlichen wahren Reichweite (ATR) unter Verwendung der ausgewählten Glättungsmethode und Periode.

ATR (Prozentualer Wert): Berechnung des ATR als Prozentsatz des aktuellen Schlusskurses.

Multiplikation des ATR: Berechnung des ATR multipliziert mit den Faktoren 2, 2.5 und 3 zur Einschätzung verschiedener Handelsszenarien.

Darstellung:

Absoluter ATR-Wert: Darstellung der absoluten ATR-Werte in Blau.

Relative ATR-Werte (%): Darstellung der prozentualen ATR-Werte, ohne Linie in der Grafik (transparent).

Multiplizierte ATR-Werte (x2, x2.5, x3): Darstellung der multiplizierten ATR-Werte in den Farben Grün (x2), Orange (x2.5) und Lila (x3).

Textbeschriftungen: Für jeden absoluten ATR-Wert und seine Multiplikationen werden Textbeschriftungen links im Chart angezeigt.

Verwendung des Indikators:

Dieser Indikator unterstützt Trader und Analysten dabei, die durchschnittliche wahre Reichweite (ATR) eines Finanzinstruments zu verstehen und zu visualisieren. Die verschiedenen Multiplikationen des ATR ermöglichen es, potenzielle Preisbewegungen zu analysieren und Handelsstrategien zu entwickeln, die auf der Volatilität basieren.

Hinweis:

Dies ist meine persönliche Meinung und Einstellung. Dieses Skript stellt keine Bankberatung oder Anlageempfehlung dar. Die Nutzung erfolgt auf eigenes Risiko und Verantwortung des Nutzers.

----------------------------------------------------------------------

ENGLISH:

Quick Summary:

This script is based on the ATR (Average True Range) indicator and has been modified to display both relative (%) and absolute values. It provides a representation of ATR in absolute and percentage terms, as well as multiplied by factors x2, x2.5, and x3. This visualization aids in setting stop-loss levels, especially for trailing stops and trailing distances.

Period:

The period is adjustable and defines the length of the ATR calculation (default: 14).

Smoothing: Various methods are available to smooth the data (RMA, SMA, EMA, WMA).

Calculations:

ATR (Absolute Value): Computes the Average True Range using the selected smoothing method and period.

ATR (Percentage Value): Calculates the ATR as a percentage of the current closing price.

Multiplication of ATR: Computes the ATR multiplied by factors 2, 2.5, and 3 to assess different trading scenarios.

Visualization:

Absolute ATR Value: Displays the absolute ATR values in blue.

Relative ATR Values (%): Shows the ATR values as percentages, without lines in the chart (transparent).

Multiplied ATR Values (x2, x2.5, x3): Presents the multiplied ATR values in green (x2), orange (x2.5), and purple (x3).

Text Labels: Text labels are shown on the left side of the chart for each absolute ATR value and its multiples.

Use of the Indicator:

This indicator helps traders and analysts understand and visualize the Average True Range (ATR) of a financial instrument. The different multipliers of ATR allow for the analysis of potential price movements and the development of trading strategies based on volatility.

Disclaimer:

This represents my personal opinion and viewpoint. This script does not constitute bank advice or investment recommendations. Use it at your own risk and responsibility.

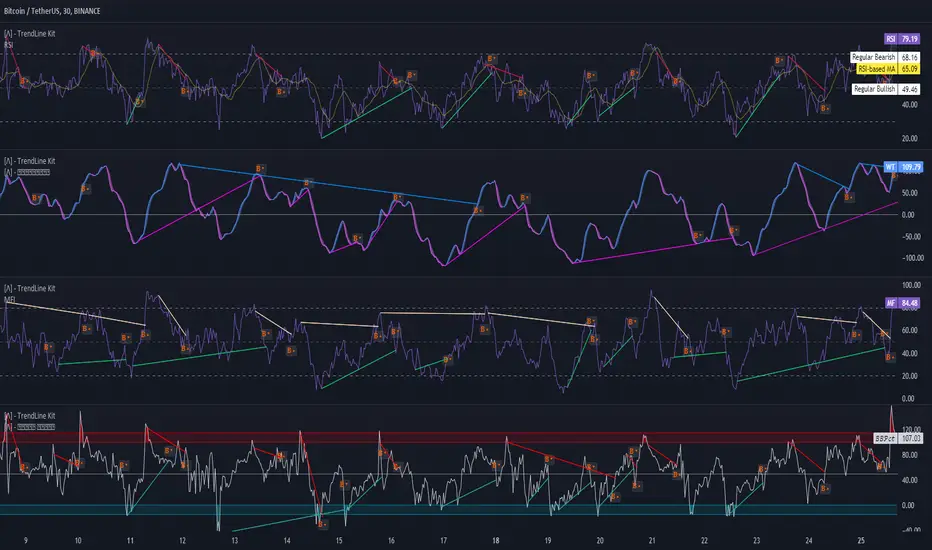

TrendLine Toolkit w/ Breaks (Real-Time)The TrendLine Toolkit script introduces an innovating capability by extending the conventional use of trendlines beyond price action to include oscillators and other technical indicators. This tool allows traders to automatically detect and display trendlines on any TradingView built-in oscillator or community-built script, offering a versatile approach to trend analysis. With breakout detection and real-time alerts, this script enhances the way traders interpret trends in various indicators.

🔲 Methodology

Trendlines are a fundamental tool in technical analysis used to identify and visualize the direction and strength of a price trend. They are drawn by connecting two or more significant points on a price chart, typically the highs or lows of consecutive price movements (pivots).

Drawing Trendlines:

Uptrend Line - Connects a series of higher lows. It signals an upward price trend.

Downtrend Line - Connects a series of lower highs. It indicates a downward price trend.

Support and Resistance:

Support Line - A trendline drawn under rising prices, indicating a level where buying interest is historically strong.

Resistance Line - A trendline drawn above falling prices, showing a level where selling interest historically prevails.

Identification of Trends:

Uptrend - Prices making higher highs and higher lows.

Downtrend - Prices making lower highs and lower lows.

Sideways (or Range-bound) - Prices moving within a horizontal range.

A trendline helps confirm the existence and direction of a trend, providing guidance in aligning with the prevailing market sentiment. Additionally, they are usually paired with breakout analysis, a breakout occurs when the price breaches a trendline. This signals a potential change in trend direction or an acceleration of the existing trend.

The script adapts this methodology to oscillators and other indicators. Instead of relying on price pivots, which can only be detected in retrospect, the script utilizes a trailing stop on the oscillator to identify potential swings in real-time, you may find more info about it here (SuperTrend toolkit) . We detect swings or pivots simply by testing for crosses between the indicator and its trailing stop.

type oscillator

float o = Oscillator Value

float s = Trailing Stop Value

oscillator osc = oscillator.new()

bool l = ta.crossunder(osc.o, osc.s) => Utilized as a formed high

bool h = ta.crossover (osc.o, osc.s) => Utilized as a formed low

This approach enables the algorithm to detect trendlines between consecutive pivot highs or lows on the oscillator itself, providing a dynamic and immediate representation of trend dynamics.

🔲 Breakout Detection

The script goes beyond trendline creation by incorporating breakout detection directly within the oscillator. After identifying a trendline, the algorithm continuously monitors the oscillator for potential breakouts, signaling shifts in market sentiment.

🔲 Setup Guide

A simple example on one of my public scripts, Z-Score Heikin-Ashi Transformed

🔲 Settings

Source - Choose an oscillator source of which to base the Toolkit on.

Zeroing - The Mid-Line value of the oscillator, for example RSI & MFI use 50.

Sensitivity - Calibrates the Sensitivity of which TrendLines are detected, higher values result in more detections.

🔲 Alerts

Bearish TrendLine

Bullish TrendLine

Bearish Breakout

Bullish Breakout

As well as the option to trigger 'any alert' call.

By integrating trendline analysis into oscillators, this Toolkit enhances the capabilities of technical analysis, bringing a dynamic and comprehensive approach to identifying trends, support/resistance levels, and breakout signals across various indicators.

Divergence Toolkit (Real-Time)The Divergence Toolkit is designed to automatically detect divergences between the price of an underlying asset and any other @TradingView built-in or community-built indicator or script. This algorithm provides a comprehensive solution for identifying both regular and hidden divergences, empowering traders with valuable insights into potential trend reversals.

🔲 Methodology

Divergences occur when there is a disagreement between the price action of an asset and the corresponding indicator. Let's review the conditions for regular and hidden divergences.

Regular divergences indicate a potential reversal in the current trend.

Regular Bullish Divergence

Price Action - Forms a lower low.

Indicator - Forms a higher low.

Interpretation - Suggests that while the price is making new lows, the indicator is showing increasing strength, signaling a potential upward reversal.

Regular Bearish Divergence

Price Action - Forms a higher high.

Indicator - Forms a lower high.

Interpretation - Indicates that despite the price making new highs, the indicator is weakening, hinting at a potential downward reversal.

Hidden divergences indicate a potential continuation of the existing trend.

Hidden Bullish Divergence

Price Action - Forms a higher low.

Indicator - Forms a lower low.

Interpretation - Suggests that even though the price is retracing, the indicator shows increasing strength, indicating a potential continuation of the upward trend.

Hidden Bearish Divergence

Price Action - Forms a lower high.

Indicator - Forms a higher high.

Interpretation - Indicates that despite a retracement in price, the indicator is still strong, signaling a potential continuation of the downward trend.

In both regular and hidden divergences, the key is to observe the relationship between the price action and the indicator. Divergences can provide valuable insights into potential trend reversals or continuations.

The methodology employed in this script involves the detection of divergences through conditional price levels rather than relying on detected pivots. Traditionally, divergences are created by identifying pivots in both the underlying asset and the oscillator. However, this script employs a trailing stop on the oscillator to detect potential swings, providing a real-time approach to identifying divergences, you may find more info about it here (SuperTrend Toolkit) . We detect swings or pivots simply by testing for crosses between the indicator and its trailing stop.

type oscillator

float o = Oscillator Value

float s = Trailing Stop Value

oscillator osc = oscillator.new()

bool l = ta.crossunder(osc.o, osc.s) => Utilized as a formed high

bool h = ta.crossover (osc.o, osc.s) => Utilized as a formed low

// Note: these conditions alone could cause repainting when they are met but canceled at a later time before the bar closes. Hence, we wait for a confirmed bar.

// The script also includes the option to immediately alert when the conditions are met, if you choose so.

By testing for conditional price levels, the script achieves similar outcomes without the delays associated with pivot-based methods.

type bar

float o = open

float h = high

float l = low

float c = close

bar b = bar.new()

bool hi = b.h < b.h => A higher price level has been created

bool lo = b.l > b.l => A lower price level has been created

// Note: These conditions do not check for certain price swings hence they may seldom result in inaccurate detection.

🔲 Setup Guide

A simple example on one of my public scripts, Standardized MACD

🔲 Utility

We may auto-detect divergences to spot trend reversals & continuations.

🔲 Settings

Source - Choose an oscillator source of which to base the Toolkit on.

Zeroing - The Mid-Line value of the oscillator, for example RSI & MFI use 50.

Sensitivity - Calibrates the sensitivity of which Divergencies are detected, higher values result in more detections but less accuracy.

Lifetime - Maximum timespan to detect a Divergence.

Repaint - Switched on, the script will trigger Divergencies as they happen in Real-Time, could cause repainting when the conditions are met but canceled at a later time before bar closes.

🔲 Alerts

Bearish Divergence

Bullish Divergence

Bearish Hidden Divergence

Bullish Hidden Divergence

As well as the option to trigger 'any alert' call.

The Divergence Toolkit provides traders with a dynamic tool for spotting potential trend reversals and continuations. Its innovative approach to real-time divergence detection enhances the timeliness of identifying market opportunities.

RSI & Backed-Weighted MA StrategyRSI & MA Strategy :

INTRODUCTION :

This strategy is based on two well-known indicators that work best together: the Relative Strength Index (RSI) and the Moving Average (MA). We're going to use the RSI as a trend-follower indicator, rather than a reversal indicator as most are used to. To the signals sent by the RSI, we'll add a condition on the chart's MA, filtering out irrelevant signals and considerably increasing our winning rate. This is a medium/long-term strategy. There's also a money management method enabling us to reinvest part of the profits or reduce the size of orders in the event of substantial losses.

RSI :

The RSI is one of the best-known and most widely used indicators in trading. Its purpose is to warn traders when an asset is overbought or oversold. It was designed to send reversal signals, but we're going to use it as a trend indicator by increasing its length to 20. The RSI formula is as follows :

RSI (n) = 100 - (100 / (1 + (H (n)/L (n))))

With n the length of the RSI, H(n) the average of days closing above the open and L(n) the average of days closing below the open.

MA :

The Moving Average is also widely used in technical analysis, to smooth out variations in an asset. The SMA formula is as follows :

SMA (n) = (P1 + P2 + ... + Pn) / n

where n is the length of the MA.

However, an SMA does not weight any of its terms, which means that the price 10 days ago has the same importance as the price 2 days ago or today's price... That's why in this strategy we use a RWMA, i.e. a back-weighted moving average. It weights old prices more heavily than new ones. This will enable us to limit the impact of short-term variations and focus on the trend that was dominating. The RWMA used weights :

The 4 most recent terms by : 100 / (4+(n-4)*1.30)

The other oldest terms by : weight_4_first_term*1.30

So the older terms are weighted 1.30 more than the more recent ones. The moving average thus traces a trend that accentuates past values and limits the noise of short-term variations.

PARAMETERS :

RSI Length : Lenght of RSI. Default is 20.

MA Type : Choice between a SMA or a RWMA which permits to minimize the impact of short term reversal. Default is RWMA.

MA Length : Length of the selected MA. Default is 19.

RSI Long Signal : Minimum value of RSI to send a LONG signal. Default is 60.

RSI Short signal : Maximum value of RSI to send a SHORT signal. Default is 40.

ROC MA Long Signal : Maximum value of Rate of Change MA to send a LONG signal. Default is 0.

ROC MA Short signal : Minimum value of Rate of Change MA to send a SHORT signal. Default is 0.

TP activation in multiple of ATR : Threshold value to trigger trailing stop Take Profit. This threshold is calculated as multiple of the ATR (Average True Range). Default value is 5 meaning that to trigger the trailing TP the price need to move 5*ATR in the right direction.

Trailing TP in percentage : Percentage value of trailing Take Profit. This Trailing TP follows the profit if it increases, remaining selected percentage below it, but stops if the profit decreases. Default is 3%.

Fixed Ratio : This is the amount of gain or loss at which the order quantity is changed. Default is 400, which means that for each $400 gain or loss, the order size is increased or decreased by a user-selected amount.

Increasing Order Amount : This is the amount to be added to or subtracted from orders when the fixed ratio is reached. The default is $200, which means that for every $400 gain, $200 is reinvested in the strategy. On the other hand, for every $400 loss, the order size is reduced by $200.

Initial capital : $1000

Fees : Interactive Broker fees apply to this strategy. They are set at 0.18% of the trade value.

Slippage : 3 ticks or $0.03 per trade. Corresponds to the latency time between the moment the signal is received and the moment the order is executed by the broker.

Important : A bot has been used to test the different parameters and determine which ones maximize return while limiting drawdown. This strategy is the most optimal on BITSTAMP:ETHUSD with a timeframe set to 6h. Parameters are set as follows :

MA type: RWMA

MA Length: 19

RSI Long Signal: >60

RSI Short Signal : <40

ROC MA Long Signal : <0

ROC MA Short Signal : >0

TP Activation in multiple ATR : 5

Trailing TP in percentage : 3

ENTER RULES :

The principle is very simple:

If the asset is overbought after a bear market, we are LONG.

If the asset is oversold after a bull market, we are SHORT.

We have defined a bear market as follows : Rate of Change (20) RWMA < 0

We have defined a bull market as follows : Rate of Change (20) RWMA > 0

The Rate of Change is calculated using this formula : (RWMA/RWMA(20) - 1)*100

Overbought is defined as follows : RSI > 60

Oversold is defined as follows : RSI < 40

LONG CONDITION :

RSI > 60 and (RWMA/RWMA(20) - 1)*100 < -1

SHORT CONDITION :

RSI < 40 and (RWMA/RWMA(20) - 1)*100 > 1

EXIT RULES FOR WINNING TRADE :

We have a trailing TP allowing us to exit once the price has reached the "TP Activation in multiple ATR" parameter, i.e. 5*ATR by default in the profit direction. TP trailing is triggered at this point, not limiting our gains, and securing our profits at 3% below this trigger threshold.

Remember that the True Range is : maximum(H-L, H-C(1), C-L(1))

with C : Close, H : High, L : Low

The Average True Range is therefore the average of these TRs over a length defined by default in the strategy, i.e. 20.

RISK MANAGEMENT :

This strategy may incur losses. The method for limiting losses is to set a Stop Loss equal to 3*ATR. This means that if the price moves against our position and reaches three times the ATR, we exit with a loss.

Sometimes the ATR can result in a SL set below 10% of the trade value, which is not acceptable. In this case, we set the SL at 10%, limiting losses to a maximum of 10%.

MONEY MANAGEMENT :

The fixed ratio method was used to manage our gains and losses. For each gain of an amount equal to the value of the fixed ratio, we increase the order size by a value defined by the user in the "Increasing order amount" parameter. Similarly, each time we lose an amount equal to the value of the fixed ratio, we decrease the order size by the same user-defined value. This strategy increases both performance and drawdown.

Enjoy the strategy and don't forget to take the trade :)

Moving Average SARHello Traders,

Today, I have brought to you an indicator that utilizes the Parabolic SAR.

To begin with, the Parabolic SAR is an indicator that trails the price in the form of a parabola, seeking out Stop And Reverse points.

The indicator I present merges the calculation formula of the Parabolic SAR with the Moving Average.

One aspect I pondered over was how to determine the starting point of this SAR. Trailing the price flow with the logic set by the moving average was fine, but the question was where to begin.

My approach involves a variable I call 'sensitiveness,' which automatically adjusts the length according to the timeframe you are observing. Using pinescript's math.ceil, I formulated: