Liquidation Strategy📈 It enters a long trade when long liquidation spikes above a set threshold.

📉 It enters a short trade when short liquidation drops below the negative threshold.

🧮 It optionally filters entries using an EMA multiplier.

🔁 It exits long when RSI crosses below its smoothed version.

🔄 It exits short when RSI crosses above its smoothed version.

🔗 It requires linking to the Liquidations indicator on Bybit or OKX charts.

Oscylatory

DNSE VN301!, ADX Momentum StrategyDiscover the tailored Pine Script for trading VN30F1M Futures Contracts intraday.

This strategy applies the Statistical Method (IQR) to break down the components of the ADX, calculating the threshold of "normal" momentum fluctuations in price to identify potential breakouts for entry and exit signals. The script automatically closes all positions by 14:30 to avoid overnight holdings.

www.tradingview.com

Settings & Backtest Results:

- Chart: 30-minute timeframe

- Initial capital: VND 100 million

- Position size: 4 contracts per trade (includes trading fees, excludes tax)

- Backtest period: Sep-2021 to Sep-2025

- Return: over 270% (with 5 ticks slippage)

- Trades executed: 1,000+

- Win rate: ~40%

- Profit factor: 1.2

Default Script Settings:

Calculates the acceleration of changes in the +DI and -DI components of the ADX, using IQR to define "normal" momentum fluctuations (adjustable via Lookback period).

Calculates the difference between each bar’s Open and Close prices, using IQR to define "normal" gaps (adjustable via Lookback period).

Entry & Exit Conditions:

Entry Long: Change in +DI or -DI > Avg IQR Value AND Close Price > Previous Close

Exit Long: (all 4 conditions must be met)

- Change in +DI or -DI > Avg IQR Value

- RSI < Previous RSI

- Close–Open Gap > Avg IQR Gap

- Close Price < Previous Close

Entry Short: Change in +DI or -DI > Avg IQR Value AND Close Price < Previous Close

Exit Short: (all 4 conditions must be met)

- Change in +DI or -DI > Avg IQR Value

- RSI > Previous RSI

- Close–Open Gap > Avg IQR Gap

- Close Price > Previous Close

Disclaimers:

Trading futures contracts carries a high degree of risk, and price movements can be highly volatile. This script is intended as a reference tool only. It should be used by individuals who fully understand futures trading, have assessed their own risk tolerance, and are knowledgeable about the strategy’s logic.

All investment decisions are the sole responsibility of the user. DNSE bears no liability for any potential losses incurred from applying this strategy in real trading. Past performance does not guarantee future results. Please contact us directly if you have specific questions about this script.

Liquidation Strategy💣 Liquidation Strategy (High-Level Overview + Usage)

This strategy is built to trade extreme liquidation events on crypto exchanges like Bybit or OKX, using TradingView’s Liquidations indicator as input.

🔧 Core Logic

Long entries: Triggered when long liquidation values spike above a set threshold.

Short entries: Triggered when short liquidation values drop below a negative threshold.

Optional EMA filter ensures liquidation values are significantly above/below their moving average.

RSI crossover logic is used to exit trades.

🛠️ Usage Instructions

Add the Liquidations Indicator: Go to TradingView → Indicators → Search for “Liquidations” under the Financials section.

Select the Correct Chart: Use a chart from Bybit or OKX, as these exchanges provide liquidation data.

Link the Data Sources: In the strategy settings, set: Long Liquidation Data to the long liquidation series from the indicator. Short Liquidation Data to the short liquidation series.

Overlay the Strategy: You can overlay this strategy directly on the Liquidations indicator for better visual alignment.

RSI Momentum Trend MM with Risk Per Trade [MTF]This is a comprehensive and highly customizable trend-following strategy based on RSI momentum. The core logic identifies strong directional moves when the RSI crosses user-defined thresholds, combined with an EMA trend confirmation. It is designed for traders who want granular control over their strategy's parameters, from signal generation to risk management and exit logic.

This script evolves a simple concept into a powerful backtesting tool, allowing you to test various money management and trade management theories across different timeframes.

Key Features

- RSI Momentum Signals: Uses RSI crosses above a "Positive" level or below a "Negative" level to generate trend signals. An EMA filter ensures entries align with the immediate trend.

- Multi-Timeframe (MTF) Analysis: The core RSI and EMA signals can be calculated on a higher timeframe (e.g., using 4H signals to trade on a 1H chart) to align trades with the larger trend. This feature helps to reduce noise and improve signal quality.

Advanced Money Management

- Risk per Trade %: Calculate position size based on a fixed percentage of equity you want to risk per trade.

- Full Equity: A more aggressive option to open each position with 100% of the available strategy equity.

Flexible Exit Logic: Choose from three distinct exit strategies to match your trading style

- Percentage (%) Based: Set a fixed Stop Loss and Take Profit as a percentage of the entry price.

- ATR Multiplier: Base your Stop Loss and Take Profit on the Average True Range (ATR), making your exits adaptive to market volatility.

- Trend Reversal: A true trend-following mode. A long position is held until an opposite "Negative" signal appears, and a short position is held until a "Positive" signal appears. This allows you to "let your winners run."

Backtest Date Range Filter: Easily configure a start and end date to backtest the strategy's performance during specific market periods (e.g., bull markets, bear markets, or high-volatility periods).

How to Use

RSI Settings

- Higher Timeframe: Set the timeframe for signal calculation. This must be higher than your chart's timeframe.

- RSI Length, Positive above, Negative below: Configure the core parameters for the RSI signals.

Money Management

Position Sizing Mode

- Choose "Risk per Trade" to use the Risk per Trade (%) input for precise risk control.

- Choose "Full Equity" to use 100% of your capital for each trade.

- Risk per Trade (%): Define the percentage of your equity to risk on a single trade (only works with the corresponding sizing mode).

SL/TP Calculation Mode

Select your preferred exit method from the dropdown. The strategy will automatically use the relevant inputs (e.g., % values, ATR Multiplier values, or the trend reversal logic).

Backtest Period Settings

Use the Start Date and End Date inputs to isolate a specific period for your backtest analysis.

License & Disclaimer

© waranyu.trkm — MIT License.

This script is for educational purposes only and should not be considered financial advice. Trading involves significant risk, and past performance is not indicative of future results. Always conduct your own research and risk assessment before making any trading decisions.

W Bottom Reversal Strategy W Bottom Reversal Strategy (15m-close entries; intrabar TP; daily MACD exit; JSON alerts v49.3-expire2)

Overview

A precision reversal strategy designed for 15-minute charts on liquid symbols. It detects a capitulation-and-stabilization “W” base using 1-hour (1H) context, confirms momentum improvement, then enters only on bar close to avoid early/“ghost” signals. Exits combine a fast intrabar take-profit (~2.7%) with a daily MACD risk-off exit that closes positions when higher-timeframe momentum turns against the setup.

How it works (high-level, matching code)

1H volatility + oversold gate (arming)

Compute 1H Bollinger-style bands (basis = SMA(close, bbLength=20), stdev multiplier bbMult=2.0).

Arm the setup when a 1H bar closes with price < 1H lower band and 1H RSI( rsiLength=14 ) < rsiThreshold (default 20.0).

1H momentum flip → pending entry

When a new 1H bar closes and 1H MACD line (EMA12−EMA26) crosses above 0 while armed and flat, set an entryPending flag.

This does not enter yet—it prepares a confirmed, bar-close entry on the lower timeframe.

Bar-close execution on the chart timeframe (15m)

On the next 15m bar close (or within N bars, see below) and still flat, fire the entry using a limit order at close × (1 − 0.00001) (≈ 0.001% below close) to reduce slippage and maintain chart/alert alignment.

Anti-late filter (no stale triggers)

If the pending entry doesn’t trigger within N chart bars (input: “Pending entry valid for N chart bars”, default 1, range 1–8), it expires and the arm state resets. This prevents late fills long after the 1H confirmation.

Exit logic

Primary: Standing intrabar take-profit at +2.7% from the average entry price (managed via strategy.exit limit).

Risk-off: On daily bar close, if Daily MACD line (EMA12−EMA26) crosses under 0, close the position (flat on daily momentum flip).

Default Properties (used for this publication)

Timeframe: 15m (with 1H and Daily higher-timeframe confirmations via request.security)

Initial capital: $10,000

Position sizing: Percent of equity = 10% per trade (enters only when flat; no stacking while in a position)

Commission: 0.05% per side

Slippage: Recommend 1 tick in Strategy Properties for realistic fills

Inputs exposed:

BB Length: 20 • BB Multiplier: 2.0

RSI Length: 14 • RSI Threshold: 20.0

MACD: Short 12, Long 26, Signal 9 (signal kept for compatibility; logic uses MACD line vs 0)

Pending entry valid for N chart bars: default 1 (1–8)

Execution behavior (per code):

calc_on_every_tick = false (evaluates on bar close)

process_orders_on_close = true (orders placed at bar close)

Limit entry at close −0.001%

Intrabar TP (2.7%)

Daily risk-off exit on MACD<0 at daily bar close

Alerts (exact behavior in code)

Uses alert() function calls with standardized JSON.

Set your alert to “Only alert() function calls” and “Once per bar close.”

Two events are emitted:

LONG_CONFIRMED on entry fire (15m bar close)

EXIT_CONFIRMED_DAILY_MACD on daily MACD<0 (daily bar close)

JSON fields include: event, version ("v49.3-expire2"), symbol, interval, price, and time.

How to use

Apply on liquid tickers (tight spreads, healthy volume).

Keep defaults initially; run across a broad, liquid watchlist to gather a proper sample.

For automation, route bar-close alerts to your executor; confirm broker lot/route settings and that limit orders at close −0.001% are acceptable.

Expect fewer signals in powerful trends; the daily risk-off helps cut failed bases.

Methodology & expectations (results transparency)

Evaluate on a dataset yielding 100+ trades before drawing conclusions.

Keep commission & slippage enabled (see defaults).

Risk sizing: With 10% of equity per trade and flat-to-flat entries, exposure aligns with typical 5–10% guidance.

No performance guarantees—outcomes depend on symbol selection, volatility regime, news, and execution quality.

Originality & value (vendor justification)

While it uses familiar building blocks (BB/RSI/MACD), the edge comes from the 1H volatility + oversold arming, 1H momentum flip, strict 15m bar-close limit execution, and the N-bar pending expiry that prevents stale triggers—paired with a dual-exit design (intrabar TP + daily risk-off). The focus is on reducing premature fills, keeping alerts 1:1 with chart marks, and capturing the first impulse out of a W-base.

Disclaimers

For educational purposes only; not financial advice. Paper-test first. Verify alerts, fills, and symbol liquidity with your broker before live use.

Changelog: v49.3-expire2 — Bar-close limit entries; anti-late pending window; standardized JSON alerts; intrabar 2.7% TP; daily MACD risk-off exit.

Daily CMO + Volume Intraday Strategy v6 by Subirrmomentum strategy. buy on next hourly candle after signal. target 5%, sl 1%

Supertrend [TradingConToto]Supertrend — ADX/DI + EMA Gap + Breakout (with Mobile UI)

What makes it original

Supertrend combines trend strength (ADX/DI), multi-timeframe bias (EMA63 and EMA 200D equivalent), a structural filter based on the distance between EMA2400 and EMA4800 expressed in ATR units, and a momentum confirmation through a previous high breakout.

This is not a random mashup — it’s a sequence of filters designed to reduce trades in ranging markets and prioritize mature trends:

Direction: +DI > -DI (trend led by buyers).

Strength: ADX > mean(ADX) (avoids weak, choppy phases).

Short-term bias: Close > EMA63.

Long-term bias: Close > EMA4800 ≈ EMA200 daily on H1.

Momentum: Close > High (immediate breakout).

Structure: (EMA2400 − EMA4800) > k·ATR (ensures separation in ATR units, filters out flat phases).

Entries & exits

Entry: when all six conditions are met and no open position exists.

Exit: if +DI < -DI or Close < EMA63.

Visuals: EMA63 is painted green while in position and red otherwise, with a supertrend-style band; “BUY” labels appear below the green band and “SELL” labels above the red band.

UI: includes a compact table (mobile-friendly) showing the state of each condition.

Default parameters used in this publication

Initial capital: 10,000

Position size: 10% of equity (≤10% per trade is considered sustainable).

Commission: 0.01% per side (adjust to your broker/market).

Slippage: 1 tick

Pyramiding: 0 (only one position at a time)

Adjust commission/slippage to match your market. For US equities, commissions are often per share; for spot crypto, 0.10–0.20% total is common. I publish with 0.01% per side as a conservative example to avoid overestimating results.

Recommended backtest dataset

Timeframe: H1

Multi-cycle window (e.g. 2015–today)

Symbols with high liquidity (e.g. NASDAQ-100 large caps, or BTC/ETH spot) to generate 100+ trades. Avoid cherry-picked short windows.

Why each filter matters

+DI > -DI + ADX > mean: reduce counter-trend trades and weak signals.

Close > EMA63 + Close > EMA4800: enforce trend alignment in short and long horizons.

Breakout High : requires immediate momentum, avoids early entries.

EMA gap in ATR units: blocks flat or compressed structures where EMA200D aligns with price.

Limitations

The breakout filter may skip healthy pullbacks; the design prioritizes continuation over perfect entry price.

No fixed trailing stop/TP; exits depend on trend degradation via DI/EMA63.

Results vary with real costs (commissions, slippage, funding). Adjust defaults to your broker.

How to use

Apply it on a clean chart (no other indicators when publishing).

Keep in mind the default parameters above; if you change them, mention it in your notes and use the same values in the Strategy Tester.

Ensure your dataset produces 100+ trades for statistical validity.

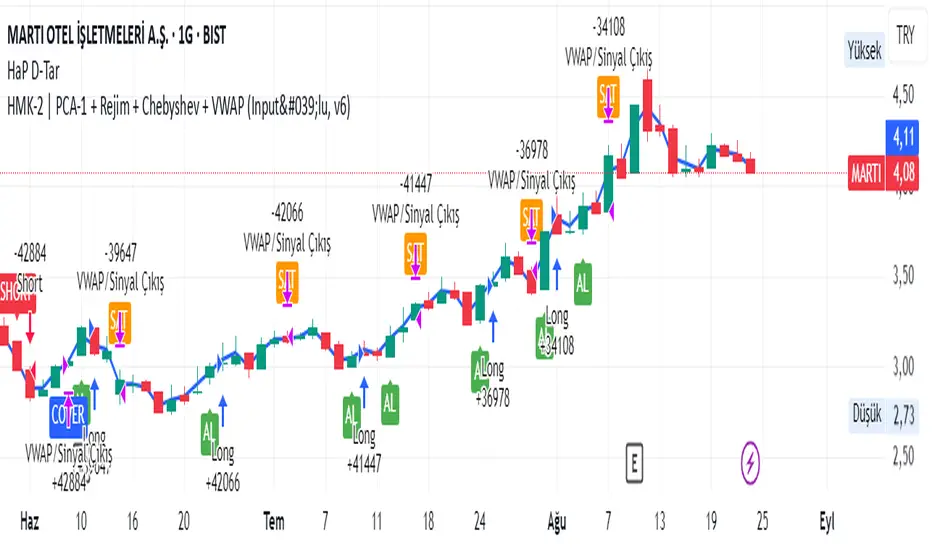

HMK-2 | PCA-1 + Rejim + Chebyshev + VWAP (Input'lu, v6)📌 HMK-2 | PCA-1 + Regime + Chebyshev + VWAP Strategy

1️⃣ Core Structure

Instead of relying on a single indicator, this system uses the Z-Score normalized average of three oscillators (RSI, MFI, ROC).

Signal (PCA-1):

RSI(14), MFI(14), ROC(5) → each is converted into a z-score.

Their average becomes the “composite signal,” our PCA-1 value.

Trend direction: If the Z-score EMA is rising → trend UP. If falling → trend DOWN.

2️⃣ Side Filters

Regime Filter (ADX + EMA)

ADX is calculated manually.

If ADX > 20 → trend exists → a 50-period EMA of this value smooths it.

This turns “trend regime” into a probability between 0–1.

Chebyshev Filter

A return series is checked against mean ± k*sigma bands.

If the return is within this band → valid signal. Extreme moves are filtered out.

VWAP Filter

Long trades: price must be above VWAP.

Short trades: price must be below VWAP.

Trades are only taken on the correct side of institutional cost averages.

3️⃣ Entry Conditions

Long:

PCA-1 signal crosses above threshold.

Trend Up + Regime OK + Chebyshev OK + Above VWAP.

Short:

PCA-1 signal crosses below threshold.

Trend Down + Regime OK + Chebyshev OK + Below VWAP.

4️⃣ Exit Mechanism

Main Exit: ATR-based stop/target.

Stop = entry price – ATR × (SL factor).

Take profit = entry price + ATR × (TP factor).

Additional Exit:

If price crosses to the opposite side of VWAP.

If PCA-1 signal crosses zero.

👉 Prevents trades from being locked, makes exits adaptive.

5️⃣ Labels / Visualization

AL / SHORT → entry points.

SAT / COVER → exit points.

VWAP line plotted in blue.

🧩 Strategy Features

Optimizable parameters:

Z-window (zWin)

Threshold

Chebyshev factor

ATR stop/target multipliers

This system works with:

Disciplined core (PCA-1 signal)

Triple protection (Regime + Chebyshev + VWAP)

Adaptive exits (ATR + VWAP/signal cross)

👉 Not a “single-indicator robot,” but a multi-filtered trade direction engine.

💡 Final Note

This is a base model of the system — open for further development.

I’ve shared the logic to give you a roadmap.

If you spot errors, fix them → that’s how you’ll improve it.

Don’t waste time asking me questions — refine and build it better yourselves.

Wishing you profitable trades. Stay well 🙏

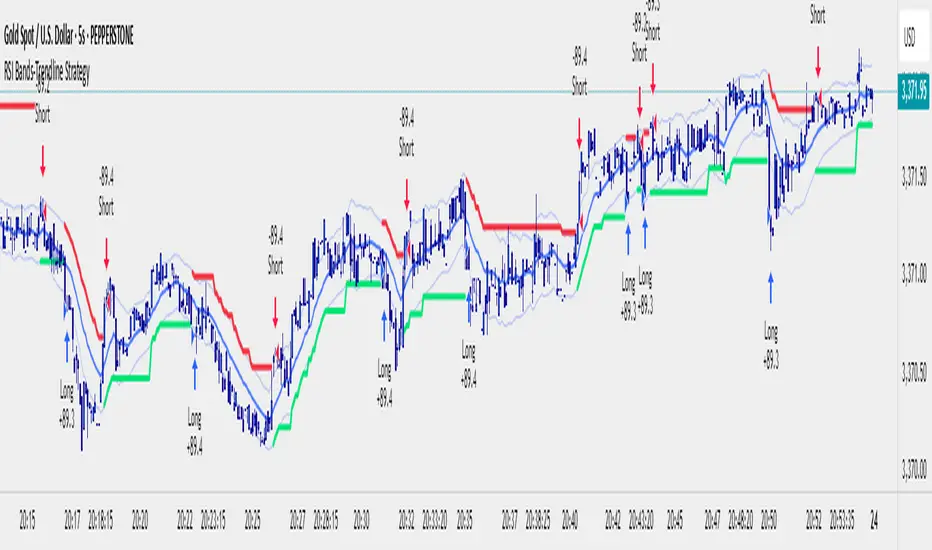

RSI Bands With RSI - ATR Trend StrategyRSI Bands With RSI-ATR Trend Line Strategy

Overview

A trend-following strategy that combines RSI regime detection with a smoothed baseline and ATR bands. Works similar to Supertrend: the line flips bullish or bearish only when price closes beyond the band, aiming to filter noise and catch clean moves.

How It Works

RSI above 50 = bullish bias, below 50 = bearish bias

A dynamic baseline is calculated from RSI and price range, then smoothed

ATR bands expand/contract with volatility

Close above the upper band → bullish flip → long entry

Close below the lower band → bearish flip → short entry

Between bands → prior trend continues

Features

Automatic Buy/Sell entries on confirmed flips

Configurable RSI, Smoothing, ATR, and Multiplier inputs

Visual trend line (green = bull, red = bear)

Backtest ready with initial capital and commission settings

Best Use Cases

Trending markets across Forex, Crypto, Indices, Commodities

Works on multiple timeframes (higher TFs = cleaner flips)

Flexible settings for conservative swing trading or aggressive scalping

⚠️ For testing/education only. Always manage risk and confirm with higher-timeframe or structure filters.

BDNS ORB Strategy v3BDNS Opening Range Breakout Strategy

What This Strategy Does This strategy implements an Opening Range Breakout (ORB) system that identifies the high and low prices during a customizable opening period, then trades breakouts above or below these levels with momentum confirmation. The strategy goes beyond basic ORB concepts by incorporating ADX momentum filtering, VWAP directional bias, dynamic position sizing, and sophisticated exit management including breakeven moves and trailing stops.

Core Strategy Logic

Opening Range Definition: The strategy tracks price action during a user-defined opening period (default: 9:30-9:35 AM ET for 5 minutes). During this time, blue horizontal lines appear marking the session high and low. A yellow background highlights this opening range period.

Breakout Detection: After the opening range completes, green and red horizontal lines appear showing the actual entry levels - these are offset from the range boundaries by a configurable number of ticks (default: 24 ticks) to filter out false breakouts and ensure committed moves.

Entry Conditions: Trades trigger when price breaks through these offset levels during the trading window (green background, default until 10:30 AM ET), but only when:

ADX momentum indicator exceeds threshold (default 24.0) in the breakout direction

Price relationship to VWAP confirms directional bias (when VWAP filter enabled)

Daily trade limits haven't been reached

Large range filtering conditions are met

Visual Elements and Usage

Range Lines: Blue lines show the actual opening range boundaries. These appear immediately when the opening session begins.

Entry Levels: Green (long) and red (short) lines show where trades will trigger, appearing after the opening range completes.

Information Table: A data table appears in the top-right showing real-time strategy status including range size in ticks, ADX readings, filter status, trade counts, and momentum conditions.

Position Management:

When in a trade, colored circles appear showing:

Lime circles: Long position targets (T1, T2, T3)

Orange circles: Short position targets

Red circles: Stop loss levels

Blue crosses: Breakeven levels (when that feature activates)

Purple lines: Trailing stop levels (when position 3 trailing activates)

Background Colors:

Yellow: Opening range session active

Green: Trading window active

Purple: Large range day detected

Gray: Large range day being skipped

Position Management System

The strategy uses a three-tier exit approach:

Position 1: Takes partial profits at first target (default 50% of range size)

Position 2: Exits at second target (default 100% of range size)

Position 3: Either exits at third target or uses trailing stop after Position 2 wins

Breakeven Feature: When enabled and price reaches the breakeven trigger level, all stop losses move to a more favorable breakeven level instead of the original stop, protecting against giving back profits.

Trailing Stop System: After Position 2 hits its target, Position 3 automatically switches to a trailing stop that moves in the trader's favor as price continues trending.

Customization for Different Instruments

The default settings are configured for MNQ (Micro NASDAQ futures) but the ORB concept is highly customizable for any futures instrument and timeframe. Range duration, breakout offsets, and filter thresholds should be adjusted based on the specific instrument's volatility characteristics and typical intraday patterns.

Filter Usage Guidelines

ADX Momentum Filter: Essential for avoiding breakouts during consolidation. Higher thresholds (30+) for trending markets, lower (20-25) for more opportunities.

VWAP Filter: Helpful in trending conditions but may reduce trade frequency. Better to disable during range-bound or mean-reverting periods.

Large Range Filter: Critical risk management tool. When the opening range exceeds your threshold:

Skip: Avoids trades when stops would be too large

Fade: Trades mean reversion back into the range

Trade: Takes breakouts regardless (higher risk)

Range Size Considerations: Setting a large range threshold (200-400 ticks) helps avoid days when both sides of the range get tested before any meaningful breakout occurs, which often leads to whipsaws.

Risk Management Features

Dynamic Stops and Targets: All exit levels scale with the opening range size, ensuring risk/reward remains consistent regardless of daily volatility. A 100-tick range day will have proportionally smaller stops than a 300-tick range day.

Position Sizing: Configure contract amounts for each position tier based on account size and risk tolerance.

Daily Trade Limits: Prevents overtrading by limiting trades per direction per day.

Breakout Offset: The tick offset from range boundaries is crucial - too small creates false signals, too large misses good moves. Test different values based on your instrument's typical noise levels.

Advanced Features

Large Third Target: Set Target 3 to 300-500% to essentially hold runners indefinitely, using the trailing stop as the primary exit method for capturing extended trends.

Fade Trading: On large range days, the strategy can trade mean reversion when initial breakouts fail, often providing good counter-trend opportunities.

Time-Based Exits: All positions close at the end of the trading window, preventing overnight risk.

Strategy Properties Used

Initial Capital: $5,000 (realistic for micro contract trading)

Commission: $0.50 per contract (realistic retail rates)

Position Size: 100% of equity (manages risk through contract quantities and stop placement)

Default quantities: 3/1/1 contracts across the three positions

The default settings assume larger account sizes or proprietary trading firm accounts where higher risk tolerance is acceptable. With MNQ at $0.50 per tick, a typical 200-tick opening range with 75% stop loss (150 ticks) would risk $375 on a 5-contract position. For smaller retail accounts, consider reducing position sizes significantly - using only Position 1 (3 contracts) would risk $225, or even reducing to 1-2 total contracts to maintain appropriate risk levels relative to account size.

Getting Started Apply the strategy to your preferred instrument

Adjust the opening range time and duration for your market

Set appropriate breakout offset based on typical noise levels

Configure large range threshold based on your risk tolerance

Test filter combinations to find what works best for your trading style

Adjust contract quantities based on your account size and risk management rules

The strategy works best on liquid instruments with clear opening sessions and sufficient volatility to generate meaningful ranges. Results will vary significantly based on market conditions, parameter settings, and the specific instrument traded.

I warrant that the information created and published by by me here on TradingView is not prohibited, doesn't constitute investment advice, and isn't created solely for qualified investors.

- Trading Bot – Dynamic RSI (Professional) - Robot Strategy -1. General Concept and Philosophy

This strategy was designed for systematic traders and work especially well on short timeframes (1 to 5 minutes), who seek to capture trend reversal movements with a high degree of confirmation. The goal is not to follow the trend, but to identify precise entry points in oversold or overbought zones, and then to exit the position dynamically to adapt to changing market conditions.

The originality of Trading Bot Dynamic RSI lies not in a single indicator, but in the intelligent fusion of several concepts:

Dynamic RSI bands for both entries and exits .

A triple confirmation filter to secure trade entries.

A fully parameterizable design ready for automation .

2. Originality at the Core of the Strategy: Key Features

Dynamic Exits on RSI Bands: This is a main original feature of this script. Unlike traditional strategies that use fixed Take-Profits and Stop-Losses, this one uses an exit RSI band, calculated with parameters independent of the entry ones. This allows the strategy to:

Adapt to Volatility: In a volatile market, the exit band will move further away, allowing for the capture of larger moves. In a ranging market, it will tighten to secure smaller gains.

Optimize Profits: The exit occurs when momentum genuinely fades, not at an arbitrary price level, thus maximizing the potential of each trade.

Triple Confirmation Filter for Precise Entries: To avoid false signals, each entry is validated by the convergence of three distinct conditions:

The base signal is generated when the price reaches an overbought or oversold zone, materialized by an RSI band calculated directly on the chart.

The WaveTrend oscillator must also be in an extreme zone, confirming that the short-term momentum is ready for a reversal.

Finally, the StochRSI must validate that the RSI itself is in an overbought or oversold condition, adding an extra layer of security.

"Automation Ready" Design: The strategy was developed with automation in mind.

Customizable Alert Messages: All messages for entries and exits (Long/Short) can be formatted to be compatible with automated trade execution platforms.

Precise Capital Management: The position size calculation can be set as a fixed amount (e.g., 100 USDT), a percentage of the total capital, or of the available capital, and includes leverage. These parameters are crucial for a trading bot.

3. Detailed Operation

Entry Logic: A position is opened only if the following three conditions are met:

The market price touches (or closes below/above) the entry RSI band (lower for a buy, upper for a sell).

The WaveTrend indicator is in the oversold zone (for a buy) or overbought zone (for a sell).

The Stochastic RSI indicator is also in the oversold zone (for a buy) or overbought zone (for a sell).

The order is placed as a limit order on the RSI band, allowing for execution at the best possible price.

Exit Logic: The primary exit is dynamic.

For a Long position, the trade is closed when the price reaches the upper exit RSI band.

For a Short position, the trade is closed when the price reaches the lower exit RSI band.

Optionally, a percentage-based Stop-Loss and Take-Profit can be activated for more traditional risk management, although the dynamic exit is the recommended default mechanism.

4. Ease of Use and Customization

Despite its internal complexity, the strategy is designed to be user-friendly :

Clear Settings Panel: Parameters are grouped by function (Long Entry, Long Exit, Quantity, etc.), and each option comes with an explanatory tooltip.

Integrated Display: All key information (performance, current settings) is displayed in clean and discreet tables directly on the chart, allowing you to see at a glance how the strategy is configured.

Total Flexibility: Although default settings are provided, every parameter (RSI lengths, levels, filters) can be adjusted to optimize the strategy on any asset (cryptocurrencies, Forex, indices...) and any timeframe.

5. Detailed Guide to User Settings

A comprehensive set of parameters

To offer you complete control and maximum flexibility, the strategy exposes a comprehensive set of parameters. Here is an overview of what you can customize:

Trading Mode and Display

Trading Mode: Choose to enable only long positions ("Long Only"), only short positions ("Short Only"), or both simultaneously ("Long and Short").

Display: Manage the information panels on the chart. You can opt for a full display, a minimal window showing the profit, or hide all information for a clean chart.

Filters Smoothing (StochRSI K)

Filters Smoothing: This key parameter adjusts the smoothing of the Stochastic RSI. A lower value will make the filter more responsive, generating more signals. A higher value will make it smoother, generating fewer but potentially more reliable signals.

LONG Position Settings

Long Only mode

Entry: Define the RSI length and Oversold level that draw the lower band for long position entries.

Exit: Independently configure the RSI length and Overbought level that draw the upper band for the dynamic position exit.

Options: Optionally enable a percentage-based Take-Profit and/or Stop-Loss.

SHORT Position Settings

Short Only Mode

Entry: Define the RSI length and Overbought level for the upper entry band for short positions.

Exit: Independently configure the RSI length and Oversold level for the lower dynamic exit band.

Options: Just like for long positions, you can enable a percentage-based Take-Profit and/or Stop-Loss.

Quantity and Leverage

Quantity Type: Calculate your position size in three ways: as a fixed cash amount, as a percentage of available capital, or as a percentage of the total account balance.

Amount: Specify the dollar amount or percentage to commit per trade.

Leverage: Set the leverage to be applied. This is crucial for automation.

Backtest Period

Backtest Period: Enable this option to limit the strategy's calculations to a specific time period. This is a powerful tool for testing performance under particular market conditions.

Bot Alert Messages

Bot Alert Messages: This section is dedicated to automation. Customize the exact text messages that will be sent by TradingView alerts for each event (enter long, exit long, etc.).

Other Settings (Advanced - Optional)

Other Settings: This section allows experienced users to fine-tune the confirmation engine. You can adjust the parameters of the WaveTrend and Stochastic RSI oscillators in detail.

Spread Calculator (Informative Only)

Spread Calculator: This handy tool helps you estimate the actual fees of your exchange to run a much more realistic backtest. This panel has no impact on the trading logic itself.

Disclaimer

This strategy provides signals based on past market conditions. Past performance is not indicative of future results. Trading involves risk, and it is the responsibility of each user to manage their risk appropriately. It is strongly recommended to conduct thorough backtests and to understand the functioning of each parameter before using this strategy in live conditions or automating it. Take into account transaction fees, spread, and slippage, which can impact real results.

PowerTrend Pro Strategy – Gold OptimizedTired of false signals on Gold?

PowerTrend Pro combines VWAP, Supertrend, RSI, and smart MA filters with trailing stops & break-even logic to deliver high-probability trades on XAUUSD.

PowerTrend Pro Strategy is a professional-grade trading system designed to capture high-probability swing and intraday opportunities on XAUUSD (Gold) and other volatile markets.

🔑 Core Features

VWAP Anchoring – institutional fair value reference to filter trades.

Supertrend (ATR-based) – adaptive trend filter tuned for Gold’s volatility.

Multi-Timeframe RSI – confirms momentum alignment across intraday and higher timeframe.

EMA + SMA Combo – ensures trades follow strong directional bias, reducing false signals.

Dynamic Risk Management

Adjustable Take Profit / Stop Loss (%)

Trailing Stop that locks in profits on extended moves

Break-Even Logic (stop loss moves to entry once price is in profit)

⚡ Gold-Tuned Presets

XAUUSD 1H → tighter TP/SL & faster entries for active intraday trading.

XAUUSD 4H → wider ATR filter & trailing stops to capture bigger swings.

Generic Mode → works on Forex, Indices, and Crypto (fully customizable).

🎯 Why It Works

Gold is notoriously volatile — quick spikes wipe out weak strategies. PowerTrend Pro solves this by combining:

✅ Institutional bias (VWAP)

✅ Adaptive trend filter (Supertrend)

✅ Momentum confirmation (RSI MTF)

✅ Robust trend structure (EMA + SMA)

✅ Smart exits (TP, SL, trailing & breakeven)

This multi-layer confirmation makes entries stronger and keeps risk under control.

🛠️ Usage

Add the strategy to your chart.

Choose a preset (XAUUSD 1H, 4H, or Generic).

Run Strategy Tester for performance metrics.

Optimize TP/SL and ATR values for your broker & market conditions.

🔥 Pro Tip: Combine this strategy with a session filter (London/NY overlap) or volume confirmation to boost accuracy in Gold.

MomentumThe strategy uses EMA200, ADX/DMI, RSI, and volume. Pivot levels and Heikin-Ashi ensure safe entries, while cooldowns and opposite-locks prevent overtrading. Exits are managed with ATR trailing stops and trend-reversal signals.

FFI-Trend Rider ProFFI-Trend Rider Pro is a trend-following strategy designed to help traders make more structured and disciplined entries.

It uses a crossover between the 11 EMA and 21 SMA to detect potential trend shifts, while avoiding premature entries by checking how far the price is from the moving averages. If the price is extended, it waits for a pullback — just like professional traders do.

The indicator also includes:

Auto stoploss based on 21 SMA

Visual background colors based on RSI to help gauge trend strength

A built-in trade info table showing current trade type, entry price, stoploss, and trailing SL

Strategy-enabled functionality for easy backtesting

🔍 Ideal For:

Intraday & Swing Traders

Traders who want fewer, high-quality trades

Anyone looking to reduce emotional decision-making

⚠️ Disclaimer:

This script is for educational purposes only and does not constitute financial advice. Always do your own analysis before making any trading decisions. Past performance is not indicative of future results.

Adaptive MVRV & RSI Strategy V6 (Dynamic Thresholds)Strategy Explanation

This is an advanced Dollar-Cost Averaging (DCA) strategy for Bitcoin that aims to adapt to long-term market cycles and changing volatility. Instead of relying on fixed buy/sell signals, it uses a dynamic, weighted approach based on a combination of on-chain data and classic momentum.

Core Components:

Dual-Indicator Signal: The strategy combines two powerful indicators for a more robust signal:

MVRV Ratio: An on-chain metric to identify when Bitcoin is fundamentally over or undervalued relative to its historical cost basis.

Weekly RSI: A classic momentum indicator to gauge long-term market strength and identify overbought/oversold conditions.

Dynamic, Self-Adjusting Thresholds: The core innovation of this strategy is that it avoids fixed thresholds (e.g., "sell when RSI is 70"). Instead, the buy and sell zones are dynamically calculated based on a long-term (2-year) moving average and standard deviation of each indicator. This allows the strategy to automatically adapt to Bitcoin's decreasing volatility and changing market structure over time.

Weighted DCA (Scaling In & Out): The strategy doesn't just buy or sell a fixed amount. The size of its trades is scaled based on conviction:

Buying: As the MVRV and RSI fall deeper into their "undervalued" zones, the percentage of available cash used for each purchase increases.

Selling: As the indicators rise further into "overvalued" territory, the percentage of the current position sold also increases.

This creates an adaptive system that systematically accumulates during periods of fear and distributes during periods of euphoria, with the intensity of its actions directly tied to the extremity of market conditions.

Institution Accumulation/DistributionLeveraging the Williams%R oscillator, the script has been optimized to pick out key turning point in the market specifically at Resistance (Overbought) or Support (Oversold)

The algo has been programmed to print both buy and sell alerts at extremes/when conditions flip eg a long position will be closed simultaneously opening a short position above resistance.

Best used as a scalping tool targeting 30m and below works well with currency pairs

Ultimate Bot v5 (Full Visual + Reversal + Sustained Signals)Ultimate Bot v5 is a powerful, all-in-one Pine Script strategy designed for traders who want both clarity and precision in their charts. It combines classic momentum indicators, volatility filters, and reversal logic to highlight high-probability trade opportunities.

🔹 Key Features

Full Visual Mode – Clean and easy-to-read buy/sell markers with large arrows and labels.

EMA Trend Detection – Fast & slow EMA crossovers for trend direction.

RSI + MACD Confirmation – Confirms entries with momentum & strength checks.

Reversal Alerts – Detects sharp drops or spikes for rebound/reversal plays.

Sustained Signal Mode – Highlights stronger continuation trends, not just short-term flips.

ADX Strength Filter (optional) – Filters out weak/noisy signals during sideways markets.

ATR Dynamic Positioning – Arrows adapt to volatility so they’re always visible.

Custom Alerts – Works with TradingView alerts for buy, sell, and reversal signals.

🔹 Why Use It?

This bot is designed to help traders:

✅ Spot early reversals and potential bounce opportunities

✅ Confirm strong momentum moves with multi-indicator checks

✅ Avoid false signals in choppy markets

✅ Trade with confidence using visual clarity

TrendPilot AI v2 — Adaptive Trend Day Trading StrategyOverview

TrendPilot AI v2 is a structured, rules-based day trading strategy that identifies and follows market momentum using a sophisticated blend of technical indicators. Optimized for 15-minute and higher timeframes on high market cap cryptocurrencies (AAVE, SOL, ETH, BCH, BTC) to minimize manipulation risks, it adapts to changing market conditions with dynamic risk management and controlled re-entry logic to maximize trend participation while minimizing noise.

Core Logic

Multiple EMA Trend Confirmation — Uses three Exponential Moving Averages (fast, medium, slow) to detect robust bullish, bearish, or neutral trends, ensuring trades align with the prevailing market direction.

ADX Momentum Filter — Employs an ADX-based filter to confirm strong trends, avoiding entries in choppy or low-momentum markets.

Smart Entry Filter — Optional ATR-based buffer (period 14, multiplier 1.5) around the fast EMA prevents entries at overextended prices, enhancing trade precision.

Flexible Exit System — Offers multiple exit options: fixed take-profit (default 1.7 offset), trend-reversal exits, or ATR-based trailing stops (period 14, multiplier 2.0), with secure modes requiring candle closes for confirmation to gain Max Profit.

Controlled Re-Entry Logic — Allows re-entries after take-profit or price-based stop-loss with configurable wait periods (default 6 bars), max attempts (default 2), and EMA touch requirements (fast, medium, or slow).

State-Aware Risk Management — Tracks trend states and recent exits to adapt entries, with daily trade limits (default 5 long/short) and loss cooldowns (default 2 stop-losses) for disciplined trading.

How to Use & Configuration

Markets & Timeframes

Works with high market cap cryptocurrencies (AAVE, SOL, ETH, BCH, BTC).

Optimized for intraday charts (15m–4h) but adaptable to higher timeframes (e.g., 1h, 4h).

Trade Direction Settings

Dual Trades — Trades both long and short, quickly re-aligning after trend reversals.

Long Only — Ignores bearish signals, ideal for bullish markets or strong uptrends.

Short Only — Ignores bullish signals, suited for bearish markets or downtrends.

Risk Management Settings

Stop Loss Types

Trend Reversal — Closes positions when an opposite trend signal is confirmed (default).

Fixed Offset — Static stop at 3.5 offset from entry price (adjustable).

ATR Based — Dynamic trailing stop using ATR (period 14, multiplier 2.0), adjusting to market volatility.

Secure SL Mode — Optional setting to trigger price-based stops only on candle closes, reducing false exits.

Maximum recommended risk per trade is 5–10% of account equity.

Trade size is configurable (default 20 units) to match individual risk appetite.

Take Profit Options

Fixed Offset — Predefined target at 1.7 offset from entry (adjustable, e.g., 2.5 for SOL).

Secure TP Mode — Exits only when a candle closes beyond the target, ensuring reliable profit capture.

Trend Reversal — Exits on opposite trend signals when fixed TP is disabled, ideal for riding longer trends.

Trade Management Controls

Smart Entry Filter — Optional ATR-based buffer (period 14, multiplier 1.5) prevents chasing overextended prices.

Max Re-Entries — Limits continuation trades per trend cycle (default 2).

Daily Trade Limits — Caps long/short trades per day (default 5 each) for disciplined trading.

Daily Loss Cooldown — Pauses trading after a set number of stop-losses (default 2) per day.

Max Bars in Trade — Closes positions after a set duration (default 1440 bars) to prevent stale trades.

Configuration Steps

Apply the strategy to your chosen symbol (e.g., AAVE/USDT, SOL/USDT) and timeframe (15m or higher).

Select Trade Direction mode (Dual, Long Only, or Short Only).

Set Stop Loss (Trend Reversal, Fixed Offset, or ATR Based) and Take Profit (fixed or trend-reversal).

Adjust Smart Entry Filter, Max Re-Entries, Daily Limits, and Loss Cooldown as needed.

Test across multiple market conditions using the performance panel (top-right, showing Total Trades, Wins, Losses, Win Rate).

Enables automated trading via webhook integration with platforms like Binance Futures.

Set up alerts for long/short entries (🟢 Long, 🔴 Short) and exits (🎯 Max TP, 🛑 Max SL, 🚨 Force Exit).

Backtesting Guidance

Use realistic commission (default 0.01%) and slippage (default 2 ticks) matching your broker and instrument.

Validate performance over long historical periods (e.g., 3–6 months) to ensure >100 trades across different market regimes.

Avoid curve-fitting by testing on multiple high market cap coins (AAVE, SOL, ETH, BCH, BTC) and avoiding over-optimization.

EMA and ATR parameters are set to balanced, industry-standard values for realistic backtesting.

Best Practices, Defaults & Disclaimer

Best Practices

Use consistent and conservative position sizing (default 20 units).

Match commission and slippage to your broker’s actual rates.

Enable secure TP/SL modes for entries and exits to reduce false signals.

Test across different symbols, timeframes, and market phases before live trading.

Keep parameters simple to avoid overfitting.

Default Settings (Recommended Starting Point)

Initial Capital: $10,000

Order Size: Fixed, 20 units

Commission: 0.01%

Slippage: 2 ticks

Take Profit Offset: 1.7 (adjustable, e.g., 2.5 for SOL)

Stop Loss Type: Trend Reversal (default), Fixed Offset (3.5), or ATR Based (period 14, multiplier 2.0)

Smart Entry Filter: ATR period 14, multiplier 1.5 (optional)

Max Re-Entries: 2 per trend cycle

Daily Trade Limits: 5 long, 5 short

Daily Loss Cooldown: 2 stop-losses

Max Bars in Trade: 1440 bars

Subscription Information

TrendPilot AI v2 is an invite-only strategy, accessible only to approved subscribers.

Benefits include full access to all features, priority support, and regular updates.

Access is limited to ensure a high-quality user experience.

Compliance Status

No functional warnings in the script.

The script uses closed candle logic, ensuring no repainting or lookahead issues.

Designed for realistic backtesting with a $10,000 account and sustainable risk (≤5–10% per trade).

Disclaimer

This strategy is intended for educational and analytical purposes only. Trading involves substantial risk, and past performance does not guarantee future results. You are solely responsible for your own trading decisions and risk management.

Developed by: TrendPilotAI Team

For questions, setup guidance, or enhancement suggestions, contact TrendPilotAI Team via TradingView.

Nifty Power -> Nifty 50 chart + EMA of RSI + avg volume strategyThis strategy works in 1 hour candle in Nifty 50 chart. In this strategy, upward trade takes place when there is a crossover of RSI 15 on EMA50 of RSI 15 and volume is greater than volume based EMA21. On the other hand, lower trade takes place when RSI 15 is less than EMA50 of RSI 15. Please note that there is no stop loss given and also that the trade will reverse as per the trend. Sometimes on somedays, there will be no trades. Also please note that this is an Intraday strategy. The trade if taken closes on 15:15 in Nifty 50. This strategy can be used for swing trading. Some pine script code such as supertrend and ema21 of close is redundant. Try not to get confused as only EMA50 of RSI 15 is used and EMA21 of volume is used. I am using built-in pinescript indicators and there is no special calculation done in the pine script code. I have taken numbars variable to count number of candles. For example, if you have 30 minuite chart then numbars variable will count the intraday candles accordingly and the same for 1 hour candles.

光速量化-头皮策略v1.1Version: Unlimited trial version.

Principle: RSI and moving average complement each other, taking a bite of both oscillation and trend.

Disadvantage: High drawdown.

Disclaimer: The scalp strategy v1.1 of Lightspeed Quantification is designed for trial users. Those who use this strategy are responsible for their own assets, and any losses incurred are not the responsibility of the author.

版本:无期限试用版。

原理:RSI与均线配合,震荡与趋势都吃一口。

缺点:回撤高。

声明:光速量化的头皮策略v1.1是面向试用者体验的,使用该策略的人请为自己的资产负责,产生任何损失与作者无关。

EMA Deviation Strategy📌 Strategy: EMA Deviation Strategy

The EMA Deviation Strategy identifies potential reversal points by measuring how far the current price deviates from its Exponential Moving Average (EMA). It dynamically tracks the minimum and maximum deviation levels over a user-defined lookback period, and enters trades when price reaches extreme zones.

🔍 Core Logic:

• Buy Entry: When price deviates significantly below the EMA, approaching the historical minimum deviation — signaling a potential rebound.

• Sell Entry: When price deviates significantly above the EMA, nearing the historical maximum deviation — signaling a possible pullback.

• Optional Take Profit / Stop Loss: Manage risk with customizable exit levels.

⚙️ Customizable Inputs:

• EMA length and lookback period

• Threshold sensitivity for entry signals

• Take profit and stop loss percentages

📈 Best Used For:

• Mean reversion setups

• Assets with cyclical or range-bound behavior

• Identifying short-term overbought/oversold conditions