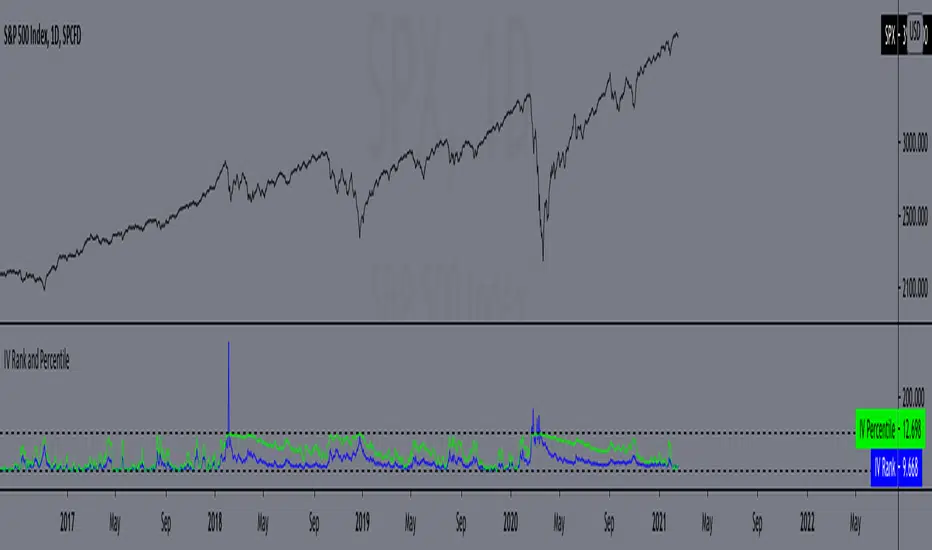

IV Rank & Percentile Suite V1.0What This Indicator Does

The IV Rank & Percentile Suite provides the volatility context options traders need to time entries. It calculates two complementary metrics—IV Rank and IV Percentile—using historical volatility as a proxy, then displays clear visual zones to identify favorable conditions for premium selling strategies.

Stop guessing if volatility is "high" or "low." This indicator tells you exactly where current volatility sits relative to recent history.

The Two Metrics Explained

IV Rank (0-100) Measures where current volatility sits within its 52-week high-low range.

IV Rank = (Current HV - 52w Low) / (52w High - 52w Low) × 100

70 means current volatility is 70% of the way between the yearly low and high

Sensitive to extreme spikes (a single high reading affects the range)

IV Percentile (0-100) Measures what percentage of days in the lookback period had lower volatility than today.

IV Percentile = (Days with lower HV / Total days) × 100

70 means volatility was lower than today on 70% of days in the past year

More stable, less affected by outlier spikes

Why Both?

IV Rank reacts faster to volatility changes. IV Percentile is more stable and statistically robust. When both agree (e.g., both above 50), you have stronger confirmation. Divergence between them can signal transitional periods.

Zone System

The indicator divides readings into three zones:

Zone ------- Default Range ---- Meaning ------------------ Premium Selling

🟢 High ≥ 50 Elevated volatility Favorable

🟡 Neutral 25-50 Normal volatility Selective

🔴 Low ≤ 25 Compressed volatility Avoid

An additional Extreme threshold (default 75) highlights prime conditions when volatility is significantly elevated.

Zone thresholds are fully customizable in settings.

How to Use It

For Premium Sellers (Iron Condors, Credit Spreads, Strangles)

Wait for IV Rank to enter the green zone (≥50)

Confirm IV Percentile agrees (also elevated)

Enter premium selling positions when both metrics align

Avoid initiating new positions when in the red zone

For Premium Buyers (Long Options, Debit Spreads)

Low IV Rank/Percentile means cheaper options

Red zone can favor directional debit strategies

Avoid buying premium when both metrics are in the green zone

General Principle:

Sell premium when volatility is high (it tends to revert to mean). Buy premium when volatility is low (if you have a directional thesis).

Inputs

Volatility Calculation

HV Period — Lookback for historical volatility calculation (default: 20)

Trading Days/Year — 252 for stocks, 365 for crypto

Lookback Periods

IV Rank Lookback — Period for high/low range (default: 252 = 1 year)

IV Percentile Lookback — Period for percentile calculation (default: 252)

Zone Thresholds

High IV Zone — Readings above this are highlighted green (default: 50)

Low IV Zone — Readings below this are highlighted red (default: 25)

Extreme High — Threshold for "prime" conditions alert (default: 75)

Display Options

Toggle IV Rank, IV Percentile, and raw HV display

Show/hide zone backgrounds

Show/hide info panel

Panel position selection

Info Panel

The panel displays:

Field ------- Description

IV Rank ------- Current reading with color coding

IV Pctl ------- Current percentile with color coding

HV 20d ------- Raw historical volatility percentage

52w Range ------- Lowest to highest HV in lookback period

Zone ------- Current zone status

Premium ------- Signal quality for premium selling

Lookback ------- Days used for calculations

R/P Spread ------- Difference between Rank and Percentile

Alerts

Six alerts are available:

Zone Transitions

IV Entered High Zone — Favorable for premium selling

IV Reached Extreme Levels — Prime conditions

IV Dropped to Low Zone — Caution for premium sellers

Threshold Crosses

IV Rank Crossed Above High Threshold

IV Rank Crossed Below Low Threshold

IV Percentile Above 75

IV Percentile Below 25

Set up alerts to get notified when conditions change without watching charts.

Technical Notes

Volatility Calculation Method

This indicator uses close-to-close historical volatility as an IV proxy:

Calculate log returns: ln(Close / Previous Close)

Take standard deviation over HV Period

Annualize: multiply by √(Trading Days)

This method correlates well with implied volatility for most liquid instruments. On highly liquid options underlyings (SPY, QQQ, major stocks), HV and IV tend to move together, making this a reliable proxy for IV Rank analysis.

Non-Repainting

All calculations use confirmed bar data. Values are fixed once a bar closes.

Lookback Requirement

The indicator needs sufficient history to calculate accurately. For a 252-day lookback, ensure your chart has at least 300+ bars of data.

Best Used On

ETFs: SPY, QQQ, IWM, DIA

Indices: SPX, NDX

High-volume stocks: AAPL, TSLA, NVDA, AMD, META

Timeframe: Daily (recommended), Weekly for longer-term view

The indicator works on any instrument but is most meaningful on underlyings with active options markets.

Important Notes

⚠️ This indicator uses historical volatility as a proxy for implied volatility. While HV and IV are correlated, they are not identical. For precise IV data, consult your options broker's platform.

⚠️ High IV Rank does not guarantee profitable premium selling. It indicates favorable conditions, not guaranteed outcomes. Position sizing and risk management remain essential.

⚠️ Past volatility patterns do not guarantee future behavior. Volatility regimes can shift, and historical ranges may not predict future ranges.

Suggested Workflow

Add to daily chart of your preferred underlying

Set up alert for "IV Entered High Zone"

When alerted, check both IV Rank and IV Percentile

If both elevated, evaluate premium selling opportunities

Use your broker's actual IV data for final entry decisions

Questions? Leave a comment below.

Iv

Implied Volatility RangeThe Implied Volatility Range is a forward-looking tool that transforms option market data into probability ranges for future prices. Based on the lognormal distribution of asset prices assumed in modern option pricing models, it converts the implied volatility curve into a volatility cone with dynamic labels that show the market’s expectations for the price distribution at a specific point in time. At the selected future date, it displays projected price levels and their percentage change from today’s close across 1, 2, and 3 standard deviation (σ) ranges:

1σ range = ~68.2% probability the price will remain within this range.

2σ range = ~95.4% probability the price will remain within this range.

3σ range = ~99.7% probability the price will remain within this range.

What makes this indicator especially useful is its ability to incorporate implied volatility skew. When only ATM IV (%) is entered, the indicator displays the standard Black–Scholes lognormal distribution. By adding High IV (%) and Low IV (%) values tied to strikes above and below the current price, the indicator interpolates between these inputs to approximate the implied volatility skew. This adjustment produces a market-implied probability distribution that indicates whether the option market is leaning bullish or bearish, based on the data entered in the menu:

ATM IV (%) = Implied volatility at the current spot price (at-the-money).

High IV (%) = Implied volatility at a strike above the current spot price.

High Strike = Strike price corresponding to the High IV input (OTM call).

Low IV (%) = Implied volatility at a strike below the current spot price.

Low Strike = Strike price corresponding to the Low IV input (OTM put).

Expiration (Day, Month, Year) = Option expiration date for the projection.

Once these inputs are entered, the indicator calculates implied probability ranges and, if both High IV and Low IV values are provided, adjusts for skew to approximate the option market’s distribution. If no implied volatility data is supplied, the indicator defaults to a lognormal distribution based on historical volatility, using past realized volatility over the same forward horizon. This keeps the tool functional even without implied volatility inputs, though in that case the output represents only an approximation of ATM IV, not the actual market view.

In summary, the Implied Volatility Range is a powerful tool that translates implied volatility inputs into a clear and practical estimate of the market’s expectations for future prices. It allows traders to visualize the probability of price ranges while also highlighting directional bias, a dimension often difficult to interpret from traditional implied volatility charts. It should be emphasized, however, that this tool reflects only the market’s expectations at a specific point in time, which may change as new information and trading activity reshape implied volatility.

IV Squeeze - Sunil Bhave This script calculates both Bollinger Bands and Keltner Channels on a 5-minute chart. It identifies IV squeeze conditions when the lower Bollinger Band is above the lower Keltner Channel and the upper Bollinger Band is below the upper Keltner Channel. When a squeeze is detected, it plots a red triangle below the chart bars and alerts you with a message.

Please note that this script is for educational purposes only.

Implied and Historical Volatility v4There is a famous option strategy📊 played on volatility📈. Where people go short on volatility, generally, this strategy is used before any significant event or earnings release. The basic phenomenon is that the Implied Volatility shoots up before the event and drops after the event, while the volatility of the security does not increase in most of the scenarios. 💹

I have tried to create an Indicator using which you

can analyse the historical change in Implied Volatility Vs Historic Volatility.

To get a basic idea of how the security moved during different events.

Notes:

a) Implied Volatility is calculated using the bisection method and Black 76 model option pricing model.

b) For the risk-free rate I have fetched the price of the “10-Year Indian Government Bond” price and calculated its yield to be used as our Risk-Free rate.

vol_coneDraws a volatility cone on the chart, using the contract's realized volatility (rv). The inputs are:

- window: the number of past periods to use for computing the realized volatility. VIX uses 30 calendar days, which is 21 trading days, so 21 is the default.

- stdevs: the number of standard deviations that the cone will cover.

- periods to project: the length of the volatility cone.

- periods per year: the number of periods in a year. for a daily chart, this is 252. for a thirty minute chart on a contract that trades 23 hours a day, this is 23 * 2 * 252 = 11592. for an accurate cone, this input must be set correctly, according to the chart's time frame.

- history: show the lagged projections. in other words, if the cone is set to project 21 periods in the future, the lines drawn show the top and bottom edges of the cone from 23 periods ago.

- rate: the current interest or discount rate. this is used to compute the forward price of the underlying contract. using an accurate forward price allows you to compare the realized volatility projection to the implied volatility projections derived from options prices.

Example settings for a 30 minute chart of a contract that trades 23 hours per day, with 1 standard deviation, a 21 day rv calculation, and half a day projected:

- stdevs: 1

- periods to project: 23

- window: 23 * 2 * 21 = 966

- periods per year: 23 * 2 * 252 = 11592

Additionally, a table is drawn in the upper right hand corner, with several values:

- rv: the contract's current realized volatility.

- rnk: the rv's percentile rank, compared to the rv values on past bars.

- acc: the proportion of times price settled inside, versus outside, the volatility cone, "periods to project" into the future. this should be around 65-70% for most contracts when the cone is set to 1 standard deviation.

- up: the upper bound of the cone for the projection period.

- dn: the lower bound of the cone for the projection period.

Limitations:

- pinescript only seems to be able to draw a limited distance into the future. If you choose too many "periods to project", the cone will start drawing vertically at some limit.

- the cone is not totally smooth owing to the facts a) it is comprised of a limited number of lines and b) each bar does not represent the same amount of time in pinescript, as some cross weekends, session gaps, etc.

IV Rank and Percentile"All stocks in the market have unique personalities in terms of implied volatility (their option prices). For example, one stock might have an implied volatility of 30%, while another has an implied volatility of 50%. Even more, the 30% IV stock might usually trade with 20% IV, in which case 30% is high. On the other hand, the 50% IV stock might usually trade with 75% IV, in which case 50% is low.

So, how do we determine whether a stock's option prices (IV) are relatively high or low?

The solution is to compare each stock's IV against its historical IV levels. We can accomplish this by converting a stock's current IV into a rank or percentile.

Implied Volatility Rank (IV Rank) Explained

Implied volatility rank (IV rank) compares a stock's current IV to its IV range over a certain time period (typically one year).

Here's the formula for one-year IV rank:

(Current IV - 1 Year Low IV) / (1 Year High IV - 1 Year Low IV) * 100

For example, the IV rank for a 20% IV stock with a one-year IV range between 15% and 35% would be:

(20% - 15%) / (35% - 15%) = 25%

An IV rank of 25% means that the difference between the current IV and the low IV is only 25% of the entire IV range over the past year, which means the current IV is closer to the low end of historical levels of implied volatility.

Furthermore, an IV rank of 0% indicates that the current IV is the very bottom of the one-year range, and an IV rank of 100% indicates that the current IV is at the top of the one-year range.

Implied Volatility Percentile (IV Percentile) Explained

Implied volatility percentile (IV percentile) tells you the percentage of days in the past that a stock's IV was lower than its current IV.

Here's the formula for calculating a one-year IV percentile:

Number of trading days below current IV / 252 * 100

As an example, let's say a stock's current IV is 35%, and in 180 of the past 252 days, the stock's IV has been below 35%. In this case, the stock's 35% implied volatility represents an IV percentile equal to:

180/252 * 100 = 71.42%

An IV percentile of 71.42% tells us that the stock's IV has been below 35% approximately 71% of the time over the past year.

Applications of IV Rank and IV Percentile

Why does it help to know whether a stock's current implied volatility is relatively high or low? Well, many traders use IV rank or IV percentile as a way to determine appropriate strategies for that stock.

For example, if a stock's IV rank is 90%, then a trader might look to implement strategies that profit from a decrease in the stock's implied volatility, as the IV rank of 90% indicates that the stock's current IV is at the top of its range over the past year (for a one-year IV rank).

On the other hand, if a stock's IV rank is 0%, then traders might look to implement strategies that profit from an increase in implied volatility, as the IV rank of 0% indicates the stock's current implied volatility is at the bottom of its range over the past year."

This script approximates IV by using the VIX products, which calculate the 30-day implied volatility of the specified security.

*Includes an option for repainting -- default value is true, meaning the script will repaint the current bar.

False = Not Repainting = Value for the current bar is not repainted, but all past values are offset by 1 bar.

True = Repainting = Value for the current bar is repainted, but all past values are correct and not offset by 1 bar.

In both cases, all of the historical values are correct, it is just a matter of whether you prefer the current bar to be realistically painted and the historical bars offset by 1, or the current bar to be repainted and the historical data to match their respective price bars.

As explained by TradingView,`f_security()` is for coders who want to offer their users a repainting/no-repainting version of the HTF data.

Bitcoin Implied VolatilityThis simple script collects data from FTX:BVOLUSD to plot BTC’s implied volatility as a standalone indicator instead of a chart.

Implied volatility is used to gauge future volatility and often used in options trading.

Historical Volatility RankSame formulation of IVR but based on Historical Volatility instead.

Serves the same purpose as IV rank.