Holt Damped Forecast [CHE]A Friendly Note on These Pine Script Scripts

Hey there! Just wanted to share a quick, heartfelt heads-up: All these Pine Script examples come straight from my own self-study adventures as a total autodidact—think late nights tinkering and learning on my own. They're purely for educational vibes, helping me (and hopefully you!) get the hang of Pine Script basics, cool indicators, and building simple strategies.

That said, please know this isn't any kind of financial advice, investment nudge, or pro-level trading blueprint. I'd love for you to dive in with your own research, run those backtests like a champ, and maybe bounce ideas off a qualified expert before trying anything in a real trading setup. No guarantees here on performance or spot-on accuracy—trading's got its risks, and those are totally on each of us.

Let's keep it fun and educational—happy coding! 😊

Holt Damped Forecast — Damped trend forecasts with fan bands for uncertainty visualization and momentum integration

Summary

This indicator applies damped exponential smoothing to generate forward price forecasts, displaying them as probabilistic fan bands to highlight potential ranges rather than point estimates. It incorporates residual-based uncertainty to make projections more reliable in varying market conditions, reducing overconfidence in strong trends. Momentum from the trend component is shown in an optional label alongside signals, aiding quick assessment of direction and strength without relying on lagging oscillators.

Motivation: Why this design?

Standard exponential smoothing often extrapolates trends indefinitely, leading to unrealistic forecasts during mean reversion or weakening momentum. This design uses damping to gradually flatten long-term projections, better suiting real markets where trends fade. It addresses the need for visual uncertainty in forecasts, helping traders avoid entries based on overly optimistic point predictions.

What’s different vs. standard approaches?

- Reference baseline: Diverges from basic Holt's linear exponential smoothing, which assumes persistent trends without decay.

- Architecture differences:

- Adds damping to the trend extrapolation for finite-horizon realism.

- Builds fan bands from historical residuals for probabilistic ranges at multiple confidence levels.

- Integrates a dynamic label combining forecast details, scaled momentum, and directional signals.

- Applies tail background coloring to recent bars based on forecast direction for immediate visual cues.

- Practical effect: Charts show converging forecast bands over time, emphasizing shorter horizons where accuracy is higher. This visibly tempers aggressive projections in trends, making it easier to spot when uncertainty widens, which signals potential reversals or consolidation.

How it works (technical)

The indicator maintains two persistent components: a level tracking the current price baseline and a trend capturing directional slope. On each bar, the level updates by blending the current source price with a one-step-ahead expectation from the prior level and damped trend. The trend then adjusts by weighting the change in level against the prior damped trend. Forecasts extend this forward over a user-defined number of steps, with damping ensuring the trend influence diminishes over distance.

Uncertainty derives from the standard deviation of historical residuals—the differences between actual prices and one-step expectations—scaled by the damping structure for the forecast horizon. Bands form around the median forecast at specified confidence intervals using these scaled errors. Initialization seeds the level to the first bar's price and trend to zero, with persistence handling subsequent updates. A security call fetches the last bar index for tail logic, using lookahead to align with realtime but introducing minor repaint on unconfirmed bars.

Parameter Guide

The Source parameter selects the price input for level and residual calculations, defaulting to close; consider using high or low for assets sensitive to volatility, as close works well for most trend-following setups. Forecast Steps (h) defines the number of bars ahead for projections, defaulting to 4—shorter values like 1 to 5 suit intraday trading, while longer ones may widen bands excessively in choppy conditions. The Color Scheme (2025 Trends) option sets the base, up, and down colors for bands, labels, and backgrounds, starting with Ruby Dawn; opt for serene schemes on clean charts or vibrant ones to stand out in dark themes.

Level Smoothing α controls the responsiveness of the price baseline, defaulting to 0.3—values above 0.5 enhance tracking in fast markets but may amplify noise, whereas lower settings filter disturbances better. Trend Smoothing β adjusts sensitivity to slope changes, at 0.1 by default; increasing to 0.2 helps detect emerging shifts quicker, but keeping it low prevents whipsaws in sideways action. Damping φ (0..1) governs trend persistence, defaulting to 0.8—near 0.9 preserves carryover in sustained moves, while closer to 0.5 curbs overextensions more aggressively.

Show Fan Bands (50/75/95) toggles the probabilistic range display, enabled by default; disable it in oscillator panes to reduce clutter, but it's key for overlay forecasts. Residual Window (Bars) sets the length for deviation estimates, at 400 bars initially—100 to 200 works for short timeframes, and 500 or more adds stability over extended histories. Line Width determines the thickness of band and median lines, defaulting to 2; go thicker at 3 to 5 for emphasis on higher timeframes or thinner for layered indicators.

Show Median/Forecast Line reveals the central projection, on by default—hide if bands provide enough detail, or keep for pinpoint entry references. Show Integrated Label activates the combined view of forecast, momentum, and signal, defaulting to true; it's right-aligned for convenience, so turn it off on smaller screens to save space. Show Tail Background colors the last few bars by forecast direction, enabled initially; pair low transparency for subtle hints or higher for bolder emphasis.

Tail Length (Bars) specifies bars to color backward from the current one, at 3 by default—1 to 2 fits scalping, while 5 or more underscores building momentum. Tail Transparency (%) fades the background intensity, starting at 80; 50 to 70 delivers strong signals, and 90 or above allows seamless blending. Include Momentum in Label adds the scaled trend value, defaulting to true—ATR% scaling here offers relative strength context across assets.

Include Long/Short/Neutral Signal in Label displays direction from the trend sign, on by default; neutral helps in ranging markets, though it can be overlooked during strong trends. Scaling normalizes momentum output (raw, ATR-relative, or level-relative), set to ATR% initially—ATR% ensures cross-asset comparability, while %Level provides percentage perspectives. ATR Length defines the period for true range averaging in scaling, at 14; align it with your chart timeframe or shorten for quicker volatility responses.

Decimals sets precision in the momentum label, defaulting to 2—0 to 1 yields clean integers, and 3 or more suits detailed forex views. Show Zero-Cross Markers places arrows at direction changes, enabled by default; keep size small to minimize clutter, with text labels for fast scanning.

Reading & Interpretation

Fan bands expand outward from the current bar, with the median line as the central forecast—narrower bands indicate lower uncertainty, wider suggest caution. Colors tint up (positive forecast vs. prior level) in the scheme's up hue and down otherwise. The optional label lists the horizon, median, and range brackets at 50%, 75%, and 95% levels, followed by momentum (scaled per mode) and signal (Long if positive trend, Short if negative, Neutral if zero). Zero-cross arrows mark trend flips: upward triangle below bar for bullish cross, downward above for bearish. Tail background reinforces the forecast direction on recent bars.

Practical Workflows & Combinations

- Trend following: Enter long on upward zero-cross if median forecast rises above price and bands contain it; confirm with higher highs/lows. Short on downward cross with falling median.

- Exits/Stops: Trail stops below 50% lower band in longs; exit if momentum drifts negative or signal turns neutral. Use wider bands (75/95%) for conservative holds in volatile regimes.

- Multi-asset/Multi-TF: Defaults work across stocks, forex, crypto on 5m-1D; scale steps by TF (e.g., 10+ on daily). Layer with volume or structure tools—avoid over-reliance on isolated crosses.

Behavior, Constraints & Performance

Closed-bar logic ensures stable historical plots, but realtime updates via security lookahead may shift forecasts until bar confirmation, introducing minor repaint on the last bar. No explicit HTF calls beyond bar index fetch, minimizing gaps but watch for low-liquidity assets. Resources include a 2000-bar lookback for residuals and up to 500 labels, with no loops—efficient for most charts. Known limits: Early bars show wide bands due to sparse residuals; assumes stationary errors, so gaps or regime shifts widen inaccuracies.

Sensible Defaults & Quick Tuning

Start with defaults for balanced smoothing on 15m-4H charts. For choppy conditions (too many crosses), lower β to 0.05 and raise residual window to 600 for stability. In trending markets (sluggish signals), increase α/β to 0.4/0.2 and shorten steps to 2. If bands overexpand, boost φ toward 0.95 to preserve trend carry. Tune colors for theme fit without altering logic.

What this indicator is—and isn’t

This is a visualization and signal layer for damped forecasts and momentum, complementing price action analysis. It isn’t a standalone system—pair with risk rules and broader context. Not predictive beyond the horizon; use for confirmation, not blind entries.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

Forecast

Volume Surprise [LuxAlgo]The Volume Surprise tool displays the trading volume alongside the expected volume at that time, allowing users to spot unexpected trading activity on the chart easily.

The tool includes an extrapolation of the estimated volume for future periods, allowing forecasting future trading activity.

🔶 USAGE

We define Volume Surprise as a situation where the actual trading volume deviates significantly from its expected value at a given time.

Being able to determine if trading activity is higher or lower than expected allows us to precisely gauge the interest of market participants in specific trends.

A histogram constructed from the difference between the volume and expected volume is provided to easily highlight the difference between the two and may be used as a standalone.

The tool can also help quantify the impact of specific market events, such as news about an instrument. For example, an important announcement leading to volume below expectations might be a sign of market participants underestimating the impact of the announcement.

Like in the example above, it is possible to observe cases where the volume significantly differs from the expected one, which might be interpreted as an anomaly leading to a correction.

🔹 Detecting Rare Trading Activity

Expected volume is defined as the mean (or median if we want to limit the impact of outliers) of the volume grouped at a specific point in time. This value depends on grouping volume based on periods, which can be user-defined.

However, it is possible to adjust the indicator to overestimate/underestimate expected volume, allowing for highlighting excessively high or low volume at specific times.

In order to do this, select "Percentiles" as the summary method, and change the percentiles value to a value that is close to 100 (overestimate expected volume) or to 0 (underestimate expected volume).

In the example above, we are only interested in detecting volume that is excessively high, we use the 95th percentile to do so, effectively highlighting when volume is higher than 95% of the volumes recorded at that time.

🔶 DETAILS

🔹 Choosing the Right Periods

Our expected volume value depends on grouping volume based on periods, which can be user-defined.

For example, if only the hourly period is selected, volumes are grouped by their respective hours. As such, to get the expected volume for the hour 7 PM, we collect and group the historical volumes that occurred at 7 PM and average them to get our expected value at that time.

Users are not limited to selecting a single period, and can group volume using a combination of all the available periods.

Do note that when on lower timeframes, only having higher periods will lead to less precise expected values. Enabling periods that are too low might prevent grouping. Finally, enabling a lot of periods will, on the other hand, lead to a lot of groups, preventing the ability to get effective expected values.

In order to avoid changing periods by navigating across multiple timeframes, an "Auto Selection" setting is provided.

🔹 Group Length

The length setting allows controlling the maximum size of a volume group. Using higher lengths will provide an expected value on more historical data, further highlighting recurring patterns.

🔹 Recommended Assets

Obtaining the expected volume for a specific period (time of the day, day of the week, quarter, etc) is most effective when on assets showing higher signs of periodicity in their trading activity.

This is visible on stocks, futures, and forex pairs, which tend to have a defined, recognizable interval with usually higher trading activity.

Assets such as cryptocurrencies will usually not have a clearly defined periodic trading activity, which lowers the validity of forecasts produced by the tool, as well as any conclusions originating from the volume to expected volume comparisons.

🔶 SETTINGS

Length: Maximum number of records in a volume group for a specific period. Older values are discarded.

Smooth: Period of a SMA used to smooth volume. The smoothing affects the expected value.

🔹 Periods

Auto Selection: Automatically choose a practical combination of periods based on the chart timeframe.

Custom periods can be used if disabling "Auto Selection". Available periods include:

- Minutes

- Hours

- Days (can be: Day of Week, Day of Month, Day of Year)

- Months

- Quarters

🔹 Summary

Method: Method used to obtain the expected value. Options include Mean (default) or Percentile.

Percentile: Percentile number used if "Method" is set to "Percentile". A value of 50 will effectively use a median for the expected value.

🔹 Forecast

Forecast Window: Number of bars ahead for which the expected volume is predicted.

Style: Style settings of the forecast.

Cyclical Phases of the Market🧭 Overview

“Cyclical Phases of the Market” automatically detects major market cycles by connecting swing lows and measuring the average number of bars between them.

Once it learns the rhythm of past cycles, it projects the next expected cycle (in time and price) using a dashed orange line and a forecast label.

In simple terms:

The indicator shows where the next potential low is statistically expected to occur, based on the timing and depth of previous cycles.

⚙️ Core Logic – Step by Step

1️⃣ Pivot Detection

The script uses the built-in ta.pivotlow() and ta.pivothigh() functions to find local turning points:

pivotLow marks a local swing low, defined by pivotLeft and pivotRight bars on each side.

Only confirmed lows are used to define the major cycle points.

Each new pivot low is stored in two arrays:

cycleLows → price level of the low

cycleBars → bar index where the low occurred

2️⃣ Cycle Identification and Drawing

Every time two consecutive swing lows are found, the indicator:

Calculates the number of bars between them (cycle length).

If that distance is greater than or equal to minCycleBars, it draws a teal line connecting the two lows — visually representing one complete cycle.

These teal lines form the historical cycle structure of the market.

3️⃣ Average Cycle Length

Once there are at least three completed cycles, the script calculates the average duration (mean number of bars between lows).

This value — avgCycleLength — represents the dominant periodicity or cycle rhythm of the market.

4️⃣ Forecasting the Next Cycle

When a valid average cycle length exists, the model projects the next expected cycle:

Time projection:

Adds avgCycleLength to the last cycle’s ending bar index to find where the next low should occur.

Price projection:

Estimates the vertical amplitude by taking the difference between the last two cycle lows (priceDiff).

Adds this same difference to the last low price to forecast the next probable low level.

The result is drawn as an orange dashed line extending into the future, representing the Next Expected Cycle.

5️⃣ Forecast Label

An orange label 🔮 appears at the projected future point showing:

Text:

🔮 Upcoming Cycle Forecast

Price:

The label marks the probable area and timing of the next cyclical low.

(Note: the date/time calculation currently multiplies bar count by 7 days, so it’s designed mainly for daily charts. On other timeframes, that conversion can be adapted.)

📊 How to Read It on the Chart

Visual Element Meaning Interpretation

Teal lines Completed historical cycles (low to low) Show actual periodic rhythm of the market

Orange dashed line Projection of the next expected cycle Anticipated path toward the next cyclical low

Orange label 🔮 Upcoming Cycle Forecast Displays expected price and bar location

Average cycle length Internal variable (bars between lows) Represents the dominant cycle period

📈 Interpretation

When teal segments show consistent spacing, the market is following a stable rhythm → cycles are predictable.

When cycle spacing shortens, the market is accelerating (volatility rising).

When it widens, the market is slowing down or entering accumulation.

The orange dashed line represents the next expected low zone:

If the market drops near this line → cyclical pattern confirmed.

If the market breaks well below → cycle amplitude has increased (trend weakening).

If the market rises above and delays → a new longer cycle may be forming.

🧠 Practical Use

Combine with oscillators (e.g., RSI or TSI) to confirm momentum alignment near projected lows.

Use in conjunction with volume to identify accumulation or exhaustion near the expected turning point.

Compare across timeframes: weekly cycles confirm long-term rhythm; daily cycles refine short-term entries.

⚡ Summary

Aspect Description

Purpose Detect and forecast recurring market cycles

Cycle basis Low-to-Low pivot analysis

Visuals Teal historical cycles + Orange forecast line

Forecast Next expected low (price and time)

Ideal timeframe Daily

Main outputs Average cycle length, next projected cycle, visual cycle map

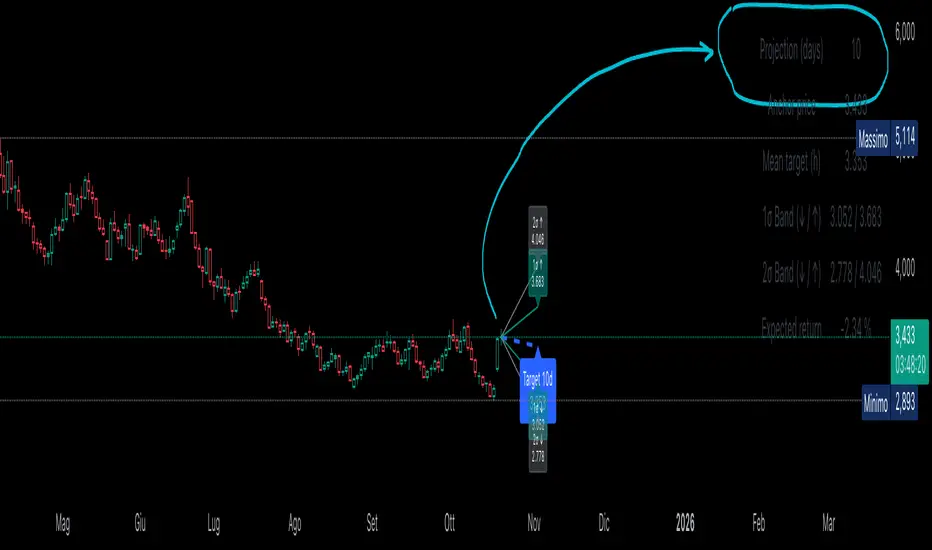

Statistical Projection over N Days (drift + σ) – v1.2 [EN]🧭 Overview

“Statistical Projection over N Days (drift + σ)” is a quantitative forecasting model that estimates the expected future price range of any asset over a chosen horizon (default = 10 days).

It combines average drift (trend direction) and historical volatility (σ) to produce a probabilistic cone of future price movement.

The indicator displays:

a blue dashed line (expected price path),

1σ / 2σ deviation bands (volatility envelopes),

and a summary table with the key forecast values and expected return.

⚙️ Core Logic (Explained Simply)

The indicator analyses recent price behavior to estimate two key elements:

the average daily tendency of the market (called drift), and

the average daily variability (called volatility).

Here’s how it works, step by step:

Measures daily percentage changes (using logarithmic returns) to understand how much the price typically moves from one bar to the next.

It then calculates the average of those returns over a chosen historical window (for example, 70 bars).

If the average is positive → the market has a rising tendency (upward drift).

If the average is negative → the market tends to decline (downward drift).

At the same time, it computes the standard deviation of those returns — this shows how “wide” the movements are, i.e. how volatile the asset is.

Using these two measures — drift and volatility — it estimates where the price is statistically expected to move over the next N bars:

The mean projection (blue dashed line) represents the most likely price path.

The 1σ and 2σ lines (teal and gray) define confidence zones, where price is expected to remain about 68% and 95% of the time, respectively.

The model updates continuously with every new bar, recalculating both drift and volatility, so the projection cone expands, contracts, or changes direction depending on the latest market behavior.

📉 Interpretation of the Blue Line

The blue dashed line (pMean) is the statistical forecast path of price over the next N bars.

🔹 When the blue line is below the current price

The recent drift (average log return) is negative → the model expects a gradual decline.

Interpretation:

The prevailing statistical bias is bearish — the market is expected to move lower toward equilibrium.

🔹 When the blue line is above the current price

The recent drift is positive → the model expects a continued rise.

Interpretation:

The price is statistically likely to trend upward, maintaining momentum in the direction of the current drift.

🔹 When the blue line is sloping upward

The mean projection pMean is rising with each new bar.

Indicates positive drift → the average daily return is positive.

Interpretation:

The asset is in a growth phase; volatility bands act as potential expansion corridors.

🔹 When the blue line is sloping downward

The mean projection pMean decreases bar after bar.

Indicates negative drift → average daily return is negative.

Interpretation:

The asset is in a corrective or declining phase, with volatility determining potential drawdown limits.

🔹 When the blue line is flat

The drift (μ) is approximately zero.

Interpretation:

The model sees no directional bias; price equilibrium dominates.

Expect a sideways range unless new volatility (σ) expansion occurs.

📈 How to Read the Entire Projection

Blue dashed line → expected mean path (most probable price trajectory).

Teal lines (±1σ) → statistically normal range (≈68% of future outcomes).

Gray lines (±2σ) → extreme bounds (≈95% of outcomes).

Labels on the right show exact forecast prices for each band.

If the actual price moves outside the gray 2σ range →

→ it signals volatility breakout or regime shift, meaning the past volatility no longer explains the present movement.

🧮 Summary Table

Located at the top-right corner, it provides:

Field Description

Projection (days) Number of bars used for projection (h).

Anchor price Starting close used for forecast.

Mean target (h) Expected price after h bars (blue line endpoint).

1σ Band (↓ / ↑) 68% confidence interval.

2σ Band (↓ / ↑) 95% confidence interval.

Expected return Projected % change from current close to mean target.

Colors can be customized — for example:

white headers,

aqua for anchor price,

lime for target,

orange/red for σ bands,

yellow for expected return.

🧠 Practical Meaning

Blue Line State Interpretation Bias

Above price, rising Ongoing positive drift Bullish

Below price, falling Negative drift Bearish

Flat, near price Neutral drift Sideways

Steep slope Strong directional momentum Trend confirmation

Price > +2σ band Excess volatility / overextension Possible correction

Price < −2σ band Undervaluation or panic Reversion likely

⚡ Summary

Aspect Description

Purpose Statistical forecast of expected price range

Method Drift (μ) + Volatility (σ) from log returns

Outputs Mean projection (blue), 1σ & 2σ bands, expected return

Interpretation Directional bias from blue line and its slope

Recommended timeframe Daily

Best use Trend confirmation, probabilistic target estimation, volatility analysis.

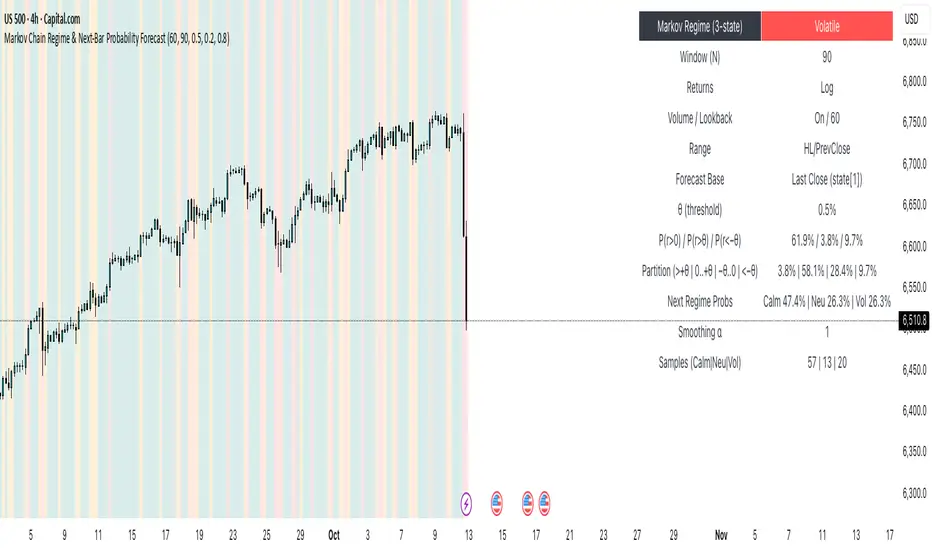

Markov Chain Regime & Next‑Bar Probability Forecast✨ What it is

A regime-aware, math-driven panel that forecasts the odds for the very next candle. It shows:

• P(next r > 0)

• P(next r > +θ)

• P(next r < −θ)

• A 4-bucket split of next-bar outcomes (>+θ | 0..+θ | −θ..0 | <−θ)

• Next-regime probabilities: Calm | Neutral | Volatile

🧠 Why the math is strong

• Markov regimes: Markets cluster in volatility “moods.” We learn a 3-state regime S∈{Calm, Neutral, Volatile} with a transition matrix A, where A = P(Sₜ₊₁=j | Sₜ=i).

• Condition on the future state: We estimate event odds given the next regime j—

q_pos(j)=P(rₜ₊₁>0 | Sₜ₊₁=j), q_gt(j)=P(rₜ₊₁>+θ | Sₜ₊₁=j), q_lt(j)=P(rₜ₊₁<−θ | Sₜ₊₁=j)—

and mix them with transitions from the current (or frozen) state sNow:

P(event) = Σⱼ A · q(event | j).

This mixture-of-regimes view (HMM-style one-step prediction) ties next-bar outcomes to where volatility is likely headed.

• Statistical hygiene: Laplace/Beta smoothing, minimum-sample gating, and unconditional fallbacks keep estimates stable. Heavy computations run on confirmed bars; “Freeze at close” avoids intrabar flicker.

📊 What each value means

• Regime label & background: 🟩 Calm, 🟧 Neutral, 🟥 Volatile — quick read of market context.

• P(next r > 0): Directional tilt for the very next bar.

• P(next r > +θ): Odds of an outsized positive move beyond θ.

• P(next r < −θ): Odds of an outsized negative move beyond −θ.

• Partition row: Distributes next-bar probability across four intuitive buckets; they ≈ sum to 100%.

• Next Regime Probs: Likelihood of switching to Calm/Neutral/Volatile on the next bar (row of A for the current/frozen state).

• Samples row: How many next-bar samples support each next-state estimate (a confidence cue).

• Smoothing α: The Laplace prior used to stabilize binary event rates.

⚙️ Inputs you control

• Returns: Log (default) or %

• Include Volume (z-score) + lookback

• Include Range (HL/PrevClose)

• Rolling window N (transitions & estimates)

• θ as percent (e.g., 0.5%)

• Freeze forecast at last close (recommended)

• Display toggles (plots, partition, samples)

🎯 How to use it

• Volatility awareness & sizing: Rising P(next regime = Volatile) → consider smaller size, wider stops, or skipping marginal entries.

• Breakout preparation: Elevated P(next r > +θ) highlights environments where range expansion is more likely; pair with your setup/trigger.

• Defense for mean-reversion: If P(next r < −θ) lifts while you’re late long (or P(next r > +θ) lifts while late short), tighten risk or wait for better context.

• Calibration tip: Start θ near your market’s typical bar size; adjust until “>+θ” flags truly meaningful moves for your timeframe.

📝 Method notes & limits

Activity features (|r|, volume z, range) are standardized; only positive z’s feed the composite activity score. Estimates adapt to instrument/timeframe; rare regimes or small windows increase variance (hence smoothing, sample gating, fallbacks). This is a context/forecast tool, not a standalone signal—combine with your entry/exit rules and risk management.

🧩 Strategies too

We also develop full strategy versions that use these probabilities for entries, filters, and position sizing. Like this publication if you’d like us to release the strategy edition next.

⚠️ Disclaimer

Educational use only. Not financial advice. Markets involve risk. Past performance does not guarantee future results.

Machine Learning Price Predictor: Ridge AR [Bitwardex]🔹Machine Learning Price Predictor: Ridge AR is a research-oriented indicator demonstrating the use of Regularized AutoRegression (Ridge AR) for short-term price forecasting.

The model combines autoregressive structure with Ridge regularization , providing stability under noisy or volatile market conditions.

The latest version introduces Bull and Bear signals , visually representing the current momentum phase and model direction directly on the chart.

Unlike traditional linear regression, Ridge AR minimizes overfitting, stabilizes coefficient dynamics, and enhances predictive consistency in correlated datasets.

The script plots:

Fit Line — in-sample fitted data;

Forecast Line — out-of-sample projection;

Trend Segments — color-coded bullish/bearish sections;

Bull/Bear Labels 🐂🐻 — dynamic visual signals showing directional bias.

Designed for researchers, students, and developers, this tool helps explore regularized time-series forecasting in Pine Script™.

🧩 Ridge AR Settings

Training Window — number of bars used for model training;

Forecast Horizon — forecast length (bars ahead);

AR Order — number of lags used as features;

Ridge Strength (λ) — regularization coefficient;

Damping Factor — exponential trend decay rate;

Trend Length — period for trend/volatility estimation;

Momentum Weight — strength of the recent move;

Mean Reversion — pullback intensity toward the mean.

🧮 Data Processing

Prefilter:

None — raw close price;

EMA — exponential smoothing;

SuperSmoother — Ehlers filter for noise reduction.

EMA Length, SuperSmoother Length — smoothing parameters.

🖥️ Display Settings

Update Mode:

Lock — static model;

Update Once Reached — rebuild after forecast horizon;

Continuous — update every bar.

Forecast Color — projection line color;

Bullish/Bearish Colors — colors for trend segments.

🐂🐻 Bull/Bear Signal System

The Bull/Bear Signal System adds directional visual cues to highlight local momentum shifts and model-based trend confirmation.

Bull (🐂) — appears when upward momentum is confirmed (momentum > 0) .

Displayed below the bar, colored with Bullish Color.

Bear (🐻) — appears when downward momentum is dominant (momentum < 0) .

Displayed above the bar, colored with Bearish Color.

Signals are generated during model recalculations or when the directional bias changes in Continuous mode.

These visual markers are analytical aids , not trading triggers.

🧠 Core Algorithmic Components

Regularized AutoRegression (Ridge AR):

Solves: (X′X+λI)−1X′y

to derive stable regression coefficients.

Matrix and Pseudoinverse Operations — implemented natively in Pine Script™.

Prefiltering (EMA / Ehlers SuperSmoother) — stabilizes noisy data.

Forecast Dynamics — integrates damping, momentum, and mean reversion.

Trend Visualization — color-coded bullish/bearish line segments.

Bull/Bear Signal Engine — visualizes real-time impulse direction.

📊 Applications

Academic and educational purposes;

Demonstration of Ridge Regression and AR models;

Analysis of bull/bear market phase transitions;

Visualization of time-series dependencies.

⚠️ Disclaimer

This script is provided for educational and research purposes only.

It does not provide trading or investment advice.

The author assumes no liability for financial losses resulting from its use.

Use responsibly and at your own risk.

KAMENICZKI PROSCAPLERPROSCAPLER is an advanced trading indicator that combines a dynamic channel with a prediction line for maximum accuracy and trading success. The indicator is designed for professional traders who need reliable signals with high success rates.

Adaptive Intelligence

Automatic optimal period detection - the indicator adapts to various market conditions

Intelligent timeframe settings - automatically optimizes periods based on TF

Dynamic adaptation - the channel changes according to volatility and trend.

High Signal Accuracy

Pearson R correlation - filters only strong trends with high reliability

Multi-timeframe confirmation - confirms signals on higher timeframe

Volatility and volume filters - eliminates false signals

RSI extreme values - captures only the best entry points

Prediction Line

Future price direction - shows where the price will move

Adaptive length - adapts to timeframe

Strong signals - when the entire prediction line is in the center of the channel

Quality Filters

Minimum Pearson R 0.5+ - only strong trends

Volume filter 1.2x - only signals with sufficient volume

ATR volatility filter - eliminates low volatility

RSI extreme levels - only at oversold/overbought values

Anomalies

Anomaly detection - captures exceptional opportunities

Bright yellow/pink color - immediately visible

Fast Reaction

Minimum trend bars = 1 - fast turning

Adaptive detection - immediate reaction to changes

Automatic optimizations - without manual settings

News & Volatility Filters

News filter - disables channel during high impact news

Volatility filter - protects against high volatility

Gap detection - filters dangerous gaps

Combined Filters

All filters must be met - maximum reliability

Multi-timeframe confirmation - double check

Pearson R validation - mathematical accuracy

Volume confirmation - institutional interest

Reaction Speed

Instant signals - without delay

Adaptive settings - automatic optimization

Fast turning - minimum 1 bar trend

Signal Accuracy

Quality filters increase success rate to 70-80%

Anomalies have 80-90% success rate

STRONG signals (prediction line in center) 85-95%

HAVE FUN :)

Foresight Cone (HoltxF1xVWAP) [KedArc Quant]Description:

This is a time-series forecasting indicator that estimates the next bar (F1) and projects a path a few bars ahead. It also draws a confidence cone based on how accurate the recent forecasts have been. You can optionally color the projection only when price agrees with VWAP.

Why it’s different

* One clear model: Everything comes from Holt’s trend-aware forecasting method—no mix of unrelated indicators.

* Transparent visuals: You see the next-bar estimate (F1), the forward projection, and a cone that widens or narrows based on recent forecast error.

* Context, not signals: The VWAP option only changes colors. It doesn’t add trade rules.

* No look-ahead: Accuracy is measured using the forecast made on the previous bar versus the current bar.

Inputs (what they mean)

* Source: Price series to forecast (default: Close).

* Preset: Quick profiles for fast, smooth, or momentum markets (see below).

* Alpha (Level): How fast the model reacts to new prices. Higher = faster, twitchier.

* Beta (Trend): How fast the model updates the slope. Higher = faster pivots, more flips in chop.

* Horizon: How many bars ahead to project. Bigger = wider cone.

* Residual Window: How many bars to judge recent accuracy. Bigger = steadier cone.

* Confidence Z: How wide the cone should be (typical setting ≈ “95% style” width).

* Show Bands / Draw Forward Path: Turn the cone and forward lines on/off.

* Color only when aligned with VWAP: Highlights projections only when price agrees with the trend side of VWAP.

* Colors / Show Panel: Styling plus a small panel with RMSE, MAPE, and trend slope.

Presets (when to pick which)

* Scalp / Fast (1-min): Very responsive; best for quick moves. More twitch in chop.

* Smooth Intraday (1–5 min): Calmer and steadier; a good default most days.

* Momentum / Breakout: Quicker slope tracking during strong pushes; may over-react in ranges.

* Custom: Set your own values if you know exactly what you want.

What is F1 here?

F1 is the model’s next-bar fair value. Crosses of price versus F1 can hint at short-term momentum shifts or mean-reversion, especially when viewed with VWAP or the cone.

How this helps

* Gives a baseline path of where price may drift and a cone that shows normal wiggle room.

* Helps you tell routine noise (inside cone) from information (edges or breaks outside the cone).

* Keeps you aware of short-term bias via the trend slope and F1.

How to use (step by step)

1. Add to chart → choose a Preset (start with Smooth Intraday).

2. Set Horizon around 8–15 bars for intraday.

3. (Optional) Turn on VWAP alignment to color only when price agrees with the trend side of VWAP.

4. Watch where price sits relative to the cone and F1:

* Inside = normal noise.

* At edges = stretched.

* Outside = possible regime change.

5. Check the panel: if RMSE/MAPE spike, expect a wider cone; consider a smoother preset or a higher timeframe.

6. Tweak Alpha/Beta only if needed: faster for momentum, slower for chop.

7. Combine with your own plan for entries, exits, and risk.

Accuracy Panel — what it tells you

Preset & Horizon: Shows which preset you’re using and how many bars ahead the projection goes. Longer horizons mean more uncertainty.

RMSE (error in price units): A “typical miss” measured in the chart’s currency (e.g., ₹).

Lower = tighter fit and a usually narrower cone. Rising = conditions getting noisier; the cone will widen.

MAPE (error in %): The same idea as RMSE but in percent.

Good for comparing different symbols or timeframes. Sudden spikes often hint at a regime change.

Slope T: The model’s short-term trend reading.

Positive = gentle up-bias; negative = gentle down-bias; near zero = mostly flat/drifty.

How to read it at a glance

Calm & directional: RMSE/MAPE steady or falling + Slope T positive (or negative) → trends tend to respect the cone’s mid/upper (or mid/lower) area.

Choppy/uncertain: RMSE/MAPE climbing or jumping → expect more whipsaw; rely more on the cone edges and higher-TF context.

Flat tape: Slope T near zero → mean-revert behavior is common; treat cone edges as stretch zones rather than breakout zones.

Warm-up & tweaks

Warm-up: Right after adding the indicator, the panel may be blank for a short time while it gathers enough bars.

Too twitchy? Switch to Smooth Intraday or increase the Residual Window.

Too slow? Use Scalp/Fast or Momentum/Breakout to react quicker.

Timeframe tips

* 1–3 min: Scalp/Fast or Momentum/Breakout; horizon \~8–12.

* 5–15 min: Smooth Intraday; horizon \~12–15.

* 30–60 min+: Consider a larger residual window for a steadier cone.

FAQ

Q: Is this a strategy or an indicator?

A: It’s an indicator only. It does not place orders, TP/SL, or run backtests.

Q: Does it repaint?

A: The next-bar estimate (F1) and the cone are calculated using only information available at that time. The forward path is a projection drawn on the last bar and will naturally update as new bars arrive. Historical bars aren’t revised with future data.

Q: What is F1?

A: F1 is the indicator’s best guess for the next bar.

Price crossing above/below F1 can hint at short-term momentum shifts or mean-reversion.

Q: What do “Alpha” and “Beta” do?

A: Alpha controls how fast the indicator reacts to new prices

(higher = faster, twitchier). Beta controls how fast the slope updates (higher = quicker pivots, more flips in chop).

Q: Why does the cone width change?

A: It reflects recent forecast accuracy. When the market gets noisy, the cone widens. When the tape is calm, it narrows.

Q: What does the Accuracy Panel tell me?

A:

* Preset & Horizon you’re using.

* RMSE: typical forecast miss in price units.

* MAPE: typical forecast miss in percent.

* Slope T: short-term trend reading (up, down, or flat).

If RMSE/MAPE rise, expect a wider cone and more whipsaw.

Q: The panel shows “…” or looks empty. Why?

A: It needs a short warm-up to gather enough bars. This is normal after you add the indicator or change settings/timeframes.

Q: Which timeframe is best?

A:

* 1–3 min: Scalp/Fast or Momentum/Breakout, horizon \~8–12.

* 5–15 min: Smooth Intraday, horizon \~12–15.

Higher timeframes work too; consider a larger residual window for steadier cones.

Q: Which preset should I start with?

A: Start with Smooth Intraday. If the market is trending hard, try Momentum/Breakout.

For very quick tapes, use Scalp/Fast. Switch back if things get choppy.

Q: What does the VWAP option do?

A: It only changes colors (highlights when price agrees with the trend side of VWAP).

It does not add or remove signals.

Q: Are there alerts?

A: Yes—alerts for price crossing F1 (up/down). Use “Once per bar close” to reduce noise on fast charts.

Q: Can I use this on stocks, futures, crypto, or FX?

A: Yes. It works on any symbol/timeframe. You may want to adjust Horizon and the Residual Window based on volatility.

Q: Can I use it with Heikin Ashi or other non-standard bars?

A: You can, but remember you’re forecasting the synthetic series of those bars. For pure price behavior, use regular candles.

Q: The cone feels too wide/too narrow. What do I change?

A:

* Too wide: lower Alpha/Beta a bit or increase the Residual Window.

* Too narrow (misses moves): raise Alpha/Beta slightly or try Momentum/Breakout.

Q: Why do results change when I switch timeframe or symbol?

A: Different noise levels and trends. The accuracy stats reset per chart, so the cone adapts to each context.

Q: Any limits or gotchas?

A: Extremely large Horizon may hit TradingView’s line-object limits; reduce Horizon or turn

off extra visuals if needed. Big gaps or news spikes will widen errors—expect the cone to react.

Q: Can this predict exact future prices?

A: No. It provides a baseline path and context. Always combine with your own rules and risk management.

Glossary

* TS (Time Series): Data over time (prices).

* Holt’s Method: A forecasting approach that tracks a current level and a trend to predict the next bars.

* F1: The indicator’s best guess for the next bar.

* F(h): The projected value h bars ahead.

* VWAP: Volume-Weighted Average Price—used here for optional color alignment.

* RMSE: Typical forecast miss in price units (how far off, on average).

* MAPE: Typical forecast miss in percent (scale-free, easy to compare).

Notes & limitations

* The panel needs a short warm-up; stats may be blank at first.

* The cone reflects recent conditions; sudden volatility changes will widen it.

* This is a tool for context. It does not place trades and does not promise results.

⚠️ Disclaimer

This script is provided for educational purposes only.

Past performance does not guarantee future results.

Trading involves risk, and users should exercise caution and use proper risk management when applying this strategy.

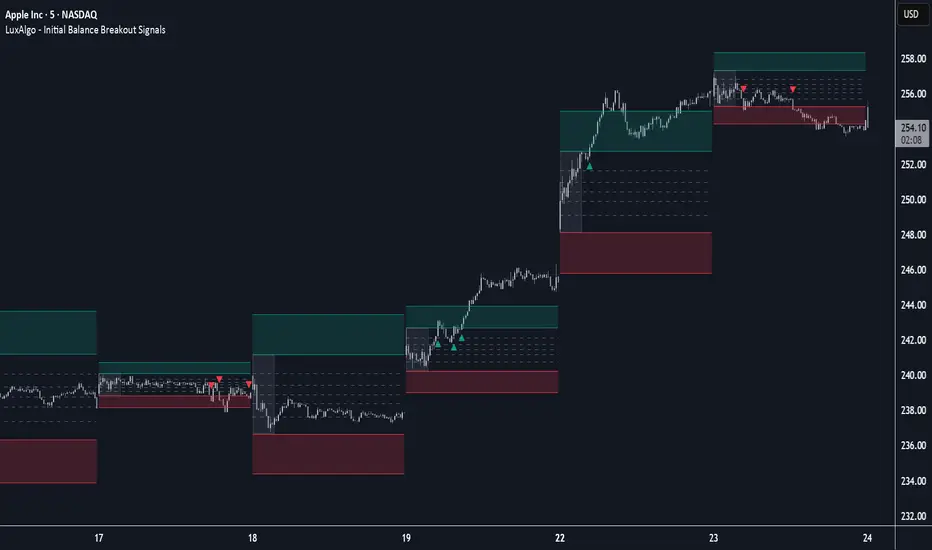

Initial Balance Breakout Signals [LuxAlgo]The Initial Balance Breakout Signals help traders identify breakouts of the Initial Balance (IB) range.

The indicator includes automatic detection of IB or can use custom sessions, highlights top and bottom IB extensions, custom Fibonacci levels, and goes further with an IB forecast with two different modes.

🔶 USAGE

The initial balance is the price range made within the first hour of the trading session. It is an intraday concept based on the idea that high volume and volatility enter the market through institutional trading at the start of the session, setting the tone for the rest of the day.

The initial balance is useful for gauging market sentiment, or, in other words, the relationship between buyers and sellers.

Bullish sentiment: Price trades above the IB range.

Mixed sentiment: Price trades within the IB range.

Bearish sentiment: Price trades below the IB range.

The initial balance high and low are important levels that many traders use to gauge sentiment. There are two main ideas behind trading around the IB range.

IB Extreme Breakout: When the price breaks and holds the IB high or low, there is a high probability that the price will continue in that direction.

IB Extreme Rejection: When the price tries to break those levels but fails, there is a high probability that it will reach the opposite IB extreme.

This indicator is a complete Initial Balance toolset with custom sessions, breakout signals, IB extensions, Fibonacci retracements, and an IB forecast. All of these features will be explained in the following sections.

🔹 Custom Sessions and Signals

By default, sessions for Initial Balance and breakout signals are in Auto mode. This means that Initial Balance takes the first hour of the trading session and shows breakout signals for the rest of the session.

With this option, traders can use the tool for open range trading, making it highly versatile. The concept behind open range (OR) is the same as that of initial balance (IB), but in OR, the range is determined by the first minute, three or five minutes, or up to the first 30 minutes of the trading session.

As shown in the image above, the top chart uses the Auto feature for the IB and Breakouts sessions. The bottom chart has the Auto feature disabled to use custom sessions for both parameters. In this case, the first three minutes of the trading session are used, turning the tool into an Open Range trading indicator.

This chart shows another example of using custom sessions to display overnight NASDAQ futures sessions.

The left chart shows a custom session from the Tokyo open to the London open, and the right chart shows a custom session from the London open to the New York open.

The chart shows both the Asian and European sessions, their top and bottom extremes, and the breakout signals from those extremes.

🔹 Initial Balance Extensions

Traders can easily extend both extremes of the Initial Balance to display their preferred targets for breakouts. Enable or disable any of them and set the IB percentage to use for the extension.

As the chart shows, the percentage selected on the settings panel directly affects the displayed levels.

Setting 25 means the tool will use a quarter of the detected initial balance range for extensions beyond the IB extremes. Setting 100 means the full IB range will be used.

Traders can use these extensions as targets for breakout signals.

🔹 Fibonacci Levels

Traders can display default or custom Fibonacci levels on the IB range to trade retracements and assess the strength of market movements. Each level can be enabled or disabled and customized by level, color, and line style.

As we can see on the chart, after the IB was completed, prices were unable to fall below the 0.236 Fibonacci level. This indicates significant bullish pressure, so it is expected that prices will rise.

Traders can use these levels as guidelines to assess the strength of the side trying to penetrate the IB. In this case, the sellers were unable to move the market beyond the first level.

🔹 Initial Balance Forecast

The tool features two different forecasting methods for the current IB. By default, it takes the average of the last ten values and applies a multiplier of one.

IB Against Previous Open: averages the difference between IB extremes and the open of the previous session.

Filter by current day of the week: averages the difference between IB extremes and the open of the current session for the same day of the week.

This feature allows traders to see the difference between the current IB and the average of the last IBs. It makes it very easy to interpret: if the current IB is higher than the average, buyers are in control; if it is lower than the average, sellers are in control.

For example, on the left side of the chart, we can see that the last day was very bullish because the IB was completely above the forecasted value. This is the IB mean of the last ten trading days.

On the right, we can see that on Monday, September 15, the IB traded slightly higher but within the forecasted value of the IB mean of the last ten Mondays. In this case, it is within expectations.

🔶 SETTINGS

Display Last X IBs: Select how many IBs to display.

Initial Balance: Choose a custom session or enable the Auto feature.

Breakouts: Enable or disable breakouts. Choose custom session or enable the Auto feature.

🔹 Extensions

Top Extension: Enable or disable the top extension and choose the percentage of IB to use.

Bottom extension: Enable or disable the bottom extension and choose the percentage of IB to use.

🔹 Fibonacci Levels

Display Fibonacci: Enable or disable Fibonacci levels.

Reverse: Reverse Fibonacci levels.

Levels, Colors & Style

Display Labels: Enable or disable labels and choose text size.

🔹 Forecast

Display Forecast: Select the forecast method.

- IB Against Previous Open: Calculates the average difference between the IB high and low and the previous day's IB open price.

- Filter by Current Day of Week: Calculates the average difference between the IB high and low and the IB open price for the same day of the week.

Forecast Memory: The number of data points used to calculate the average.

Forecast Multiplier: This multiplier will be applied to the average. Bigger numbers will result in wider predicted ranges.

Forecast Colors: Choose from a variety of colors.

Forecast Style: Choose a line style.

🔹 Style

Initial Balance Colors

Extension Transparency: Choose the extension's transparency. 0 is solid, and 100 is fully transparent.

Implied Volatility RangeThe Implied Volatility Range is a forward-looking tool that transforms option market data into probability ranges for future prices. Based on the lognormal distribution of asset prices assumed in modern option pricing models, it converts the implied volatility curve into a volatility cone with dynamic labels that show the market’s expectations for the price distribution at a specific point in time. At the selected future date, it displays projected price levels and their percentage change from today’s close across 1, 2, and 3 standard deviation (σ) ranges:

1σ range = ~68.2% probability the price will remain within this range.

2σ range = ~95.4% probability the price will remain within this range.

3σ range = ~99.7% probability the price will remain within this range.

What makes this indicator especially useful is its ability to incorporate implied volatility skew. When only ATM IV (%) is entered, the indicator displays the standard Black–Scholes lognormal distribution. By adding High IV (%) and Low IV (%) values tied to strikes above and below the current price, the indicator interpolates between these inputs to approximate the implied volatility skew. This adjustment produces a market-implied probability distribution that indicates whether the option market is leaning bullish or bearish, based on the data entered in the menu:

ATM IV (%) = Implied volatility at the current spot price (at-the-money).

High IV (%) = Implied volatility at a strike above the current spot price.

High Strike = Strike price corresponding to the High IV input (OTM call).

Low IV (%) = Implied volatility at a strike below the current spot price.

Low Strike = Strike price corresponding to the Low IV input (OTM put).

Expiration (Day, Month, Year) = Option expiration date for the projection.

Once these inputs are entered, the indicator calculates implied probability ranges and, if both High IV and Low IV values are provided, adjusts for skew to approximate the option market’s distribution. If no implied volatility data is supplied, the indicator defaults to a lognormal distribution based on historical volatility, using past realized volatility over the same forward horizon. This keeps the tool functional even without implied volatility inputs, though in that case the output represents only an approximation of ATM IV, not the actual market view.

In summary, the Implied Volatility Range is a powerful tool that translates implied volatility inputs into a clear and practical estimate of the market’s expectations for future prices. It allows traders to visualize the probability of price ranges while also highlighting directional bias, a dimension often difficult to interpret from traditional implied volatility charts. It should be emphasized, however, that this tool reflects only the market’s expectations at a specific point in time, which may change as new information and trading activity reshape implied volatility.

Cyclic Reversal Engine [AlgoPoint]Overview

Most indicators focus on price and momentum, but they often ignore a critical third dimension: time. Markets move in rhythmic cycles of expansion and contraction, but these cycles are not fixed; they speed up in trending markets and slow down in choppy conditions.

The Cyclic Reversal Engine is an advanced analytical tool designed to decode this rhythm. Instead of relying on static, lagging formulas, this indicator learns from past market behavior to anticipate when the current trend is statistically likely to reach its exhaustion point, providing high-probability reversal signals.

It achieves this by combining a sophisticated time analysis with a robust price-action confirmation.

How It Works: The Core Logic

The indicator operates on a multi-stage process to identify potential turning points in the market.

1. Market Regime Analysis (The Brain): Before analyzing any cycles, the indicator first diagnoses the current "personality" of the market. Using a combination of the ADX, Choppiness Index, and RSI, it classifies the market into one of three primary regimes:

- Trending: Strong, directional movement.

- Ranging: Sideways, non-directional chop.

- Reversal: An over-extended state (overbought/oversold) where a turn is imminent.

2. Adaptive Cycle Learning (The "Machine Learning" Aspect): This is the indicator's smartest feature. It constantly analyzes past cycles by measuring the bar-count between significant swing highs and swing lows. Crucially, it learns the average cycle duration for each specific market regime. For example, it learns that "in a strong trending market, a new swing low tends to occur every 35 bars," while "in a ranging market, this extends to 60 bars."

3. The Countdown & Timing Signal: The indicator identifies the last major swing high or low and starts a bar-by-bar countdown. Based on the current market regime, it selects the appropriate learned cycle length from its memory. When the bar count approaches this adaptive target, the indicator determines that a reversal is "due" from a timing perspective.

4. Price Confirmation (The Trigger): A signal is never generated based on timing alone. Once the timing condition is met (the cycle is "due"), the indicator waits for a final price-action confirmation. The default confirmation is the RSI entering an extreme overbought or oversold zone, signaling momentum exhaustion. The signal is only triggered when Time + Price Confirmation align.

How to Use This Indicator

- The Dashboard: The panel in the bottom-right corner is your command center.

- Market Regime: Shows the current market personality analyzed by the engine.

- Adaptive Cycle / Bar Count: This is the core of the indicator. It shows the target cycle length for the current regime (e.g., 50) and the current bar count since the last swing point (e.g., 45). The background turns orange when the bar count enters the "due zone," indicating that you should be on high alert for a reversal.

- BUY/SELL Signals: A label appears on the chart only when the two primary conditions are met:

The timing is right (Bar Count has reached the Adaptive Cycle target).

The price confirms exhaustion (RSI is in an extreme zone).

A BUY signal suggests a downtrend cycle is likely complete, and a SELL signal suggests an uptrend cycle is likely complete.

Key Settings

- Pivot Lookback: Controls the sensitivity of the swing point detection. Higher values will identify more significant, longer-term cycles.

- Market Regime Engine: The ADX, Choppiness, and RSI settings can be fine-tuned to adjust how the indicator classifies the market's personality.

- Require Price Confirmation: You can toggle the RSI confirmation on or off. It is highly recommended to keep it enabled for higher-quality signals.

Daily Seasonality Strength + Prediction TableDaily Seasonality Strength + Prediction Table

Return Estimates:

This indicator uses historical price data to calculate average returns for each day (of the week or month) and uses these to predict the next day’s return.

Seasonality Strength:

It measures seasonality strength by comparing predicted returns with actual returns, using the inverse of MSE (higher values mean stronger seasonality).

supports up to 10 assets

This script is for informational and educational purposes only. It does not constitute financial, investment, or trading advice. I am not a financial advisor. Any decisions you make based on this indicator are your own responsibility. Always do your own research and consult with a qualified financial professional before making any investment decisions.

Past performance is no guarantee of future results. The value of the instruments may fluctuate and is not guaranteed

Seasonality Monte Carlo Forecaster [BackQuant]Seasonality Monte Carlo Forecaster

Plain-English overview

This tool projects a cone of plausible future prices by combining two ideas that traders already use intuitively: seasonality and uncertainty. It watches how your market typically behaves around this calendar date, turns that seasonal tendency into a small daily “drift,” then runs many randomized price paths forward to estimate where price could land tomorrow, next week, or a month from now. The result is a probability cone with a clear expected path, plus optional overlays that show how past years tended to move from this point on the calendar. It is a planning tool, not a crystal ball: the goal is to quantify ranges and odds so you can size, place stops, set targets, and time entries with more realism.

What Monte Carlo is and why quants rely on it

• Definition . Monte Carlo simulation is a way to answer “what might happen next?” when there is randomness in the system. Instead of producing a single forecast, it generates thousands of alternate futures by repeatedly sampling random shocks and adding them to a model of how prices evolve.

• Why it is used . Markets are noisy. A single point forecast hides risk. Monte Carlo gives a distribution of outcomes so you can reason in probabilities: the median path, the 68% band, the 95% band, tail risks, and the chance of hitting a specific level within a horizon.

• Core strengths in quant finance .

– Path-dependent questions : “What is the probability we touch a stop before a target?” “What is the expected drawdown on the way to my objective?”

– Pricing and risk : Useful for path-dependent options, Value-at-Risk (VaR), expected shortfall (CVaR), stress paths, and scenario analysis when closed-form formulas are unrealistic.

– Planning under uncertainty : Portfolio construction and rebalancing rules can be tested against a cloud of plausible futures rather than a single guess.

• Why it fits trading workflows . It turns gut feel like “seasonality is supportive here” into quantitative ranges: “median path suggests +X% with a 68% band of ±Y%; stop at Z has only ~16% odds of being tagged in N days.”

How this indicator builds its probability cone

1) Seasonal pattern discovery

The script builds two day-of-year maps as new data arrives:

• A return map where each calendar day stores an exponentially smoothed average of that day’s log return (yesterday→today). The smoothing (90% old, 10% new) behaves like an EWMA, letting older seasons matter while adapting to new information.

• A volatility map that tracks the typical absolute return for the same calendar day.

It calculates the day-of-year carefully (with leap-year adjustment) and indexes into a 365-slot seasonal array so “March 18” is compared with past March 18ths. This becomes the seasonal bias that gently nudges simulations up or down on each forecast day.

2) Choice of randomness engine

You can pick how the future shocks are generated:

• Daily mode uses a Gaussian draw with the seasonal bias as the mean and a volatility that comes from realized returns, scaled down to avoid over-fitting. It relies on the Box–Muller transform internally to turn two uniform random numbers into one normal shock.

• Weekly mode uses bootstrap sampling from the seasonal return history (resampling actual historical daily drifts and then blending in a fraction of the seasonal bias). Bootstrapping is robust when the empirical distribution has asymmetry or fatter tails than a normal distribution.

Both modes seed their random draws deterministically per path and day, which makes plots reproducible bar-to-bar and avoids flickering bands.

3) Volatility scaling to current conditions

Markets do not always live in average volatility. The engine computes a simple volatility factor from ATR(20)/price and scales the simulated shocks up or down within sensible bounds (clamped between 0.5× and 2.0×). When the current regime is quiet, the cone narrows; when ranges expand, the cone widens. This prevents the classic mistake of projecting calm markets into a storm or vice versa.

4) Many futures, summarized by percentiles

The model generates a matrix of price paths (capped at 100 runs for performance inside TradingView), each path stepping forward for your selected horizon. For each forecast day it sorts the simulated prices and pulls key percentiles:

• 5th and 95th → approximate 95% band (outer cone).

• 16th and 84th → approximate 68% band (inner cone).

• 50th → the median or “expected path.”

These are drawn as polylines so you can immediately see central tendency and dispersion.

5) A historical overlay (optional)

Turn on the overlay to sketch a dotted path of what a purely seasonal projection would look like for the next ~30 days using only the return map, no randomness. This is not a forecast; it is a visual reminder of the seasonal drift you are biasing toward.

Inputs you control and how to think about them

Monte Carlo Simulation

• Price Series for Calculation . The source series, typically close.

• Enable Probability Forecasts . Master switch for simulation and drawing.

• Simulation Iterations . Requested number of paths to run. Internally capped at 100 to protect performance, which is generally enough to estimate the percentiles for a trading chart. If you need ultra-smooth bands, shorten the horizon.

• Forecast Days Ahead . The length of the cone. Longer horizons dilute seasonal signal and widen uncertainty.

• Probability Bands . Draw all bands, just 95%, just 68%, or a custom level (display logic remains 68/95 internally; the custom number is for labeling and color choice).

• Pattern Resolution . Daily leans on day-of-year effects like “turn-of-month” or holiday patterns. Weekly biases toward day-of-week tendencies and bootstraps from history.

• Volatility Scaling . On by default so the cone respects today’s range context.

Plotting & UI

• Probability Cone . Plots the outer and inner percentile envelopes.

• Expected Path . Plots the median line through the cone.

• Historical Overlay . Dotted seasonal-only projection for context.

• Band Transparency/Colors . Customize primary (outer) and secondary (inner) band colors and the mean path color. Use higher transparency for cleaner charts.

What appears on your chart

• A cone starting at the most recent bar, fanning outward. The outer lines are the ~95% band; the inner lines are the ~68% band.

• A median path (default blue) running through the center of the cone.

• An info panel on the final historical bar that summarizes simulation count, forecast days, number of seasonal patterns learned, the current day-of-year, expected percentage return to the median, and the approximate 95% half-range in percent.

• Optional historical seasonal path drawn as dotted segments for the next 30 bars.

How to use it in trading

1) Position sizing and stop logic

The cone translates “volatility plus seasonality” into distances.

• Put stops outside the inner band if you want only ~16% odds of a stop-out due to noise before your thesis can play.

• Size positions so that a test of the inner band is survivable and a test of the outer band is rare but acceptable.

• If your target sits inside the 68% band at your horizon, the payoff is likely modest; outside the 68% but inside the 95% can justify “one-good-push” trades; beyond the 95% band is a low-probability flyer—consider scaling plans or optionality.

2) Entry timing with seasonal bias

When the median path slopes up from this calendar date and the cone is relatively narrow, a pullback toward the lower inner band can be a high-quality entry with a tight invalidation. If the median slopes down, fade rallies toward the upper band or step aside if it clashes with your system.

3) Target selection

Project your time horizon to N bars ahead, then pick targets around the median or the opposite inner band depending on your style. You can also anchor dynamic take-profits to the moving median as new bars arrive.

4) Scenario planning & “what-ifs”

Before events, glance at the cone: if the 95% band already spans a huge range, trade smaller, expect whips, and avoid placing stops at obvious band edges. If the cone is unusually tight, consider breakout tactics and be ready to add if volatility expands beyond the inner band with follow-through.

5) Options and vol tactics

• When the cone is tight : Prefer long gamma structures (debit spreads) only if you expect a regime shift; otherwise premium selling may dominate.

• When the cone is wide : Debit structures benefit from range; credit spreads need wider wings or smaller size. Align with your separate IV metrics.

Reading the probability cone like a pro

• Cone slope = seasonal drift. Upward slope means the calendar has historically favored positive drift from this date, downward slope the opposite.

• Cone width = regime volatility. A widening fan tells you that uncertainty grows fast; a narrow cone says the market typically stays contained.

• Mean vs. price gap . If spot trades well above the median path and the upper band, mean-reversion risk is high. If spot presses the lower inner band in an up-sloping cone, you are in the “buy fear” zone.

• Touches and pierces . Touching the inner band is common noise; piercing it with momentum signals potential regime change; the outer band should be rare and often brings snap-backs unless there is a structural catalyst.

Methodological notes (what the code actually does)

• Log returns are used for additivity and better statistical behavior: sim_ret is applied via exp(sim_ret) to evolve price.

• Seasonal arrays are updated online with EWMA (90/10) so the model keeps learning as each bar arrives.

• Leap years are handled; indexing still normalizes into a 365-slot map so the seasonal pattern remains stable.

• Gaussian engine (Daily mode) centers shocks on the seasonal bias with a conservative standard deviation.

• Bootstrap engine (Weekly mode) resamples from observed seasonal returns and adds a fraction of the bias, which captures skew and fat tails better.

• Volatility adjustment multiplies each daily shock by a factor derived from ATR(20)/price, clamped between 0.5 and 2.0 to avoid extreme cones.

• Performance guardrails : simulations are capped at 100 paths; the probability cone uses polylines (no heavy fills) and only draws on the last confirmed bar to keep charts responsive.

• Prerequisite data : at least ~30 seasonal entries are required before the model will draw a cone; otherwise it waits for more history.

Strengths and limitations

• Strengths :

– Probabilistic thinking replaces single-point guessing.

– Seasonality adds a small but meaningful directional bias that many markets exhibit.

– Volatility scaling adapts to the current regime so the cone stays realistic.

• Limitations :

– Seasonality can break around structural changes, policy shifts, or one-off events.

– The number of paths is performance-limited; percentile estimates are good for trading, not for academic precision.

– The model assumes tomorrow’s randomness resembles recent randomness; if regime shifts violently, the cone will lag until the EWMA adapts.

– Holidays and missing sessions can thin the seasonal sample for some assets; be cautious with very short histories.

Tuning guide

• Horizon : 10–20 bars for tactical trades; 30+ for swing planning when you care more about broad ranges than precise targets.

• Iterations : The default 100 is enough for stable 5/16/50/84/95 percentiles. If you crave smoother lines, shorten the horizon or run on higher timeframes.

• Daily vs. Weekly : Daily for equities and crypto where month-end and turn-of-month effects matter; Weekly for futures and FX where day-of-week behavior is strong.

• Volatility scaling : Keep it on. Turn off only when you intentionally want a “pure seasonality” cone unaffected by current turbulence.

Workflow examples

• Swing continuation : Cone slopes up, price pulls into the lower inner band, your system fires. Enter near the band, stop just outside the outer line for the next 3–5 bars, target near the median or the opposite inner band.

• Fade extremes : Cone is flat or down, price gaps to the upper outer band on news, then stalls. Favor mean-reversion toward the median, size small if volatility scaling is elevated.

• Event play : Before CPI or earnings on a proxy index, check cone width. If the inner band is already wide, cut size or prefer options structures that benefit from range.

Good habits

• Pair the cone with your entry engine (breakout, pullback, order flow). Let Monte Carlo do range math; let your system do signal quality.

• Do not anchor blindly to the median; recalc after each bar. When the cone’s slope flips or width jumps, the plan should adapt.

• Validate seasonality for your symbol and timeframe; not every market has strong calendar effects.

Summary

The Seasonality Monte Carlo Forecaster wraps institutional risk planning into a single overlay: a data-driven seasonal drift, realistic volatility scaling, and a probabilistic cone that answers “where could we be, with what odds?” within your trading horizon. Use it to place stops where randomness is less likely to take you out, to set targets aligned with realistic travel, and to size positions with confidence born from distributions rather than hunches. It will not predict the future, but it will keep your decisions anchored to probabilities—the language markets actually speak.

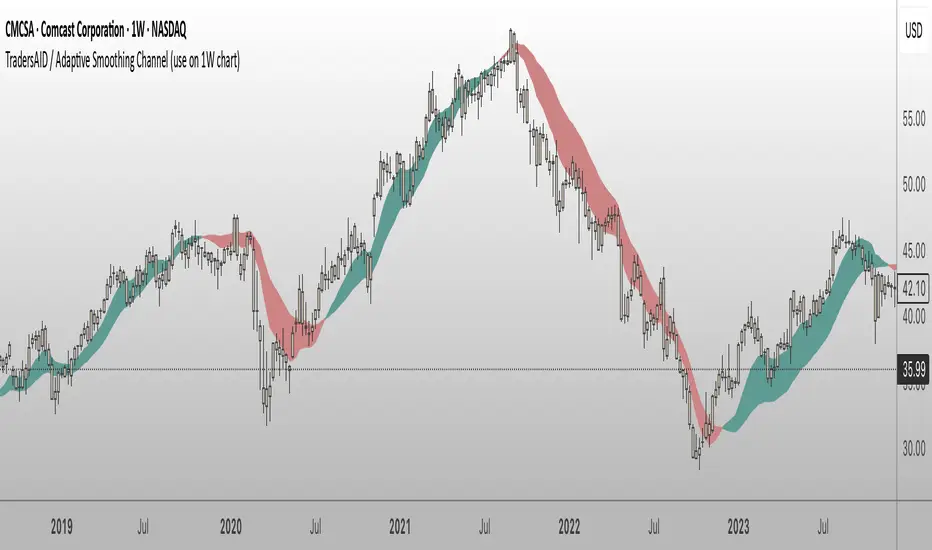

TradersAID / Adaptive Smoothing Channel (use on 1W chart)TradersAID – Adaptive Smoothing Channel (use on 1-Week chart)

Overview

TradersAID – Adaptive Smoothing Channel is a two-line price overlay designed to help traders interpret trend structure and shifting momentum zones on the 1-week chart only.

Unlike traditional moving averages or fixed smoothing methods, this tool uses an adaptive approach inspired by Kalman filtering — a concept widely used in robotics and control systems to track signals in noisy environments. Applied to price, this allows the band to adapt to directional flow and volatility while filtering out distracting short-term fluctuations.

1.What It Does

This tool builds a dynamic corridor around price using:

• A faster line that follows near-term directional movement

• A slower line that anchors broader market structure

Together, they form a responsive band that:

• Tilts with trend direction (via slope)

• Expands or contracts with volatility

• Fills the space between to show directional rhythm

It’s especially useful for observing how price moves within sustained trends or compression zones, helping traders visually interpret market structure with more clarity.

2. How to Use It

• Trend Structure:

Follow the slope of the band to understand overall direction. A narrowing band may indicate consolidation; a widening band may reflect strong follow-through.

• Momentum Compression Zones:

Watch for tightening distance between the lines — this may signal the market is preparing for a structural transition or breakout.

• Clarity Layer:

Overlay this tool with others (e.g. TradersAID Warning Dots) to reduce noise and improve decision context.

3. Key Features

• Dual Adaptive Lines: One fast, one slow — capturing different time dynamics

• Shaded Fill Zone: Highlights directional bias and rhythm

• 3 Reaction Modes: Slow / Regular / Fast for different sensitivities

• Overlay Style: Plots directly on price

• Minimalist Layout: Clean visual language

4. Technical Basis (Why It’s Closed Source)

This tool is based on a custom smoothing logic inspired by Kalman filtering, adapted specifically for charting market structure.

While it does not replicate a full Kalman system, it borrows key principles: dynamically adjusting to noisy input while maintaining structural clarity.

The algorithm was developed internally to provide a visual layer that integrates into the broader TradersAID analysis system — offering something distinct from public indicators. Its behavior, flexibility, and integration were designed to serve advanced structural analysis, and as such, the script is closed to protect proprietary logic and intellectual property.

5. Settings

• Mode Selector: Fast / Regular / Slow

• Color Fill Toggle & Styling

• Frame Lock:

✅ This script is built to work exclusively on the 1-week timeframe.

6. Disclaimer

This tool is for educational and informational purposes only. It does not offer financial advice or generate trading signals. Always use with your own strategy and discretion.

BeeQuant - Hive Bars🔶 OVERVIEW

The "Hive Bars" indicator is a truly revolutionary analytical instrument, meticulously engineered to transcend the limitations of conventional price charting and unveil the profound, underlying essence of market dynamics. Imagine possessing a sophisticated visual engine that intelligently reconstructs raw price data into unique, dynamically consolidated "Hive Bars." These specialized constructs intuitively reveal the dominant market momentum and highlight high-conviction signals often obscured by the ubiquitous noise of traditional candlesticks. This indicator acts as a precision filter, illuminating exactly when pivotal shifts are occurring by coloring these reconstructed units with an adaptive, unparalleled accuracy. It is expertly crafted for the discerning trader seeking an undeniable analytical advantage, offering a fresh, meticulously refined perspective that enables the discernment of concealed patterns, fostering more decisive and confident trading actions. Crucially, "Hive Bars" now feature proactive, real-time alert capabilities, ensuring no critical market inflection point ever goes unnoticed.

__________________________________________________________________________

🧠 CONCEPTS

At its intellectual core, the "Hive Bars" indicator operates upon an advanced, proprietary framework that fundamentally reinterprets market data. It presents this refined information through its unique "Hive Bars"—specialized visual constructs that dynamically encapsulate the consolidated spirit and true directional bias of price action, delivering unparalleled clarity.