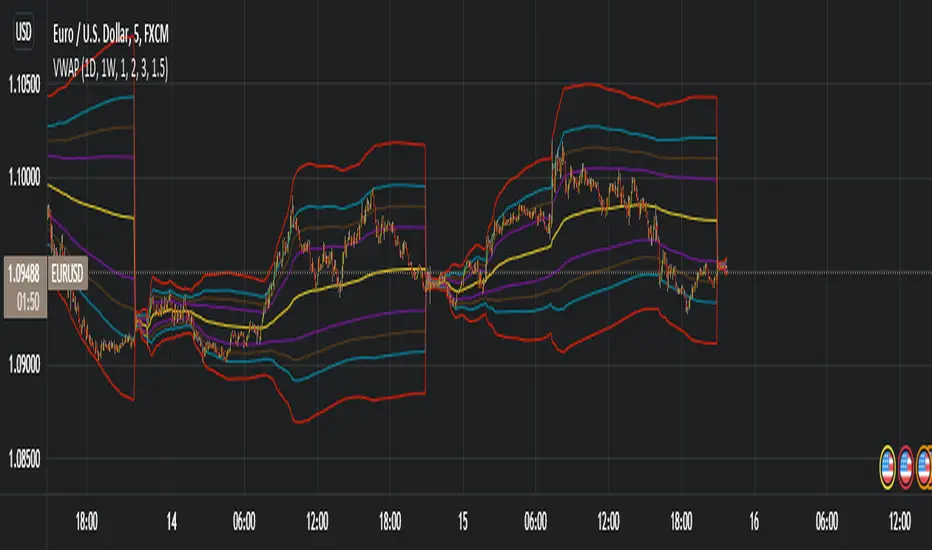

Neo Matrix

What is NeonMoney Indicator?

NeonMoney Indicator is a trend following indicator which gives strong support and resistance indications with some moving averages.

Description

After the long research of 2 years along with 100’s of indicators & oscillators we have created this wonderful indicator which can avoid signals in a choppy market & gives perfect signal to buy and sell at a right time with high winning probability and higher reward to risk.

Main part of this indicator is timeframe period that is it shifts from one to another pivots , vwap and MAs tf automatically which helps in top down analysis.

This indicator is made with Vwap , MA, cpr and fibonacci pivots calculations. It can be useful to trade every market like in crypto, forex, commodities and as well as stock market . To use this indicator trader must have basic understanding of candle pattern and chart pattern identification studies with moving averages retrenchments.

This indicator works well & gives better results if you have moving average retrenchment knowledge. When candles are retrenching specific moving average line then also sometimes traders get confuse whether to enter with moving average direction / favor or not. So, to come out from this confusion this indicator is very useful. Because it gives signal in moving average favors and target at pivot levels. So ultimately traders gain some confident on his/her trade that he/she is in the right side of the market.

Another advantage of this indicator is in some of the criteria it gives fix signal in-between the candle formation & once signal is given then it will not change.

About uses instruction and components.

Time frame – 1m, 3m , 15m, 1H, 4H, DailyTF

Components: Vwap , MAs, CPR , and Fibonacci Pivots .

Dotted line - Vwap

Straight gray line and zone - CPR

Curvy Gray lines - MAs

Colorful lines - Fibonacci pivots

D-VWAP

Donchian Anchored Vwap + HandoffsIn this script I try to incorporate Brian Shannon's Anchored VWAP hand off system into an automated initial anchoring system using Donchian Highs and Lows.

I have also added an average of all the hand-off vwaps.

Higher values in "Donchain Lookback" will display longer term sentiment and vice versa.

*Credit to trader dysrupt for their 'Anchored VWAP Hand-off' script

Automated Anchored VWAPThis was reasonably easy to put together and I can't find one that does this in the Library and I've been wanting one. Of course, the drawing tool is just fantastic, but sometimes it can be forgotten as new pivots emerge.

What you'll find elsewhere in the Library is a nice variety of fancier methods for determining an anchor point with labels, lines, timestamps and standard deviations.

This is just a simple script to pull the Anchored VWAP off of the most recent pivot and update that as new pivots become defined.

I wanted it to be really portable so it could easily work into other things you're working on while also keeping the chart reasonably clean.

The way this functions is as follows: A new pivot is found and VWAP is calculated from it. At that point the prior aVWAP is no longer tracked and it picks up from the new pivot .

Of course this means that the plot doesn't generate until the pivot is actually confirmed, which in turn means that the plot doesn't reach back to the pivot , it begins based on whatever "right bars" period you end up choosing.

I kind of like it that way, because you have your eyes on the one that matters until the new one matters.

The downside is that it doesn't track old pivots . The old aVWAP might still be in play. But if you track all of the old one's you'll have a 100 lines on your chart and no one wants that.

I recommend when you look back and think the old one is still in play, use the drawing tool to keep it on the chart.

Otherwise, let the script do the work for you.

Hope its helpful. Let me know what you think should be done to make it better.

[TTI] Pinch AVWAPs––––History & Credit

This indicator came from studying Alpha trends and the concept from CMT Brian Shannon

–––––What it does

Upon uploading choose two dates from which the script will calculate Anchored VWAP from both dates. The dates can be easily moved for faster adjustment and re-calculation.

–––––How to use it

If you are trading a breakout methodology like myself, look for the "pinch" of the AVWAPs. Preferably, a bottom AVWAP moving up and a top AVWAP moving down. Choose important dates (this is rather subjective) for the AVWAP dates. These can be important events like Earnings or Divident Announcements. Or places where there is a change of structure of the Supply and Demand dynamic.

VWAP OscilatorVWAP Oscillator - Awesome Oscillator but using different period Volume Weighted Average Price values instead of moving averages. Used to get an idea of the momentum of price movements and when momentum might be reversing.

VWAP Heatmap SharesThis is a heatmap for the major share as listed on the FTMO MT4 account.

The pairs listed are:

1. AAPL - Apple

2. AMZN - Amazon

3. FB - Facebook.

4. GOOG - Google

5. MSFT - Microsoft

6. V - VISA

7. RACE - Ferrari

8. T - AT&T

9. BABA - Alibaba

10. BAC - bank of America

11. NFLX - Netflix

12. PFE - Pftzer

13. NVDA - Nvidia

14. TSLA - Tesla

15. WMT - Walmart

16. ZM - Zoom Video Communications.

The purple lines represent the VWAP for each of the stocks. The number represents the angle of the vwap. The bars above and below indicates the position of current price action above and below the VWAP.

Three Legged GooseThree Legged Goose

Three-Legged Goose is an all-in-one intraday trading system.

It features a sleek and customizable Opening range overlay with infinitely generating price targets, Average Daily Range Zones, Curated Anchored VWAPs, Total Volume and ATR analysis, as well as our state of the art Market Momentum Trend detection.

Three-Legged Goose also has important Daily levels, including the Previous Day's High and Low and the Current Days Open, three fully customizable Exponential Moving Averages, a customizable ema cloud, and a toggleable standard vwap.

Using this indicator allows you to get rid of any unnecessary indicators that are taking up those valuable slots in TradingView.

AVWAP + ORBS:

The Opening Range Breakout system builds off of our recommended 15min opening range and does all of your price target calculations based on the width of the opening range. These targets are fully customizable within the settings,

to allow fine-tuning from ticker to ticker. We have programmed three Anchored vwaps at different time intervals to act as a dynamic trend-finding instrument. These, along with the opening range breakout system, can help you quickly spot the day's trend and dynamic support and resistance long before your standard moving averages have caught up with price intraday.

Average Daily Range Zones:

We believe these zones to be essential to trading, especially with our system. These zones tend to act as areas of major support and resistance as well as give an idea of the projected volatility of the underlying.

Market Momentum Trend Detection:

We paint our momentum analysis directly on your candles. By taking the overall Market Internals + the underlying's Price movement, we can determine areas where we feel comfortable adding risk on or taking risk off.

This will help those that struggle at identifying trends and valid reversals.

All of the default settings are our recommended settings.

Please check the Author Instructions Below for how to gain access to our indicators.

JxModi CamarillaAddition to the Camarilla Pivots, This script will allow user to Add 4+1 more Indicators -EMA-9/20/50/200 & VWAP .

As well EMA can be change.

All the Support(L) and Resistance(H) levels can be enabled / disabled from settings. It will allow to select multiple combinations of support(L) & Resistance(H) levels across levels at any of the Time-frames individually and combined.

All EMA & VWAP Indicators can be can be enabled / disabled from settings.

Camarilla pivots Support(L) & Resistance(H) levels Can be Changed for any of the Time frames.

VWAP Heatmap Commodities and Indices V2Here is the Crashcourse trading VWAP for indices and Commodities. Same deal as the forex heatmap. It works best being on a 5 minute chart. Suggestion is to put it on the EURUSD together with the forex heatmap so you can see all the price action on one screen. You are looking for an approach to the VWAP and looking for a bounce. Remember if you have no gradient you have no trade!!!

The instruments covered:

1. US500 / S&P500 Capital.com

2. US100 / Nasdaq Capital.com

2. US30 / Dow Jones Capital.com

4. UK100 / FTSE100 Capital.com

5. JP225 / Nikkei225 Capital.com

6. DAX / DE40 Currency.com

7. AUS200 Capital.com

8. HK50 Capital.com

9. FRA40 / CAC Capital.com

10. Gold Capital.com

11. USoil / WTI Capital.com

12. UKoil / Brent Capital.com

These present the best volume and price data to give you the most reliable signals as far as I have determined.

Improvements coming for this will be to incorporate a slope for the vwap and to make better levels.

VWAP BreadthThe Concept

The volume-weighted average price (VWAP) is an indicator that gives the average price of a security based on both volume and price. VWAP is calculated by adding up the dollars traded (price*volume) and dividing it by the total volume. Generally speaking, prices above VWAP is bullish, while prices below VWAP is bearish.

VWAP can also be used as a breadth indicator, represented by the % of stocks above VWAP (orange line in above chart). However, the raw data of daily VWAP breadth is extremely noisy and hard for traders to decipher any tradable pattern.

This script aims to address this issue by adding multiple bars of VWAP breadth together, and then calculating the mean and standard deviation (STDEV) of previous accumulated VWAP breadth values.

The Signals:

20 days of accumulated VWAP breadth shows that:

1. Big market (S&P500 or Nasdaq) rallies happen when VWAP breadth is above mean.

2. Big market selloffs happen when VWAP breadth is below mean.

3. VWAP breadth above +2 STDEV is overbought but still bullish (overbought suggests strong buying interest despite the potential for a temporary pullback).

4. VWAP breadth below -2 STDEV is oversold but still bearish (oversold suggests strong selling interest despite the potential for a temporary rebound).

5. A VWAP breadth decreasing during an uptrend forms a bearish divergence.

6. A VWAP breadth increasing during a downtrend forms a bullish divergence.

The Variables:

Users can change how many bars of data to add together. I personally use 20 bars of accumulated data in daily charts.

The STDEV lookback period has a default value of 1000 bars, and does not need to be changed unless users experience lag.

Heatmap VWAP Forex v1This is an indicator for those subscribed to the Crash Course Trading Programme. It shows where the VWAP is in relation to current price action.

It is recommended you open this heat map using the TV trading view desktop and display it on one tab. It is also recommended you keep it on the EURUSD tab.

For all currency pairs it picks up the price action and volume from OANDA so you dont have to scan these charts looking for trades. It is strongly recommended you use OANDA as this has volume within the signal which is necessary to calculate the VWAP.

It covers the following forex pairs and these are in each column designated by the corresponding two letter abbreviation:

CLMN

1. EU – EURUSD

2. EG – EURGBP

3. EC – EURCHF

4. GU – GBPUSD

5. AU – AUDUSD

6. UJ – USDJPY

7. UC – USDCHF

8. AJ – AUDJPY

9. UL – USDCAD – L stands for Loonie

10. NU – NZDUSD

11. GJ – GBPJPY

12. EA – EURAUD

13. AL – AUDCAD – L stands for Loonie

Price action is at the VWAP when the column cell is bellow as indicated by the yellow box on the left hand side of the heatmap.

If the cell is red, it means that price action is below the VWAP.

If the cell is green, it means that the price is above the VWAP.

The higher it is above or below the VWAP it shows the box being higher or lower than the yellow row and is indicated by +/- Standard Deviation on the left hand side.

The aspects we are looking for are:

1. A gradient.

2. A pullback after price action has passed through the vwap.

3. You need a good reversal bar such as a engulfing / pinbar or high/low test bar or traintracks or day/morning star. These are some examples and you are not limited to just these. If you need help with candlesticks please get in touch and we will cover this to ensure you know what types of candlesticks you are looking for.

4. Look for confirmation with Stochastic RSI 3, 3, 9, 21 or Stoch 5,3,3 or what you like in this regard. It is a momentum indicator and overbought and undersold does apply to it. It indicates the energy that price action has, not necessarily zones where you can sell or buy.

5. Divergence. Again, if you do not fully understand this topic get in touch and we can go through this.

Remember, WITHOUT a gradient you have no trade. If there is no trade there today, that is fine, there is no desperate need to trade straight away.

Please add any comments to how useful you find this or if you would like improvements and I will see what I can do.

Z distance from VWAP Variation (jkf)This is a variation from LazyBear's Z-Distance from VWAP.

I use 3 different timeframes, where shorter term timeframes above longer term signals bullish.

Upper and lower bounds can impact too. Persistently high or low values will null the readings. So watch for that.

Key Levels// How it Works \\

Calculating Previous Days, Weeks and Monthly open, high, low, close and vwaps

Plots these levels on your chart

// Settings \\

You can enable/disable any of the levels you want to see

You can also change the amount of bars back the levels are plotted back to

// Use Case \\

These levels are often used in different methods of Technical analysis for support and resistance.

// Suggestions \\

Happy for anyone to make any suggestions on changes which could improve the script,

// Terms \\

Feel free to use the script, If you do use the script could you please just tag me as I am interested to see how people are using it. Good Luck!

Distance from Vwap// How it Works \\

Measuring the distance of the close price from a higher timeframe VWAP - Volume Weighted Average Price

There is a threshold which is calculated by looking back at the previous x amount of bars and storing the highest/lowest values

If the distance from the vwap stretches above that threshold, the histogram will go green if price is above VWAP and red if its below the vwap

If the distance from the vwap reaches below the low threshold you will see the histogram flashes orange

// Settings \\

In the settings you have the ability to change what timeframe the indicator is calculated on, as well as this you can change the timeframe the VWAP is calculated on.

I always recommend using a higher timeframe vwap as they tend to me more respected

e.g on the hourly timeframe, I use the weekly VWAP, on 1 minute timeframe you may want to use 4 hour timeframe but obviously feel free to experiment

// Use Case \\

When histogram is flashing green, prices is pulling far away from the vwap, obviously you don't want to be buying a falling knife but if you have levels of confluence this can help spot reversals.

I personally wait until the first candle after its been green to get confirmation of the fall weakening. Vica versa for reds and shorts/sells.

When you see orange flashes, this shows that price has been consolidating and the price is very close to the higher time frame VWAP which could be considered a safe entry point as they tend to lead to a big move to follow

// Suggestions \\

Happy for anyone to make any suggestions on changes which could improve the script,

// Terms \\

Feel free to use the script, If you do use the script could you please just tag me as I am interested to see how people are using it. Good Luck!

Y/Q/M/W aVWAP BandsYearly, Quarterly, Monthly or Weekly VWAP with Standard Deviation Envelope

Previous Y/Q/M/W VWAP and Band are extended forward automatically*

VWAP standard deviation envelope serves as a kind of Value Area, with the boundaries of the envelope acting as support and resistance. Previous envelops often show confluence with price action once price retests them.

Helpful to form a bias on the available time frames, find areas of support and resistance, and determine acceptance/rejection from breakouts or consolidations.

* this is a unique feature of this script

Anchored VWAP with Custom Volume IndexNot a regular AVWAP - this one allows you to use up to 39 sources added together as your volume source

This enables you to use many different pairs from many different exchanges when dealing with crypto

OR you can enhance your intermarket analysis charting abilities enabling you to place the AVWAP on multiple symbols on one chart

Hope you enjoy!

NOTE:

All the symbols must have a history that goes back as far as the chosen date!

When placing at a date in the past, ensure all the sources of volume have history going back as far as you have chosen OR the AVWAP will not appear

VWAP From Multiple Sources With Cloud & Percentage GapVWAP CLOUD FROM CLOSE, OPEN, HIGH & LOW SOURCES WITH CLOUD & PERCENTAGE GAP

VWAP stands for volume weighted average price and shows the average price of buys/sells based on volume traded across the current session. This VWAP is based off of the Daily session.

***HOW TO USE***

Use the purple cloud between the VWAPs as your entry points as price will typically bounce from that cloud area.

The Yellow Line is the VWAP using the close price as a source.

The Green Line is the VWAP using the open price as a source.

The Blue Line is the VWAP using the high price as a source.

The Purple Line is the VWAP using the low price as a source.

When price is above the VWAP cloud, the background will paint green because the trend is bullish.

When price is below the VWAP cloud, the background will paint red because the trend is bearish.

In the bottom right hand corner, three is a table that will show you the current percentage gap between current price and the VWAP using close as the source.

All sources and colors can be easily switched in the settings menu.

***MARKETS***

This indicator can be used as a signal on all markets, including stocks, crypto, futures and forex.

***TIMEFRAMES***

This vwap indicator can be used on all timeframes but is calculated using the daily session.

***TIPS***

Try using numerous indicators of ours on your chart so you can instantly see the bullish or bearish trend of multiple indicators in real time without having to analyze the data. Some of our favorites are our Auto Fibonacci, Volume Profile, Directional Movement Index, Momentum, Auto Support And Resistance and Money Flow Index in combination with this VWAP Cloud. The other indicators all have real time Bullish and Bearish labels as well so you can immediately understand each indicator's trend.

[GarufiCommunity] Multi Indicator: VWAPs, MA, Pivot PointsThis script provides a collection of indicators to help traders look at multiple trends while maintaining a consistent configuration, even when jumping around different timeframes and symbols.

Additionally, this collection is particularly useful when trading decisions involve looking at dozens of indicators and analyzing, in aggregate, their confluence.

With this collection of indicators you can configure anchored VWAPs, MA, and Pivot Points:

- Anchored VWAPs: For each you define a fixed time and date to anchor it in the graph, and it stays consistent even when you change the symbol. An example use case can be setting one of the VWAPs to always start on the first candle on January 1st 2021, and a second VWAP a decade prior, so you don’t need to keep manually adjusting/adding VWAPs to the graph. At the moment you can define up to 4 anchored VWAPs.

- MA and Pivot Points: For each you can set independent timeframes, periods, and types, while using a single configuration panel. This helps reduce the amount of clicking needed when trying different configurations, such as testing different MA and Pivot periods and comparing how each behave in the graph (this personally helps me build trust in indicators). Permits use of up to 3 MAs and 2 Pivot Points.

Lastly, this script leverages and reuses modified code from the sources below:

- Médias e Tempos-v.2.1 by VeraLucia (with permission);

- Multiple Anchored VWAP v1.0 by GuilhermeNogueira (with permission);

- Pivot Point by TradingView.

TBM VWAP Bands Style SetupA stripped down and modified version of the 'VWAP with Standard Deviation Bands' indicator by pmk07. The bands have been modified and styled to match those used on the Tradovate platform by Matt from the Trades By Matt youtube channel so if you would like to know how they should be used go to his youtube channel and watch his strategy explanation video.

rth vwap and midMidpoint and VWAP are often important inflection points in daytrading. I managed to find a script providing me with a 24 hour session midline by NorthStarDayTrading and a RTH VWAP script by LDBC. So I decided to merge those two to get a RTH mid and vwap.

Koalafied RVWAPThis indicator shows both the Rolling VWAP and Standard Deviations as set by the user. The Rolling VWAP calculation is similar to the standard VWAP although it calculates the volume weighted average price over the specified period of time (lookback), resetting for each subsequent bar.

The unique aspect of this indicator is that instead of calculating the RVWAP over the current timeframes lookback period, the option is available to select a High-Time-Frame setting instead.

This has two different methods of calculation

1 - Based on HTF security requests (both repainting and non-repainting)

2 - Automatic calculation of number of current timeframe bars that make up the HTF lookback period (smoother and non-repainting plot)

Additionally a smooth function is included for the HTF input setting.