SURF (ex-mafgi) 2.5 4m design @VanyaKsenyaSURF

designed by my 2 older kids, idea by me.

Correlation long only indicator which is fun to use and easy to decipher (hopefully).

What it does, is you can pick up to 3 assets that correlate with the asset you study.

Then it calculates the fear and greed index for each of the assets, and assigns it a weight based on either of the 3 included correlation measuring methods - simple, volatility-based, time-shifted, and (not yet working as of now) - grander causality method.

When the correlated assets are in fear zone (for positively correlated assets) - it shows a surfer who is ready to surf the upcoming wave up.

However, be cautious and take your profit when you see a palm tree or the sea throws out some green seaweed.

Waves are deep back in the sea and dark blue, with a lot of wet sand on the beach - good entry points for longs.

Opposite - good for shorts. When waves are so high that they reach the dry sand.

Enjoy!

(don't forget to check and modify the list of the assets which you think might corellate with the asset you're studying or trading).

Współczynnik Korelacji (CC)

CorrelationMulti-Timeframe Correlation Indicator

This Pine Script indicator measures the correlation between the current symbol and a reference symbol (default: GLD) across three different timeframes. It provides traders with valuable insights into how assets move in relation to each other over short, medium, and long-term periods.

Key Features

Multiple Timeframe Analysis: Calculates correlation coefficients over three customizable periods (default: 20, 50, and 200 bars)

Visual Reference Lines: Displays horizontal lines at +1, 0, and -1 to indicate perfect positive correlation, no correlation, and perfect negative correlation

Color-Coded Outputs: Shows short-term correlation in green, medium-term in yellow, and long-term in red for easy visual interpretation

Understanding Correlation

The correlation coefficient measures the statistical relationship between two data series, ranging from -1 to +1:

+1: Perfect positive correlation (both assets move together in the same direction)

0: No correlation (movements are random and independent)

-1: Perfect negative correlation (assets move in opposite directions)

How To Use This Indicator

Market Relationships: Identify how strongly your current asset correlates with the reference symbol

Diversification Analysis: Find assets with negative correlations to build a diversified portfolio

Divergence Opportunities: Watch for changes in correlation patterns that might signal trading opportunities

Trend Confirmation: Use correlation with benchmark assets to confirm broader market trends

Customization Options

Reference Symbol: Change the default GLD to any other symbol you want to compare against

Period Lengths: Adjust the short, medium, and long timeframes to match your trading strategy and timeframe

This indicator helps traders make more informed decisions by understanding the interrelationships between different assets across various timeframes, potentially improving portfolio construction and risk management strategies.

Correlation TableThis indicator displays a vertical table that shows the correlation between the asset currently loaded on the chart and up to 32 selected trading pairs. It offers the following features:

Chart-Based Correlation: Correlations are calculated based on the asset you have loaded in your chart, providing relevant insights for your current market focus.

Configurable Pairs: Choose from a list of 32 symbols (e.g., AUDUSD, EURUSD, GBPUSD, etc.) with individual checkboxes to include or exclude each pair in the correlation analysis.

Custom Correlation Length: Adjust the lookback period for the correlation calculation to suit your analysis needs.

Optional EMA Smoothing: Enable an Exponential Moving Average (EMA) on the price data, with a configurable EMA length, to smooth the series before calculating correlations.

Color-Coded Output: The table cells change color based on the correlation strength and direction—neutral, bullish (green), or bearish (red)—making it easy to interpret at a glance.

Clear Table Layout: The indicator outputs a neatly organized vertical table with headers for "Pair" and "Correlation," ensuring the information is displayed cleanly and is easy to understand.

Ideal for traders who want a quick visual overview of how different instruments correlate with their current asset, this tool supports informed multi-asset analysis

ITALIANO:

Questo indicatore visualizza una tabella verticale che mostra la correlazione tra l'asset attualmente caricato sul grafico e fino a 32 coppie di trading selezionate. Offre le seguenti funzionalità:

Correlazione basata sul grafico: le correlazioni vengono calcolate in base all'asset caricato nel grafico, fornendo informazioni pertinenti per il tuo attuale focus di mercato.

Coppie configurabili: scegli da un elenco di 32 simboli (ad esempio, AUDUSD, EURUSD, GBPUSD, ecc.) con caselle di controllo individuali per includere o escludere ciascuna coppia nell'analisi della correlazione.

Lunghezza di correlazione personalizzata: regola il periodo di lookback per il calcolo della correlazione in base alle tue esigenze di analisi.

Smoothing EMA opzionale: abilita una media mobile esponenziale (EMA) sui dati dei prezzi, con una lunghezza EMA configurabile, per smussare la serie prima di calcolare le correlazioni.

Output codificato a colori: le celle della tabella cambiano colore in base alla forza e alla direzione della correlazione, neutra, rialzista (verde) o ribassista (rosso), rendendola facile da interpretare a colpo d'occhio.

Clear Table Layout: l'indicatore genera una tabella verticale ordinatamente organizzata con intestazioni per "Coppia" e "Correlazione", assicurando che le informazioni siano visualizzate in modo chiaro e siano facili da comprendere.

Ideale per i trader che desiderano una rapida panoramica visiva di come diversi strumenti siano correlati con il loro asset corrente, questo strumento supporta un'analisi multi-asset informata

XAUMOvisionXAUMOvision: T he XAU/USD Composite Correlation Indicator with Weighted Spillover & Dynamic Lines

XAUMOvision is a custom-built trading indicator designed to track the intricate relationship between XAU/USD (Gold) and key economic factors: DXY (US Dollar Index), US Treasury Yields, S&P 500, and Crude Oil. By blending correlation metrics with weighted spillover effects, XAUMOvision offers actionable insights to refine your Gold trading strategy.

Core Features of XAUMOvision

1. Correlation (CC)

Definition: Measures how closely two assets move together over a given period.

Calculation: Pearson Correlation is used to assess Gold's relationship with:

DXY: Negative correlation—when DXY rises, Gold typically falls.

US Treasury Yields: Negative correlation—higher yields reduce Gold’s appeal.

S&P 500: Opposite movement, as Gold acts as a safe-haven.

Crude Oil: Positive correlation—both often rise during inflationary pressures.

2. Weighted Spillover

What It Does: Quantifies how movements in each asset (DXY, Yields, etc.) influence Gold.

Weighting: User-defined values (e.g., DXY weight = 0.4) scale each factor’s impact.

Result: A total spillover score reveals bullish or bearish sentiment for XAU/USD.

3. Composite Bias Line

Purpose: Consolidates spillover impacts into a single sentiment indicator.

Readings:

Strong Bullish: Composite Bias > 0.5.

Neutral: Close to 0.

Strong Bearish: Composite Bias < -0.5.

Output: A directional bias to guide your trading decisions.

4. Traffic Signal Line

Visual Cues:

Green: Strong Bullish Signal.

Red: Strong Bearish Signal.

Gray: Neutral—avoid trading.

Utility: A quick, color-coded overview of market conditions.

Using XAUMOvision Effectively

When to Use

During high volatility or major news events (e.g., CPI, interest rate decisions).

To understand macroeconomic forces driving Gold’s price action.

Recommended Timeframes

4-Hour: Ideal for swing traders seeking medium-term setups.

Daily: Perfect for macro trend analysis.

Weekly: Suitable for long-term investors aligning with broader trends.

---------------------------------------------------------------------------------

Practical Example

Monday, January 13, 2025 (Neutral Market)

Market Behavior: Gold stagnated (-0.96%), with low volume (681.13K).

Indicator Insights:

Composite Spillover: -0.92 (mild bearish pressure).

Traffic Signal Line: Gray—stay out of the market.

Bias Line: Weak Bearish (-1), signaling no strong trend.

Result: XAUMOvision kept traders from entering a choppy, low-volume market.

Wednesday, January 15, 2025 (CPI-Driven Rally)

CPI Release: Core CPI softer than expected (0.2% vs. 0.3%), weakening the DXY and Yields. Gold surged.

Indicator Insights:

Composite Spillover: +0.57 (strong bullish sentiment).

Traffic Signal Line: Green—clear buy signal.

Bias Line: Strong Bullish (+2), confirming the trend.

Result: Traders aligned with institutional flows and profited from the CPI-driven rally.

--------------------------------------------------------------------------------

Why XAUMOvision Stands Out

Avoids Bad Trades: Neutral signals and low-volume days keep you sidelined during indecisive markets.

Pinpoints Big Moves: Green signals during high-impact events help you capitalize on major trends.

Volume Validation: Confirms institutional activity to distinguish real trends from fakeouts.

Conclusion: Trade Like a Pro

XAUMOvision blends macroeconomic analysis with real-time technical indicators, ensuring you stay ahead of market moves. Whether navigating neutral markets or CPI-driven surges, this tool provides clarity and confidence in your trading decisions. For swing traders and macro enthusiasts, XAUMOvision is the ultimate weapon in Gold trading.

Cross-Asset Correlation Trend IndicatorCross-Asset Correlation Trend Indicator

This indicator uses correlations between the charted asset and ten others to calculate an overall trend prediction. Each ticker is configurable, and by analyzing the trend of each asset, the indicator predicts an average trend for the main asset on the chart. The strength of each asset's trend is weighted by its correlation to the charted asset, resulting in a single average trend signal. This can be a rather robust and effective signal, though it is often slow.

Functionality Overview :

The Cross-Asset Correlation Trend Indicator calculates the average trend of a charted asset based on the correlation and trend of up to ten other assets. Each asset is assigned a trend signal using a simple EMA crossover method (two customizable EMAs). If the shorter EMA crosses above the longer one, the asset trend is marked as positive; if it crosses below, the trend is negative. Each trend is then weighted by the correlation coefficient between that asset’s closing price and the charted asset’s closing price. The final output is an average weighted trend signal, which combines each trend with its respective correlation weight.

Input Parameters :

EMA 1 Length : Sets the period of the shorter EMA used to determine trends.

EMA 2 Length : Sets the period of the longer EMA used to determine trends.

Correlation Length : Defines the lookback period used for calculating the correlation between the charted asset and each of the other selected assets.

Asset Tickers : Each of the ten tickers is configurable, allowing you to set specific assets to analyze correlations with the charted asset.

Show Trend Table : Toggle to show or hide a table with each asset’s weighted trend. The table displays green, red, or white text for each weighted trend, indicating positive, negative, or neutral trends, respectively.

Table Position : Choose the position of the trend table on the chart.

Recommended Use :

As always, it’s essential to backtest the indicator thoroughly on your chosen asset and timeframe to ensure it aligns with your strategy. Feel free to modify the input parameters as needed—while the defaults work well for me, they may need adjustment to better suit your assets, timeframes, and trading style.

As always, I wish you the best of luck and immense fortune as you develop your systems. May this indicator help you make well-informed, profitable decisions!

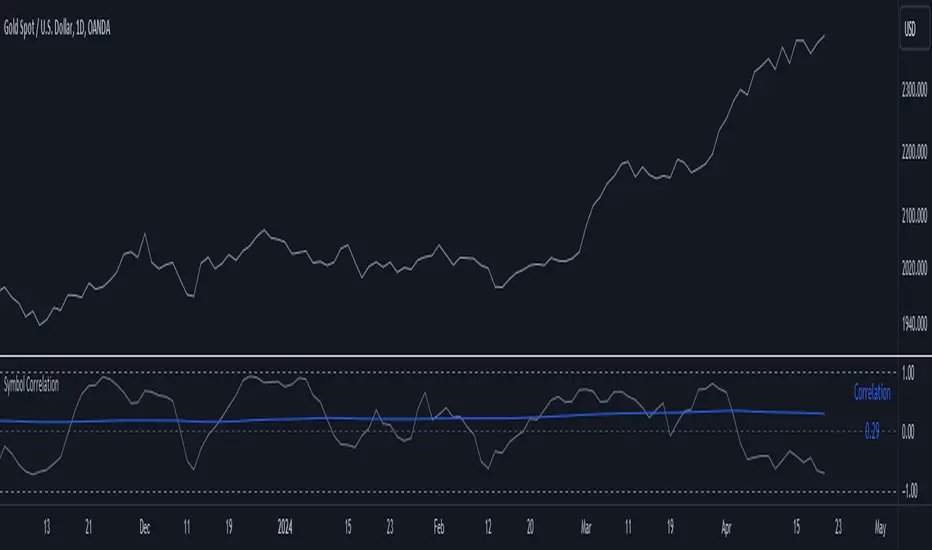

Symbol CorrelationThe "Symbol Correlation" indicator calculates and displays the correlation between the chosen symbol's price and another selected source over a specified period. It also includes a moving average (SMA) of this correlation to provide a smoothed view of the relationship.

Why SMA and Table Display ?

The inclusion of SMA (Simple Moving Average) with adjustable length (SMA Length) enhances the indicator's utility by smoothing out short-term fluctuations in correlation, allowing for clearer trend identification. The SMA helps to visualize the underlying trend in correlation, making it easier to spot changes and patterns over time.

The table display of the correlation SMA value offers a concise summary of this trend. By showcasing the current correlation SMA alongside its historical values, traders can quickly gauge the relationship's strength relative to previous periods.

Interpreting the Indicator:

1. Correlation Values: The primary plot shows the raw correlation values between the symbol's price and the specified source. A value of 1 indicates a perfect positive correlation, -1 signifies a perfect negative correlation, and 0 suggests no linear relationship.

2. Correlation SMA: The SMA line represents the average correlation over a defined period (SMA Length). Rising SMA values indicate strengthening correlation trends, while declining values suggest weakening correlations.

3. Choosing SMA Length: Traders can adjust the SMA Length parameter to tailor the moving average to their specific analysis horizon. Shorter SMA lengths react quickly to price changes but may be more volatile, while longer SMA lengths smooth out noise but respond slower to recent changes.

In summary, the "Symbol Correlation" indicator is a valuable tool for assessing the evolving relationship between a symbol's price and an external source. Its use of SMA and tabular presentation facilitates a nuanced understanding of correlation trends, aiding traders in making informed decisions based on market dynamics.

Historical Correlation [LuxAlgo]The Historical Correlation tool aims to provide the historical correlation coefficients of up to 10 pairs of user-defined tickers starting from a user-defined point in time.

Users can choose to display the historical values as lines or the most recent correlation values as a heat map.

🔶 USAGE

This tool provides historical correlation coefficients, the correlation coefficient between two assets highlight their linear relationship and is always within the range (-1, 1).

It is a simple and easy to use statistical tool, with the following interpretation:

Positive correlation (values close to +1.0): the two assets move in sync, they rise and fall at the same time.

Negative correlation (values close to -1.0): the two assets move in opposite directions: when one goes up, the other goes down and vice versa.

No correlation (values close to 0): the two assets move independently.

The user must confirm the selection of the anchor point in order for the tool to be executed; this can be done directly on the chart by clicking on any bar, or via the date field in the settings panel.

For the parameter Anchor period , the user can choose between the following values NONE, HOURLY, DAILY, WEEKLY, MONTHLY, QUARTERLY and YEARLY. If NONE is selected, there will be no resetting of the calculations, otherwise the calculations will start from the first bar of the new period.

There is a wide range of trading strategies that make use of correlation coefficients between assets, some examples are:

Pair Trading: Traders may wish to take advantage of divergences in the price movements of highly positively correlated assets; even highly positively correlated assets do not always move in the same direction; when assets with a correlation close to +1.0 diverge in their behavior, traders may see this as an opportunity to buy one and sell the other in the expectation that the assets will return to the likely same price behavior.

Sector rotation: Traders may want to favor some sectors that are expected to perform in the next cycle, tracking the correlation between different sectors and between the sector and the overall market.

Diversification: Traders can aim to have a diversified portfolio of uncorrelated assets. From a risk management perspective, it is useful to know the correlation between the assets in your portfolio, if you hold equal positions in positively correlated assets, your risk is tilted in the same direction, so if the assets move against you, your risk is doubled. You can avoid this increased risk by choosing uncorrelated assets so that they move independently.

Hedging: Traders may want to hedge positions with correlated assets, from a hedging perspective, if you are long an asset, you can hedge going long a negative correlated asset or going short a positive correlated asset.

Traders generally need to develop awareness, a key point is to be aware of the relationships between the assets we hold or trade, the historical correlation is an invaluable tool in our arsenal which allows us to make better informed decisions.

On this chart we have an example of historical correlations for several futures markets.

We can clearly see how positively correlated the Nasdaq100 and Dow30 are with the SP500 over the whole period, or how the correlation between the Euro and the SP500 falls from almost +85% to almost -4% since 2021.

As we can see, correlations, like everything else in the market, are not static and vary over time depending on many factors, from macro to technical and everything in between.

🔹 Heatmap

The chart above shows the tool with the default settings and the Drawing Mode set to 'HEATMAP'.

We can see the current correlation between the assets, in this case the FX pairs.

The highest positive correlation is +90% (+0.90) between EURUSD and GBPUSD.

The highest negative correlation is -78% (-0.78) between EURUSD and USDJPY.

The pair with no correlation is AUDUSD and EURCAD with 1% (0.01)

On the above chart we can see the current correlations for the futures markets.

Currently, the assets that are less correlated to the SP500 are NaturalGas and the Euro, the more positive correlations are Nasdaq100 and Dow20, and the more negative correlations are the Yen, Treasury Bonds and 10-Year Notes.

🔶 DETAILS

🔹 Anchor Period

This chart shows the standard FX correlations with the Anchor Period set to `MONTHLY`.

We can clearly see how the calculations restart with the new month, in this case we can clearly see the differences between the correlations from month to month.

Let us look at the correlation coefficient between GBPUSD and USDJPY

In January, their correlation started at close to -100%, rose to close to +50%, only to fall to close to 0% and remain there for the second half of the month.

In February it was -90% in the first few days of the month and is now around -57%.

And between AUDUSD and EURCAD

Last month their correlation was negative for most of the month, reaching -70% and ending around -14%.

This month their correlation has never gone below +21% and at the time of writing is close to +53%.

🔶 SETTINGS

Anchor point: Starting point from which the tool is executed

Anchor period: At the beginning of each new period, the tool will reset the calculations

Pairs from 1 to 10: For each pair of tickers, you can: enable/disable the pair, select the color and specify the two tickers from which you wish to obtain the correlation

🔹 Style

Drawing Mode: Output style, `LINES` will show the historical correlations as lines, `HEATMAP` will show the current correlations with a color gradient from green for correlations near 1 to red for correlations near -1.

Cross Correlation [Kioseff Trading]Hello!

This script "Cross Correlation" calculates up to ~10,000 lag-symbol pair cross correlation values simultaneously!

Cross correlation calculation for 20 symbols simultaneously

+/- Lag Range is theoretically infinite (configurable min/max)

Practically, calculate up to 10000 lag-symbol pairs

Results can be sorted by greatest absolute difference or greatest sum

Ability to "isolate" the symbol on your chart and check for cross correlation against a list of symbols

Script defaults to stock pairs when on a stock, Forex pairs when on a Forex pair, crypto when on a crypto coin, futures when on a futures contract.

A custom symbol list can be used for cross correlation checking

Can check any number of available historical data points for cross correlation

Practical Assessment

Ideally, we can calculate cross correlation to determine if, in a list of assets, any of the assets frequently lead or lag one another.

Example

Say we are comparing the log returns for the previous 10 days for SPY and XLU.

*A single time-interval corresponds to the timeframe of your chart i.e. 1-minute chart = 1-minute time interval. We're using days for this example.

(Example Results)

A lag value (k) +/-3 is used.

The cross correlation (normalized) for k = +3 is -0.787

The cross correlation (normalized) for k = -3 is 0.216

A positive "k" value indicates the correlation when Asset A (SPY) leads Asset B (XLU)

A negative "k" value indicates the correlation when Asset B (XLU) leads Asset A (SPY)

A normalized cross correlation of -0.787 for k = +3 indicates an "adequately strong" negative relationship when SPY leads XLU by 3 days.

When SPY increases or decreases - XLU frequently moves in the opposite direction 3 days later.

A cross correlation value of 0.216 at k = −3 indicates a "weak" positive correlation when XLU leads SPY by 3 days.

There's a slight tendency for SPY to move in the same direction as XLU 3 days later.

After the cross-correlation score is normalized it will fall between -1 and 1.

A cross-correlation score of 1 indicates a perfect directional relationship between asset A and asset B at the corresponding lag (k).

A cross correlation of -1 indicates a perfect inverse relationship between asset A and asset B at the corresponding lag (k).

A cross correlation of 0 indicates no correlation at the corresponding lag (k).

The image above shows the primary usage for the script!

The image above further explains the data points located in the table!

The image above shows the script "isolating" the symbol on my chart and checking the cross correlation between the symbol and a list of symbols!

Wrapping Up

With this information, hopefully you can find some meaningful lead-lag relationships amongst assets!

Thank you for checking this out (:

Correlation TrackerCorrelation Tracker Indicator

The Correlation Tracker indicator calculates and visualizes the correlation between two symbols on a chart. It helps traders and investors understand the relationship and strength of correlation between the selected symbol and another symbol of their choice.

Indicator Features:

- Correlation Calculation: The indicator calculates the correlation between two symbols based on the provided lookback period.

- Correlation Scale: The correlation value is normalized to a scale ranging from 0 to 1 for easy interpretation.

- Table Display: A table is displayed on the chart showing the correlation value and a descriptive label indicating the strength of the correlation.

- Customization Options: Users can customize the text color, table background color, and choose whether to display the Pearson correlation value.

- The Correlation Tracker indicator utilizes a logarithmic scale calculation, making it particularly suitable for longer timeframes such as weekly charts, thereby providing a more accurate and balanced measure of correlations across a wide range of values.

How to Use:

1. Select the symbol for which you want to track the correlation (default symbol is "SPX").

2. Adjust the lookback period to define the historical data range for correlation calculation.

3. Customize the text color and table background color according to your preference.

4. Choose whether to display the Pearson correlation value or a descriptive label for correlation strength.

5. Observe the correlation line on the chart, which changes color based on the strength of the correlation.

6. Refer to the correlation table for the exact correlation value or the descriptive label indicating the correlation strength.

Note: The indicator can be applied to any time frame chart and is not limited to logarithmic scale.

Correlation Coefficient - DXY & XAUPublishing my first indicator on TradingView. Essentially a modification of the Correlation Coefficient indicator, that displays a 2 ticker symbols' correlation coefficient vs, the chart presently loaded.. You can modify the symbols, but the default uses DXY and XAU, which have been displaying strong negative correlation.

As with the built-in CC (Correlation Coefficient) indicator, readings are taken the same way:

Positive Correlation = anything above 0 | stronger as it moves up towards 1 | weaker as it moves back down towards 0

Negative Correlation = anything below 0 | stronger moving down towards -1 | weaker moving back up towards 0

This is primarily created to work with the Bitcoin weekly chart, for comparing DXY and Gold (XAU) price correlations (in advance, when possible). If you change the chart timeframe to something other than weekly, consider playing with the Length input, which is set to 35 by default where I think it best represents correlations with Bitcoin's weekly timeframe for DXY and Gold.

The intention is that you might be able to determine future direction of Bitcoin based on positive or negative correlations of Gold and/or the US Dollar Index. DXY has been making peaks and valleys prior to Bitcoin since after March 2020 black swan event, where it peaked just after instead. In the future, it may flip over again and Bitcoin may hit major highs or lows prior to DXY, again. So, keep an eye on the charts for all 3, as well as the indicator correlations.

Currently, we've moved back into negative correlation between Bitcoin and DXY, and positive correlation with Bitcoin and Gold:

Negative Correlation b/w Bitcoin and DXY - if DXY moves up, Bitcoin likely moves down, or if DXY moves down, Bitcoin likely moves up (or if Bitcoin were to move first before DXY, as it did on March 2020, instead)

Positive Correlation b/w Bitcoin and Gold - Bitcoin and Gold will likely move up or down with each other.

DXY is represented by the green histogram and label, Gold is represented by the yellow histogram and label. Again, you can modify the tickers you want to check against, and you can modify the colors for their histograms / labels.

The inspiration from came from noticing areas of same date or delayed negative correlation between Bitcoin and DXY, here is one of my most recent posts about that:

Please let me know if you have any questions, or would like to see updates to the indicator to make it easier to use or add more useful features to it.

I hope this becomes useful to you in some way. Thank you for your support!

Cheers,

dudebruhwhoa :)

MA Correlation CoefficientThis script helps you visualize the correlation between the price of an asset and 4 moving averages of your choice. This indicator can help you identify trendy markets as well as trend-shifts.

Disclaimer

Bear in mind that there is always some lag when using Moving-Averages, hence the purpose of this indicator is as a trend identification tool rather than an entry-exit strategy.

Working Principle

The basic idea behind this indicator is the following:

In a trendy market you will find high correlation between price and all kinds of Moving-Averages. This works both ways, no matter bull or bear trend.

In sideways markets you might find a mix of correlations accross timeframes (2018) or high correlation with Low-Timeframe averages and low correlation with High-Timeframe averages (2021/2022).

Trend shifts might be characterised by a 'staircase' type of correlation (yellow), where the asset regains correlation with higher timeframe averages

Indicator Options

1. Source : data used for indicator calculation

1. Correlation Window : size of moving window for correlation calculation

2. Average Type :

Simple-Moving-Average (SMA)

Exponential-Moving-Average (EMA)

Hull-Moving-Average (HMA)

Volume-Weighted-Moving-Average (VWMA)

3. Lookback : number of past candles to calculate average

4. Gradient : modify gradient colors. colors relate to correlation values.

Plot Explanation

The indicator plots, using colors, the correlation of the asset with 4 averages. For every candle, 4 correlation values are generated, corresponding to 4 colors. These 4 colors are stacked one on top of the other generating the patterns explained above. These patterns may help you identify what kind of market you're in.

Crypto Correlation MatrixA crypto correlation matrix or table is a tool that displays the correlation between different cryptocurrencies and other financial assets. The matrix provides an overview of the degree to which various cryptocurrencies move in tandem or independently of each other. Each cell represents the correlation between the row and column assets respectively.

The correlation matrix can be useful for traders and investors in several ways:

First, it allows them to identify trends and patterns in the behavior of different cryptocurrencies. By looking at the correlations between different assets, traders can gain insight into the intra-relationships of the crypto market and make more informed trading decisions. For example, if two cryptocurrencies have a high positive correlation, meaning that they tend to move in the same direction, a trader may want to diversify their portfolio by choosing to invest in only one of the two assets.

Additionally, the correlation matrix can help traders and investors to manage risk. By analyzing the correlations between different assets, traders can identify opportunities to hedge their positions or limit their exposure to particular risks. For example, if a trader holds a portfolio of cryptocurrencies that are highly correlated with each other, they may be at greater risk of losses if the market moves against them. By diversifying their portfolio with assets that are less correlated with each other, they can reduce their overall risk.

Some of the unique properties for this specific script are the correlation strength levels in conjunction with the color gradient of cells, intended for clearer readability.

Features:

Supports up to 64 different crypto assets.

Dark/Light mode.

Correlation strength levels and cell coloring.

Adjustable positioning on the chart.

Alerts at the close of a bar. (Daily timeframe or higher recommended)

Correlation Coefficient TableThis is a sample PineSript code implementation using Correlation Coefficient. It uses the ta.correlation library of Pinescript and calculates the correlation based on user input length. The results are then plotted on a table. The corr value displays the actual correlation coefficient value while the Corr Status displays the interpretation of the correlation coefficient values.

The script takes the following input

Source Symbol - This is the base symbol which will be used in calculating correlation coefficient. In my case, since i am looking more often on crypto. I defaulted it to BTCUSDT

Symbol 1 - Symbol 5 - These are the coins that will be compared to our base symbol for correlation.

Source - You can select on which price source you want to be calculated. By default this is set to candle close price.

Length - The number of price bar to look back and retrieve correlation coefficient. Set to 20 bars by default.

Table Settings - Since the correlation coefficient are displayed on a table. An option to customize the table settings are presented.

The Correlation Status column was based on this Interpretation:

For more information, read this article www.tradingview.com

Bitcoin Correlation MapHello everyone,

This indicator shows the correlation coefficients of altcoins with bitcoin in a table.

What is the correlation coefficient?

The correlation coefficient is a value that takes a value between 0 and 1 when a parity makes similar movements with the reference parity, and takes a value between 0 and -1 when it makes opposite movements.

In order to obtain more meaningful and real-time results in this indicator, the weighted average of the correlation values of the last 200bar was used. You can change the bar length as you wish. With the correlation value, you can see the parities that have similar movements with bitcoin and integrate them into your strategy.

You can change the coin list as you wish, and you can also calculate their correlation with etherium instead of bitcoin .

The indicator shows the correlation value of 36 altcoins at the moment.

The indicator indicates the color of the correlated parities as green and the color of the inversely correlated parities as red.

Cheers

Correlation Coefficient: Visible Range Dynamic Average R -Correlation Coefficient with Dynamic Average R (shows R average for the visible chart only, changes as you zoom in or out)

-Label: Vis-Avg-R = Visable Average R

-the Correlation Coefficient function for Pearson's R is taken from "BA🐷 CC" indicator by @balipour (highly recommended; more thorough treatment of R and other stats, but without the dynamic average)

-I wrote this primarily to add a dynamic Average R, showing correlation for arbitrary start times/end times; whether it be the last month, last year, of some specific period from the past (backtest mode)

-I have been using this to get an idea of correlation regimes over time between Bonds vs Stocks (ZB1! vs ES1!).

-As you see from the above, most of 2022 has seen an unusually strong positive correlation between Bonds and Stocks

~~inputs:

-lookback length for calculation of R

-Backtest mode (true by default): displays Average R for ONLY the visible range displayed on any part of chart history (LHS to RHS of screen only)

-source for both Ticker and compared Asset (close, open, high, low, ohlc4.. etc)

~~some other assets worth comparing:

Aussie vs Gold; Aussie vs ES; Btc vs ES; Copper vs ES

Multi Delta-Agnostic Correlation Coefficient (tartigradia)Display three DACC plots simultaneously, to visualize both directional (up on top, down at bottom) and adirectional DACC (in the middle) simultaneously.

Delta Agnostic Correlation calculates a correlation between two symbols based only on the sign of their changes using a Sign Test (en.m.wikipedia.org), regardless of the amplitude of price change. Compared to a standard Pearson correlation (quantitative test), Sign Test correlations (discrete test) are highly sensitive to directional change with 0 lag, at the expense of lacking sensitivity to quantity correlation (ie, it does not matter if changes are big or small).

Hence, this Delta-Agnostic Correlation Coefficient (DCC or DACC) indicator is better used to detect early changes in correlations, and then confirmation with a typical Pearson correlation or a non-parametric Spearman test or Mutual Information (all three are quantitative tests, hence accounting for quantity and not just direction) can allow to be more sensitive to quantities too and hence be a robust combination to demonstrate strong correlations both in direction and amplitude.

Adequate statistical significance testing, using a two-sided binomial statistical test, is also implemented. Note however that one assumption of the sign test may here be violated: independence of observations for each symbol. If you assume the market is not acting on a random walk, then there is a temporal autocorrelation, and this biases the sign test. However, in practice, the test works well enough.

The directional variants of the test allow to test the correlation hypothesis only if the index symbol goes into one direction. For example, if we suspect that the index symbol is correlated with the current symbol but only when the index symbol is bullish, we can select "Up" to test this hypothesis. Note that given the specificities of how directional and adirectional tests differ in how they work, the default fill is different: zero-value fill for adirectional test to simulate how price action tend to lose momentum during market close periods, previous DCC_MA (= no change in DCC value) during both market close periods and when the direction is opposite for the directional variants of the test, so that while the market is moving opposite, we don't lose the statistical significance built up to now, otherwise it would be nonsensical (for the directional tests).

For more information on the theory behind, see the original DACC indicator, which is the same script but with only one plot:

Oasis Trading Group: Correlation Table The Correlation Table is an indicator that is used to measure the Correlation Coefficient of multiple assets at the same time in an easy to read table.

A quick introduction into reading a Correlation Coefficient:

A strong positive correlation (one asset moves in one direction the other asset also moves in the same direction) = +1.00

A strong negative correlation (one asset moves in one direction the other asset moves in the opposing direction) = -1.00

Typically you would like to see the correlation strength to be greater than 0.7 or less than -0.7 for there to be a tradable correlation. A reading close to zero would not offer optimal trade entries.

The other data the indicator is showing is the overall trend. This reading is a simple calculation based on the correlation length the user inputs, the indicator will determine if price action is trending up or down based on this length.

The indicator has a reading for the current timeframe that is on the chart and also a second timeframe which is defaulted to the daily.

This indicator is an add-on to the and I hope to have more updates coming soon.

For Access or Questions: Private message us. Thank you.

Correlation ZonesThis indicator highlights zones with strong, weak and negative correlation. Unlike standard coefficient indicator it will help to filter out noise when analyzing dependencies between two assets.

With default input setting Correlation_Threshold=0.5:

- Zones with correlation above 0.5, will be colored in green (strong correlation)

- Zones with correlation from -0.5 to 0.5 will be colored grey (weak correlation)

- Zones with correlation below -0.5 will be colore red (strong negative correlation)

Input parameter "Correlation_Threshold" can be modified in settings.

Provided example demonstrates BTCUSD correlation with NASDAQ Composite . I advice to use weekly timeframe and set length to 26 week for this study

Kendall Rank Correlation Coefficient (alt)This is a non-parametric correlation statistical test, which is less sensitive to magnitude and more to direction, hence why some people call this a "concordance test".

This indicator was originally created by Alex Orekhov (everget), if you like this one, please show the original author some love:

This version is extended by tartigradia (2022) to make it more readily useable:

* Update to pinescript v5

* Default compare to current symbol (instead of only fixed symbols)

* Add 1.0, 0.0 and -1.0 correlation levels lines.

This indicator plots both the Kendall correlation in orange, and the more classical parametric Pearson correlation in purple for comparison. Either can be disabled in the Style tab.

Correlation with P-Value & Confidence Interval (alt)Shows the Pearson correlation between two symbols, including statistical significance test.

This is a fork of the original script by Balipour, with the addition of EMA that can be used instead of SMA in the Pearson correlation as an attempt to capture correlation trend changes more quickly, and conversion to pinescript v5. In the end, the EMA does not help much, for a faster capture of correlation trend changes, another kind of correlation is necessary, such as sign test correlation (another one of my indicators implement this idea).

Please show the original indicator's author some love if you appreciate this work:

Delta-Agnostic Correlation Coefficient (alt)Calculate a sort of correlation between two symbols based only on the sign of their changes, regardless of the amplitude of price change.

When positive, the two symbols tend to move together. When negative, the symbols move in opposite directions.

Since there is no significance calculation, and that the result is binary, keep in mind that correlation will always tend to go towards 1 or -1 even when there is no correlation. To reduce this issue, an EMA or SMA is applied to smooth out transitions: SMA smoothes over the selected length period but adds lag, whereas EMA smoothes amplitude without any additional lag. Hence, to know if the correlation is true or not, try to look at the amplitude and the number of consecutive days the correlation is maintained (both quantities are related), because when the correlation is spurious, it will tend to switch more or less alternatively between 1 and -1 and hence will hover around 0, whereas if the correlation is true, it will get further away from 0 and closer to 1 or -1.

In addition, since there is some time lag for the correlation to switch sign, the area is colored to know the current candle's correlation, regardless of past data's correlation: blue is a positive correlation (1), yellow is negative. The coloring can allow to know a trend reversal early on, but it's noisy.

Finally, symbols with closing days are better accounted for, with the correlation set to 0 on closed days (e.g., on week-ends), and the area is then colored in gray to signal that there is no new correlation data.

This is an improved fork over the original indicator by alexjvale, please show him some love if you like this work:

Normalized Correlation CoefficientThis is a normalized correlation coefficient that can be used with any timeframe or symbol desired (found in the indicator settings). The normalization function makes the coefficient bound between 0-1. There is a subjective threshold at 0.80 where anything below the threshold tends to be higher risk in trading as opposed to above the threshold.

Suggestions:

- Use a timeframe slightly higher than your current chart for optimal results.

- Do not use as a standalone strategy, rather, use it as a layer of confirmation.

- For altcoin cryptocurrencies, we suggest tethering the indicator to the "OTHERS" chart.

Greater Currency Correlation Matrix (Forex)Other available matrixes I found have a limited number of forex symbols. Consequentially, you need to keep switching them if you want to do a proper analysis. As a result of that, I produced my own currency matrix.

Correlation studies relationships between different price charts.

High correlation may be completely random in the short term, but it may signify a fundamental relationship between the two symbols if calculated over the long term.

For example, the currency of an oil-producing country may rally along with oil, whereas the importer's currency may drop. This means that watching the oil price chart may be worth it for such pairs.

The script includes all Major and Minor pairs with the addition of Gold (XAUEUR) and two optional symbols.

▬▬▬▬

To avoid too frequent use of security(), I decided to calculate all symbol values from EUR pairs. It should improve performance and keep room for some additional symbols in the future.

Please report any bugs.