VIX Monitor [Zero54]NSE:BANKNIFTY1!

This is a simple but invaluable tool for both day traders and positional traders. VIX is about market expectations of volatility

The VIX is a very good and sound measure of risk in the markets. It gives these stock traders who are in intraday trading and short term traders an idea of whether the volatility is going up or going down in the market. They can calibrate their strategy accordingly. When the volatility is likely to shoot up sharply, the intraday traders run the risk of stop losses getting triggered quickly. Hence they can either reduce their leverage or they can widen their stop losses accordingly.

Also if you notice VIX is a very good and reliable gauge of index movement. If you plot the VIX and the Nifty movement you will see a clear negative correlation in the charts itself. Markets typically tend to peak out when the VIX is bottoming out and the markets tend to bottom out when the VIX is peaking out. This is a useful input for index trades.

You can use this simple indicator to monitor VIX real time. You can use it for short time frame intraday and also multi-hour, multi-day charts. You can also plot a moving average to gauge the VIX trend.

Also is the ability to monitor, Nifty and BankNifty the same way you are able to monitor the VIX (as explained above). The overall market moves in correlation with these main Indexes. So if you are trading a specific counter, you can also keep an eye on the index to get an idea where the counter may be going next.

The source code is open, please feel to modify or re-use as you feel it’s necessary. Any changes, improvements, bugs, please let me know.

Please like/boost this indicator and also add your comments, if you find it useful.

Vi%

VIX, ATR, and Volatility Indicatorhere what the indictor do !

The "VIX, ATR, and Volatility Indicator" combines the Volatility Index (VIX), Average True Range (ATR), and moving averages to provide insights into market volatility.

VIX (Volatility Index):

The VIX measures the expected volatility in the market over the next 30 days. A higher VIX value indicates increased market volatility, while a lower value suggests lower volatility.

ATR (Average True Range):

The ATR is a technical indicator that measures the average range between high and low prices over a specified period. It provides a sense of the market's volatility by considering price movements. Higher ATR values indicate greater volatility, while lower values indicate lower volatility.

Moving Averages:

The indicator calculates both an Exponential Moving Average (EMA) and Simple Moving Average (SMA) with a specific period (e.g., 50).

Moving averages smooth out price data to identify trends and potential areas of support or resistance.

Volatility Detection:

By comparing the current closing price to the EMA and SMA, the indicator determines if there is high volatility.

If the current closing price is higher than either the EMA or SMA, it indicates potential high volatility.

Visualization:

The VIX and ATR are typically plotted on the chart, providing a visual representation of market volatility and price range.

Additionally, markers or labels may be used to highlight periods of high volatility when the current price exceeds the moving averages.

what are the VIX and ATR

Volatility Index (VIX):

Monitor the VIX value from financial platforms or market data providers. A higher VIX value indicates increased market volatility, suggesting potential trading opportunities. Conversely, a lower VIX value indicates lower volatility, which may influence your trading strategy.

Average True Range (ATR):

Calculate the ATR manually or use charting platforms that provide ATR as an indicator.

Plot the ATR on your trading chart to visualize the range of price movements.

Determine suitable entry and exit points based on ATR values. For example, higher ATR values may indicate larger potential price swings, while lower ATR values may suggest a more stable market.

how it work

Fetching VIX Data:

The request.security function is used to fetch the daily VIX data from the "CBOE:VIX" symbol. It retrieves the closing price of the VIX for each day.

Calculating ATR:

The ta.atr function calculates the Average True Range (ATR) with a period of 14. ATR measures the average range between the high and low prices over the specified period, providing an indication of market volatility.

Calculating Moving Averages:

Two types of moving averages are calculated: Exponential Moving Average (EMA) and Simple Moving Average (SMA). Both moving averages are calculated using a period of 50, but you can adjust the period as needed.

The ta.ema function calculates the Exponential Moving Average, which places greater weight on recent prices.

The ta.sma function calculates the Simple Moving Average, which gives equal weight to all prices in the period.

Identifying High Volatility:

The indicator determines if there is high volatility by comparing the current closing price to both the EMA and SMA.

If the current closing price is higher than either the EMA or SMA, the isHighVolatility variable is set to true, indicating potential high volatility.

Plotting the Indicators:

The VIX and ATR are plotted using the plot function, assigning colors and line widths for visual differentiation.

The plotshape function is used to plot markers below the bars to indicate highly volatile periods. The isHighVolatility variable determines when the markers appear.

Magic VIBIntroducing the "Magic Vib Indicator" – a powerful tool designed to identify and highlight unique market scenarios known as "magic volume imbalances." This indicator is specifically crafted to recognize specific candlestick patterns that have demonstrated a significant impact on price movements.

The Magic Vib Indicator is meticulously engineered to detect a particular pattern, which occurs when the high of the first candle aligns perfectly with the open of the subsequent candle, while simultaneously witnessing the close of the first candle matching the low of the second candle. These precise conditions generate what is commonly referred to as a "magic vib."

This indicator has been developed with the sole purpose of capturing these magical moments in the market. By systematically scanning and analyzing price data, it spots instances where these extraordinary price imbalances occur. Once identified, the indicator promptly marks these candles on your trading platform, providing clear visual cues for enhanced decision-making.

The Magic Vib Indicator acts as a catalyst for traders and investors, as it has proven to be a reliable precursor to significant price reactions. These marked candles act as potent signals, suggesting an impending shift in market sentiment and a high probability of substantial price movement. The resulting price action often sees significant volatility, making it an enticing opportunity for those seeking substantial gains.

However, it's important to note that while the Magic Vib Indicator offers valuable guidance, it should not be the sole basis for trading decisions. It is crucial to incorporate other technical and fundamental analysis tools, risk management strategies, and market awareness to achieve consistent success.

In summary, the Magic Vib Indicator represents a breakthrough in technical analysis, specifically tailored to identify and mark candles exhibiting the remarkable characteristics of a "magic volume imbalance." By harnessing the power of this indicator, traders can anticipate substantial price reactions, allowing them to seize opportunities and maximize their trading outcomes.

TTP VIX SpyTTP VIX Spy is an indicator that uses data from TVC:VIX to better time entries in the market.

The assumption used is that when the VIX is coming down from the top of its range then the risk on assets can move to the upside and when the VIX is is pushing higher there's a high likelihood or risk on assets going down.

This indicator observes the momentum of VIX using MACD. It offers two different signals both for longs and shorts: signal 1 and 2.

Signal 1 is activate when the begging of a new trend for the VIX is confirmed.

Signal 2 is activated when the VIX pulls back from an extreme value.

You can configure the parameters of the internal super trend and the look back for the slope applied to price and RSIs.

The indicator offers the following filter parameters:

- Price RSI slope: it filters signals that have RSI slope pointing in the opposite direction of the signal.

- Counter trend: it filters signals that are not counter trending super trend.

- Wide BBW: it filters signals that happen when there hasn't been high price volatility

- Price slope: it filters signals when the price is not pointing in the direction of the signal (buy: up, sell: down)

- VIX RSI filter: it filters VIX RSI values overextended. MACD can be in the right range, but sometimes RSI contradicts it. By default is OFF since it can cause false negatives.

- Working days only: it filters signals that occur in the weekend.

The colours below the price action show how the VIX momentum is changing. Transitions from red into pink and then green show how the fear is fading which tends to lead to lead to bullish moves, and the opposite when the transitions are from green to red.

Performance and initial thoughts.

I have tried VIX Spy on both BINANCE:BTCUSDT.P and BINANCE:ETHUSDT.P and it seems to offer a decent win ratio. As you can see I had to add many filter to remove bad entries and left toggles available to decide which ones you want to use.

I tried the signal in the 4H, 1H and 15min with mixed results. I tend to incline for the results in the 1H.

VIX signal offers a backtestable stream and alerts both for signals 1 and 2.

VIX HeatmapVIX HeatMap

Instructions:

- To be used with the S&P500 index (ES, SPX, SPY, any S&P ETF) as that's the input from where the CBOE calculates and measures the VIX. Can also be used with the Dow Jones, Nasdaq, & Nasdaq100.

Description:

- Expected Implied Volatility regime simplified & visualized. Know if we are in a high, medium, or low volatility regime, instantly.

- Ranges from Hot to Cold: The hotter the heat-map, the higher the implied volatility and fear & vice versa.

- The VIX HeatMap, color-maps important VIX levels (7 in this case) in measuring volatility for day trading & swing trading.

Using the VIX HeatMap:

- A LOW level volatility environment: Represented by "cooler" colors (Blue & White) depicts that the level of volatility and fear is low. Percentage moves on the index level are going to be tame and less volatile more often than not. Low fear = low perceived risk.

- A MEDIUM level volatility environment: Represented by "warmer" colors (Green & Yellow) depicts that the markets are transitioning from a calmer period or from a more fearful period. Market volatility here will be higher and provide more volatile swings in price.

- A HIGH level volatility environment: Represented by "hotter" colors (Orange, Red, & Purple) depicts that the markets are very fearful at the moment and will have big swings in both directions. Historically, extreme VIX levels tend to coincide with bottoms but are in no way predictive of the exact timing as the volatile moves can continue for an extended period of time.

- Transitioning between the 7 VIX Zones: Each and every one of these specific VIX zone levels is important.

1. Extreme low: <16

2. Low: 16 to 20

3. Normal: 20 to 24

4. Medium: 24 to 28

5. Med-High: 28 to 32

6. High: 32 to 36

7. Extreme high: >36

- These VIX levels in particular measure volatility changes that have a major impact on switching between smaller time frames and measuring depths of a sell move and vice versa. Each level also behaves as its own support & resistance level in terms of taking a bit of effort to switch regimes, and aids in identifying and measuring the potential depth of pullbacks in bull markets and bounces in bear markets to reveal reversal points.

- Examples of VIX level supports depicted on the chart marked with arrows. From left to right:

1. March 10th: Markets jumped 2 volatility levels in 2 days. The fluctuations from blue to yellow to green where a sign that price action would reverse from the selloff.

2. March 28th: As soon as we move from green to the blue VIX level (<20), markets began to rally and only ended when the volatility level moved sub VIX 16 (white).

3. May 4th & 24th: Next we see the 2 dips where volatility levels went from blue to green (VIX > 20), marked bottoms and reversed higher.

4. June 1st: We see a change in VIX regime yet again into lower VIX level and markets rocket higher.

Knowing the current VIX regime is a very important tool and aid in trading, now easily visualized.

BankNifty targets using VIX Version 2Original Idea Credit: Verified Market Waves

Hi,

After watching different videos online on how to get targets of BankNifty & Nifty decided to write this small script using VIX.

Nothing great but I really like the concept of getting high and low targets for the day or weekly or monthly or yearly.

What does the script do

1. We get closing of India Vix & BankNifty and Nifty

2. We get square root of Daily (365 days) | Weekly (52) | Monthly (12) & Yearly (1)

3. We divide India Vix closing with different square root to get a decimal value.

4. We use the derived value from step 3 which is used as % to calculate high and low values on BankNifty close price.

Small explanation via below screen shot to understand how to use it.

As always it comes with source code so you can modify as per your requirement.

Hope it helps 👍

Historical VolatilityThis script calculates the historical volatility of a given market using the standard deviation of its returns over a specified lookback period.

The indicator also includes a volatility Simple Moving Average (SMA), a VIX SMA, and the VIX index as reference market.

The script uses the inputs from the user to adjust the calculation, such as lookback period, volatility SMA period, and reference market.

The Historical Volatility indicator can be a useful tool for traders and investors who want to measure the degree of variation of a market's price over time, which can help them to better understand market trends and potential risks. This script is licensed under the Mozilla Public License 2.0, which means that it can be used, modified, and distributed under the terms of this license.

Adaptive Fusion ADX VortexIntroduction

The Adaptive Fusion ADX DI Vortex Indicator is a powerful tool designed to help traders identify trend strength and potential trend reversals in the market. This indicator uses a combination of technical analysis (TA) and mathematical concepts to provide accurate and reliable signals.

Features

The Adaptive Fusion ADX DI Vortex Indicator has several features that make it a powerful tool for traders. The Fusion Mode combines the Vortex Indicator and the ADX DI indicator to provide a more accurate picture of the market. The Hurst Exponent Filter helps to filter out choppy markets (inspired by balipour). Additionally, the indicator can be customized with various inputs and settings to suit individual trading strategies.

Signals

The enterLong signal is generated when the algorithm detects that it's a good time to buy a stock or other asset. This signal is based on certain conditions such as the values of technical indicators like ADX, Vortex, and Fusion. For example, if the ADX value is above a certain threshold and there is a crossover between the plus and minus lines of the ADX indicator, then the algorithm will generate an enterLong signal.

Similarly, the enterShort signal is generated when the algorithm detects that it's a good time to sell a stock or other asset. This signal is also based on certain conditions such as the values of technical indicators like ADX, Vortex, and Fusion. For example, if the ADX value is above a certain threshold and there is a crossunder between the plus and minus lines of the ADX indicator, then the algorithm will generate an enterShort signal.

The exitLong and exitShort signals are generated when the algorithm detects that it's a good time to close a long or short position, respectively. These signals are also based on certain conditions such as the values of technical indicators like ADX, Vortex, and Fusion. For example, if the ADX value crosses above a certain threshold or there is a crossover between the minus and plus lines of the ADX indicator, then the algorithm will generate an exitLong signal.

Usage

Traders can use this indicator in a variety of ways, depending on their trading strategy and style. Short-term traders may use it to identify short-term trends and potential trade opportunities, while long-term traders may use it to identify long-term trends and potential investment opportunities. The indicator can also be used to confirm other technical indicators or trading signals. Personally, I prefer to use it for short-term trades.

Strengths

One of the strengths of the Adaptive Fusion ADX DI Vortex Indicator is its accuracy and reliability. The indicator uses a combination of TA and mathematical concepts to provide accurate and reliable signals, helping traders make informed trading decisions. It is also versatile and can be used in a variety of trading strategies.

Weaknesses

While this indicator has many strengths, it also has some weaknesses. One of the weaknesses is that it can generate false signals in choppy or sideways markets. Additionally, the indicator may lag behind the market, making it less effective in fast-moving markets. That's a reason why I included the Hurst Exponent Filter and special smoothing.

Concepts

The Adaptive ADX DI Vortex Indicator with Fusion Mode and Hurst Filter is based on several key concepts. The Average Directional Index (ADX) is used to measure trend strength, while the Vortex Indicator is used to identify trend reversals. The Hurst Exponent is used to filter out noise and provide a more accurate picture of the market.

In conclusion, the Adaptive Fusion ADX DI Vortex Indicator is a versatile and powerful tool for traders. By combining technical analysis and mathematical concepts, this indicator provides accurate and reliable signals for identifying trend strength and potential trend reversals. While it has some weaknesses, its many strengths and features make it a valuable addition to any trader's toolbox.

---

Credits to:

▪️@cheatcountry – Hann Window Smoohing

▪️@loxx – VHF and T3

▪️@balipour – Hurst Exponent Filter

LNL Simple Hedging ToolLNL Simple Hedging Tool

Simple Hedging Tool was created specifically for swing traders who struggle with hedging. This tool helps to spot the ideal moments to put the hedges on (protection of the portfolio during "high risk" times). Simple Hedging Tool will not help you when day trading. It was designed for the daily charts. It is called simple because it is pretty much self-explanatory indicator. The candles are either blue or yellow. Meaning of the colors depend on the version you are using. This tool consist of two versions:

SPX Version:

This version was designed for indexes & overall market benchmarks. In contrast with the VIX version, the SPX version is little more sophisticated since it is based on key market internals. Blue arrows above the candles? More often than not this is signalizing that the key market internals are now approaching bearish signals which means it is the best time to hedge any bullish positions. On the contrary, the yellow arrows are the good reason to lighten up of the shorts & ease off the gas pedal on any bearish outlooks.

VIX Version:

Apart from the black swan events (big market crashes) Vix usually oscillates between the daily extremes. The VIX version is based on a simple bollinger band technique which is visualized with blue & yellow arrows. Whenever the yellow arrows & candles appear, it is good time to put the hedges on & perhaps lighten up on longs.

IMPORTANT DISCLAIMER:

The signals from this tool WILL NOT TELL YOU where to buy or sell! But rather when is a good time TO NOT buy or TO NOT sell. Once the signals appear it does not necessarily mean that the move is over & reversion willl happen immidiately. These signals can be flashing for days even weeks. They are not flashing for you to change the bias but rather tighten up your exposure in case your portfolio is mostly one sided.

Hope it helps.

Volatility Spike EstimatorPlots the Average True Range (ATR), its historical mean, the upper threshold for a volatility spike, and uses background color to show the likelihood of a volatility spike based on the current ATR value.

Green background indicates an increased likelihood of a volatility spike, while red background means a spike might have already occurred or be in progress.

Update: In this version, we added a short-term ATR calculation with an adjustable input parameter, shortTermATRLength. The likelihood of a volatility spike is now estimated based on the short-term ATR instead of the original ATR. This change makes the indicator more sensitive to recent market conditions and can help detect potential volatility spikes more quickly.

VIB / GIB v1.0The VIB / GIB indicator

V1 ----- 13 Feb 2023 ------------ Inital release.

This gives the user the ability to easily display VIB(Volume ImBalances) and GIB(Gap ImBalances) on their chart.

Volume imbalances (VIB) are created when there is a price difference between the close of a candle and the opening of the next candle. This price difference can be used as a level of support or resistance in future trading.

A Gap imbalance (GIB) has the same principles as a VIB, but also has the feature that no wick closes through the gap, showing an even more powerful imbalance in the market at that point.

GIBs and VIBs can be individually switched on or off via the settings, and optional icons can also be activated or not to show where the imbalance took place.

Please note that this is purely an indicator that should be used with other confluence before making trading decisions.

VIX Rule of 16There’s an interesting aspect of VIX that has to do with the number 16. (approximately the square root of the number of trading days in a year).

In any statistical model, 68.2% of price movement falls within one standard deviation (1 SD ). The rest falls into the “tails” outside of 1 SD .

When you divide any implied volatility (IV) reading (such as VIX ) by 16, the annualized number becomes a daily number

The essence of the “rule of 16.” Once you get it, you can do all sorts of tricks with it.

If the VIX is trading at 16, then one-third of the time, the market expects the S&P 500 Index (SPX) to trade up or down by more than 1% (because 16/16=1). A VIX at 32 suggests a move up or down of more than 2% a third of the time, and so on.

• VIX of 16 – 1/3 of the time the SPX will have a daily change of at least 1%

• VIX of 32 – 1/3 of the time the SPX will have a daily change of at least 2%

• VIX of 48 – 1/3 of the time the SPX will have a daily change of at least 3%

VIX/VOLI RatioWe all know TVC:VIX . But what is NASDAQ:VOLI ?

VOLI is basically a measure of expectations for market volatility over the next 30 calendar days as expressed by ATM options on AMEX:SPY

nations.com

So why is this VIX /VOLI ratio important? It's because it can give an important measure of options skew.

It can show the premium of OTM options (particularly puts) over ATM.

It can show if traders are interested in owning wings in AMEX:SPY

Not a lot of info can be taken by just looking at the ratio as a standalone nominal value. Plus, the ratio is noisy and spotting a clear trend can be hard.

For these reasons, I decided to code this indicator (which is best used on the Daily chart).

I added two EMA clouds, 7 and 12 and color code them with respect to their positions. If 7 > 12, cloud will be green. If 7 < 12, cloud will be red. This will give a better view of how the ratio is trending.

I then added a lookback period that can be changed from the indicator's setting (along with the fast and slow EMAs).

The lookback period will be used to get the following parameters:

- highest value

- lowest value

- 10th, 30th, 50th, 70th and 90th percentiles

- Percentile Rank

- Average, Median and Mode

Having all these values in a table will give a better idea of where the current ratio sits.

Volatility Inverse Correlation CandleThis is an educational tool that can help you find direct or inverse relations between two assets.

In this case I am using VIX and SPX .

The way it works is the next one :

So I am looking at the current open value of VIX in comparison with the previous close ( if it either above or below) and after on the SPX I am looking into the history and see for example which type of candle we had in respect with the opening value from VIX .

So for example, lets imagine that today is monday, and the weekly open value from VIX was higher than previous friday close value. Now I am going to see with the inverse correlation , if based on this idea, the current weekly candle from SPX finished in a bear candle.

The same can be applied for the bearish situation, so if we had an open from VIX lower than previous close, we are looking to check the SPX bull candle accuracy.

At the same time, for a different type of calculation I have added an internal lookup into heikin ashi values.

If you have any questions please let me know !

Williams Vix Fix ultra complete indicator (Tartigradia)Williams VixFix is a realized volatility indicator developed by Larry Williams, and can help in finding market bottoms.

Indeed, as Williams describe in his paper, markets tend to find the lowest prices during times of highest volatility, which usually accompany times of highest fear. The VixFix is calculated as how much the current low price statistically deviates from the maximum within a given look-back period.

Although the VixFix originally only indicates market bottoms, its inverse may indicate market tops. As masa_crypto writes : "The inverse can be formulated by considering "how much the current high value statistically deviates from the minimum within a given look-back period." This transformation equates Vix_Fix_inverse. This indicator can be used for finding market tops, and therefore, is a good signal for a timing for taking a short position." However, in practice, the Inverse VixFix is much less reliable than the classical VixFix, but is nevertheless a good addition to get some additional context.

For more information on the Vix Fix, which is a strategy published under public domain:

* The VIX Fix, Larry Williams, Active Trader magazine, December 2007, web.archive.org

* Fixing the VIX: An Indicator to Beat Fear, Amber Hestla-Barnhart, Journal of Technical Analysis, March 13, 2015, ssrn.com

* Replicating the CBOE VIX using a synthetic volatility index trading algorithm, Dayne Cary and Gary van Vuuren, Cogent Economics & Finance, Volume 7, 2019, Issue 1, doi.org

Created By ChrisMoody on 12-26-2014...

V3 MAJOR Update on 1-05-2014

tista merged LazyBear's Black Dots filter in 2020:

Extended by Tartigradia in 10-2022:

* Can select a symbol different from current to calculate vixfix, allows to select SP:SPX to mimic the original VIX index.

* Inverse VixFix (from masa_crypto and web.archive.org)

* VixFix OHLC Bars plot

* Price / VixFix Candles plot (Pro Tip: draw trend lines to find good entry/exit points)

* Add ADX filtering, Minimaxis signals, Minimaxis filtering (from samgozman )

* Convert to pinescript v5

* Allow timeframe selection (MTF)

* Skip off days (more accurate reproduction of original VIX)

* Reorganized, cleaned up code, commented out parts, commented out or removed unused code (eg, some of the KC calculations)

* Changed default Bollinger Band settings to reduce false positives in crypto markets.

Set Index symbol to SPX, and index_current = false, and timeframe Weekly, to reproduce the original VIX as close as possible by the VIXFIX (use the Add Symbol option, because you want to plot CBOE:VIX on the same timeframe as the current chart, which may include extended session / weekends). With the Weekly timeframe, off days / extended session days should not change much, but with lower timeframes this is important, because nights and weekends can change how the graph appears and seemingly make them different because of timing misalignment when in reality they are not when properly aligned.

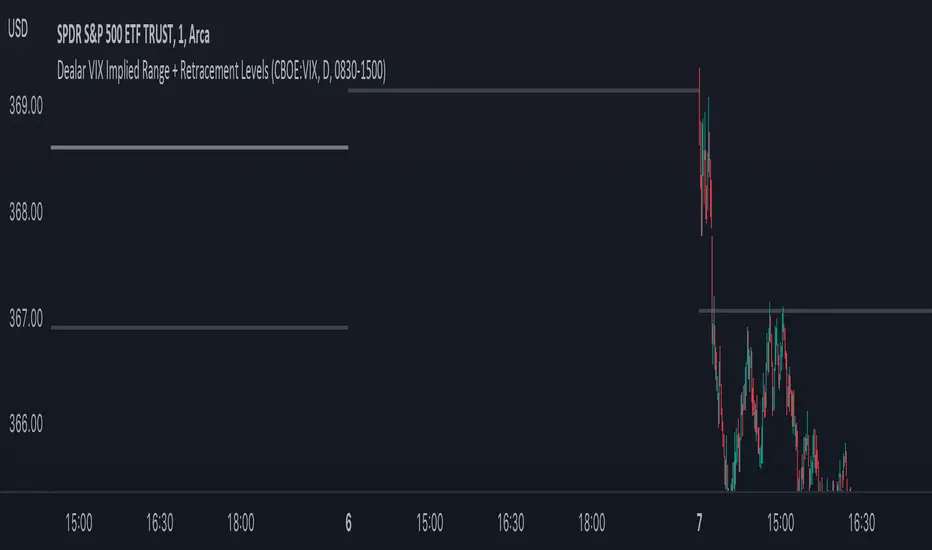

Dealar VIX Implied Range + Retracement LevelsThis Implied range Is derived by the VIX(1 sd annual +/- Implied move.)

This Indicator plots the daily Implied range, A lot of quantitative trading firms/ MM firms hedge their delta & gamma exposure around the Implied range(prop calc). I have added retracement levels as well, so you have more pivot levels.

Enjoy!

Full Volatility Statistics and Forecast

This is a tool designed to translate the data from the expected volatility of different assets, such as for example VIX, which measures the volatility of SP500 index.

Once get the data from the volatility asset we want to measure(for this test I have used VIX), we are going to translate it the required timeframe expected move by dividing the initial value into :

252 = if we want to use the daily timeframe, since there are ~252 aproximative daily trading days

52 = if we want to use the weekly timeframe, since there 52 trading weeks in a year

12 = if we want to use the monthly timeframe, since there are 12 months in a year

For this example I have used 252 with the daily timeframe.

In this scenario, we can see that we had 5711 total cnadles which we analysed, and in this case, we had 942 crosses, where the daily movement ended up either above or below the channel made from the opening daily candle value + expected movement from the volatility, giving as a total of 16.5% of occurances that volatility was higher than expected, and in 83.5% of the times, we can see that the price stayed within our channel.

At the same time, we can see that we had 6 max losses in a row ( OUT) AND 95 max wins in a row (IN), and at the same time in those moments when the volatility crosses happen we had a 0.51% avg movements when the top crossed happened, and 0.67% avg movements when the bot happened.

Lastly on the second part of the panel, we had E which means the expected movement of today, for example it has 61.056$ , so lets say price opened on 4083, our top is 4083 + 61 and our bot is 4083 - 61 ( giving us the daily channel). At continuation we can see that overall the avg bull candle os 0.714% and avg bear candle was 0.805% .

I hope this tool will help you with your future analysis and trades !

If you have any questions please let me know !

VIPThis indicator is using the modified "SSS".

This strategy uses combined indicators to create LONG entry points, the strategy was first found by saudALThaidy.

How to use: Open your asset and pick a timeframe between 5min and 2hours (recommended: 30min, 45min), the strategy will give entry points itself, you can monitor and take profit manually(recommended), or you can use the exit setup.

exit setup:

Take Profit : close the trade and take profit after the specified percentage from the entry point gets hit.

Use Stop Percentage : if false, trade will be closed if it gets below MA line, if true it will use the next set up.

StopLose Percentage : specify a percentage to close the trade if the asset price goes below it.

Important Notes:

As saudALThaidy states that the strategy must be used with -heiken ashi- candles for the best result.

for best use of the strategy, use (Take Profit = 1,Use Stop Percentage=false) to get every trade, and take profit manually when ever you see the best.

For any notes on the strategy to be edited, or for another strategies ideas please comment.

vol_boxA simple script to draw a realized volatility forecast, in the form of a box. The script calculates realized volatility using the EWMA method, using a number of periods of your choosing. Using the "periods per year", you can adjust the script to work on any time frame. For example, if you are using an hourly chart with bitcoin, there are 24 periods * 365 = 8760 periods per year. This setting is essential for the realized volatility figure to be accurate as an annualized figure, like VIX.

By default, the settings are set to mimic CBOE volatility indices. That is, 252 days per year, and 20 period window on the daily timeframe (simulating a 30 trading day period).

Inside the box are three figures:

1. The current realized volatility.

2. The rank. E.g. "10%" means the current realized volatility is less than 90% of realized volatility measures.

3. The "accuracy": how often price has closed within the box, historically.

Inputs:

stdevs: the number of standard deviations for the box

periods to project: the number of periods to forecast

window: the number of periods for calculating realized volatility

periods per year: the number of periods in one year (e.g. 252 for the "D" timeframe)

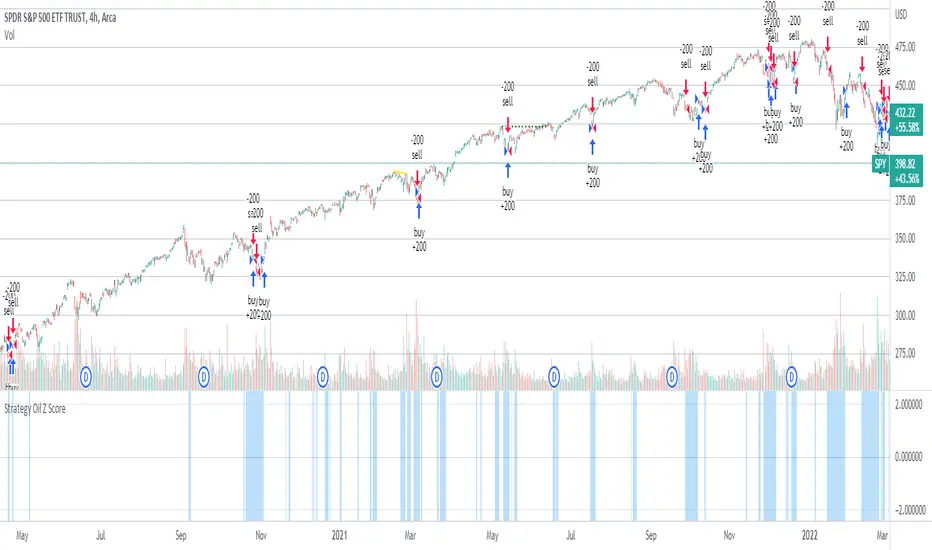

Strategy Oil Z ScoreObjective is to find forward looking indicators to find good entries into major index's.

In similar vein to my Combo Z Score script I have implemented one looking at oil and oil volatility. Interestingly the script out performs WITHOUT applying the EMA in longer timeframes but under performs in shorter timeframes, for example 2007 vs 2019. Likely due to the bullish nature of the past decade (by and large). You have some options on the underlying included Oil vs OVX (Best), MOVE vs OVX and VIX vs OVX. Oil vs OVX out performs Combo Z Script. Favours Spy over QQQ or derivations (SPXL etc).

Williams Vix Fix Bottoms and TopsThis indicator uses the very popular Williams Vix Fix for Bottoms by Chris Moody but not only does it search for bottoms, it can also be switch to work for tops for those who look to short the market. I've also added in a few options like flipping the indicator, color adjustments on the settings page, as well as cut a few of the options I feel did not need to be in which cluttered the screen when the settings were opened. In his later revisions of the Williams Vix Fix, CM took out the functions which draw the high/low ranges as well as the standard deviation which is what this indicator uses to show entry points. I have added options back on to draw these, I think it's useful. To be honest, I have not messed around with the number settings much so I am not sure how adjusting the look back range or going for smaller / bigger percentage changes would change how well the indicator works. It seems to work very well at its default settings.

With the Bollinger Band deviation, you have to remember that it looks back at the set amount of candles (20 by default) and uses those for the standard deviation: 1 dev = 68%, 2 dev = 95%, 3 dev = 99.7%

These percentages mean that at 2 dev, 95% of the last 20 candles will remain within the boundaries of the Bollinger Bands. Three tends to be too high, one is usually too low. Two is pretty good.

The lowest percentile option probably won't change much other than bring up the bottom line which doesn't effect the alerts or signals, just something to observe.

The highest percentile option makes a difference similar to the stand deviation and Bollinger Band. The higher you put it, the less likely it will get triggered but the more reliant it of a signal it should be.

As always, I have left notes throughout the code and I did leave in the code that was original but commented it out as I don't believe it's worth having.

I like to have the high/lows drawn, as well as the standard deviation. Then I find that the filtered entries are most accurate signals to follow. Simple entry is hit or miss, Aggressive entry is always early but sometimes that's not a great thing.

Strategy: Combo Z ScoreStrategy version of Combo Z Score

Objective:

Can we use both VIX and MOVE relationships to indicate movement in the SPY? VIX (forward contract on SPY options) correlations are quite common as forward indicators however MOVE (forward contract on bonds) also provides a slightly different level of insight

Using the Z-Score of VIX vs VVIX and MOVE vs inverted VIX (there is no M of Move so we use inverted Vix as a proxy) we get some helpful indications of potential future moves. Added %B to give us some exposure to momentum. Toggle VIX or MOVE.

If anyone has a better idea of inverted Vix to proxy forward interest in MOVE let me know.

Noticeable delta is that Vix only approach over the back test period is slightly better. Questions would be, what is the structure and nature of the market over the test period and in a bear market would MOVE or combined perform better.

Combo Z ScoreObjective:

Can we use both VIX and MOVE relationships to indicate movement in the SPY? VIX (forward contract on SPY options) correlations are quite common as forward indicators however MOVE (forward contract on bonds) also provides a slightly different level of insight

Using the Z-Score of VIX vs VVIX and MOVE vs inverted VIX (there is no M of Move so we use inverted Vix as a proxy) we get some helpful indications of potential future moves. Added %B to give us some exposure to momentum. Toggle VIX or MOVE.

If anyone has a better idea of inverted Vix to proxy forward interest in MOVE let me know.