Advanced Correlation Monitor📊 Advanced Correlation Monitor - Pine Script v6

🎯 What does this indicator do?

Monitors real-time correlations between 13 different asset pairs and alerts you when historically strong correlations break, indicating potential trading opportunities or changes in market dynamics.

🚀 Key Features

✨ Multi-Market Monitoring

7 Forex Pairs (GBPUSD/DXY, EURUSD/GBPUSD, etc.)

6 Index/Stock Pairs (SPY/S&P500, DAX/NASDAQ, TSLA/NVDA, etc.)

Fully configurable - change any pair from inputs

📈 Dual Correlation Analysis

Long Period (90 bars): Identifies historically strong correlations

Short Period (6 bars): Detects recent breakdowns

Pearson Correlation using Pine Script v6 native functions

🎨 Intuitive Visualization

Real-time table with 6 information columns

Color coding: Green (correlated), Red (broken), Gray (normal)

Visual states: 🟢 OK, 🔴 BROKEN, ⚫ NORMAL

🚨 Smart Alert System

Only alerts previously correlated pairs (>80% historical)

Detects breakdowns when short correlation <80%

Consolidated alert with all affected pairs

🛠️ Flexible Configuration

Adjustable Parameters:

📅 Periods: Long (30-500), Short (2-50)

🎯 Threshold: 50%-99% (default 80%)

🎨 Table: Configurable position and size

📊 Symbols: All pairs are configurable

Default Pairs:

FOREX: INDICES/STOCKS:

- GBPUSD vs DXY • SPY vs S&P500

- EURUSD vs GBPUSD • DAX vs S&P500

- EURUSD vs DXY • DAX vs NASDAQ

- USDCHF vs DXY • TSLA vs NVDA

- GBPUSD vs USDCHF • MSFT vs NVDA

- EURUSD vs USDCHF • AAPL vs NVDA

- EURUSD vs EURCAD

💡 Practical Use Cases

🔄 Pairs Trading

Detects when strong correlations break for:

Statistical arbitrage

Mean reversion trading

Divergence opportunities

🛡️ Risk Management

Identifies when "safe" assets start moving independently:

Portfolio diversification

Smart hedging

Regime change detection

📊 Market Analysis

Understand underlying market structure:

Forex/DXY correlations

Tech sector rotation

Regional market disconnection

🎓 Results Interpretation

Reading Example:

EURUSD vs DXY: -98.57% → -98.27% | 🟢 OK

└─ Perfect negative correlation maintained (EUR rises when DXY falls)

TSLA vs NVDA: 78.12% → 0% | ⚫ NORMAL

└─ Lost tech correlation (divergence opportunity)

Trading Signals:

🟢 → 🔴: Broken correlation = Possible opportunity

Large difference: Indicates correlation tension

Multiple breaks: Market regime change

Wyszukaj w skryptach "细算江西救护车家长倒赚了四万三+-医疗花费13万(家长视频)++医保报"

DA Cloud - DynamicDA Cloud - Dynamic | Detailed Overview

🌟 What Makes This Indicator Special

The DA Cloud - Dynamic is an advanced technical analysis tool that creates adaptive support and resistance zones that expand and contract based on market volatility. Unlike traditional static indicators, this cloud system "breathes" with the market, providing dynamic levels that adjust to changing market conditions.

📊 Core Components

1. Multi-Layered Cloud Structure

Resistance Cloud (Red): Three dynamic resistance levels (RL1, RL2, RL3) with intermediate channels (RC1, RC2)

Support Cloud (Green): Three dynamic support levels (SL1, SL2, SL3) with intermediate channels (SC1, SC2)

Trend Cloud (Blue): Five trend lines (TU2, TU1, TM, TL1, TL2) that flow through the center

Confirmation Line (Purple): A fast-reacting line that confirms trend changes

2. Forward Displacement Technology

The entire cloud system is projected 21 bars into the future (Fibonacci number), allowing traders to see potential support and resistance levels before price reaches them. This predictive element is inspired by Ichimoku Cloud theory but enhanced with modern volatility dynamics.

🔬 How It Works (Without Revealing the Secret Sauce)

Volatility-Responsive Design

The indicator continuously measures market volatility across multiple timeframes

During high volatility periods (like major breakouts), clouds expand dramatically

During consolidation, clouds contract and tighten around price

This creates a "breathing" effect that adapts to market conditions

Multi-Timeframe Analysis

Incorporates Fibonacci sequence periods (3, 13, 21, 34, 55) for calculations

Blends short-term responsiveness with long-term stability

Creates smooth, flowing lines that filter out market noise

Dynamic Level Calculation

Levels are not fixed percentages or static bands

Each level adapts based on current market structure and volatility

Channel lines (RC1, RC2, SC1, SC2) provide intermediate support/resistance

🎯 Key Features

1. Touch Point Detection

Colored dots appear when price touches key levels

Red dots = resistance touch

Green dots = support touch

Blue dots = trend median touch

2. Entry/Exit Signals

"Cloud Entry" labels when confirmation line crosses above SL1

"Cloud Exit" labels when confirmation line crosses below RL1

Background color changes based on bullish/bearish bias

3. Information Table

Real-time display of key levels (RL1, TM, SL1)

Current bias indicator (BULLISH/BEARISH)

Updates dynamically as market moves

⚙️ Customization Options

Main Controls:

Sensitivity (5-50): How responsive clouds are to price movements

Smoothing (1-50): Controls the flow and smoothness of cloud lines

Forward Displacement (0-50): How many bars to project the cloud forward

Advanced Volatility Settings:

Volatility Lookback (50-1000): Period for establishing volatility baseline

Volatility Smoothing (1-50): Reduces spikes in volatility expansion

Expansion Power (0.1-2.0): Controls how dramatically clouds expand

Range Divisor (1.0-20.0): Master control for overall cloud width

Level Spacing:

Individual multipliers for each resistance and support level

Allows fine-tuning of cloud structure to match different markets

Trend Spacing:

Separate controls for inner and outer trend bands

Customize the trend cloud density

📈 Trading Applications

1. Trend Identification

Price above TM (Trend Median) = Bullish bias

Price below TM = Bearish bias

Cloud color and width indicate trend strength

2. Support/Resistance Trading

Use RL1/SL1 as primary targets and reversal zones

RC1/RC2 and SC1/SC2 provide intermediate levels

RL3/SL3 mark extreme levels often seen at major tops/bottoms

3. Volatility Analysis

Expanding clouds signal increasing volatility and potential big moves

Contracting clouds indicate consolidation and potential breakout setup

Cloud width helps with position sizing and risk management

4. Multi-Timeframe Confirmation

Works on all timeframes from 1-minute to monthly

Higher timeframes show major market structure

Lower timeframes provide precise entry/exit points

🎓 Best Practices

Combine with Volume: High volume at cloud levels increases reliability

Watch for Touch Clusters: Multiple touches at a level indicate strength

Monitor Cloud Expansion: Sudden expansion often precedes major moves

Use Multiple Timeframes: Confirm signals across different time periods

Respect the Trend Median: This is often the most important level

⚡ Performance Notes

Optimized for up to 2000 bars of historical data

Smooth performance with 500+ lines and labels

Works on all markets: Crypto, Forex, Stocks, Commodities

📝 Version Info

Current Version: 1.0

Dynamic volatility expansion system

Full customization suite

Touch point detection

Entry/exit signals

Forward displacement projection

Expansion Triangle [TradingFinder] MegaPhone Broadening🔵 Introduction

The Expanding Triangle, also known as the Broadening Formation, is one of the key technical analysis patterns that clearly reflects growing market volatility, increasing indecision among participants, and the potential for sharp price explosions.

This pattern is typically defined by a sequence of higher highs and lower lows, forming within two diverging trendlines. Unlike traditional triangles that converge to a breakout point, the expanding triangle pattern becomes wider over time, leaving no precise apex for a breakout to occur.

From a price action perspective, the pattern represents a prolonged tug-of-war between buyers and sellers, where neither side has taken control yet. Each aggressive swing opens the door to new opportunities whether it's a trend reversal, range trading, or a momentum breakout. This dual nature makes the pattern highly versatile across market conditions, from exhausted trend ends to volatile consolidation zones.

The custom-built indicator for this pattern uses a combination of smart algorithms and detailed analysis of swing dynamics to automatically detect expanding triangles and highlight low-risk entry points.

Traders can use this tool to capitalize on high-probability setups from shorting near the upper edge of the structure with confirmation, to trading bearish breakouts during trend continuations, or entering long positions near the lower boundary during bullish reversals. The chart examples included in this article demonstrate these three highly practical trading scenarios in live market conditions.

A major advantage of this indicator lies in its structural filtering engine, which analyzes the behavior of each price leg in the triangle. With four adjustable filter levels from Very Aggressive, which highlights all potential patterns, to Very Defensive, which only triggers when price actually touches the triangle's trendlines the indicator ensures that only structurally sound and verified setups appear on the chart, reducing noise and false signals significantly.

Long Setup :

Short Setup :

🔵 How to Use

The pattern typically forms in conditions of heightened uncertainty and volatility, where price swings generate a series of higher highs and lower lows. The expanding triangle consists of three key legs bounded by diverging trendlines. The indicator intelligently analyzes each leg's direction and angle to determine whether a valid pattern is forming.

At the core of the indicator’s logic is its leg filtering system, which controls the quality of the pattern and filters out weak or noisy setups. Four structural filter modes are available to suit different trading styles and risk preferences. In Very Aggressive mode, filters are disabled, and the indicator detects any pattern purely based on the sequence of swing points.

This mode is ideal for traders who want to see everything and apply their own discretion.

In Aggressive mode, the indicator checks whether each new leg extends no more than twice the length of the previous one. If a leg overshoots excessively, the structure is invalidated.

In Defensive mode, the filter enforces a minimum movement requirement each leg must move at least 2% of the previous one. This prevents the formation of shallow, weak patterns that visually resemble triangles but lack substance.

The strictest setting, Very Defensive, combines all previous filters and additionally requires the price to physically touch the triangle’s trendlines before issuing a signal. This ensures that setups only appear when real market interaction with key structural levels has occurred, not based on assumptions or geometry alone. This mode is ideal for traders seeking maximum precision and minimal risk.

🟣 Bullish Setup

A bullish setup within the Expanding Triangle pattern occurs when price revisits the lower support boundary after a series of broad swings typically near the third leg of the formation. This area often represents a shift in momentum, where sellers begin to lose strength and buyers prepare to take control.

Ideally, the setup is accompanied by a bullish reversal candle (e.g. doji, pin bar, or engulfing) near the lower trendline. If the Very Defensive filter is active, the indicator will only issue a signal if price makes a confirmed touch on the trendline and reacts from that level. This significantly improves signal accuracy and filters out premature entries.

After confirmation, traders may choose to enter a long position on the bullish candle or shortly afterward. A logical stop-loss is placed just below the recent swing low within the pattern. The target can be set at or near the upper trendline, or projected using the full height of the triangle added to the breakout point. On higher timeframes, this reversal often marks the beginning of a strong uptrend.

🟣 Bearish Setup

A bearish setup forms when price climbs toward the upper resistance trendline, usually as the third leg completes. This is where buyers often begin to show exhaustion, and sellers step in with strength providing an ideal low-risk entry point for short positions.

As with the bullish setup, if the Candle Confirmation filter is enabled, the indicator will only show a signal when a bearish reversal candle forms at the point of contact. If Defensive or Very Defensive filters are also active, the setup must meet strict criteria of proportionate leg movement and an actual trendline touch to qualify.

Once confirmed, traders can enter on the reversal candle, placing a stop-loss slightly above the recent high. The target can be set at the lower trendline or calculated based on the triangle's full height, projected downward. This setup is particularly useful at the end of weak bullish trends or in volatile market tops.

🔵 Settings

🟣 Logic Settings

Pivot Period : Defines how many bars are analyzed to identify swing highs and lows. Higher values detect larger, slower structures, while lower values respond to faster patterns. The default value of 13 offers a balanced sensitivity.

Pattern Filter :

Very Aggressive : Detects all patterns based on point sequence with no structural checks.

Aggressive : Ensures each leg is no more than 2x the size of the previous one.

Defensive : Requires each leg to be at least 2% the size of the previous leg.

Very Defensive : The strictest level; only confirms patterns when price touches trendlines.

Candle Confirmation : When enabled, the indicator requires a valid confirmation candle (doji, pin bar, engulfing) at the interaction point with the trendline before issuing a signal. This reduces false entries and improves entry precision.

🟣 Alert Settings

Alert : Enables alerts for SSS.

Message Frequency : Determines the frequency of alerts. Options include 'All' (every function call), 'Once Per Bar' (first call within the bar), and 'Once Per Bar Close' (final script execution of the real-time bar). Default is 'Once per Bar'.

Show Alert Time by Time Zone : Configures the time zone for alert messages. Default is 'UTC'.

🔵 Conclusion

The Expanding Triangle pattern, with its wide structure and volatility-driven nature, represents chaos but also opportunity. For traders who can read its behavior, it provides some of the most powerful setups for reversals, breakouts, and range-based trades. While the pattern may seem messy at first glance, it is built on clear logic and when properly detected, it offers high-probability opportunities.

This indicator doesn’t just draw expanding triangles it intelligently evaluates their structural quality, validates price interaction through candle confirmation, and allows the trader to fine-tune the detection logic through adjustable filter levels. Whether you’re a reversal trader looking for a turning point, or a breakout trader hunting momentum, this tool adapts to your strategy.

In volatile or uncertain markets, where fakeouts and sudden shifts are common, this indicator can become a cornerstone of your trading system helping you turn volatility into structured, high-quality opportunities.

Fibonacci retracementHi all!

This indicator will show you the most recent Fibonacci retracement in the current trend. So if the trend is bullish the Fibonacci retracement will be drawn from swing low to high and from swing high to low in a bearish trend.

The uniqueness in this script lies in the adaptation to trend. To only plot the Fibonacci retracements according to the current market trend.

The trend is determined through break of structures (BOS) and change of characters (CHoCH). A change of character can be of type change of character plus (with a failed swing) and will then be shown as CHoCH+. This is possible through my library 'MarketStructure' (). It only uses break of structures and change of characters to be able to determine the trend, if you want a more detailed picture of the market structure you can use my script 'Market structure' ().

History and what to look for

Fibonacci retracement levels are used by many traders and are levels that are not Fibonacci sequence numbers themselves but they deriver from them. Some examples are:

23,6% - Divide a number by one three places ahead (e.g. 13/55)

38,2% - Divide a number by the one two places ahead (e.g. 21/55)

50% - Not from the Fibonacci sequence, but it's a number that price has reacted from in the past. Markets tend to retrace half a move before continuing

61,8% - The "golden retracement level". It derives from the "golden ratio" and is a core component of the Fibonacci sequence. The further you go in the Fibonacci sequence the preceding number divided by the current number will get closer and closer to this "golden ratio". This level is considered the most important Fibonacci retracement level by many traders

78,6% - Square root of 61.8%. This is often considered a deep correction (but not a trend reversal) and are often used for late entries

These levels are considered "key" and most significant. You want to look for a retracement of the price (down in a bullish trend and up in a bearish trend) to give you good entries.

Settings

For the trend you can set the pivot/swing lengths (right and left) and use the checkbox if you want these pivots to have labels. This can be done in the 'Market strucure' section.

In the 'Fibonacci retracement' section there is settings for the actual Fibonacci retracement. You can enable the trendline, set the color and the style of it. You can select which levels that should be shown by the indicator. There are 11 levels enabled by default, they are; 0-4.236. All settings in this section tries to be as similar to the "Fib Retracement" tool in Tradingview. You can also select the style of these lines (solid, dashed or dotted) and if you want them to extend to the right or not.

After this you can select if the Fibonacci retracement should be reversed or not, if prices should be displayed, if levels should be displayed and if to show the decimal levels or percentages and lastly the font size of these labels.

All defaults are based on the "Fib Retracement" tool by Tradingview.

Visualization

This indicator aims to be as visually similar to the default ("Fib Retracement") tool here on Tradingview. It will plot the Fibonacci retracement (called Auto Fibonacci/Auto fib) according to the trend from the library 'MarketStrucure'. The big differences from the "Fib Retracement" tool by Tradingview is that it's automatic (that adapts to trend), the market structure is visualized through lines and labels (showing 'BOS' for break of structures and 'CHoCH'/'CHoCH+' for change of characters) and that the labels showing information about the levels are positioned to be highly visible (left if <50% otherwise right if in a bullish trend, vice versa in a bearish trend or if reversed).

Don't hesitate if you have any feedback or nice feature suggestions!

Best of trading luck!

Staccked SMA - Regime Switching & Persistance StatisticsThis indicator is designed to identify the prevailing market regime by analyzing the behavior of a "stack" of Simple Moving Averages (SMAs). It helps you understand whether the market is currently trending, mean-reverting, or moving randomly.

Core Concept: SMA Correlation

At its heart, the indicator examines the relationship between a set of nine SMAs with different lengths (3, 5, 8, 13, 21, 34, 55, 89, 144) and the lengths themselves.

In a strong trending market (either up or down), the SMAs will be neatly "stacked" in order of their length. The shortest SMA will be furthest from the longest SMA, creating a strong, almost linear visual pattern. When we measure the statistical correlation between the SMA values and their corresponding lengths, we get a value close to +1 (perfect uptrend stack) or -1 (perfect downtrend stack). The absolute value of this correlation will be very high (close to 1).

In a mean-reverting or sideways market, the SMAs will be tangled and crisscrossing each other. There is no clear order, and the relationship between an SMA's length and its price value is weak. The correlation will be close to 0.

This indicator calculates this Pearson correlation on every bar, giving a continuous measure of how ordered or "trendy" the SMAs are. An absolute correlation above 0.8 is considered strongly trending, while a value between 0.4 and 0.8 suggests a mean-reverting character. Below 0.4, the market is likely random or choppy.

Regime Classification and Statistics

The indicator doesn't just look at the current correlation; it analyzes its behavior over a user-defined lookback window (default is 252 bars) to classify the overall market "regime."

It presents its findings in a clear table:

📊 |SMA Correlation| Regime Table: This main table provides a snapshot of the current market character.

Median: Shows the median absolute correlation over the lookback period, giving a central tendency of the market's behavior.

% > 0.80: The percentage of time the market was in a strong trend during the lookback period.

% < 0.80 & > 0.40: The percentage of time the market showed mean-reverting characteristics.

🧠 Regime: The final classification. It's labeled "📈 Trend-Dominant" if the median correlation is high and it has spent a significant portion of the time trending. It's labeled "🔄 Mean-Reverting" if the median is in the middle range and it has spent significant time in that state. Otherwise, it's considered "⚖️ Random/ Choppy".

📐 Regime Significance: This tells you how statistically confident you can be in the current regime classification, using a Z-score to compare its occurrence against random chance. ⭐⭐⭐ indicates high confidence (99%), while "❌ Not Significant" means the pattern could be random.

Regime Transition Probabilities

Optionally, a second table can be displayed that shows the historical probability of the market transitioning from one regime to another over different time horizons (t+5, t+10, t+15, and t+20 bars).

📈 → 🔄 → ⚖️ Transition Table: This table answers questions like, "If the market is trending now (From: 📈), what is the probability it will be mean-reverting (→ 🔄) in 10 bars?"

This provides powerful insights into the market's cyclical nature, helping you anticipate future behavior based on past patterns. For example, you might find that after a period of strong trending, a transition to a choppy state is more likely than a direct switch to a mean-reverting

Indicator Settings

Lookback Window for Regime Classification: This sets the number of recent bars (default is 252) the script analyzes to determine the current market regime (Trending, Mean-Reverting, or Random). A larger number provides a more stable, long-term view, while a smaller number makes the classification more sensitive to recent price action.

Show Regime Transition Table: A simple toggle (on/off) to show or hide the table that displays the probabilities of the market switching from one regime to another.

Lookback Offset for Starting Regime: This determines the "starting point" in the past for calculating regime transitions. The default is 20 bars ago. The script looks at the regime at this point and then checks what it became at later points.

Step 1, 2, 3, 4 Offset (bars): These define the future time intervals (5, 10, 15, and 20 bars by default) for the transition probability table. For example, the script checks the regime at the "Lookback Offset" and then sees what it transitioned to 5, 10, 15, and 20 bars later.

Significance Filter Settings

Use Regime Significance Filter: When enabled, this filter ensures that the regime transition statistics only count transitions that were "statistically significant." This helps to filter out noise and focus on more reliable patterns.

Min Stars Required (1=90%, 2=95%, 3=99%): This sets the minimum confidence level required for a regime to be included in the transition statistics when the significance filter is on.

1 ⭐: Requires at least 90% confidence.

2 ⭐⭐: Requires at least 95% confidence (default).

3 ⭐⭐⭐: Requires at least 99% confidence.

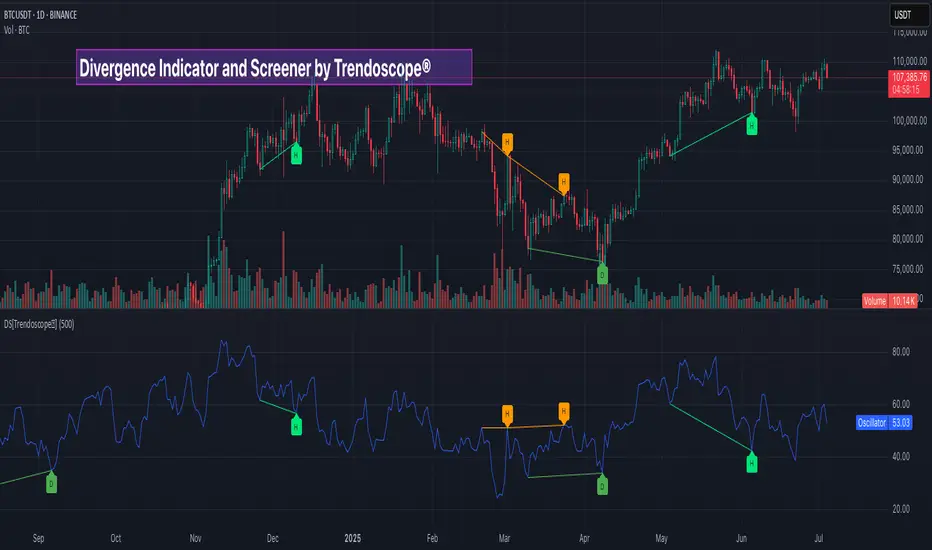

Divergence Screener [Trendoscope®]🎲Overview

The Divergence Screener is a powerful TradingView indicator designed to detect and visualize bullish and bearish divergences, including hidden divergences, between price action and a user-selected oscillator. Built with flexibility in mind, it allows traders to customize the oscillator type, trend detection method, and other parameters to suit various trading strategies. The indicator is non-overlay, displaying divergence signals directly on the oscillator plot, with visual cues such as lines and labels on the chart for easy identification.

This indicator is ideal for traders seeking to identify potential reversal or continuation signals based on price-oscillator divergences. It supports multiple oscillators, trend detection methods, and alert configurations, making it versatile for different markets and timeframes.

🎲Features

🎯Customizable Oscillator Selection

Built-in Oscillators : Choose from a variety of oscillators including RSI, CCI, CMO, COG, MFI, ROC, Stochastic, and WPR.

External Oscillator Support : Users can input an external oscillator source, allowing integration with custom or third-party indicators.

Configurable Length : Adjust the oscillator’s period (e.g., 14 for RSI) to fine-tune sensitivity.

🎯Divergence Detection

The screener identifies four types of divergences:

Bullish Divergence : Price forms a lower low, but the oscillator forms a higher low, signaling potential upward reversal.

Bearish Divergence : Price forms a higher high, but the oscillator forms a lower high, indicating potential downward reversal.

Bullish Hidden Divergence : Price forms a higher low, but the oscillator forms a lower low, suggesting trend continuation in an uptrend.

Bearish Hidden Divergence : Price forms a lower high, but the oscillator forms a higher high, suggesting trend continuation in a downtrend.

🎯Flexible Trend Detection

The indicator offers three methods to determine the trend context for divergence detection:

Zigzag : Uses zigzag pivots to identify trends based on higher highs (HH), higher lows (HL), lower highs (LH), and lower lows (LL).

MA Difference : Calculates the trend based on the difference in a moving average (e.g., SMA, EMA) between divergence pivots.

External Trend Signal : Allows users to input an external trend signal (positive for uptrend, negative for downtrend) for custom trend analysis.

🎯Zigzag-Based Pivot Analysis

Customizable Zigzag Length : Adjust the zigzag length (default: 13) to control the sensitivity of pivot detection.

Repaint Option : Choose whether divergence lines repaint based on the latest data or wait for confirmed pivots, balancing responsiveness and reliability.

🎯Visual and Alert Features

Divergence Visualization : Divergence lines are drawn between price pivots and oscillator pivots, color-coded for easy identification:

Bullish Divergence : Green

Bearish Divergence : Red

Bullish Hidden Divergence : Lime

Bearish Hidden Divergence : Orange

Labels and Tooltips : Labels (e.g., “D” for divergence, “H” for hidden) appear on price and oscillator pivots, with tooltips providing detailed information such as price/oscillator values, ratios, and pivot directions.

Alerts : Configurable alerts for each divergence type (bullish, bearish, bullish hidden, bearish hidden) trigger on bar close, ensuring timely notifications.

🎲 How It Works

🎯Oscillator Calculation

The indicator calculates the selected oscillator (or uses an external source) and plots it on the chart.

Oscillator values are stored in a map for reference during divergence calculations.

🎯Pivot Detection

A zigzag algorithm identifies pivots in the oscillator data, with configurable length and repainting options.

Price and oscillator pivots are compared to detect divergences based on their direction and ratio.

🎯Divergence Identification

The indicator compares price and oscillator pivot directions (HH, HL, LH, LL) to identify divergences.

Trend context is determined using the selected method (Zigzag, MA Difference, or External).

Divergences are classified as bullish, bearish, bullish hidden, or bearish hidden based on price-oscillator relationships and trend direction.

🎯Visualization and Alerts

Valid divergences are drawn as lines connecting price and oscillator pivots, with corresponding labels.

Alerts are triggered for allowed divergence types, providing detailed information via tooltips.

🎯Validation

Divergence lines are validated to ensure no intermediate bars violate the divergence condition, enhancing signal reliability.

🎲 Usage Instructions as Indicator

🎯Add to Chart:

Add the “Divergence Screener ” to your TradingView chart.

The indicator appears in a separate pane below the price chart, plotting the oscillator and divergence signals.

🎯Configure Settings:

Adjust the oscillator type and length to match your trading style.

Select a trend detection method and configure related parameters (e.g., MA type/length or external signal).

Set the zigzag length and repainting preference.

Enable/disable alerts for specific divergence types.

I🎯nterpret Signals:

Bullish Divergence (Green) : Look for potential buy opportunities in a downtrend.

Bearish Divergence (Red) : Consider sell opportunities in an uptrend.

Bullish Hidden Divergence (Lime) : Confirm continuation in an uptrend.

Bearish Hidden Divergence (Orange): Confirm continuation in a downtrend.

Use tooltips on labels to review detailed pivot and divergence information.

🎯Set Alerts:

Create alerts for each divergence type to receive notifications via TradingView’s alert system.

Alerts include detailed text with price, oscillator, and divergence information.

🎲 Example Scenarios as Indicator

🎯 With External Oscillator (Use MACD Histogram as Oscillator)

In order to use MACD as an oscillator for divergence signal instead of the built in options, follow these steps.

Load MACD Indicator from Indicator library

From Indicator settings of Divergence Screener, set Use External Oscillator and select MACD Histograme from the dropdown

You can now see that the oscillator pane shows the data of selected MACD histogram and divergence signals are generated based on the external MACD histogram data.

🎯 With External Trend Signal (Supertrend Ladder ATR)

Now let's demonstrate how to use external direction signals using Supertrend Ladder ATR indicator. Please note that in order to use the indicator as trend source, the indicator should return positive integer for uptrend and negative integer for downtrend. Steps are as follows:

Load the desired trend indicator. In this example, we are using Supertrend Ladder ATR

From the settings of Divergence Screener, select "External" as Trend Detection Method

Select the trend detection plot Direction from the dropdown. You can now see that the divergence signals will rely on the new trend settings rather than the built in options.

🎲 Using the Script with Pine Screener

The primary purpose of the Divergence Screener is to enable traders to scan multiple instruments (e.g., stocks, ETFs, forex pairs) for divergence signals using TradingView’s Pine Screener, facilitating efficient comparison and identification of trading opportunities.

To use the Divergence Screener as a screener, follow these steps:

Add to Favorites : Add the Divergence Screener to your TradingView favorites to make it available in the Pine Screener.

Create a Watchlist : Build a watchlist containing the instruments (e.g., stocks, ETFs, or forex pairs) you want to scan for divergences.

Access Pine Screener : Navigate to the Pine Screener via TradingView’s main menu: Products -> Screeners -> Pine, or directly visit tradingview.com/pine-screener/.

Select Watchlist : Choose the watchlist you created from the Watchlist dropdown in the Pine Screener interface.

Choose Indicator : Select Divergence Screener from the Choose Indicator dropdown.

Configure Settings : Set the desired timeframe (e.g., 1 hour, 1 day) and adjust indicator settings such as oscillator type, zigzag length, or trend detection method as needed.

Select Filter Criteria : Select the condition on which the watchlist items needs to be filtered. Filtering can only be done on the plots defined in the script.

Run Scan : Press the Scan button to display divergence signals across the selected instruments. The screener will show which instruments exhibit bullish, bearish, bullish hidden, or bearish hidden divergences based on the configured settings.

🎲 Limitations and Possible Future Enhancements

Limitations are

Custom input for oscillator and trend detection cannot be used in pine screener.

Pine screener has max 500 bars available.

Repaint option is by default enabled. When in repaint mode expect the early signal but the signals are prone to repaint.

Possible future enhancements

Add more built-in options for oscillators and trend detection methods so that dependency on external indicators is limited

Multi level zigzag support

log.info() - 5 Exampleslog.info() is one of the most powerful tools in Pine Script that no one knows about. Whenever you code, you want to be able to debug, or find out why something isn’t working. The log.info() command will help you do that. Without it, creating more complex Pine Scripts becomes exponentially more difficult.

The first thing to note is that log.info() only displays strings. So, if you have a variable that is not a string, you must turn it into a string in order for log.info() to work. The way you do that is with the str.tostring() command. And remember, it's all lower case! You can throw in any numeric value (float, int, timestamp) into str.string() and it should work.

Next, in order to make your output intelligible, you may want to identify whatever value you are logging. For example, if an RSI value is 50, you don’t want a bunch of lines that just say “50”. You may want it to say “RSI = 50”.

To do that, you’ll have to use the concatenation operator. For example, if you have a variable called “rsi”, and its value is 50, then you would use the “+” concatenation symbol.

EXAMPLE 1

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

//@version=6

indicator("log.info()")

rsi = ta.rsi(close,14)

log.info(“RSI= ” + str.tostring(rsi))

Example Output =>

RSI= 50

Here, we use double quotes to create a string that contains the name of the variable, in this case “RSI = “, then we concatenate it with a stringified version of the variable, rsi.

Now that you know how to write a log, where do you view them? There isn’t a lot of documentation on it, and the link is not conveniently located.

Open up the “Pine Editor” tab at the bottom of any chart view, and you’ll see a “3 dot” button at the top right of the pane. Click that, and right above the “Help” menu item you’ll see “Pine logs”. Clicking that will open that to open a pane on the right of your browser - replacing whatever was in the right pane area before. This is where your log output will show up.

But, because you’re dealing with time series data, using the log.info() command without some type of condition will give you a fast moving stream of numbers that will be difficult to interpret. So, you may only want the output to show up once per bar, or only under specific conditions.

To have the output show up only after all computations have completed, you’ll need to use the barState.islast command. Remember, barState is camelCase, but islast is not!

EXAMPLE 2

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

//@version=6

indicator("log.info()")

rsi = ta.rsi(close,14)

if barState.islast

log.info("RSI=" + str.tostring(rsi))

plot(rsi)

However, this can be less than ideal, because you may want the value of the rsi variable on a particular bar, at a particular time, or under a specific chart condition. Let’s hit these one at a time.

In each of these cases, the built-in bar_index variable will come in handy. When debugging, I typically like to assign a variable “bix” to represent bar_index, and include it in the output.

So, if I want to see the rsi value when RSI crosses above 0.5, then I would have something like

EXAMPLE 3

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

//@version=6

indicator("log.info()")

rsi = ta.rsi(close,14)

bix = bar_index

rsiCrossedOver = ta.crossover(rsi,0.5)

if rsiCrossedOver

log.info("bix=" + str.tostring(bix) + " - RSI=" + str.tostring(rsi))

plot(rsi)

Example Output =>

bix=19964 - RSI=51.8449459867

bix=19972 - RSI=50.0975830828

bix=19983 - RSI=53.3529808079

bix=19985 - RSI=53.1595745146

bix=19999 - RSI=66.6466337654

bix=20001 - RSI=52.2191767466

Here, we see that the output only appears when the condition is met.

A useful thing to know is that if you want to limit the number of decimal places, then you would use the command str.tostring(rsi,”#.##”), which tells the interpreter that the format of the number should only be 2 decimal places. Or you could round the rsi variable with a command like rsi2 = math.round(rsi*100)/100 . In either case you’re output would look like:

bix=19964 - RSI=51.84

bix=19972 - RSI=50.1

bix=19983 - RSI=53.35

bix=19985 - RSI=53.16

bix=19999 - RSI=66.65

bix=20001 - RSI=52.22

This would decrease the amount of memory that’s being used to display your variable’s values, which can become a limitation for the log.info() command. It only allows 4096 characters per line, so when you get to trying to output arrays (which is another cool feature), you’ll have to keep that in mind.

Another thing to note is that log output is always preceded by a timestamp, but for the sake of brevity, I’m not including those in the output examples.

If you wanted to only output a value after the chart was fully loaded, that’s when barState.islast command comes in. Under this condition, only one line of output is created per tick update — AFTER the chart has finished loading. For example, if you only want to see what the the current bar_index and rsi values are, without filling up your log window with everything that happens before, then you could use the following code:

EXAMPLE 4

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

//@version=6

indicator("log.info()")

rsi = ta.rsi(close,14)

bix = bar_index

if barstate.islast

log.info("bix=" + str.tostring(bix) + " - RSI=" + str.tostring(rsi))

Example Output =>

bix=20203 - RSI=53.1103309071

This value would keep updating after every new bar tick.

The log.info() command is a huge help in creating new scripts, however, it does have its limitations. As mentioned earlier, only 4096 characters are allowed per line. So, although you can use log.info() to output arrays, you have to be aware of how many characters that array will use.

The following code DOES NOT WORK! And, the only way you can find out why will be the red exclamation point next to the name of the indicator. That, and nothing will show up on the chart, or in the logs.

// CODE DOESN’T WORK

//@version=6

indicator("MW - log.info()")

var array rsi_arr = array.new()

rsi = ta.rsi(close,14)

bix = bar_index

rsiCrossedOver = ta.crossover(rsi,50)

if rsiCrossedOver

array.push(rsi_arr, rsi)

if barstate.islast

log.info("rsi_arr:" + str.tostring(rsi_arr))

log.info("bix=" + str.tostring(bix) + " - RSI=" + str.tostring(rsi))

plot(rsi)

// No code errors, but will not compile because too much is being written to the logs.

However, after putting some time restrictions in with the i_startTime and i_endTime user input variables, and creating a dateFilter variable to use in the conditions, I can limit the size of the final array. So, the following code does work.

EXAMPLE 5

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

// CODE DOES WORK

//@version=6

indicator("MW - log.info()")

i_startTime = input.time(title="Start", defval=timestamp("01 Jan 2025 13:30 +0000"))

i_endTime = input.time(title="End", defval=timestamp("1 Jan 2099 19:30 +0000"))

var array rsi_arr = array.new()

dateFilter = time >= i_startTime and time <= i_endTime

rsi = ta.rsi(close,14)

bix = bar_index

rsiCrossedOver = ta.crossover(rsi,50) and dateFilter // <== The dateFilter condition keeps the array from getting too big

if rsiCrossedOver

array.push(rsi_arr, rsi)

if barstate.islast

log.info("rsi_arr:" + str.tostring(rsi_arr))

log.info("bix=" + str.tostring(bix) + " - RSI=" + str.tostring(rsi))

plot(rsi)

Example Output =>

rsi_arr:

bix=20210 - RSI=56.9030578034

Of course, if you restrict the decimal places by using the rounding the rsi value with something like rsiRounded = math.round(rsi * 100) / 100 , then you can further reduce the size of your array. In this case the output may look something like:

Example Output =>

rsi_arr:

bix=20210 - RSI=55.6947486019

This will give your code a little breathing room.

In a nutshell, I was coding for over a year trying to debug by pushing output to labels, tables, and using libraries that cluttered up my code. Once I was able to debug with log.info() it was a game changer. I was able to start building much more advanced scripts. Hopefully, this will help you on your journey as well.

KST Strategy [Skyrexio]Overview

KST Strategy leverages Know Sure Thing (KST) indicator in conjunction with the Williams Alligator and Moving average to obtain the high probability setups. KST is used for for having the high probability to enter in the direction of a current trend when momentum is rising, Alligator is used as a short term trend filter, while Moving average approximates the long term trend and allows trades only in its direction. Also strategy has the additional optional filter on Choppiness Index which does not allow trades if market is choppy, above the user-specified threshold. Strategy has the user specified take profit and stop-loss numbers, but multiplied by Average True Range (ATR) value on the moment when trade is open. The strategy opens only long trades.

Unique Features

ATR based stop-loss and take profit. Instead of fixed take profit and stop-loss percentage strategy utilizes user chosen numbers multiplied by ATR for its calculation.

Configurable Trading Periods. Users can tailor the strategy to specific market windows, adapting to different market conditions.

Optional Choppiness Index filter. Strategy allows to choose if it will use the filter trades with Choppiness Index and set up its threshold.

Methodology

The strategy opens long trade when the following price met the conditions:

Close price is above the Alligator's jaw line

Close price is above the filtering Moving average

KST line of Know Sure Thing indicator shall cross over its signal line (details in justification of methodology)

If the Choppiness Index filter is enabled its value shall be less than user defined threshold

When the long trade is executed algorithm defines the stop-loss level as the low minus user defined number, multiplied by ATR at the trade open candle. Also it defines take profit with close price plus user defined number, multiplied by ATR at the trade open candle. While trade is in progress, if high price on any candle above the calculated take profit level or low price is below the calculated stop loss level, trade is closed.

Strategy settings

In the inputs window user can setup the following strategy settings:

ATR Stop Loss (by default = 1.5, number of ATRs to calculate stop-loss level)

ATR Take Profit (by default = 3.5, number of ATRs to calculate take profit level)

Filter MA Type (by default = Least Squares MA, type of moving average which is used for filter MA)

Filter MA Length (by default = 200, length for filter MA calculation)

Enable Choppiness Index Filter (by default = true, setting to choose the optional filtering using Choppiness index)

Choppiness Index Threshold (by default = 50, Choppiness Index threshold, its value shall be below it to allow trades execution)

Choppiness Index Length (by default = 14, length used in Choppiness index calculation)

KST ROC Length #1 (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)

KST ROC Length #2 (by default = 15, value used in KST indicator calculation, more information in Justification of Methodology)

KST ROC Length #3 (by default = 20, value used in KST indicator calculation, more information in Justification of Methodology)

KST ROC Length #4 (by default = 30, value used in KST indicator calculation, more information in Justification of Methodology)

KST SMA Length #1 (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)

KST SMA Length #2 (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)

KST SMA Length #3 (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)

KST SMA Length #4 (by default = 15, value used in KST indicator calculation, more information in Justification of Methodology)

KST Signal Line Length (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)

User can choose the optimal parameters during backtesting on certain price chart.

Justification of Methodology

Before understanding why this particular combination of indicator has been chosen let's briefly explain what is KST, Williams Alligator, Moving Average, ATR and Choppiness Index.

The KST (Know Sure Thing) is a momentum oscillator developed by Martin Pring. It combines multiple Rate of Change (ROC) values, smoothed over different timeframes, to identify trend direction and momentum strength. First of all, what is ROC? ROC (Rate of Change) is a momentum indicator that measures the percentage change in price between the current price and the price a set number of periods ago.

ROC = 100 * (Current Price - Price N Periods Ago) / Price N Periods Ago

In our case N is the KST ROC Length inputs from settings, here we will calculate 4 different ROCs to obtain KST value:

KST = ROC1_smooth × 1 + ROC2_smooth × 2 + ROC3_smooth × 3 + ROC4_smooth × 4

ROC1 = ROC(close, KST ROC Length #1), smoothed by KST SMA Length #1,

ROC2 = ROC(close, KST ROC Length #2), smoothed by KST SMA Length #2,

ROC3 = ROC(close, KST ROC Length #3), smoothed by KST SMA Length #3,

ROC4 = ROC(close, KST ROC Length #4), smoothed by KST SMA Length #4

Also for this indicator the signal line is calculated:

Signal = SMA(KST, KST Signal Line Length)

When the KST line rises, it indicates increasing momentum and suggests that an upward trend may be developing. Conversely, when the KST line declines, it reflects weakening momentum and a potential downward trend. A crossover of the KST line above its signal line is considered a buy signal, while a crossover below the signal line is viewed as a sell signal. If the KST stays above zero, it indicates overall bullish momentum; if it remains below zero, it points to bearish momentum. The KST indicator smooths momentum across multiple timeframes, helping to reduce noise and provide clearer signals for medium- to long-term trends.

Next, let’s discuss the short-term trend filter, which combines the Williams Alligator and Williams Fractals. Williams Alligator

Developed by Bill Williams, the Alligator is a technical indicator that identifies trends and potential market reversals. It consists of three smoothed moving averages:

Jaw (Blue Line): The slowest of the three, based on a 13-period smoothed moving average shifted 8 bars ahead.

Teeth (Red Line): The medium-speed line, derived from an 8-period smoothed moving average shifted 5 bars forward.

Lips (Green Line): The fastest line, calculated using a 5-period smoothed moving average shifted 3 bars forward.

When the lines diverge and align in order, the "Alligator" is "awake," signaling a strong trend. When the lines overlap or intertwine, the "Alligator" is "asleep," indicating a range-bound or sideways market. This indicator helps traders determine when to enter or avoid trades.

The next indicator is Moving Average. It has a lot of different types which can be chosen to filter trades and the Least Squares MA is used by default settings. Let's briefly explain what is it.

The Least Squares Moving Average (LSMA) — also known as Linear Regression Moving Average — is a trend-following indicator that uses the least squares method to fit a straight line to the price data over a given period, then plots the value of that line at the most recent point. It draws the best-fitting straight line through the past N prices (using linear regression), and then takes the endpoint of that line as the value of the moving average for that bar. The LSMA aims to reduce lag and highlight the current trend more accurately than traditional moving averages like SMA or EMA.

Key Features:

It reacts faster to price changes than most moving averages.

It is smoother and less noisy than short-term EMAs.

It can be used to identify trend direction, momentum, and potential reversal points.

ATR (Average True Range) is a volatility indicator that measures how much an asset typically moves during a given period. It was introduced by J. Welles Wilder and is widely used to assess market volatility, not direction.

To calculate it first of all we need to get True Range (TR), this is the greatest value among:

High - Low

abs(High - Previous Close)

abs(Low - Previous Close)

ATR = MA(TR, n) , where n is number of periods for moving average, in our case equals 14.

ATR shows how much an asset moves on average per candle/bar. A higher ATR means more volatility; a lower ATR means a calmer market.

The Choppiness Index is a technical indicator that quantifies whether the market is trending or choppy (sideways). It doesn't indicate trend direction — only the strength or weakness of a trend. Higher Choppiness Index usually approximates the sideways market, while its low value tells us that there is a high probability of a trend.

Choppiness Index = 100 × log10(ΣATR(n) / (MaxHigh(n) - MinLow(n))) / log10(n)

where:

ΣATR(n) = sum of the Average True Range over n periods

MaxHigh(n) = highest high over n periods

MinLow(n) = lowest low over n periods

log10 = base-10 logarithm

Now let's understand how these indicators work in conjunction and why they were chosen for this strategy. KST indicator approximates current momentum, when it is rising and KST line crosses over the signal line there is high probability that short term trend is reversing to the upside and strategy allows to take part in this potential move. Alligator's jaw (blue) line is used as an approximation of a short term trend, taking trades only above it we want to avoid trading against trend to increase probability that long trade is going to be winning.

Almost the same for Moving Average, but it approximates the long term trend, this is just the additional filter. If we trade in the direction of the long term trend we increase probability that higher risk to reward trade will hit the take profit. Choppiness index is the optional filter, but if it turned on it is used for approximating if now market is in sideways or in trend. On the range bounded market the potential moves are restricted. We want to decrease probability opening trades in such condition avoiding trades if this index is above threshold value.

When trade is open script sets the stop loss and take profit targets. ATR approximates the current volatility, so we can make a decision when to exit a trade based on current market condition, it can increase the probability that strategy will avoid the excessive stop loss hits, but anyway user can setup how many ATRs to use as a stop loss and take profit target. As was said in the Methodology stop loss level is obtained by subtracting number of ATRs from trade opening candle low, while take profit by adding to this candle's close.

Backtest Results

Operating window: Date range of backtests is 2023.01.01 - 2025.05.01. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 60%

Maximum Single Position Loss: -5.53%

Maximum Single Profit: +8.35%

Net Profit: +5175.20 USDT (+51.75%)

Total Trades: 120 (56.67% win rate)

Profit Factor: 1.747

Maximum Accumulated Loss: 1039.89 USDT (-9.1%)

Average Profit per Trade: 43.13 USDT (+0.6%)

Average Trade Duration: 27 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe and chart (optimal performance observed on 1h BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrexio commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation.

LVN/HVN Auto Detection [PhenLabs]📊 PhenLabs - LVN/HVN Auto Detection

Version: PineScript™ v6

📌 Description

The PhenLabs LVN/HVN Auto Detection indicator is an advanced volume profile analysis tool that automatically identifies Low Volume Nodes (LVN) and High Volume Nodes (HVN) across multiple trading sessions. This sophisticated indicator analyzes volume distribution patterns to pinpoint critical support and resistance levels where price is likely to react, providing traders with high-probability zones for entries, exits, and risk management.

Unlike traditional volume indicators that only show current activity, this tool builds comprehensive volume profiles from historical sessions and intelligently filters the most significant levels. It combines real-time volume analysis with dynamic level detection, offering both visual bubbles for immediate volume activity and persistent horizontal lines that act as ongoing support/resistance references.

🚀 Points of Innovation

Multi-Session Volume Profile Analysis - Automatically calculates and analyzes volume profiles across the last 5 trading sessions

Intelligent Level Separation Logic - Prevents overlapping signals by maintaining minimum separation between LVN and HVN levels

Dynamic Timeframe Adaptation - Automatically adjusts session lengths based on chart timeframe for optimal level detection

Real-Time Activity Bubbles - Shows volume activity strength through different bubble sizes at key levels

Persistent Line Management - Creates horizontal lines that extend until price crosses them, providing ongoing reference points

Dual Threshold System - Independent percentage-based thresholds for both LVN and HVN identification

🔧 Core Components

Volume Profile Engine : Builds 20-row volume profiles for each analyzed session, distributing volume across price levels

Level Identification Algorithm : Uses percentage-based thresholds to classify volume distribution patterns

Separation Logic : Ensures minimum distance between conflicting levels, prioritizing HVN when overlap occurs

Line Management System : Tracks active support/resistance lines and removes them when price crosses through

Volume Activity Monitor : Compares current volume to 13-period moving average for activity classification

🔥 Key Features

Customizable Thresholds : LVN threshold (5-35%, default 20%) and HVN threshold (65-95%, default 80%) for precise level filtering

Volume Activity Multiplier : Adjustable volume threshold (0.5+, default 1.5) for bubble and line creation sensitivity

Flexible Display Modes : Choose between Lines only, Bubbles only, or Both for optimal chart clarity

Smart Level Separation : Minimum separation percentage (0.1-2%, default 0.5%) prevents conflicting signals

Color Customization : Independent color controls for LVN (red) and HVN (blue) elements

Performance Optimization : Processes every 15 bars with maximum 500 active lines for smooth operation

🎨 Visualization

Colored Bubbles : Three sizes (large, medium, small) indicate volume activity strength at key levels

Horizontal Lines : Persistent support/resistance lines with width corresponding to volume activity

Dual Color System : Semi-transparent red for LVN areas, semi-transparent blue for HVN zones

Information Tooltip : Optional table showing usage guidelines and optimization tips

📖 Usage Guidelines

Volume Thresholds

LVN Threshold

○ Default: 20.0%

○ Range: 5.0-35.0%

○ Description: Price levels with volume below this percentage are marked as LVNs. Lower values create fewer, more significant levels. Typical range 15-25% works for most instruments.

HVN Threshold

○ Default: 80.0%

○ Range: 65.0-95.0%

○ Description: Price levels with volume above this percentage are marked as HVNs. Higher values create fewer, stronger levels. Range 75-85% is optimal for most trading.

Display Controls

Volume Threshold

○ Default: 1.5

○ Range: 0.5+

○ Description: Multiplier for volume significance (High=2+threshold, Medium=1+threshold, Low=0+threshold). Higher values require more volume for signals.

✅ Best Use Cases

Swing Trading : Identify key levels for position entries and exits over multiple days

Scalping : Use bubbles for immediate volume activity confirmation at critical levels

Risk Management : Place stops beyond LVN levels where price moves quickly

Breakout Trading : Monitor HVN levels for potential breakout or rejection scenarios

Multi-Timeframe Analysis : Combine with higher timeframe levels for confluence

⚠️ Limitations

Timeframe Sensitivity : Lower timeframes may produce too many levels; higher timeframes recommended for cleaner signals

Volume Data Dependency : Accuracy depends on reliable volume data from your data provider

Historical Analysis : Uses past volume data which may not predict future price behavior

Performance Impact : High number of active lines may affect chart performance on slower devices

💡 What Makes This Unique

Automated Session Analysis : No manual drawing required - automatically analyzes multiple sessions

Intelligent Filtering : Advanced separation logic prevents overlapping and conflicting signals

Adaptive Processing : Adjusts to different timeframes automatically for optimal level detection

Dual Visualization System : Combines persistent lines with real-time activity indicators

🔬 How It Works

1. Volume Profile Construction :

Analyzes the last 5 trading sessions with dynamic session length based on timeframe

Divides each session’s price range into 20 equal levels for volume distribution analysis

2. Level Classification :

Calculates volume percentage at each price level relative to session maximum

Identifies LVN levels below threshold and HVN levels above threshold

3. Signal Generation :

Creates bubbles when volume activity exceeds thresholds at identified levels

Draws horizontal lines that persist until price crosses through them

💡 Note : For optimal results, increase your chart timeframe if you see too many levels. The indicator performs best on 15-minute and higher timeframes where volume patterns are more meaningful and less noisy.

Tensor Market Analysis Engine (TMAE)# Tensor Market Analysis Engine (TMAE)

## Advanced Multi-Dimensional Mathematical Analysis System

*Where Quantum Mathematics Meets Market Structure*

---

## 🎓 THEORETICAL FOUNDATION

The Tensor Market Analysis Engine represents a revolutionary synthesis of three cutting-edge mathematical frameworks that have never before been combined for comprehensive market analysis. This indicator transcends traditional technical analysis by implementing advanced mathematical concepts from quantum mechanics, information theory, and fractal geometry.

### 🌊 Multi-Dimensional Volatility with Jump Detection

**Hawkes Process Implementation:**

The TMAE employs a sophisticated Hawkes process approximation for detecting self-exciting market jumps. Unlike traditional volatility measures that treat price movements as independent events, the Hawkes process recognizes that market shocks cluster and exhibit memory effects.

**Mathematical Foundation:**

```

Intensity λ(t) = μ + Σ α(t - Tᵢ)

```

Where market jumps at times Tᵢ increase the probability of future jumps through the decay function α, controlled by the Hawkes Decay parameter (0.5-0.99).

**Mahalanobis Distance Calculation:**

The engine calculates volatility jumps using multi-dimensional Mahalanobis distance across up to 5 volatility dimensions:

- **Dimension 1:** Price volatility (standard deviation of returns)

- **Dimension 2:** Volume volatility (normalized volume fluctuations)

- **Dimension 3:** Range volatility (high-low spread variations)

- **Dimension 4:** Correlation volatility (price-volume relationship changes)

- **Dimension 5:** Microstructure volatility (intrabar positioning analysis)

This creates a volatility state vector that captures market behavior impossible to detect with traditional single-dimensional approaches.

### 📐 Hurst Exponent Regime Detection

**Fractal Market Hypothesis Integration:**

The TMAE implements advanced Rescaled Range (R/S) analysis to calculate the Hurst exponent in real-time, providing dynamic regime classification:

- **H > 0.6:** Trending (persistent) markets - momentum strategies optimal

- **H < 0.4:** Mean-reverting (anti-persistent) markets - contrarian strategies optimal

- **H ≈ 0.5:** Random walk markets - breakout strategies preferred

**Adaptive R/S Analysis:**

Unlike static implementations, the TMAE uses adaptive windowing that adjusts to market conditions:

```

H = log(R/S) / log(n)

```

Where R is the range of cumulative deviations and S is the standard deviation over period n.

**Dynamic Regime Classification:**

The system employs hysteresis to prevent regime flipping, requiring sustained Hurst values before regime changes are confirmed. This prevents false signals during transitional periods.

### 🔄 Transfer Entropy Analysis

**Information Flow Quantification:**

Transfer entropy measures the directional flow of information between price and volume, revealing lead-lag relationships that indicate future price movements:

```

TE(X→Y) = Σ p(yₜ₊₁, yₜ, xₜ) log

```

**Causality Detection:**

- **Volume → Price:** Indicates accumulation/distribution phases

- **Price → Volume:** Suggests retail participation or momentum chasing

- **Balanced Flow:** Market equilibrium or transition periods

The system analyzes multiple lag periods (2-20 bars) to capture both immediate and structural information flows.

---

## 🔧 COMPREHENSIVE INPUT SYSTEM

### Core Parameters Group

**Primary Analysis Window (10-100, Default: 50)**

The fundamental lookback period affecting all calculations. Optimization by timeframe:

- **1-5 minute charts:** 20-30 (rapid adaptation to micro-movements)

- **15 minute-1 hour:** 30-50 (balanced responsiveness and stability)

- **4 hour-daily:** 50-100 (smooth signals, reduced noise)

- **Asset-specific:** Cryptocurrency 20-35, Stocks 35-50, Forex 40-60

**Signal Sensitivity (0.1-2.0, Default: 0.7)**

Master control affecting all threshold calculations:

- **Conservative (0.3-0.6):** High-quality signals only, fewer false positives

- **Balanced (0.7-1.0):** Optimal risk-reward ratio for most trading styles

- **Aggressive (1.1-2.0):** Maximum signal frequency, requires careful filtering

**Signal Generation Mode:**

- **Aggressive:** Any component signals (highest frequency)

- **Confluence:** 2+ components agree (balanced approach)

- **Conservative:** All 3 components align (highest quality)

### Volatility Jump Detection Group

**Volatility Dimensions (2-5, Default: 3)**

Determines the mathematical space complexity:

- **2D:** Price + Volume volatility (suitable for clean markets)

- **3D:** + Range volatility (optimal for most conditions)

- **4D:** + Correlation volatility (advanced multi-asset analysis)

- **5D:** + Microstructure volatility (maximum sensitivity)

**Jump Detection Threshold (1.5-4.0σ, Default: 3.0σ)**

Standard deviations required for volatility jump classification:

- **Cryptocurrency:** 2.0-2.5σ (naturally volatile)

- **Stock Indices:** 2.5-3.0σ (moderate volatility)

- **Forex Major Pairs:** 3.0-3.5σ (typically stable)

- **Commodities:** 2.0-3.0σ (varies by commodity)

**Jump Clustering Decay (0.5-0.99, Default: 0.85)**

Hawkes process memory parameter:

- **0.5-0.7:** Fast decay (jumps treated as independent)

- **0.8-0.9:** Moderate clustering (realistic market behavior)

- **0.95-0.99:** Strong clustering (crisis/event-driven markets)

### Hurst Exponent Analysis Group

**Calculation Method Options:**

- **Classic R/S:** Original Rescaled Range (fast, simple)

- **Adaptive R/S:** Dynamic windowing (recommended for trading)

- **DFA:** Detrended Fluctuation Analysis (best for noisy data)

**Trending Threshold (0.55-0.8, Default: 0.60)**

Hurst value defining persistent market behavior:

- **0.55-0.60:** Weak trend persistence

- **0.65-0.70:** Clear trending behavior

- **0.75-0.80:** Strong momentum regimes

**Mean Reversion Threshold (0.2-0.45, Default: 0.40)**

Hurst value defining anti-persistent behavior:

- **0.35-0.45:** Weak mean reversion

- **0.25-0.35:** Clear ranging behavior

- **0.15-0.25:** Strong reversion tendency

### Transfer Entropy Parameters Group

**Information Flow Analysis:**

- **Price-Volume:** Classic flow analysis for accumulation/distribution

- **Price-Volatility:** Risk flow analysis for sentiment shifts

- **Multi-Timeframe:** Cross-timeframe causality detection

**Maximum Lag (2-20, Default: 5)**

Causality detection window:

- **2-5 bars:** Immediate causality (scalping)

- **5-10 bars:** Short-term flow (day trading)

- **10-20 bars:** Structural flow (swing trading)

**Significance Threshold (0.05-0.3, Default: 0.15)**

Minimum entropy for signal generation:

- **0.05-0.10:** Detect subtle information flows

- **0.10-0.20:** Clear causality only

- **0.20-0.30:** Very strong flows only

---

## 🎨 ADVANCED VISUAL SYSTEM

### Tensor Volatility Field Visualization

**Five-Layer Resonance Bands:**

The tensor field creates dynamic support/resistance zones that expand and contract based on mathematical field strength:

- **Core Layer (Purple):** Primary tensor field with highest intensity

- **Layer 2 (Neutral):** Secondary mathematical resonance

- **Layer 3 (Info Blue):** Tertiary harmonic frequencies

- **Layer 4 (Warning Gold):** Outer field boundaries

- **Layer 5 (Success Green):** Maximum field extension

**Field Strength Calculation:**

```

Field Strength = min(3.0, Mahalanobis Distance × Tensor Intensity)

```

The field amplitude adjusts to ATR and mathematical distance, creating dynamic zones that respond to market volatility.

**Radiation Line Network:**

During active tensor states, the system projects directional radiation lines showing field energy distribution:

- **8 Directional Rays:** Complete angular coverage

- **Tapering Segments:** Progressive transparency for natural visual flow

- **Pulse Effects:** Enhanced visualization during volatility jumps

### Dimensional Portal System

**Portal Mathematics:**

Dimensional portals visualize regime transitions using category theory principles:

- **Green Portals (◉):** Trending regime detection (appear below price for support)

- **Red Portals (◎):** Mean-reverting regime (appear above price for resistance)

- **Yellow Portals (○):** Random walk regime (neutral positioning)

**Tensor Trail Effects:**

Each portal generates 8 trailing particles showing mathematical momentum:

- **Large Particles (●):** Strong mathematical signal

- **Medium Particles (◦):** Moderate signal strength

- **Small Particles (·):** Weak signal continuation

- **Micro Particles (˙):** Signal dissipation

### Information Flow Streams

**Particle Stream Visualization:**

Transfer entropy creates flowing particle streams indicating information direction:

- **Upward Streams:** Volume leading price (accumulation phases)

- **Downward Streams:** Price leading volume (distribution phases)

- **Stream Density:** Proportional to information flow strength

**15-Particle Evolution:**

Each stream contains 15 particles with progressive sizing and transparency, creating natural flow visualization that makes information transfer immediately apparent.

### Fractal Matrix Grid System

**Multi-Timeframe Fractal Levels:**

The system calculates and displays fractal highs/lows across five Fibonacci periods:

- **8-Period:** Short-term fractal structure

- **13-Period:** Intermediate-term patterns

- **21-Period:** Primary swing levels

- **34-Period:** Major structural levels

- **55-Period:** Long-term fractal boundaries

**Triple-Layer Visualization:**

Each fractal level uses three-layer rendering:

- **Shadow Layer:** Widest, darkest foundation (width 5)

- **Glow Layer:** Medium white core line (width 3)

- **Tensor Layer:** Dotted mathematical overlay (width 1)

**Intelligent Labeling System:**

Smart spacing prevents label overlap using ATR-based minimum distances. Labels include:

- **Fractal Period:** Time-based identification

- **Topological Class:** Mathematical complexity rating (0, I, II, III)

- **Price Level:** Exact fractal price

- **Mahalanobis Distance:** Current mathematical field strength

- **Hurst Exponent:** Current regime classification

- **Anomaly Indicators:** Visual strength representations (○ ◐ ● ⚡)

### Wick Pressure Analysis

**Rejection Level Mathematics:**

The system analyzes candle wick patterns to project future pressure zones:

- **Upper Wick Analysis:** Identifies selling pressure and resistance zones

- **Lower Wick Analysis:** Identifies buying pressure and support zones

- **Pressure Projection:** Extends lines forward based on mathematical probability

**Multi-Layer Glow Effects:**

Wick pressure lines use progressive transparency (1-8 layers) creating natural glow effects that make pressure zones immediately visible without cluttering the chart.

### Enhanced Regime Background

**Dynamic Intensity Mapping:**

Background colors reflect mathematical regime strength:

- **Deep Transparency (98% alpha):** Subtle regime indication

- **Pulse Intensity:** Based on regime strength calculation

- **Color Coding:** Green (trending), Red (mean-reverting), Neutral (random)

**Smoothing Integration:**

Regime changes incorporate 10-bar smoothing to prevent background flicker while maintaining responsiveness to genuine regime shifts.

### Color Scheme System

**Six Professional Themes:**

- **Dark (Default):** Professional trading environment optimization

- **Light:** High ambient light conditions

- **Classic:** Traditional technical analysis appearance

- **Neon:** High-contrast visibility for active trading

- **Neutral:** Minimal distraction focus

- **Bright:** Maximum visibility for complex setups

Each theme maintains mathematical accuracy while optimizing visual clarity for different trading environments and personal preferences.

---

## 📊 INSTITUTIONAL-GRADE DASHBOARD

### Tensor Field Status Section

**Field Strength Display:**

Real-time Mahalanobis distance calculation with dynamic emoji indicators:

- **⚡ (Lightning):** Extreme field strength (>1.5× threshold)

- **● (Solid Circle):** Strong field activity (>1.0× threshold)

- **○ (Open Circle):** Normal field state

**Signal Quality Rating:**

Democratic algorithm assessment:

- **ELITE:** All 3 components aligned (highest probability)

- **STRONG:** 2 components aligned (good probability)

- **GOOD:** 1 component active (moderate probability)

- **WEAK:** No clear component signals

**Threshold and Anomaly Monitoring:**

- **Threshold Display:** Current mathematical threshold setting

- **Anomaly Level (0-100%):** Combined volatility and volume spike measurement

- **>70%:** High anomaly (red warning)

- **30-70%:** Moderate anomaly (orange caution)

- **<30%:** Normal conditions (green confirmation)

### Tensor State Analysis Section

**Mathematical State Classification:**

- **↑ BULL (Tensor State +1):** Trending regime with bullish bias

- **↓ BEAR (Tensor State -1):** Mean-reverting regime with bearish bias

- **◈ SUPER (Tensor State 0):** Random walk regime (neutral)

**Visual State Gauge:**

Five-circle progression showing tensor field polarity:

- **🟢🟢🟢⚪⚪:** Strong bullish mathematical alignment

- **⚪⚪🟡⚪⚪:** Neutral/transitional state

- **⚪⚪🔴🔴🔴:** Strong bearish mathematical alignment

**Trend Direction and Phase Analysis:**

- **📈 BULL / 📉 BEAR / ➡️ NEUTRAL:** Primary trend classification

- **🌪️ CHAOS:** Extreme information flow (>2.0 flow strength)

- **⚡ ACTIVE:** Strong information flow (1.0-2.0 flow strength)

- **😴 CALM:** Low information flow (<1.0 flow strength)

### Trading Signals Section

**Real-Time Signal Status:**

- **🟢 ACTIVE / ⚪ INACTIVE:** Long signal availability

- **🔴 ACTIVE / ⚪ INACTIVE:** Short signal availability

- **Components (X/3):** Active algorithmic components

- **Mode Display:** Current signal generation mode

**Signal Strength Visualization:**

Color-coded component count:

- **Green:** 3/3 components (maximum confidence)

- **Aqua:** 2/3 components (good confidence)

- **Orange:** 1/3 components (moderate confidence)

- **Gray:** 0/3 components (no signals)

### Performance Metrics Section

**Win Rate Monitoring:**

Estimated win rates based on signal quality with emoji indicators:

- **🔥 (Fire):** ≥60% estimated win rate

- **👍 (Thumbs Up):** 45-59% estimated win rate

- **⚠️ (Warning):** <45% estimated win rate

**Mathematical Metrics:**

- **Hurst Exponent:** Real-time fractal dimension (0.000-1.000)

- **Information Flow:** Volume/price leading indicators

- **📊 VOL:** Volume leading price (accumulation/distribution)

- **💰 PRICE:** Price leading volume (momentum/speculation)

- **➖ NONE:** Balanced information flow

- **Volatility Classification:**

- **🔥 HIGH:** Above 1.5× jump threshold

- **📊 NORM:** Normal volatility range

- **😴 LOW:** Below 0.5× jump threshold

### Market Structure Section (Large Dashboard)

**Regime Classification:**

- **📈 TREND:** Hurst >0.6, momentum strategies optimal

- **🔄 REVERT:** Hurst <0.4, contrarian strategies optimal

- **🎲 RANDOM:** Hurst ≈0.5, breakout strategies preferred

**Mathematical Field Analysis:**

- **Dimensions:** Current volatility space complexity (2D-5D)

- **Hawkes λ (Lambda):** Self-exciting jump intensity (0.00-1.00)

- **Jump Status:** 🚨 JUMP (active) / ✅ NORM (normal)

### Settings Summary Section (Large Dashboard)

**Active Configuration Display:**

- **Sensitivity:** Current master sensitivity setting

- **Lookback:** Primary analysis window

- **Theme:** Active color scheme

- **Method:** Hurst calculation method (Classic R/S, Adaptive R/S, DFA)

**Dashboard Sizing Options:**

- **Small:** Essential metrics only (mobile/small screens)

- **Normal:** Balanced information density (standard desktop)

- **Large:** Maximum detail (multi-monitor setups)

**Position Options:**

- **Top Right:** Standard placement (avoids price action)

- **Top Left:** Wide chart optimization

- **Bottom Right:** Recent price focus (scalping)