SeparatorsSession - H1 and below Time Frame

Day - H4 and below Time Frame

Month - D Time Frame

Quarter - W Time Frame

Wyszukaj w skryptach "session"

Session Key Levels Lines (with Labels)This is an extension of the previous indicator, it just plots all the information you need automatically for you so you dont have to lift a finger. hope it helps :)

Session Moving AveragesAdds EMAs and SMAs to chart using 8am-8pm EST values. Completely configurable in settings.

Some platforms allow users to configure what time frame they would like to view market data. One popular selection is 8am-8pm EST as 8am is when institutional orders go through. An argument can be made that price action before 8am EST is not valid yet moving averages will use that data.

This matters less for shorter moving averages such as a 9 or 20 ema, but it dramatically changes the 200 or the 50 sma for example.

This script allows you to ignore that pre-market data (or any data you choose to configure in the settings) and select up to 3 moving averages (either Exponential or Simple) for a set time.

By default the moving averages include the 9-ema (gray), 20-ema (green), and 200-sma (purple) and is set to 8am-8pm EST

This is configurable in the settings including the time frame you would like the moving averages to start using market data.

By default the script will use your charts timeframe. You are able to use multi-time frames with this script just scroll down to "timeframe", then click "chart" in settings... this will then allow you to select a timeframe.

A popular choice is 5-minute value of 8am-8pm EST moving averages. This means regardless of the time frame you are on (sub 1-minute, 1-minute, etc.) the script will display 5-minute data.

Final note: In settings you are able to turn on/off shapes (the gray lines at the bottom) which shows when the data is being used. This can be helpful on certain tickers that trade continuously such as /ES or /NQ.

Session Time RangesHave you ever wondered if you are trading at the right time of the day or feel like all the good trades happen when you are sleeping? Well now you can check your theory :)

This Script allows you to highlight a time range on your chart over a 24hour time period. For example 3AM to 6AM

The script has two time variables, set your start time and end time based on a 24 hour clock and set the time zone offset variable to match your charts time zone. For example New York -4 (for utc just enter 0 for no offset )

This is a quick script I put together so hopefully it is error free enjoy :)

Session P4L MTFCorrected indicator for better support of smaller time frames. version 3.0 with better interface. thank you

Session P EdgesThis is an attempt to chart the primary balance ranges, however,

I have been having difficulty getting the lows to work in the graph, any assistance would be welcome

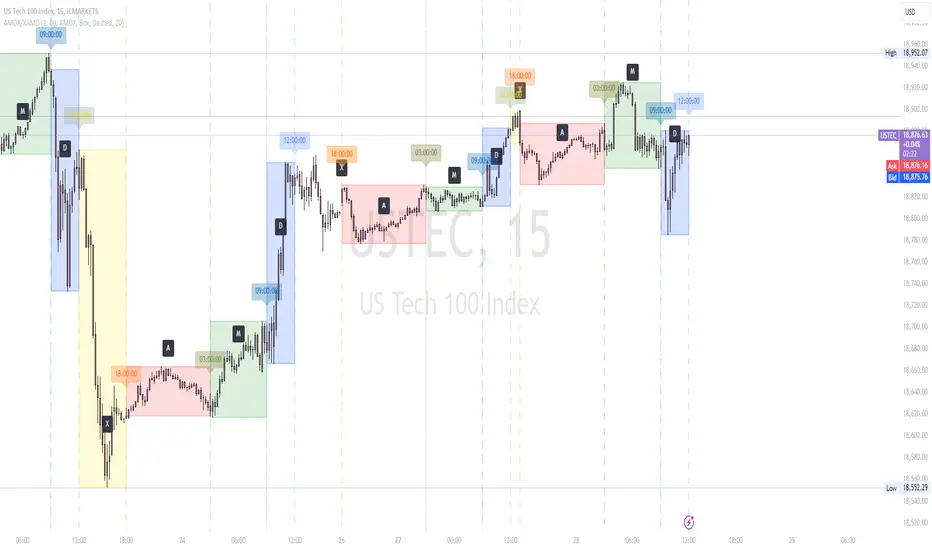

AMDX/XAMD indicatorThe AMDX/XAMD indicator is designed to highlight specific trading sessions on the chart using distinct colors and optional vertical lines. Users can choose between two session types, AMDX or XAMD, and customize the visual appearance of the sessions. This tool is particularly useful for traders who want to analyze market behavior during different trading periods.

Meaning of AMDX:

A: Accumulation

M: Manipulation

D: Distribution

X: Continuation Or Reversal

Features:

Session Highlighting:

AMDX Sessions: Split into four segments - A, M, D, X.

XAMD Sessions: Split into four segments - X, A, M, D.

Customizable Colors:

Choose individual colors for each session (A, M, D, X).

Adjust the transparency of the session boxes for better visual integration with the chart.

Drawing Styles:

Box Style: Draws colored boxes around the session ranges.

Line Style: Draws vertical lines at session start and end times.

Vertical Lines:

Option to enable or disable vertical lines at session boundaries.

Customizable line style: Solid, Dotted, or Dashed.

Session Labels:

Automatically labels each session for easy identification.

Customization Options:

Session Type: Select between AMDX and XAMD session types.

Colors: Set custom colors for each session and vertical lines.

Border Width: Adjust the width of the session box borders.

Transparency: Control the transparency level of the session boxes.

Drawing Style: Choose between Box and Line styles for session representation.

Vertical Lines: Enable or disable vertical lines and select the line style.

How It Works:

The indicator calculates the start and end times for each session based on the selected session type (AMDX or XAMD). It then draws either boxes or lines to highlight these sessions on the chart. The indicator also includes options to draw vertical lines at the session boundaries and labels each session with a corresponding letter (A, M, D, X).

Use Cases:

Market Session Analysis: Easily identify and analyze market behavior during different trading sessions.

Intraday Trading: Helps intraday traders to focus on specific time segments of the trading day.

Visual Segmentation: Provides a clear visual segmentation of the trading day, aiding in better decision-making.

Times for AMDX/XAMD session:

A Session: 18:00 (previous day) to 03:00 (current day)

M Session: 03:00 to 09:00

D Session: 09:00 to 12:00

X Session: 12:00 to 18:00

Time for the XAMD session :

X Session: 18:00 (previous day) to 00:00 (current day)

A Session: 00:00 to 09:00

M Session: 09:00 to 12:00

D Session: 12:00 to 18:00

Time Zone PSenseiTitle: Time Zone PS Indicator

Author: Orlando Depablos

Description:

The Time Zone PS Indicator is a tool designed to help traders visualize different trading sessions on their charts. It allows users to specify three different trading sessions: the start of the day, the London session, and the New York (NYC) session. Each session is represented by a distinct color-coded background on the chart.

Features:

Customizable Sessions: Traders can define the start time and end time for each trading session according to their preference. This flexibility enables users to tailor the indicator to their specific trading strategies session time zones.

Session Display Control: Users have the option to choose whether they want to display each trading session on the chart. This feature allows for a clutter-free charting experience, where traders can focus on the sessions relevant to their analysis.

Visual Clarity: The indicator uses distinct colors for each trading session, making it easy for traders to differentiate between different time zones. This visual clarity aids in quickly identifying key trading periods throughout the day.

How to Use:

Setting Up Sessions: Use the input options to define the start and end times for the start of the day, the London session, and the NYC session. Adjust these values based on your trading preferences and time zone.

Display Preferences: Toggle the display options to choose which trading sessions you want to visualize on the chart. This allows for a customizable charting experience tailored to your specific needs.

Interpreting the Chart: Once configured, the indicator will display color-coded backgrounds on the chart corresponding to the defined trading sessions. Interpret these visual cues to identify key trading periods and plan your trading strategies accordingly.

Originality:

The Time Zone PS Indicator adds value to the TradingView community by providing traders with a customizable tool to visualize different trading sessions. While similar indicators exist, this script offers flexibility and ease of use, enhancing the charting experience for traders across various time zones.

Use Cases:

Session-Based Analysis: Traders can use the indicator to analyze price action within specific trading sessions, such as the London or NYC session, to identify potential trading opportunities.

Time Zone Adjustment: Traders operating in different time zones can adjust the indicator settings to align with their local trading hours, ensuring accurate visualization of relevant trading sessions.

Strategy Development: The indicator can aid in the development of trading strategies that capitalize on price movements during specific trading sessions, helping traders optimize their trading performance.

Chart Visualization:

The indicator provides a clear and concise visualization of different trading sessions on the chart. Each session is represented by a color-coded background, allowing traders to quickly identify key trading periods and make informed trading decisions.

Volume Profile [Makit0]VOLUME PROFILE INDICATOR v0.5 beta

Volume Profile is suitable for day and swing trading on stock and futures markets, is a volume based indicator that gives you 6 key values for each session: POC, VAH, VAL, profile HIGH, LOW and MID levels. This project was born on the idea of plotting the RTH sessions Value Areas for /ES in an automated way, but you can select between 3 different sessions: RTH, GLOBEX and FULL sessions.

Some basic concepts:

- Volume Profile calculates the total volume for the session at each price level and give us market generated information about what price and range of prices are the most traded (where the value is)

- Value Area (VA): range of prices where 70% of the session volume is traded

- Value Area High (VAH): highest price within VA

- Value Area Low (VAL): lowest price within VA

- Point of Control (POC): the most traded price of the session (with the most volume)

- Session HIGH, LOW and MID levels are also important

There are a huge amount of things to know of Market Profile and Auction Theory like types of days, types of openings, relationships between value areas and openings... for those interested Jim Dalton's work is the way to come

I'm in my 2nd trading year and my goal for this year is learning to daytrade the futures markets thru the lens of Market Profile

For info on Volume Profile: TV Volume Profile wiki page at www.tradingview.com

For info on Market Profile and Market Auction Theory: Jim Dalton's book Mind over markets (this is a MUST)

BE AWARE: this indicator is based on the current chart's time interval and it only plots on 1, 2, 3, 5, 10, 15 and 30 minutes charts.

This is the correlation table TV uses in the Volume Profile Session Volume indicator (from the wiki above)

Chart Indicator

1 - 5 1

6 - 15 5

16 - 30 10

31 - 60 15

61 - 120 30

121 - 1D 60

This indicator doesn't follow that correlation, it doesn't get the volume data from a lower timeframe, it gets the data from the current chart resolution.

FEATURES

- 6 key values for each session: POC (solid yellow), VAH (solid red), VAL (solid green), profile HIGH (dashed silver), LOW (dashed silver) and MID (dotted silver) levels

- 3 sessions to choose for: RTH, GLOBEX and FULL

- select the numbers of sessions to plot by adding 12 hours periods back in time

- show/hide POC

- show/hide VAH & VAL

- show/hide session HIGH, LOW & MID levels

- highlight the periods of time out of the session (silver)

- extend the plotted lines all the way to the right, be careful this can turn the chart unreadable if there are a lot of sessions and lines plotted

SETTINGS

- Session: select between RTH (8:30 to 15:15 CT), GLOBEX (17:00 to 8:30 CT) and FULL (17:00 to 15:15 CT) sessions. RTH by default

- Last 12 hour periods to show: select the deph of the study by adding periods, for example, 60 periods are 30 natural days and around 22 trading days. 1 period by default

- Show POC (Point of Control): show/hide POC line. true by default

- Show VA (Value Area High & Low): show/hide VAH & VAL lines. true by default

- Show Range (Session High, Low & Mid): show/hide session HIGH, LOW & MID lines. true by default

- Highlight out of session: show/hide a silver shadow over the non session periods. true by default

- Extension: Extend all the plotted lines to the right. false by default

HOW TO SETUP

BE AWARE THIS INDICATOR PLOTS ONLY IN THE FOLLOWING CHART RESOLUTIONS: 1, 2, 3, 5, 10, 15 AND 30 MINUTES CHARTS. YOU MUST SELECT ONE OF THIS RESOLUTIONS TO THE INDICATOR BE ABLE TO PLOT

- By default this indicator plots all the levels for the last RTH session within the last 12 hours, if there is no plot try to adjust the 12 hours periods until the seesion and the periods match

- For Globex/Full sessions just select what you want from the dropdown menu and adjust the periods to plot the values

- Show or hide the levels you want with the 3 groups: POC line, VA lines and Session Range lines

- The highlight and extension options are for a better visibility of the levels as POC or VAH/VAL

THANKS TO

@watsonexchange for all the help, ideas and insights on this and the last two indicators (Market Delta & Market Internals) I'm working on my way to a 'clean chart' but for me it's not an easy path

@PineCoders for all the amazing stuff they do and all the help and tools they provide, in special the Script-Stopwatch at that was key in lowering this indicator's execution time

All the TV and Pine community, open source and shared knowledge are indeed the best way to help each other

IF YOU REALLY LIKE THIS WORK, please send me a comment or a private message and TELL ME WHAT you trade, HOW you trade it and your FAVOURITE SETUP for pulling out money from the market in a consistent basis, I'm learning to trade (this is my 2nd year) and I need all the help I can get

GOOD LUCK AND HAPPY TRADING

ICT Opening Range Projections (tristanlee85)ICT Opening Range Projections

This indicator visualizes key price levels based on ICT's (Inner Circle Trader) "Opening Range" concept. This 30-minute time interval establishes price levels that the algorithm will refer to throughout the session. The indicator displays these levels, including standard deviation projections, internal subdivisions (quadrants), and the opening price.

🟪 What It Does

The Opening Range is a crucial 30-minute window where market algorithms establish significant price levels. ICT theory suggests this range forms the basis for daily price movement.

This script helps you:

Mark the high, low, and opening price of each session.

Divide the range into quadrants (premium, discount, and midpoint/Consequent Encroachment).

Project potential price targets beyond the range using configurable standard deviation multiples .

🟪 How to Use It

This tool aids in time-based technical analysis rooted in ICT's Opening Range model, helping you observe price interaction with algorithmic levels.

Example uses include:

Identifying early structural boundaries.

Observing price behavior within premium/discount zones.

Visualizing initial displacement from the range to anticipate future moves.

Comparing price reactions at projected standard deviation levels.

Aligning price action with significant times like London or NY Open.

Note: This indicator provides a visual framework; it does not offer trade signals or interpretations.

🟪 Key Information

Time Zone: New York time (ET) is required on your chart.

Sessions: Supports multiple sessions, including NY midnight, NY AM, NY PM, and three custom timeframes.

Time Interval: Supports multi-timeframe up to 15 minutes. Best used on a 1-minute chart for accuracy.

🟪 Session Options

The Opening Range interval is configurable for up to 6 sessions:

Pre-defined ICT Sessions:

NY Midnight: 12:00 AM – 12:30 AM ET

NY AM: 9:30 AM – 10:00 AM ET

NY PM: 1:30 PM – 2:00 PM ET

Custom Sessions:

Three user-defined start/end time pairs.

This example shows a custom session from 03:30 - 04:00:

🟪 Understanding the Levels

The Opening Price is the open of the first 1-minute candle within the chosen session.

At session close, the Opening Range is calculated using its High and Low . An optional swing-based mode uses swing highs/lows for range boundaries.

The range is divided into quadrants by its midpoint ( Consequent Encroachment or CE):

Upper Quadrant: CE to high (premium).

Lower Quadrant: Low to CE (discount).

These subdivisions help visualize internal range dynamics, where price often reacts during algorithmic delivery.

🟪 Working with Ranges

By default, the range is determined by the highest high and lowest low of the 30-minute session:

A range can also be determined by the highest/lowest swing points:

Quadrants outline the premium and discount of a range that price will reference:

Small ranges still follow the same algorithmic logic, but may be deemed insignificant for one's trading. These can be filtered in the settings by specifying a minimum ticks limit. In this example, the range is 42 ticks (10.5 points) but the indicator is configured for 80 ticks (20 points). We can select which levels will plot if the range is below the limit. Here, only the 00:00 opening price is plotted:

You may opt to include the range high/low, quadrants, and projections as well. This will plot a red (configurable) range bracket to indicate it is below the limit while plotting the levels:

🟪 Price Projections

Projections extend beyond the Opening Range using standard deviations, framing the market beyond the initial session and identifying potential targets. You define the standard deviation multiples (e.g., 1.0, 1.5, 2.0).

Both positive and negative extensions are displayed, symmetrically projected from the range's high and low.

The Dynamic Levels option plots only the next projection level once price crosses the previous extreme. For example, only the 0.5 STDEV level plots until price reaches it, then the 1.0 level appears, and so on. This continues up to your defined maximum projections, or indefinitely if standard deviations are set to 0.

This example shows dynamic levels for a total of 6 sessions, only 1 of which meet a configured minimum limit of 50 ticks:

Small ranges followed by significant displacement are impacted the most with the number of levels plotted. You may hide projections when configuring the minimum ticks.

A fixed standard deviation will plot levels in both directions, regardless of the price range. Here, we plot up to 3.0 which hiding projections for small ranges:

🟪 Legal Disclaimer

This indicator is provided for informational and educational purposes only. It is not financial advice, and should not be construed as a recommendation to buy or sell any financial instrument. Trading involves substantial risk, and you could lose a significant amount of money. Past performance is not indicative of future results. Always consult with a qualified financial professional before making any trading or investment decisions. The creators and distributors of this indicator assume no responsibility for your trading outcomes.

Custom V2 KillZone US / FVG / EMAThis indicator is designed for traders looking to analyze liquidity levels, opportunity zones, and the underlying trend across different trading sessions. Inspired by the ICT methodology, this tool combines analysis of Exponential Moving Averages (EMA), session management, and Fair Value Gap (FVG) detection to provide a structured and disciplined approach to trading effectively.

Indicator Features

Identifying the Underlying Trend with Two EMAs

The indicator uses two EMAs on different, customizable timeframes to define the underlying trend:

EMA1 (default set to a daily timeframe): Represents the primary underlying trend.

EMA2 (default set to a 4-hour timeframe): Helps identify secondary corrections or impulses within the main trend.

These two EMAs allow traders to stay aligned with the market trend by prioritizing trades in the direction of the moving averages. For example, if prices are above both EMAs, the trend is bullish, and long trades are favored.

Analysis of Market Sessions

The indicator divides the day into key trading sessions:

Asian Session

London Session

US Pre-Open Session

Liquidity Kill Session

US Kill Zone Session

Each session is represented by high and low zones as well as mid-lines, allowing traders to visualize liquidity levels reached during these periods. Tracking the price levels in different sessions helps determine whether liquidity levels have been "swept" (taken) or not, which is essential for ICT methodology.

Liquidity Signal ("OK" or "STOP")

A specific signal appears at the end of the "Liquidity Kill" session (just before the "US Kill Zone" session):

"OK" Signal: Indicates that liquidity conditions are favorable for trading the "US Kill Zone" session. This means that liquidity levels have been swept in previous sessions (Asian, London, US Pre-Open), and the market is ready for an opportunity.

"STOP" Signal: Indicates that it is not favorable to trade the "US Kill Zone" session, as certain liquidity conditions have not been met.

The "OK" or "STOP" signal is based on an analysis of the high and low levels from previous sessions, allowing traders to ensure that significant liquidity zones have been reached before considering positions in the "Kill Zone".

Detection of Fair Value Gaps (FVG) in the US Kill Zone Session

When an "OK" signal is displayed, the indicator identifies Fair Value Gaps (FVG) during the "US Kill Zone" session. These FVGs are areas where price may return to fill an "imbalance" in the market, making them potential entry points.

Bullish FVG: Detected when there is a bullish imbalance, providing a buying opportunity if conditions align with the underlying trend.

Bearish FVG: Detected when there is a bearish imbalance, providing a selling opportunity in the trend direction.

FVG detection aligns with the ICT Silver Bullet methodology, where these imbalance zones serve as probable entry points during the "US Kill Zone".

How to Use This Indicator

Check the Underlying Trend

Before trading, observe the two EMAs (daily and 4-hour) to understand the general market trend. Trades will be prioritized in the direction indicated by these EMAs.

Monitor Liquidity Signals After the Asian, London, and US Pre-Open Sessions

The high and low levels of each session help determine if liquidity has already been swept in these areas. At the end of the "Liquidity Kill" session, an "OK" or "STOP" label will appear:

"OK" means you can look for trading opportunities in the "US Kill Zone" session.

"STOP" means it is preferable not to take trades in the "US Kill Zone" session.

Look for Opportunities in the US Kill Zone if the Signal is "OK"

When the "OK" label is present, focus on the "US Kill Zone" session. Use the Fair Value Gaps (FVG) as potential entry points for trades based on the ICT methodology. The identified FVGs will appear as colored boxes (bullish or bearish) during this session.

Use ICT Methodology to Manage Your Trades

Follow the FVGs as potential reversal zones in the direction of the trend, and manage your positions according to your personal strategy and the rules of the ICT Silver Bullet method.

Customizable Settings

The indicator includes several customization options to suit the trader's preferences:

EMA: Length, source (close, open, etc.), and timeframe.

Market Sessions: Ability to enable or disable each session, with color and line width settings.

Liquidity Signals: Customization of colors for the "OK" and "STOP" labels.

FVG: Option to display FVGs or not, with customizable colors for bullish and bearish FVGs, and the number of bars for FVG extension.

-------------------------------------------------------------------------------------------------------------

Cet indicateur est conçu pour les traders souhaitant analyser les niveaux de liquidité, les zones d’opportunité, et la tendance de fond à travers différentes sessions de trading. Inspiré de la méthodologie ICT, cet outil combine l'analyse des moyennes mobiles exponentielles (EMA), la gestion des sessions de marché, et la détection des Fair Value Gaps (FVG), afin de fournir une approche structurée et disciplinée pour trader efficacement.

Opening Range Breakout with Multi-Timeframe Liquidity]═══════════════════════════════════════

OPENING RANGE BREAKOUT WITH MULTI-TIMEFRAME LIQUIDITY

═══════════════════════════════════════

A professional Opening Range Breakout (ORB) indicator enhanced with multi-timeframe liquidity detection, trading session visualization, volume analysis, and trend confirmation tools. Designed for intraday trading with comprehensive alert system.

───────────────────────────────────────

WHAT THIS INDICATOR DOES

───────────────────────────────────────

This indicator combines multiple trading concepts:

- Opening Range Breakout (ORB) - Customizable time period detection with automatic high/low identification

- Multi-Timeframe Liquidity - HTF (Higher Timeframe) and LTF (Lower Timeframe) key level detection

- Trading Sessions - Tokyo, London, New York, and Sydney session visualization

- Volume Analysis - Volume spike detection and strength measurement

- Multi-Timeframe Confirmation - Trend bias from higher timeframes

- EMA Integration - Trend filter and dynamic support/resistance

- Smart Alerts - Quality-filtered breakout notifications

───────────────────────────────────────

HOW IT WORKS

───────────────────────────────────────

OPENING RANGE BREAKOUT (ORB):

Concept:

The Opening Range is a period at the start of a trading session where price establishes an initial high and low. Breakouts beyond this range often indicate the direction of the day's trend.

Detection Method:

- Default: 15-minute opening range (configurable)

- Custom Range: Set specific session times with timezone support

- Automatically identifies ORH (Opening Range High) and ORL (Opening Range Low)

- Tracks ORB mid-point for reference

Range Establishment:

1. Session starts (or custom time begins)

2. Tracks highest high and lowest low during the period

3. Range confirmed at end of opening period

4. Levels extend throughout the session

Breakout Detection:

- Bullish Breakout: Close above ORH

- Bearish Breakout: Close below ORL

- Mid-point acts as bias indicator

Visual Display:

- Shaded box during range formation

- Horizontal lines for ORH, ORL, and mid-point

- Labels showing level values

- Color-coded fills based on selected method

Fill Color Methods:

1. Session Comparison:

- Green: Current OR mid > Previous OR mid

- Red: Current OR mid < Previous OR mid

- Gray: Equal or first session

- Shows day-over-day momentum

2. Breakout Direction (Recommended):

- Green: Price currently above ORH (bullish breakout)

- Red: Price currently below ORL (bearish breakout)

- Gray: Price inside range (no breakout)

- Real-time breakout status

MULTI-TIMEFRAME LIQUIDITY:

Two-Tier System for comprehensive level identification:

HTF (Higher Timeframe) Key Liquidity:

- Default: 4H timeframe (configurable to Daily, Weekly)

- Identifies major institutional levels

- Uses pivot detection with adjustable parameters

- Suitable for swing highs/lows where large orders rest

LTF (Lower Timeframe) Key Liquidity:

- Default: 1H timeframe (configurable)

- Provides precision entry/exit levels

- Finer granularity for intraday trading

- Captures minor swing points

Calculation Method:

- Pivot high/low detection algorithm

- Configurable left bars (lookback) and right bars (confirmation)

- Timeframe multiplier for accurate multi-timeframe detection

- Automatic level extension

Mitigation System:

- Tracks when levels are swept (broken)

- Configurable mitigation type: Wick or Close-based

- Option to remove or show mitigated levels

- Display limit prevents chart clutter

Asset-Specific Optimization:

The indicator includes quick reference settings for different assets:

- Major Forex (EUR/USD, GBP/USD): Default settings optimal

- Crypto (BTC/ETH): Left=12, Right=4, Display=7

- Gold: HTF=1D, Left=20

TRADING SESSIONS:

Four Major Sessions with Full Customization:

Tokyo Session:

- Default: 04:00-13:00 UTC+4

- Asian trading hours

- Often sets daily range

London Session:

- Default: 11:00-20:00 UTC+4

- Highest liquidity period

- Major institutional activity

New York Session:

- Default: 16:00-01:00 UTC+4

- US market hours

- High-impact news events

Sydney Session:

- Default: 01:00-10:00 UTC+4

- Earliest Asian activity

- Lower volatility

Session Features:

- Shaded background boxes

- Session name labels

- Optional open/close lines

- Session high/low tracking with colored lines

- Each session has independent color settings

- Fully customizable times and timezones

VOLUME ANALYSIS:

Volume-Based Trade Confirmation:

Volume MA:

- Configurable period (default: 20)

- Establishes average volume baseline

- Used for spike detection

Volume Spike Detection:

- Identifies when volume exceeds MA * multiplier

- Default: 1.5x average volume

- Confirms breakout strength

Volume Strength Measurement:

- Calculates current volume as percentage of average

- Shows relative volume intensity

- Used in alert quality filtering

High Volume Bars:

- Identifies bars above 50th percentile

- Additional confirmation layer

- Indicates institutional participation

MULTI-TIMEFRAME CONFIRMATION:

Trend Bias from Higher Timeframes:

HTF 1 (Trend):

- Default: 1H timeframe

- Uses EMA to determine intermediate trend

- Compares current timeframe EMA to HTF EMA

HTF 2 (Bias):

- Default: 4H timeframe

- Uses 50 EMA for longer-term bias

- Confirms overall market direction

Bias Classifications:

- Bullish Bias: HTF close > HTF 50 EMA AND Current EMA > HTF1 EMA

- Bearish Bias: HTF close < HTF 50 EMA AND Current EMA < HTF1 EMA

- Neutral Bias: Mixed signals between timeframes

EMA Stack Analysis:

- Compares EMA alignment across timeframes

- +1: Bullish stack (lower TF EMA > higher TF EMA)

- -1: Bearish stack (lower TF EMA < higher TF EMA)

- 0: Neutral/crossed

Usage:

- Filters false breakouts

- Confirms trend direction

- Improves trade quality

EMA INTEGRATION:

Dynamic EMA for Trend Reference:

Features:

- Configurable period (default: 20)

- Customizable color and width

- Acts as dynamic support/resistance

- Trend filter for ORB trades

Application:

- Above EMA: Favor long breakouts

- Below EMA: Favor short breakouts

- EMA cross: Potential trend change

- Distance from EMA: Momentum gauge

SMART ALERT SYSTEM:

Quality-Filtered Breakout Notifications:

Alert Types:

1. Standard ORB Breakout

2. High Quality ORB Breakout

Quality Criteria:

- Volume Confirmation: Volume > 1.2x average

- MTF Confirmation: Bias aligned with breakout direction

Standard Alert:

- Basic breakout detection

- Price crosses ORH or ORL

- Icon: 🚀 (bullish) or 🔻 (bearish)

High Quality Alert:

- Both volume AND MTF confirmed

- Stronger probability setup

- Icon: 🚀⭐ (bullish) or 🔻⭐ (bearish)

Alert Information Includes:

- Alert quality rating

- Breakout level and current price

- Volume strength percentage (if enabled)

- MTF bias status (if enabled)

- Recommended action

One Alert Per Bar:

- Prevents alert spam

- Uses flag system to track sent alerts

- Resets on new ORB session

───────────────────────────────────────

HOW TO USE

───────────────────────────────────────

OPENING RANGE SETUP:

Basic Configuration:

1. Select time period for opening range (default: 15 minutes)

2. Choose fill color method (Breakout Direction recommended)

3. Enable historical data display if needed

Custom Range (Advanced):

1. Enable Custom Range toggle

2. Set specific session time (e.g., 0930-0945)

3. Select appropriate timezone

4. Useful for specific market opens (NYSE, LSE, etc.)

LIQUIDITY LEVELS SETUP:

Quick Configuration by Asset:

- Forex: Use default settings (Left=15, Right=5)

- Crypto: Set Left=12, Right=4, Display=7

- Gold: Set HTF=1D, Left=20

HTF Liquidity:

- Purpose: Major support/resistance levels

- Recommended: 4H for day trading, 1D for swing trading

- Use as profit targets or reversal zones

LTF Liquidity:

- Purpose: Entry/exit refinement

- Recommended: 1H for day trading, 4H for swing trading

- Use for position management

Mitigation Settings:

- Wick-based: More sensitive (default)

- Close-based: More conservative

- Remove or Show mitigated levels based on preference

TRADING SESSIONS SETUP:

Enable/Disable Sessions:

- Master toggle for all sessions

- Individual session controls

- Show/hide session names

Session High/Low Lines:

- Enable to see session extremes

- Each session has custom colors

- Useful for range trading

Customization:

- Adjust session times for your broker

- Set timezone to match your location

- Customize colors for visibility

VOLUME ANALYSIS SETUP:

Enable Volume Analysis:

1. Toggle on Volume Analysis

2. Set MA length (20 recommended)

3. Adjust spike multiplier (1.5 typical)

Usage:

- Confirm breakouts with volume

- Identify climactic moves

- Filter false signals

MULTI-TIMEFRAME SETUP:

HTF Selection:

- HTF 1 (Trend): 1H for day trading, 4H for swing

- HTF 2 (Bias): 4H for day trading, 1D for swing

Interpretation:

- Trade only with bias alignment

- Neutral bias: Be cautious

- Bias changes: Potential reversals

EMA SETUP:

Configuration:

- Period: 20 for responsive, 50 for smoother

- Color: Choose contrasting color

- Width: 1-2 for visibility

Usage:

- Filter trades: Long above, Short below

- Dynamic support/resistance reference

- Trend confirmation

ALERT SETUP:

TradingView Alert Creation:

1. Enable alerts in indicator settings

2. Enable ORB Breakout Alerts

3. Right-click chart → Add Alert

4. Select this indicator

5. Choose "Any alert() function call"

6. Configure delivery method (mobile, email, webhook)

Alert Filtering:

- All alerts include quality rating

- High Quality alerts = Volume + MTF confirmed

- Standard alerts = Basic breakout only

───────────────────────────────────────

TRADING STRATEGIES

───────────────────────────────────────

CLASSIC ORB STRATEGY:

Setup:

1. Wait for opening range to complete

2. Price breaks and closes above ORH or below ORL

3. Volume > average (if enabled)

4. MTF bias aligned (if enabled)

Entry:

- Bullish: Buy on break above ORH

- Bearish: Sell on break below ORL

- Consider retest entries for better risk/reward

Stop Loss:

- Bullish: Below ORL or range mid-point

- Bearish: Above ORH or range mid-point

- Adjust based on volatility

Targets:

- Initial: Range width extension (ORH + range width)

- Secondary: HTF liquidity levels

- Final: Session high/low or major support/resistance

ORB + LIQUIDITY CONFLUENCE:

Enhanced Setup:

1. Opening range established

2. HTF liquidity level near or beyond ORH/ORL

3. Breakout occurs with volume

4. Price targets the liquidity level

Entry:

- Enter on ORB breakout

- Target the HTF liquidity level

- Use LTF liquidity for position management

Management:

- Partial profits at ORB + range width

- Move stop to breakeven at LTF liquidity

- Final exit at HTF liquidity sweep

ORB REJECTION STRATEGY (Counter-Trend):

Setup:

1. Price breaks above ORH or below ORL

2. Weak volume (below average)

3. MTF bias opposite to breakout

4. Price closes back inside range

Entry:

- Failed bullish break: Short below ORH

- Failed bearish break: Long above ORL

Stop Loss:

- Beyond the failed breakout level

- Or beyond session extreme

Target:

- Opposite end of opening range

- Range mid-point for partial profit

SESSION-BASED ORB TRADING:

Tokyo Session:

- Typically narrower ranges

- Good for range trading

- Wait for London open breakout

London Session:

- Highest volume and volatility

- Strong ORB setups

- Major liquidity sweeps common

New York Session:

- Strong trending moves

- News-driven volatility

- Good for momentum trades

Sydney Session:

- Quieter conditions

- Suitable for range strategies

- Sets up Tokyo session

EMA-FILTERED ORB:

Rules:

- Only take bullish breaks if price > EMA

- Only take bearish breaks if price < EMA

- Ignore counter-trend breaks

Benefits:

- Reduces false signals

- Aligns with larger trend

- Improves win rate

───────────────────────────────────────

CONFIGURATION GUIDE

───────────────────────────────────────

OPENING RANGE SETTINGS:

Time Period:

- 15 min: Standard for most markets

- 30 min: Wider range, fewer breakouts

- 60 min: For slower markets or swing trades

Custom Range:

- Use for specific market opens

- NYSE: 0930-1000 EST

- LSE: 0800-0830 GMT

- Set timezone to match exchange

Historical Display:

- Enable: See all previous session data

- Disable: Cleaner chart, current session only

LIQUIDITY SETTINGS:

Left Bars (5-30):

- Lower: More frequent, sensitive levels

- Higher: Fewer, more significant levels

- Recommended: 15 for most markets

Right Bars (1-25):

- Confirmation period

- Higher: More reliable, less frequent

- Recommended: 5 for balance

Display Limit (1-20):

- Number of active levels shown

- Higher: More context, busier chart

- Recommended: 7 for clarity

Extension Options:

- Short: Levels visible near formation

- Current: Extended to current bar (recommended)

- Max: Extended indefinitely

VOLUME SETTINGS:

MA Length (5-50):

- Shorter: More responsive to spikes

- Longer: Smoother baseline

- Recommended: 20 for balance

Spike Multiplier (1.0-3.0):

- Lower: More sensitive spike detection

- Higher: Only extreme spikes

- Recommended: 1.5 for day trading

MULTI-TIMEFRAME SETTINGS:

HTF 1 (Trend):

- 5m chart: Use 15m or 1H

- 15m chart: Use 1H or 4H

- 1H chart: Use 4H or 1D

HTF 2 (Bias):

- One level higher than HTF 1

- Provides longer-term context

- Don't use same as HTF 1

EMA SETTINGS:

Length:

- 20: Responsive, more signals

- 50: Smoother, stronger filter

- 200: Long-term trend only

Style:

- Choose contrasting color

- Width 1-2 for visibility

- Match your trading style

───────────────────────────────────────

BEST PRACTICES

───────────────────────────────────────

Chart Timeframe Selection:

- ORB Trading: Use 5m or 15m charts

- Session Review: Use 1H or 4H charts

- Swing Trading: Use 1H or 4H charts

Quality Over Quantity:

- Wait for high-quality alerts (volume + MTF)

- Avoid trading every breakout

- Focus on confluence setups

Risk Management:

- Position size based on range width

- Wider ranges = smaller positions

- Use stop losses always

- Take partial profits at targets

Market Conditions:

- Best results in trending markets

- Reduce position size in choppy conditions

- Consider session overlaps for volatility

- Avoid trading near major news if inexperienced

Continuous Improvement:

- Track win rate by session

- Note which confluence factors work best

- Adjust settings based on market volatility

- Review performance weekly

───────────────────────────────────────

PERFORMANCE OPTIMIZATION

───────────────────────────────────────

This indicator is optimized with:

- max_bars_back declarations for efficient processing

- Conditional calculations based on enabled features

- Proper memory management for drawing objects

- Minimal recalculation on each bar

Best Practices:

- Disable unused features (sessions, MTF, volume)

- Limit historical display to reduce rendering

- Use appropriate timeframe for your strategy

- Clear old drawing objects periodically

───────────────────────────────────────

EDUCATIONAL DISCLAIMER

───────────────────────────────────────

This indicator combines established trading concepts:

- Opening Range Breakout theory (price action)

- Liquidity level detection (pivot analysis)

- Session-based trading (time-of-day patterns)

- Volume analysis (confirmation technique)

- Multi-timeframe analysis (trend alignment)

All calculations use standard technical analysis methods:

- Pivot high/low detection algorithms

- Moving averages for trend and volume

- Session time filtering

- Timeframe security functions

The indicator identifies potential trading setups but does not predict future price movements. Success requires proper application within a complete trading strategy including risk management, position sizing, and market context.

───────────────────────────────────────

USAGE DISCLAIMER

───────────────────────────────────────

This tool is for educational and analytical purposes. Opening Range Breakout trading involves substantial risk. The alert system and quality filters are designed to identify potential setups but do not guarantee profitability. Always conduct independent analysis, use proper risk management, and never risk capital you cannot afford to lose. Past performance does not indicate future results. Trading intraday breakouts requires experience and discipline.

───────────────────────────────────────

CREDITS & ATTRIBUTION

───────────────────────────────────────

ORIGINAL SOURCE:

This indicator builds upon concepts from LuxAlgo's-ORB

4H Candle Curves4H Candle Curves - Detailed User Guide

OVERVIEW

This indicator reveals curve vs continuation behavior in NQ Futures by analyzing how price responds after breaking the first-hour range. Based on 10+ years of statistical analysis (2013-2025, 3,136+ trading days), it identifies which 4-hour sessions exhibit mean reversion (curve) behavior versus trend continuation when Q2 (second hour) breaks Q1 (first hour) extremes.

⚠️ IMPORTANT: This indicator is specifically designed for NQ FUTURES ONLY. All curve probabilities and statistics were derived from a decade-long dataset of NQ 1-minute bars. Using this on other instruments will produce inaccurate results.

CORE CONCEPT: THE CURVE

What is a "Curve"?

A curve occurs when price breaks out of the first hour's range in Q2 (hour 2), but then reverses direction in the second half (Q3+Q4) to make a new extreme on the opposite side.

Curve Example (Upside Break → Downside Reversal):

Q1 (Hour 1): Price establishes range 25,000 - 25,050

Q2 (Hour 2): Price breaks ABOVE Q1 high, reaches 25,100

Q3+Q4 (Hours 3-4): Price curves back down, makes new LOW below 25,000

Result: Q2 broke high, but second half curved back to make new low below Q1 = CURVE

What is "Continuation"?

Continuation occurs when Q2 breaks Q1 range and the second half extends further in the same direction.

Continuation Example (Upside Break → Further Upside):

Q1 (Hour 1): Price establishes range 25,000 - 25,050

Q2 (Hour 2): Price breaks ABOVE Q1 high, reaches 25,100

Q3+Q4 (Hours 3-4): Price continues higher, makes new HIGH above 25,100

Result: Q2 broke high, second half made new high above Q2 = CONTINUATION

THE CRITICAL DISCOVERY: 6AM IS THE CURVE SESSION

Curve Probabilities by Session:

When Q2 Breaks Q1 HIGH:

6AM: 60.6% curve (new low below Q1) | 38.5% continuation

2AM: 38.4% curve | 46.7% continuation (balanced)

10AM: 17.2% curve | 60.4% continuation ← STRONG continuation bias

6PM: 29.6% curve | 59.0% continuation

10PM: 27.5% curve | 55.1% continuation

When Q2 Breaks Q1 LOW:

6AM: 64.4% curve (new high above Q1) | 35.0% continuation ← HIGHEST curve

2AM: 42.8% curve | 43.3% continuation (balanced)

10AM: 16.7% curve | 51.6% continuation ← STRONG continuation bias

6PM: 33.7% curve | 51.1% continuation

10PM: 33.1% curve | 48.6% continuation

Key Insight:

6AM is THE ONLY SESSION with >60% curve probability in both directions. This makes it a uniquely exploitable mean reversion session. When Q2 breaks Q1 range during 6AM, expect the second half to curve back 60-64% of the time.

10AM shows the opposite: Strong continuation bias (60% when Q2 breaks high, 52% when Q2 breaks low). 10AM breakouts tend to follow through.

HOW IT WORKS: THE QUARTER SYSTEM

The Six 4-Hour Candles (EST):

Each trading day (6pm-5pm) is divided into six 4-hour periods:

6PM (18:00-22:00) - Evening/Globex open | Blue box

10PM (22:00-02:00) - Asia session | Purple box

2AM (02:00-06:00) - Early London | Orange box

6AM (06:00-10:00) - Late London + NY Open | Green box ← THE CURVE SESSION

10AM (10:00-14:00) - NY Morning | Red box ← THE CONTINUATION SESSION

2PM (14:00-17:00) - NY Afternoon | Yellow box (3 hours only)

The Four Quarters:

Each 4-hour candle (except 2PM) is divided into four 1-hour quarters:

Q1 (Hour 1, minutes 0-60): Establishes initial range

Q2 (Hour 2, minutes 60-120): Tests Q1 range - breaks or holds?

Q3 (Hour 3, minutes 120-180): Second half begins

Q4 (Hour 4, minutes 180-240): Second half completes

2PM candle only has 3 hours (14:00-17:00), so quarters are adjusted accordingly.

The Three-Step Analysis:

STEP 1: Q1 Establishes Range

The first hour sets the high and low for the session. This becomes the reference range.

STEP 2: Q2 Break Detection

The indicator monitors whether Q2 (hour 2) breaks above Q1 high or below Q1 low.

STEP 3: Second Half Response

Once Q2 breaks Q1 range, the indicator tracks what happens in Q3+Q4:

Does price CURVE back to make new extreme on opposite side?

Does price CONTINUE to make new extreme in same direction?

Or does price stay within the established range?

VISUAL ELEMENTS EXPLAINED

1. 4-Hour Candle Boxes

Colored boxes display the high-to-low range of each 4H candle:

Blue = 6PM (evening session start)

Purple = 10PM (Asia session)

Orange = 2AM (early London)

Green = 6AM ← THE CURVE SESSION (watch for mean reversion)

Red = 10AM ← THE CONTINUATION SESSION (trend follow-through)

Yellow = 2PM (afternoon close, 3 hours only)

2. Quarter Separator Lines

Vertical dotted lines mark the boundaries between quarters (1H, 2H, 3H marks). This helps you see:

When Q1 ends (after 1 hour)

When Q2 ends / second half begins (after 2 hours)

When Q3 ends (after 3 hours)

3. Candle Name Labels

At the 2-hour mark (Q2/Q3 boundary), a label shows:

Candle name (e.g., "6am")

Directional indicator:

🔼 = Q2 broke Q1 HIGH

🔽 = Q2 broke Q1 LOW

⚠️ = Q2 broke BOTH Q1 high and low (extended range)

No symbol = Q2 stayed within Q1 range

THE LIVE STATUS TABLE

Located in your chosen corner (default: bottom-right), this table shows real-time analysis of the current 4H candle.

Header Row:

"LIVE: CANDLE" - Shows which 4H session you're currently in

Quarter Row:

"Quarter: Q1/Q2/Q3/Q4 (Hour X)" - Shows which quarter you're currently forming

STATUS Section:

The status updates dynamically based on what has happened:

During Q1-Q2 (First Half):

"⏳ Q1 Building..." - First hour forming, range being established

"⏳ Q2 Building..." - Second hour in progress, Q2 within Q1 range so far

"🔼 Q2 Broke Q1 HIGH" - Q2 has broken above Q1 high

"🔽 Q2 Broke Q1 LOW" - Q2 has broken below Q1 low

"⚠️ Q2 Broke BOTH Q1 Extremes" - Q2 extended range in both directions

During Q3-Q4 (Second Half):

"✓ CURVE CONFIRMED" - Q2 broke one direction, second half reversed to opposite side

"✓ CONTINUATION CONFIRMED" - Q2 broke one direction, second half extended further same direction

"⏳ 2nd Half In Progress" - Q2 broke Q1, waiting to see if curve or continuation

"📊 No Q2 Break Occurred" - Q2 stayed within Q1 range (no curve/continuation setup)

EXPECTATION Section:

Shows the probabilities based on the current state:

When Q2 breaks Q1 high in 6AM:

EXPECT 2nd half:

CURVE (low < Q1): 60.6%

CONT (high > Q2): 38.5%

This tells you there's a 60.6% chance the second half will curve back to make a new low below Q1, versus 38.5% chance it continues higher above Q2.

When curve/continuation is confirmed:

Q2 broke high → 2nd half made new LOW below Q1

Curve: 60.6%

Shows what actually happened and the historical probability.

Color Coding:

Purple background = Curve confirmed (mean reversion occurred)

Green background = Continuation confirmed (upside extension)

Red background = Continuation confirmed (downside extension)

Blue background = Second half in progress, watching

Yellow background = No Q2 break (no setup)

Gray background = Still in first half, building

THE CURVE REFERENCE TABLE

Located in your chosen corner (default: bottom-left), this table provides a quick reference for all sessions.

Table Structure:

TOP SECTION: "When Q2 BREAKS Q1 HIGH"

BOTTOM SECTION: "When Q2 BREAKS Q1 LOW"

How to Read:

"Curve" column = % of time second half makes new extreme on OPPOSITE side

"Cont" column = % of time second half makes new extreme in SAME direction

"Winner" column = Which behavior is more likely

Purple highlight = Curve is the winner (higher %)

Blue highlight = Continuation is the winner

🔥 symbol = Strong edge (>60%)

Quick Reference Usage:

You're in 10AM session, Q2 just broke Q1 high. Look at top section, 10AM row:

Curve: 17.2%

Cont: 60.4%

Winner: CONT

Interpretation: 10AM breakouts tend to follow through. Only 17% chance of curving back. Trade with the break, not against it.

PRACTICAL TRADING EXAMPLES

Example 1: Perfect 6AM Curve Setup

Scenario:

6AM candle in progress

7:00 AM: Q1 ends, range is 18,000 - 18,050

7:30 AM: Price breaks above 18,050, reaches 18,075 (Q2 broke Q1 high)

Live table shows: "🔼 Q2 Broke Q1 HIGH"

Expectation: "CURVE (low < Q1): 60.6%"

Trading Decision:

Even though price broke to new highs, the 60.6% curve probability suggests looking for short opportunities expecting price to curve back below 18,000 in Q3-Q4.

Typical Outcome:

8:15 AM (Q3): Price starts declining

9:15 AM (Q4): Price makes new low at 17,990

Result: ✓ CURVE CONFIRMED

Example 2: 10AM Continuation Signal

Scenario:

10AM candle in progress

11:00 AM: Q1 ends, range is 18,100 - 18,150

11:45 AM: Price breaks above 18,150, reaches 18,180 (Q2 broke Q1 high)

Live table shows: "🔼 Q2 Broke Q1 HIGH"

Expectation: "CONT (high > Q2): 60.4%"

Trading Decision:

With 60.4% continuation probability, breakout likely to follow through. Look for long opportunities expecting extension above 18,180 in Q3-Q4.

Typical Outcome:

12:30 PM (Q3): Price continues higher to 18,200

1:15 PM (Q4): Price makes new high at 18,225

Result: ✓ CONTINUATION CONFIRMED

Example 3: Using Reference Table During Live Trading

You see Q2 breaking Q1 low during 2AM session:

Quick reference check:

2AM row, "When Q2 BREAKS Q1 LOW" section

Curve: 42.8% | Cont: 43.3% | Winner: Balanced

Interpretation: This is a coin flip - 2AM session is balanced when Q2 breaks low. Don't force a directional bias. Wait for second half price action confirmation or skip the setup.

Example 4: No Setup Scenario

Scenario:

6AM candle, Q2 ends at 8:00 AM

Q2 stayed within Q1 range (no break above or below)

Live table shows: "📊 No Q2 Break Occurred"

Trading Decision:

No curve/continuation setup exists. This analysis only applies when Q2 breaks Q1 range. Monitor for different strategies or wait for next 4H candle.

UNDERSTANDING THE UNDERLYING METHODOLOGY

Data Foundation:

Instrument: NQ Futures (E-mini NASDAQ-100)

Timeframe: 1-minute bars for precise quarter tracking

Period: January 2013 - December 2025

Sample: 3,136+ complete trading days

Total 4H Candles Analyzed: ~18,800+ individual sessions

Analysis Process:

For each 4H candle in the dataset:

Calculate Q1 high and low (first hour range)

Track whether Q2 breaks Q1 high, Q1 low, both, or neither

When Q2 breaks Q1 range, measure second half response:

Did Q3+Q4 make new low below Q1? (curve when Q2 broke high)

Did Q3+Q4 make new high above Q1? (curve when Q2 broke low)

Did Q3+Q4 make new high above Q2? (continuation when Q2 broke high)

Did Q3+Q4 make new low below Q2? (continuation when Q2 broke low)

Calculate percentages for each session

Why NQ-Specific?

Different futures contracts exhibit different intraday personality:

NQ (NASDAQ):

Tech-heavy, volatility-prone

6AM shows extreme curve behavior (60-64%) due to NY Open reversal tendency

10AM shows strong continuation (60%) as trends establish

ES (S&P 500) would show different probabilities because:

Lower volatility than NQ

Different institutional participation patterns

Different response to macro events

The indicator's probabilities are calibrated specifically to NQ behavior patterns. Using it on ES, RTY, or other instruments will produce misleading signals.

ORIGINALITY & INNOVATION

What Makes This Indicator Unique:

Quarter-Based Curve Analysis: Unlike traditional indicators that only identify breakouts, this tracks what happens after the breakout. The curve vs continuation framework is novel and provides directional edge.

Session-Specific Behavior: Recognizes that 6AM behaves fundamentally differently than 10AM. Most indicators apply the same logic across all sessions. This indicator provides session-specific probabilities.

Statistical Validation: Every probability shown is backed by 10+ years of data (2,900+ candles per session). Not based on theory or discretionary observation.

Real-Time Quarter Tracking: Precisely identifies which quarter you're in and what stage of the pattern is forming. Provides forward-looking probabilities based on current state.

The 6AM Discovery: The 60-64% curve probability in 6AM is a quantified, repeatable edge that contradicts traditional "breakout = continuation" assumptions. This session exhibits mean reversion characteristics that most traders miss.

Dual-Direction Analysis: Tracks both upside breaks (Q2 > Q1 high) and downside breaks (Q2 < Q1 low) separately, as they can have different probabilities.

Visual Quarter System: The combination of colored boxes, quarter separators, and real-time labels provides instant visual understanding of pattern stage and expected behavior.

HOW TO USE THIS INDICATOR

Step 1: Identify Current 4H Candle

Check which colored box you're in and what session it represents.

Step 2: Wait for Q2 to Complete

The setup doesn't exist until Q2 (hour 2) breaks Q1 range. Monitor the live table.

Step 3: Check Q2 Break Status

Did Q2 break Q1 high? Q1 low? Both? Or neither?

Step 4: Consult Reference Table

Look up current session in curve reference table. What's the probability?

Step 5: Apply Session-Specific Strategy

For 6AM (60-64% curve):

Q2 breaks high → Expect curve back for new low

Q2 breaks low → Expect curve back for new high

Strategy: FADE the Q2 break, look for reversal entries in Q3-Q4

For 10AM (52-60% continuation):

Q2 breaks high → Expect continuation higher

Q2 breaks low → Expect continuation lower

Strategy: TRADE WITH the Q2 break, look for continuation entries in Q3-Q4

For 2AM (38-43% curve, 43-47% continuation):

Balanced probabilities

Strategy: Wait for Q3 price action to confirm direction, or skip

For 6PM/10PM (50-59% continuation):

Moderate continuation bias

Strategy: Lean with the break but use tight stops

Step 6: Monitor Live Status

Watch the live table for confirmation:

"✓ CURVE CONFIRMED" = Mean reversion occurred

"✓ CONTINUATION CONFIRMED" = Follow-through occurred

"⏳ 2nd Half In Progress" = Still developing

BEST PRACTICES

Focus on 6AM for curve trades - This is THE high-probability mean reversion session

Focus on 10AM for continuation trades - This is THE high-probability breakout session

Be cautious with 2AM - Balanced probabilities mean lower edge

Use quarter separators - Enter trades early in Q3 after Q2 break, don't wait for Q4

Combine with price action - Don't blindly fade 6AM or follow 10AM; wait for confirming price structure

Respect the 60% rule - 6AM curve happens 60% of time, which means 40% it doesn't. Manage risk accordingly

Watch for "No Q2 Break" - If Q2 doesn't break Q1, this analysis doesn't apply

Consider overnight context - If 6AM opens with huge gap, curve probability may be affected

SETTINGS & CUSTOMIZATION

Display Settings:

Show 4H Candle Boxes - Toggle colored range boxes

Box Colors - Customize color for each session

Show Quarter Separators - Show/hide 1H, 2H, 3H lines

Show Candle Name Labels - Show/hide session labels at 2H mark

Separator Line Style - Solid/Dashed/Dotted

Max Historical Candles - How many past 4H candles to display (1-50)

Table Settings:

Show Live Status Table - Toggle real-time analysis table

Show Curve Reference Table - Toggle probability reference table

Table Positions - Place tables in any corner

Table Text Size - Tiny/Small/Normal

LIMITATIONS & DISCLAIMERS

NQ FUTURES ONLY - All probabilities are NQ-specific, do not use on other instruments

Requires Q2 break - No curve/continuation setup exists if Q2 stays within Q1 range

Probabilities, not certainties - 60% means it happens 6 out of 10 times, not every time

Lower timeframe noise - 1-minute tracking can be choppy, consider using 5min+ for entries

Gap days - Large overnight gaps may affect curve/continuation probabilities

Not standalone - Use as confluence with your strategy, not as sole decision factor

Historical performance - Past statistics don't guarantee future results

WHY THE CURVE CONCEPT MATTERS

Traditional trading wisdom says: "Breakout = Continuation"

This indicator proves that's not always true. Specifically, during the 6AM session (late London + NY Open), when Q2 breaks the Q1 range, price curves back to the opposite extreme 60-64% of the time.

This creates a unique exploitable edge:

Most breakout traders go LONG when Q2 breaks Q1 high

But in 6AM, 60.6% of the time, price curves back down for new low

Shorting the breakout (counter-intuitive) is the higher-probability trade

The 10AM session shows the opposite:

Breakouts in 10AM tend to follow through (52-60%)

Traditional "trade the breakout" strategy works better here

By knowing which session you're in, you can adapt your strategy to match the session's personality.

FINAL NOTES

This indicator distills 10+ years of NQ intraday behavior into actionable, session-specific probabilities. The discovery that 6AM exhibits 60-64% curve behavior while 10AM exhibits 52-60% continuation behavior provides a statistical edge for mean reversion and trend-following traders respectively.

The highest-probability setups:

6AM Q2 break → FADE (60-64% edge for curve)

10AM Q2 break → FOLLOW (52-60% edge for continuation)

2AM = SKIP (balanced probabilities, no clear edge)

Master the 6AM curve and 10AM continuation first. These two sessions provide the clearest statistical edges.

Remember: Trade with proper risk management. This tool provides probabilities based on historical behavior, not predictions of future performance.

CANDLE RANGE THEORY (H1 Only)Hello traders.

This indicator identifies CRT candles

-Each candle is a range.

-Each candle has its own po3.

-Focus on specific times of the day. By recognizing the importance of time and price, we can capture high-quality trades. Together with HTF PD array, Look for 4-hour candles forming at specific times of the day. (1am - 5am - 9am EST)

-After the 1st candle, wait for the 2nd candle to clear the high/low of the 1st candle and then close inside the 1st candle range at a specific time (1-5-9) and look for entries in the LTF

Why choose 1 5 9 hours EST?

### **1. 1:00 AM (EST)**

- **Trading Session:** This is the time between the Tokyo (Asian) session and the Sydney (Australian) session. The Asian market is very active.

- **Characteristics:**

- Liquidity: Moderate, as only the Asian market is active.

- Volatility: Pairs involving JPY (Japanese Yen), AUD (Australian Dollar), and NZD (New Zealand Dollar) tend to have higher volatility.

- Trading Opportunities: Suitable for traders who like to trade trends or news in the Asian region.

- **Note:** Volatility may be lower than the London or New York session.

### **2. 5:00 AM (EST)**

- **Trading Session:** This is the time near the end of the Tokyo session and the London (European) session is about to open.

- **Characteristics:**

- Liquidity: Starts to increase due to the preparation of the European market.

- Volatility: This is the time between two trading sessions, there can be strong fluctuations, especially in major currency pairs such as EUR/USD, GBP/USD.

- Trading opportunities: Suitable for breakout trading strategies when liquidity increases.

- **Note:** The overlap between Tokyo and London can cause sudden fluctuations.

### **3. 9:00 AM (EST)**

- **Trading sessions:** This time is within the London session and near the beginning of the New York session.

- **Characteristics:**

- Liquidity: Very high, as this is the period between the two largest sessions – London and New York.

- Volatility: Extremely strong, especially for major currency pairs such as EUR/USD, GBP/USD, USD/JPY.

- Trading opportunities: Suitable for both news trading and trend trading, as this is the time when a lot of economic data is released (usually from the US or the European region).

- **Note:** High volatility can bring big profits, but also comes with high risks.

### **Summary of effects:**

- **1 AM (EST):** Moderate volatility, focusing on Asian currency pairs.

- **5 AM (EST):** Increased liquidity and volatility, suitable for breakout trading.

- **9 AM (EST):** High volatility and high liquidity, the best time for Forex trading.

==> How to trade, when the high/low of CRT is swept, move to LTF to wait for confirmation to enter the order

Only sell at high level and buy at discount price.

Find CE at specific important time. Trading CRT with HTF direction has better win rate.

The more inside bars, the higher the probability.

Place a partial and Move breakeven at 50% range.

Do a backtest and post your chart.

High Low Levels by JZCustom High Low Levels Indicator - features

Clearly plotted high and low levels for specific trading sessions. This indicator provides visual representations of key price levels during various trading periods. Below are the main features and benefits of this indicator:

1. Display high and low levels for each session

- previous day high/low: display the high and low from the previous day, giving you a better understanding of how the price moves compared to the prior day.

- asia, london, and custom sessions: track the high and low levels for the major trading sessions (asian and london) and two custom user-defined sessions.

2. Complete line and label customization

- custom line appearance: choose the color, line style (solid, dashed, dotted), and line thickness for each trading session. you can also decide if the lines should extend beyond the current price action.

- custom labels: define your own label texts for each custom session. this way, you can label the levels precisely and easily track price movements.

3. Define your own trading sessions

- add up to two custom sessions (custom and custom 2), which can be defined using precise start and end times (hour and minute).

- each custom session allows you to specify the label text for the high and low levels, enabling you to easily differentiate different parts of the day on the chart.

4. Clear and intuitive design

- grouped settings: all settings are grouped based on trading sessions, so you can easily customize every aspect of the visual representation.

- simple toggle on/off: you can easily enable or disable each line (previous day, asia, london, custom 1, custom 2). this allows you to keep your chart clean and focus only on the important levels you need at any moment.

5. Flexible time zones

- time zone settings: set the time zone (utc, europe/london, america/new_york, asia/tokyo) to properly align the timeframes for each level depending on the market you're focusing on.

6. Automatic cleanup of old lines and labels

- old levels removal: automatically remove old lines and labels to prevent clutter on your chart. this ensures that only current, relevant levels for each trading day or session are displayed.

7. Precise plotting and line extension

- accurate level markings: the indicator calculates the precise times when the high and low levels were reached and plots lines that visually represent these levels.

- line extension options: you have the option to extend the high/low lines beyond their point of calculation, which helps with identifying price action trends beyond the current period.

Dec 7, 2024

Release Notes

Changes and Improvements for Users:

1. Customizable Offset for Lines and Labels:

- A new input, `Line and Label Offset`, allows users to control how far the lines and their associated text labels extend. This ensures the labels and lines remain aligned and can be adjusted as needed.

2. Unified Offset Control:

- The same offset value is applied to all types of lines and labels (e.g., Previous Day High/Low, Asia High/Low, London High/Low, and custom sessions). Users can change this in one place to affect the entire script consistently.

3. Enhanced Flexibility:

- Users now have more control over the appearance and position of their lines and labels, making the indicator adaptable to different chart setups and personal preferences.

These updates aim to enhance user convenience and customization, ensuring a more tailored charting experience.

Monday range by MatboomThe "Monday Range" Pine Script indicator calculates and displays the lowest and highest prices during a specified trading session, focusing on Mondays. Users can configure the trading session parameters, such as start and end times and time zone. The indicator visually highlights the session range on the chart by plotting the session low and high prices and applying a background color within the session period. The customizable days of the week checkboxes allow users to choose which days the indicator should consider for analysis.

Session Configuration:

session = input.session("0000-0000", title="Trading Session")

timeZone = input.string("UTC", title="Time Zone")

monSession = input.bool(true, title="Mon ", group="Trading Session", inline="d1")

tueSession = input.bool(true, title="Tue ", group="Trading Session", inline="d1")

Users can configure the trading session start and end times and the time zone.

Checkboxes for Monday (monSession) and Tuesday (tueSession) sessions are provided.

SessionLow and SessionHigh Functions:

SessionLow(sessionTime, sessionTimeZone=syminfo.timezone) => ...

SessionHigh(sessionTime, sessionTimeZone=syminfo.timezone) => ...

Custom functions to calculate the lowest (SessionLow) and highest (SessionHigh) prices during a specified trading session.

InSession Function:

InSession(sessionTimes, sessionTimeZone=syminfo.timezone) => ...

Determines if the current bar is inside the specified trading session.

Days of Week String and Session String:

sessionDays = ""

if monSession

sessionDays += "2"

if tueSession

sessionDays += "3"

tradingSession = session + ":" + sessionDays

Constructs a string representing the selected days of the week for the session.

Fetch Session Low and High:

sessLow = SessionLow(tradingSession, timeZone)

sessHigh = SessionHigh(tradingSession, timeZone)

Calls the custom functions to obtain the session low and high prices.

Plot Session Low and High and Background Color for Session

plot(sessLow, color=color.red, title="Session Low")

plot(sessHigh, color=color.red, title="Session Low")

bgcolor(InSession(tradingSession, timeZone) ? color.new(color.aqua, 90) : na)

skThis Pine Script is an indicator designed to mark and highlight specific trading sessions on a TradingView chart. Here's a description of the script's functionality:

1. *Session Selection*: The script allows you to select a session time frame using the `session_input` input. The available options for session time frames are "D" (daily), "W" (weekly), "M" (monthly), "H" (hourly), "15" (15 minutes), "5" (5 minutes), and "1" (1 minute).

2. *Session Times*: You can specify the start and end times for three different trading sessions - CBDR (Central Bank Dealer Range), Asia, and London - using the corresponding input options. These times are specified in Indian Standard Time (IST).

3. *Time Calculation*: The script calculates the start and end times for each session based on the specified hours and minutes. It uses the `timestamp` function to create time objects for these sessions.

4. *Session Highlighting*: The script creates rectangles on the chart to highlight each session:

- CBDR Session: A gray rectangle is drawn during the CBDR session time.

- Asia Session: Another gray rectangle is drawn during the Asia session time.

- London Session: A green rectangle is drawn at the top of the chart during the London session time.

5. *Transparency*: The rectangles have a transparency level of 90%, allowing you to see the price data beneath them while still marking the sessions.

6. *Overlay*: The indicator is set to overlay on the price chart, so it doesn't obstruct the price data.

7. *Customization*: You can customize the session times and appearance by adjusting the input values in the settings panel of the indicator.

Overall, this script provides a visual way to identify and highlight specific trading sessions on your TradingView chart, helping traders understand price action in different market sessions.

Adaptive Market Wave TheoryAdaptive Market Wave Theory

🌊 CORE INNOVATION: PROBABILISTIC PHASE DETECTION WITH MULTI-AGENT CONSENSUS

Adaptive Market Wave Theory (AMWT) represents a fundamental paradigm shift in how traders approach market phase identification. Rather than counting waves subjectively or drawing static breakout levels, AMWT treats the market as a hidden state machine —using Hidden Markov Models, multi-agent consensus systems, and reinforcement learning algorithms to quantify what traditional methods leave to interpretation.

The Wave Analysis Problem:

Traditional wave counting methodologies (Elliott Wave, harmonic patterns, ABC corrections) share fatal weaknesses that AMWT directly addresses:

1. Non-Falsifiability : Invalid wave counts can always be "recounted" or "adjusted." If your Wave 3 fails, it becomes "Wave 3 of a larger degree" or "actually Wave C." There's no objective failure condition.

2. Observer Bias : Two expert wave analysts examining the same chart routinely reach different conclusions. This isn't a feature—it's a fundamental methodology flaw.

3. No Confidence Measure : Traditional analysis says "This IS Wave 3." But with what probability? 51%? 95%? The binary nature prevents proper position sizing and risk management.

4. Static Rules : Fixed Fibonacci ratios and wave guidelines cannot adapt to changing market regimes. What worked in 2019 may fail in 2024.

5. No Accountability : Wave methodologies rarely track their own performance. There's no feedback loop to improve.

The AMWT Solution:

AMWT addresses each limitation through rigorous mathematical frameworks borrowed from speech recognition, machine learning, and reinforcement learning:

• Non-Falsifiability → Hard Invalidation : Wave hypotheses die permanently when price violates calculated invalidation levels. No recounting allowed.

• Observer Bias → Multi-Agent Consensus : Three independent analytical agents must agree. Single-methodology bias is eliminated.

• No Confidence → Probabilistic States : Every market state has a calculated probability from Hidden Markov Model inference. "72% probability of impulse state" replaces "This is Wave 3."

• Static Rules → Adaptive Learning : Thompson Sampling multi-armed bandits learn which agents perform best in current conditions. The system adapts in real-time.

• No Accountability → Performance Tracking : Comprehensive statistics track every signal's outcome. The system knows its own performance.

The Core Insight:

"Traditional wave analysis asks 'What count is this?' AMWT asks 'What is the probability we are in an impulsive state, with what confidence, confirmed by how many independent methodologies, and anchored to what liquidity event?'"

🔬 THEORETICAL FOUNDATION: HIDDEN MARKOV MODELS

Why Hidden Markov Models?

Markets exist in hidden states that we cannot directly observe—only their effects on price are visible. When the market is in an "impulse up" state, we see rising prices, expanding volume, and trending indicators. But we don't observe the state itself—we infer it from observables.

This is precisely the problem Hidden Markov Models (HMMs) solve. Originally developed for speech recognition (inferring words from sound waves), HMMs excel at estimating hidden states from noisy observations.

HMM Components:

1. Hidden States (S) : The unobservable market conditions

2. Observations (O) : What we can measure (price, volume, indicators)

3. Transition Matrix (A) : Probability of moving between states

4. Emission Matrix (B) : Probability of observations given each state

5. Initial Distribution (π) : Starting state probabilities

AMWT's Six Market States:

State 0: IMPULSE_UP

• Definition: Strong bullish momentum with high participation

• Observable Signatures: Rising prices, expanding volume, RSI >60, price above upper Bollinger Band, MACD histogram positive and rising

• Typical Duration: 5-20 bars depending on timeframe

• What It Means: Institutional buying pressure, trend acceleration phase

State 1: IMPULSE_DN

• Definition: Strong bearish momentum with high participation

• Observable Signatures: Falling prices, expanding volume, RSI <40, price below lower Bollinger Band, MACD histogram negative and falling

• Typical Duration: 5-20 bars (often shorter than bullish impulses—markets fall faster)

• What It Means: Institutional selling pressure, panic or distribution acceleration

State 2: CORRECTION

• Definition: Counter-trend consolidation with declining momentum

• Observable Signatures: Sideways or mild counter-trend movement, contracting volume, RSI returning toward 50, Bollinger Bands narrowing

• Typical Duration: 8-30 bars

• What It Means: Profit-taking, digestion of prior move, potential accumulation for next leg

State 3: ACCUMULATION

• Definition: Base-building near lows where informed participants absorb supply

• Observable Signatures: Price near recent lows but not making new lows, volume spikes on up bars, RSI showing positive divergence, tight range

• Typical Duration: 15-50 bars

• What It Means: Smart money buying from weak hands, preparing for markup phase

State 4: DISTRIBUTION

• Definition: Top-forming near highs where informed participants distribute holdings

• Observable Signatures: Price near recent highs but struggling to advance, volume spikes on down bars, RSI showing negative divergence, widening range

• Typical Duration: 15-50 bars

• What It Means: Smart money selling to late buyers, preparing for markdown phase

State 5: TRANSITION

• Definition: Regime change period with mixed signals and elevated uncertainty

• Observable Signatures: Conflicting indicators, whipsaw price action, no clear momentum, high volatility without direction