Patient Trendfollower (7)(alpha)Patient Trendfollower consists of 21 and 55 EMA, Commodity Channel Index and Supertrend indicator. It confirms a trend and gives you a signal on a pullback. Original creation worked on 1h EURUSD chart.

►Long setup:

• 21 EMA is above 55 EMA, which is above the Supertrend indicator.

• Commodity Channel Index is an oscillator, which prints into the chart if extreme levels are reached. Green is for a level above 100 or below -100, red is above 140 or below -140 and black is above 180 or below -180.

• If 21 EMA > 55EMA > Supertrend and an oversold signal appear, you can buy into the trend.

• When backtesting on 1h EURUSD, profit target 400 pips worked best with a stop-loss below Supertrend's bottom and the size of your spread.

• A picture shows two valid entries.

: This part still malfunctions and shows red dots over some green ones. It is important to disable red ones in the settings to see green ones.

Some more long signals:

Some short signals:

►Backtesting data with default settings and trading only green CCI signals with mentioned risk management strategy:

• 212 closed trades

• 58.96% profitable with average win trade 348 USD and average loss trade 263 USD when only green signals are followed.

• Profit factor 1.903, Sharpee 0.792

• 20 bars is average for all trades, short trades were 18 bars long on average.

With given data, you can see the strategy is profitable by itself. However, original risk management settings do work only on 1h charts of EURUSD and would need to be adjusted for other instruments based on average volatility.

Even though the profitability is low, you can increase your odds by a great margin, if you properly use price action (impulsive and corrective moves, patterns, bar analysis), if you trade when major exchanges are open, you may also use wave analysis such as Elliot Waves or Market Profiles to predict whether the next day might be a trending day. My backtesting program didn't consider these ideas.

Unfortunately, I won't be making backtesting strategy public with it anytime soon, because it still has some parts that do not work. I am ok with that since I understand the code and know what does malfunction and how. Then, there are parts which I am not sure how to fix yet. This is why the indicator is still considered alpha.

In the future when a strategy is published, you will also be able to set your own overbought/oversold values without entering the code itself and probably some other features. But I am not in a hurry for that. You can give me feedback on UX and try to figure out the best setups for other symbols, it might help to improve the automatic testing script when I know what I should achieve. My main point is to make this public for friends who can already be using it on EURUSD at least.

Close doesn't always have to be 400 pips, you might want to close on a logical level such as strong resistance or a trendline too.

Thanks to:

• @everget for providing Supertrend solution.

• Satik FX who hand-tested the system by hand and reported results in this article . He is my main inspiration for creating the complete indicator as one because I want to be able to show and hide it with a single click. My future scripts will also work as a whole strategy each by itself.

• The number in the script's name comes from Satik's numbering. A mentioned article was his seventh shared strategy.

Wyszukaj w skryptach "profitable"

NR4 / NR7 + Inside BarIndicator Script for identifying Narrow Range 4 / 7 + Inside Bar

It also helps to check whether NR4 / NR7 breakout trading has been profitable or not in the past in a particular instrument.

It has helped me to select profitable scripts and avoid losing ones. Can be used for anytime frame.

SIGNAL

NR4 == Narrowest range of 4 periods + signal day is an inside bar

NR4 & NR7 == Narrowest range of 7 periods + signal day is an inside bar

SIGNAL "PROFIT" -

Prior day was NR4 / NR7 and next day price broke out of prior day range in 1 direction and closed in the direction of breakout away from breakout price, resulting in a profit trade.

SIGNAL "LOSS" -

Prior day was NR4 / NR7 and next day price broke out of prior day range and returned back to close inside the narrow zone OR went in opposite direction after the initial breakout, resulting in a loss trade.

TradingView Alerts to MT4 MT5 + dynamic variables NON-REPAINTINGAccidentally, I’m sharing open-source profitable Forex strategy. Accidentally, because this was aimed to be purely educational material. A few days ago TradingView released a very powerful feature of dynamic values from PineScript now being allowed to be passed in Alerts. And thanks to TradingConnector, they could be instantly executed in MT4 or MT5 platform of any broker in the world. So yeah - TradingConnector works with indices and commodities, too.

The logic of this EURUSD 6h strategy is very simple - it is based on Stochastic crossovers with stop-loss set under most recent pivot point. Setting stop-loss with surgical precision is possible exactly thanks to allowance of dynamic values in alerts. TradingConnector has been also upgraded to take advantage of these dynamic values and it now enables executing trades with pre-calculated stop-loss, take-profit, as well as stop and limit orders.

Another fresh feature of TradingConnector, is closing positions only partly - provided that the broker allows it, of course. A position needs to have trade_id specified at entry, referred to in further alerts with partial closing. Detailed spec of alerts syntax and functionalities can be found at TradingConnector website. How to include dynamic variables in alert messages can be seen at the very end of the script in alertcondition() calls.

The strategy also takes commission into consideration.

Slippage is intentionally left at 0. Due to shorter than 1 second delivery time of TradingConnector, slippage is practically non-existing. This can be achieved especially if you’re using VPS server, hosted in the same datacenter as your brokers’ servers. I am using such setup, it is doable. Small slippage and spread is already included in commission value.

This strategy is NON-REPAINTING and uses NO TRAILING-STOP or any other feature known to be faulty in TradingView backtester. Does it make this strategy bulletproof and 100% success-guaranteed? Hell no! Remember the no.1 rule of backtesting - no matter how profitable and good looking a script is, it only tells about the past. There is zero guarantee the same strategy will get similar results in the future.

To turn this script into study so that alerts can be produced, do 2 things:

1. comment “strategy” line at the beginning and uncomment “study” line

2. comment lines 54-59 and uncomment lines 62-65.

Then add script to the chart and configure alerts.

This script was build for educational purposes only.

Certainly this is not financial advice. Anybody using this script or any of its parts in any way, must be aware of high risks connected with trading.

Thanks @LucF and @a.tesla2018 for helping me with code fixes :)

Kirk65 UTBot Strategy FixedCredits to @HPotter for the orginal code.

Credits to @Yo_adriiiiaan for recently publishing the UT Bot study based on the original code.

Credits to @TradersAITradingPlans for making UT Bot strategy.

Strategy fixed with time period by Kirk65.

UT Bot works great with 2 hour time frame with Heikin Ashi, but riskier. Use "Once per bar" In alerts with 1.5% stoploss. If the price goes against Alerts, stoploss will save your assets. Wait until next Alert.

4 hour time frame is less risky and less profitable.

Happy trading..

Kirk65

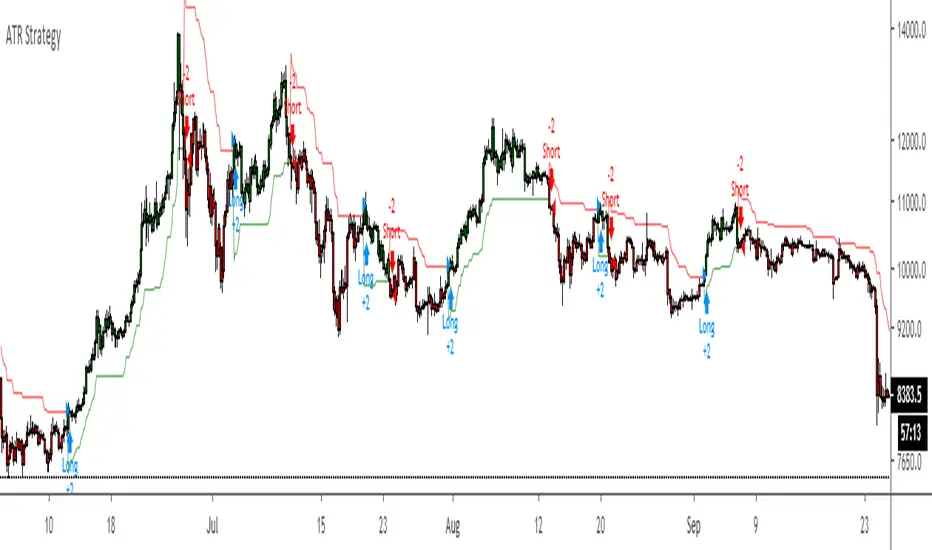

ATR Strategy Back test Original script by HPotter

ATR strategy is profitable.

Buy when it says buy and sell when it says sell.

QuantCat Mom Finder Strategy (1H)QuantCat Momentum Finder Strategy

This strategy is designed to be used on the 1 hour time frame, on all x/btc pairs.

The beautiful thing is it plots the take profit, and stoploss for you for each entry- where I would say use the stoploss for sure and feel with water with how the price action is looking when in profit.

In this strategy, I actually implemented my own trading style into building the strategy. Having to replicate my own trading strategy into an algorithm, I can't make it exactly perfect to how I would trade, but what I can do is try and program the parameters that give it the absolute best chance of making a big move with a small drawdown- which replicates part of my momentum trading style. Here I am using RSI, MACD, EMA and trend filtering values to find moments where there has been a momentum change to play the rest of the move. It only picks the best entries.

There is always a 3-4 R/R move on average with with these trades, meaning 1 in 4 only need to hit to be a break even trader- where most of these strategies have about 35% hit rate.

The stoploss is so crucial to minimise any damage from huge unexpected candles, the strategies can just be used for entries as well, you don't have to stick to the exact formula- of the long and short system, but this by itself is profitable.

The system nets positive results on

-ETH/BTC

-LTC/BTC

-XRP/BTC

-ADA/BTC

-NEO/BTC etc.

We also have a free 15M strategy available too.

You can join our discord server to get live alerts for the strategy as well as speak to our devs! Link in signature below!!!

QuantCat Intraday Strategy (15M)QuantCat Intraday Strategy

This strategy is designed to be used on the 15 minute time frame, on liquid x/btc pairs and BTC/USD.

It works by having 2 moving averages, automatic stop loss calculation, and taking positions on MA crosses and MA zone bounces for confirmation.

Stoploss is so crucial to minimise any damage from huge unexpected candles, the strategies can just be used for entries as well, you don't have to stick to the exact formula- of the long and short system, but this by itself is profitable.

The system nets positive results on

-BTC/USD

-ETH/BTC

-LTC/BTC

-XRP/BTC

There is a small element of trend filtering also for the MA's, but I found adding it in actually hindered performance when testing and training the strategies unless it was using a loose value.

You can get live alerts for this strategy and speak to our developers by joining our server on discord! (Link in signature)

Odin's Kraken (TK Cross Strategy)A simple, yet profitable, trend following system based on 1 hour TK Crosses and ADX.

Works best on ETH/BTC, but is also profitable on other large-cap altcoin BTC pairs (ADA/BTC, EOS/BTC, and TRX/BTC ).

I'm still just getting started in the algo trading world, but if you have any questions I am more than happy to answer them in the comment section here or on Twitter (@pascaltmn).

Cheers.

PivotBoss TriggersI have collected the four PivotBoss indicators into one big indicator. Eventually I will delete the individual ones, since you can just turn off the ones you don't need in the style controller. Cheers.

Wick Reversal

When the market has been trending lower then suddenly forms a reversal wick candlestick , the likelihood of

a reversal increases since buyers have finally begun to overwhelm the sellers. Selling pressure rules the decline,

but responsive buyers entered the market due to perceived undervaluation. For the reversal wick to open near the

high of the candle, sell off sharply intra-bar, and then rally back toward the open of the candle is bullish , as it

signifies that the bears no longer have control since they were not able to extend the decline of the candle, or the

trend. Instead, the bulls were able to rally price from the lows of the candle and close the bar near the top of its

range, which is bullish - at least for one bar, which hadn't been the case during the bearish trend.

Essentially, when a reversal wick forms at the extreme of a trend, the market is telling you that the trend

either has stalled or is on the verge of a reversal. Remember, the market auctions higher in search of sellers, and

lower in search of buyers. When the market over-extends itself in search of market participants, it will find itself

out of value, which means responsive market participants will look to enter the market to push price back toward

an area of perceived value. This will help price find a value area for two-sided trade to take place. When the

market finds itself too far out of value, responsive market participants will sometimes enter the market with

force, which aggressively pushes price in the opposite direction, essentially forming reversal wick candlesticks .

This pattern is perhaps the most telling and common reversal setup, but requires steadfast confirmation in order

to capitalize on its power. Understanding the psychology behind these formations and learning to identify them

quickly will allow you to enter positions well ahead of the crowd, especially if you've spotted these patterns at

potentially overvalued or undervalued areas.

Fade (Extreme) Reversal

The extreme reversal setup is a clever pattern that capitalizes on the ongoing psychological patterns of

investors, traders, and institutions. Basically, the setup looks for an extreme pattern of selling pressure and then

looks to fade this behavior to capture a bullish move higher (reverse for shorts). In essence, this setup is visually

pointing out oversold and overbought scenarios that forces responsive buyers and sellers to come out of the dark

and put their money to work-price has been over-extended and must be pushed back toward a fair area of value

so two-sided trade can take place.

This setup works because many normal investors, or casual traders, head for the exits once their trade

begins to move sharply against them. When this happens, price becomes extremely overbought or oversold,

creating value for responsive buyers and sellers. Therefore, savvy professionals will see that price is above or

below value and will seize the opportunity. When the scared money is selling, the smart money begins to buy, and

Vice versa.

Look at it this way, when the market sells off sharply in one giant candlestick , traders that were short

during the drop begin to cover their profitable positions by buying. Likewise, the traders that were on the

sidelines during the sell-off now see value in lower prices and begin to buy, thus doubling up on the buying

pressure. This helps to spark a sharp v-bottom reversal that pushes price in the opposite direction back toward

fair value.

Engulfing (Outside) Reversal

The power behind this pattern lies in the psychology behind the traders involved in this setup. If you have

ever participated in a breakout at support or resistance only to have the market reverse sharply against you, then

you are familiar with the market dynamics of this setup. What exactly is going on at these levels? To understand

this concept is to understand the outside reversal pattern. Basically, market participants are testing the waters

above resistance or below support to make sure there is no new business to be done at these levels. When no

initiative buyers or sellers participate in range extension, responsive participants have all the information they

need to reverse price back toward a new area of perceived value.

As you look at a bullish outside reversal pattern, you will notice that the current bar's low is lower than the

prior bar's low. Essentially, the market is testing the waters below recently established lows to see if a downside

follow-through will occur. When no additional selling pressure enters the market, the result is a flood of buying

pressure that causes a springboard effect, thereby shooting price above the prior bar's highs and creating the

beginning of a bullish advance.

If you recall the child on the trampoline for a moment, you'll realize that the child had to force the bounce

mat down before he could spring into the air. Also, remember Jennifer the cake baker? She initially pushed price

to $20 per cake, which sent a flood of orders into her shop. The flood of buying pressure eventually sent the price

of her cakes to $35 apiece. Basically, price had to test the $20 level before it could rise to $35.

Let's analyze the outside reversal setup in a different light for a moment. One of the reasons I like this setup

is because the two-bar pattern reduces into the wick reversal setup, which we covered earlier in the chapter. If

you are not familiar with candlestick reduction, the idea is simple. You are taking the price data over two or more

candlesticks and combining them to create a single candlestick . Therefore, you will be taking the open, high, low,

and close prices of the bars in question to create a single composite candlestick .

Doji Reversal

The doji candlestick is the epitome of indecision. The pattern illustrates a virtual stalemate between buyers

and sellers, which means the existing trend may be on the verge of a reversal. If buyers have been controlling a

bullish advance over a period of time, you will typically see full-bodied candlesticks that personify the bullish

nature of the move. However, if a doji candlestick suddenly appears, the indication is that buyers are suddenly

not as confident in upside price potential as they once were. This is clearly a point of indecision, as buyers are no

longer pushing price to higher valuation, and have allowed sellers to battle them to a draw-at least for this one

candlestick . This leads to profit taking, as buyers begin to sell their profitable long positions, which is heightened

by responsive sellers entering the market due to perceived overvaluation. This "double whammy" of selling

pressure essentially pushes price lower, as responsive sellers take control of the market and push price back

toward fair value.

APEX - Moving Averages [v1]A moving average is the most known indicator that takes into consideration price from the last several periods of the price and calculates a smoothed line also known as a Moving average. This way you will cut out a lot of the noise and have a different view.

The most common usage is the moving average crossover system when you buy and sell when a crossover happens. This system is in general not very profitable but can be used effectively in trending markets.

There is really no general rule to what length should be used. The most well-known and respected lengths are 20 / 50 / 100 / 200 for almost all average. These values are respected as strong resistance and support levels. but if you plan to use a crossover Systems the most profitable settings tend to be when the averages are close together 14 and 28 etc. But this is an area I would appeal to for you to really try out what works and what does not.

Other uses of moving averages are the following:

Crossover system

Moving averages are pointing up and price crosses below (Buy Pullback)

The slow-moving average is Below the fast moving average to help to identify possible bullishness

Can be used as support and resistance lines

If you are an advanced user you may want to try out the following techniques:

Create your own moving average by combining several of those together with the source function

Using the Average True Range to create Keltner Channels

Using Standard deviation to create Bollinger bands (Bollinger bands are also accessible on their own)

You can use Moving averages to smooth the noise on other indicators such as RSI / CCI / MFI

Renko Strategy Open_CloseSimple Renko strategy, very profitable. Thanks to vacalo69 for the idea.

Rules when the strategy opens order at market as follows:

- Buy when previous brick (-1) was bearish and previous brick (-2) was bearish too and actual brick close is bullish

- Sell when previous brick (-1) was bullish and previous brick (-2) was bullish too and actual brick close is bearish

Rules when the strategy send stop order are the same but this time a stop buy or stop sell is placed (better overall results).

Note that strategy open an order only after that condition is met, at the beginning of next candle, so the actual close is not the actual price.

Only input is the brick size multiplier for stop loss and take profit: SL and TP are placed at (brick size)x(multiplier) Or put it very high if you want startegy to close order on opposite signal.

Adjust brick size considering:

- Strategy works well if there are three or more consecutive bricks of same "color"

- Expected Profit

- Drawdown

- Time on trade

This strategy uses Renko charts with TRADITIONAL bricks, so no repaint.

Study with alerts, MT4 expert advisor and jforex automatic strategy are available at request.

Please use comment section for any feedback.

DARVAS BOX MTFMULTIPLE TIME FRAME VERSION OF DARVAS BOX:

You can view different time frame values of Darvas Box levels on any chart

What Is the Darvas Box?

The Darvas Box strategy was developed by Nicholas Darvas. Aside from being a well known dancer, he began trading stock in the 1950s. Based on his success in trading, he was approached to write a book on his strategy. The book, “How I Made $2,000,000 in the Stock Market,” outlines his rather simple approach … simple once you understand the basic concepts and rationale of the strategy.

Darvas Box is an indicator that simply draws lines along highs and lows, and then adjusts them as new highs and lows form. The indicator is available on many trading platforms, such as Thinkorswim. Traders may wish to draw their own boxes though, based on recent highs and lows; Darvas was able to do so (based on telegram quotes) more than half a century ago.

Darvas Box Rules

I shall not follow advisory services.

I shall be cautious of broker advice.

I shall ignore Wall Street sayings or truisms, no matter how ancient or revered.

I shall only trade stocks on major exchanges with adequate volume .

I shall not listen to (or trade off of) rumors or tips, no matter how well researched they may sound.

I will use a sound strategy instead of gamble…I must study this strategy (originally this approach was fundamental analysis , which didn’t work for him, so he developed his Darvas Box trading method).

I will hold one position for longer, as opposed to juggling a bunch of positions for a short period of time.

Darvas looked for increasing volume when selecting stocks to trade; this alerted him to stocks that were being accumulated and were likely to see strong trends.

Darvas believed in buying stocks that presented an upper box limit breakout, but also had an upward Earnings trend. This was especially the case when the major indexes had experienced a decline.

When an upper box limit is broken, buy. From his book, the entry price was usually about 1 to 2% above the upper box limit.

If you enter a trade and the price proceeds to drop out of the new box, and back into the old box, exit the trade.

Entry and stop loss orders should be set in advance, so trades aren’t missed and risk is controlled.

Place, and trail the stop loss order to below the low of the most recent box. This initial stop loss was pretty tight, because Darvas assumed when a price broke out of an old box, it was entering a new box. Therefore, the stop was placed just below the high of old box which was just broken (low of new box).

Record trades, including reasons why you entered and exited.

General conditions of the market must favor buying. Don’t buy stocks when the major indexes are in a bear market, or when volume is flat or declining.

If you are stopped out, but the price moves back into the higher box again providing another buy signal, buy again, using the same stop loss location.

Since the stop is being trailed up, more funds can be added on each consecutive breakout.

The Bottom Line

Nicholas Darvas was a dancer, but committed a great deal of time to developing and then mastering his stock trading method. It’s a trend following method based on breakouts to higher boxes. Risk is controlled by placing a stop below new higher boxes as they form. During choppy conditions the strategy won’t be profitable. This is why Darvas also attempted to only trade stocks with increasing volume and rising Earnings . Trading his method requires a lot of discipline, but can produce big profits when strong trends develop.

source: traderhq.com

Creator: Nicholas DARVAS

Here's the link to a complete list of all my indicators:

tr.tradingview.com

Şimdiye kadar paylaştığım indikatörlerin tam listesi için: tr.tradingview.com

Combo Basic IndicatorsThe indicator consists of multiple time frame SMA and PSAR, the very basic indicator but could be profitable.

SMA can be used as dynamic Support-Resistant levels, and value of higher time frame are considered more significant (major level).

For example, Bitcoin currently has weekly support at 6568$, and regarding to SMA of lower time frame (Day, 4H,..) that are near then concluded as sideways condition.

However, trading opportunities still can be found for short term and tight range (scalping).

Build A Bot Hull TriggerThis is the automated trading system we built during the 60-Minute Build-A-Bot webinar on September 12, 2018. We had a lot of fun, and implemented a TON of indicators LIVE during this webinar! And the best part is that as a group we researched, designed, and built a profitable robot in exactly 60 minutes!

We started by voting on the type of trading system, and this is a trend following system because it got the most votes. Then, the attendees in the webinar sent in their suggestions for indicators and settings during the live webinar (still counting toward the 60 minutes). Once we had the indicators on the chart, and we discussed various settings we could use, we got to work building the robot, and ran the first strategy test...and it was profitable!

This version uses the Hull Moving Average as a trigger for initiating the trade, and everything else is the same for the filters. The other version uses the CCI as a trigger for the trade, and many other indicators as filters.

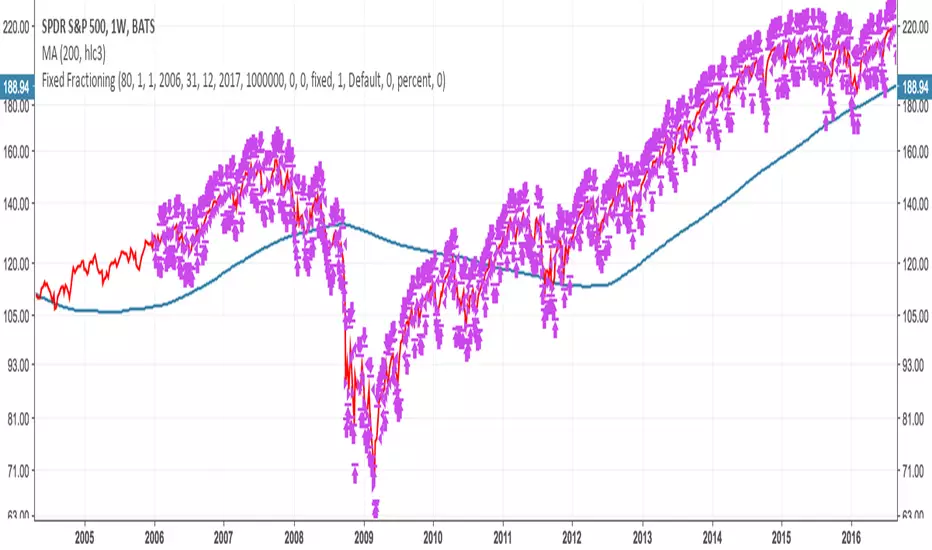

basic fixed fraction strategyOne of the most common trading strategy is to invest a certain percentage in an asset, and keep the percentage fixed. For example you invest 2% in a stock, and as the value goes up you sell. And as the value goes down you buy. Always trying to keep the value of how much you have invested in that asset at 2%.

This works very well with assets that are stable. If you have something that fluctuates around a value, you will find yourself that each time it has gone back to the value in which you entered, you have actually gained something. With an asset that grows it also works. But in general you might find that more aggressive investments are more profitable. On the other side if there is a bubble, and you invest from the beginning using this strategy you will find yourself at the end of the bubble having gained something. Not as much as having bought all at the beginning and having sold all at the end, but still you will have sold going up, and bought going down. Plus you will have gained in the fluctuation.

Where is instead very dangerous is in stock and assets that go to zero. This because you might invest just 2% in an investment. But then as the strategy works you keep investing more as you are trying to keep 2%. You basically can lose all your money in this way (like if you were invested 100% in an asset). Very dangerous. This is why you should only use this with assets that you are sure cannot go to zero (an ETF on S & P 500 could be a good example).

So I coded this strategy on TradingView. basically it will ask you what percentage you want to invest. Then starts with entering with an order of that amount, and will then keep sitself at the same percentage. The system is discrete, as it can only buy a discrete number of contract.

Note that if you use this for cryptocurrency (where you can buy a fraction of a coin, like 0.01 btc) then you should multiply the money that you have by 10, 100, 1000 ... depending on how many digits after the comma your exchange permit you to trade.

If you are using this for forex or crypto it is quite easy that the number of order will explode. As such I added the date range taken from Allanster great script

One way to use Fixed Fractioning is to calculate the Kelly Index of an asset (which will give you a percentage), and then invest half or a quarter of the kelly in that coin, and then keep this fixed.

Another way (which goes well beyond what this script can do alone) to use the Fixed Fractioning is, if you have two assets that are anticorrelated (has a negative correlation), then investing a certain percentage of your capital in one and another percentage in another. And then each time one goes up (and the other goes down) you sell the one that is going up, and buy the one that is going down to keep the percentages fixed.

Something else, it is pretty common for people to invest around 80% of their money in an ETF that follows tha S&P500. This is why here we use 80%. Generally I have seen a more common investment strategy to be around 2%.

As everybody says: I am not responsible for your money. Study before investing.

GBTC Premium to NAV IndicatorWhen bitcoin is in an uptrend, a very profitable strategy is to buy GBTC when premium to NAV is low, and sell when it reaches extremes. This can be far more profitable than buying bitcoin itself.

DARVAS BOX by KIVANÇ fr3762What Is the Darvas Box?

The Darvas Box strategy was developed by Nicholas Darvas. Aside from being a well known dancer, he began trading stock in the 1950s. Based on his success in trading, he was approached to write a book on his strategy. The book, “How I Made $2,000,000 in the Stock Market,” outlines his rather simple approach … simple once you understand the basic concepts and rationale of the strategy.

Darvas Box is an indicator that simply draws lines along highs and lows, and then adjusts them as new highs and lows form. The indicator is available on many trading platforms, such as Thinkorswim. Traders may wish to draw their own boxes though, based on recent highs and lows; Darvas was able to do so (based on telegram quotes) more than half a century ago.

Darvas Box Rules

I shall not follow advisory services.

I shall be cautious of broker advice.

I shall ignore Wall Street sayings or truisms, no matter how ancient or revered.

I shall only trade stocks on major exchanges with adequate volume .

I shall not listen to (or trade off of) rumors or tips, no matter how well researched they may sound.

I will use a sound strategy instead of gamble…I must study this strategy (originally this approach was fundamental analysis , which didn’t work for him, so he developed his Darvas Box trading method).

I will hold one position for longer, as opposed to juggling a bunch of positions for a short period of time.

Darvas looked for increasing volume when selecting stocks to trade; this alerted him to stocks that were being accumulated and were likely to see strong trends.

Darvas believed in buying stocks that presented an upper box limit breakout, but also had an upward Earnings trend. This was especially the case when the major indexes had experienced a decline.

When an upper box limit is broken, buy. From his book, the entry price was usually about 1 to 2% above the upper box limit.

If you enter a trade and the price proceeds to drop out of the new box, and back into the old box, exit the trade.

Entry and stop loss orders should be set in advance, so trades aren’t missed and risk is controlled.

Place, and trail the stop loss order to below the low of the most recent box. This initial stop loss was pretty tight, because Darvas assumed when a price broke out of an old box, it was entering a new box. Therefore, the stop was placed just below the high of old box which was just broken (low of new box).

Record trades, including reasons why you entered and exited.

General conditions of the market must favor buying. Don’t buy stocks when the major indexes are in a bear market, or when volume is flat or declining.

If you are stopped out, but the price moves back into the higher box again providing another buy signal, buy again, using the same stop loss location.

Since the stop is being trailed up, more funds can be added on each consecutive breakout.

The Bottom Line

Nicholas Darvas was a dancer, but committed a great deal of time to developing and then mastering his stock trading method. It’s a trend following method based on breakouts to higher boxes. Risk is controlled by placing a stop below new higher boxes as they form. During choppy conditions the strategy won’t be profitable. This is why Darvas also attempted to only trade stocks with increasing volume and rising Earnings . Trading his method requires a lot of discipline, but can produce big profits when strong trends develop.

source: traderhq.com

Creator: Nicholas DARVAS

Noro's Hundred Strategy v1.0Strategy uses:

1) Fast RSI (period = 7 bars)

2) Color of bars

Strategy

If RSI less than 30 is also 4 red candles in a row - to open long-position

If RSI more than 70 is also 4 green candles in a row - to open short-position

If long-position is open and there is 1 green candle - to close a position

If short-position is open and there is 1 red candle - to close a position

Only profit

Very dangerous thing! Strategy will close a position only if a position profitable. Most likely you will lose all money if you use this function.

Noro's Trend MAs Strategy v2.3Don't use on pairs of type "crypto/crypto"!

Only for pairs like "crypto/fiat" ("BTC/USD", "BTC/CNY", "ETH/USD", "ETH/CNY", etc)

Trade strategy which uses only 2 MA.

The slow MA (blue) is used for definition of a trend

The fast MA (red) is used for an entrance to the transaction

For:

- For H1

- For crypto/fiat

- Good for "BTC/USD", "ETH/USD"

Recomended:

Long = true (if it is profitable as a result of backtests)

Short = true (if it is profitable as a result of backtests)

Stops = false

Stop, % = any

Use Fast MA = true

Fast MA Period = 5

Slow MA Period = 21

Bars Q = (2 for "bitcoin/fiat" or 1 for "crypto/fiat")

Extreme = true (if "crypto/fiat")

In the new version 2.3

+ Dates

Noro's Primitive Strategy v1.0It is calculated what long a candle body

Average length of a body of a candle, for the last 30 candles is calculated

If the candle red and a body of a candle is more average / 2 - to open long (and to close short)

If long is open, a body of a candle is more average / 2, the candle green and a position is profitable - to close long

If the candle green and a body of a candle is more average / 2 - to open short (and to close long)

If it is open short, a body of a candle is more average / 2, the candle red and a position is profitable - to close short

Noro's ColorBar Strategy v1.0It is calculated what long a candle body

Average length of a body of a candle, for the last 30 candles is calculated

If the candle red and a body of a candle is more average - to open long (and to close short)

If long is open, the candle green and a position is profitable - to close long

If the candle green and a body of a candle is more average - to open short (and to close long)

If it is open short, the candle red and a position is profitable - to close short

Noro's Trend MAs Strategy v2.0Don't use on pairs of type "crypto/crypto"!

Only for pairs like "crypto/fiat" ("BTC/USD", "BTC/CNY", "ETH/USD", "ETH/CNY", etc)

Trade strategy which uses only 2 MA.

The slow MA (blue) is used for definition of a trend

The fast MA (red) is used for an entrance to the transaction

For:

- For H1

- For crypto/fiat

- Good for "BTC/USD", "ETH/USD"

Recomended:

Long = true (if it is profitable as a result of backtests)

Short = true (if it is profitable as a result of backtests)

Stops = false

Stop, % = any

OHLC4 = any

Use Fast MA = true

Fast MA Period = 5

Slow MA Period = 21

Bars Q = (2 for "bitcoin/fiat" or 1 for "crypto/fiat")

Extreme = true (if "crypto/fiat")

In the new version 2.0

- CryptoBottom is added

Noro's Trend MAs Strategy v1.9 ExtremeExtreme version of Noro's Trend MAs strategy.

Don't use on pairs of type "crypto/crypto"!

Only for pairs like "crypto/fiat" ("BTC/USD", "BTC/CNY", "ETH/USD", "ETH/CNY", etc)

Trade strategy which uses only 2 MA.

The slow MA (blue) is used for definition of a trend

The fast MA (red) is used for an entrance to the transaction

For:

- For H1

- For crypto/fiat

- Good for "BTC/USD", "ETH/USD"

Recomended:

Long = true (if it is profitable as a result of backtests)

Short = true (if it is profitable as a result of backtests)

Stops = false

Stop, % = any

OHLC4 = any

Use Fast MA = true

Fast MA Period = 5

Slow MA Period = 21

Bars Q = (2 for "bitcoin/fiat" or 1 for "crypto/fiat")

Extreme = true (if "crypto/fiat")

In the new version 1.9

- Extreme is added