Super Momentum StrategyThis is a strategy utilizing multiple of Evergets RMI (thanks to him for permission to publish) and a Chance Momentum.

It buys when 4 of the RMIs are below their thresholds and sells when they are above. There is a 5th one I added last night that works in Reverse - buy when its above and sell when below, which should work better for pyramiding strats by using it at the right rate to set the overall trend.

Very basic sample below, I could have set it up better as my example but just want to publish.

Wyszukaj w skryptach "momentum"

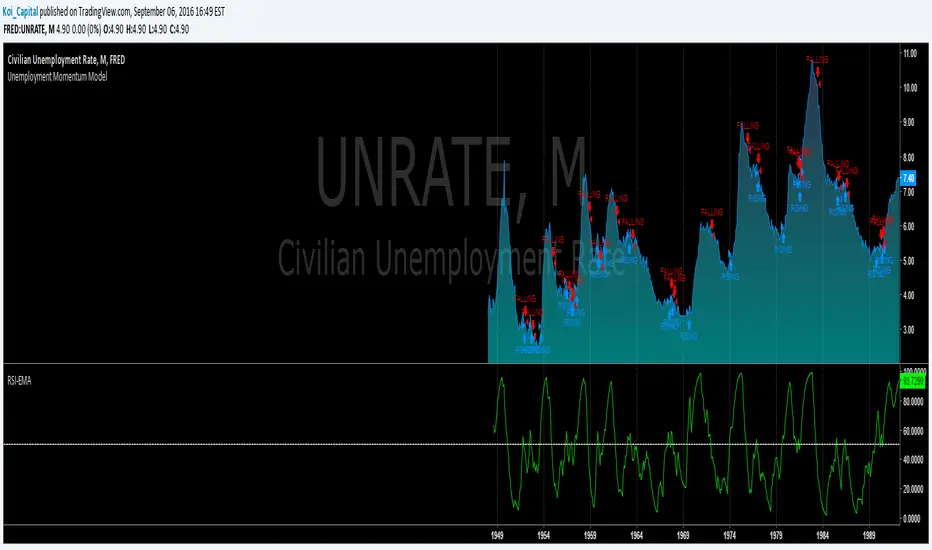

Unemployment Momentum ModelThis model uses a Smoothed RSI to measure the momentum of the Civilian Unemployment Rate as published by FRED. The behavior of the unemployment rate makes it ideal for applying momentum-based timing techniques because it tends to rise sharply in a short time period and then declines gradually over a longer period. Using other basic momentum-based timing techniques also works well (e.g., EMA crossover, MACD, ROC, etc.)

Please note that you cannot trade the unemployment rate directly. This model is meant to help you understand the state of the current economy in the context of unemployment.

Momentum Long + Short Strategy (BTC 3H)Momentum Long + Short Strategy (BTC 3H)

🔍 How It Works, Step by Step

Detect the Trend (📈/📉)

Calculate two moving averages (100-period and 500-period), either EMA or SMA.

For longs, we require MA100 > MA500 (uptrend).

For shorts, we block entries if MA100 exceeds MA500 by more than a set percentage (to avoid fading a powerful uptrend).

Apply Momentum Filters (⚡️)

RSI Filter: Measures recent strength—only allow longs when RSI crosses above its smoothed average, and shorts when RSI dips below the oversold threshold.

ADX Filter: Gauges trend strength—ensures we only enter when a meaningful trend exists (optional).

ATR Filter: Confirms volatility—avoids choppy, low-volatility conditions by requiring ATR to exceed its smoothed value (optional).

Confirm Entry Conditions (✅)

Long Entry:

Price is above both MAs

Trend alignment & optional filters pass ✅

Short Entry:

Price is below both MAs and below the lower Bollinger Band

RSI is sufficiently oversold

Trend-blocker & ATR filter pass ✅

Position Sizing & Risk (💰)

Each trade uses 100 % of account equity by default.

One pyramid addition allowed, so you can scale in if the move continues.

Commission and slippage assumptions built in for realistic backtests.

Stops & Exits (🛑)

Long Stop-Loss: e.g. 3 % below entry.

Long Auto-Exit: If price falls back under the 500-period MA.

Short Stop-Loss: e.g. 3 % above entry.

Short Take-Profit: e.g. 4 % below entry.

🎨 Why It’s Powerful & Customizable

Modular Filters: Turn on/off RSI, ADX, ATR filters to suit different market regimes.

Adjustable Thresholds: Fine-tune stop-loss %, take-profit %, RSI lengths, MA gaps and more.

Multi-Timeframe Potential: Although coded for 3 h BTC, you can adapt it to stocks, forex or other cryptos—just recalibrate!

Backtest Fine-Tuned: Default settings were optimized via backtesting on historical BTC data—but they’re not guarantees of future performance.

⚠️ Warning & Disclaimer

This strategy is for educational purposes only and designed for a toy fund. Crypto markets are highly volatile—you can lose 100 % of your capital. It is not a predictive “holy grail” but a rules-based framework using past data. The parameters have been fine-tuned on historical data and are not valid for future trades without fresh calibration. Always practice with paper-trading first, use proper risk management, and do your own research before risking real money. 🚨🔒

Good luck exploring and experimenting! 🚀📊

MCOTs Intuition StrategyInitial Capital: The strategy starts with an initial capital of $50,000.

Execution: Trades are executed on every price tick to capture all potential movements.

Contract Size: The default position size is one contract per trade.

Timeframe: Although not explicitly mentioned, this strategy is intended for a one-minute timeframe.

RSI Calculation: The Relative Strength Index (RSI) is calculated over a user-defined period (default is 14 periods).

Standard Deviation: The script calculates the standard deviation of the change in RSI values to determine the threshold for entering trades.

Exhaustion Detection: Before entering a long or short position, the script checks for exhaustion in the RSI’s momentum. This is to avoid entering trades during extreme conditions where a reversal is likely.

Entry Conditions: A long position is entered when the current RSI momentum exceeds the standard deviation threshold and is less than the previous momentum multiplied by an exhaustion factor. A short position is entered under the opposite conditions.

Limit Orders for Exit: Instead of traditional stop loss and take profit orders, the strategy uses limit orders to exit positions. This means the strategy sets a desired price level to close the position and waits for the market to reach this price.

Profit Target and Stop Loss: The script allows setting a profit target and stop loss in terms of ticks, which are the smallest measurable increments in price movement for the traded asset.

blah blah whatever

Reversal Trap Sniper – Verified VersionReversal Trap Sniper

Overview

Reversal Trap Sniper is a counterintuitive momentum-following strategy that identifies "reversal traps"—situations where traders expect a market reversal based on RSI, but the price continues trending. By detecting these failed reversal signals, the strategy enters trades in the trend direction, often catching strong follow-through moves.

How It Works

The system monitors the Relative Strength Index (RSI). When RSI moves above the overbought level (e.g., 70) and then drops back below it, many traders interpret this as a sell signal.

However, this strategy treats such moves with caution. If the RSI pulls back below the overbought threshold but the price continues to rise, the system considers it a "reversal trap"—a fakeout.

In such cases, instead of going short, the strategy enters a long position, assuming that the trend is still valid and those betting on a reversal may fuel a breakout.

Similarly, if RSI rises above the oversold level from below, but price continues falling, a short trade is triggered.

Entries are followed by ATR-based stop-loss and dynamic take-profit (2× risk), with a fallback time-based exit after 30 bars.

Key Features

- Detects failed RSI-based reversals ("traps")

- Follows momentum after the trap is triggered

- Uses ATR for dynamic stop-loss and take-profit

- Auto-exit after a fixed bar count (30 bars)

- Visual markers on chart for transparency

- Realistic trading assumptions: 0.05% commission, slippage, and capped pyramiding

Parameter Explanation

RSI Length (14): Standard RSI calculation period

Overbought/Oversold Levels (70/30): Common thresholds used by many traders

ATR Length (14): Used to define stop-loss and target dynamically

Risk-Reward Ratio (2.0): Take-profit is set at 2× the stop-loss distance

Max Holding Bars (30): Ensures trades don’t remain open indefinitely

Pyramiding (10): Allows scaling into trades, simulating real-world strategy stacking

Originality Note

This strategy inverts traditional RSI logic. Instead of treating overbought/oversold conditions as signals for reversal, it waits for those signals to fail. Only after such failures, confirmed by continued price action in the same direction, does the system enter trades. This logic is based on the behavioral observation that failed reversal signals often trigger stronger trend continuation—making this strategy uniquely positioned to exploit trap scenarios.

Disclaimer

This script is for educational and research purposes only. Trading involves risk, and past performance does not guarantee future results. Always test thoroughly before applying with live capital.

ZenBlockChain ETH long-only strategyZenBlockChain ETH long-only strategy massively outperform buy and hold ETH for the same time period, not just for cumulative return but also different measurement. ZenBlockChain ETH long-only strategy using many complicated momentum indicators to trade ETH. This strategy is most effective on 24h window, and could be a great way to diversify our previous ZenBlockChain BTC long-only strategy which is most effective on 12h window. The losing trade for this ETH strategy keeping taking small losses and trade much frequently. However, winning trades is way better than losing trades, so this strategy still massively outperforms buy and hold ETH during the different economic cycles.

------------------------------------------------------------------------------------------------------------------------------------------------------------------

ZenBlockChain ETH做多策略大幅勝過買進持有ETH策略, 不僅總報酬方面大幅勝過,在其他不同財務指標也大幅勝出。ZenBlockChain ETH做多策略使用各種複雜的動能策略去交易ETH,尤其在24小時的的K棒有最佳的表現。此策略非常適合結合我們先前發表的ZenBlockChain BTC做多策略當作投資組合,兩種策略在時間區間與標的都能分散其風險。ZenBlockChain ETH做多策略交易較為頻繁且不斷有小額損失,然而贏家交易遠勝小額的輸家交易,因此此策略在多數不同經濟循環都能大幅勝過買進持有ETH策略。

EMA 12/26 With ATR Volatility StoplossThe EMA 12/26 With ATR Volatility Stoploss

The EMA 12/26 With ATR Volatility Stoploss strategy is a meticulously designed systematic trading approach tailored for navigating financial markets through technical analysis. By integrating the Exponential Moving Average (EMA) and Average True Range (ATR) indicators, the strategy aims to identify optimal entry and exit points for trades while prioritizing disciplined risk management. At its core, it is a trend-following system that seeks to capitalize on price momentum, employing volatility-adjusted stop-loss mechanisms and dynamic position sizing to align with predefined risk parameters. Additionally, it offers traders the flexibility to manage profits either by compounding returns or preserving initial capital, making it adaptable to diverse trading philosophies. This essay provides a comprehensive exploration of the strategy’s underlying concepts, key components, strengths, limitations, and practical applications, without delving into its technical code.

=====

Core Philosophy and Objectives

The EMA 12/26 With ATR Volatility Stoploss strategy is built on the premise of capturing short- to medium-term price trends with a high degree of automation and consistency. It leverages the crossover of two EMAs—a fast EMA (12-period) and a slow EMA (26-period)—to generate buy and sell signals, which indicate potential trend reversals or continuations. To mitigate the inherent risks of trading, the strategy incorporates the ATR indicator to set stop-loss levels that adapt to market volatility, ensuring that losses remain within acceptable bounds. Furthermore, it calculates position sizes based on a user-defined risk percentage, safeguarding capital while optimizing trade exposure.

A distinctive feature of the strategy is its dual profit management modes:

SnowBall (Compound Profit): Profits from successful trades are reinvested into the capital base, allowing for progressively larger position sizes and potential exponential portfolio growth.

ZeroRisk (Fixed Equity): Profits are withdrawn, and trades are executed using only the initial capital, prioritizing capital preservation and minimizing exposure to market downturns.

This duality caters to both aggressive traders seeking growth and conservative traders focused on stability, positioning the strategy as a versatile tool for various market environments.

=====

Key Components of the Strategy

1. EMA-Based Signal Generation

The strategy’s trend-following mechanism hinges on the interaction between the Fast EMA (12-period) and Slow EMA (26-period). EMAs are preferred over simple moving averages because they assign greater weight to recent price data, enabling quicker responses to market shifts. The key signals are:

Buy Signal: Triggered when the Fast EMA crosses above the Slow EMA, suggesting the onset of an uptrend or bullish momentum.

Sell Signal: Occurs when the Fast EMA crosses below the Slow EMA, indicating a potential downtrend or the end of a bullish phase.

To enhance signal reliability, the strategy employs an Anchor Point EMA (AP EMA), a short-period EMA (e.g., 2 days) that smooths the input price data before calculating the primary EMAs. This preprocessing reduces noise from short-term price fluctuations, improving the accuracy of trend detection. Additionally, users can opt for a Consolidated EMA (e.g., 18-period) to display a single trend line instead of both EMAs, simplifying chart analysis while retaining trend insights.

=====

2. Volatility-Adjusted Risk Management with ATR

Risk management is a cornerstone of the strategy, achieved through the use of the Average True Range (ATR), which quantifies market volatility by measuring the average price range over a specified period (e.g., 10 days). The ATR informs the placement of stop-loss levels, which are set at a multiple of the ATR (e.g., 2x ATR) below the entry price for long positions. This approach ensures that stop losses are proportionate to current market conditions—wider during high volatility to avoid premature exits, and narrower during low volatility to protect profits.

For example, if a stock’s ATR is $1 and the multiplier is 2, the stop loss for a buy at $100 would be set at $98. This dynamic adjustment enhances the strategy’s adaptability, preventing stop-outs from normal market noise while capping potential losses.

=====

3. Dynamic Position Sizing

The strategy calculates position sizes to align with a user-defined Risk Per Trade, typically expressed as a percentage of capital (e.g., 2%). The position size is determined by:

The available capital, which varies depending on whether SnowBall or ZeroRisk mode is selected.

The distance between the entry price and the ATR-based stop-loss level, which represents the per-unit risk.

The desired risk percentage, ensuring that the maximum loss per trade does not exceed the specified threshold.

For instance, with a $1,000 capital, a 2% risk per trade ($20), and a stop-loss distance equivalent to 5% of the entry price, the strategy computes the number of units (shares or contracts) to ensure the total loss, if the stop loss is hit, equals $20. To prevent over-leveraging, the strategy includes checks to ensure that the position’s dollar value does not exceed available capital. If it does, the position size is scaled down to fit within the capital constraints, maintaining financial discipline.

=====

4. Flexible Capital Management

The strategy’s dual profit management modes—SnowBall and ZeroRisk—offer traders strategic flexibility:

SnowBall Mode: By compounding profits, traders can increase their capital base, leading to larger position sizes over time. This is ideal for those with a long-term growth mindset, as it harnesses the power of exponential returns.

ZeroRisk Mode: By withdrawing profits and trading solely with the initial capital, traders protect their gains and limit exposure to market volatility. This conservative approach suits those prioritizing stability over aggressive growth.

These options allow traders to tailor the strategy to their risk tolerance, financial goals, and market outlook, enhancing its applicability across different trading styles.

=====

5. Time-Based Trade Filtering

To optimize performance and relevance, the strategy includes an option to restrict trading to a specific time range (e.g., from 2018 onward). This feature enables traders to focus on periods with favorable market conditions, avoid historically volatile or unreliable data, or align the strategy with their backtesting objectives. By confining trades to a defined timeframe, the strategy ensures that performance metrics reflect the intended market context.

=====

Strengths of the Strategy

The EMA 12/26 With ATR Volatility Stoploss strategy offers several compelling advantages:

Systematic and Objective: By adhering to predefined rules, the strategy eliminates emotional biases, ensuring consistent execution across market conditions.

Robust Risk Controls: The combination of ATR-based stop losses and risk-based position sizing caps losses at user-defined levels, fostering capital preservation.

Customizability: Traders can adjust parameters such as EMA periods, ATR multipliers, and risk percentages, tailoring the strategy to specific markets or preferences.

Volatility Adaptation: Stop losses that scale with market volatility enhance the strategy’s resilience, accommodating both calm and turbulent market phases.

Enhanced Visualization: The use of color-coded EMAs (green for bullish, red for bearish) and background shading provides intuitive visual cues, simplifying trend and trade status identification.

=====

Limitations and Considerations

Despite its strengths, the strategy has inherent limitations that traders must address:

False Signals in Range-Bound Markets: EMA crossovers may generate misleading signals in sideways or choppy markets, leading to whipsaws and unprofitable trades.

Signal Lag: As lagging indicators, EMAs may delay entry or exit signals, causing traders to miss rapid trend shifts or enter trades late.

Overfitting Risk: Excessive optimization of parameters to fit historical data can impair the strategy’s performance in live markets, as past patterns may not persist.

Impact of High Volatility: In extremely volatile markets, wider stop losses may result in larger losses than anticipated, challenging risk management assumptions.

Data Reliability: The strategy’s effectiveness depends on accurate, continuous price data, and discrepancies or gaps can undermine signal accuracy.

=====

Practical Applications

The EMA 12/26 With ATR Volatility Stoploss strategy is versatile, applicable to diverse markets such as stocks, forex, commodities, and cryptocurrencies, particularly in trending environments. To maximize its potential, traders should adopt a rigorous implementation process:

Backtesting: Evaluate the strategy’s historical performance across various market conditions to assess its robustness and identify optimal parameter settings.

Forward Testing: Deploy the strategy in a demo account to validate its real-time performance, ensuring it aligns with live market dynamics before risking capital.

Ongoing Monitoring: Continuously track trade outcomes, analyze performance metrics, and refine parameters to adapt to evolving market conditions.

Additionally, traders should consider market-specific factors, such as liquidity and volatility, when applying the strategy. For instance, highly liquid markets like forex may require tighter ATR multipliers, while less liquid markets like small-cap stocks may benefit from wider stop losses.

=====

Conclusion

The EMA 12/26 With ATR Volatility Stoploss strategy is a sophisticated, systematic trading framework that blends trend-following precision with disciplined risk management. By leveraging EMA crossovers for signal generation, ATR-based stop losses for volatility adjustment, and dynamic position sizing for risk control, it offers a balanced approach to capturing market trends while safeguarding capital. Its flexibility—evident in customizable parameters and dual profit management modes—makes it suitable for traders with varying risk appetites and objectives. However, its limitations, such as susceptibility to false signals and signal lag, necessitate thorough testing and prudent application. Through rigorous backtesting, forward testing, and continuous refinement, traders can harness this strategy to achieve consistent, risk-adjusted returns in trending markets, establishing it as a valuable tool in the arsenal of systematic trading.

Trend Vector Pro v2.0Title: Trend Vector Pro v2.0

👨💻 Developed by: Mohammed Bedaiwi

💡 Strategy Overview & Coherence

Trend Vector Pro (TVPro) is a momentum-based trend & reversal strategy that uses a custom smoothed oscillator, an optional ADX filter, and classic Pivot Points to create a single, coherent trading framework.

Instead of stacking random indicators, TVPro is built around these integrated components:

A custom momentum engine (signal generation)

An optional ADX filter (trend quality control)

Daily Pivot Points (context, targets & S/R)

Swing-based “Golden Bar” trailing stops (trade management)

Optional extended bar detection (overextension alerts)

All parts are designed to work together and are documented below to address originality & usefulness requirements.

🔍 Core Components & Justification

1. Custom Momentum Engine (Main Signal Source)

TVPro’s engine is a custom oscillator derived from the bar midpoint ( hl2 ), similar in spirit to the Awesome Oscillator but adapted and fully integrated into the strategy. It measures velocity and acceleration of price, letting the script distinguish between strong impulses, weakening trends, and pure noise.

2. ADX Filter (Trend Strength Validation – Optional)

Uses Average Directional Index (ADX) as a gatekeeper.

Why this matters: This prevents the strategy from firing signals in choppy, non-trending environments (when ADX is below the threshold) and keeps trades focused on periods of clear directional strength.

3. Classic Pivot Points (Context & Targets)

Calculates Daily Pivot Points ( PP, R1-R3, S1-S3 ) via request.security() using prior session data.

Why this matters: Momentum gives the signal, ADX validates the environment, and Pivots add external structure for risk and target planning. This is a designed interaction, not a random mashup.

🧭 Trend State Logic (5-State Bar Coloring)

The strategy uses the momentum's value + slope to define five states, turning the chart into a visual momentum map:

🟢 STRONG BULL (Bright Green): Momentum accelerating UP. → Strong upside impulse.

🌲 WEAK BULL (Dark Green): Momentum decelerating DOWN (while positive). → Pullback/pause zone.

🔴 STRONG BEAR (Bright Red): Momentum accelerating DOWN. → Strong downside impulse.

🍷 WEAK BEAR (Dark Red): Momentum decelerating UP (while negative). → Rally/short-covering zone.

🔵 NEUTRAL / CHOP (Cyan): Momentum is near zero (based on noise threshold). → Consolidation / low volatility.

🎯 Signal Logic Modes

TVPro provides two selectable entry styles, controlled by input:

Reversals Only (Cleaner Mode – Default): Targets trend flips. Entry triggers when the current state is Bullish (or Bearish) and the previous state was not. This reduces noise and over-trading.

All Strong Pulses (Aggressive Mode): Targets acceleration phases. Entry triggers when the bar turns to STRONG BULL or STRONG BEAR after any other state. This mode produces more trades.

📌 Risk Management Tools

Golden Bars – Trailing Stops: Yellow “Trail” Arrows mark confirmed Swing Highs/Lows. These are used as logical trailing stop levels based on market structure.

Extended Bars: Detects when price closes outside a 2-standard-deviation channel, flagging overextension where a pullback is more likely.

Pivot Points: Used as external targets for Take Profit and structural stop placement.

⚙️ Strategy Defaults (Crucial for Publication Compliance)

To keep backtest results realistic and in line with House Rules, TVPro is published with the following fixed default settings:

Order Size: 5% of equity per trade ( default_qty_value = 5 )

Commission: 0.04% per order ( commission_value = 0.04 )

Slippage: 2 ticks ( slippage = 2 )

Initial Capital: 10,000

📘 How to Trade with Trend Vector Pro

Entry: Take Long when a Long signal appears and confirm the bar is Green (Bull state). Short for Red (Bear state).

Stop Loss: Place the initial SL near the latest swing High/Low, or near a relevant Pivot level.

Trade Management: Follow Golden (Trail) Arrows to trail your stop behind structure.

Exits: Exit when: the trailing stop is hit, Price reaches a major Pivot level, or an opposite signal prints.

🛑 Disclaimer

This script is for educational purposes only and does not constitute financial advice. Past performance does not guarantee future results. Always forward-test and use proper risk management before applying any strategy to live trading.

SuperTrend AI Oscillator StrategySuperTrend AI Oscillator Strategy

Overview

This strategy is a trend-following approach that combines the SuperTrend indicator with oscillator-based filtering.

By identifying market trends while utilizing oscillator-based momentum analysis, it aims to improve entry precision.

Additionally, it incorporates a trailing stop to strengthen risk management while maximizing profits.

This strategy can be applied to various markets, including Forex, Crypto, and Stocks, as well as different timeframes. However, its effectiveness varies depending on market conditions, so thorough testing is required.

Features

1️⃣ Trend Identification Using SuperTrend

The SuperTrend indicator (a volatility-adjusted trend indicator based on ATR) is used to determine trend direction.

A long entry is considered when SuperTrend turns bullish.

A short entry is considered when SuperTrend turns bearish.

The goal is to capture clear trend reversals and avoid unnecessary trades in ranging markets.

2️⃣ Entry Filtering with an Oscillator

The Super Oscillator is used to filter entry signals.

If the oscillator exceeds 50, it strengthens long entries (indicating strong bullish momentum).

If the oscillator drops below 50, it strengthens short entries (indicating strong bearish momentum).

This filter helps reduce trades in uncertain market conditions and improves entry accuracy.

3️⃣ Risk Management with a Trailing Stop

Instead of a fixed stop loss, a SuperTrend-based trailing stop is implemented.

The stop level adjusts automatically based on market volatility.

This allows profits to run while managing downside risk effectively.

4️⃣ Adjustable Risk-Reward Ratio

The default risk-reward ratio is set at 1:2.

Example: A 1% stop loss corresponds to a 2% take profit target.

The ratio can be customized according to the trader’s risk tolerance.

5️⃣ Clear Trade Signals & Visual Support

Green "BUY" labels indicate long entry signals.

Red "SELL" labels indicate short entry signals.

The Super Oscillator is plotted in a separate subwindow to visually assess trend strength.

A real-time trailing stop is displayed to support exit strategies.

These visual aids make it easier to identify entry and exit points.

Trading Parameters & Considerations

Initial Account Balance: Default is $7,000 (adjustable).

Base Currency: USD

Order Size: 10,000 USD

Pyramiding: 1

Trading Fees: $0.94 per trade

Long Position Margin: 50%

Short Position Margin: 50%

Total Trades (M5 Timeframe): 1,032

Visual Aids for Clarity

This strategy includes clear visual trade signals to enhance decision-making:

Green "BUY" labels for long entries

Red "SELL" labels for short entries

Super Oscillator plotted in a subwindow with a 50 midline

Dynamic trailing stop displayed for real-time trend tracking

These visual aids allow traders to quickly identify trade setups and manage positions with greater confidence.

Summary

The SuperTrend AI Oscillator Strategy is developed based on indicators from Black Cat and LuxAlgo.

By integrating high-precision trend analysis with AI-based oscillator filtering, it provides a strong risk-managed trading approach.

Important Notes

This strategy does not guarantee profits—performance varies based on market conditions.

Past performance does not guarantee future results. Markets are constantly changing.

Always test extensively with backtesting and demo trading before using it in live markets.

Risk management, position sizing, and market conditions should always be considered when trading.

Conclusion

This strategy combines trend analysis with momentum filtering, enhancing risk management in trading.

By following market trends carefully, making precise entries, and using trailing stops, it seeks to reduce risk while maximizing potential profits.

Before using this strategy, be sure to test it thoroughly via backtesting and demo trading, and adjust the settings to match your trading style.

EMA Pullback Speed Strategy 📌 **Overview**

The **EMA Pullback Speed Strategy** is a trend-following approach that combines **price momentum** and **Exponential Moving Averages (EMA)**.

It aims to identify high-probability entry points during brief pullbacks within ongoing uptrends or downtrends.

The strategy evaluates **speed of price movement**, **relative position to dynamic EMA**, and **candlestick patterns** to determine ideal timing for entries.

One of the key concepts is checking whether the price has **“not pulled back too much”**, helping focus only on situations where the trend is likely to continue.

⚠️ This strategy is designed for educational and research purposes only. It does not guarantee future profits.

🧭 **Purpose**

This strategy addresses the common issue of **"jumping in too late during trends and taking unnecessary losses."**

By waiting for a healthy pullback and confirming signs of **trend resumption**, traders can enter with greater confidence and reduce false entries.

🎯 **Strategy Objectives**

* Enter in the direction of the prevailing trend to increase win rate

* Filter out false signals using pullback depth, speed, and candlestick confirmations

* Predefine Take-Profit (TP) and Stop-Loss (SL) levels for safer, rule-based trading

✨ **Key Features**

* **Dynamic EMA**: Reacts faster when price moves quickly, slower when market is calm – adapting to current momentum

* **Pullback Filter**: Avoids trades when price pulls back too far (e.g., more than 5%), indicating a trend may be weakening

* **Speed Check**: Measures how strongly the price returns to the trend using candlestick body speed (open-to-close range in ticks)

📊 **Trading Rules**

**■ Long Entry Conditions:**

* Current price is above the dynamic EMA (indicating uptrend)

* Price has pulled back toward the EMA (a "buy the dip" situation)

* Pullback depth is within the threshold (not excessive)

* Candlesticks show consecutive bullish closes and break the previous high

* Price speed is strong (positive movement with momentum)

**■ Short Entry Conditions:**

* Current price is below the dynamic EMA (indicating downtrend)

* Price has pulled back up toward the EMA (a "sell the rally" setup)

* Pullback is within range (not too deep)

* Candlesticks show consecutive bearish closes and break the previous low

* Price speed is negative (downward momentum confirmed)

**■ Exit Conditions (TP/SL):**

* **Take-Profit (TP):** Fixed 1.5% target above/below entry price

* **Stop-Loss (SL):** Based on recent price volatility, calculated using ATR × 4

💰 **Risk Management Parameters**

* Symbol & Timeframe: BTCUSD on 1-hour chart (H1)

* Test Capital: \$3000 (simulated account)

* Commission: 0.02%

* Slippage: 2 ticks (minimal execution lag)

* Max risk per trade: 5% of account balance

* Backtest Period: Aug 30, 2023 – May 9, 2025

* Profit Factor (PF): 1.965 (Net profit ÷ Net loss, including spreads & fees)

⚙️ **Trading Parameters & Indicator Settings**

* Maximum EMA Length: 50

* Accelerator Multiplier: 3.0

* Pullback Threshold: 5.0%

* ATR Period: 14

* ATR Multiplier (SL distance): 4.0

* Fixed TP: 1.5%

* Short-term EMA: 21

* Long-term EMA: 50

* Long Speed Threshold: ≥ 1000.0 (ticks)

* Short Speed Threshold: ≤ -1000.0 (ticks)

⚠️Adjustments are based on BTCUSD.

⚠️Forex and other currency pairs require separate adjustments.

🔧 **Strategy Improvements & Uniqueness**

Unlike basic moving average crossovers or RSI triggers, this strategy emphasizes **"momentum-supported pullbacks"**.

By combining dynamic EMA, speed checks, and candlestick signals, it captures trades **as if surfing the wave of a trend.**

Its built-in filters help **avoid overextended pullbacks**, which often signal the trend is ending – making it more robust than traditional trend-following systems.

✅ **Summary**

The **EMA Pullback Speed Strategy** is easy to understand, rule-based, and highly reproducible – ideal for both beginners and intermediate traders.

Because it shows **clear visual entry/exit points** on the chart, it’s also a great tool for practicing discretionary trading decisions.

⚠️ Past performance is not a guarantee of future results.

Always respect your Stop-Loss levels and manage your position size according to your risk tolerance.

VIDYA Auto-Trading(Reversal Logic)Overview

This script is a dynamic trend-following strategy based on the Variable Index Dynamic Average (VIDYA). It adapts in real time to market volatility, aiming to enhance entry precision and optimize risk management.

⚠️ This strategy is intended for educational and research purposes. Past performance does not guarantee future results. All results are based on historical simulations using fixed parameters.

Strategy Objectives

The objective of this strategy is to respond swiftly to sudden price movements and trend reversals, providing consistent and reliable trade signals under historical testing conditions. It is designed to be intuitive and efficient for traders of all levels.

Key Features

Momentum Sensitivity via VIDYA: Reacts quickly to momentum shifts, allowing for accurate trend-following entries.

Volatility-Based ATR Bands: Automatically adjusts stop levels and entry conditions based on current market volatility.

Intuitive Trend Visualization: Uptrends are marked with green zones, and downtrends with red zones, giving traders clear visual guidance.

Trading Rules

Long Entry: Triggered when price crosses above the upper band. Any existing short position is closed.

Short Entry: Triggered when price crosses below the lower band. Any existing long position is closed.

Exit Conditions: Positions are reversed based on signal changes, using a position reversal strategy.

Risk Management Parameters

Market: ETHUSD(5M)

Account Size: $3,000 (reasonable approximation for individual traders)

Commission: 0.02%

Slippage: 2 pip

Risk per Trade: 5% of account equity (adjusted to comply with TradingView guidelines for realistic risk levels)

Number of Trades: 251 (based on backtest over the selected dataset)

⚠️ The risk per trade and other values can be customized. Users are encouraged to adapt these to their individual needs and broker conditions.

Trading Parameters & Considerations

VIDYA Length: 10

VIDYA Momentum: 20

Distance factor for upper/lower bands: 2

Source: close

Visual Support

Trend zones, entry points, and directional shifts are clearly plotted on the chart. These visual cues enhance the analytical experience and support faster decision-making.

Visual elements are designed to improve interpretability and are not intended as financial advice or trade signals.

Strategy Improvements & Uniqueness

Inspired by the public work of BigBeluga, this script evolves the original concept with meaningful enhancements. By combining VIDYA and ATR bands, it offers greater adaptability and practical value compared to conventional trend-following strategies.

This adaptation is original work and not a direct copy. Improvements are designed to enhance usability, risk control, and market responsiveness.

Summary

This strategy offers a responsive and adaptive approach to trend trading, built on momentum detection and volatility-adjusted risk management. It balances clarity, precision, and practicality—making it a powerful tool for traders seeking reliable trend signals.

⚠️ All results are based on historical data and are subject to change under different market conditions. This script does not guarantee profit and should be used with caution and proper risk management.

Momentum Alligator 4h Bitcoin StrategyOverview

The Momentum Alligator 4h Bitcoin Strategy is a trend-following trading system that operates on dual time frames. It utilizes the 1D Williams Alligator indicator to identify the prevailing major price trend and seeks trading opportunities on the 4-hour (4h) time frame when the momentum is turning up. The strategy is designed to close trades if the trend fails to develop or holding position if price continues increasing without any significant correction. Note that this strategy is specifically tailored for the 4-hour time frame.

Unique Features

2-layers market noise filtering system: Trades are only initiated in the direction of the 1D trend, determined by the Williams Alligator indicator. This higher time frame confirmation filters out minor trade signals, focusing on more substantial opportunities. At the same time, strategy has additional filter on 4h time frame with Awesome Oscillator which is showing the current price momentum.

Flexible Risk Management: The strategy exclusively opens long positions, resulting in fewer trades during bear markets. It incorporates a dynamic stop-loss mechanism, which can either follow the jaw line of the 4h Alligator or a user-defined fixed stop-loss. This flexibility helps manage risk and avoid non-trending markets.

Methodology

The strategy initiates a long position when the d-line of Stochastic RSI crosses up it's k-line. It means that there is a high probability that price momentum reversed from down to up. To avoid overtrading in potentially choppy markets, it skips the next two trades following a winning trade, anticipating sideways movement after a significant price surge.

This strategy has two layers trades filtering system: 4h and 1D time frames. The first one is awesome oscillator. It shall be increasing and value has to be higher than it's 5-period SMA. This is an additional confirmation that long trade is opened in the direction of the current momentum. As it was mentioned above, all entry signals are validated against the 1D Williams Alligator indicator. A trade is only opened if the price is above all three lines of the 1D Alligator, ensuring alignment with the major trend.

A trade is closed if the price hits the 4h jaw line of the Alligator or reaches the user-defined stop-loss level.

Risk Management

The strategy employs a combined approach to risk management:

It allows positions to ride the trend as long as the price continues to move favorably, aiming to capture significant price movements. It features a user-defined stop-loss parameter to mitigate risks based on individual risk tolerance. By default, this stop-loss is set to a 2% drop from the entry point, but it can be adjusted according to the trader's preferences.

Justification of Methodology

This strategy leverages Stochastic RSI on 4h time frame to open long trade when momentum started reversing to the upside. On the one hand, Stochastic RSI is one of the most sensitive indicator, which allows to react fast on the potential trend reversal. On the other hand, this indicator can be too sensitive and provide a lot of false trend changing signals. To eliminate this weakness we use two-layers trades filtering system.

The first layer is the 4h Awesome oscillator. This is less sensitive momentum indicator. Usually it starts increasing when price has already passed significant distance from the actual reversal point. The strategy opens long trade only is Awesome oscillator is increasing and above it's 5-period SMA. This approach increases the probability to filter the false signals during the choppy market or if the reversal is false.

The second layer filter is the Williams Alligator indicator on 1D time frame. The 1D Alligator serves as a filter for identifying the primary trend and increases probability to avoid the trades with low potential because trading against major trend usually is more risky. It's much better to catch the trend continuation than local bounce.

Last but not least feature of this strategy is close trades condition. It uses the flexible approach. First of all, user can set up the fixed stop-loss according to his own risk-tolerance, by default this value is 2% of price movement. It restricts the potential loss at the moment when trade has just been opened. Moreover strategy utilizes the 4h Williams Alligator's jaw line to exit the trade. If price fell below it trade is closed. This approach helps to not keep open trade if trend is not developing and hold it if price continues going up.

Backtest Results:

Operating window: Date range of backtests is 2021.01.01 - 2024.05.01. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 50%

Maximum Single Position Loss: -3.04%

Maximum Single Profit: +29.67%

Net Profit: +6228.01 USDT (+62.28%)

Total Trades: 118 (24.58% win rate)

Profit Factor: 1.71

Maximum Accumulated Loss: 1527.69 USDT (-11.52%)

Average Profit per Trade: 52.78 USDT (+0.89%)

Average Trade Duration: 60 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

How to Use:

Add the script to favorites for easy access.

Apply to the 4h timeframe desired chart (optimal performance observed on the BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

Broadview Economic StudioThank you for taking the time to read this description. We'll be taking a look at the Broadview Economic Studio. This has been a work-in-progress for years and is a very powerful tool for planning trades with complex volume scaling strategies. We will be talking about many indicators and types of indicators used in the public domain, but it is NOT recommended to reverse engineer our scripts as there is quite a bit of logic in the code that works to make each common approach entirely unique. So although you may understand quite a bit about oscillators, the way they work with the rest of the logic within the script may change the way you know them to work from elsewhere.

In the chart snapshot above you'll see a mild configuration where I only had to tweak a few settings. Commissions are set to 0.1%, starting capital is set to $10,000, and slippage is off. In my tests orders came through less than a penny off. Generally speaking, there are really only two situations in which you should be concerned about slippage. The first is if you trade really low timeframe charts like the 1 second. This tool, while it works for any timeframe, is programmed on the 45 minute timeframe and works best there. The other situation in which you should be prepared for slippage is if you're using extremely high volume trades in the hundreds of thousands or millions depending on the market cap and liquidity of the asset you're studying. Large orders like that have to be split up among several deals and that can cause slippage.

There are 31 primary inputs for users to tweak. Each input is grouped within a module called a Suite. Each suite has a focus like filtering signals or strategically allocating volume according to your strategy. Everything starts with the Origin Suite. The Origin Suite is a group of inputs that generates Tops & Bottoms from price action. It uses math like Rate of Change, where one can specify a required rate of change before an Origin signal can be made, and users can specify how much lower in price a bar must be compared to previous bars. So with the Origin Suite, users can control how often they want to see originating signals and under what conditions they can appear.

We used to use WVF and CVI to produce top and bottom signals, but our Origin Suite works much better for systematically generating profitable configurations.

The triangles you see on the chart represent markers, potential signals, or Prop Signals as they're referred to within the script. The blue arrows represent trades where Prop Signals were allowed to pass as true long signals. There are two ways to ignore Prop Signals. You can filter the markers entirely, or you can reduce their volume scaling to the minimum which is usually $10 for most exchanges. We're first going to be talking about some of the primary DCA inputs before we talk about the technology we use to filter and overload signals.

Here are some important features found within the script:

Base Orders

Safety Orders

Take Profits

Change-Based Volume Scaling

Ignoring Low or Medium Changes

Overloading

Filtering

Alert Messages w/ Volume Scaling

Let's walk through each of these features in more depth.

The Base Order is the initial Long position within a series. It comes in first and is followed by all of its Safety Orders. The Base Order is set to $25 within the script by default. Keeping the base order low allows one to reserve more of their capital for Safety Orders that are lower within a dip, and thus, lower the user's Position Average. The primary feature of this script is to help users plan their volume scaling strategically, and this is where we start. It's this kind of due diligence and effort in protecting trades that makes this script unique.

So we start with a low Base Order. Then, we follow with a lot of Safety Orders. Typically in DCA this is done in consistent time intervals and in consistent amounts. So in regular DCA one may invest the same amount bi-weekly on pay day. They use the financial instrument as a sort of savings and average their position over their consistent investments. This is not where the bleeding edge of DCA is today though. In modern Doller Cost Averaging, I would expect to see signals and volume scaling based on logic.. as opposed to being consistent intervals.

This sets up the explanation of the primary means of volume scaling within the script. Mathematically, we start with the net balance. This is your specified starting balance plus any wins or losses. Users specify what % of their Available Balance they would like to start with when volume scaling. This percent of capital is then multiplied by a Safety Order Multiplier. The safety order multiplier is made up of a number specified by the user, multiplied by the number of the Safety Order you're on. So user's can control this equation/algorithm and scale their investments as the number of Safety Orders increases and drops in price become more opportune.

The Take Profit within the script lets users specify their desired ROI from a series. So if a user sets a 60% take profit, the script will set a price from the position average that when reached will give the user a 60% ROI for the series including its Base Order and all its Safety Orders.

Before moving on, let's talk about the amazing internal reporting found in the script. When you zoom in on the blue arrows, you can see each trade is accompanied by some extremely helpful information. This is just another feature that makes this script unique, it is the feature that gives us accurate reporting and ultimately allows us to connect with TradingView's Strategy Tester in a way that provides instant backtests with good merit. With this reporting not only can users get reports and information on trades made on different assets with different configurations, but user's can perform a deep dive on each configuration and know exactly what was going on for each trade. The first number is the number of the safety order the script is on. Remember, this is used in the primary volume scaling math. The second number is the amount the script spent on the current trade. The third number denotes the cumulative spending for the series. The final number displays the script's available balance at that time. With these numbers, the TradingView Strategy Tester, and the List of Trades feature, users can practice as much due diligence as they need during their studies.

Let's move on to talking about my favorite suite within the script, the Volume Scaling Suite. Here there are two primary means of controlling volume scaling. Although, in the near future there will be more.

In this suite you'll find Change-Based Volume Scaling and Position Average Volume Scaling. Position Average Volume Scaling is quite easy to explain. This feature only allows signals to pass if they are lower in price than your base order. In this way, users can apply most of their capital to trades that lower their position average. Simply having the money in the market can boost profits, but having a lower Position Average is the entire reason we DCA. Change-Based Volume Scaling is quite a bit more complex.

In theory, one could argue that every moment is a great moment to buy. It's just that some moments are more opportune than others. So it's not about perfect signals as much as it's about proper volume scaling.

Change-Based Volume Scaling allows us to set rules that dictate how much volume scaling is used based on the asset's current delta, or Rate of Change.

Using CBVS, one can downscale capital applied to signals with a low ROC, or simply ignore them. So if a signal comes in and the price hasn't changed very much then you can automatically use less volume for the trade. One can do the same thing for medium changes, and the user can specify what quantifies as a low or medium change. Users can give extra volume to signals with a greater rate of change, or overload signals with a high rate of change! So the CBVS feature gives users the ability to allocate volume based on logic rooted in the asset's rate of change. If a signal has dropped a lot in price, then generally, it is deserving of more capital and that's what makes this feature unique and so powerful.

There are two kinds of Overloading found in the script. There's overloading from CBVS, and then overloading from the 4 signal filtering suites. There's an important difference to note before we move on. Overloading performed by CBVS is based on ignored signals. So if you ignore low or medium change signals, and you have CBVS Overloading on, the script will allocate more capital to High Change signals. When signals are ignored, they are downscaled to $10. Whereas with the filtering suites, if a signal is filtered the Prop Signal triangle marker is removed entirely. The overloading in that scenario is simply applied to signals that aren't filtered. The reason it's done this way is because allowing ignored signals to still come in, with the lowest volume scaling possible, keeps the Safety Order count rising which works in the volume scaling math. This math is intrinsic to getting capital deep within dips and crashes.

So in future versions we may allow ignored signals to be filtered out entirely but for the time being, simply scaling them down to the lowest possible amount is what produces the best and most consistent configurations.

Let's talk about filtering signals, and the overloading provided within each filtering suite.

Here you can see our Overbought & Oversold Heatmap V3. This is a unique indicator that takes 15 common oscillators and visualizes them in a way that clearly denotes confluence. Looking at this indicator makes it easer to read cycles and trends. It is quite common for investors to base their entire scripts on one or more of the oscillators found within the OBOS Heatmap V3. So the OBOS Heatmap V3 is an awesome way to ensure your signals follow an oversold trend! The orange represents an oscillator being oversold, while the yellow represents it being overbought. Generally, when an asset is oversold it is a better time to buy. One can filter signals based on this information and use the Heatmap's unique ability to quantify confluences. In this script users can set a sensitivity and that sets the number of oscillators that must be in agreement before a signal is allowed to pass.

Here are the oscillators found within the OBOS Heatmap:

*Please keep in mind that although some of these oscillators may have big names, the code and math in the script may work differently than you're used to. This is because the code and math is changed quite a bit, and the overall intended functionality of the OBOS Heatmap has a larger scope than any one indicator. It's also important to note that the lengths for these oscillators are set low and are meant to classify the individual signal as either overbought or oversold, and not the entire period. So while the OBOS Heatmap is awesome for trends and cycles, it's ultimately meant to classify individual price bars as either overbought or oversold according to a consensus.*

Relative Strength Index

Money Flow Index

Commodity Channel Index

Aroon Oscillator

Relative Volatility Index

Fast Stochastic Detrended Price Oscillator

Fast Stochastic Elders Force Index

Fast Stochastic Relative Strength Index

Fast Stochastic Relative Vigor Index

Fast Stochastic Klinger Oscillator

Fast Stochastic Awesome Oscillator

Fast Stochastic Ultimate Oscillator

Fast Stochastic Chande Momentum Oscillator

Fast Stochastic On Balance Volume Oscillator

Fast Stochastic Moving Average Convergence/Divergence

Each band of the Overbought & Oversold Heatmap represents an oscillator. When it's orange it's said to be oversold. When it's yellow it's said to be overbought. The indicator turns purple during trends and reversals where it is neither overbought nor oversold. It can differentiate between uptrends and downtrends with differing colors of purple, but the OBOS Heatmap is not used for trends or cycles in this script. It is used to quantify oversold confluence.

Let's talk about the Dominance Suite.

First note in the top portion of the screenshot above, you will see various colors in the script. It replaces the price line with something we call Price Flow bars. So when you add the script it's best to make the stock price line invisible in TV settings. The Price Flow Bars use a preset EMA to color price action as being in either a downward momentum or upward momentum. The triangular signals represent dark teal for the initial long marker within a series, dark green for long orders and long signals that convert into safety orders, and light green for safety orders. This is more logic that makes this script really unique. The dark green initial long marker signals are rarely seen. You can find them at the beginning of a new series of signals and they work to establish when a new series of signals should begin. The dark green signals actually denote a long base order opportunity, but if a series has already started then these signals are converted into Safety Orders. The Safety Orders then come in light green, and red for Prop Shorts. Prop Shorts work with Initial Longs to establish the start of a new series. More on that math I cannot tell.

In the bottom half of the screenshot is the Dominance Suite itself. It's another one of the four filtering suites found in the script. It is made up of 7 oscillators that work to classify a price bar as being controlled by either the bears or the bulls. If a price bar is controlled by the bears it is said to be a better investment. The Dominance Suite works by applying a moving average to the balance of power. This is the way TradingView has intended the balance of power to be used, and works quite nicely in classifying individual price bars as either bearish or bullish. It's not an overall trend indicator as much as it states whether a bar is mostly controlled by the bears or the bulls.

Here are the oscillators found within the Dominance Suite:

SMA of BOP

EMA of BOP

HMA of BOP

WMA of BOP

VWMA of BOP

TEMA of BOP

LSMA of BOP

Within the script, there is an input for a negative threshold. When each of these 7 oscillators is in confluence and below this set threshold, the Prop Long will be allowed to pass as a real trade.

Keep in mind that each filtering suite also has the option to overload signals.

So not only can you filter signals based on these suites but you can also apply additional volume scaling to signals that don't get filtered.

Here we have the True Oscillator. The True Oscillator is a brand new oscillator. It's similar to things like the RSI or DPO, but technically speaking it considers many more factors into its average than other oscillators. It considers balance of power, sentiment, volume, momentum, gravity, and places special-strategic weighting on price data based on whether it's opening, closing, high, or low. If you stack the True Oscillator up with the RSI you'll notice right away they look similar, but each movement is quite different. Overall the movements are more balanced, the individual bars are more consistent with price data, and the swings are more clearly pronounced while simultaneously having a better register of strength in momentum. We use this indicator to filter and overload signals, to trade according to momentum, and to provide a 16th independent oscillator that can check the OBOS Heatmap without having to be confluent.

The final filtering suite is based on Net Volume. It classifies signals as oversold when there is a significant negative trend in net volume. If Net Volume is under 0, and trends downward for either 3, 4, or 5 bars in a row then it will mark a signal as oversold and allow it to pass. Then, if overloading for this suite is turned on it will allocate more volume to signals it does not filter out.

There is a lot that can be said about this strategy. The primary takeaway though is that it's not just one strategy. It's a tool for everyone, to help them plan their approach to different assets in different market climates. This tool can help you study current market conditions. It can allow you to plan a strategic approach to market segments, and see how your strategy would fare if new market data performed similarly. It's not just one strategy, but more of a strategy printer.

The Origin Suite allows users to plan the positioning of their signals. The Overbought & Oversold Suite allows users to filter their signals based on whether or not they are oversold. The Dominance Suite allows users to filter signals based on whether the market is being controlled by the bears or the bulls. The True Oscillator gives users the ability to filter signals based on a deep and powerful momentum oscillator. The Net Volume Suite lets users filter signals based on volume trends. When signals are filtered, signals that pass, can be overloaded with additional volume scaling. Features like Change-Based Volume Scaling and Position Average Volume Scaling give users plenty of inputs to create complex volume scaling strategies. Common-sense DCA inputs allow users to scale into markets the way pros do.

The Broadview Economic Studio is a powerful tool for planning trades with complex volume scaling strategies.

Users can plan their approach to different kinds of markets. They can link the script with their bot or broker like 3Commas, and the script will automatically send the correct volume scaling through to the bot.

Thank you for your time, and for reading the description of the Broadview Economic Studio.

Waverider [Loxx]Waverider is a momentum strategy that probes historical data to find the optimal entries based on measures of volatility and gaussian adaptive filtering. To accomplish this, after each successful trade, XX trades will be skipped until a specific loss count is achieved after which the strategy will activate again, searching for the next trade.

Features

Select long/short profit target and stoploss by %

Skip weekends

Toggle on/off adaptive divergence detection and forced exit

Momentum Breakout StrategyBacktest a strategy where, when a candlestick on a timeframe rises more than a certain %, it enters a trade.

MomentumSync-PSAR: RSI·ADX Filtered 3-Tier Exit StrategyTriSAR-E3 is a precision swing trading strategy designed to capitalize on early trend reversals using a Triple Confirmation Model. It triggers entries based on an early Parabolic SAR bullish flip, supported by RSI strength and ADX trend confirmation, ensuring momentum-backed participation.

Exits are tactically managed through a 3-step staged exit after a PSAR bearish reversal is detected, allowing gradual profit booking and downside protection.

This balanced approach captures trend moves early while intelligently scaling out, making it suitable for directional traders seeking both agility and control.

Momentum PulseMomentum Pulse Strategy for NIFTY & SENSEX CE/PE Options

This strategy is designed specifically for NIFTY and SENSEX Call (CE) and Put (PE) options. It generates long entry signals and long exits based on momentum filters, making it ideal for options with an opening price between 150-200.

Key Features:

Focus on CE and PE: The strategy should be applied on both CE and PE options of the same index.

Capital Allocation : Use 30% of your capital for CE and 30% for PE positions , ensuring balanced risk distribution.

Entry & Exit : The strategy signals only long entries and long exits based on momentum.

Stop-Loss : A 15% stop-loss is recommended to protect against excessive drawdown.

Note : This strategy is tailored for intraday trading, and it works best when used with disciplined risk management practices.

Strategy Myth-Busting #6 - PSAR+MA+SQZMOM+HVI - [MYN]This is part of a new series we are calling "Strategy Myth-Busting" where we take open public manual trading strategies and automate them. The goal is to not only validate the authenticity of the claims but to provide an automated version for traders who wish to trade autonomously.

Our sixth one we are automating is " I Tested ''7% Profit Per Day" Scalping Strategy 100 Times ( Unexpected Results ) " from " TradeIQ " which claims to have made 175% profit on the 5 min chart of BTCUSD with a having a 61% win rate in just 32 days.

Originally, we mimicked verbatim the indicators and settings TradeIQ was using however weren't getting promising results anything close to the claim so we decided to try and improve on it. We changed the static Parabolic SAR to be adaptive based upon the timeframe. We did this by using an adjustable multiplier for the PSAR Max. Also, In TradeIQ's revised version he substituted Hawkeye's Volume Indicator in lieu of Squeeze Momentum. We found that including both indicators we were getting better results so included them both. Feel free to experiment more. Would love to see how this could be improved on.

This strategy uses a combination of 4 open-source public indicators:

Parabolic Sar (built in)

10 in 1 MA's by hiimannshu

Squeeze Momentum by lazybear

HawkEYE Volume Indicator by lazybear

Trading Rules

5m timeframe and above. We saw equally good results in the higher (3h - 4h) timeframes as well.

Long Entry:

Parabolic Sar shifts below price at last dot above and then previous bar needs to breach above that.

Price action has to be below both MA's and 50MA needs to be above 200MA

Squeeze Momentum needsd to be in green or close to going green

HawkEYE Volume Indicator needs to be show a green bar on the histagram

Short Entry:

Parabolic Sar shifts above price at last dot below and then previous bar needs to breach below that.

Price action needs to be above both MA's and 50MA needs to be below 200MA

Squeeze Momentum needsd to be in red or close to going red

HawkEYE Volume Indicator needs to be show a red bar on the histagram

If you know of or have a strategy you want to see myth-busted or just have an idea for one, please feel free to message me.

Momentum Line StrategyI got the idea of an algorithm using a gap, which would behave a bit like RSI, therefore I called it momentum. Don't know if it's very useful or how to improve it, it can keeps you in trends, however it suffers from whipsawing. My first attempt in programming a strategy.

Profitable Pair Correlation Divergence Scanner v6This strategy identifies divergence opportunities between two correlated assets using a combination of Z-Score spread analysis, trend confirmation, RSI & MACD momentum checks, correlation filters, and ATR-based stop-loss/take-profit management. It’s optimized for positive P&L and realistic trade execution.

Key Features:

Pair Divergence Detection:

Measures deviation between returns of two assets and identifies overbought/oversold spread conditions using Z-Score.

Trend Alignment:

Trades only in the direction of the primary asset’s trend using a fast EMA vs slow EMA filter.

Momentum Confirmation:

Confirms trades with RSI and MACD to reduce false signals.

Correlation Filter:

Ensures the pair is strongly correlated before taking trades, avoiding noisy signals.

Risk Management:

Dynamic ATR-based stop-loss and take-profit ensures proper reward-to-risk ratio.

Exit Conditions:

Automatically closes positions when Z-Score normalizes, or ATR-based exits are hit.

How It Works:

Calculate Returns:

Computes returns for both assets over the selected timeframe.

Z-Score Spread:

Calculates the spread between returns and normalizes it using moving average and standard deviation.

Trend Filter:

Only takes long trades if the fast EMA is above the slow EMA, and short trades if the fast EMA is below the slow EMA.

Momentum Confirmation:

Confirms trade direction with RSI (>50 for longs, <50 for shorts) and MACD alignment.

Correlation Check:

Ensures the pair’s recent correlation is strong enough to validate divergence signals.

Trade Execution:

Opens positions when Z-Score crosses thresholds and all conditions align. Positions close when Z-Score normalizes or ATR-based SL/TP is hit.

Plot Explanation:

Z-Score: Blue line shows divergence magnitude.

Entry Levels: Red/Green lines mark long/short thresholds.

Exit Zone: Gray lines show normalization zone.

EMA Trend Lines: Purple (fast), Orange (slow) for trend alignment.

Correlation: Teal overlay shows current correlation strength.

Usage Tips:

Use highly correlated pairs for best results (e.g., EURUSD/GBPUSD).

Run on higher timeframe charts (1h or 4h) to reduce noise.

Adjust ATR multiplier based on volatility to avoid premature stops.

Combine with alerts for automated notifications or webhook execution.

Conclusion:

The Profitable Pair Correlation Divergence Scanner v6 is designed for traders who want systematic, low-risk, positive P&L trading opportunities with minimal manual monitoring. By combining trend alignment, momentum confirmation, correlation filters, and dynamic exits, it reduces false signals and improves execution reliability.

Run it on TradingView and watch how it captures divergence opportunities while maintaining positive P&L across trades.

Momentum Reversal / Dip Buyer [Score Based]Strategy Overview

Momentum Reversal / Dip Buyer is a quantitative reversal engine designed to fade stretched moves and buy dips / sell rallies when multiple momentum and context factors line up. It’s built for liquid instruments especially for ticker CME_MINI:ES1! and works best on intraday timeframes like the 5-minute or 1-minute chart.

Core Logic

This strategy builds a composite Momentum Score by combining:

Price Location: Relative to 100 SMA, 1000 EMA, and VWAP (trend / regime filter).

RSI: Overbought/oversold and mid-zone strength.

VWMO (Volume-Weighted Momentum): Direction and strength of volume-weighted price drift.

ADX: Trend strength filter (high vs low trend environment).

Full Stoch (%K): Short-term exhaustion and mean-reversion context.

CCI: Overbought/oversold turns (key trigger).

MFI: Volume-confirmed buying/selling pressure.

ATR Regime: High vs low volatility environment.

Cumulative Delta: Whether net aggressor flow is rising or falling.

From this, a single Momentum Score is computed each bar:

Longs: Taken when the score is depressed (scoreLow) and CCI crosses up from oversold.

Shorts: Taken when the score is elevated (scoreHigh) and CCI crosses down from overbought.

Risk Management & Trade Logic

Max Daily Trades: Hard cap on entries per day.

Hard Stop: Fixed % stop based on entry price.

Profit Target: Target ATR Multiplier × main ATR from entry.

Breakeven Logic: Optional; moves stop to breakeven (plus optional offset) after price moves a configurable multiple of the main ATR in your favor.

Trailing Stop (Separate ATR): Optional; uses its own ATR length and ATR-based trigger and distance. This lets you run slower ATR for targets while using a tighter, more reactive ATR for the trail.

Session Control

Trading Window: Optional session filter (e.g., 09:30–16:00). Entries are only allowed inside the defined window.

Force Flat at Session End: Option to automatically close all open positions when the session ends.

Visuals

The script plots entry arrows and a compact dashboard displaying: current Momentum Score, daily trade usage, and CCI status.

Disclaimer:

This script is for educational and research purposes only and is not financial advice. Past performance does not guarantee future results. Always forward-test and adjust parameters to your own risk tolerance and market.

Shoutout and all credit goes to AuclairsCapital for building the base foundation of this strategy on ThinkScript

CSS_LFU_v0.1Overview:

A multi-factor, market-adaptive swing strategy designed for intraday and short-term crypto trading. It synthesizes momentum, volatility, and trend signals into a unified composite score over a configurable lookback window. The strategy leverages a modular, signal-weighted approach to ensure robust entry timing while remaining compatible with human-in-the-loop validation and algorithmic execution.

Core Modules:

AJFFRSI (RSX-based Momentum): Measures smoothed price momentum with noise-reduction filters to detect crossovers relative to the QQE trailing stop.

QQE (Quantitative Qualitative Easing RSI): A modified RSI with a dynamic trailing stop that adapts to short-term volatility, identifying exhaustion and potential reversal points.

Keltner Channel Zones: Determines overextension relative to trend, providing buy/sell zones based on ATR-banded EMA.

WaveTrend Oscillator: Confirms short-term swings and market direction through smoothed oscillator cross signals.

Rolling Composite Score: Aggregates module signals over a unified lookback (e.g., 144 bars) to normalize noise and capture consistent trends.

Signal Logic:

Each module outputs a discrete score (+1 / 0 / -1).

The rolling composite score sums all module scores over the lookback period.

Long positions trigger when the rolling score meets or exceeds the long threshold.

Short positions trigger when the rolling score meets or falls below the short threshold.

Multi-dimensional signal aggregation reduces false positives from single indicators.

Rolling lookback ensures score normalization across different volatility regimes.

Highly modular: easy to adapt modules or weights to different instruments or timeframes.

Fully compatible with automated execution pipelines, including custom exchange screener bots.

Use Case:

Ideal for quant-driven altcoin or multi-asset strategies where high-frequency validation is critical and sequential module weighting enhances trend flip detection.

Advanced Breakout System v2.0Advanced Breakout System v2.0

Developed by: Mohammed Bedaiwi

This script hunts for high-probability breakouts by combining price consolidation zones, volume spikes vs. average volume, smart money flow (OBV), and a Momentum Override for explosive moves that skip consolidation. Additionally, it automatically identifies and plots Support and Resistance levels with price labels to help you visualize market structure.

The system follows a "Watch & Confirm" logic: it first prints a WATCH setup, then a BUY only if price confirms strength.

💡 JUSTIFICATION OF CONCEPTS (MASHUP & ORIGINALITY)

This script is an original mashup combining several analytical concepts to address common breakout failures:

Volatility Compression Engine: Uses built-in functions like ta.highest() and ta.lowest() to mathematically define the setup phase where price volatility is compressed below a user-defined threshold.

Volume Spike Confirmation: The breakout must be confirmed by a volume increase greater than a moving average of volume, signaling strong market interest.

Smart Volume Filter (OBV): This is the key component. By checking if ta.obv is above its own Moving Average, we confirm that accumulation has been occurring during the consolidation period, suggesting institutional positioning before the price break.

Multi-Exit Risk System: Employs dynamic exits (EMA cross, volume dump, bearish pattern) instead of static stop-losses to manage risk adaptively based on real-time market action.

Market Structure Visualization: The script also includes a Support & Resistance engine to plot key swing pivots and price labels for visual context.

✅ STRATEGY RESULTS & POLICY COMPLIANCE

To ensure non-misleading and transparent backtesting results, this strategy is published with the following fully compliant properties:

Dataset Compliance: The backtest is performed on the CMTL Daily (1D) chart across a long history, generating 201 total trades. This significantly exceeds the minimum requirement of 100 trades, providing a robust test dataset.

Risk Control: The strategy uses a conservative order size set to 2% of equity (default_qty_value=2), strictly adhering to the sustainable risk recommendation of 5-10% of equity per trade.

Transaction Costs: Realistic trading conditions are modeled using 0.07% commission and 3 ticks slippage to prevent the overestimation of profitability.

⚙️ VISUAL GUIDE & SIGNAL LOGIC

Key Color Legend (Visual Guide):

WATCH – Setup (Yellow Arrow Down): Potential breakout setup detected.

BUY – Confirmation (Green Arrow Up): Confirmed breakout, triggered when price trades above the high of the WATCH candle.

SELL – Break (Orange Arrow): Short-term trend weakness, triggered when price closes below the Fast EMA (9).

SELL – Dump (Dark Red Arrow): Distribution / volume dump, triggered by a bearish candle with abnormally high volume.

SELL – Pattern (Purple Arrow): Bearish price-action pattern (such as a bearish engulfing).

Support & Resistance Lines (Red/Green): Small horizontal lines plotted at key swing points with exact price labels.

⌨️ INPUTS (DEFAULT SETTINGS)

Entry settings: Consolidation Lookback (default 20) = bars used to detect consolidation. Consolidation Range % (default 12%) = max allowed range size. Volume Spike Multiplier (default 1.2) = factor above average volume to count as a spike. Force Signal on Big Moves (default ON) = forces a WATCH signal on high-momentum moves.

Exit settings: Enable Fast Exit (EMA 9) toggles the SELL – Break signal. Dump Volume Multiplier defines what counts as “dump” volume.

Support & Resistance: Adjustable Pivot Left/Right bars control the sensitivity of the support and resistance lines.

⚠️ Disclaimer Trading involves significant risk of loss. This script is for educational and informational purposes only and is not financial advice or a recommendation to buy or sell any asset. BUY and SELL signals are rule-based and derived from historical behavior and do not guarantee future performance. Always use your own analysis and risk management. This is an open-source strategy; users are encouraged to test it across different symbols and timeframes.