Multiple Liquidity ChannelsSame as liquidity channels but 25 / 50 / 75 levels in the same indicator.

Wyszukaj w skryptach "liquidity"

BTC LL->HH Liquidity Sweep / BOS / Retest / 4H Bias v6_8BTC LL->HH Liquidity Sweep / BOS / Retest / 4H Bias v6_8

Buy vs Sell Liquidity + Difference (Bottom Right)Script Summary (Short Notes)

⚙️ Purpose

Tracks and displays Buy Volume vs Sell Volume difference during the day, based on candle direction.

Useful for spotting liquidity imbalance between buyers and sellers.

📊 How It Works

Volume Classification

If close > open → counts volume as Buy Volume

If close < open → counts volume as Sell Volume

Aggregation Timeframe

You can select a timeframe (1, 2, 3, 5, 15, 30 mins)

Script recalculates data from that aggregation level.

Daily Reset

At the start of a new trading day, totals reset to zero.

Cumulative Calculation

Adds all buy/sell volumes as the day progresses.

Calculates:

Total Volume

Difference (BUY − SELL)

Percentages (%)

Smart Money Concepts Pro – OB, FVG, Liquidity + Trade SetupsThis script is a complete Smart Money Concepts (SMC) toolkit designed for traders who want clean and actionable charts without clutter.

It combines the most important institutional concepts into one indicator:

Order Blocks (OB): auto-detection of bullish and bearish order blocks with mitigation tracking, merging and TTL (time-to-live).

Fair Value Gaps (FVG): automatic gap recognition with size filters, mitigation tracking and lifetime control.

Liquidity Pools (EQH/EQL): equal highs and equal lows marked with tolerance (ATR-based or fixed).

Break of Structure (BOS): up/down structure shifts plotted directly on the chart.

Multi-Timeframe (HTF): option to use higher timeframe data (e.g. H4, Daily) for stronger zones.

Trend Filter: show zones only in the direction of market structure.

Trade Setups: automatic signals for OB Retest + Trend setups, with entry, stop-loss and take-profit levels (custom R-R).

Flexible Zone Extension: choose between extending zones to the live bar or fixed box width for a cleaner look when scrolling.

Features

Fully customizable (pivot length, ATR filters, box width, TTL, zone colors)

Separate presets for Scalping, Intraday, Swing trading styles

Visual trade planning with entry/SL/TP lines and optional labels

Works across all markets (crypto, forex, indices, stocks)

How to use

Bias: identify overall direction (BOS + HTF zones).

Wait: for price to return to an unmitigated OB or FVG.

Entry: take the setup signal (OB retest + trend filter).

Risk: stop-loss at opposite OB boundary.

Target: TP based on chosen R-R multiple (default 2R).

⚡ Whether you scalp short-term moves or swing trade HTF zones, this indicator gives you a clear institutional edge in spotting supply/demand imbalances and high-probability setups.

Mimic liquidity Order Blocks Modifiedits help to find liquidity order block and the bull bear percentage also delta

Stop Hunt Candlesticks (Liquidity Wicks)🕯️ Stop Hunt Candlesticks

Wick Highlighter – Spot Extreme Wicks Instantly

This indicator highlights candles where the upper or lower wick exceeds a customizable percentage of the asset’s price — perfect for quickly spotting strong rejections, liquidity grabs, stop hunts or exhaustion moves.

💡 Key Features

Visual Background Highlight: Automatically colors the chart background when a wick surpasses your defined % threshold (default 1%).

Customizable Threshold: Adjust wick sensitivity to suit different assets or timeframes.

Upper & Lower Wick Filters: Choose whether to track upper wicks, lower wicks, or both.

Dynamic Price Basis: Compare wick size relative to Close, Open, HL2, or OC2.

Optional Labels: Display the exact wick percentage directly on the chart.

Alerts Ready: Get notified whenever a candle shows an extreme wick condition.

⚙️ How It Works

The script measures each candle’s wick size relative to your chosen price basis:

Upper wick % = (High − max(Open, Close)) / Basis × 100

Lower wick % = (min(Open, Close) − Low) / Basis × 100

If the result exceeds your chosen threshold, the chart background changes color.

Red for upper wicks, green for lower wicks by default.

🎯 Use Cases

Identify strong rejections or stop hunts near key levels.

Confirm price exhaustion or potential reversals.

Filter fake breakouts or high-volatility events.

🧩 Customization

Tweak colors, transparency, and label visibility to fit seamlessly into your chart setup.

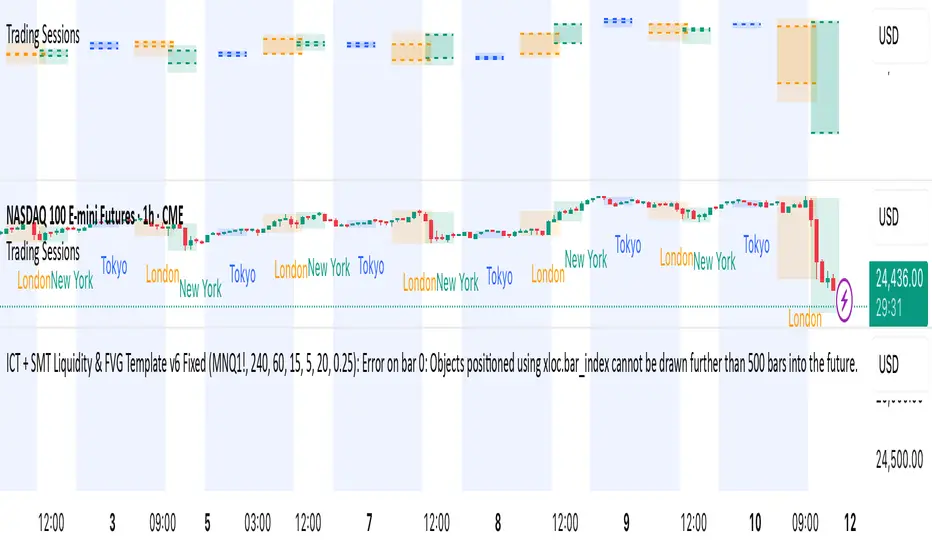

ICT + SMT Liquidity & FVG Template mnqict concepts with smt divergence for mnq. marking out liquidity sweeps, sessions, highs and lows.

Smart Money Volume Activity [AlgoAlpha]🟠 OVERVIEW

This tool visualizes how Smart Money and Retail participants behave through lower-timeframe volume analysis. It detects volume spikes far beyond normal activity, classifies them as institutional or retail, and projects those zones as reactive levels. The script updates dynamically with each bar, showing when large players enter while tracking whether those events remain profitable. Each event is drawn as a horizontal line with bubble markers and summarized in a live P/L table comparing Smart Money versus Retail.

🟠 CONCEPTS

The core logic uses Z-score normalization on lower-timeframe volumes (like 5m inside a 1h chart). This lets the script detect statistically extreme bursts of buying or selling activity. It classifies each detected event as:

Smart Money — volume inside the candle body (suggesting hidden accumulation or distribution)

Retail — volume closing at bar extremes (suggesting chase entries or panic exits)

When new events appear, the script plots them as horizontal levels that persist until price interacts again. Each level acts as a potential reaction zone or liquidity footprint. The integrated P/L table then measures which class (Retail or Smart Money) is currently “winning” — comparing cumulative profitable versus losing volume.

🟠 FEATURES

Classifies flows into Smart Money or Retail based on candle-body context.

Displays live P/L comparison table for Smart vs Retail performance.

Alerts for each detected Smart or Retail buy/sell event.

🟠 USAGE

Setup : Add the script to any chart. Set Lower Timeframe Value (e.g., “5” for 5m) smaller than your main chart timeframe. The Period input controls how many bars are analyzed for the Z-score baseline. The Threshold (|Z|) decides how extreme a volume must be to plot a level.

Read the chart : Horizontal lines mark where heavy Smart or Retail volume occurred. Bright bubbles show the strongest events — their size reflects Z-score intensity. The on-chart table updates live: green cells show profitable flows, red cells show losing flows. A dominant green Smart Money row suggests institutions are currently controlling price.

See what others are doing :

Settings that matter : Raising Threshold (|Z|) filters noise, showing only large players. Increasing Period smooths results but reacts slower to new bursts. Use Show = “Both” for full comparison or isolate “Smart Money” / “Retail” to focus on one class.

Yen Carry Composite Index + Macro Flow GaugeWhat This Indicator Does

This chart visualizes the strength, trend, and macro conditions supporting or weakening the yen carry trade a strategy where investors borrow in low yielding yen to invest in higher yielding assets

How It Works: Core Components

Composite Index (Blue Line):

A weighted blend of z-scores from:

USD/JPY (strength of USD vs JPY)

10Y yield spread (US – Japan)

AUD/JPY (risk proxy for carry appetite)

VIX (global risk sentiment, inverted)

Z-scores normalize each input to show how far it deviates from recent history (not raw values).

Positive composite trend ⬅️ strong carry environment

Negative composite trend ➡️ signs of unwind or stress

Individual Z-Score Lines:

🟥 USD/JPY

🟩 Yield Spread (US10Y − JP10Y)

🟪 FX Proxy (AUD/JPY)

🟦 VIX (risk sentiment)

Threshold Lines & Signal Markers:

Green 🟢⬅️🟢🟢 “carry active” threshold (+1.5 std dev)

Red dashed line 🔴➡️🔴🔴→ “carry unwind risk” (−1.5 std dev)

Carry Trade Strength Gauge (Horizontal Bar, Bottom-Right) www.tradingview.com

Slots:

🟢 = strong carry inflow conditions

⚪ = neutral midpoint

🔴 = outflow / unwind pressure

A directional arrow (⬅️ or ➡️) shows momentum:

➡️ = composite rising → improving carry environment

⬅️ = composite falling → deteriorating carry conditions

Arrow is placed at the current strength level, visually combining position + momentum

Labels “Inflows” and “Outflows” flank the bar for clarity

Use Case Summary

Macro risk overlay for JPY pairs, EM FX, bond carry strategies

Detect early unwind phases (e.g. if arrow ⬅️ appears in red zone)

Confirm entry/exit in directional JPY trades or expected liquidity to enter the markets

Debt Refinance Cycle + Liquidity vs BTC (Wk) — Overlay Part 1Debt Refi Cycle - Overlay script (BTC + Liquidity + DRCI/Z normalized to BTC range)

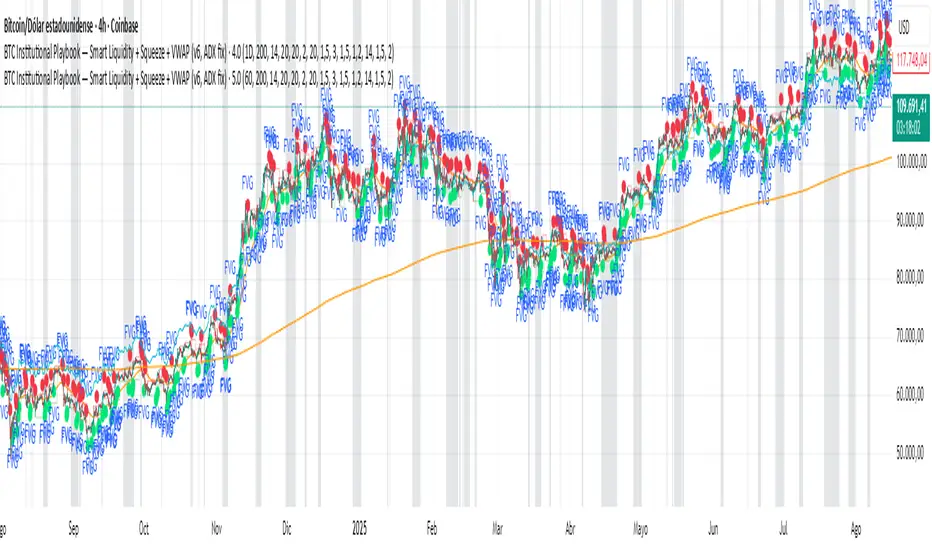

BTC Institutional Playbook Smart Liquidity + SqueezeBTC Institutional Playbook — Smart Liquidity + Squeeze + VWAP (v6, ADX fix)

Samurai Liquidity Hunter ProA professional tool developed by the Samurai team and based on the logic of volume analysis.

It has unique mathematics on the volume delta for easy detection of places on the chart where the most significant liquidity was removed.

These are real ranges of entry and exit of large money, which give us a real advantage in making trading decisions.

Global Liquidity Proxy vs BitcoinGlobal Liquidity Proxy vs Bitcoin. Helps to understand the cycles with liquidty.

Global Liquidity Proxy (Fed + ECB + BoJ + PBoC)Global Liquidity Proxy (Fed + ECB + BoJ + PBoC) Vs BTC

Swing High/Low Levels (Auto Remove)Plots untapped swing high and low levels from higher timeframes. Used for liquidity sweep strategy. Cluster of swing levels are a magnet for price to return to and reverse. Indicator gives option for candle body or wick for sweep to remove lines.

Balanced Big Wicks (50/50) HighlighterThis open-source indicator highlights candles with balanced long wicks (50/50 style)—that is, candles where both upper and lower shadows are each at least 30–60% of the full range and within ~8% of each other, while retaining a substantial body. This specific structure often reflects indecision or liquidity sweeps and can precede strong breakout moves.

How It Works (Inputs and Logic)

Min wick % (each side): 30–60% of candle range

Max body %: up to 60% of range (preserves strong body presence)

Equality tolerance: wicks within 8% of each other

ATR filter (multiples of ATR14): ensures only significant-range candles are flagged

When a “50/50” candle forms, it’s visually colored and labeled; audibly alertable.

How to Use It

Long setup: price closes above the wick-high → potential long entry (SL below wick-low, TP = 1:1).

Short setup: price closes below wick-low → potential short entry (SL above wick-high, TP = 1:1).

Especially effective on 5–15 minute scalping charts when aligned with high-volume sessions or HTF trend context.

Why This Indicator Is Unique

Unlike standard wick or doji voters, this script specifically filters for candles with a strong body and symmetrical wicks, paired with a range filter, reducing noise significantly.

Important Notes

No unrealistic claims: backtested setups indicate high occurrence of clean breakouts, though performance depends on market structure.

Script built responsibly: uses real-time calculations only, no future-data lookahead.

Visuals on the published chart reflect default input values exactly.

Global Sessions with Trend & Liquidity Features:

-Session ranges with customizable lines & colors

-Opening range markers and optional background shading

-Automatic trend detection per session (Bullish / Bearish / Neutral)

-Indicators when highs/lows are broken

-Clean visual design with toggles for minimal or detailed display

This Pine Script code is designed to help traders visualize and analyze different market sessions. It's a tool that displays the trading hours for the Asian, London, and New York sessions right on the chart.

The main purpose is to show when these key markets are open and to highlight their price ranges. It also includes features to track the trend within each session and to identify "liquidity sweeps" or moments when the price breaks the high or low of a previous session.

In simple terms, it helps a trader see what the market is doing and where the price is likely to go, all based on the major global trading times. It's especially useful for day traders who want to align their strategies with the activity of specific markets.

P.S. Apologies to users not in the EST timezone! This version is hardcoded to Eastern Standard Time, and I'm not currently sure how to automatically adjust it for different timezones. But you can adjust manually and click the dropdown menu to Save As Default.

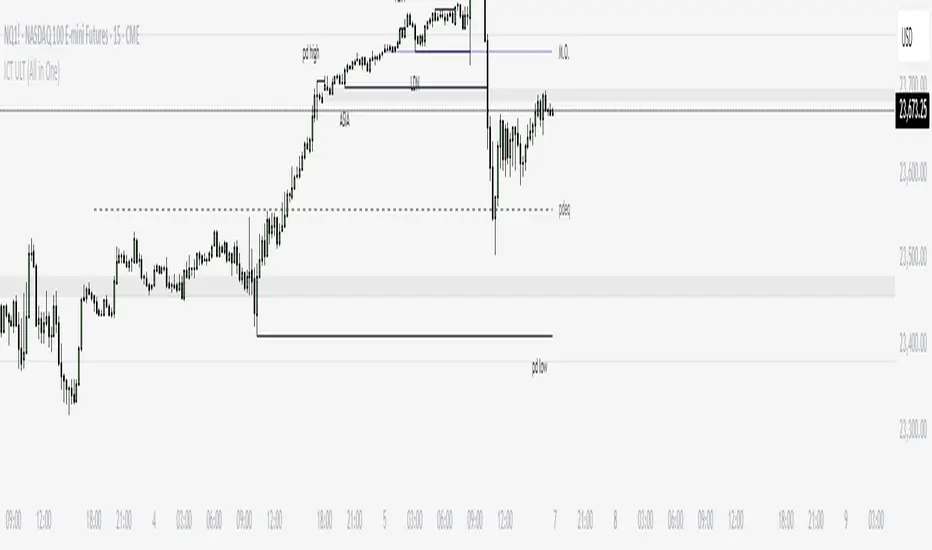

ICT ULT

This indicator is for lazy people like me who want to automate the process of marking certain ICT key levels using the indicator's features, such as:

Custom Killzone/Session Liquidity Levels in form of Highs and Lows

Killzone Drawings (Boxes)

Previous Day High/Low (PDH/PDL)

Previous Day Equlibrium (PDEQ)

Previous Week High/Low

New Day/Week Opening Gaps (NDOG/NWOG)

Custom Opening Prices (horizontal) (e.g. Midnight Open)

Custom Timestamps (vertical)

*Note: All features are completely customizable

inspired by: @tradeforopp

NQ Liquidity + Inverse FVG Strategy Alertsuses inversion FVG's and targets NQ liquidity

hhsajdhds

d

d

d

d

sa

s

a

s

dgasjjekkje

j

k

Combined Liquidity & Session LevelsPlots session highs and lows, as well as lower timeframe liquidity levels

ICT Session High/Low LevelsThis indicator automatically plots the Highs and Lows of completed sessions and draws lines for the Asian session and London session. Levels are displayed only after each session has closed. A simple tool for liquidity work and intraday context (SMC/ICT).

Buy/Sell Volume VWAP with Liquidity and Price SensitivityBuy/Sell Volume VWAP with Liquidity & Price Sensitivity

A dual-VWAP overlay that separates buy-side vs sell-side pressure using lower-timeframe volume and recent price behavior. It shows two adaptive VWAP lines and a bias cloud to make trend and imbalance easy to see—no params fussing required.

What you’ll see

Buy VWAP (green) and Sell VWAP (red) plotted on the chart

Slope-aware coloring : brighter when that side is improving, darker when easing

Bias cloud: green when Buy > Sell, red when Sell > Buy

Optional last-value bubbles on the price scale for quick readouts

How it works

Looks inside each bar (lower timeframe, e.g., 1-second) to estimate buy vs sell pressure

Blends that pressure with recent price movement to keep the lines responsive but stable

Maintains separate VWAP tracks for buy-side and sell-side and resets daily or at a time you choose

How to use it

Trend & bias: When Buy VWAP stays above Sell VWAP (green cloud), buyers have the upper hand; the opposite (red cloud) favors sellers.

Conviction: A wider gap between the two lines often means a stronger imbalance.

Context: Use alongside structure (higher highs/lows, key levels) for confirmation—this is not a stand-alone signal.

Inputs

Timeframe: Lower-TF sampling (default 1S).

Reset Time: Defaults to 09:30 (session open); set to your market.

Appearance: Two-shade palettes for buy/sell, line width, last-value bubbles, and cloud opacity.

Tips

Works on most symbols and intraday timeframes; lower-TF sampling can be heavier on resources.

If the cloud flips frequently, consider viewing on a slightly higher chart timeframe for cleaner structure.

Disclaimer

For educational use only. Not investment advice. Test on replay/paper before live decisions.