Wyszukaj w skryptach "demand"

Supply and Demand ZonesSupply/demand

Best for swings

One can also use the same for intraday by using daily zones

Supply & DemandWe can think of imbalanced as a signal of a huge order being filled.

For those who do not know what imbalanced candle are, an imbalanced candles are formed when the price move with force in a direction.

Taking the last 3 candles, when the wicks the of 1st and 3rd candle does not fully overlap the middle one, an imbalanced candle is formed.

Usually when a huge hands place its order it never gets filled entirely and the price usually comes back to this zone to fulfil the remaining order.

This indicator highlight range defined by previous high and low pivot right before an imbalanced candle.

Zones highlighted become zones to watch to enter a trade and become either supply or demand zone.

Engulfing Detector (Supply and Demand)Bullish and bearish engulfing candles marked with horizontal lines around engulfed candle.

This indicator can be used to assist in locating potential supply and demand zones.

The fresh zones will be of green and red line colors and the tested zone lines are grey in color.

Fear & Greed Index (Zeiierman)█ Overview

The Fear & Greed Index is an indicator that provides a comprehensive view of market sentiment. By analyzing various market factors such as market momentum, stock price strength, stock price breadth, put and call options, junk bond demand, market volatility, and safe haven demand, the Index can depict the overall emotions driving market behavior, categorizing them into two main sentiments: Fear and Greed.

Fear: Indicates a market scenario where investors are scared, possibly leading to a sell-off or a stagnant market. In such conditions, the indicator helps in identifying potential buying opportunities as assets may be undervalued.

Greed: Represents a state where investors are overly confident and buying aggressively, which can lead to inflated asset prices. The indicator in such cases can signal overbought conditions, advising caution or potential short opportunities.

█ How It Works

The Fear & Greed Index is an aggregate of seven distinct indicators, each gauging a specific dimension of stock market activity. These indicators include market momentum, stock price strength, stock price breadth, put and call options, junk bond demand, market volatility, and safe haven demand. The Index assesses the deviation of each individual indicator from its average, in relation to its typical fluctuations. In compiling the final score, which ranges from 0 to 100, the Index assigns equal weight to each indicator. A score of 100 denotes the highest level of Greed, while a score of 0 represents the utmost level of fear.

S&P 500's Momentum: The Index monitors the S&P 500's position relative to its 125-day moving average. Positive momentum (price above the average) signals growing confidence among investors (Greed), while negative momentum (price below the average) indicates rising fear.

Stock Price Strength: By comparing the number of stocks hitting 52-week highs to those at 52-week lows on the NYSE, the Index gauges market breadth. An extreme number of highs indicates Greed, whereas an extreme number of lows suggests Fear.

Stock Price Breadth (Market Volume): Using the McClellan Volume Summation Index, which considers the volume of advancing versus declining stocks, the Index assesses whether the market is broadly participating in a trend, or if a smaller subset of stocks is driving it.

Put and Call Options: The put/call ratio helps gauge investor sentiment. A rising ratio, particularly above 1, indicates increasing fear, as more investors are buying puts to protect against a decline. A falling ratio suggests growing confidence.

Market Volatility (VIX): The VIX measures expected market volatility. Higher values generally indicate Fear, while lower values point to Greed. The Fear & Greed Index compares the VIX to its 50-day moving average to understand its trend.

Safe Haven Demand: The performance of stocks versus bonds over a 20-day period helps understand where investors are putting their money. Bonds outperforming stocks is a sign of Fear, while the opposite suggests Greed.

Junk Bond Demand: By comparing the yields on junk bonds to safer investment-grade bonds, the Index gauges risk appetite. A narrower yield spread suggests Greed (investors are taking more risk), while a wider spread indicates Fear.

The Fear & Greed Index combines these components, scales, and averages them to produce a single value between 0 (Extreme Fear) and 100 (Extreme Greed).

█ How to Use

The Fear & Greed Index serves as a tool to evaluate the prevailing sentiments in the market. Investors, often driven by emotions, can react impulsively, and sentiment indicators like the Fear & Greed Index aim to highlight these emotional states, helping investors recognize personal biases that might impact their investment choices. When integrated with fundamental analysis and additional analytical instruments, the Index becomes a valuable resource for understanding and interpreting market moods and tendencies.

The Fear & Greed Index operates on the principle that excessive fear can result in stocks trading well below their intrinsic values,

while uncontrolled Greed can push prices above what they should be.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

Credit Spread RegimeThe Credit Market as Economic Barometer

Credit spreads are among the most reliable leading indicators of economic stress. When corporations borrow money by issuing bonds, investors demand a premium above the risk-free Treasury rate to compensate for the possibility of default. This premium, known as the credit spread, fluctuates based on perceptions of economic health, corporate profitability, and systemic risk.

The relationship between credit spreads and economic activity has been studied extensively. Two papers form the foundation of this indicator. Pierre Collin-Dufresne, Robert Goldstein, and Spencer Martin published their influential 2001 paper in the Journal of Finance, documenting that credit spread changes are driven by factors beyond firm-specific credit quality. They found that a substantial portion of spread variation is explained by market-wide factors, suggesting credit spreads contain information about aggregate economic conditions.

Simon Gilchrist and Egon Zakrajsek extended this research in their 2012 American Economic Review paper, introducing the concept of the Excess Bond Premium. They demonstrated that the component of credit spreads not explained by default risk alone is a powerful predictor of future economic activity. Elevated excess spreads precede recessions with remarkable consistency.

What Credit Spreads Reveal

Credit spreads measure the difference in yield between corporate bonds and Treasury securities of similar maturity. High yield bonds, also called junk bonds, carry ratings below investment grade and offer higher yields to compensate for greater default risk. Investment grade bonds have lower yields because the probability of default is smaller.

The spread between high yield and investment grade bonds is particularly informative. When this spread widens, investors are demanding significantly more compensation for taking on credit risk. This typically indicates deteriorating economic expectations, tighter financial conditions, or increasing risk aversion. When the spread narrows, investors are comfortable accepting lower premiums, signaling confidence in corporate health.

The Gilchrist-Zakrajsek research showed that credit spreads contain two distinct components. The first is the expected default component, which reflects the probability-weighted cost of potential defaults based on corporate fundamentals. The second is the excess bond premium, which captures additional compensation demanded beyond expected defaults. This excess premium rises when investor risk appetite declines and financial conditions tighten.

The Implementation Approach

This indicator uses actual option-adjusted spread data from the Federal Reserve Economic Database (FRED), available directly in TradingView. The ICE BofA indices represent the industry standard for measuring corporate bond spreads.

The primary data sources are FRED:BAMLH0A0HYM2, the ICE BofA US High Yield Index Option-Adjusted Spread, and FRED:BAMLC0A0CM, the ICE BofA US Corporate Index Option-Adjusted Spread for investment grade bonds. These indices measure the spread of corporate bonds over Treasury securities of similar duration, expressed in basis points.

Option-adjusted spreads account for embedded options in corporate bonds, providing a cleaner measure of credit risk than simple yield spreads. The methodology developed by ICE BofA is widely used by institutional investors and central banks for monitoring credit conditions.

The indicator offers two modes. The HY-IG excess spread mode calculates the difference between high yield and investment grade spreads, isolating the pure compensation for below-investment-grade credit risk. This measure is less affected by broad interest rate movements. The HY-only mode tracks the absolute high yield spread, capturing both credit risk and the overall level of risk premiums in the market.

Interpreting the Regimes

Credit conditions are classified into four regimes based on Z-scores calculated from the spread proxy.

The Stress regime occurs when spreads reach extreme levels, typically above a Z-score of 2.0. At this point, credit markets are pricing in significant default risk and economic deterioration. Historically, stress regimes have coincided with recessions, financial crises, and major market dislocations. The 2008 financial crisis, the 2011 European debt crisis, the 2016 commodity collapse, and the 2020 pandemic all triggered credit stress regimes.

The Elevated regime, between Z-scores of 1.0 and 2.0, indicates above-normal risk premiums. Credit conditions are tightening. This often occurs in the build-up to stress events or during periods of uncertainty. Risk management should be heightened, and exposure to credit-sensitive assets may be reduced.

The Normal regime covers Z-scores between -1.0 and 1.0. This represents typical credit conditions where spreads fluctuate around historical averages. Standard investment approaches are appropriate.

The Low regime occurs when spreads are compressed below a Z-score of -1.0. Investors are accepting below-average compensation for credit risk. This can indicate complacency, strong economic confidence, or excessive risk-taking. While often associated with favorable conditions, extremely tight spreads sometimes precede sudden reversals.

Credit Cycle Dynamics

Beyond static regime classification, the indicator tracks the direction and acceleration of spread movements. This reveals where credit markets stand in the credit cycle.

The Deteriorating phase occurs when spreads are elevated and continuing to widen. Credit conditions are actively worsening. This phase often precedes or coincides with economic downturns.

The Recovering phase occurs when spreads are elevated but beginning to narrow. The worst may be over. Credit conditions are improving from stressed levels. This phase often accompanies the early stages of economic recovery.

The Tightening phase occurs when spreads are low and continuing to compress. Credit conditions are very favorable and improving further. This typically occurs during strong economic expansions but may signal building complacency.

The Loosening phase occurs when spreads are low but beginning to widen from compressed levels. The extremely favorable conditions may be normalizing. This can be an early warning of changing sentiment.

Relationship to Economic Activity

The predictive power of credit spreads for economic activity is well-documented. Gilchrist and Zakrajsek found that the excess bond premium predicts GDP growth, industrial production, and unemployment rates over horizons of one to four quarters.

When credit spreads spike, the cost of corporate borrowing increases. Companies may delay or cancel investment projects. Reduced investment leads to slower growth and eventually higher unemployment. The transmission mechanism runs from financial conditions to real economic activity.

Conversely, tight credit spreads lower borrowing costs and encourage investment. Easy credit conditions support economic expansion. However, excessively tight spreads may encourage over-leveraging, planting seeds for future stress.

Practical Application

For equity investors, credit spreads provide context for market risk. Equities and credit often move together because both reflect corporate health. Rising credit spreads typically accompany falling stock prices. Extremely wide spreads historically have coincided with equity market bottoms, though timing the reversal remains challenging.

For fixed income investors, spread regimes guide sector allocation decisions. During stress regimes, flight to quality favors Treasuries over corporates. During low regimes, spread compression may offer limited additional return for credit risk, suggesting caution on high yield.

For macro traders, credit spreads complement other indicators of financial conditions. Credit stress often leads equity volatility, providing an early warning signal. Cross-asset strategies may use credit regime as a filter for position sizing.

Limitations and Considerations

FRED data updates with a lag, typically one business day for the ICE BofA indices. For intraday trading decisions, more current proxies may be necessary. The data is most reliable on daily timeframes.

Credit spreads can remain at extreme levels for extended periods. Mean reversion signals indicate elevated probability of normalization but do not guarantee timing. The 2008 crisis saw spreads remain elevated for many months before normalizing.

The indicator is calibrated for US credit markets. Application to other regions would require different data sources such as European or Asian credit indices. The relationship between spreads and subsequent economic activity may vary across market cycles and structural regimes.

References

Collin-Dufresne, P., Goldstein, R.S., and Martin, J.S. (2001). The Determinants of Credit Spread Changes. Journal of Finance, 56(6), 2177-2207.

Gilchrist, S., and Zakrajsek, E. (2012). Credit Spreads and Business Cycle Fluctuations. American Economic Review, 102(4), 1692-1720.

Krishnamurthy, A., and Muir, T. (2017). How Credit Cycles across a Financial Crisis. Working Paper, Stanford University.

Polynomial Regression Bands + Channel [DW]This is an experimental study designed to calculate polynomial regression for any order polynomial that TV is able to support.

This study aims to educate users on polynomial curve fitting, and the derivation process of Least Squares Moving Averages (LSMAs).

I also designed this study with the intent of showcasing some of the capabilities and potential applications of TV's fantastic new array functions.

Polynomial regression is a form of regression analysis in which the relationship between the independent variable x and the dependent variable y is modeled as a polynomial of nth degree (order).

For clarification, linear regression can also be described as a first order polynomial regression. The process of deriving linear, quadratic, cubic, and higher order polynomial relationships is all the same.

In addition, although deriving a polynomial regression equation results in a nonlinear output, the process of solving for polynomials by least squares is actually a special case of multiple linear regression.

So, just like in multiple linear regression, polynomial regression can be solved in essentially the same way through a system of linear equations.

In this study, you are first given the option to smooth the input data using the 2 pole Super Smoother Filter from John Ehlers.

I chose this specific filter because I find it provides superior smoothing with low lag and fairly clean cutoff. You can, of course, implement your own filter functions to see how they compare if you feel like experimenting.

Filtering noise prior to regression calculation can be useful for providing a more stable estimation since least squares regression can be rather sensitive to noise.

This is especially true on lower sampling lengths and higher degree polynomials since the regression output becomes more "overfit" to the sample data.

Next, data arrays are populated for the x-axis and y-axis values. These are the main datasets utilized in the rest of the calculations.

To keep the calculations more numerically stable for higher periods and orders, the x array is filled with integers 1 through the sampling period rather than using current bar numbers.

This process can be thought of as shifting the origin of the x-axis as new data emerges.

This keeps the axis values significantly lower than the 10k+ bar values, thus maintaining more numerical stability at higher orders and sample lengths.

The data arrays are then used to create a pseudo 2D matrix of x power sums, and a vector of x power*y sums.

These matrices are a representation the system of equations that need to be solved in order to find the regression coefficients.

Below, you'll see some examples of the pattern of equations used to solve for our coefficients represented in augmented matrix form.

For example, the augmented matrix for the system equations required to solve a second order (quadratic) polynomial regression by least squares is formed like this:

(∑x^0 ∑x^1 ∑x^2 | ∑(x^0)y)

(∑x^1 ∑x^2 ∑x^3 | ∑(x^1)y)

(∑x^2 ∑x^3 ∑x^4 | ∑(x^2)y)

The augmented matrix for the third order (cubic) system is formed like this:

(∑x^0 ∑x^1 ∑x^2 ∑x^3 | ∑(x^0)y)

(∑x^1 ∑x^2 ∑x^3 ∑x^4 | ∑(x^1)y)

(∑x^2 ∑x^3 ∑x^4 ∑x^5 | ∑(x^2)y)

(∑x^3 ∑x^4 ∑x^5 ∑x^6 | ∑(x^3)y)

This pattern continues for any n ordered polynomial regression, in which the coefficient matrix is a n + 1 wide square matrix with the last term being ∑x^2n, and the last term of the result vector being ∑(x^n)y.

Thanks to this pattern, it's rather convenient to solve the for our regression coefficients of any nth degree polynomial by a number of different methods.

In this script, I utilize a process known as LU Decomposition to solve for the regression coefficients.

Lower-upper (LU) Decomposition is a neat form of matrix manipulation that expresses a 2D matrix as the product of lower and upper triangular matrices.

This decomposition method is incredibly handy for solving systems of equations, calculating determinants, and inverting matrices.

For a linear system Ax=b, where A is our coefficient matrix, x is our vector of unknowns, and b is our vector of results, LU Decomposition turns our system into LUx=b.

We can then factor this into two separate matrix equations and solve the system using these two simple steps:

1. Solve Ly=b for y, where y is a new vector of unknowns that satisfies the equation, using forward substitution.

2. Solve Ux=y for x using backward substitution. This gives us the values of our original unknowns - in this case, the coefficients for our regression equation.

After solving for the regression coefficients, the values are then plugged into our regression equation:

Y = a0 + a1*x + a1*x^2 + ... + an*x^n, where a() is the ()th coefficient in ascending order and n is the polynomial degree.

From here, an array of curve values for the period based on the current equation is populated, and standard deviation is added to and subtracted from the equation to calculate the channel high and low levels.

The calculated curve values can also be shifted to the left or right using the "Regression Offset" input

Changing the offset parameter will move the curve left for negative values, and right for positive values.

This offset parameter shifts the curve points within our window while using the same equation, allowing you to use offset datapoints on the regression curve to calculate the LSMA and bands.

The curve and channel's appearance is optionally approximated using Pine's v4 line tools to draw segments.

Since there is a limitation on how many lines can be displayed per script, each curve consists of 10 segments with lengths determined by a user defined step size. In total, there are 30 lines displayed at once when active.

By default, the step size is 10, meaning each segment is 10 bars long. This is because the default sampling period is 100, so this step size will show the approximate curve for the entire period.

When adjusting your sampling period, be sure to adjust your step size accordingly when curve drawing is active if you want to see the full approximate curve for the period.

Note that when you have a larger step size, you will see more seemingly "sharp" turning points on the polynomial curve, especially on higher degree polynomials.

The polynomial functions that are calculated are continuous and differentiable across all points. The perceived sharpness is simply due to our limitation on available lines to draw them.

The approximate channel drawings also come equipped with style inputs, so you can control the type, color, and width of the regression, channel high, and channel low curves.

I also included an input to determine if the curves are updated continuously, or only upon the closing of a bar for reduced runtime demands. More about why this is important in the notes below.

For additional reference, I also included the option to display the current regression equation.

This allows you to easily track the polynomial function you're using, and to confirm that the polynomial is properly supported within Pine.

There are some cases that aren't supported properly due to Pine's limitations. More about this in the notes on the bottom.

In addition, I included a line of text beneath the equation to indicate how many bars left or right the calculated curve data is currently shifted.

The display label comes equipped with style editing inputs, so you can control the size, background color, and text color of the equation display.

The Polynomial LSMA, high band, and low band in this script are generated by tracking the current endpoints of the regression, channel high, and channel low curves respectively.

The output of these bands is similar in nature to Bollinger Bands, but with an obviously different derivation process.

By displaying the LSMA and bands in tandem with the polynomial channel, it's easy to visualize how LSMAs are derived, and how the process that goes into them is drastically different from a typical moving average.

The main difference between LSMA and other MAs is that LSMA is showing the value of the regression curve on the current bar, which is the result of a modelled relationship between x and the expected value of y.

With other MA / filter types, they are typically just averaging or frequency filtering the samples. This is an important distinction in interpretation. However, both can be applied similarly when trading.

An important distinction with the LSMA in this script is that since we can model higher degree polynomial relationships, the LSMA here is not limited to only linear as it is in TV's built in LSMA.

Bar colors are also included in this script. The color scheme is based on disparity between source and the LSMA.

This script is a great study for educating yourself on the process that goes into polynomial regression, as well as one of the many processes computers utilize to solve systems of equations.

Also, the Polynomial LSMA and bands are great components to try implementing into your own analysis setup.

I hope you all enjoy it!

--------------------------------------------------------

NOTES:

- Even though the algorithm used in this script can be implemented to find any order polynomial relationship, TV has a limit on the significant figures for its floating point outputs.

This means that as you increase your sampling period and / or polynomial order, some higher order coefficients will be output as 0 due to floating point round-off.

There is currently no viable workaround for this issue since there isn't a way to calculate more significant figures than the limit.

However, in my humble opinion, fitting a polynomial higher than cubic to most time series data is "overkill" due to bias-variance tradeoff.

Although, this tradeoff is also dependent on the sampling period. Keep that in mind. A good rule of thumb is to aim for a nice "middle ground" between bias and variance.

If TV ever chooses to expand its significant figure limits, then it will be possible to accurately calculate even higher order polynomials and periods if you feel the desire to do so.

To test if your polynomial is properly supported within Pine's constraints, check the equation label.

If you see a coefficient value of 0 in front of any of the x values, reduce your period and / or polynomial order.

- Although this algorithm has less computational complexity than most other linear system solving methods, this script itself can still be rather demanding on runtime resources - especially when drawing the curves.

In the event you find your current configuration is throwing back an error saying that the calculation takes too long, there are a few things you can try:

-> Refresh your chart or hide and unhide the indicator.

The runtime environment on TV is very dynamic and the allocation of available memory varies with collective server usage.

By refreshing, you can often get it to process since you're basically just waiting for your allotment to increase. This method works well in a lot of cases.

-> Change the curve update frequency to "Close Only".

If you've tried refreshing multiple times and still have the error, your configuration may simply be too demanding of resources.

v4 drawing objects, most notably lines, can be highly taxing on the servers. That's why Pine has a limit on how many can be displayed in the first place.

By limiting the curve updates to only bar closes, this will significantly reduce the runtime needs of the lines since they will only be calculated once per bar.

Note that doing this will only limit the visual output of the curve segments. It has no impact on regression calculation, equation display, or LSMA and band displays.

-> Uncheck the display boxes for the drawing objects.

If you still have troubles after trying the above options, then simply stop displaying the curve - unless it's important to you.

As I mentioned, v4 drawing objects can be rather resource intensive. So a simple fix that often works when other things fail is to just stop them from being displayed.

-> Reduce sampling period, polynomial order, or curve drawing step size.

If you're having runtime errors and don't want to sacrifice the curve drawings, then you'll need to reduce the calculation complexity.

If you're using a large sampling period, or high order polynomial, the operational complexity becomes significantly higher than lower periods and orders.

When you have larger step sizes, more historical referencing is used for x-axis locations, which does have an impact as well.

By reducing these parameters, the runtime issue will often be solved.

Another important detail to note with this is that you may have configurations that work just fine in real time, but struggle to load properly in replay mode.

This is because the replay framework also requires its own allotment of runtime, so that must be taken into consideration as well.

- Please note that the line and label objects are reprinted as new data emerges. That's simply the nature of drawing objects vs standard plots.

I do not recommend or endorse basing your trading decisions based on the drawn curve. That component is merely to serve as a visual reference of the current polynomial relationship.

No repainting occurs with the Polynomial LSMA and bands though. Once the bar is closed, that bar's calculated values are set.

So when using the LSMA and bands for trading purposes, you can rest easy knowing that history won't change on you when you come back to view them.

- For those who intend on utilizing or modifying the functions and calculations in this script for their own scripts, I included debug dialogues in the script for all of the arrays to make the process easier.

To use the debugs, see the "Debugs" section at the bottom. All dialogues are commented out by default.

The debugs are displayed using label objects. By default, I have them all located to the right of current price.

If you wish to display multiple debugs at once, it will be up to you to decide on display locations at your leisure.

When using the debugs, I recommend commenting out the other drawing objects (or even all plots) in the script to prevent runtime issues and overlapping displays.

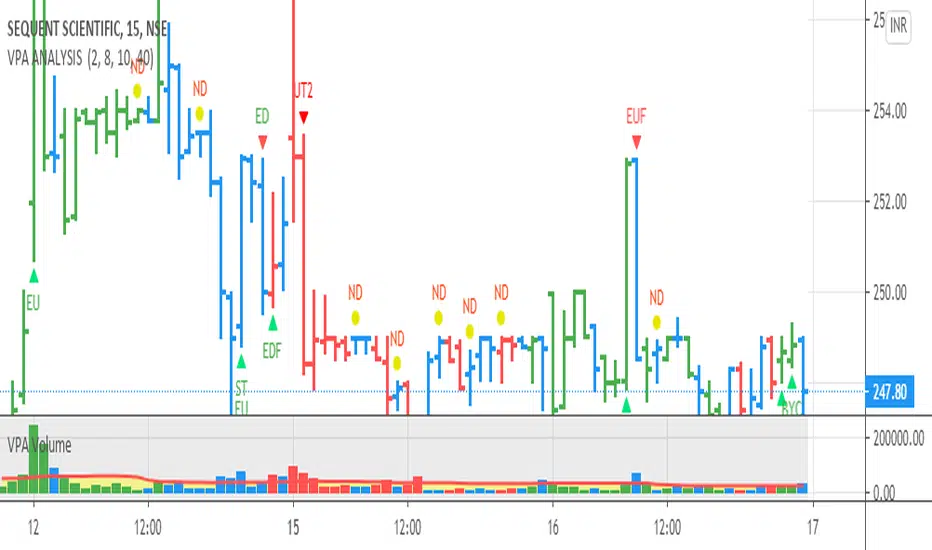

VPA ANALYSIS VPA Analysis provide the indications for various conditions as per the Volume Spread Analysis concept. The various legends are provided below

LEGEND DETAILS

UT1 - Upthrust Bar: This will be widespread Bar on high Volume closing on the low. This normally happens after an up move. Here the smart money move the price to the High and then quickly brings to the Low trapping many retail trader who rushed into in order not to miss the bullish move. This is a bearish Signal

UT2 -Upthrust Bar Confirmation: A widespread Down Bar following a Upthrust Bar. This confirms the weakness of the Upthrust Bar. Expect the stock to move down

Confirms . This is a Bearish Signal

PUT - Pseudo Upthrust: An Upthrust Bar in bar action but the volume remains average. This still indicates weakness. Indicate Possible Bearishness

PUC -Pseudo Upthrust Confirmation: widespread Bar after a pseudo–Upthrust Bar confirms the weakness of the Pseudo Upthrust Bar

Confirms Bearishness

BC - Buying Climax: A very wide Spread bar on ultra-High Volume closing at the top. Such a Bar indicates the climatic move in an uptrend. This Bar traps many retailers as the uptrend ends and reverses quickly. Confirms Bearishness

TC - Trend Change: This Indicates a possible Trend Change in an uptrend. Indicates Weakness

SEC- Sell Condition: This bar indicates confluence of some bearish signals. Possible end of Uptrend and start of Downtrend soon. Bearish Signal

UT - Upthrust Condition: When multiple bearish signals occur, the legend is printed in two lines. The Legend “UT” indicates that an upthrust condition is present. Bearish Signal

ND - No demand in uptrend: This bar indicates that there is no demand. In an uptrend this indicates weakness. Bearish Signal

ND - No Demand: This bar indicates that there is no demand. This can occur in any part of the Trend. In all place other than in an uptrend this just indicates just weakness

ED - Effort to Move Down: Widespread Bar closing down on High volume or above average volume . The smart money is pushing the prices down. Bearish Signal

EDF - Effort to Move Down Failed: Widespread / above average spread Bar closing up on High volume or above average volume appearing after ‘Effort to move down” bar.

This indicates that the Effort to move the pries down has failed. Bullish signal

SV - Stopping Volume: A high volume medium to widespread Bar closing in the upper middle part in a down trend indicates that smart money is buying. This is an indication that the down trend is likely to end soon. Indicates strength

ST1 - Strength Returning 1: Strength seen returning after a down trend. High volume adds to strength. Indicates Strength

ST2 - Strength Returning 2: Strength seen returning after a down trend. High volume adds to strength.

BYC - Buy Condition: This bar indicates confluence of some bullish signals Possible end of downtrend and start of uptrend soon. Indicates Strength

EU - Effort to Move Up: Widespread Bar closing up on High volume or above average volume . The smart money is pushing the prices up. Bullish Signal

EUF - Effort to Move Up Failed: Widespread / above average spread Bar closing down on High volume or above average volume appearing after ‘Effort to move up” bar.

This indicates that the Effort to move the pries up has failed. Bearish Signal

LVT- Low Volume Test: A low volume bar dipping into previous supply area and closing in the upper part of the Bar. A successful test is a positive sign. Indicates Strength

ST(after a LVT ) - Strength after Successful Low Volume Test: An up Bar closing near High after a Test confirms strength. Bullish Signal

RUT - Reverse Upthrust Bar: This will be a widespread Bar on high Volume closing on the high is a Down Trend. Here the buyers have become active and move the prices from the low to High. The down Move is likely to end and up trend likely to start soon. indicates Strength

NS - No supply Bar: This bar indicates that there is no supply. This is a sign of strength especially in a down trend. Indicates strength

ST - Strength Returns: When multiple bullish signals occur, the legend is printed in two lines. The Legend “ST” indicates that an condition of strength other than the condition mentioned in the second line is present. Bullish Signals

BAR COLORS

Green- Bullish / Strength

Red - Bearish / weakness

Blue / White - Sentiment Changing from bullish to Bearish and Vice Versa

RSI Analytic Volume Matrix [RAVM] Overview

RSI Analytic Volume Matrix is an overlay indicator that turns classic RSI into a multi-layered market-reading engine. Instead of treating RSI 30 and 70 as simple buy/sell lines, RAVM combines RSI geometry (angle and acceleration), statistical volume analysis, and a 5×5 VSA-inspired matrix to describe what is really happening inside each candle.

The script is designed as an educational and analytical tool. It does not generate trading signals. Instead, it helps you read the market context, understand where the pressure is coming from (buyers vs. sellers), and see how price, momentum, and volume interact in real time.

Concept & Philosophy

RAVM is built around a hierarchical logic and a few core ideas:

• Hierarchical State Machine: First, RSI defines a context (where we are in the 0–100 range). Then the geometric engine evaluates the angle-of-turn of RSI using a Z-Score. Only after a meaningful geometric event is detected does the system promote a bar to a potential setup (warning vs. confirmed).

• Geometric Primacy: The angle and acceleration of RSI (RSI geometry) are more important than the raw RSI level itself. RAVM uses a geometric veto: if the geometric trigger is not confirmed, the confidence score is capped below 50%, even if volume looks interesting.

• RSI Beyond 30 and 70: Being above 70 or below 30 is not treated as an automatic overbought/oversold signal. RAVM treats those zones as contextual factors that contribute only a partial portion of the final score, alongside geometry, total volume expansion, buy/sell balance, and delta power.

• Volume Decomposition: Volume is decomposed into total, buy-side, sell-side, and delta components. Each of these is normalized with a Z-Score over a shared statistical window, so RSI geometry and volume live in the same statistical context.

• Educational Scoring Pipeline: RAVM builds a 0–100 "Quantum Score" for each detected setup. The score expresses how strong the story is across four dimensions: geometry (RSI angle-of-turn), total volume expansion, which side is driving that volume (buyers vs. sellers), and the power of delta. The score is designed for learning and weighting, not for mechanical trade entries.

• VSA Matrix Engine: A 5×5 matrix combines momentum states and volume dynamics. Each cell corresponds to an interpreted VSA-style scenario (Absorption, Distribution, No Demand, Stopping Volume, Strong Reversal, etc.), shown both as text and as a heatmap dashboard on the chart.

How RAVM Works

1. RSI Context & Geometry

RAVM starts with a classic RSI, but it does not stop at simple level checks. It computes the velocity and acceleration of RSI and normalizes them via a Z-Score to produce an Angle-of-Turn metric (Z-AoT). This Z-AoT is then mapped into a 0–1 intensity value called MSI (Momentum Shift Intensity).

The script monitors both classic RSI zones (around 30 and 70) and geometric triggers. Entering the lower or upper zone is treated as a contextual event only. A setup becomes "confirmed" when a significant geometric turn is detected (based on Z-AoT thresholds). Otherwise, the bar is at most a warning.

2. Volume & Statistical Engine

The volume engine can work in two modes: a geometric approximation (based on candle structure) or a more precise intrabar mode using up/down volume requests. In both cases, RAVM builds a volume packet consisting of:

• Total volume

• Buy-side volume

• Sell-side volume

• Delta (buy – sell)

Each of these series is normalized using a Z-Score over the same statistical window that is used for RSI geometry. This allows RAVM to answer questions such as: Is total volume exceptional on this bar? Is the expansion mostly coming from buyers or from sellers? Is delta unusually strong or weak compared to recent history?

3. Scoring System (Quantum Score)

For each bar where a setup is active, RAVM computes a 0–100 score intended as an educational confidence measure. The scoring pipeline follows this sequence:

A. RSI Geometry (MSI): Measures the strength of the RSI angle-of-turn via Z-AoT. This has geometric primacy over simple level checks.

B. RSI Zone Context: Being below 30 or above 70 contributes only a partial bonus to the score, reflecting the idea that these zones are context, not automatic signals. Mildly supportive zones (e.g., RSI below 50 for bullish contexts) can also contribute with lower weight.

C. Total Volume Expansion: A normalized Volume Power term expresses how exceptional the total volume is relative to its recent distribution. If there is no meaningful volume expansion, the score remains modest even if RSI geometry looks interesting.

D. Which Side Is Driving the Volume: RAVM then checks whether the expansion is primarily on the buy side or the sell side, using Z-Score statistics for buy and sell volume separately. This stage does not yet rely on delta as a power metric; it simply answers the question: "Is this expansion mostly driven by buyers, sellers, or both?"

E. Delta as Final Power: Only at the final stage does the script bring in delta and its Z-Score as a measure of how one-sided the pressure really is. A strong negative delta during a bullish context, for example, can highlight absorption, while a strong positive delta against a bearish context can highlight distribution or a buying climax.

If a setup is not geometrically confirmed (for example, a simple entry into RSI 30/70 without a strong geometric turn), RAVM caps the final score below 50%. This "Geometric Veto" enforces the idea that RSI geometry must confirm before a scenario can be considered high-confidence.

4. Overlay UI & Smart Labels

RAVM is an overlay indicator: all information is drawn directly on the price chart, not in a separate pane. When a setup is active, a smart label is attached to the bar, together with a vertical connector line. Each label shows:

• Direction of the setup (bullish or bearish)

• Trigger type (classic OS/OB vs. geometric/hidden)

• Status (warning vs. confirmed)

• Quantum Score as a percentage

Confirmed setups use stronger colors and solid connectors, while warnings use softer colors and dotted connectors. The script also manages label placement to avoid overlap, keeping the chart clean and readable.

In addition to labels, a dashboard table is drawn on the chart. It displays the currently active matrix scenario, the dominant bias, a short textual interpretation, the full 5×5 heatmap, and summary metrics such as RSI, MSI, and Volume Power.

RSI Is Not Just 30 and 70

One of the central design decisions in RAVM is to treat RSI 30 and 70 as context, not as fixed buy/sell buttons. Many traders mechanically assume that RSI below 30 means "buy" and RSI above 70 means "sell". RAVM explicitly rejects this simplification.

Instead, the script asks a series of deeper questions: How sharp is the angle-of-turn of RSI right now? Is total volume expanding or contracting? Is that expansion dominated by buyers or sellers? Is delta confirming the move, or is there a hidden absorption or distribution taking place?

In the scoring logic, being in a lower or upper RSI zone contributes only part of the final score. Geometry, volume expansion, the buy/sell split, and delta power all have to align before a high-confidence scenario emerges. This makes RAVM much closer to a structured market-reading tool than a classic overbought/oversold indicator.

Matrix User Manual – Reading the 5×5 Grid

The heart of RAVM is its 5×5 matrix, where the vertical axis represents momentum states (M1–M5) and the horizontal axis represents volume dynamics (V1–V5). Each cell in this grid corresponds to a VSA-style scenario. The dashboard highlights the currently active cell and prints a textual description so you can read the story at a glance.

1. Confirmation Scenarios

These scenarios occur when momentum direction and volume expansion are aligned:

• Bullish Confirmation / Strong Reversal: Momentum is shifting strongly upward (often from a depressed RSI context), and expanded volume is driven mainly by buyers. Often seen as a strong bullish reversal or continuation signal from a VSA perspective.

• Bearish Confirmation / Strong Drop: Momentum is turning decisively downward, and expanded volume is driven mainly by sellers. This maps to strong bearish continuation or sharp reversal patterns.

2. Absorption & Stopping Volume

• Absorption: Total volume expands, but the dominant flow is opposite to the recent price move or the geometric bias. For example, heavy selling volume while the geometric context is bullish. This can indicate smart money quietly absorbing orders from the crowd.

• Stopping Volume: Exceptionally high volume appears near the end of an extended move, while momentum begins to decelerate. Price may still print new extremes, but the effort vs. result relationship signals potential exhaustion and the possibility of a turn.

3. Distribution & Buying Climax

• Distribution: Heavy buying volume appears within a bearish or topping context. Rather than healthy accumulation, this often represents larger players offloading inventory to late buyers. The matrix will typically flag this as a bearish-leaning scenario despite strong upside prints.

• Buying Climax: A surge of buy-side volume near the end of a strong uptrend, with momentum starting to weaken. From a VSA point of view, this is often the last push where retail aggressively buys what smart money is selling.

4. No Demand & No Supply

• No Demand: Price attempts to rise but does so on low, non-expansive volume. The market is not interested in following the move, and the lack of participation often precedes weakness or sideways action.

• No Supply: Price tries to push lower on thin volume. Selling pressure is limited, and the lack of supply can precede stabilization or recovery if buyers step back in.

5. Trend Exhaustion

• Uptrend Exhaustion: Momentum remains nominally bullish, but the quality of volume deteriorates (e.g., more effort, less net result). The matrix marks this as an uptrend losing internal strength, often after a series of aggressive moves.

• Downtrend Exhaustion: Similar logic in the opposite direction: strong prior downtrend, but increasingly inefficient downside progress relative to the volume invested. This can precede accumulation or a relief rally.

6. Effort vs. Result Scenarios

• Bullish Effort, Little Result: Buyers invest notable volume, but price progress is limited. This may reveal hidden selling into strength or a lack of follow-through from the broader market.

• Bearish Effort, Little Result: Sellers push volume, but price does not decline proportionally. This can indicate absorption of selling pressure and potential underlying demand.

7. Neutral, Churn & Thin Markets

• Neutral / Thin Market: Momentum and volume both remain muted. RAVM marks these as neutral cells where aggressive decision-making is usually less attractive and observing the broader structure is more important.

• High Volume Churn / Volatility: Both sides are active with high volume but limited directional progress. This can correspond to battle zones, local ranges, or high volatility rotations where the main message is conflict rather than clear trend.

Inputs & Options

RAVM includes several input groups to adapt the tool to your preferences:

• Localization: Multiple language options for all labels and dashboard text (e.g., English, Farsi, Turkish, Russian).

• RSI Core Settings: RSI length, source, and upper/lower contextual zones (typically around 30 and 70).

• Geometric Engine: Z-AoT sigma thresholds, confirmation ratios, and normalization window multiplier. These control how sensitive the script is to RSI angle-of-turn events.

• Volume Engine: Choice between geometric approximation and intrabar up/down volume, Z-Score thresholds for volume expansion, and related parameters.

• Visual Interface: Toggles for smart labels, dashboard table, font sizes, dashboard position, and color themes for bullish, bearish, and warning states.

Disclaimer

RSI Analytic Volume Matrix is provided for educational and research purposes only. It does not constitute financial advice and is not a signal generator. Any trading decisions you make based on this tool, or any other, are entirely your own responsibility. Always consider your own risk management rules and conduct your own analysis.

Langlands-Operadic Möbius Vortex (LOMV)Langlands-Operadic Möbius Vortex (LOMV)

Where Pure Mathematics Meets Market Reality

A Revolutionary Synthesis of Number Theory, Category Theory, and Market Dynamics

🎓 THEORETICAL FOUNDATION

The Langlands-Operadic Möbius Vortex represents a groundbreaking fusion of three profound mathematical frameworks that have never before been combined for market analysis:

The Langlands Program: Harmonic Analysis in Markets

Developed by Robert Langlands (Fields Medal recipient), the Langlands Program creates bridges between number theory, algebraic geometry, and harmonic analysis. In our indicator:

L-Function Implementation:

- Utilizes the Möbius function μ(n) for weighted price analysis

- Applies Riemann zeta function convergence principles

- Calculates quantum harmonic resonance between -2 and +2

- Measures deep mathematical patterns invisible to traditional analysis

The L-Function core calculation employs:

L_sum = Σ(return_val × μ(n) × n^(-s))

Where s is the critical strip parameter (0.5-2.5), controlling mathematical precision and signal smoothness.

Operadic Composition Theory: Multi-Strategy Democracy

Category theory and operads provide the mathematical framework for composing multiple trading strategies into a unified signal. This isn't simple averaging - it's mathematical composition using:

Strategy Composition Arity (2-5 strategies):

- Momentum analysis via RSI transformation

- Mean reversion through Bollinger Band mathematics

- Order Flow Polarity Index (revolutionary T3-smoothed volume analysis)

- Trend detection using Directional Movement

- Higher timeframe momentum confirmation

Agreement Threshold System: Democratic voting where strategies must reach consensus before signal generation. This prevents false signals during market uncertainty.

Möbius Function: Number Theory in Action

The Möbius function μ(n) forms the mathematical backbone:

- μ(n) = 1 if n is a square-free positive integer with even number of prime factors

- μ(n) = -1 if n is a square-free positive integer with odd number of prime factors

- μ(n) = 0 if n has a squared prime factor

This creates oscillating weights that reveal hidden market periodicities and harmonic structures.

🔧 COMPREHENSIVE INPUT SYSTEM

Langlands Program Parameters

Modular Level N (5-50, default 30):

Primary lookback for quantum harmonic analysis. Optimized by timeframe:

- Scalping (1-5min): 15-25

- Day Trading (15min-1H): 25-35

- Swing Trading (4H-1D): 35-50

- Asset-specific: Crypto 15-25, Stocks 30-40, Forex 35-45

L-Function Critical Strip (0.5-2.5, default 1.5):

Controls Riemann zeta convergence precision:

- Higher values: More stable, smoother signals

- Lower values: More reactive, catches quick moves

- High frequency: 0.8-1.2, Medium: 1.3-1.7, Low: 1.8-2.3

Frobenius Trace Period (5-50, default 21):

Galois representation lookback for price-volume correlation:

- Measures harmonic relationships in market flows

- Scalping: 8-15, Day Trading: 18-25, Swing: 25-40

HTF Multi-Scale Analysis:

Higher timeframe context prevents trading against major trends:

- Provides market bias and filters signals

- Improves win rates by 15-25% through trend alignment

Operadic Composition Parameters

Strategy Composition Arity (2-5, default 4):

Number of algorithms composed for final signal:

- Conservative: 4-5 strategies (higher confidence)

- Moderate: 3-4 strategies (balanced approach)

- Aggressive: 2-3 strategies (more frequent signals)

Category Agreement Threshold (2-5, default 3):

Democratic voting minimum for signal generation:

- Higher agreement: Fewer but higher quality signals

- Lower agreement: More signals, potential false positives

Swiss-Cheese Mixing (0.1-0.5, default 0.382):

Golden ratio φ⁻¹ based blending of trend factors:

- 0.382 is φ⁻¹, optimal for natural market fractals

- Higher values: Stronger trend following

- Lower values: More contrarian signals

OFPI Configuration:

- OFPI Length (5-30, default 14): Order Flow calculation period

- T3 Smoothing (3-10, default 5): Advanced exponential smoothing

- T3 Volume Factor (0.5-1.0, default 0.7): Smoothing aggressiveness control

Unified Scoring System

Component Weights (sum ≈ 1.0):

- L-Function Weight (0.1-0.5, default 0.3): Mathematical harmony emphasis

- Galois Rank Weight (0.1-0.5, default 0.2): Market structure complexity

- Operadic Weight (0.1-0.5, default 0.3): Multi-strategy consensus

- Correspondence Weight (0.1-0.5, default 0.2): Theory-practice alignment

Signal Threshold (0.5-10.0, default 5.0):

Quality filter producing:

- 8.0+: EXCEPTIONAL signals only

- 6.0-7.9: STRONG signals

- 4.0-5.9: MODERATE signals

- 2.0-3.9: WEAK signals

🎨 ADVANCED VISUAL SYSTEM

Multi-Dimensional Quantum Aura Bands

Five-layer resonance field showing market energy:

- Colors: Theme-matched gradients (Quantum purple, Holographic cyan, etc.)

- Expansion: Dynamic based on score intensity and volatility

- Function: Multi-timeframe support/resistance zones

Morphism Flow Portals

Category theory visualization showing market topology:

- Green/Cyan Portals: Bullish mathematical flow

- Red/Orange Portals: Bearish mathematical flow

- Size/Intensity: Proportional to signal strength

- Recursion Depth (1-8): Nested patterns for flow evolution

Fractal Grid System

Dynamic support/resistance with projected L-Scores:

- Multiple Timeframes: 10, 20, 30, 40, 50-period highs/lows

- Smart Spacing: Prevents level overlap using ATR-based minimum distance

- Projections: Estimated signal scores when price reaches levels

- Usage: Precise entry/exit timing with mathematical confirmation

Wick Pressure Analysis

Rejection level prediction using candle mathematics:

- Upper Wicks: Selling pressure zones (purple/red lines)

- Lower Wicks: Buying pressure zones (purple/green lines)

- Glow Intensity (1-8): Visual emphasis and line reach

- Application: Confluence with fractal grid creates high-probability zones

Regime Intensity Heatmap

Background coloring showing market energy:

- Black/Dark: Low activity, range-bound markets

- Purple Glow: Building momentum and trend development

- Bright Purple: High activity, strong directional moves

- Calculation: Combines trend, momentum, volatility, and score intensity

Six Professional Themes

- Quantum: Purple/violet for general trading and mathematical focus

- Holographic: Cyan/magenta optimized for cryptocurrency markets

- Crystalline: Blue/turquoise for conservative, stability-focused trading

- Plasma: Gold/magenta for high-energy volatility trading

- Cosmic Neon: Bright neon colors for maximum visibility and aggressive trading

📊 INSTITUTIONAL-GRADE DASHBOARD

Unified AI Score Section

- Total Score (-10 to +10): Primary decision metric

- >5: Strong bullish signals

- <-5: Strong bearish signals

- Quality ratings: EXCEPTIONAL > STRONG > MODERATE > WEAK

- Component Analysis: Individual L-Function, Galois, Operadic, and Correspondence contributions

Order Flow Analysis

Revolutionary OFPI integration:

- OFPI Value (-100% to +100%): Real buying vs selling pressure

- Visual Gauge: Horizontal bar chart showing flow intensity

- Momentum Status: SHIFTING, ACCELERATING, STRONG, MODERATE, or WEAK

- Trading Application: Flow shifts often precede major moves

Signal Performance Tracking

- Win Rate Monitoring: Real-time success percentage with emoji indicators

- Signal Count: Total signals generated for frequency analysis

- Current Position: LONG, SHORT, or NONE with P&L tracking

- Volatility Regime: HIGH, MEDIUM, or LOW classification

Market Structure Analysis

- Möbius Field Strength: Mathematical field oscillation intensity

- CHAOTIC: High complexity, use wider stops

- STRONG: Active field, normal position sizing

- MODERATE: Balanced conditions

- WEAK: Low activity, consider smaller positions

- HTF Trend: Higher timeframe bias (BULL/BEAR/NEUTRAL)

- Strategy Agreement: Multi-algorithm consensus level

Position Management

When in trades, displays:

- Entry Price: Original signal price

- Current P&L: Real-time percentage with risk level assessment

- Duration: Bars in trade for timing analysis

- Risk Level: HIGH/MEDIUM/LOW based on current exposure

🚀 SIGNAL GENERATION LOGIC

Balanced Long/Short Architecture

The indicator generates signals through multiple convergent pathways:

Long Entry Conditions:

- Score threshold breach with algorithmic agreement

- Strong bullish order flow (OFPI > 0.15) with positive composite signal

- Bullish pattern recognition with mathematical confirmation

- HTF trend alignment with momentum shifting

- Extreme bullish OFPI (>0.3) with any positive score

Short Entry Conditions:

- Score threshold breach with bearish agreement

- Strong bearish order flow (OFPI < -0.15) with negative composite signal

- Bearish pattern recognition with mathematical confirmation

- HTF trend alignment with momentum shifting

- Extreme bearish OFPI (<-0.3) with any negative score

Exit Logic:

- Score deterioration below continuation threshold

- Signal quality degradation

- Opposing order flow acceleration

- 10-bar minimum between signals prevents overtrading

⚙️ OPTIMIZATION GUIDELINES

Asset-Specific Settings

Cryptocurrency Trading:

- Modular Level: 15-25 (capture volatility)

- L-Function Precision: 0.8-1.3 (reactive to price swings)

- OFPI Length: 10-20 (fast correlation shifts)

- Cascade Levels: 5-7, Theme: Holographic

Stock Index Trading:

- Modular Level: 25-35 (balanced trending)

- L-Function Precision: 1.5-1.8 (stable patterns)

- OFPI Length: 14-20 (standard correlation)

- Cascade Levels: 4-5, Theme: Quantum

Forex Trading:

- Modular Level: 35-45 (smooth trends)

- L-Function Precision: 1.6-2.1 (high smoothing)

- OFPI Length: 18-25 (disable volume amplification)

- Cascade Levels: 3-4, Theme: Crystalline

Timeframe Optimization

Scalping (1-5 minute charts):

- Reduce all lookback parameters by 30-40%

- Increase L-Function precision for noise reduction

- Enable all visual elements for maximum information

- Use Small dashboard to save screen space

Day Trading (15 minute - 1 hour):

- Use default parameters as starting point

- Adjust based on market volatility

- Normal dashboard provides optimal information density

- Focus on OFPI momentum shifts for entries

Swing Trading (4 hour - Daily):

- Increase lookback parameters by 30-50%

- Higher L-Function precision for stability

- Large dashboard for comprehensive analysis

- Emphasize HTF trend alignment

🏆 ADVANCED TRADING STRATEGIES

The Mathematical Confluence Method

1. Wait for Fractal Grid level approach

2. Confirm with projected L-Score > threshold

3. Verify OFPI alignment with direction

4. Enter on portal signal with quality ≥ STRONG

5. Exit on score deterioration or opposing flow

The Regime Trading System

1. Monitor Aether Flow background intensity

2. Trade aggressively during bright purple periods

3. Reduce position size during dark periods

4. Use Möbius Field strength for stop placement

5. Align with HTF trend for maximum probability

The OFPI Momentum Strategy

1. Watch for momentum shifting detection

2. Confirm with accelerating flow in direction

3. Enter on immediate portal signal

4. Scale out at Fibonacci levels

5. Exit on flow deceleration or reversal

⚠️ RISK MANAGEMENT INTEGRATION

Mathematical Position Sizing

- Use Galois Rank for volatility-adjusted sizing

- Möbius Field strength determines stop width

- Fractal Dimension guides maximum exposure

- OFPI momentum affects entry timing

Signal Quality Filtering

- Trade only STRONG or EXCEPTIONAL quality signals

- Increase position size with higher agreement levels

- Reduce risk during CHAOTIC Möbius field periods

- Respect HTF trend alignment for directional bias

🔬 DEVELOPMENT JOURNEY

Creating the LOMV was an extraordinary mathematical undertaking that pushed the boundaries of what's possible in technical analysis. This indicator almost didn't happen. The theoretical complexity nearly proved insurmountable.

The Mathematical Challenge

Implementing the Langlands Program required deep research into:

- Number theory and the Möbius function

- Riemann zeta function convergence properties

- L-function analytical continuation

- Galois representations in finite fields

The mathematical literature spans decades of pure mathematics research, requiring translation from abstract theory to practical market application.

The Computational Complexity

Operadic composition theory demanded:

- Category theory implementation in Pine Script

- Multi-dimensional array management for strategy composition

- Real-time democratic voting algorithms

- Performance optimization for complex calculations

The Integration Breakthrough

Bringing together three disparate mathematical frameworks required:

- Novel approaches to signal weighting and combination

- Revolutionary Order Flow Polarity Index development

- Advanced T3 smoothing implementation

- Balanced signal generation preventing directional bias

Months of intensive research culminated in breakthrough moments when the mathematics finally aligned with market reality. The result is an indicator that reveals market structure invisible to conventional analysis while maintaining practical trading utility.

🎯 PRACTICAL IMPLEMENTATION

Getting Started

1. Apply indicator with default settings

2. Select appropriate theme for your markets

3. Observe dashboard metrics during different market conditions

4. Practice signal identification without trading

5. Gradually adjust parameters based on observations

Signal Confirmation Process

- Never trade on score alone - verify quality rating

- Confirm OFPI alignment with intended direction

- Check fractal grid level proximity for timing

- Ensure Möbius field strength supports position size

- Validate against HTF trend for bias confirmation

Performance Monitoring

- Track win rate in dashboard for strategy assessment

- Monitor component contributions for optimization

- Adjust threshold based on desired signal frequency

- Document performance across different market regimes

🌟 UNIQUE INNOVATIONS

1. First Integration of Langlands Program mathematics with practical trading

2. Revolutionary OFPI with T3 smoothing and momentum detection

3. Operadic Composition using category theory for signal democracy

4. Dynamic Fractal Grid with projected L-Score calculations

5. Multi-Dimensional Visualization through morphism flow portals

6. Regime-Adaptive Background showing market energy intensity

7. Balanced Signal Generation preventing directional bias

8. Professional Dashboard with institutional-grade metrics

📚 EDUCATIONAL VALUE

The LOMV serves as both a practical trading tool and an educational gateway to advanced mathematics. Traders gain exposure to:

- Pure mathematics applications in markets

- Category theory and operadic composition

- Number theory through Möbius function implementation

- Harmonic analysis via L-function calculations

- Advanced signal processing through T3 smoothing

⚖️ RESPONSIBLE USAGE

This indicator represents advanced mathematical research applied to market analysis. While the underlying mathematics are rigorously implemented, markets remain inherently unpredictable.

Key Principles:

- Use as part of comprehensive trading strategy

- Implement proper risk management at all times

- Backtest thoroughly before live implementation

- Understand that past performance does not guarantee future results

- Never risk more than you can afford to lose

The mathematics reveal deep market structure, but successful trading requires discipline, patience, and sound risk management beyond any indicator.

🔮 CONCLUSION

The Langlands-Operadic Möbius Vortex represents a quantum leap forward in technical analysis, bringing PhD-level pure mathematics to practical trading while maintaining visual elegance and usability.

From the harmonic analysis of the Langlands Program to the democratic composition of operadic theory, from the number-theoretic precision of the Möbius function to the revolutionary Order Flow Polarity Index, every component works in mathematical harmony to reveal the hidden order within market chaos.

This is more than an indicator - it's a mathematical lens that transforms how you see and understand market structure.

Trade with mathematical precision. Trade with the LOMV.

*"Mathematics is the language with which God has written the universe." - Galileo Galilei*

*In markets, as in nature, profound mathematical beauty underlies apparent chaos. The LOMV reveals this hidden order.*

— Dskyz, Trade with insight. Trade with anticipation.

BTC - Cycle Integrity Index (CII) BTC - Cycle Integrity Index (CII) | RM

Are we following a calendar or a capital flow? Is the Halving still the heartbeat of Bitcoin, or has the institutional "Engine" taken over?

The most polarized debate in the digital asset space today centers on a single question: Is the 4-year Halving Cycle dead? While some market participants wait for a pre-ordained calendar countdown, the reality of 2026 suggests that visual guesswork is no longer sufficient. As institutional gravity takes hold, we cannot rely on the simple "Clock" of the past. Instead, we must audit the Integrity of the present.

The Cycle Integrity Index (CII) was engineered to move beyond simple price action and provide a clinical answer to the market's biggest mystery: "Is this trend supported by structural substance, or is it merely speculative foam?" By aggregating eight diverse Pillars into a single 0-100% score, this model uses Gaussian Distributions and Sigmoid Normalization to distinguish between professional accumulation and retail-driven chaos. We aren't guessing where we are in a cycle; we are measuring the internal health of the asset's engine in real-time.

Why these 8 Pillars?

The CII does not rely on a single indicator because the "New Era" of Bitcoin is multi-dimensional. To capture the full picture, I selected eight specific pillars that cover the three layers of market truth:

• The Capital Layer: Global Liquidity (M2) and ETF Flows (Wall Street Absorption).

• The Network Layer: Mining Difficulty and Security Backbone expansion.

• The Sentiment Layer: Long-Term Holder conviction, Valuation Heat (MVRV), and Corporate Adoption (MSTR). While alternatives like the Pi Cycle or RSI exist, they are often "one-dimensional." The CII is a synthesis—a modular engine where every part validates the others.

How the Calculation Works

The CII is a sophisticated model for Bitcoin. It aggregates 8 diverse pillars into a single 0-100% score in the following way:

• Mathematical Normalization: We don't just use raw prices. We use Gaussian Distributions to find "Institutional DNA" in drawdowns and Sigmoid (S-Curve) functions to score volatility and valuation.

• Dynamic Weighting: The index is modular. If a data source (like a specific on-chain metric) is toggled off, the engine automatically redistributes the weight among the active sensors so the final integrity score is always balanced to 100%.

• Multi-Source Integration: The script pulls from Global Liquidity (M2), ETF flows, Corporate Treasury premiums (MSTR), and Network Difficulty to create a truly "Full-Stack" view of the asset.

The 8 Pillars of Integrity

Pillar 1: Drawdown DNA The "Identity Crisis" Filter

• Concept: Audits the depth of corrections to distinguish between "Institutional Floors" and "Retail Panics."

• Logic: Historically, retail crashes reached -80%, while institutions view -20% to -25% as primary value entries.

• Implementation: Uses a Gaussian (Normal) Distribution centered at -25%. Scores of 10/10 are awarded for holding institutional targets; scores decay as drawdowns accelerate toward legacy "crash" levels.

Basis: DNA Drawdown

Pillar 2: Volatility Regime The "Smoothness" Audit

• Concept: Measures the "vibration" of the trend. High-integrity moves are characterized by "smooth" price action.

• Logic: Erratic volatility signals speculative bubbles; consistent "volatility clusters" indicate professional trend-following.

• Implementation: Calculates a Z-Score of the 14-day ATR against a 100-day benchmark. This is passed through a Sigmoid function to penalize "chaotic" price shocks while rewarding stability.

Basis: RVPM

Pillar 3: Liquidity Sync (Global M2) The Macro Heartbeat

• Concept: Audits whether price growth is fueled by monetary expansion or internal speculative leverage.

• Logic: True cycle integrity requires a positive correlation between Central Bank balance sheets and price action.

• Implementation: Aggregates a custom Global Liquidity Proxy (Fed, RRP, TGA, PBoC, ECB, BoJ). It measures the Pearson Correlation between BTC and M2 with a standardized 80-day transmission lag.

Basis: Liquisync

Pillar 4: ETF Absorption (Wall Street Entry) The "Cost Basis" Defense

• Concept: Tracks the aggregate institutional cost-basis since the January 2024 Spot ETF launch.

• Logic: Integrity is high when the "Wall Street Floor" is defended; it fails when the aggregate position is underwater.

• Implementation: A Cumulative VWAP engine tracking the "Big 3" (IBIT, FBTC, BITB). Scoring decays based on the percentage distance the price drifts below this institutional average entry.

Basis: Institutional Cost Corridor

Note: Turning this to OFF will significantly expand the timeframe of the indicator on the chart (otherwise it will just start in 2024)

Pillar 5: LTH Dormancy (Conviction) The HODL Floor Audit

• Concept: Monitors the conviction of Long-Term Holders (LTH) to identify supply-side constraints.

• Logic: Sustainable cycles require stable or increasing 1Y+ dormant supply; rapid "thawing" signals distribution.

• Implementation: Uses Min-Max Normalization on the Active 1Y Supply over a 252-day window. A score of 10/10 indicates peak annual holding conviction.

Basis: RHODL Proxy & VDD Multiple

Pillar 6: Valuation Intensity The MVRV Heat Map

• Concept: Measures market "overheat" by comparing Market Value to Realized Value.

• Logic: High integrity trends rise steadily; vertical spikes in MVRV indicate "speculative foam" and bubble risk.

• Implementation: Performs a Relative Rank Analysis of the MVRV Ratio over a 730-day window, passed through a high-steepness Sigmoid curve to identify extreme valuation anomalies.

Pillar 7: Miner Stress The Security Backbone

• Concept: Tracks Mining Difficulty to ensure network infrastructure is expanding alongside price.

• Logic: Difficulty expansion signals health; drops in difficulty (Miner Stress) signal capitulation and sell-side pressure.

• Implementation: Monitors the 30-day Rate of Change (ROC) of Global Mining Difficulty. Maintains a 10/10 score during expansion; decays rapidly during network contraction.

Pillar 8: Corporate Adoption The MSTR NAV Proxy

• Concept: Audits the MicroStrategy (MSTR) premium as a barometer for institutional demand.

• Logic: A high premium indicates a willingness to pay a "convenience fee" for BTC exposure; a collapsing premium signals waning appetite.

• Implementation: Calculates the Adjusted Enterprise Value (Market Cap + Debt - Cash) relative to the Net Asset Value (NAV) of its BTC holdings.

Note1: Debt and share parameters are user-adjustable to maintain accuracy as corporate balance sheets evolve.

Note2: I just included this because I was curious about the mNAV calculation I saw in other scripts, where the printed value often does not match exactly the propagated value from the MSTR page itself. Hence, for my live calculation, we calculate the Adjusted Enterprise Value to find the "Market NAV" (mNAV). Unlike simpler scripts that only look at Market Cap vs. Bitcoin holdings, our engine accounts for the Capital Structure . We explicitly factor in the corporate debt (approx. $8.24B long-term + $7.95B convertible notes) and subtract the cash reserves (approx. $2.18B) to find the true cost Wall Street is paying for the underlying Bitcoin. Since this will ran "old" very quickly, I recommend to update in the code by yourself from time to time, or just de-select this parameter.

Interpretation Guide

• Score 100% (The Perfect Storm): This represents a state of "Maximum Integrity." All 8 pillars are in perfect institutional alignment—liquidity is surging, conviction is at yearly highs, and price action is perfectly smooth. This is the hallmark of a healthy, structural parabolic run.

• 75% - 100% (High Integrity): Robust trend. Price is supported by structural demand and macro tailwinds.

• 35% - 75% (Equilibrium): Transition zone. The market is digesting gains or waiting for a new liquidity pulse.

• 0% - 35% (Fragile): Speculative foam. Structural support has failed.

• Score 0% (The Ghost Trend): Absolute structural failure. All pillars (liquidity, miners, LTH, ETFs) have broken down. Note: Due to the robust nature of the Bitcoin network, the index naturally floors around 20-30% during deep bear markets, as specific pillars (like Miner Security) rarely drop to zero.

To provide a complete experience, I have included the Cycle Triad —a visualization layer consisting of the Halving, Ideal Peak, and Ideal Low. It is important to understand the role of this feature:

• Benchmark Only (Not Calculated): The Triad is based purely on historical evidence from previous Bitcoin epochs. While the Halving is fixed anyway, the "Ideal Peak" or "Ideal Low" are not calculated or computed by the 8 pillars. These are user-adjustable temporal anchors drawn on the chart to provide a static map of the "Legacy 4-Year Cycle."

• The Temporal Audit: The power of the CII lies in comparing the Engine (the 8 Pillars) against the Clock (the Triad) . By overlaying historical time-windows on top of our integrity math, we can see if the "New Era" is currently ahead of, behind, or perfectly in sync with the past.

• The "Peak Divergence" Logic: Based on the specific models selected for this ECU—specifically Volatility Decay and Valuation Heat —traders will notice that a cycle peak often coincides with a low integrity score (Red Zone) . While the index measures structural health, a low score is a byproduct of a market that has become "too hot to handle."

• Regime Detection: Although the primary goal is to audit the "New Era," the CII is highly effective at detecting overheated regimes. When the score drops toward the 25–35% range, the structural floor is giving way to speculative foam—making it a dual-purpose tool for both cycle analysis and risk management.

Dashboard Calibration & Settings

Cycle Triad Calibration

• Ideal Peak/Trough Window: Defines the historical "Average Days" from a Halving to the cycle top and bottom. This sets the vertical anchors for the Halving, Peak, and Low labels.

• Show Cycle Triad: A master toggle to enable or disable the temporal lines and labels on your dashboard.

The CII Master ECU is fully modular. You can toggle individual pillars ON/OFF to focus on specific market dimensions, and calibrate the sensitivity of each sensor to match your strategic bias.

• P1: Drawdown DNA Lookback (Weeks): Defines the window for the "Rolling High." Inst. Target (%): The specific percentage drawdown you define as "Institutional Support" (e.g., -25%).

• P2: Volatility Regime Benchmark (Days): The historical window used to define "Normal" vs. "Abnormal" volatility.

• P3: Liquidity Sync Corr. Window (Bars): The lookback for the Pearson Correlation calculation. Transmission Lag (Bars): The delay (standard 80 days) for Central Bank M2 to hit price.

• P4: ETF Absorption FBTC Ticker: The data source for the ETF volume audit (Default: CBOE:FBTC).

• P5: LTH Dormancy LTH Source: The ticker for 1Y+ Active Supply (Default: GLASSNODE:BTC_ACTIVE1Y). Norm. Window: The lookback (252 days) used to rank current conviction.

• P6: Valuation Intensity MVRV Source: The ticker for the MVRV Ratio (Default: INTOTHEBLOCK:BTC_MVRV). Relative Window: The lookback (730 days) to calculate the valuation rank.

• P7: Miner Stress Mining Diff: The data source for Global Mining Difficulty (Default: QUANDL:BCHAIN/DIFF).

• P8: Corporate Adoption Shares (M) & BTC (K): The balance sheet parameters for MicroStrategy (MSTR). Update these as the company executes new purchases to maintain mNAV accuracy.

Operational Usage This index is best used on the Daily (D) (recommended - description for inputs optimized for this time-window) or Weekly (W) timeframes. While the code is optimized to fetch daily data regardless of your chart setting, the structural "Integrity" of a cycle is a macro phenomenon and should be viewed with a medium-to-long-term lens.

The Verdict: Is the 4-Year Cycle Still Alive?

Based on the data provided by the CII Master ECU, the answer remains a nuanced "Work in Progress." The evidence presents a fascinating conflict between legacy patterns and the new institutional regime:

• The Case for the Cycle: Historically, a local "Peak" in price corresponds with a "Local Low" in our integrity indicator (Red Zone). We observed this exact phenomenon in October 2025. When viewed through the lens of the "Ideal Peak" anchor, this alignment suggests that the 4-year temporal rhythm is still exerts a massive influence on market behavior.

• The Case for the New Era: While the timing of the October 2025 peak followed the legacy script, the intensity did not. Previous cycle tops produced far more aggressive and persistent "Red Zone" clusters. The relative brevity of the integrity breakdown suggests that the "Institutional Era" provides a much higher floor than the retail-driven bubbles of 2017 and 2021.

• The Institutional Floor: Our data shows that while "Tops" still resemble the 4-year cycle, the "Lows" now reflect a regime of constant institutional absorption. This suggests that the brutal 80% drawdowns of the past may be replaced by the "Institutional DNA" of Pillar 1.