VDUB_BINARY_PRO_3NEW UPDATED BINARY PRO 3_V2 HERE -

VDUB_BINARY_PRO_3_V1 UPGRADE from binary PRO 1 / testing/ / experimental / Trade the curves / Highs -Lows / Band cross over/ Testing using heikin ashi

//Linear Regression Curve

//Centre band

//CM_Gann Swing HighLow V2/Modified////// MA input NOT WORKING ! - I broke it :s

//Vdub_Tetris_V2/ Modified

*Update Tip /Optional

Set the centre band to '34 to run centre line

Wyszukaj w skryptach "curve"

Advanced Speedometer Gauge [PhenLabs]Advanced Speedometer Gauge

Version: PineScript™v6

📌 Description

The Advanced Speedometer Gauge is a revolutionary multi-metric visualization tool that consolidates 13 distinct trading indicators into a single, intuitive speedometer display. Instead of cluttering your workspace with multiple oscillators and panels, this gauge provides a unified interface where you can switch between different metrics while maintaining consistent visual interpretation.

Built on PineScript™ v6, the indicator transforms complex technical calculations into an easy-to-read semi-circular gauge with color-coded zones and a precision needle indicator. Each of the 13 available metrics has been carefully normalized to a 0-100 scale, ensuring that whether you’re analyzing RSI, volume trends, or volatility extremes, the visual interpretation remains consistent and intuitive.

The gauge is designed for traders who value efficiency and clarity. By consolidating multiple analytical perspectives into one compact display, you can quickly assess market conditions without the visual noise of traditional multi-indicator setups. All metrics are non-overlapping, meaning each provides unique insights into different aspects of market behavior.

🚀 Points of Innovation

13 selectable metrics covering momentum, volume, volatility, trend, and statistical analysis, all accessible through a single dropdown menu

Universal 0-100 normalization system that standardizes different indicator scales for consistent visual interpretation across all metrics

Semi-circular gauge design with 21 arc segments providing smooth precision and clear visual feedback through color-coded zones

Non-redundant metric selection ensuring each indicator provides unique market insights without analytical overlap

Advanced metrics including MFI (volume-weighted momentum), CCI (statistical deviation), Volatility Rank (extended lookback), Trend Strength (ADX-style), Choppiness Index, Volume Trend, and Price Distance from MA

Flexible positioning system with 5 chart locations, 3 size options, and fully customizable color schemes for optimal workspace integration

🔧 Core Components

Metric Selection Engine: Dropdown interface allowing instant switching between 13 different technical indicators, each with independent parameter controls

Normalization System: All metrics converted to 0-100 scale using indicator-specific algorithms that preserve the statistical significance of each measurement

Semi-Circular Gauge: Visual display using 21 arc segments arranged in curved formation with two-row thickness for enhanced visibility

Color Zone System: Three distinct zones (0-40 green, 40-70 yellow, 70-100 red) providing instant visual feedback on metric extremes

Needle Indicator: Dynamic pointer that positions across the gauge arc based on precise current metric value

Table Implementation: Professional table structure ensuring consistent positioning and rendering across different chart configurations

🔥 Key Features

RSI (Relative Strength Index): Classic momentum oscillator measuring overbought/oversold conditions with adjustable period length (default 14)

Stochastic Oscillator: Compares closing price to price range over specified period with smoothing, ideal for identifying momentum shifts

MFI (Money Flow Index): Volume-weighted RSI that combines price movement with volume to measure buying and selling pressure intensity

CCI (Commodity Channel Index): Measures statistical deviation from average price, normalized from typical -200 to +200 range to 0-100 scale

Williams %R: Alternative overbought/oversold indicator using high-low range analysis, inverted to match 0-100 scale conventions

Volume %: Current volume relative to moving average expressed as percentage, capped at 100 for extreme spikes

Volume Trend: Cumulative directional volume flow showing whether volume is flowing into up moves or down moves over specified period

ATR Percentile: Current Average True Range position within historical range using specified lookback period (default 100 bars)

Volatility Rank: Close-to-close volatility measured against extended historical range (default 252 days), differs from ATR in calculation method

Momentum: Rate of change calculation showing price movement speed, centered at 50 and normalized to 0-100 range

Trend Strength: ADX-style calculation using directional movement to quantify trend intensity regardless of direction

Choppiness Index: Measures market choppiness versus trending behavior, where high values indicate ranging markets and low values indicate strong trends

Price Distance from MA: Measures current price over-extension from moving average using standard deviation calculations

🎨 Visualization

Semi-Circular Arc Display: Curved gauge spanning from 0 (left) to 100 (right) with smooth progression and two-row thickness for visibility

Color-Coded Zones: Green zone (0-40) for low/oversold conditions, yellow zone (40-70) for neutral readings, red zone (70-100) for high/overbought conditions

Needle Indicator: Downward-pointing triangle (▼) positioned precisely at current metric value along the gauge arc

Scale Markers: Vertical line markers at 0, 25, 50, 75, and 100 positions with corresponding numerical labels below

Title Display: Merged cell showing “𓄀 PhenLabs” branding plus currently selected metric name in monospace font

Large Value Display: Current metric value shown with two decimal precision in large text directly below title

Table Structure: Professional table with customizable background color, text color, and transparency for minimal chart obstruction

📖 Usage Guidelines

Metric Selection

Select Metric: Default: RSI | Options: RSI, Stochastic, Volume %, ATR Percentile, Momentum, MFI (Money Flow), CCI (Commodity Channel), Williams %R, Volatility Rank, Trend Strength, Choppiness Index, Volume Trend, Price Distance | Choose the technical indicator you want to display on the gauge based on your current analytical needs

RSI Settings

RSI Length: Default: 14 | Range: 1+ | Controls the lookback period for RSI calculation, shorter periods increase sensitivity to recent price changes

Stochastic Settings

Stochastic Length: Default: 14 | Range: 1+ | Lookback period for stochastic calculation comparing close to high-low range

Stochastic Smooth: Default: 3 | Range: 1+ | Smoothing period applied to raw stochastic value to reduce noise and false signals

Volume Settings

Volume MA Length: Default: 20 | Range: 1+ | Moving average period used to calculate average volume for comparison with current volume

Volume Trend Length: Default: 20 | Range: 5+ | Period for calculating cumulative directional volume flow trend

ATR and Volatility Settings

ATR Length: Default: 14 | Range: 1+ | Period for Average True Range calculation used in ATR Percentile metric

ATR Percentile Lookback: Default: 100 | Range: 20+ | Historical range used to determine current ATR position as percentile

Volatility Rank Lookback (Days): Default: 252 | Range: 50+ | Extended lookback period for Volatility Rank metric using close-to-close volatility

Momentum and Trend Settings

Momentum Length: Default: 10 | Range: 1+ | Lookback period for rate of change calculation in Momentum metric

Trend Strength Length: Default: 20 | Range: 5+ | Period for directional movement calculations in ADX-style Trend Strength metric

Advanced Metric Settings

MFI Length: Default: 14 | Range: 1+ | Lookback period for Money Flow Index calculation combining price and volume

CCI Length: Default: 20 | Range: 1+ | Period for Commodity Channel Index statistical deviation calculation

Williams %R Length: Default: 14 | Range: 1+ | Lookback period for Williams %R high-low range analysis

Choppiness Index Length: Default: 14 | Range: 5+ | Period for calculating market choppiness versus trending behavior

Price Distance MA Length: Default: 50 | Range: 10+ | Moving average period used for Price Distance standard deviation calculation

Visual Customization

Position: Default: Top Right | Options: Top Left, Top Right, Bottom Left, Bottom Right, Middle Right | Controls gauge placement on chart for optimal workspace organization

Size: Default: Normal | Options: Small, Normal, Large | Adjusts overall gauge dimensions and text size for different monitor resolutions and preferences

Low Zone Color (0-40): Default: Green (#00FF00) | Customize color for low/oversold zone of gauge arc

Medium Zone Color (40-70): Default: Yellow (#FFFF00) | Customize color for neutral/medium zone of gauge arc

High Zone Color (70-100): Default: Red (#FF0000) | Customize color for high/overbought zone of gauge arc

Background Color: Default: Semi-transparent dark gray | Customize gauge background for contrast and chart integration

Text Color: Default: White (#FFFFFF) | Customize all text elements including title, value, and scale labels

✅ Best Use Cases

Quick visual assessment of market conditions when you need instant feedback on whether an asset is in extreme territory across multiple analytical dimensions

Workspace organization for traders who monitor multiple indicators but want to reduce chart clutter and visual complexity

Metric comparison by switching between different indicators while maintaining consistent visual interpretation through the 0-100 normalization

Overbought/oversold identification using RSI, Stochastic, Williams %R, or MFI depending on whether you prefer price-only or volume-weighted analysis

Volume analysis through Volume %, Volume Trend, or MFI to confirm price movements with corresponding volume characteristics

Volatility monitoring using ATR Percentile or Volatility Rank to identify expansion/contraction cycles and adjust position sizing

Trend vs range identification by comparing Trend Strength (high values = trending) against Choppiness Index (high values = ranging)

Statistical over-extension detection using CCI or Price Distance to identify when price has deviated significantly from normal behavior

Multi-timeframe analysis by duplicating the gauge on different timeframe charts to compare metric readings across time horizons

Educational purposes for new traders learning to interpret technical indicators through consistent visual representation

⚠️ Limitations

The gauge displays only one metric at a time, requiring manual switching to compare different indicators rather than simultaneous multi-metric viewing

The 0-100 normalization, while providing consistency, may obscure the raw values and specific nuances of each underlying indicator

Table-based visualization cannot be exported or saved as an image separately from the full chart screenshot

Optimal parameter settings vary by asset type, timeframe, and market conditions, requiring user experimentation for best results

💡 What Makes This Unique

Unified Multi-Metric Interface: The only gauge-style indicator offering 13 distinct metrics through a single interface, eliminating the need for multiple oscillator panels

Non-Overlapping Analytics: Each metric provides genuinely unique insights—MFI combines volume with price, CCI measures statistical deviation, Volatility Rank uses extended lookback, Trend Strength quantifies directional movement, and Choppiness Index measures ranging behavior

Universal Normalization System: All metrics standardized to 0-100 scale using indicator-appropriate algorithms that preserve statistical meaning while enabling consistent visual interpretation

Professional Visual Design: Semi-circular gauge with 21 arc segments, precision needle positioning, color-coded zones, and clean table implementation that maintains clarity across all chart configurations

Extensive Customization: Independent parameter controls for each metric, five position options, three size presets, and full color customization for seamless workspace integration

🔬 How It Works

1. Metric Calculation Phase:

All 13 metrics are calculated simultaneously on every bar using their respective algorithms with user-defined parameters

Each metric applies its own specific calculation method—RSI uses average gains vs losses, Stochastic compares close to high-low range, MFI incorporates typical price and volume, CCI measures deviation from statistical mean, ATR calculates true range, directional indicators measure up/down movement, and statistical metrics analyze price relationships

2. Normalization Process:

Each calculated metric is converted to a standardized 0-100 scale using indicator-appropriate transformations

Some metrics are naturally 0-100 (RSI, Stochastic, MFI, Williams %R), while others require scaling—CCI transforms from ±200 range, Momentum centers around 50, Volume ratio caps at 2x for 100, ATR and Volatility Rank calculate percentile positions, and Price Distance scales by standard deviations

3. Gauge Rendering:

The selected metric’s normalized value determines the needle position across 21 arc segments spanning 0-100

Each arc segment receives its color based on position—segments 0-8 are green zone, segments 9-14 are yellow zone, segments 15-20 are red zone

The needle indicator (▼) appears in row 5 at the column corresponding to the current metric value, providing precise visual feedback

4. Table Construction:

The gauge uses TradingView’s table system with merged cells for title and value display, ensuring consistent positioning regardless of chart configuration

Rows are allocated as follows: Row 0 merged for title, Row 1 merged for large value display, Row 2 for spacing, Rows 3-4 for the semi-circular arc with curved shaping, Row 5 for needle indicator, Row 6 for scale markers, Row 7 for numerical labels at 0/25/50/75/100

All visual elements update on every bar when barstate.islast is true, ensuring real-time accuracy without performance impact

💡 Note:

This indicator is designed for visual analysis and market condition assessment, not as a standalone trading system. For best results, combine gauge readings with price action analysis, support and resistance levels, and broader market context. Parameter optimization is recommended based on your specific trading timeframe and asset class. The gauge works on all timeframes but may require different parameter settings for intraday versus daily/weekly analysis. Consider using multiple instances of the gauge set to different metrics for comprehensive market analysis without switching between settings.

On-Chain Signals [LuxAlgo]The On-Chain Signals indicator uses fundamental blockchain metrics to provide traders with an objective technical view of their favorite cryptocurrencies.

It uses IntoTheBlock datasets integrated within TradingView to generate four key signals: Net Network Growth, In the Money, Concentration, and Large Transactions.

Together, these four signals provide traders with an overall directional bias of the market. All of the data can be visualized as a gauge, table, historical plot, or average.

🔶 USAGE

The main goal of this tool is to provide an overall directional bias based on four blockchain signals, each with three possible biases: bearish, neutral, or bullish. The thresholds for each signal bias can be adjusted on the settings panel.

These signals are based on IntoTheBlock's On-Chain Signals.

Net network growth: Change in the total number of addresses over the last seven periods; i.e., how many new addresses are being created.

In the Money: Change in the seven-period moving average of the total supply in the money. This shows how many addresses are profitable.

Concentration: Change in the aggregate addresses of whales and investors from the previous period. These are addresses holding at least 0.1% of the supply. This shows how many addresses are in the hands of a few.

Large Transactions: Changes in the number of transactions over $100,000. This metric tracks convergence or divergence from the 21- and 30-day EMAs and indicates the momentum of large transactions.

All of these signals together form the blockchain's overall directional bias.

Bearish: The number of bearish individual signals is greater than the number of bullish individual signals.

Neutral: The number of bearish individual signals is equal to the number of bullish individual signals.

Bullish: The number of bullish individual signals is greater than the number of bearish individual signals.

If the overall directional bias is bullish, we can expect the price of the observed cryptocurrency to increase. If the bias is bearish, we can expect the price to decrease. If the signal is neutral, the price may be more likely to stay the same.

Traders should be aware of two things. First, the signals provide optimal results when the chart is set to the daily timeframe. Second, the tool uses IntoTheBlock data, which is available on TradingView. Therefore, some cryptocurrencies may not be available.

🔹 Display Mode

Traders have three different display modes at their disposal. These modes can be easily selected from the settings panel. The gauge is set by default.

🔹 Gauge

The gauge will appear in the center of the visible space. Traders can adjust its size using the Scale parameter in the Settings panel. They can also give it a curved effect.

The number of bars displayed directly affects the gauge's resolution: More bars result in better resolution.

The chart above shows the effect that different scale configurations have on the gauge.

🔹 Historical Data

The chart above shows the historical data for each of the four signals.

Traders can use this mode to adjust the thresholds for each signal on the settings panel to fit the behavior of each cryptocurrency. They can also analyze how each metric impacts price behavior over time.

🔹 Average

This display mode provides an easy way to see the overall bias of past prices in order to analyze price behavior in relation to the underlying blockchain's directional bias.

The average is calculated by taking the values of the overall bias as -1 for bearish, 0 for neutral, and +1 for bullish, and then applying a triangular moving average over 20 periods by default. Simple and exponential moving averages are available, and traders can select the period length from the settings panel.

🔶 DETAILS

The four signals are based on IntoTheBlock's On-Chain Signals. We gather the data, manipulate it, and build the signals depending on each threshold.

Net network growth

float netNetworkGrowthData = customData('_TOTALADDRESSES')

float netNetworkGrowth = 100*(netNetworkGrowthData /netNetworkGrowthData - 1)

In the Money

float inTheMoneyData = customData('_INOUTMONEYIN')

float averageBalance = customData('_AVGBALANCE')

float inTheMoneyBalance = inTheMoneyData*averageBalance

float sma = ta.sma(inTheMoneyBalance,7)

float inTheMoney = ta.roc(sma,1)

Concentration

float whalesData = customData('_WHALESPERCENTAGE')

float inverstorsData = customData('_INVESTORSPERCENTAGE')

float bigHands = whalesData+inverstorsData

float concentration = ta.change(bigHands )*100

Large Transactions

float largeTransacionsData = customData('_LARGETXCOUNT')

float largeTX21 = ta.ema(largeTransacionsData,21)

float largeTX30 = ta.ema(largeTransacionsData,30)

float largeTransacions = ((largeTX21 - largeTX30)/largeTX30)*100

🔶 SETTINGS

Display mode: Select between gauge, historical data and average.

Average: Select a smoothing method and length period.

🔹 Thresholds

Net Network Growth : Bullish and bearish thresholds for this signal.

In The Money : Bullish and bearish thresholds for this signal.

Concentration : Bullish and bearish thresholds for this signal.

Transactions : Bullish and bearish thresholds for this signal.

🔹 Dashboard

Dashboard : Enable/disable dashboard display

Position : Select dashboard location

Size : Select dashboard size

🔹 Gauge

Scale : Select the size of the gauge

Curved : Enable/disable curved mode

Select Gauge colors for bearish, neutral and bullish bias

🔹 Style

Net Network Growth : Enable/disable historical plot and choose color

In The Money : Enable/disable historical plot and choose color

Concentration : Enable/disable historical plot and choose color

Large Transacions : Enable/disable historical plot and choose color

AWR R & LR Oscillator with plots & tableHello trading viewers !

I'm glad to share with you one of my favorite indicator. It's the aggregate of many things. It is partly based on an indicator designed by gentleman goat. Many thanks to him.

1. Oscillator and Correlation Calculations

Overview and Functionality: This part of the indicator computes up to 10 Pearson correlation coefficients between a chosen source (typically the close price, though this is user-configurable) and the bar index over various periods. Starting with an initial period defined by the startPeriod parameter and increasing by a set increment (periodIncrement), each correlation coefficient is calculated using the built-in ta.correlation function over successive ranges. These coefficients are stored in an array, and the indicator calculates their average (avgPR) to provide a complete view of the market trend strength.

Display Features: Each individual coefficient, as well as the overall average, is plotted on the chart using a specific color. Horizontal lines (both dashed and solid) are drawn at levels 0, ±0.8, and ±1, serving as visual thresholds. Additionally, conditional fills in red or blue highlight when values exceed these thresholds, helping the user quickly identify potential extreme conditions (such as overbought or oversold situations).

2. Visual Signals and Automated Alerts

Graphical Signal Enhancements: To reinforce the analysis, the indicator uses graphical elements like emojis and shape markers. For example:

If all 10 curves drop below -0.79, a 🌋 emoji appears at the bottom of the chart;

When curves 2 through 10 are below -0.79, a ⛰️ emoji is displayed below the bar, potentially serving as a buy signal accompanied by an alert condition;

Likewise, symmetrical conditions for correlations exceeding 0.79 produce corresponding emojis (🤿 and 🏖️) at the top or bottom of the chart.

Alerts and Notifications: Using these visual triggers, several alertcondition statements are defined within the script. This allows users to set up TradingView alerts and receive real-time notifications whenever the market reaches these predefined critical zones identified by the multi-period analysis.

3. Regression Channel Analysis

Principles and Calculations: In addition to the oscillator, the indicator implements an analysis of regression channels. For each of the 8 configurable channels, the user can set a range of periods (for example, min1 to max1, etc.). The function calc_regression_channel iterates through the defined period range to find the optimal period that maximizes a statistical measure derived from a regression parameter calculated by the function r(p). Once this optimal period is identified, the indicator computes two key points (A and B) which define the main regression line, and then creates a channel based on the calculated deviation (an RMSE multiplied by a user-defined factor).

The regression channels are not displayed on the chart but are used to plot shapes & fullfilled a table.

Blue shapes are plotted when 6th channel or 7th channel are lower than 3 deviations

Yellow shapes are plotted when 6th channel or 7th channel are higher than 3 deviations

4. Scores, Conditions, and the Summary Table

Scoring System: The indicator goes further by assigning scores across multiple analytical categories, such as:

1. BigPear Score

What It Represents: This score is based on a longer-term moving average of the Pearson correlation values (SMA 100 of the average of the 10 curves of correlation of Pearson). The BigPear category is designed to capture where this longer-term average falls within specific ranges.

Conditions: The script defines nine boolean conditions (labeled BigPear1up through BigPear9up for the “up” direction).

Here's the rules :

BigPear1up = (bigsma_avgPR <= 0.5 and bigsma_avgPR > 0.25)

BigPear2up = (bigsma_avgPR <= 0.25 and bigsma_avgPR > 0)

BigPear3up = (bigsma_avgPR <= 0 and bigsma_avgPR > -0.25)

BigPear4up = (bigsma_avgPR <= -0.25 and bigsma_avgPR > -0.5)

BigPear5up = (bigsma_avgPR <= -0.5 and bigsma_avgPR > -0.65)

BigPear6up = (bigsma_avgPR <= -0.65 and bigsma_avgPR > -0.7)

BigPear7up = (bigsma_avgPR <= -0.7 and bigsma_avgPR > -0.75)

BigPear8up = (bigsma_avgPR <= -0.75 and bigsma_avgPR > -0.8)

BigPear9up = (bigsma_avgPR <= -0.8)

Conditions: The script defines nine boolean conditions (labeled BigPear1down through BigPear9down for the “down” direction).

BigPear1down = (bigsma_avgPR >= -0.5 and bigsma_avgPR < -0.25)

BigPear2down = (bigsma_avgPR >= -0.25 and bigsma_avgPR < 0)

BigPear3down = (bigsma_avgPR >= 0 and bigsma_avgPR < 0.25)

BigPear4down = (bigsma_avgPR >= 0.25 and bigsma_avgPR < 0.5)

BigPear5down = (bigsma_avgPR >= 0.5 and bigsma_avgPR < 0.65)

BigPear6down = (bigsma_avgPR >= 0.65 and bigsma_avgPR < 0.7)

BigPear7down = (bigsma_avgPR >= 0.7 and bigsma_avgPR < 0.75)

BigPear8down = (bigsma_avgPR >= 0.75 and bigsma_avgPR < 0.8)

BigPear9down = (bigsma_avgPR >= 0.8)

Weighting:

If BigPear1up is true, 1 point is added; if BigPear2up is true, 2 points are added; and so on up to 9 points from BigPear9up.

Total Score:

The positive score (posScoreBigPear) is the sum of these weighted conditions.

Similarly, there is a negative score (negScoreBigPear) that is calculated using a mirrored set of conditions (named BigPear1down to BigPear9down), each contributing a negative weight (from -1 to -9).

In essence, the BigPear score tells you—in a weighted cumulative way—where the longer-term correlation average falls relative to predefined thresholds.

2. Pear Score

What It Represents: This category uses the immediate average of the Pearson correlations (avgPR) rather than a longer-term smoothed version. It reflects a more current picture of the market’s correlation behavior.

How It’s Calculated:

Conditions: There are nine conditions defined for the “up” scenario (named Pear1up through Pear9up), which partition the range of avgPR into intervals. For instance:

Pear1up = (avgPR > -0.2 and avgPR <= 0)

Pear2up = (avgPR > -0.4 and avgPR <= -0.2)

Pear3up = (avgPR > -0.5 and avgPR <= -0.4)

Pear4up = (avgPR > -0.6 and avgPR <= -0.5)

Pear5up = (avgPR > -0.65 and avgPR <= -0.6)

Pear6up = (avgPR > -0.7 and avgPR <= -0.65)

Pear7up = (avgPR > -0.75 and avgPR <= -0.7)

Pear8up = (avgPR > -0.8 and avgPR <= -0.75)

Pear9up = (avgPR > -1 and avgPR <= -0.8)

There are nine conditions defined for the “down” scenario (named Pear1down through Pear9down), which partition the range of avgPR into intervals. For instance:

Pear1down = (avgPR >= 0 and avgPR < 0.2)

Pear2down = (avgPR >= 0.2 and avgPR < 0.4)

Pear3down = (avgPR >= 0.4 and avgPR < 0.5)

Pear4down = (avgPR >= 0.5 and avgPR < 0.6)

Pear5down = (avgPR >= 0.6 and avgPR < 0.65)

Pear6down = (avgPR >= 0.65 and avgPR < 0.7)

Pear7down = (avgPR >= 0.7 and avgPR < 0.75)

Pear8down = (avgPR >= 0.75 and avgPR < 0.8)

Pear9down = (avgPR >= 0.8 and avgPR <= 1)

Weighting:

Each condition has an associated weight, such as 0.9 for Pear1up, 1.9 for Pear2up, and so on, up to 9 for Pear9up.

Sum up :

Pear1up = 0.9

Pear2up = 1.9

Pear3up = 2.9

Pear4up = 3.9

Pear5up = 4.99

Pear6up = 6

Pear7up = 7

Pear8up = 8

Pear9up = 9

Total Score:

The positive score (posScorePear) is the sum of these values for each condition that returns true.

A corresponding negative score (negScorePear) is calculated using conditions for when avgPR falls on the positive side, with similar weights in the negative direction.

This score quantifies the current correlation reading by translating its relative level into a numeric score through a weighted sum.

3. Trendpear Score

What It Represents: The Trendpear score is more dynamic as it compares the current avgPR with its short-term moving average (sma_avgPR / 14 periods ) and also considers its relationship with an even longer moving average (bigsma_avgPR / 100 periods). It is meant to capture the trend or momentum in the correlation behavior.

How It’s Calculated:

Conditions: Nine conditions (from Trendpear1up to Trendpear9up) are defined to check:

Whether avgPR is below, equal to, or above sma_avgPR by different margins;

Whether it is trending upward (i.e., it is higher than its previous value).

Here are the rules

Trendpear1up = (avgPR <= sma_avgPR -0.2) and (avgPR >= avgPR )

Trendpear2up = (avgPR > sma_avgPR -0.2) and (avgPR <= sma_avgPR -0.07) and (avgPR >= avgPR )

Trendpear3up = (avgPR > sma_avgPR -0.07) and (avgPR <= sma_avgPR -0.03) and (avgPR >= avgPR )

Trendpear4up = (avgPR > sma_avgPR -0.03) and (avgPR <= sma_avgPR -0.02) and (avgPR >= avgPR )

Trendpear5up = (avgPR > sma_avgPR -0.02) and (avgPR <= sma_avgPR -0.01) and (avgPR >= avgPR )

Trendpear6up = (avgPR > sma_avgPR -0.01) and (avgPR <= sma_avgPR -0.001) and (avgPR >= avgPR )

Trendpear7up = (avgPR >= sma_avgPR) and (avgPR >= avgPR ) and (avgPR <= bigsma_avgPR)

Trendpear8up = (avgPR >= sma_avgPR) and (avgPR >= avgPR ) and (avgPR >= bigsma_avgPR -0.03)

Trendpear9up = (avgPR >= sma_avgPR) and (avgPR >= avgPR ) and (avgPR >= bigsma_avgPR)

Weighting:

The weights here are not linear. For example, the lightest condition may add 0.1 point, whereas the most extreme condition (e.g., when avgPR is not only above the moving average but also reaches a high proportion relative to bigsma_avgPR) might add as much as 90 points.

Trendpear1up = 0.1

Trendpear2up = 0.2

Trendpear3up = 0.3

Trendpear4up = 0.4

Trendpear5up = 0.5

Trendpear6up = 0.69

Trendpear7up = 7

Trendpear8up = 8.9

Trendpear9up = 90

Total Score:

The positive score (posScoreTrendpear) is the sum of the weights from all conditions that are satisfied.

A negative counterpart (negScoreTrendpear) exists similarly for when the trend indicates a downward bias.

Trendpear integrates both the level and the direction of change in the correlations, giving a strong numeric indication when the market starts to diverge from its short-term average.

4. Deviation Score

What It Represents: The “Écart” score quantifies how far the asset’s price deviates from the boundaries defined by the regression channels. This metric can indicate if the price is excessively deviating—which might signal an eventual reversion—or confirming a breakout.

How It’s Calculated:

Conditions: For each channel (with at least seven channels contributing to the scoring from the provided code), there are three levels of deviation:

First tier (EcartXup): Checks if the price is below the upper boundary but above a second boundary.

Second tier (EcartXup2): Checks if the price has dropped further, between a lower and a more extreme boundary.

Third tier (EcartXup3): Checks if the price is below the most extreme limit.

Weighting:

Each tier within a channel has a very small weight for the lowest severities (for example, 0.0001 for the first tier, 0.0002 for the second, 0.0003 for the third) with weights increasing with the channel index.

First channel : 0.0001 to 0.0003 (very short term)

Second channel : 0.001 to 0.003 (short term)

Third channel : 0.01 to 0.03 (short mid term)

4th channel : 0.1 to 0.3 ( mid term)

5th channel: 1 to 3 (long mid term)

6th channel : 10 to 30 (long term)

7th channel : 100 to 300 (very long term)

Total Score:

The overall positive score (posScoreEcart) is the sum of all the weights for conditions met among the first, second, and third tiers.

The corresponding negative score (negScoreEcart) is calculated similarly (using conditions when the price is above the channel boundaries), with the weights being the same in magnitude but negative in sign.

This layered scoring method allows the indicator to reflect both minor and major deviations in a gradated and cumulative manner.

Example :

Score + = 321.0001

Score - = -0.111

The asset price is really overextended in long term view, not for mid term & short term expect the in the very short term.

Score + = 0.0033

Score - = -1.11

The asset price is really extended in short term view, not for mid term (even a bit underextended) & long term is neutral

5. Slope Score

What It Represents: The Slope score captures the trend direction and steepness of the regression channels. It reflects whether the regression line (and hence the underlying trend) is sloping upward or downward.

How It’s Calculated:

Conditions:

if the slope has a uptrend = 1

if the slope has a downtrend = -1

Weighting:

First channel : 0.0001 to 0.0003 (very short term)

Second channel : 0.001 to 0.003 (short term)

Third channel : 0.01 to 0.03 (short mid term)

4th channel : 0.1 to 0.3 ( mid term)

5th channel: 1 to 3 (long mid term)

6th channel : 10 to 30 (long term)

7th channel : 100 to 300 (very long term)

The positive slope conditions incrementally add weights from 0.0001 for the smallest positive slopes to 100 for the largest among the seven checks. And negative for the downward slopes.

The positive score (posScoreSlope) is the sum of all the weights from the upward slope conditions that are met.

The negative score (negScoreSlope) sums the negative weights when downward conditions are met.

Example :

Score + = 111

Score - = -0.1111

Trend is up for longterm & down for mid & short term

The slope score therefore emphasizes both the magnitude and the direction of the trend as indicated by the regression channels, with an intentional asymmetry that flags strong downtrends more aggressively.

Summary

For each category—BigPear, Pear, Trendpear, Écart, and Slope—the indicator evaluates a defined set of conditions. Each condition is a binary test (true/false) based on different thresholds or comparisons (for example, comparing the current value to a moving average or a channel boundary). When a condition is true, its assigned weight is added to the cumulative score for that category. These individual scores, both positive and negative, are then displayed in a table, making it easy for the trader to see at a glance where the market stands according to each analytical dimension.

This comprehensive, weighted approach allows the indicator to encapsulate several layers of market information into a single set of scores, aiding in the identification of potential trading opportunities or market reversals.

5. Practical Use and Application

How to Use the Indicator:

Interpreting the Signals:

On your chart, observe the following components:

The individual correlation curves and their average, plotted with visual thresholds;

Visual markers (such as emojis and shape markers) that signal potential oversold or overbought conditions

The summary table that aggregates the scores from each category, offering a quick glance at the market’s state.

Trading Alerts and Decisions: Set your TradingView alerts through the alertcondition functions provided by the indicator. This way, you receive immediate notifications when critical conditions are met, allowing you to react as soon as the market reaches key levels. This tool is especially beneficial for advanced traders who want to combine multiple technical dimensions to optimize entry and exit points with a confluence of signals.

Conclusion and Additional Insights

In summary, this advanced indicator innovatively combines multi-scale Pearson correlation analysis (via multiple linear regressions) with robust regression channel analysis. It offers a deep and nuanced view of market dynamics by delivering clear visual signals and a comprehensive numerical summary through a built-in score table.

Combine this indicator with other tools (e.g., oscillators, moving averages, volume indicators) to enhance overall strategy robustness.

MACD of RSI [TORYS]MACD of RSI — Momentum & Divergence Scanner

Description:

This enhanced oscillator applies MACD logic directly to the Relative Strength Index (RSI) rather than price, giving traders a clearer look at internal momentum and early shifts in trend strength. Now featuring a custom histogram, dual MA types, and RSI-based divergence detection — it’s a complete toolkit for identifying exhaustion, acceleration, and hidden reversal points in real time.

How It Works:

Calculates the MACD line as the difference between a fast and slow moving average of RSI. Adds a Signal Line (MA of the MACD) and plots a Histogram to show momentum acceleration/deceleration. Both RSI MAs and the Signal Line can be toggled between EMA and SMA for custom tuning.

Divergence Detection:

Bullish Divergence : Price makes a lower low while RSI makes a higher low → labeled with a green “D” below the curve.

Bearish Divergence : Price makes a higher high while RSI makes a lower high → labeled with a red “D” above the curve.

Configurable lookback window for tuning sensitivity to pivots, with 4 as the sweet spot.

RSI Pivot Dot Signals:

Plots green dots at RSI oversold pivot lows below 30,

Plots red dots at overbought pivot highs above 70.

Helps detect short-term exhaustion or bounce zones, plotted right on the MACD-RSI curve.

RSI 50 Crosses (Optional):

Optional ▲ and ▼ labels when RSI crosses its 50 midline — useful for momentum trend shifts or pullback confirmation, or to detect consolidation.

Histogram:

Plotted as a column chart showing the distance between MACD and Signal Line.

Colored dynamically:

Bright green : Momentum rising above zero

Light green : Weakening above zero

Bright red : Momentum falling below zero

Light red : Weakening below zero

The zero line serves as the mid-point:

Above = Bullish Bias

Below = Bearish Bias

How to Interpret:

Momentum Confirmation:

Use MACD cross above Signal Line with a rising histogram to confirm breakouts or trend entries.

Histogram shrinking near zero = momentum weakening → caution or reversal.

Exhaustion & Reversals:

Dot signals near RSI extremes + histogram peak can suggest overbought/oversold pressure.

Use divergence labels ("D") to spot early reversal signals before price breaks structure.

Inputs & Settings:

RSI Length

Fast/Slow MA Lengths for MACD (applied to RSI)

Signal Line Length

MA Type: Choose between EMA and SMA for MACD and Signal Line

Pivot Sensitivity for dot markers

Divergence Logic Toggle

Show/hide RSI 50 Crosses

Best For:

Traders who want momentum insight from inside RSI, not price

Scalpers using divergence or exhaustion entries

Swing traders seeking entry confirmation from signal crossovers

Anyone using multi-timeframe confluence with RSI and trend filters

Pro Tips:

Combine this with:

Bollinger Bands breakouts and reversals

VWAP or EMAs to filter entries by trend

Volume spikes or BBW squeezes for volatility confirmation

TTM Scalper Alert to sync structure and momentum

regressionsLibrary "regressions"

This library computes least square regression models for polynomials of any form for a given data set of x and y values.

fit(X, y, reg_type, degrees)

Takes a list of X and y values and the degrees of the polynomial and returns a least square regression for the given polynomial on the dataset.

Parameters:

X (array) : (float ) X inputs for regression fit.

y (array) : (float ) y outputs for regression fit.

reg_type (string) : (string) The type of regression. If passing value for degrees use reg.type_custom

degrees (array) : (int ) The degrees of the polynomial which will be fit to the data. ex: passing array.from(0, 3) would be a polynomial of form c1x^0 + c2x^3 where c2 and c1 will be coefficients of the best fitting polynomial.

Returns: (regression) returns a regression with the best fitting coefficients for the selecected polynomial

regress(reg, x)

Regress one x input.

Parameters:

reg (regression) : (regression) The fitted regression which the y_pred will be calulated with.

x (float) : (float) The input value cooresponding to the y_pred.

Returns: (float) The best fit y value for the given x input and regression.

predict(reg, X)

Predict a new set of X values with a fitted regression. -1 is one bar ahead of the realtime

Parameters:

reg (regression) : (regression) The fitted regression which the y_pred will be calulated with.

X (array)

Returns: (float ) The best fit y values for the given x input and regression.

generate_points(reg, x, y, left_index, right_index)

Takes a regression object and creates chart points which can be used for plotting visuals like lines and labels.

Parameters:

reg (regression) : (regression) Regression which has been fitted to a data set.

x (array) : (float ) x values which coorispond to passed y values

y (array) : (float ) y values which coorispond to passed x values

left_index (int) : (int) The offset of the bar farthest to the realtime bar should be larger than left_index value.

right_index (int) : (int) The offset of the bar closest to the realtime bar should be less than right_index value.

Returns: (chart.point ) Returns an array of chart points

plot_reg(reg, x, y, left_index, right_index, curved, close, line_color, line_width)

Simple plotting function for regression for more custom plotting use generate_points() to create points then create your own plotting function.

Parameters:

reg (regression) : (regression) Regression which has been fitted to a data set.

x (array)

y (array)

left_index (int) : (int) The offset of the bar farthest to the realtime bar should be larger than left_index value.

right_index (int) : (int) The offset of the bar closest to the realtime bar should be less than right_index value.

curved (bool) : (bool) If the polyline is curved or not.

close (bool) : (bool) If true the polyline will be closed.

line_color (color) : (color) The color of the line.

line_width (int) : (int) The width of the line.

Returns: (polyline) The polyline for the regression.

series_to_list(src, left_index, right_index)

Convert a series to a list. Creates a list of all the cooresponding source values

from left_index to right_index. This should be called at the highest scope for consistency.

Parameters:

src (float) : (float ) The source the list will be comprised of.

left_index (int) : (float ) The left most bar (farthest back historical bar) which the cooresponding source value will be taken for.

right_index (int) : (float ) The right most bar closest to the realtime bar which the cooresponding source value will be taken for.

Returns: (float ) An array of size left_index-right_index

range_list(start, stop, step)

Creates an from the start value to the stop value.

Parameters:

start (int) : (float ) The true y values.

stop (int) : (float ) The predicted y values.

step (int) : (int) Positive integer. The spacing between the values. ex: start=1, stop=6, step=2:

Returns: (float ) An array of size stop-start

regression

Fields:

coeffs (array__float)

degrees (array__float)

type_linear (series__string)

type_quadratic (series__string)

type_cubic (series__string)

type_custom (series__string)

_squared_error (series__float)

X (array__float)

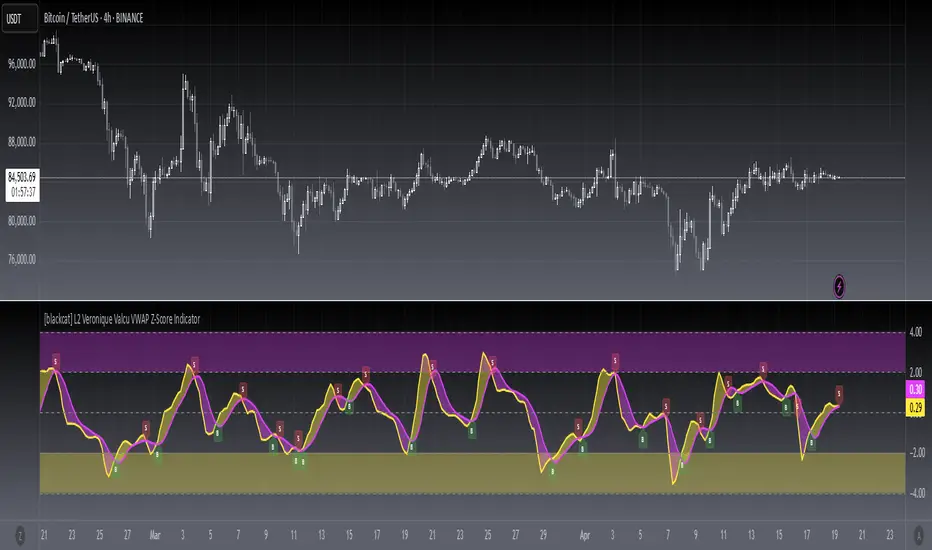

[blackcat] L2 Veronique Valcu VWAP Z-Score IndicatorLevel: 2

Background

Veronique Valcu's article "Z-Score Indicator" in Feb,2003 provided a description and commentary on a new method of displaying directional change normalized in terms of standard deviation. This indicator is realized in pine script here by using the following function code, adding vwap function, called vwap ZScore.

Function

This indicator has three input, "AvgLen", "Smooth1" and "Smooth2." Price is fixed in selected vwap price. AvgLen describes the length of the sample considered in the standard deviation calculation. Once created and verified, the function can be easily called in any indicator or strategy.

Inputs

AvgLen --> Length input for vwap Zscore.

Smooth1 and Smooth2 --> Smoothing length.

Key Signal

Curve1 --> vwap ZScore output fast signal

Curve2 --> vwap ZScore output slow signal

Remarks

This is a Level 2 free and open source indicator.

Feedbacks are appreciated.

Williams %R - Multi TimeframeThis indicator implements the William %R multi-timeframe. On the 1H chart, the curves for 1H (with signal), 4H, and 1D are displayed. On the 4H chart, the curves for 4H (with signal) and 1D are shown. On all other timeframes, only the %R and signal are displayed. The indicator is useful to use on 1H and 4H charts to find confluence among the different curves and identify better entries based on their alignment across all timeframes. Signals above 80 often indicate a potential bearish reversal in price, while signals below 20 often suggest a bullish price reversal.

Demand and Supply Conditions with SignalsIntroduction:

This document outlines a trading strategy that utilizes price action analysis and color signals to make informed trading decisions. The strategy focuses on identifying demand and supply conditions, curve patterns, and generating signals based on historical price data. The colors associated with each condition and signal serve as visual indicators to assist in decision-making.

I. Strategy Overview:

Objective:

The objective of this trading strategy is to identify potential trading opportunities based on price action analysis and color signals.

Key Components:

Demand Condition: A green upward-facing triangle indicates a potential demand condition.

Supply Condition: A red downward-facing triangle indicates a potential supply condition.

Curve Pattern Condition: A blue upward-facing triangle indicates a potential curve pattern condition.

Signal Condition: A yellow upward-facing triangle indicates a potential buy signal.

II. Understanding the Colors:

* Green: Represents the demand condition, which suggests potential buying pressure in the market. A green upward-facing triangle is plotted on the chart when the demand condition is met at a specific candle or bar.

* Red: Represents the supply condition, which suggests potential selling pressure in the market. A red downward-facing triangle is plotted on the chart when the supply condition is met at a specific candle or bar.

* Blue: Represents the curve pattern condition, which suggests the presence of a specific pattern based on price action analysis. A blue upward-facing triangle is plotted on the chart when the curve pattern condition is met at a specific candle or bar.

* Yellow: Represents the signal condition, which is a combination of the demand condition and the curve pattern condition. A yellow upward-facing triangle is plotted on the chart when the signal condition is met at a specific candle or bar, indicating a potential buy signal.

III. Decision-Making Process:

* Demand and Supply Conditions: Identify potential buying opportunities when a green demand condition is present. Consider potential selling opportunities when a red supply condition is present. Use these conditions to assess the overall market sentiment and potential price reversals.

* Curve Patterns: Analyze the presence of blue curve pattern conditions to identify specific price patterns. These patterns can provide additional confirmation for potential trading decisions.

* Signal Condition: Pay attention to the yellow signal condition, which indicates a potential buy signal. Evaluate the overall market context and consider entering a buy position when the signal condition is met.

* Risk Management: Implement proper risk management techniques such as setting stop-loss orders and position sizing to protect against potential losses.

IV. Conclusion:

This trading strategy leverages price action analysis and color signals to identify potential trading opportunities. The colors associated with each condition and signal serve as visual aids to highlight specific points on the chart. It's important to thoroughly backtest and validate the strategy before applying it to real-world trading scenarios. Additionally, always consider market conditions, risk management, and individual trading preferences when making trading decisions.

Disclaimer: Trading involves risks, and this document does not guarantee profitable outcomes. Traders should exercise caution and perform their own due diligence before engaging in any trading activity.

Remember to continually review and adapt your trading strategy based on market conditions and personal experiences to enhance its effectiveness.

InterpolationLibrary "Interpolation"

Functions for interpolating values. Can be useful in signal processing or applied as a sigmoid function.

linear(k, delta, offset, unbound) Returns the linear adjusted value.

Parameters:

k : A number (float) from 0 to 1 representing where the on the line the value is.

delta : The amount the value should change as k reaches 1.

offset : The start value.

unbound : When true, k values less than 0 or greater than 1 are still calculated. When false (default), k values less than 0 will return the offset value and values greater than 1 will return (offset + delta).

quadIn(k, delta, offset, unbound) Returns the quadratic (easing-in) adjusted value.

Parameters:

k : A number (float) from 0 to 1 representing where the on the curve the value is.

delta : The amount the value should change as k reaches 1.

offset : The start value.

unbound : When true, k values less than 0 or greater than 1 are still calculated. When false (default), k values less than 0 will return the offset value and values greater than 1 will return (offset + delta).

quadOut(k, delta, offset, unbound) Returns the quadratic (easing-out) adjusted value.

Parameters:

k : A number (float) from 0 to 1 representing where the on the curve the value is.

delta : The amount the value should change as k reaches 1.

offset : The start value.

unbound : When true, k values less than 0 or greater than 1 are still calculated. When false (default), k values less than 0 will return the offset value and values greater than 1 will return (offset + delta).

quadInOut(k, delta, offset, unbound) Returns the quadratic (easing-in-out) adjusted value.

Parameters:

k : A number (float) from 0 to 1 representing where the on the curve the value is.

delta : The amount the value should change as k reaches 1.

offset : The start value.

unbound : When true, k values less than 0 or greater than 1 are still calculated. When false (default), k values less than 0 will return the offset value and values greater than 1 will return (offset + delta).

cubicIn(k, delta, offset, unbound) Returns the cubic (easing-in) adjusted value.

Parameters:

k : A number (float) from 0 to 1 representing where the on the curve the value is.

delta : The amount the value should change as k reaches 1.

offset : The start value.

unbound : When true, k values less than 0 or greater than 1 are still calculated. When false (default), k values less than 0 will return the offset value and values greater than 1 will return (offset + delta).

cubicOut(k, delta, offset, unbound) Returns the cubic (easing-out) adjusted value.

Parameters:

k : A number (float) from 0 to 1 representing where the on the curve the value is.

delta : The amount the value should change as k reaches 1.

offset : The start value.

unbound : When true, k values less than 0 or greater than 1 are still calculated. When false (default), k values less than 0 will return the offset value and values greater than 1 will return (offset + delta).

cubicInOut(k, delta, offset, unbound) Returns the cubic (easing-in-out) adjusted value.

Parameters:

k : A number (float) from 0 to 1 representing where the on the curve the value is.

delta : The amount the value should change as k reaches 1.

offset : The start value.

unbound : When true, k values less than 0 or greater than 1 are still calculated. When false (default), k values less than 0 will return the offset value and values greater than 1 will return (offset + delta).

expoIn(k, delta, offset, unbound) Returns the exponential (easing-in) adjusted value.

Parameters:

k : A number (float) from 0 to 1 representing where the on the curve the value is.

delta : The amount the value should change as k reaches 1.

offset : The start value.

unbound : When true, k values less than 0 or greater than 1 are still calculated. When false (default), k values less than 0 will return the offset value and values greater than 1 will return (offset + delta).

expoOut(k, delta, offset, unbound) Returns the exponential (easing-out) adjusted value.

Parameters:

k : A number (float) from 0 to 1 representing where the on the curve the value is.

delta : The amount the value should change as k reaches 1.

offset : The start value.

unbound : When true, k values less than 0 or greater than 1 are still calculated. When false (default), k values less than 0 will return the offset value and values greater than 1 will return (offset + delta).

expoInOut(k, delta, offset, unbound) Returns the exponential (easing-in-out) adjusted value.

Parameters:

k : A number (float) from 0 to 1 representing where the on the curve the value is.

delta : The amount the value should change as k reaches 1.

offset : The start value.

unbound : When true, k values less than 0 or greater than 1 are still calculated. When false (default), k values less than 0 will return the offset value and values greater than 1 will return (offset + delta).

using(fn, k, delta, offset, unbound) Returns the adjusted value by function name.

Parameters:

fn : The name of the function. Allowed values: linear, quadIn, quadOut, quadInOut, cubicIn, cubicOut, cubicInOut, expoIn, expoOut, expoInOut.

k : A number (float) from 0 to 1 representing where the on the curve the value is.

delta : The amount the value should change as k reaches 1.

offset : The start value.

unbound : When true, k values less than 0 or greater than 1 are still calculated. When false (default), k values less than 0 will return the offset value and values greater than 1 will return (offset + delta).

Bollinger Bands Forecast with Signals (Zeiierman)█ Overview

Bollinger Bands Forecast with Signals (Zeiierman) extends classic Bollinger Bands into a forward-looking framework. Instead of only showing where volatility has been, it projects where the basis (midline) and band width are likely to drift next, based on recent trend and volatility behavior.

The projection is built from the measured slopes of the Bollinger basis, the standard deviation (or ATR, depending on the mode), and a volatility “breathing” component. On top of that, the script includes an optional projected price path that can be blended with a deterministic random walk, plus rejection signals to highlight failed band breaks.

█ How It Works

⚪ Bollinger Core

The script first computes standard Bollinger Bands using the selected Source, Length, and Multiplier:

Basis = SMA(Source, Length)

Band width = Multiplier × StDev(Source, Length)

Upper/Lower = Basis ± Width

This remains the “live” (non-forecast) structure on the chart.

⚪ Trend & Volatility Slope Estimation

To project forward, the indicator measures directional drift and volatility drift using linear regression differences:

Basis slope from the Bollinger basis

StDev slope from the Bollinger deviation

ATR slope for ATR-based projection mode

These slopes drive the forecast bands forward, reflecting the market’s recent directional and volatility regime.

⚪ Projection Engine (Forecast Bands)

At the last bar, the indicator draws projected basis, upper, and lower lines out to Forecast Bars. The projected basis can be:

Trend (straight linear projection)

Curved (ease-in/out transition toward projected endpoints)

Smoothed (extra smoothing on projected basis/width)

⚪ Price Path Projection + Optional Random Walk

In addition to projecting the bands, the script can draw a price forecast path made of a small number of zigzag swings.

Each swing targets a point offset from the projected basis by a multiple of the projected half-width (“width units”).

Decay gradually reduces swing size as the forecast deepens.

The Optional Random Walk Blend adds a deterministic drift component to the zigzag path. It’s not true randomness; it’s a stable pseudo-random sequence, so the drawing doesn’t jump around on refresh, while still adding “natural” variation.

⚪ Rejection Signals

Signals are based on failed attempts to break a band:

Bear Signal (Down): price tries to push above the upper band, then falls back inside, while still closing above the basis.

Bull Signal (Up): price tries to push below the lower band, then returns back inside, while still closing below the basis.

█ How to Use

⚪ Forward Support/Resistance Corridors

Treat the projected upper/lower bands as a future volatility envelope, not a guarantee:

The upper projection ≈ is likely a resistance level if the regime persists

The lower projection ≈ is likely a support level if the regime persists

Best used for trade planning, targets, and “where price could travel” under similar conditions.

⚪ Regime Read: Trend + Volatility

The projection shape is informative:

Rising basis + expanding width → trend with increasing volatility (needs wider stops / more caution)

Flat basis + compressing width → contraction regime (often precedes expansion)

⚪ Signals for Mean-Reversion / Failed Breakouts

The rejection markers are useful for fade-style setups:

A Down signal near/after upper-band failure can imply rotation back toward the basis.

An Up signal near/after lower-band failure can imply snap-back toward the basis.

With MA filtering enabled, signals are constrained to align with the broader bias, helping reduce chop-driven noise.

█ Related Publications

Donchian Predictive Channel (Zeiierman)

█ Settings

⚪ Bollinger Band

Controls the live Bollinger Bands on the chart.

Source – Price used for calculations.

Length – Lookback period; higher = smoother, lower = more reactive.

Multiplier – Bandwidth; higher = wider bands, lower = tighter bands.

⚪ Forecast

Controls the forward projection of the Bollinger Bands.

Forecast Bars – How far into the future the bands are projected.

Trend Length – Lookback used to estimate trend and volatility slopes.

Forecast Band Mode – Defines projection behavior (linear, curved, breathing, ATR-based, or smoothed).

⚪ Price Forecast

Controls the projected price path inside the bands.

ZigZag Swings – Number of projected oscillations.

Amplitude – Distance from basis, measured in bandwidth units.

Decay – Shrinks swings further into the forecast.

⚪ Random-Walk

Adds controlled randomness to the price path.

Enable – Toggle random-walk influence.

Blend – Strength of randomness vs. zigzag.

Step Size – Size of random steps (band-width units).

Decay – Reduces randomness as the forecast deepens.

Seed – Changes the (stable) random sequence.

⚪ Signals

Controls rejection/mean-reversion signals.

Show Signals – Enable/disable signal markers.

MA Filter (Type/Length) – Filters signals by trend direction.

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

Coin Jin Multi SMA+ BB+ SMA forecast Ver 2.0Coin Jin Multi SMA + BB + SMA Forecast 2.0

개요

여러 개의 단순이동평균(SMA: 5/20/60/112/224/448/896 + 사용자 정의 X1/X2), 볼린저 밴드(BB), 그리고 접선 기반 곡선 예측선을 한 번에 표시합니다. 예측선은 선형회귀 기울기와 그 변화율(가속도)을 EMA로 스무딩해 곡선 외삽으로 앞으로 그려지며, 어떤 줌에서도 깔끔하게 보이도록 점선(dotted) 스타일을 강제할 수 있습니다.

스택 마커(정배열/역배열) 안내

조건: 이동평균이 정배열(5>20>60>112>224>448>(896)) 또는 역배열(5<20<60<112<224<448<(896))로 새로 전환되는 순간 삼각형 마커가 생성됩니다.

896일선 포함(with 896): SOLID 마커로 표시, Bull = 초록색, Bear = 빨간색.

896일선 미포함(no 896): HOLLOW(윤곽) 마커로 표시, 시선을 덜 끌도록 투명도 70 적용(Bull = 연두, Bear = 빨강 동일색).

방향: Bull = ▼(위, abovebar) / Bear = ▲(아래, belowbar) 로 배치됩니다.

주요 기능

SMA 7종 기본 + 사용자 정의 SMA 2개(X1/X2) 추가(기본 꺼짐, 길이/색/두께/타입 자유).

BB: 길이/배수/선두께/밴드 채움(기본 90% 투명) 지원.

예측선: Forward bars(1–100, 기본 30), 기울기 산출 길이, 스무딩 강도, 세그먼트 개수, 점/대시 스타일 선택 및 도트 강제.

스택(정/역배열) 전환 마커: with 896=SOLID, no 896=HOLLOW(투명도 70).

처음 사용하는 분들을 위한 팁 (중요)

가격 스케일을 ‘우측’으로 고정하세요.

방법 ① 차트 우측 축을 사용(기본).

방법 ② 지표 레전드의 ‘⋯’ 메뉴 → Move to → Right scale.

예측선이 본선과 어긋나 보이면 스케일이 좌측/양측으로 되어 있거나 자동 합침된 경우이니 Right scale로 맞춰주세요.

입력 요약

MA Source, 각 SMA on/off·길이·색·두께·타입

BB length/mult/width/fill/opacity(기본 90)

Forecast bars ahead(1–100), slope lookback, smoothing, segments, style/opacity, 적용 대상 선택(SMA별)

주의/면책

예측선은 가격 예언 도구가 아니라 시각적 외삽 보조지표입니다. 단독 매매 판단에 사용하지 마세요.

공개 스크린샷은 본 지표만 보이도록 깔끔하게 캡처해 주세요(다른 지표/드로잉 혼합 금지).

변경사항(v2.0)

곡선 예측선 안정화 및 도트 강제 개선.

스택 마커 no 896 상태 HOLLOW 투명도 70 적용(가독성 향상).

사용자 정의 SMA X1/X2 추가(기본 OFF).

Coin Jin Multi SMA + BB + SMA Forecast 2.0 (English)

Overview

This indicator plots multiple Simple Moving Averages (SMA: 5/20/60/112/224/448/896 + two user-defined X1/X2), Bollinger Bands, and a tangent-based curved forecast in one overlay. The forecast extrapolates forward using the linear-regression slope and its rate of change (acceleration) smoothed by EMA, and you can force a dotted look so it stays clean at any zoom level.

Stack Markers (Bullish/Bearish alignment)

Markers appear only when a full bullish stack (5>20>60>112>224>448>(896)) or bearish stack (5<20<60<112<224<448<(896)) is newly formed.

With 896 included: shown as SOLID triangles — Bull = green, Bear = red.

Without 896: shown as HOLLOW (outline) with 70 transparency to reduce visual weight — Bull = lime, Bear = red (same hue).

Orientation: Bull = ▼ abovebar, Bear = ▲ belowbar.

Features

7 standard SMAs + two custom SMAs (X1/X2) (default OFF; fully configurable length/color/width/style).

BB with length/multiplier/width/fill (default fill opacity 90%).

Forecast controls: forward bars (1–100, default 30), slope window, smoothing, segment count, style/opacity, force dotted option.

Stack markers: with 896 = SOLID, without 896 = HOLLOW (70 transparency).

First-time setup (Important)

Pin the indicator to the Right price scale.

Option A: Use the right price axis.

Option B: Indicator legend “⋯” → Move to → Right scale.

If the forecast appears detached from the MA, your series is likely on the left/both scales; switch to Right scale.

Inputs

MA source; per-SMA on/off, length, color, width, style

BB length/multiplier/width/fill/opacity (default 90)

Forecast bars ahead (1–100), slope lookback, smoothing, segments, style/opacity, per-SMA apply switches

Disclaimer

The forecast is a visual extrapolation, not a price prediction. Do not use it alone to make trading decisions.

For publication, please use a clean screenshot that shows only this indicator (no mixed overlays).

What’s new in v2.0

More robust curved forecast with improved “force dotted” rendering.

HOLLOW (no 896) markers now use 70 transparency for better readability.

Added two user-defined SMAs (X1/X2), OFF by default.

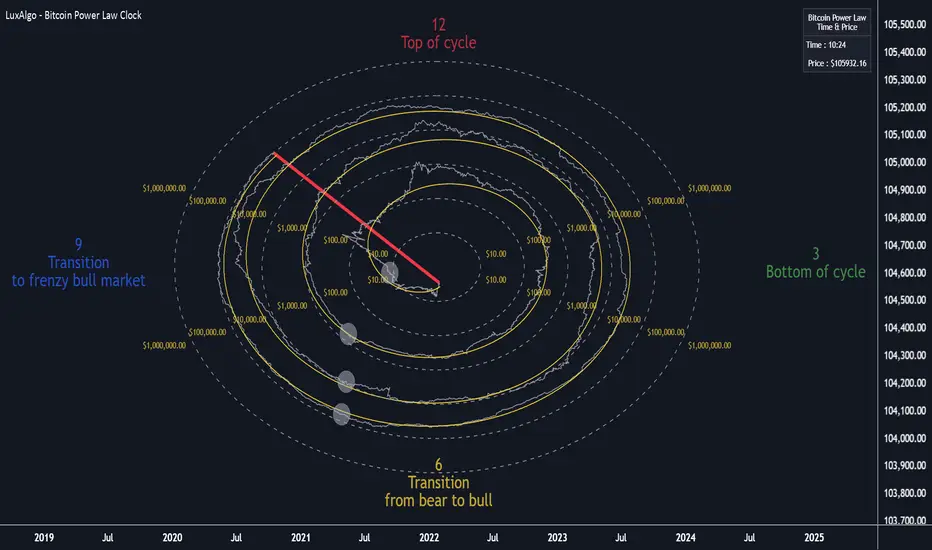

Bitcoin Power Law Clock [LuxAlgo]The Bitcoin Power Law Clock is a unique representation of Bitcoin prices proposed by famous Bitcoin analyst and modeler Giovanni Santostasi.

It displays a clock-like figure with the Bitcoin price and average lines as spirals, as well as the 12, 3, 6, and 9 hour marks as key points in the cycle.

🔶 USAGE

Giovanni Santostasi, Ph.D., is the creator and discoverer of the Bitcoin Power Law Theory. He is passionate about Bitcoin and has 12 years of experience analyzing it and creating price models.

As we can see in the above chart, the tool is super intuitive. It displays a clock-like figure with the current Bitcoin price at 10:20 on a 12-hour scale.

This tool only works on the 1D INDEX:BTCUSD chart. The ticker and timeframe must be exact to ensure proper functionality.

According to the Bitcoin Power Law Theory, the key cycle points are marked at the extremes of the clock: 12, 3, 6, and 9 hours. According to the theory, the current Bitcoin prices are in a frenzied bull market on their way to the top of the cycle.

🔹 Enable/Disable Elements

All of the elements on the clock can be disabled. If you disable them all, only an empty space will remain.

The different charts above show various combinations. Traders can customize the tool to their needs.

🔹 Auto scale

The clock has an auto-scale feature that is enabled by default. Traders can adjust the size of the clock by disabling this feature and setting the size in the settings panel.

The image above shows different configurations of this feature.

🔶 SETTINGS

🔹 Price

Price: Enable/disable price spiral, select color, and enable/disable curved mode

Average: Enable/disable average spiral, select color, and enable/disable curved mode

🔹 Style

Auto scale: Enable/disable automatic scaling or set manual fixed scaling for the spirals

Lines width: Width of each spiral line

Text Size: Select text size for date tags and price scales

Prices: Enable/disable price scales on the x-axis

Handle: Enable/disable clock handle

Halvings: Enable/disable Halvings

Hours: Enable/disable hours and key cycle points

🔹 Time & Price Dashboard

Show Time & Price: Enable/disable time & price dashboard

Location: Dashboard location

Size: Dashboard size

LGMM (flat buffers) — multivariate poly + latent statesLGMM POLYNOMIAL BANDS — DISCOVER THE MARKET’S HIDDEN STATES

Overview

Latent-Gaussian-Mixture-Models (LGMMs) view price action as a mix of several invisible regimes: trending up, drifting sideways, sudden volatility spikes, and so on.

A Gaussian Mixture learns these states directly from data and outputs, for every bar, the probability that the market is in each state.

This indicator feeds those probabilities into a rolling polynomial regression that draws a fair-value line, then builds adaptive upper and lower bands.

Band width expands when recent residuals are large *and* when the state mix is uncertain, and contracts when price is calm or one regime clearly dominates.

Crossing back into the band from below generates a buy flag; crossing back into the band from above generates a sell flag (or take-profit for longs).

Key Inputs

Price source – default is Close; you can choose HL2, OHLC4, etc.

Training window (bars) – look-back length for every retrain. 252 bars (one trading year) is a balanced default for US stocks on daily timeframe. Use fewer bars for intraday charts (say 7*24=168 for 1H bars on crypto), more for weekly periods.

Polynomial degree – 1 for a straight trend line, 2 for a curved fit. Curved fits are better when the symbol shows persistent drift.

Hidden states K – number of regimes the mixture tracks (1 to 3). Three states often map well to up-trend, chop, down-trend.

Band width ×σ – multiplier on the entropy-weighted standard deviation. Smaller values (1.5-2) give more trades; larger values (2.5-3) give fewer, higher-conviction trades.

Offline μ,σ pairs (optional) – paste component means and sigmas from an offline LGMM (format: mu1,sigma1;mu2,sigma2;…). Leave blank to let the script use its built-in approximation.

Quick Start

Add the indicator to a chart and wait until the initial Training window has filled.

Watch for green BUY triangles when price closes back above the lower band and red SELL triangles when price closes back below the upper band.

Fine-tune:

– Increase Training window to reduce noise.

– Decrease Band width ×σ for more frequent signals.

– Experiment with Hidden states K; more states capture richer behaviour but need longer windows to stay reliable.

Tips

Bands widen automatically in chaotic periods and tighten when one regime dominates.

Combine with a volume filter or a higher-time-frame trend to reduce whipsaws.

If you already run an LGMM in Python or Matlab, paste its component parameters for a perfect match between your back-test and the TradingView plot.

Works on all markets and time-frames, provided you have at least five times the Training window’s bars in history.

Happy trading!

Relative Crypto Dominance Polar Chart [LuxAlgo]The Relative Crypto Dominance Polar Chart tool allows traders to compare the relative dominance of up to ten different tickers in the form of a polar area chart, we define relative dominance as a combination between traded dollar volume and volatility, making it very easy to compare them at a glance.

🔶 USAGE

The use is quite simple, traders just have to load the indicator on the chart, and the graph showing the relative dominance will appear.

The 10 tickers loaded by default are the major cryptocurrencies by market cap, but traders can select any ticker in the settings panel.

Each area represents dominance as volatility (radius) by dollar volume (arc length); a larger area means greater dominance on that ticker.

🔹 Choosing Period

The tool supports up to five different periods

Hourly

Daily

Weekly

Monthly

Yearly

By default, the tool period is set on auto mode, which means that the tool will choose the period depending on the chart timeframe

timeframes up to 2m: Hourly

timeframes up to 15m: Daily

timeframes up to 1H: Weekly

timeframes up to 4H: Monthly

larger timeframes: Yearly

🔹 Sorting & Sizing

Traders can sort the graph areas by volatility (radius of each area) in ascending or descending order; by default, the tickers are sorted as they are in the settings panel.

The tool also allows you to adjust the width of the chart on a percentage basis, i.e., at 100% size, all the available width is used; if the graph is too wide, just decrease the graph size parameter in the settings panel.

🔹 Set your own style

The tool allows great customization from the settings panel, traders can enable/disable most of the components, and add a very nice touch with curved lines enabled for displaying the areas with a petal-like effect.

🔶 SETTINGS

Period: Select up to 5 different time periods from Hourly, Daily, Weekly, Monthly and Yearly. Enable/disable Auto mode.

Tickers: Enable/disable and select tickers and colors

🔹 Style

Graph Order: Select sort order

Graph Size: Select percentage of width used

Labels Size: Select size for ticker labels

Show Percent: Show dominance in % under each ticker

Curved Lines: Enable/disable petal-like effect for each area

Show Title: Enable/disable graph title

Show Mean: Enable/disable volatility average and select color

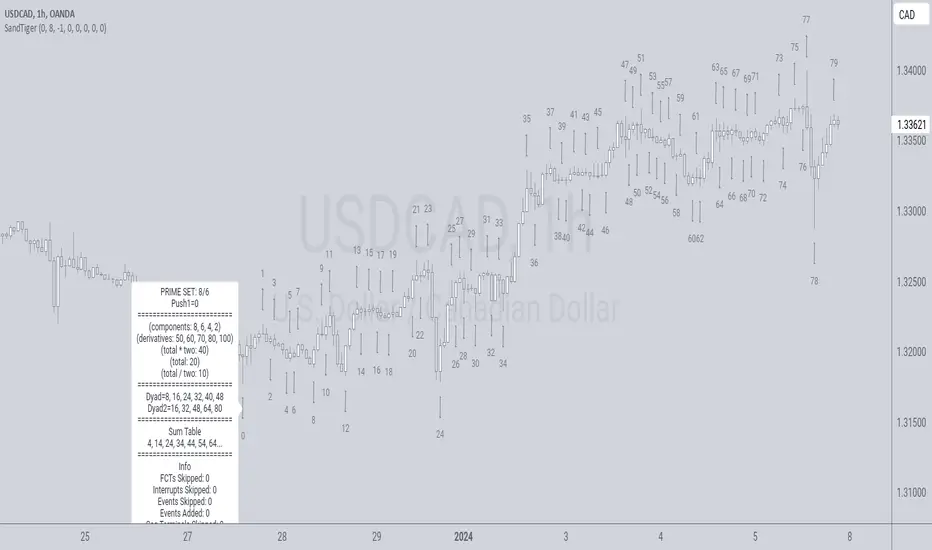

SandTigerSandTiger is an auto-counting tool that counts naturally occurring events in a price series. This version has been reduced to 377 lines of code and should run faster than previous versions. Although not shown here, I highly recommend running my 'ELB' script with SandTiger. ELB is an 'event locator' and will mark all points that SandTiger numbers - giving you visual cues as to where these points are located. ELB also displays support/resistance levels.

SandTiger is designed to be used with MAGENTA - a counting system for Forex and other markets.

MAGENTA is a free and open framework for understanding and explaining price movement in financial markets. Any materials associated with MAGENTA are strictly for educational purposes only.

SandTiger tracks Component Values, Dyads, and Sum Table Values (STV's) over straight and curved trends, allowing a trader to discern where directional shifts are likely to occur.

SandTiger requires just 3 things to function accurately:

1) A correct starting point (this will typically be an obvious trend turn high or low in a series of price moves).

2) A 'push 1' count ('push 1' runs from the starting point to the event prior to the first terminal of the first FCT or Fractured Counter-Trend).

3) A 'high prime' value (the high prime count runs from the starting point through to the second terminal of the first FCT with no skips).

FRAMEWORK OVERVIEW: 'Component' values are filtered from the prime set (including the half prime and further reductions). Once we have the comp table we add the values to get a 'total'. With the 'total' we divide and multiply by two to get two additional values. 'Derivatives' are based on various calculations using these three values.

We're looking for 'total/2' to count into either itself, 'total', 'total*2', or a derivative. Comp counts are in Tx form and counted from trend start. If the trend doesn't turn on a comp value it will likely turn on a Dyad or STV value. If that also doesn't happen it's likely you have a 'curved' trend/sequence that will turn on one of the above after moving away from its high/low. This can also be traded using SandTiger's 'Seg Terminals' skip option.

Sum tables and Dyad values are drawn from the 'primes' and Dyads use the 'push1' value as well. In a structural trend, primes are gotten by counting pushpulls 1 & 2 in 'Ti' form. Comps, Sum table values, and Dyads are equivalent, sequences can turn on either value type belonging to the 1st or 2nd prime set. Both STV's and Dyads are counted in 'Tx' form (except where count-through signals occur).

Types and antitypes correlate and are associated with a 12-count 'cycle.' (Ti = 'Terminals Included'; Tx = 'Terminals eXcluded'; both refer to FCT terminals)

THE STRATEGY:

For Structures: Trade Comps, Dyads, and STV's from sets 1 (all) and 2 (Dyads and STV's only) in the 'main' segment then on the 'carry-over' by skipping segment terminals. If a PC or cycle caps the sequence, trade that as well.

For NSM's: Trade movements that flash a signal prior to the end of the initial cycle. The mark will be the push1 value. Twelve will be the 'high prime.' Skip interrupts and trade carry-over values.

The first version of SandTiger was conceived/planned/authored by Erek A.D. and coded by Erek A.D. and @SimpleCryptoLife beginning in August 2022 and finishing in Dec. 2022

The current version was written and developed July 3, 2023 and has been refined and upgraded by Erek A.D. through Jan. 2024...

ZigzagLiteLibrary "ZigzagLite"

Lighter version of the Zigzag Library. Without indicators and sub-component divisions

method getPrices(pivots)

Gets the array of prices from array of Pivots

Namespace types: Pivot

Parameters:

pivots (Pivot ) : array array of Pivot objects

Returns: array array of pivot prices

method getBars(pivots)

Gets the array of bars from array of Pivots

Namespace types: Pivot

Parameters:

pivots (Pivot ) : array array of Pivot objects

Returns: array array of pivot bar indices

method getPoints(pivots)

Gets the array of chart.point from array of Pivots

Namespace types: Pivot

Parameters:

pivots (Pivot ) : array array of Pivot objects

Returns: array array of pivot points

method getPoints(this)

Namespace types: Zigzag

Parameters:

this (Zigzag)

method calculate(this, ohlc, ltfHighTime, ltfLowTime)

Calculate zigzag based on input values and indicator values

Namespace types: Zigzag

Parameters:

this (Zigzag) : Zigzag object