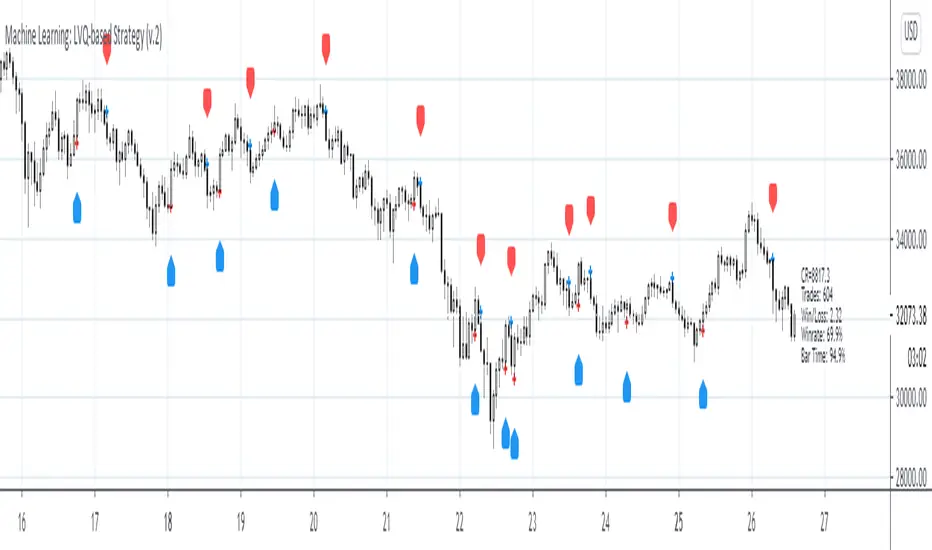

Optimized Grid with KNN_2.0Strategy Overview

This strategy, named "Optimized Grid with KNN_2.0," is designed to optimize trading decisions using a combination of grid trading, K-Nearest Neighbors (KNN) algorithm, and a greedy algorithm. The strategy aims to maximize profits by dynamically adjusting entry and exit thresholds based on market conditions and historical data.

Key Components

Grid Trading:

The strategy uses a grid-based approach to place buy and sell orders at predefined price levels. This helps in capturing profits from market fluctuations.

K-Nearest Neighbors (KNN) Algorithm:

The KNN algorithm is used to optimize entry and exit points based on historical price data. It identifies the nearest neighbors (similar price movements) and adjusts the thresholds accordingly.

Greedy Algorithm:

The greedy algorithm is employed to dynamically adjust the stop-loss and take-profit levels. It ensures that the strategy captures maximum profits by adjusting thresholds based on recent price changes.

Detailed Explanation

Grid Trading:

The strategy defines a grid of price levels where buy and sell orders are placed. The openTh and closeTh parameters determine the thresholds for opening and closing positions.

The t3_fast and t3_slow indicators are used to generate trading signals based on the crossover and crossunder of these indicators.

KNN Algorithm:

The KNN algorithm is used to find the nearest neighbors (similar price movements) in the historical data. It calculates the distance between the current price and historical prices to identify the most similar price movements.

The algorithm then adjusts the entry and exit thresholds based on the average change in price of the nearest neighbors.

Greedy Algorithm:

The greedy algorithm dynamically adjusts the stop-loss and take-profit levels based on recent price changes. It ensures that the strategy captures maximum profits by adjusting thresholds in real-time.

The algorithm uses the average_change variable to calculate the average price change of the nearest neighbors and adjusts the thresholds accordingly.

Wyszukaj w skryptach "algo"

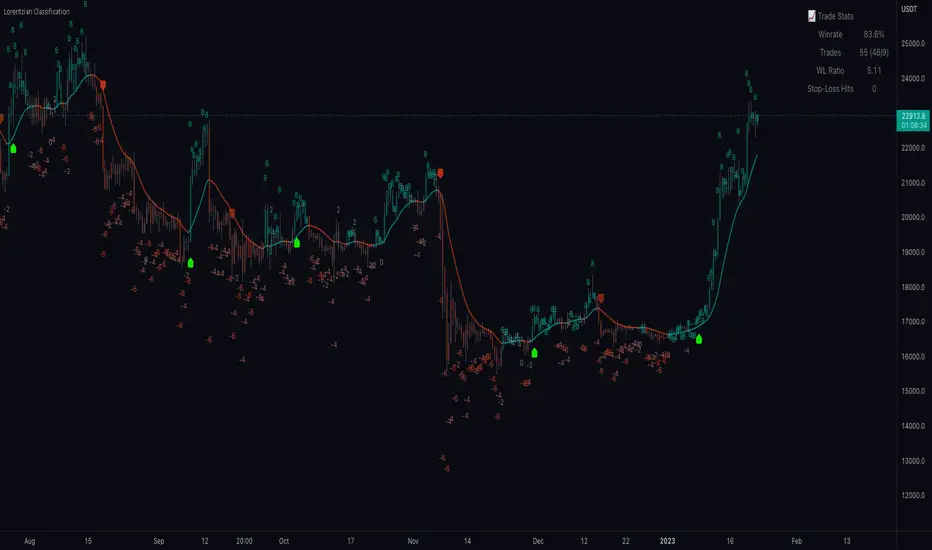

Machine Learning: Lorentzian Classification█ OVERVIEW

A Lorentzian Distance Classifier (LDC) is a Machine Learning classification algorithm capable of categorizing historical data from a multi-dimensional feature space. This indicator demonstrates how Lorentzian Classification can also be used to predict the direction of future price movements when used as the distance metric for a novel implementation of an Approximate Nearest Neighbors (ANN) algorithm.

█ BACKGROUND

In physics, Lorentzian space is perhaps best known for its role in describing the curvature of space-time in Einstein's theory of General Relativity (2). Interestingly, however, this abstract concept from theoretical physics also has tangible real-world applications in trading.

Recently, it was hypothesized that Lorentzian space was also well-suited for analyzing time-series data (4), (5). This hypothesis has been supported by several empirical studies that demonstrate that Lorentzian distance is more robust to outliers and noise than the more commonly used Euclidean distance (1), (3), (6). Furthermore, Lorentzian distance was also shown to outperform dozens of other highly regarded distance metrics, including Manhattan distance, Bhattacharyya similarity, and Cosine similarity (1), (3). Outside of Dynamic Time Warping based approaches, which are unfortunately too computationally intensive for PineScript at this time, the Lorentzian Distance metric consistently scores the highest mean accuracy over a wide variety of time series data sets (1).

Euclidean distance is commonly used as the default distance metric for NN-based search algorithms, but it may not always be the best choice when dealing with financial market data. This is because financial market data can be significantly impacted by proximity to major world events such as FOMC Meetings and Black Swan events. This event-based distortion of market data can be framed as similar to the gravitational warping caused by a massive object on the space-time continuum. For financial markets, the analogous continuum that experiences warping can be referred to as "price-time".

Below is a side-by-side comparison of how neighborhoods of similar historical points appear in three-dimensional Euclidean Space and Lorentzian Space:

This figure demonstrates how Lorentzian space can better accommodate the warping of price-time since the Lorentzian distance function compresses the Euclidean neighborhood in such a way that the new neighborhood distribution in Lorentzian space tends to cluster around each of the major feature axes in addition to the origin itself. This means that, even though some nearest neighbors will be the same regardless of the distance metric used, Lorentzian space will also allow for the consideration of historical points that would otherwise never be considered with a Euclidean distance metric.

Intuitively, the advantage inherent in the Lorentzian distance metric makes sense. For example, it is logical that the price action that occurs in the hours after Chairman Powell finishes delivering a speech would resemble at least some of the previous times when he finished delivering a speech. This may be true regardless of other factors, such as whether or not the market was overbought or oversold at the time or if the macro conditions were more bullish or bearish overall. These historical reference points are extremely valuable for predictive models, yet the Euclidean distance metric would miss these neighbors entirely, often in favor of irrelevant data points from the day before the event. By using Lorentzian distance as a metric, the ML model is instead able to consider the warping of price-time caused by the event and, ultimately, transcend the temporal bias imposed on it by the time series.

For more information on the implementation details of the Approximate Nearest Neighbors (ANN) algorithm used in this indicator, please refer to the detailed comments in the source code.

█ HOW TO USE

Below is an explanatory breakdown of the different parts of this indicator as it appears in the interface:

Below is an explanation of the different settings for this indicator:

General Settings:

Source - This has a default value of "hlc3" and is used to control the input data source.

Neighbors Count - This has a default value of 8, a minimum value of 1, a maximum value of 100, and a step of 1. It is used to control the number of neighbors to consider.

Max Bars Back - This has a default value of 2000.

Feature Count - This has a default value of 5, a minimum value of 2, and a maximum value of 5. It controls the number of features to use for ML predictions.

Color Compression - This has a default value of 1, a minimum value of 1, and a maximum value of 10. It is used to control the compression factor for adjusting the intensity of the color scale.

Show Exits - This has a default value of false. It controls whether to show the exit threshold on the chart.

Use Dynamic Exits - This has a default value of false. It is used to control whether to attempt to let profits ride by dynamically adjusting the exit threshold based on kernel regression.

Feature Engineering Settings:

Note: The Feature Engineering section is for fine-tuning the features used for ML predictions. The default values are optimized for the 4H to 12H timeframes for most charts, but they should also work reasonably well for other timeframes. By default, the model can support features that accept two parameters (Parameter A and Parameter B, respectively). Even though there are only 4 features provided by default, the same feature with different settings counts as two separate features. If the feature only accepts one parameter, then the second parameter will default to EMA-based smoothing with a default value of 1. These features represent the most effective combination I have encountered in my testing, but additional features may be added as additional options in the future.

Feature 1 - This has a default value of "RSI" and options are: "RSI", "WT", "CCI", "ADX".

Feature 2 - This has a default value of "WT" and options are: "RSI", "WT", "CCI", "ADX".

Feature 3 - This has a default value of "CCI" and options are: "RSI", "WT", "CCI", "ADX".

Feature 4 - This has a default value of "ADX" and options are: "RSI", "WT", "CCI", "ADX".

Feature 5 - This has a default value of "RSI" and options are: "RSI", "WT", "CCI", "ADX".

Filters Settings:

Use Volatility Filter - This has a default value of true. It is used to control whether to use the volatility filter.

Use Regime Filter - This has a default value of true. It is used to control whether to use the trend detection filter.

Use ADX Filter - This has a default value of false. It is used to control whether to use the ADX filter.

Regime Threshold - This has a default value of -0.1, a minimum value of -10, a maximum value of 10, and a step of 0.1. It is used to control the Regime Detection filter for detecting Trending/Ranging markets.

ADX Threshold - This has a default value of 20, a minimum value of 0, a maximum value of 100, and a step of 1. It is used to control the threshold for detecting Trending/Ranging markets.

Kernel Regression Settings:

Trade with Kernel - This has a default value of true. It is used to control whether to trade with the kernel.

Show Kernel Estimate - This has a default value of true. It is used to control whether to show the kernel estimate.

Lookback Window - This has a default value of 8 and a minimum value of 3. It is used to control the number of bars used for the estimation. Recommended range: 3-50

Relative Weighting - This has a default value of 8 and a step size of 0.25. It is used to control the relative weighting of time frames. Recommended range: 0.25-25

Start Regression at Bar - This has a default value of 25. It is used to control the bar index on which to start regression. Recommended range: 0-25

Display Settings:

Show Bar Colors - This has a default value of true. It is used to control whether to show the bar colors.

Show Bar Prediction Values - This has a default value of true. It controls whether to show the ML model's evaluation of each bar as an integer.

Use ATR Offset - This has a default value of false. It controls whether to use the ATR offset instead of the bar prediction offset.

Bar Prediction Offset - This has a default value of 0 and a minimum value of 0. It is used to control the offset of the bar predictions as a percentage from the bar high or close.

Backtesting Settings:

Show Backtest Results - This has a default value of true. It is used to control whether to display the win rate of the given configuration.

█ WORKS CITED

(1) R. Giusti and G. E. A. P. A. Batista, "An Empirical Comparison of Dissimilarity Measures for Time Series Classification," 2013 Brazilian Conference on Intelligent Systems, Oct. 2013, DOI: 10.1109/bracis.2013.22.

(2) Y. Kerimbekov, H. Ş. Bilge, and H. H. Uğurlu, "The use of Lorentzian distance metric in classification problems," Pattern Recognition Letters, vol. 84, 170–176, Dec. 2016, DOI: 10.1016/j.patrec.2016.09.006.

(3) A. Bagnall, A. Bostrom, J. Large, and J. Lines, "The Great Time Series Classification Bake Off: An Experimental Evaluation of Recently Proposed Algorithms." ResearchGate, Feb. 04, 2016.

(4) H. Ş. Bilge, Yerzhan Kerimbekov, and Hasan Hüseyin Uğurlu, "A new classification method by using Lorentzian distance metric," ResearchGate, Sep. 02, 2015.

(5) Y. Kerimbekov and H. Şakir Bilge, "Lorentzian Distance Classifier for Multiple Features," Proceedings of the 6th International Conference on Pattern Recognition Applications and Methods, 2017, DOI: 10.5220/0006197004930501.

(6) V. Surya Prasath et al., "Effects of Distance Measure Choice on KNN Classifier Performance - A Review." .

█ ACKNOWLEDGEMENTS

@veryfid - For many invaluable insights, discussions, and advice that helped to shape this project.

@capissimo - For open sourcing his interesting ideas regarding various KNN implementations in PineScript, several of which helped inspire my original undertaking of this project.

@RikkiTavi - For many invaluable physics-related conversations and for his helping me develop a mechanism for visualizing various distance algorithms in 3D using JavaScript

@jlaurel - For invaluable literature recommendations that helped me to understand the underlying subject matter of this project.

@annutara - For help in beta-testing this indicator and for sharing many helpful ideas and insights early on in its development.

@jasontaylor7 - For helping to beta-test this indicator and for many helpful conversations that helped to shape my backtesting workflow

@meddymarkusvanhala - For helping to beta-test this indicator

@dlbnext - For incredibly detailed backtesting testing of this indicator and for sharing numerous ideas on how the user experience could be improved.

Adaptive MA constructor [lastguru]Adaptive Moving Averages are nothing new, however most of them use EMA as their MA of choice once the preferred smoothing length is determined. I have decided to make an experiment and separate length generation from smoothing, offering multiple alternatives to be combined. Some of the combinations are widely known, some are not. This indicator is based on my previously published public libraries and also serve as a usage demonstration for them. I will try to expand the collection (suggestions are welcome), however it is not meant as an encyclopaedic resource, so you are encouraged to experiment yourself: by looking on the source code of this indicator, I am sure you will see how trivial it is to use the provided libraries and expand them with your own ideas and combinations. I give no recommendation on what settings to use, but if you find some useful setting, combination or application ideas (or bugs in my code), I would be happy to read about them in the comments section.

The indicator works in three stages: Prefiltering, Length Adaptation and Moving Averages.

Prefiltering is a fast smoothing to get rid of high-frequency (2, 3 or 4 bar) noise.

Adaptation algorithms are roughly subdivided in two categories: classic Length Adaptations and Cycle Estimators (they are also implemented in separate libraries), all are selected in Adaptation dropdown. Length Adaptation used in the Adaptive Moving Averages and the Adaptive Oscillators try to follow price movements and accelerate/decelerate accordingly (usually quite rapidly with a huge range). Cycle Estimators, on the other hand, try to measure the cycle period of the current market, which does not reflect price movement or the rate of change (the rate of change may also differ depending on the cycle phase, but the cycle period itself usually changes slowly).

Chande (Price) - based on Chande's Dynamic Momentum Index (CDMI or DYMOI), which is dynamic RSI with this length

Chande (Volume) - a variant of Chande's algorithm, where volume is used instead of price

VIDYA - based on VIDYA algorithm. The period oscillates from the Lower Bound up (slow)

VIDYA-RS - based on Vitali Apirine's modification of VIDYA algorithm (he calls it Relative Strength Moving Average). The period oscillates from the Upper Bound down (fast)

Kaufman Efficiency Scaling - based on Efficiency Ratio calculation originally used in KAMA

Deviation Scaling - based on DSSS by John F. Ehlers

Median Average - based on Median Average Adaptive Filter by John F. Ehlers

Fractal Adaptation - based on FRAMA by John F. Ehlers

MESA MAMA Alpha - based on MESA Adaptive Moving Average by John F. Ehlers

MESA MAMA Cycle - based on MESA Adaptive Moving Average by John F. Ehlers, but unlike Alpha calculation, this adaptation estimates cycle period

Pearson Autocorrelation* - based on Pearson Autocorrelation Periodogram by John F. Ehlers

DFT Cycle* - based on Discrete Fourier Transform Spectrum estimator by John F. Ehlers

Phase Accumulation* - based on Dominant Cycle from Phase Accumulation by John F. Ehlers

Length Adaptation usually take two parameters: Bound From (lower bound) and To (upper bound). These are the limits for Adaptation values. Note that the Cycle Estimators marked with asterisks(*) are very computationally intensive, so the bounds should not be set much higher than 50, otherwise you may receive a timeout error (also, it does not seem to be a useful thing to do, but you may correct me if I'm wrong).

The Cycle Estimators marked with asterisks(*) also have 3 checkboxes: HP (Highpass Filter), SS (Super Smoother) and HW (Hann Window). These enable or disable their internal prefilters, which are recommended by their author - John F. Ehlers. I do not know, which combination works best, so you can experiment.

Chande's Adaptations also have 3 additional parameters: SD Length (lookback length of Standard deviation), Smooth (smoothing length of Standard deviation) and Power (exponent of the length adaptation - lower is smaller variation). These are internal tweaks for the calculation.

Length Adaptaton section offer you a choice of Moving Average algorithms. Most of the Adaptations are originally used with EMA, so this is a good starting point for exploration.

SMA - Simple Moving Average

RMA - Running Moving Average

EMA - Exponential Moving Average

HMA - Hull Moving Average

VWMA - Volume Weighted Moving Average

2-pole Super Smoother - 2-pole Super Smoother by John F. Ehlers

3-pole Super Smoother - 3-pole Super Smoother by John F. Ehlers

Filt11 -a variant of 2-pole Super Smoother with error averaging for zero-lag response by John F. Ehlers

Triangle Window - Triangle Window Filter by John F. Ehlers

Hamming Window - Hamming Window Filter by John F. Ehlers

Hann Window - Hann Window Filter by John F. Ehlers

Lowpass - removes cyclic components shorter than length (Price - Highpass)

DSSS - Derivation Scaled Super Smoother by John F. Ehlers

There are two Moving Averages that are drown on the chart, so length for both needs to be selected. If no Adaptation is selected ( None option), you can set Fast Length and Slow Length directly. If an Adaptation is selected, then Cycle multiplier can be selected for Fast and Slow MA.

More information on the algorithms is given in the code for the libraries used. I am also very grateful to other TradingView community members (they are also mentioned in the library code) without whom this script would not have been possible.

Exotic SMA Explorations Treasure TroveThis is my "Exotic SMA Explorations Treasure Trove" intended for educational purposes, yet these functions will also have utility in special applications with other algorithms. Firstly, the Pine built-in sma() is exceedingly more efficient computationally on TV servers than these functions will be. I just wanted to make that very crystal clear. My notes elaborate on this in the code blatantly.

Anyhow, the simple moving average(SMA) is one of the most common averaging filters used in a wide variety of algorithms. "Simply put," it's name says a lot about it. The purpose of this script, is to demonstrate variations of it's calculation in a multitude of exotic forms. In certain scenarios our algorithms may require a specific mathemagical touch that is pertinent to our intended goals. Like screwdrivers, we often need different types depending on the objective we are trying to attain. The SMA also serves as the most basic of finite impulse response(FIR) algorithms. For example, things like weighted moving averages can be constructed by using the foundational code of SMA.

One other intended demonstration of this script, is running multiple functions for comparison. I have had to use this from time to time for my own comparisons of performance. Also, imbedded into this code is a method to generically and recklessly in this case, adapt an algorithm. I will warn you, RSI was NEVER intended to adapt an algorithm. It only serves as a crude method to display the versatility of these different algorithms, whether it be a benefit or hinderance concerning dynamic adaptability.

Lastly, this script shows the versatility of TV's NEW additions input(group=) and input(inline=) upgrades in action. The "Immense Power of Pine" is always evolving and will continue to do so, I assure you of that. We can now categorize our input()s without using the input(type=input.bool) hackTrick. Although, that still will have it's enduring versatility, at least for myself.

NOTICE: You have absolute freedom to use this source code any way you see fit within your new Pine projects. You don't have to ask for my permission to reuse these functions in your published scripts, simply because I have better things to do than answer requests for the reuse of these functions. Sufficient accreditation regarding this script and compliance with "TV's House Rules" regarding code reuse, is as easy as copying the functions in their entirety as is. Fair enough? Good!

When available time provides itself, I will consider your inquiries, thoughts, and concepts presented below in the comments section, should you have any questions or comments regarding this indicator. When my indicators achieve more prevalent use by TV members, I may implement more ideas when they present themselves as worthy additions. Have a profitable future everyone!

MLMatrixLibOverview

MLMatrixLib is a comprehensive Pine Script v6 library implementing machine learning algorithms using native matrix operations. This library provides traders and developers with a toolkit of statistical and ML methods for building quantitative trading systems, performing data analysis, and creating adaptive indicators.

How It Works

The library leverages Pine Script's native matrix type to perform efficient linear algebra operations. Each algorithm is implemented from first principles, using matrix decomposition, iterative optimization, and statistical estimation techniques. All functions are designed for numerical stability with careful handling of edge cases.

---

Library Contents (34 Sections)

Section 1: Utility Functions & Matrix Operations

Core building blocks including:

• identity(n) - Creates n×n identity matrix

• diagonal(values) - Creates diagonal matrix from array

• ones(rows, cols) / zeros(rows, cols) - Matrix constructors

• frobeniusNorm(m) / l1Norm(m) - Matrix norm calculations

• hadamard(m1, m2) - Element-wise multiplication

• columnMeans(m) / rowMeans(m) - Statistical aggregations

• standardize(m) - Z-score normalization (zero mean, unit variance)

• minMaxNormalize(m) - Scale values to range

• fitStandardScaler(m) / fitMinMaxScaler(m) - Reusable scaler parameters

• addBiasColumn(m) - Prepend column of ones for regression

• arrayMedian(arr) / arrayPercentile(arr, p) - Array statistics

Section 2: Activation Functions

Numerically stable implementations:

• sigmoid(x) / sigmoidMatrix(m) - Logistic function with overflow protection

• tanhActivation(x) / tanhMatrix(m) - Hyperbolic tangent

• relu(x) / reluMatrix(m) - Rectified Linear Unit

• leakyRelu(x, alpha) - Leaky ReLU with configurable slope

• elu(x, alpha) - Exponential Linear Unit

• Derivatives for backpropagation: sigmoidDerivative, tanhDerivative, reluDerivative

Section 3: Linear Regression (OLS)

Ordinary Least Squares implementation using the normal equation (X'X)⁻¹X'y:

• fitLinearRegression(X, y) - Fits model, returns coefficients, R², standard error

• fitSimpleLinearRegression(x, y) - Single-variable regression

• predictLinear(model, X) - Generate predictions

• predictionInterval(model, X, confidence) - Confidence intervals using t-distribution

• Model type stores: coefficients, R-squared, residuals, standard error

Section 4: Weighted Linear Regression

Generalized least squares with observation weights:

• fitWeightedLinearRegression(X, y, weights) - Solves (X'WX)⁻¹X'Wy

• Useful for downweighting outliers or emphasizing recent data

Section 5: Polynomial Regression

Fits polynomials of arbitrary degree:

• fitPolynomialRegression(x, y, degree) - Constructs Vandermonde matrix

• predictPolynomial(model, x) - Evaluate polynomial at points

Section 6: Ridge Regression (L2 Regularization)

Adds penalty term λ||β||² to prevent overfitting:

• fitRidgeRegression(X, y, lambda) - Solves (X'X + λI)⁻¹X'y

• Lambda parameter controls regularization strength

Section 7: LASSO Regression (L1 Regularization)

Coordinate descent algorithm for sparse solutions:

• fitLassoRegression(X, y, lambda, maxIter, tolerance) - Iterative soft-thresholding

• Produces sparse coefficients by driving some to exactly zero

• softThreshold(x, lambda) - Core shrinkage operator

Section 8: Elastic Net (L1 + L2 Regularization)

Combines LASSO and Ridge penalties:

• fitElasticNet(X, y, lambda, alpha, maxIter, tolerance)

• Alpha balances L1 vs L2: alpha=1 is LASSO, alpha=0 is Ridge

Section 9: Huber Robust Regression

Iteratively Reweighted Least Squares (IRLS) for outlier resistance:

• fitHuberRegression(X, y, delta, maxIter, tolerance)

• Delta parameter defines transition between L1 and L2 loss

• Downweights observations with large residuals

Section 10: Quantile Regression

Estimates conditional quantiles using linear programming approximation:

• fitQuantileRegression(X, y, tau, maxIter, tolerance)

• Tau specifies quantile (0.5 = median, 0.25 = lower quartile, etc.)

Section 11: Logistic Regression (Binary Classification)

Gradient descent optimization of cross-entropy loss:

• fitLogisticRegression(X, y, learningRate, maxIter, tolerance)

• predictProbability(model, X) - Returns probabilities

• predictClass(model, X, threshold) - Returns binary predictions

Section 12: Linear SVM (Support Vector Machine)

Sub-gradient descent with hinge loss:

• fitLinearSVM(X, y, C, learningRate, maxIter)

• C parameter controls regularization (higher = harder margin)

• predictSVM(model, X) - Returns class predictions

Section 13: Recursive Least Squares (RLS)

Online learning with exponential forgetting:

• createRLSState(nFeatures, lambda, delta) - Initialize state

• updateRLS(state, x, y) - Update with new observation

• Lambda is forgetting factor (0.95-0.99 typical)

• Useful for adaptive indicators that update incrementally

Section 14: Covariance and Correlation

Matrix statistics:

• covarianceMatrix(m) - Sample covariance

• correlationMatrix(m) - Pearson correlations

• pearsonCorrelation(x, y) - Single correlation coefficient

• spearmanCorrelation(x, y) - Rank-based correlation

Section 15: Principal Component Analysis (PCA)

Dimensionality reduction via eigendecomposition:

• fitPCA(X, nComponents) - Power iteration method

• transformPCA(X, model) - Project data onto principal components

• Returns components, explained variance, and mean

Section 16: K-Means Clustering

Lloyd's algorithm with k-means++ initialization:

• fitKMeans(X, k, maxIter, tolerance) - Cluster data points

• predictCluster(model, X) - Assign new points to clusters

• withinClusterVariance(model) - Measure cluster compactness

Section 17: Gaussian Mixture Model (GMM)

Expectation-Maximization algorithm:

• fitGMM(X, k, maxIter, tolerance) - Soft clustering with probabilities

• predictProbaGMM(model, X) - Returns membership probabilities

• Models data as mixture of Gaussian distributions

Section 18: Kalman Filter

Linear state estimation:

• createKalman1D(processNoise, measurementNoise, ...) - 1D filter

• createKalman2D(processNoise, measurementNoise) - Position + velocity tracking

• kalmanStep(state, measurement) - Predict-update cycle

• Optimal filtering for noisy measurements

Section 19: K-Nearest Neighbors (KNN)

Instance-based learning:

• fitKNN(X, y) - Store training data

• predictKNN(model, X, k) - Classify by majority vote

• predictKNNRegression(model, X, k) - Average of k neighbors

• predictKNNWeighted(model, X, k) - Distance-weighted voting

Section 20: Neural Network (Feedforward)

Multi-layer perceptron:

• createNeuralNetwork(architecture) - Define layer sizes

• trainNeuralNetwork(nn, X, y, learningRate, epochs) - Backpropagation

• predictNN(nn, X) - Forward pass

• Supports configurable hidden layers

Section 21: Naive Bayes Classifier

Gaussian Naive Bayes:

• fitNaiveBayes(X, y) - Estimate class-conditional distributions

• predictNaiveBayes(model, X) - Maximum a posteriori classification

• Assumes feature independence given class

Section 22: Anomaly Detection

Statistical outlier detection:

• fitAnomalyDetector(X, contamination) - Mahalanobis distance-based

• detectAnomalies(model, X) - Returns anomaly scores

• isAnomaly(model, X, threshold) - Binary classification

Section 23: Dynamic Time Warping (DTW)

Time series similarity:

• dtw(series1, series2) - Compute DTW distance

• Handles sequences of different lengths

• Useful for pattern matching

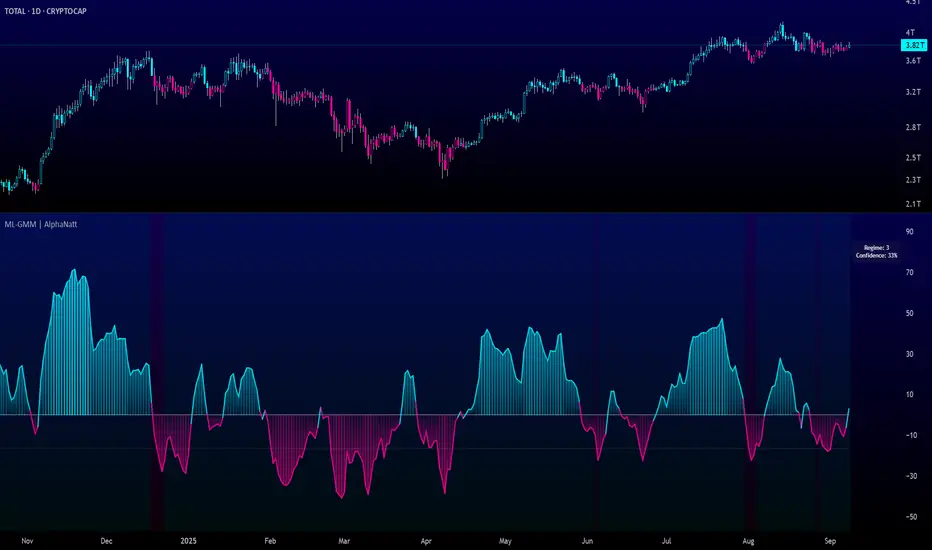

Section 24: Markov Chain / Regime Detection

Discrete state transitions:

• fitMarkovChain(states, nStates) - Estimate transition matrix

• predictNextState(transitionMatrix, currentState) - Most likely next state

• stationaryDistribution(transitionMatrix) - Long-run probabilities

Section 25: Hidden Markov Model (Simple)

Baum-Welch algorithm:

• fitHMM(observations, nStates, maxIter) - EM training

• viterbi(model, observations) - Most likely state sequence

• Useful for regime detection

Section 26: Exponential Smoothing & Holt-Winters

Time series smoothing:

• exponentialSmooth(data, alpha) - Simple exponential smoothing

• holtWinters(data, alpha, beta, gamma, seasonLength) - Triple smoothing

• Captures trend and seasonality

Section 27: Entropy and Information Theory

Information measures:

• entropy(probabilities) - Shannon entropy in bits

• conditionalEntropy(jointProbs, marginalProbs) - H(X|Y)

• mutualInformation(probsX, probsY, jointProbs) - I(X;Y)

• kldivergence(p, q) - Kullback-Leibler divergence

Section 28: Hurst Exponent

Long-range dependence measure:

• hurstExponent(data) - R/S analysis

• H < 0.5: mean-reverting, H = 0.5: random walk, H > 0.5: trending

Section 29: Change Detection (CUSUM)

Cumulative sum control chart:

• cusumChangeDetection(data, threshold, drift) - Detect regime changes

• cusumOnline(value, prevCusumPos, prevCusumNeg, target, drift) - Streaming version

Section 30: Autocorrelation

Serial dependence analysis:

• autocorrelation(data, maxLag) - ACF for all lags

• partialAutocorrelation(data, maxLag) - PACF via Durbin-Levinson

• Useful for time series model identification

Section 31: Ensemble Methods

Model combination:

• baggingPredict(models, X) - Average predictions

• votingClassify(models, X) - Majority vote

• Improves robustness through aggregation

Section 32: Model Evaluation Metrics

Performance assessment:

• mse(actual, predicted) / rmse / mae / mape - Regression metrics

• accuracy(actual, predicted) - Classification accuracy

• precision / recall / f1Score - Binary classification metrics

• confusionMatrix(actual, predicted, nClasses) - Multi-class evaluation

• rSquared(actual, predicted) / adjustedRSquared - Goodness of fit

Section 33: Cross-Validation

Model validation:

• trainTestSplit(X, y, trainRatio) - Random split

• Foundation for walk-forward validation

Section 34: Trading Convenience Functions

Trading-specific utilities:

• priceMatrix(length) - OHLC data as matrix

• logReturns(length) - Log return series

• rollingSlope(src, length) - Linear trend strength

• kalmanFilter(src, processNoise, measurementNoise) - Filtered price

• kalmanFilter2D(src, ...) - Price with velocity estimate

• adaptiveMA(src, sensitivity) - Kalman-based adaptive moving average

• volAdjMomentum(src, length) - Volatility-normalized momentum

• detectSRLevels(length, nLevels) - K-means based S/R detection

• buildFeatures(src, lengths) - Multi-timeframe feature construction

• technicalFeatures(length) - Standard indicator feature set (RSI, MACD, BB, ATR, etc.)

• lagFeatures(src, lags) - Time-lagged features

• sharpeRatio(returns) - Risk-adjusted return measure

• sortinoRatio(returns) - Downside risk-adjusted return

• maxDrawdown(equity) - Maximum peak-to-trough decline

• calmarRatio(returns, equity) - Return/drawdown ratio

• kellyCriterion(winRate, avgWin, avgLoss) - Optimal position sizing

• fractionalKelly(...) - Conservative Kelly sizing

• rollingBeta(assetReturns, benchmarkReturns) - Market exposure

• fractalDimension(data) - Market complexity measure

---

Usage Example

```

import YourUsername/MLMatrixLib/1 as ml

// Create feature matrix

matrix X = ml.priceMatrix(50)

X := ml.standardize(X)

// Fit linear regression

ml.LinearRegressionModel model = ml.fitLinearRegression(X, y)

float prediction = ml.predictLinear(model, X_new)

// Kalman filter for smoothing

float smoothedPrice = ml.kalmanFilter(close, 0.01, 1.0)

// Detect support/resistance levels

array levels = ml.detectSRLevels(100, 3)

// K-means clustering for regime detection

ml.KMeansModel km = ml.fitKMeans(features, 3)

int cluster = ml.predictCluster(km, newFeature)

```

---

Technical Notes

• All matrix operations use Pine Script's native matrix type

• Numerical stability ensured through:

- Clamping exponential arguments to prevent overflow

- Division by zero protection with epsilon thresholds

- Iterative algorithms with convergence tolerance

• Designed for bar-by-bar execution in Pine Script's event-driven model

• Compatible with Pine Script v6

---

Disclaimer

This library provides mathematical tools for quantitative analysis. It does not constitute financial advice. Past performance of any algorithm does not guarantee future results. Users are responsible for validating models on their specific use cases and understanding the limitations of each method.

Adaptive Genesis Engine [AGE]ADAPTIVE GENESIS ENGINE (AGE)

Pure Signal Evolution Through Genetic Algorithms

Where Darwin Meets Technical Analysis

🧬 WHAT YOU'RE GETTING - THE PURE INDICATOR

This is a technical analysis indicator - it generates signals, visualizes probability, and shows you the evolutionary process in real-time. This is NOT a strategy with automatic execution - it's a sophisticated signal generation system that you control .

What This Indicator Does:

Generates Long/Short entry signals with probability scores (35-88% range)

Evolves a population of up to 12 competing strategies using genetic algorithms

Validates strategies through walk-forward optimization (train/test cycles)

Visualizes signal quality through premium gradient clouds and confidence halos

Displays comprehensive metrics via enhanced dashboard

Provides alerts for entries and exits

Works on any timeframe, any instrument, any broker

What This Indicator Does NOT Do:

Execute trades automatically

Manage positions or calculate position sizes

Place orders on your behalf

Make trading decisions for you

This is pure signal intelligence. AGE tells you when and how confident it is. You decide whether and how much to trade.

🔬 THE SCIENCE: GENETIC ALGORITHMS MEET TECHNICAL ANALYSIS

What Makes This Different - The Evolutionary Foundation

Most indicators are static - they use the same parameters forever, regardless of market conditions. AGE is alive . It maintains a population of competing strategies that evolve, adapt, and improve through natural selection principles:

Birth: New strategies spawn through crossover breeding (combining DNA from fit parents) plus random mutation for exploration

Life: Each strategy trades virtually via shadow portfolios, accumulating wins/losses, tracking drawdown, and building performance history

Selection: Strategies are ranked by comprehensive fitness scoring (win rate, expectancy, drawdown control, signal efficiency)

Death: Weak strategies are culled periodically, with elite performers (top 2 by default) protected from removal

Evolution: The gene pool continuously improves as successful traits propagate and unsuccessful ones die out

This is not curve-fitting. Each new strategy must prove itself on out-of-sample data through walk-forward validation before being trusted for live signals.

🧪 THE DNA: WHAT EVOLVES

Every strategy carries a 10-gene chromosome controlling how it interprets market data:

Signal Sensitivity Genes

Entropy Sensitivity (0.5-2.0): Weight given to market order/disorder calculations. Low values = conservative, require strong directional clarity. High values = aggressive, act on weaker order signals.

Momentum Sensitivity (0.5-2.0): Weight given to RSI/ROC/MACD composite. Controls responsiveness to momentum shifts vs. mean-reversion setups.

Structure Sensitivity (0.5-2.0): Weight given to support/resistance positioning. Determines how much price location within swing range matters.

Probability Adjustment Genes

Probability Boost (-0.10 to +0.10): Inherent bias toward aggressive (+) or conservative (-) entries. Acts as personality trait - some strategies naturally optimistic, others pessimistic.

Trend Strength Requirement (0.3-0.8): Minimum trend conviction needed before signaling. Higher values = only trades strong trends, lower values = acts in weak/sideways markets.

Volume Filter (0.5-1.5): Strictness of volume confirmation. Higher values = requires strong volume, lower values = volume less important.

Risk Management Genes

ATR Multiplier (1.5-4.0): Base volatility scaling for all price levels. Controls whether strategy uses tight or wide stops/targets relative to ATR.

Stop Multiplier (1.0-2.5): Stop loss tightness. Lower values = aggressive profit protection, higher values = more breathing room.

Target Multiplier (1.5-4.0): Profit target ambition. Lower values = quick scalping exits, higher values = swing trading holds.

Adaptation Gene

Regime Adaptation (0.0-1.0): How much strategy adjusts behavior based on detected market regime (trending/volatile/choppy). Higher values = more reactive to regime changes.

The Magic: AGE doesn't just try random combinations. Through tournament selection and fitness-weighted crossover, successful gene combinations spread through the population while unsuccessful ones fade away. Over 50-100 bars, you'll see the population converge toward genes that work for YOUR instrument and timeframe.

📊 THE SIGNAL ENGINE: THREE-LAYER SYNTHESIS

Before any strategy generates a signal, AGE calculates probability through multi-indicator confluence:

Layer 1 - Market Entropy (Information Theory)

Measures whether price movements exhibit directional order or random walk characteristics:

The Math:

Shannon Entropy = -Σ(p × log(p))

Market Order = 1 - (Entropy / 0.693)

What It Means:

High entropy = choppy, random market → low confidence signals

Low entropy = directional market → high confidence signals

Direction determined by up-move vs down-move dominance over lookback period (default: 20 bars)

Signal Output: -1.0 to +1.0 (bearish order to bullish order)

Layer 2 - Momentum Synthesis

Combines three momentum indicators into single composite score:

Components:

RSI (40% weight): Normalized to -1/+1 scale using (RSI-50)/50

Rate of Change (30% weight): Percentage change over lookback (default: 14 bars), clamped to ±1

MACD Histogram (30% weight): Fast(12) - Slow(26), normalized by ATR

Why This Matters: RSI catches mean-reversion opportunities, ROC catches raw momentum, MACD catches momentum divergence. Weighting favors RSI for reliability while keeping other perspectives.

Signal Output: -1.0 to +1.0 (strong bearish to strong bullish)

Layer 3 - Structure Analysis

Evaluates price position within swing range (default: 50-bar lookback):

Position Classification:

Bottom 20% of range = Support Zone → bullish bounce potential

Top 20% of range = Resistance Zone → bearish rejection potential

Middle 60% = Neutral Zone → breakout/breakdown monitoring

Signal Logic:

At support + bullish candle = +0.7 (strong buy setup)

At resistance + bearish candle = -0.7 (strong sell setup)

Breaking above range highs = +0.5 (breakout confirmation)

Breaking below range lows = -0.5 (breakdown confirmation)

Consolidation within range = ±0.3 (weak directional bias)

Signal Output: -1.0 to +1.0 (bearish structure to bullish structure)

Confluence Voting System

Each layer casts a vote (Long/Short/Neutral). The system requires minimum 2-of-3 agreement (configurable 1-3) before generating a signal:

Examples:

Entropy: Bullish, Momentum: Bullish, Structure: Neutral → Signal generated (2 long votes)

Entropy: Bearish, Momentum: Neutral, Structure: Neutral → No signal (only 1 short vote)

All three bullish → Signal generated with +5% probability bonus

This is the key to quality. Single indicators give too many false signals. Triple confirmation dramatically improves accuracy.

📈 PROBABILITY CALCULATION: HOW CONFIDENCE IS MEASURED

Base Probability:

Raw_Prob = 50% + (Average_Signal_Strength × 25%)

Then AGE applies strategic adjustments:

Trend Alignment:

Signal with trend: +4%

Signal against strong trend: -8%

Weak/no trend: no adjustment

Regime Adaptation:

Trending market (efficiency >50%, moderate vol): +3%

Volatile market (vol ratio >1.5x): -5%

Choppy market (low efficiency): -2%

Volume Confirmation:

Volume > 70% of 20-bar SMA: no change

Volume below threshold: -3%

Volatility State (DVS Ratio):

High vol (>1.8x baseline): -4% (reduce confidence in chaos)

Low vol (<0.7x baseline): -2% (markets can whipsaw in compression)

Moderate elevated vol (1.0-1.3x): +2% (trending conditions emerging)

Confluence Bonus:

All 3 indicators agree: +5%

2 of 3 agree: +2%

Strategy Gene Adjustment:

Probability Boost gene: -10% to +10%

Regime Adaptation gene: scales regime adjustments by 0-100%

Final Probability: Clamped between 35% (minimum) and 88% (maximum)

Why These Ranges?

Below 35% = too uncertain, better not to signal

Above 88% = unrealistic, creates overconfidence

Sweet spot: 65-80% for quality entries

🔄 THE SHADOW PORTFOLIO SYSTEM: HOW STRATEGIES COMPETE

Each active strategy maintains a virtual trading account that executes in parallel with real-time data:

Shadow Trading Mechanics

Entry Logic:

Calculate signal direction, probability, and confluence using strategy's unique DNA

Check if signal meets quality gate:

Probability ≥ configured minimum threshold (default: 65%)

Confluence ≥ configured minimum (default: 2 of 3)

Direction is not zero (must be long or short, not neutral)

Verify signal persistence:

Base requirement: 2 bars (configurable 1-5)

Adapts based on probability: high-prob signals (75%+) enter 1 bar faster, low-prob signals need 1 bar more

Adjusts for regime: trending markets reduce persistence by 1, volatile markets add 1

Apply additional filters:

Trend strength must exceed strategy's requirement gene

Regime filter: if volatile market detected, probability must be 72%+ to override

Volume confirmation required (volume > 70% of average)

If all conditions met for required persistence bars, enter shadow position at current close price

Position Management:

Entry Price: Recorded at close of entry bar

Stop Loss: ATR-based distance = ATR × ATR_Mult (gene) × Stop_Mult (gene) × DVS_Ratio

Take Profit: ATR-based distance = ATR × ATR_Mult (gene) × Target_Mult (gene) × DVS_Ratio

Position: +1 (long) or -1 (short), only one at a time per strategy

Exit Logic:

Check if price hit stop (on low) or target (on high) on current bar

Record trade outcome in R-multiples (profit/loss normalized by ATR)

Update performance metrics:

Total trades counter incremented

Wins counter (if profit > 0)

Cumulative P&L updated

Peak equity tracked (for drawdown calculation)

Maximum drawdown from peak recorded

Enter cooldown period (default: 8 bars, configurable 3-20) before next entry allowed

Reset signal age counter to zero

Walk-Forward Tracking:

During position lifecycle, trades are categorized:

Training Phase (first 250 bars): Trade counted toward training metrics

Testing Phase (next 75 bars): Trade counted toward testing metrics (out-of-sample)

Live Phase (after WFO period): Trade counted toward overall metrics

Why Shadow Portfolios?

No lookahead bias (uses only data available at the bar)

Realistic execution simulation (entry on close, stop/target checks on high/low)

Independent performance tracking for true fitness comparison

Allows safe experimentation without risking capital

Each strategy learns from its own experience

🏆 FITNESS SCORING: HOW STRATEGIES ARE RANKED

Fitness is not just win rate. AGE uses a comprehensive multi-factor scoring system:

Core Metrics (Minimum 3 trades required)

Win Rate (30% of fitness):

WinRate = Wins / TotalTrades

Normalized directly (0.0-1.0 scale)

Total P&L (30% of fitness):

Normalized_PnL = (PnL + 300) / 600

Clamped 0.0-1.0. Assumes P&L range of -300R to +300R for normalization scale.

Expectancy (25% of fitness):

Expectancy = Total_PnL / Total_Trades

Normalized_Expectancy = (Expectancy + 30) / 60

Clamped 0.0-1.0. Rewards consistency of profit per trade.

Drawdown Control (15% of fitness):

Normalized_DD = 1 - (Max_Drawdown / 15)

Clamped 0.0-1.0. Penalizes strategies that suffer large equity retracements from peak.

Sample Size Adjustment

Quality Factor:

<50 trades: 1.0 (full weight, small sample)

50-100 trades: 0.95 (slight penalty for medium sample)

100 trades: 0.85 (larger penalty for large sample)

Why penalize more trades? Prevents strategies from gaming the system by taking hundreds of tiny trades to inflate statistics. Favors quality over quantity.

Bonus Adjustments

Walk-Forward Validation Bonus:

if (WFO_Validated):

Fitness += (WFO_Efficiency - 0.5) × 0.1

Strategies proven on out-of-sample data receive up to +10% fitness boost based on test/train efficiency ratio.

Signal Efficiency Bonus (if diagnostics enabled):

if (Signals_Evaluated > 10):

Pass_Rate = Signals_Passed / Signals_Evaluated

Fitness += (Pass_Rate - 0.1) × 0.05

Rewards strategies that generate high-quality signals passing the quality gate, not just profitable trades.

Final Fitness: Clamped at 0.0 minimum (prevents negative fitness values)

Result: Elite strategies typically achieve 0.50-0.75 fitness. Anything above 0.60 is excellent. Below 0.30 is prime candidate for culling.

🔬 WALK-FORWARD OPTIMIZATION: ANTI-OVERFITTING PROTECTION

This is what separates AGE from curve-fitted garbage indicators.

The Three-Phase Process

Every new strategy undergoes a rigorous validation lifecycle:

Phase 1 - Training Window (First 250 bars, configurable 100-500):

Strategy trades normally via shadow portfolio

All trades count toward training performance metrics

System learns which gene combinations produce profitable patterns

Tracks independently: Training_Trades, Training_Wins, Training_PnL

Phase 2 - Testing Window (Next 75 bars, configurable 30-200):

Strategy continues trading without any parameter changes

Trades now count toward testing performance metrics (separate tracking)

This is out-of-sample data - strategy has never seen these bars during "optimization"

Tracks independently: Testing_Trades, Testing_Wins, Testing_PnL

Phase 3 - Validation Check:

Minimum_Trades = 5 (configurable 3-15)

IF (Train_Trades >= Minimum AND Test_Trades >= Minimum):

WR_Efficiency = Test_WinRate / Train_WinRate

Expectancy_Efficiency = Test_Expectancy / Train_Expectancy

WFO_Efficiency = (WR_Efficiency + Expectancy_Efficiency) / 2

IF (WFO_Efficiency >= 0.55): // configurable 0.3-0.9

Strategy.Validated = TRUE

Strategy receives fitness bonus

ELSE:

Strategy receives 30% fitness penalty

ELSE:

Validation deferred (insufficient trades in one or both periods)

What Validation Means

Validated Strategy (Green "✓ VAL" in dashboard):

Performed at least 55% as well on unseen data compared to training data

Gets fitness bonus: +(efficiency - 0.5) × 0.1

Receives priority during tournament selection for breeding

More likely to be chosen as active trading strategy

Unvalidated Strategy (Orange "○ TRAIN" in dashboard):

Failed to maintain performance on test data (likely curve-fitted to training period)

Receives 30% fitness penalty (0.7x multiplier)

Makes strategy prime candidate for culling

Can still trade but with lower selection probability

Insufficient Data (continues collecting):

Hasn't completed both training and testing periods yet

OR hasn't achieved minimum trade count in both periods

Validation check deferred until requirements met

Why 55% Efficiency Threshold?

If a strategy earned 10R during training but only 5.5R during testing, it still proved an edge exists beyond random luck. Requiring 100% efficiency would be unrealistic - market conditions change between periods. But requiring >50% ensures the strategy didn't completely degrade on fresh data.

The Protection: Strategies that work great on historical data but fail on new data are automatically identified and penalized. This prevents the population from being polluted by overfitted strategies that would fail in live trading.

🌊 DYNAMIC VOLATILITY SCALING (DVS): ADAPTIVE STOP/TARGET PLACEMENT

AGE doesn't use fixed stop distances. It adapts to current volatility conditions in real-time.

Four Volatility Measurement Methods

1. ATR Ratio (Simple Method):

Current_Vol = ATR(14) / Close

Baseline_Vol = SMA(Current_Vol, 100)

Ratio = Current_Vol / Baseline_Vol

Basic comparison of current ATR to 100-bar moving average baseline.

2. Parkinson (High-Low Range Based):

For each bar: HL = log(High / Low)

Parkinson_Vol = sqrt(Σ(HL²) / (4 × Period × log(2)))

More stable than close-to-close volatility. Captures intraday range expansion without overnight gap noise.

3. Garman-Klass (OHLC Based):

HL_Term = 0.5 × ²

CO_Term = (2×log(2) - 1) × ²

GK_Vol = sqrt(Σ(HL_Term - CO_Term) / Period)

Most sophisticated estimator. Incorporates all four price points (open, high, low, close) plus gap information.

4. Ensemble Method (Default - Median of All Three):

Ratio_1 = ATR_Current / ATR_Baseline

Ratio_2 = Parkinson_Current / Parkinson_Baseline

Ratio_3 = GK_Current / GK_Baseline

DVS_Ratio = Median(Ratio_1, Ratio_2, Ratio_3)

Why Ensemble?

Takes median to avoid outliers and false spikes

If ATR jumps but range-based methods stay calm, median prevents overreaction

If one method fails, other two compensate

Most robust approach across different market conditions

Sensitivity Scaling

Scaled_Ratio = (Raw_Ratio) ^ Sensitivity

Sensitivity 0.3: Cube root - heavily dampens volatility impact

Sensitivity 0.5: Square root - moderate dampening

Sensitivity 0.7 (Default): Balanced response to volatility changes

Sensitivity 1.0: Linear - full 1:1 volatility impact

Sensitivity 1.5: Exponential - amplified response to volatility spikes

Safety Clamps: Final DVS Ratio always clamped between 0.5x and 2.5x baseline to prevent extreme position sizing or stop placement errors.

How DVS Affects Shadow Trading

Every strategy's stop and target distances are multiplied by the current DVS ratio:

Stop Loss Distance:

Stop_Distance = ATR × ATR_Mult (gene) × Stop_Mult (gene) × DVS_Ratio

Take Profit Distance:

Target_Distance = ATR × ATR_Mult (gene) × Target_Mult (gene) × DVS_Ratio

Example Scenario:

ATR = 10 points

Strategy's ATR_Mult gene = 2.5

Strategy's Stop_Mult gene = 1.5

Strategy's Target_Mult gene = 2.5

DVS_Ratio = 1.4 (40% above baseline volatility - market heating up)

Stop = 10 × 2.5 × 1.5 × 1.4 = 52.5 points (vs. 37.5 in normal vol)

Target = 10 × 2.5 × 2.5 × 1.4 = 87.5 points (vs. 62.5 in normal vol)

Result:

During volatility spikes: Stops automatically widen to avoid noise-based exits, targets extend for bigger moves

During calm periods: Stops tighten for better risk/reward, targets compress for realistic profit-taking

Strategies adapt risk management to match current market behavior

🧬 THE EVOLUTIONARY CYCLE: SPAWN, COMPETE, CULL

Initialization (Bar 1)

AGE begins with 4 seed strategies (if evolution enabled):

Seed Strategy #0 (Balanced):

All sensitivities at 1.0 (neutral)

Zero probability boost

Moderate trend requirement (0.4)

Standard ATR/stop/target multiples (2.5/1.5/2.5)

Mid-level regime adaptation (0.5)

Seed Strategy #1 (Momentum-Focused):

Lower entropy sensitivity (0.7), higher momentum (1.5)

Slight probability boost (+0.03)

Higher trend requirement (0.5)

Tighter stops (1.3), wider targets (3.0)

Seed Strategy #2 (Entropy-Driven):

Higher entropy sensitivity (1.5), lower momentum (0.8)

Slight probability penalty (-0.02)

More trend tolerant (0.6)

Wider stops (1.8), standard targets (2.5)

Seed Strategy #3 (Structure-Based):

Balanced entropy/momentum (0.8/0.9), high structure (1.4)

Slight probability boost (+0.02)

Lower trend requirement (0.35)

Moderate risk parameters (1.6/2.8)

All seeds start with WFO validation bypassed if WFO is disabled, or must validate if enabled.

Spawning New Strategies

Timing (Adaptive):

Historical phase: Every 30 bars (configurable 10-100)

Live phase: Every 200 bars (configurable 100-500)

Automatically switches to live timing when barstate.isrealtime triggers

Conditions:

Current population < max population limit (default: 8, configurable 4-12)

At least 2 active strategies exist (need parents)

Available slot in population array

Selection Process:

Run tournament selection 3 times with different seeds

Each tournament: randomly sample active strategies, pick highest fitness

Best from 3 tournaments becomes Parent 1

Repeat independently for Parent 2

Ensures fit parents but maintains diversity

Crossover Breeding:

For each of 10 genes:

Parent1_Fitness = fitness

Parent2_Fitness = fitness

Weight1 = Parent1_Fitness / (Parent1_Fitness + Parent2_Fitness)

Gene1 = parent1's value

Gene2 = parent2's value

Child_Gene = Weight1 × Gene1 + (1 - Weight1) × Gene2

Fitness-weighted crossover ensures fitter parent contributes more genetic material.

Mutation:

For each gene in child:

IF (random < mutation_rate):

Gene_Range = GENE_MAX - GENE_MIN

Noise = (random - 0.5) × 2 × mutation_strength × Gene_Range

Mutated_Gene = Clamp(Child_Gene + Noise, GENE_MIN, GENE_MAX)

Historical mutation rate: 20% (aggressive exploration)

Live mutation rate: 8% (conservative stability)

Mutation strength: 12% of gene range (configurable 5-25%)

Initialization of New Strategy:

Unique ID assigned (total_spawned counter)

Parent ID recorded

Generation = max(parent generations) + 1

Birth bar recorded (for age tracking)

All performance metrics zeroed

Shadow portfolio reset

WFO validation flag set to false (must prove itself)

Result: New strategy with hybrid DNA enters population, begins trading in next bar.

Competition (Every Bar)

All active strategies:

Calculate their signal based on unique DNA

Check quality gate with their thresholds

Manage shadow positions (entries/exits)

Update performance metrics

Recalculate fitness score

Track WFO validation progress

Strategies compete indirectly through fitness ranking - no direct interaction.

Culling Weak Strategies

Timing (Adaptive):

Historical phase: Every 60 bars (configurable 20-200, should be 2x spawn interval)

Live phase: Every 400 bars (configurable 200-1000, should be 2x spawn interval)

Minimum Adaptation Score (MAS):

Initial MAS = 0.10

MAS decays: MAS × 0.995 every cull cycle

Minimum MAS = 0.03 (floor)

MAS represents the "survival threshold" - strategies below this fitness level are vulnerable.

Culling Conditions (ALL must be true):

Population > minimum population (default: 3, configurable 2-4)

At least one strategy has fitness < MAS

Strategy's age > culling interval (prevents premature culling of new strategies)

Strategy is not in top N elite (default: 2, configurable 1-3)

Culling Process:

Find worst strategy:

For each active strategy:

IF (age > cull_interval):

Fitness = base_fitness

IF (not WFO_validated AND WFO_enabled):

Fitness × 0.7 // 30% penalty for unvalidated

IF (Fitness < MAS AND Fitness < worst_fitness_found):

worst_strategy = this_strategy

worst_fitness = Fitness

IF (worst_strategy found):

Count elite strategies with fitness > worst_fitness

IF (elite_count >= elite_preservation_count):

Deactivate worst_strategy (set active flag = false)

Increment total_culled counter

Elite Protection:

Even if a strategy's fitness falls below MAS, it survives if fewer than N strategies are better. This prevents culling when population is generally weak.

Result: Weak strategies removed from population, freeing slots for new spawns. Gene pool improves over time.

Selection for Display (Every Bar)

AGE chooses one strategy to display signals:

Best fitness = -1

Selected = none

For each active strategy:

Fitness = base_fitness

IF (WFO_validated):

Fitness × 1.3 // 30% bonus for validated strategies

IF (Fitness > best_fitness):

best_fitness = Fitness

selected_strategy = this_strategy

Display selected strategy's signals on chart

Result: Only the highest-fitness (optionally validated-boosted) strategy's signals appear as chart markers. Other strategies trade invisibly in shadow portfolios.

🎨 PREMIUM VISUALIZATION SYSTEM

AGE includes sophisticated visual feedback that standard indicators lack:

1. Gradient Probability Cloud (Optional, Default: ON)

Multi-layer gradient showing signal buildup 2-3 bars before entry:

Activation Conditions:

Signal persistence > 0 (same directional signal held for multiple bars)

Signal probability ≥ minimum threshold (65% by default)

Signal hasn't yet executed (still in "forming" state)

Visual Construction:

7 gradient layers by default (configurable 3-15)

Each layer is a line-fill pair (top line, bottom line, filled between)

Layer spacing: 0.3 to 1.0 × ATR above/below price

Outer layers = faint, inner layers = bright

Color transitions from base to intense based on layer position

Transparency scales with probability (high prob = more opaque)

Color Selection:

Long signals: Gradient from theme.gradient_bull_mid to theme.gradient_bull_strong

Short signals: Gradient from theme.gradient_bear_mid to theme.gradient_bear_strong

Base transparency: 92%, reduces by up to 8% for high-probability setups

Dynamic Behavior:

Cloud grows/shrinks as signal persistence increases/decreases

Redraws every bar while signal is forming

Disappears when signal executes or invalidates

Performance Note: Computationally expensive due to linefill objects. Disable or reduce layers if chart performance degrades.

2. Population Fitness Ribbon (Optional, Default: ON)

Histogram showing fitness distribution across active strategies:

Activation: Only draws on last bar (barstate.islast) to avoid historical clutter

Visual Construction:

10 histogram layers by default (configurable 5-20)

Plots 50 bars back from current bar

Positioned below price at: lowest_low(100) - 1.5×ATR (doesn't interfere with price action)

Each layer represents a fitness threshold (evenly spaced min to max fitness)

Layer Logic:

For layer_num from 0 to ribbon_layers:

Fitness_threshold = min_fitness + (max_fitness - min_fitness) × (layer / layers)

Count strategies with fitness ≥ threshold

Height = ATR × 0.15 × (count / total_active)

Y_position = base_level + ATR × 0.2 × layer

Color = Gradient from weak to strong based on layer position

Line_width = Scaled by height (taller = thicker)

Visual Feedback:

Tall, bright ribbon = healthy population, many fit strategies at high fitness levels

Short, dim ribbon = weak population, few strategies achieving good fitness

Ribbon compression (layers close together) = population converging to similar fitness

Ribbon spread = diverse fitness range, active selection pressure

Use Case: Quick visual health check without opening dashboard. Ribbon growing upward over time = population improving.

3. Confidence Halo (Optional, Default: ON)

Circular polyline around entry signals showing probability strength:

Activation: Draws when new position opens (shadow_position changes from 0 to ±1)

Visual Construction:

20-segment polyline forming approximate circle

Center: Low - 0.5×ATR (long) or High + 0.5×ATR (short)

Radius: 0.3×ATR (low confidence) to 1.0×ATR (elite confidence)

Scales with: (probability - min_probability) / (1.0 - min_probability)

Color Coding:

Elite (85%+): Cyan (theme.conf_elite), large radius, minimal transparency (40%)

Strong (75-85%): Strong green (theme.conf_strong), medium radius, moderate transparency (50%)

Good (65-75%): Good green (theme.conf_good), smaller radius, more transparent (60%)

Moderate (<65%): Moderate green (theme.conf_moderate), tiny radius, very transparent (70%)

Technical Detail:

Uses chart.point array with index-based positioning

5-bar horizontal spread for circular appearance (±5 bars from entry)

Curved=false (Pine Script polyline limitation)

Fill color matches line color but more transparent (88% vs line's transparency)

Purpose: Instant visual probability assessment. No need to check dashboard - halo size/brightness tells the story.

4. Evolution Event Markers (Optional, Default: ON)

Visual indicators of genetic algorithm activity:

Spawn Markers (Diamond, Cyan):

Plots when total_spawned increases on current bar

Location: bottom of chart (location.bottom)

Color: theme.spawn_marker (cyan/bright blue)

Size: tiny

Indicates new strategy just entered population

Cull Markers (X-Cross, Red):

Plots when total_culled increases on current bar

Location: bottom of chart (location.bottom)

Color: theme.cull_marker (red/pink)

Size: tiny

Indicates weak strategy just removed from population

What It Tells You:

Frequent spawning early = population building, active exploration

Frequent culling early = high selection pressure, weak strategies dying fast

Balanced spawn/cull = healthy evolutionary churn

No markers for long periods = stable population (evolution plateaued or optimal genes found)

5. Entry/Exit Markers

Clear visual signals for selected strategy's trades:

Long Entry (Triangle Up, Green):

Plots when selected strategy opens long position (position changes 0 → +1)

Location: below bar (location.belowbar)

Color: theme.long_primary (green/cyan depending on theme)

Transparency: Scales with probability:

Elite (85%+): 0% (fully opaque)

Strong (75-85%): 10%

Good (65-75%): 20%

Acceptable (55-65%): 35%

Size: small

Short Entry (Triangle Down, Red):

Plots when selected strategy opens short position (position changes 0 → -1)

Location: above bar (location.abovebar)

Color: theme.short_primary (red/pink depending on theme)

Transparency: Same scaling as long entries

Size: small

Exit (X-Cross, Orange):

Plots when selected strategy closes position (position changes ±1 → 0)

Location: absolute (at actual exit price if stop/target lines enabled)

Color: theme.exit_color (orange/yellow depending on theme)

Transparency: 0% (fully opaque)

Size: tiny

Result: Clean, probability-scaled markers that don't clutter chart but convey essential information.

6. Stop Loss & Take Profit Lines (Optional, Default: ON)

Visual representation of shadow portfolio risk levels:

Stop Loss Line:

Plots when selected strategy has active position

Level: shadow_stop value from selected strategy

Color: theme.short_primary with 60% transparency (red/pink, subtle)

Width: 2

Style: plot.style_linebr (breaks when no position)

Take Profit Line:

Plots when selected strategy has active position

Level: shadow_target value from selected strategy

Color: theme.long_primary with 60% transparency (green, subtle)

Width: 2

Style: plot.style_linebr (breaks when no position)

Purpose:

Shows where shadow portfolio would exit for stop/target

Helps visualize strategy's risk/reward ratio

Useful for manual traders to set similar levels

Disable for cleaner chart (recommended for presentations)

7. Dynamic Trend EMA

Gradient-colored trend line that visualizes trend strength:

Calculation:

EMA(close, trend_length) - default 50 period (configurable 20-100)

Slope calculated over 10 bars: (current_ema - ema ) / ema × 100

Color Logic:

Trend_direction:

Slope > 0.1% = Bullish (1)

Slope < -0.1% = Bearish (-1)

Otherwise = Neutral (0)

Trend_strength = abs(slope)

Color = Gradient between:

- Neutral color (gray/purple)

- Strong bullish (bright green) if direction = 1

- Strong bearish (bright red) if direction = -1

Gradient factor = trend_strength (0 to 1+ scale)

Visual Behavior:

Faint gray/purple = weak/no trend (choppy conditions)

Light green/red = emerging trend (low strength)

Bright green/red = strong trend (high conviction)

Color intensity = trend strength magnitude

Transparency: 50% (subtle, doesn't overpower price action)

Purpose: Subconscious awareness of trend state without checking dashboard or indicators.

8. Regime Background Tinting (Subtle)

Ultra-low opacity background color indicating detected market regime:

Regime Detection:

Efficiency = directional_movement / total_range (over trend_length bars)

Vol_ratio = current_volatility / average_volatility

IF (efficiency > 0.5 AND vol_ratio < 1.3):

Regime = Trending (1)

ELSE IF (vol_ratio > 1.5):

Regime = Volatile (2)

ELSE:

Regime = Choppy (0)

Background Colors:

Trending: theme.regime_trending (dark green, 92-93% transparency)

Volatile: theme.regime_volatile (dark red, 93% transparency)

Choppy: No tint (normal background)

Purpose:

Subliminal regime awareness

Helps explain why signals are/aren't generating

Trending = ideal conditions for AGE

Volatile = fewer signals, higher thresholds applied

Choppy = mixed signals, lower confidence

Important: Extremely subtle by design. Not meant to be obvious, just subconscious context.

📊 ENHANCED DASHBOARD

Comprehensive real-time metrics in single organized panel (top-right position):

Dashboard Structure (5 columns × 14 rows)

Header Row:

Column 0: "🧬 AGE PRO" + phase indicator (🔴 LIVE or ⏪ HIST)

Column 1: "POPULATION"

Column 2: "PERFORMANCE"

Column 3: "CURRENT SIGNAL"

Column 4: "ACTIVE STRATEGY"

Column 0: Market State

Regime (📈 TREND / 🌊 CHAOS / ➖ CHOP)

DVS Ratio (current volatility scaling factor, format: #.##)

Trend Direction (▲ BULL / ▼ BEAR / ➖ FLAT with color coding)

Trend Strength (0-100 scale, format: #.##)

Column 1: Population Metrics

Active strategies (count / max_population)

Validated strategies (WFO passed / active total)

Current generation number

Total spawned (all-time strategy births)

Total culled (all-time strategy deaths)

Column 2: Aggregate Performance

Total trades across all active strategies

Aggregate win rate (%) - color-coded:

Green (>55%)

Orange (45-55%)

Red (<45%)

Total P&L in R-multiples - color-coded by positive/negative

Best fitness score in population (format: #.###)

MAS - Minimum Adaptation Score (cull threshold, format: #.###)

Column 3: Current Signal Status

Status indicator:

"▲ LONG" (green) if selected strategy in long position

"▼ SHORT" (red) if selected strategy in short position

"⏳ FORMING" (orange) if signal persisting but not yet executed

"○ WAITING" (gray) if no active signal

Confidence percentage (0-100%, format: #.#%)

Quality assessment:

"🔥 ELITE" (cyan) for 85%+ probability

"✓ STRONG" (bright green) for 75-85%

"○ GOOD" (green) for 65-75%

"- LOW" (dim) for <65%

Confluence score (X/3 format)

Signal age:

"X bars" if signal forming

"IN TRADE" if position active

"---" if no signal

Column 4: Selected Strategy Details

Strategy ID number (#X format)

Validation status:

"✓ VAL" (green) if WFO validated

"○ TRAIN" (orange) if still in training/testing phase

Generation number (GX format)

Personal fitness score (format: #.### with color coding)

Trade count

P&L and win rate (format: #.#R (##%) with color coding)

Color Scheme:

Panel background: theme.panel_bg (dark, low opacity)

Panel headers: theme.panel_header (slightly lighter)

Primary text: theme.text_primary (bright, high contrast)

Secondary text: theme.text_secondary (dim, lower contrast)

Positive metrics: theme.metric_positive (green)

Warning metrics: theme.metric_warning (orange)

Negative metrics: theme.metric_negative (red)

Special markers: theme.validated_marker, theme.spawn_marker

Update Frequency: Only on barstate.islast (current bar) to minimize CPU usage

Purpose:

Quick overview of entire system state

No need to check multiple indicators

Trading decisions informed by population health, regime state, and signal quality

Transparency into what AGE is thinking

🔍 DIAGNOSTICS PANEL (Optional, Default: OFF)

Detailed signal quality tracking for optimization and debugging:

Panel Structure (3 columns × 8 rows)

Position: Bottom-right corner (doesn't interfere with main dashboard)

Header Row:

Column 0: "🔍 DIAGNOSTICS"

Column 1: "COUNT"

Column 2: "%"

Metrics Tracked (for selected strategy only):

Total Evaluated:

Every signal that passed initial calculation (direction ≠ 0)

Represents total opportunities considered

✓ Passed:

Signals that passed quality gate and executed

Green color coding

Percentage of evaluated signals

Rejection Breakdown:

⨯ Probability:

Rejected because probability < minimum threshold

Most common rejection reason typically

⨯ Confluence:

Rejected because confluence < minimum required (e.g., only 1 of 3 indicators agreed)

⨯ Trend:

Rejected because signal opposed strong trend

Indicates counter-trend protection working

⨯ Regime:

Rejected because volatile regime detected and probability wasn't high enough to override

Shows regime filter in action

⨯ Volume:

Rejected because volume < 70% of 20-bar average

Indicates volume confirmation requirement

Color Coding:

Passed count: Green (success metric)

Rejection counts: Red (failure metrics)

Percentages: Gray (neutral, informational)

Performance Cost: Slight CPU overhead for tracking counters. Disable when not actively optimizing settings.

How to Use Diagnostics

Scenario 1: Too Few Signals

Evaluated: 200

Passed: 10 (5%)

⨯ Probability: 120 (60%)

⨯ Confluence: 40 (20%)

⨯ Others: 30 (15%)

Diagnosis: Probability threshold too high for this strategy's DNA.

Solution: Lower min probability from 65% to 60%, or allow strategy more time to evolve better DNA.

Scenario 2: Too Many False Signals

Evaluated: 200

Passed: 80 (40%)

Strategy win rate: 45%

Diagnosis: Quality gate too loose, letting low-quality signals through.

Solution: Raise min probability to 70%, or increase min confluence to 3 (all indicators must agree).

Scenario 3: Regime-Specific Issues

⨯ Regime: 90 (45% of rejections)

Diagnosis: Frequent volatile regime detection blocking otherwise good signals.

Solution: Either accept fewer trades during chaos (recommended), or disable regime filter if you want signals regardless of market state.

Optimization Workflow:

Enable diagnostics

Run 200+ bars

Analyze rejection patterns

Adjust settings based on data

Re-run and compare pass rate

Disable diagnostics when satisfied

⚙️ CONFIGURATION GUIDE

🧬 Evolution Engine Settings

Enable AGE Evolution (Default: ON):

ON: Full genetic algorithm (recommended for best results)

OFF: Uses only 4 seed strategies, no spawning/culling (static population for comparison testing)

Max Population (4-12, Default: 8):

Higher = more diversity, more exploration, slower performance

Lower = faster computation, less exploration, risk of premature convergence

Sweet spot: 6-8 for most use cases

4 = minimum for meaningful evolution

12 = maximum before diminishing returns

Min Population (2-4, Default: 3):

Safety floor - system never culls below this count

Prevents population extinction during harsh selection

Should be at least half of max population

Elite Preservation (1-3, Default: 2):

Top N performers completely immune to culling

Ensures best genes always survive

1 = minimal protection, aggressive selection

2 = balanced (recommended)

3 = conservative, slower gene pool turnover

Historical: Spawn Interval (10-100, Default: 30):

Bars between spawning new strategies during historical data

Lower = faster evolution, more exploration

Higher = slower evolution, more evaluation time per strategy

30 bars = ~1-2 hours on 15min chart

Historical: Cull Interval (20-200, Default: 60):

Bars between culling weak strategies during historical data

Should be 2x spawn interval for balanced churn

Lower = aggressive selection pressure

Higher = patient evaluation

Live: Spawn Interval (100-500, Default: 200):

Bars between spawning during live trading

Much slower than historical for stability

Prevents population chaos during live trading

200 bars = ~1.5 trading days on 15min chart

Live: Cull Interval (200-1000, Default: 400):

Bars between culling during live trading

Should be 2x live spawn interval

Conservative removal during live trading

Historical: Mutation Rate (0.05-0.40, Default: 0.20):

Probability each gene mutates during breeding (20% = 2 out of 10 genes on average)

Higher = more exploration, slower convergence

Lower = more exploitation, faster convergence but risk of local optima

20% balances exploration vs exploitation

Live: Mutation Rate (0.02-0.20, Default: 0.08):

Mutation rate during live trading

Much lower for stability (don't want population to suddenly degrade)

8% = mostly inherits parent genes with small tweaks

Mutation Strength (0.05-0.25, Default: 0.12):

How much genes change when mutated (% of gene's total range)

0.05 = tiny nudges (fine-tuning)

0.12 = moderate jumps (recommended)

0.25 = large leaps (aggressive exploration)

Example: If gene range is 0.5-2.0, 12% strength = ±0.18 possible change

📈 Signal Quality Settings

Min Signal Probability (0.55-0.80, Default: 0.65):

Quality gate threshold - signals below this never generate

0.55-0.60 = More signals, accept lower confidence (higher risk)

0.65 = Institutional-grade balance (recommended)

0.70-0.75 = Fewer but higher-quality signals (conservative)

0.80+ = Very selective, very few signals (ultra-conservative)

Min Confluence Score (1-3, Default: 2):

Required indicator agreement before signal generates

1 = Any single indicator can trigger (not recommended - too many false signals)

2 = Requires 2 of 3 indicators agree (RECOMMENDED for balance)

3 = All 3 must agree (very selective, few signals, high quality)

Base Persistence Bars (1-5, Default: 2):

Base bars signal must persist before entry

System adapts automatically: