Sri_Momentum Burst Histogram📝 Description :

🌀 Sri_Momentum Burst Histogram — A Custom Momentum and Volatility Fusion Tool

The Sri_Momentum Burst Histogram is a unique technical analysis tool designed to visualize sudden changes in price momentum in the form of a dynamic, color-coded histogram. This indicator helps traders identify trend accelerations, early momentum shifts, and potential exhaustion in real time.

By combining a MACD-like momentum engine with a volatility-sensitive Bollinger Band range, this script offers an enhanced view of market bursts — moments where momentum "pops" beyond typical ranges. The result is a refined perspective on market sentiment, helping traders to anticipate reversals, follow breakouts, and assess the relative strength of ongoing trends.

🧠 Core Methodology

The indicator calculates the difference between a fast and slow EMA (Exponential Moving Average), similar to a MACD histogram.

This difference is then compared across candles to gauge the rate of change in momentum — referred to here as a “momentum burst.”

A sensitivity multiplier allows you to scale the response based on your preferred timeframe and trading style.

A volatility band, derived from Bollinger Band logic, is used to frame the relative intensity of the momentum change.

The histogram is divided into two parts:

Green/Lime Bars represent increasing and decreasing bullish momentum.

Red/Orange Bars represent increasing and decreasing bearish momentum.

⚙️ Customizable Inputs

Momentum Sensitivity: Adjust the responsiveness of the burst detection mechanism.

Short EMA Period: Sets the lookback period for the fast EMA.

Long EMA Period: Sets the lookback period for the slow EMA.

Volatility Band Length: Controls the length used for Bollinger Band calculations.

Band Std Dev Multiplier: Adjusts how wide the volatility range should be, based on price dispersion.

📈 How to Use It

Use the green/red histogram bars to visually gauge momentum strength and direction.

Watch for transitions in color intensity (e.g., green to lime, red to orange) as early warning signs of trend exhaustion or reversal.

Combine with other indicators like RSI, MACD, ADX, or volume profiles to confirm entry/exit points.

Useful in both trending and ranging markets, especially on lower timeframes for scalping or intraday setups.

✅ Key Features

Easy-to-read histogram with intuitive color coding.

Fully customizable settings for fine-tuned signal control.

Can be used on any asset class — stocks, forex, crypto, commodities.

Optimized for real-time use with minimal lag.

🔐 This script is an original creation, developed independently by adapting publicly known mathematical concepts into a unique visualization tool. All function and variable names have been customized for originality and compliance with TradingView’s publishing and community standards.

💡 Developed by: @venkat_27

🧩 For educational purposes only — not financial advice.

Wyszukaj w skryptach "adx"

Ergodic Market Divergence (EMD)Ergodic Market Divergence (EMD)

Bridging Statistical Physics and Market Dynamics Through Ensemble Analysis

The Revolutionary Concept: When Physics Meets Trading

After months of research into ergodic theory—a fundamental principle in statistical mechanics—I've developed a trading system that identifies when markets transition between predictable and unpredictable states. This indicator doesn't just follow price; it analyzes whether current market behavior will persist or revert, giving traders a scientific edge in timing entries and exits.

The Core Innovation: Ergodic Theory Applied to Markets

What Makes Markets Ergodic or Non-Ergodic?

In statistical physics, ergodicity determines whether a system's future resembles its past. Applied to trading:

Ergodic Markets (Mean-Reverting)

- Time averages equal ensemble averages

- Historical patterns repeat reliably

- Price oscillates around equilibrium

- Traditional indicators work well

Non-Ergodic Markets (Trending)

- Path dependency dominates

- History doesn't predict future

- Price creates new equilibrium levels

- Momentum strategies excel

The Mathematical Framework

The Ergodic Score combines three critical divergences:

Ergodic Score = (Price Divergence × Market Stress + Return Divergence × 1000 + Volatility Divergence × 50) / 3

Where:

Price Divergence: How far current price deviates from market consensus

Return Divergence: Momentum differential between instrument and market

Volatility Divergence: Volatility regime misalignment

Market Stress: Adaptive multiplier based on current conditions

The Ensemble Analysis Revolution

Beyond Single-Instrument Analysis

Traditional indicators analyze one chart in isolation. EMD monitors multiple correlated markets simultaneously (SPY, QQQ, IWM, DIA) to detect systemic regime changes. This ensemble approach:

Reveals Hidden Divergences: Individual stocks may diverge from market consensus before major moves

Filters False Signals: Requires broader market confirmation

Identifies Regime Shifts: Detects when entire market structure changes

Provides Context: Shows if moves are isolated or systemic

Dynamic Threshold Adaptation

Unlike fixed-threshold systems, EMD's boundaries evolve with market conditions:

Base Threshold = SMA(Ergodic Score, Lookback × 3)

Adaptive Component = StDev(Ergodic Score, Lookback × 2) × Sensitivity

Final Threshold = Smoothed(Base + Adaptive)

This creates context-aware signals that remain effective across different market environments.

The Confidence Engine: Know Your Signal Quality

Multi-Factor Confidence Scoring

Every signal receives a confidence score based on:

Signal Clarity (0-35%): How decisively the ergodic threshold is crossed

Momentum Strength (0-25%): Rate of ergodic change

Volatility Alignment (0-20%): Whether volatility supports the signal

Market Quality (0-20%): Price convergence and path dependency factors

Real-Time Confidence Updates

The Live Confidence metric continuously updates, showing:

- Current opportunity quality

- Market state clarity

- Historical performance influence

- Signal recency boost

- Visual Intelligence System

Adaptive Ergodic Field Bands

Dynamic bands that expand and contract based on market state:

Primary Color: Ergodic state (mean-reverting)

Danger Color: Non-ergodic state (trending)

Band Width: Expected price movement range

Squeeze Indicators: Volatility compression warnings

Quantum Wave Ribbons

Triple EMA system (8, 21, 55) revealing market flow:

Compressed Ribbons: Consolidation imminent

Expanding Ribbons: Directional move developing

Color Coding: Matches current ergodic state

Phase Transition Signals

Clear entry/exit markers at regime changes:

Bull Signals: Ergodic restoration (mean reversion opportunity)

Bear Signals: Ergodic break (trend following opportunity)

Confidence Labels: Percentage showing signal quality

Visual Intensity: Stronger signals = deeper colors

Professional Dashboard Suite

Main Analytics Panel (Top Right)

Market State Monitor

- Current regime (Ergodic/Non-Ergodic)

- Ergodic score with threshold

- Path dependency strength

- Quantum coherence percentage

Divergence Metrics

- Price divergence with severity

- Volatility regime classification

- Strategy mode recommendation

- Signal strength indicator

Live Intelligence

- Real-time confidence score

- Color-coded risk levels

- Dynamic strategy suggestions

Performance Tracking (Left Panel)

Signal Analytics

- Total historical signals

- Win rate with W/L breakdown

- Current streak tracking

- Closed trade counter

Regime Analysis

- Current market behavior

- Bars since last signal

- Recommended actions

- Average confidence trends

Strategy Command Center (Bottom Right)

Adaptive Recommendations

- Active strategy mode

- Primary approach (mean reversion/momentum)

- Suggested indicators ("weapons")

- Entry/exit methodology

- Risk management guidance

- Comprehensive Input Guide

Core Algorithm Parameters

Analysis Period (10-100 bars)

Scalping (10-15): Ultra-responsive, more signals, higher noise

Day Trading (20-30): Balanced sensitivity and stability

Swing Trading (40-100): Smooth signals, major moves only Default: 20 - optimal for most timeframes

Divergence Threshold (0.5-5.0)

Hair Trigger (0.5-1.0): Catches every wiggle, many false signals

Balanced (1.5-2.5): Good signal-to-noise ratio

Conservative (3.0-5.0): Only extreme divergences Default: 1.5 - best risk/reward balance

Path Memory (20-200 bars)

Short Memory (20-50): Recent behavior focus, quick adaptation

Medium Memory (50-100): Balanced historical context

Long Memory (100-200): Emphasizes established patterns Default: 50 - captures sufficient history without lag

Signal Spacing (5-50 bars)

Aggressive (5-10): Allows rapid-fire signals

Normal (15-25): Prevents clustering, maintains flow

Conservative (30-50): Major setups only Default: 15 - optimal trade frequency

Ensemble Configuration

Select markets for consensus analysis:

SPY: Broad market sentiment

QQQ: Technology leadership

IWM: Small-cap risk appetite

DIA: Blue-chip stability

More instruments = stronger consensus but potentially diluted signals

Visual Customization

Color Themes (6 professional options):

Quantum: Cyan/Pink - Modern trading aesthetic

Matrix: Green/Red - Classic terminal look

Heat: Blue/Red - Temperature metaphor

Neon: Cyan/Magenta - High contrast

Ocean: Turquoise/Coral - Calming palette

Sunset: Red-orange/Teal - Warm gradients

Display Controls:

- Toggle each visual component

- Adjust transparency levels

- Scale dashboard text

- Show/hide confidence scores

- Trading Strategies by Market State

- Ergodic State Strategy (Primary Color Bands)

Market Characteristics

- Price oscillates predictably

- Support/resistance hold

- Volume patterns repeat

- Mean reversion dominates

Optimal Approach

Entry: Fade moves at band extremes

Target: Middle band (equilibrium)

Stop: Just beyond outer bands

Size: Full confidence-based position

Recommended Tools

- RSI for oversold/overbought

- Bollinger Bands for extremes

- Volume profile for levels

- Non-Ergodic State Strategy (Danger Color Bands)

Market Characteristics

- Price trends persistently

- Levels break decisively

- Volume confirms direction

- Momentum accelerates

Optimal Approach

Entry: Breakout from bands

Target: Trail with expanding bands

Stop: Inside opposite band

Size: Scale in with trend

Recommended Tools

- Moving average alignment

- ADX for trend strength

- MACD for momentum

- Advanced Features Explained

Quantum Coherence Metric

Measures phase alignment between individual and ensemble behavior:

80-100%: Perfect sync - strong mean reversion setup

50-80%: Moderate alignment - mixed signals

0-50%: Decoherence - trending behavior likely

Path Dependency Analysis

Quantifies how much history influences current price:

Low (<30%): Technical patterns reliable

Medium (30-50%): Mixed influences

High (>50%): Fundamental shift occurring

Volatility Regime Classification

Contextualizes current volatility:

Normal: Standard strategies apply

Elevated: Widen stops, reduce size

Extreme: Defensive mode required

Signal Strength Indicator

Real-time opportunity quality:

- Distance from threshold

- Momentum acceleration

- Cross-validation factors

Risk Management Framework

Position Sizing by Confidence

90%+ confidence = 100% position size

70-90% confidence = 75% position size

50-70% confidence = 50% position size

<50% confidence = 25% or skip

Dynamic Stop Placement

Ergodic State: ATR × 1.0 from entry

Non-Ergodic State: ATR × 2.0 from entry

Volatility Adjustment: Multiply by current regime

Multi-Timeframe Alignment

- Check higher timeframe regime

- Confirm ensemble consensus

- Verify volume participation

- Align with major levels

What Makes EMD Unique

Original Contributions

First Ergodic Theory Trading Application: Transforms abstract physics into practical signals

Ensemble Market Analysis: Revolutionary multi-market divergence system

Adaptive Confidence Engine: Institutional-grade signal quality metrics

Quantum Coherence: Novel market alignment measurement

Smart Signal Management: Prevents clustering while maintaining responsiveness

Technical Innovations

Dynamic Threshold Adaptation: Self-adjusting sensitivity

Path Memory Integration: Historical dependency weighting

Stress-Adjusted Scoring: Market condition normalization

Real-Time Performance Tracking: Built-in strategy analytics

Optimization Guidelines

By Timeframe

Scalping (1-5 min)

Period: 10-15

Threshold: 0.5-1.0

Memory: 20-30

Spacing: 5-10

Day Trading (5-60 min)

Period: 20-30

Threshold: 1.5-2.5

Memory: 40-60

Spacing: 15-20

Swing Trading (1H-1D)

Period: 40-60

Threshold: 2.0-3.0

Memory: 80-120

Spacing: 25-35

Position Trading (1D-1W)

Period: 60-100

Threshold: 3.0-5.0

Memory: 100-200

Spacing: 40-50

By Market Condition

Trending Markets

- Increase threshold

- Extend memory

- Focus on breaks

Ranging Markets

- Decrease threshold

- Shorten memory

- Focus on restores

Volatile Markets

- Increase spacing

- Raise confidence requirement

- Reduce position size

- Integration with Other Analysis

- Complementary Indicators

For Ergodic States

- RSI divergences

- Bollinger Band squeezes

- Volume profile nodes

- Support/resistance levels

For Non-Ergodic States

- Moving average ribbons

- Trend strength indicators

- Momentum oscillators

- Breakout patterns

- Fundamental Alignment

- Check economic calendar

- Monitor sector rotation

- Consider market themes

- Evaluate risk sentiment

Troubleshooting Guide

Too Many Signals:

- Increase threshold

- Extend signal spacing

- Raise confidence minimum

Missing Opportunities

- Decrease threshold

- Reduce signal spacing

- Check ensemble settings

Poor Win Rate

- Verify timeframe alignment

- Confirm volume participation

- Review risk management

Disclaimer

This indicator is for educational and informational purposes only. It does not constitute financial advice. Trading involves substantial risk of loss and is not suitable for all investors. Past performance does not guarantee future results.

The ergodic framework provides unique market insights but cannot predict future price movements with certainty. Always use proper risk management, conduct your own analysis, and never risk more than you can afford to lose.

This tool should complement, not replace, comprehensive trading strategies and sound judgment. Markets remain inherently unpredictable despite advanced analysis techniques.

Transform market chaos into trading clarity with Ergodic Market Divergence.

Created with passion for the TradingView community

Trade with insight. Trade with anticipation.

— Dskyz , for DAFE Trading Systems

Disparity Index with Volatility ZonesDisparity Index with Volatility Zones

is a momentum oscillator that measures the percentage difference between the current price and its simple moving average (SMA). This allows traders to identify overbought/oversold conditions, assess momentum strength, and detect potential trend reversals or continuations.

🔍 Core Concept:

The Disparity Index (DI) is calculated as:

DI = 100 × (Price − SMA) / SMA

A positive DI indicates the price is trading above its moving average (potential bullish sentiment), while a negative DI suggests the price is below the average (potential bearish sentiment).

This version of the Disparity Index introduces a dual-zone volatility framework, offering deeper insight into the market's current state.

🧠 What Makes This Version Unique?

1. High Volatility Zones

When DI crosses above +1.0% or below –1.0%, it often indicates the start or continuation of a strong trend.

Sustained readings beyond these thresholds typically align with trending phases, offering opportunities for momentum-based entries.

A reversal back within ±1.0% after exceeding these levels can suggest a shift in momentum — similar to how RSI exits the overbought/oversold zones before reversals.

These thresholds act as dynamic markers for breakout confirmation and potential trend exhaustion.

2. Low Volatility Zones

DI values between –0.5% and +0.5% define the low-volatility zone, shaded for visual clarity.

This area typically indicates market indecision, sideways price action, or consolidation.

Trading within this range may favor range-bound or mean-reversion strategies, as trend momentum is likely limited.

The logic is similar to interpreting a flat ADX, tight Bollinger Bands, or contracting Keltner Channels — all suggesting consolidation.

⚙️ Features:

Customizable moving average length and input source

Adjustable thresholds for overbought/oversold and low-volatility zones

Optional visual fill between low-volatility bounds

Clean and minimal chart footprint (non-essential plots hidden by default)

📈 How to Use:

1. Trend Confirmation:

A break above +1.0% can be used as a bullish continuation signal.

A break below –1.0% may confirm bearish strength.

Long periods above/below these thresholds support trend-following entries.

2. Reversal Detection:

If DI returns below +1.0% after exceeding it, bullish momentum may be fading.

If DI rises above –1.0% after falling below, bearish pressure may be weakening.

These shifts resemble overbought/oversold transitions in oscillators like RSI or Stochastic, and can be paired with divergence, volume, or price structure analysis for higher reliability.

3. Sideways Market Detection:

DI values within ±0.5% indicate low volatility or a non-trending environment.

Traders may avoid breakout entries during these periods or apply range-trading tactics instead.

Observing transitions out of the low-volatility zone can help anticipate breakouts.

4. Combine with Other Indicators:

DI signals can be enhanced using tools like MACD, Volume Oscillators, or Moving Averages.

For example, a DI breakout beyond ±1.0% supported by a MACD crossover or volume spike can help validate trend initiation.

This indicator is especially powerful when paired with Bollinger Bands:

A simultaneous price breakout from the Bollinger Band and DI moving beyond ±1.0% can help identify early trend inflection points.

This combination supports entering positions early in a developing trend, improving the efficiency of trend-following strategies and enhancing decision-making precision.

It also helps filter false breakouts when DI fails to confirm the move outside the band.

This indicator is designed for educational and analytical purposes and works across all timeframes and asset classes.

It is particularly useful for traders seeking a clear framework to identify momentum strength, filter sideways markets, and improve entry timing within a larger trading system.

VWAP Predictive Breakout + RSI + OB + Trend/Chop📈 VWAP Predictive Breakout + RSI + Order Blocks + Trend/Chop Filter

This multi-layered day trading and scalping tool is designed to predict price direction after a VWAP breakout, rather than react to it. It combines volume, RSI, candlestick structure, order blocks, and trend/chop analysis to improve the accuracy of intraday signals.

🔍 Core Features

VWAP Predictive Breakout

Signals are generated when price breaks above/below VWAP with strength (volume spike + strong candle body), supported by trend confirmation.

RSI Momentum Filter

Uses RSI divergence behavior to validate breakouts, filtering out weak or exhausted moves.

Order Block Detection

Marks bullish and bearish engulfing patterns and checks for proximity to these zones as confirmation for breakouts.

Trend vs Chop Detection

Uses ADX, ATR, EMA distance, Bollinger Band width, and candlestick cleanliness to dynamically identify whether the market is trending or choppy.

Clean Candle Behavior

Filters out noisy or indecisive candles by analyzing wick-to-body ratio and ATR-based body size.

📌 Visual Markers

🟢 Buy Signal: Green triangle below bar

🔴 Sell Signal: Red triangle above bar

🟢⚪ Bullish Order Block: Green circle

🔴⚪ Bearish Order Block: Red circle

🟩 Trending Background: Light green

🟥 Choppy Background: Light red

🛎 Alerts Included

Long signal: VWAP breakout + RSI + Order Block + Clean Candle

Short signal: VWAP breakdown + RSI + Order Block + Clean Candle

🧠 Best Use Cases

Scalping high-probability VWAP reversals or continuations

Day trading in markets where trend clarity is critical

Filtering noise in sideways conditions using real-time chop detection

Hybrid: RSI + Breakout + DashboardHybrid RSI + Breakout Strategy

Adaptive trading system that switches modes based on market regime:

Ranging: Buys when RSI < 30 and sells when RSI > 70.

Trending: Enters momentum breakouts only in the direction of the 200-EMA bias, with ADX confirming trend strength.

Risk Management: Trailing stop locks profits and caps drawdown.

Optimized for BTC, ETH, and SOL on 1 h–1 D charts; back-tested from 2017 onward. Educational use only—run your own tests before deploying live funds.

Angel Signal proAngel Signal Pro is a comprehensive technical analysis tool that integrates multiple indicators for a structured market assessment.

RSI, MACD, and ADX — evaluate trend strength and identify potential entry and exit points.

Momentum and ATR — measure price acceleration and volatility, assisting in risk management.

Stochastic Oscillator — detects overbought and oversold conditions.

SMA (50, 100, 200) — tracks key moving averages with the option to enable all at once.

Cryptocurrency price display — select and monitor real-time prices of any cryptocurrency available on the BINANCE exchange.

Automatic trend detection— classifies trends as bullish, bearish, or neutral based on RSI and MACD signals.

Customizable table — presents key indicator values in a structured and convenient format. The table also provides automatic trend detection across different timeframes (TF), allowing you to assess the current market situation more accurately on various levels.

Automatic gap detection — identifies market gaps, helping to spot potential trading opportunities.

Buy and sell signals — the system generates buy and sell signals based on the analysis of five key indicator values, allowing traders to respond quickly to market changes.

Bollinger Bands — helps assess market volatility and identify support and resistance levels, as well as potential reversal points, by detecting when prices move outside of normal volatility ranges.

Customization settings — in Angel Signal Pro, you can select which indicators and features you want to display. All elements can be turned on or off according to your preferences. There is also the ability to change colors and the appearance of each element, allowing you to tailor the interface to your personal preferences and make the tool more convenient to use.

Angel Signal Pro is suitable for traders of all experience levels and helps navigate market conditions with confidence.

29 мар.

Информация о релизе

Added Super Trend, improved the quality of buy and sell signals, and enhanced settings. Now, all toggle buttons for enabling and disabling indicators follow one another.

30 мар.

Информация о релизе

Fixed several errors in the settings and improved gap search.

nineLivesUtilLibLibrary "nineLivesUtilLib"

isDateInRange(currentTime, useTimeFilter, startDate, endDate)

Checks if the current time is within the specified date range.

Parameters:

currentTime (int) : The current bar's time (time).

useTimeFilter (bool) : Bool 📅: Enable the date range filter.

startDate (int) : Timestamp 📅: The start date for the filter.

endDate (int) : Timestamp 📅: The end date for the filter.

Returns: True if the current time is within the range or filtering is disabled, false otherwise.

@example

inDateRange = nineLivesUtilLib.isDateInRange(time, useTimeFilter, startDate, endDate)

if inDateRange

// Execute trading logic

checkVolumeCondition(currentVolume, useVolumeFilter, volumeThresholdMultiplier, volumeLength)

Checks if the current volume meets the threshold condition.

Parameters:

currentVolume (float) : The current bar's volume (volume).

useVolumeFilter (bool) : Bool 📊: Enable the volume filter.

volumeThresholdMultiplier (float) : Float 📊: Volume threshold relative to average (e.g., 1.5 for 1.5x average).

volumeLength (int) : Int 📊: Lookback length for the volume average.

Returns: True if the volume condition is met or filtering is disabled, false otherwise.

@example

volumeOk = nineLivesUtilLib.checkVolumeCondition(volume, useVolumeFilter, volumeThreshold, volumeLength)

if volumeOk

// Proceed with trading logic

checkMultiTimeframeCondition(currentClose, currentOpen, htfClose, htfOpen, useMultiTimeframe, alignment)

Checks alignment with higher timeframe direction.

Parameters:

currentClose (float) : Float: The current bar's closing price (close).

currentOpen (float) : Float: The current bar's opening price (open).

htfClose (float) : Float: The closing price from the higher timeframe (must be fetched by the calling script using request.security).

htfOpen (float) : Float: The opening price from the higher timeframe (must be fetched by the calling script using request.security).

useMultiTimeframe (bool) : Bool ⏱️: Enable multi-timeframe analysis.

alignment (string) : String ⏱️: Desired alignment ("same", "opposite", "any").

Returns: True if the timeframe alignment condition is met or analysis is disabled, false otherwise.

@example

// In the calling script:

= request.security(syminfo.tickerid, higherTimeframe, )

tfOk = nineLivesUtilLib.checkMultiTimeframeCondition(close, open, htfClose, htfOpen, useMultiTimeframe, tfAlignment)

if tfOk

// Proceed with trading logic

checkMarketRegime(useMarketRegime, regimeIndicator, regimeThreshold, regimeLength, regimeMode)

Detects the market regime (trending or ranging) and checks if trading is allowed.

Parameters:

useMarketRegime (bool) : Bool 🔍: Enable market regime detection.

regimeIndicator (string) : String 🔍: Indicator to use ("ADX" or "Volatility").

regimeThreshold (int) : Int 🔍: Threshold for trend strength/volatility.

regimeLength (simple int) : Int 🔍: Lookback length for the indicator.

regimeMode (string) : String 🔍: Trading mode based on regime ("trend_only", "range_only", "adaptive").

Returns: A tuple containing:

: conditionMet (bool) - True if trading is allowed based on the regime mode and detection, false otherwise.

: inTrendingRegime (bool) - True if the current regime is trending based on the indicator and threshold.

@example

= nineLivesUtilLib.checkMarketRegime(useMarketRegime, regimeIndicator, regimeThreshold, regimeLength, regimeMode)

if regimeOk

// Proceed with trading logic

applyCooldown(buySignal, sellSignal, cooldownBars)

Applies a cooldown period after a signal.

Parameters:

buySignal (bool) : Bool: Buy signal (potentially after primary entry logic).

sellSignal (bool) : Bool: Sell signal (potentially after primary entry logic).

cooldownBars (int) : Int ⏳: The number of bars to wait after a signal before allowing another.

Returns: A tuple containing:

: cooldownFilteredBuy (bool) - Buy signal after cooldown filter.

: cooldownFilteredSell (bool) - Sell signal after cooldown filter.

@example

= nineLivesUtilLib.applyCooldown(rawBuySignal, rawSellSignal, iCool)

applyAllFilters(rawBuy, rawSell, inDateRange, tradeDirection, volumeOk, tfOk, regimeOk, drawdownOk, cooldownOkBuy, cooldownOkSell)

Applies all filtering conditions to the buy and sell signals.

Parameters:

rawBuy (bool) : Bool: The initial buy signal candidate (from primary entry logic, e.g., after cooldown).

rawSell (bool) : Bool: The initial sell signal candidate (from primary entry logic, e.g., after cooldown).

inDateRange (bool) : Bool 📅: Result from isDateInRange.

tradeDirection (string) : String 🔄: Overall trade direction preference ("longs_only", "shorts_only", "both").

volumeOk (bool) : Bool 📊: Result from checkVolumeCondition.

tfOk (bool) : Bool ⏱️: Result from checkMultiTimeframeCondition.

regimeOk (bool) : Bool 🔍: Result from checkMarketRegime.

drawdownOk (bool) : Bool 📉: Result from checkDrawdownExceeded (or equivalent).

cooldownOkBuy (bool) : Bool ⏳: Result from applyCooldown for buy.

cooldownOkSell (bool) : Bool ⏳: Result from applyCooldown for sell.

Returns: A tuple containing:

: finalBuySignal (bool) - The final buy signal after all filters.

: finalSellSignal (bool) - The final sell signal after all filters.

@example

= nineLivesUtilLib.applyAllFilters(cooldownBuy, cooldownSell, inDateRange, tradeDirection, volumeOk, tfOk, regimeOk, !drawdownExceeded, cooldownBuy, cooldownSell)

NOTE: This function filters signals generated by your primary entry logic (e.g., EMA crossover).

checkDrawdownExceeded(currentEquity, useMaxDrawdown, maxDrawdownPercent)

Tracks maximum equity and checks if current drawdown exceeds a threshold.

Parameters:

currentEquity (float) : Float: The strategy's current equity (strategy.equity).

useMaxDrawdown (bool) : Bool 📉: Enable max drawdown protection.

maxDrawdownPercent (float) : Float 📉: The maximum allowed drawdown as a percentage.

Returns: True if drawdown protection is enabled and the current drawdown exceeds the threshold, false otherwise.

@example

drawdownExceeded = nineLivesUtilLib.checkDrawdownExceeded(strategy.equity, useMaxDrawdown, maxDrawdownPercent)

if drawdownExceeded

// Consider stopping entries or exiting positions in the strategy script

calculateExitPrice(positionAvgPrice, percentage, isStop, isLong)

Calculates a stop loss or take profit price based on a percentage from the average entry price.

Parameters:

positionAvgPrice (float) : Float: The average price of the current position (strategy.position_avg_price).

percentage (float) : Float: The stop loss or take profit percentage (e.g., 2.0 for 2%).

isStop (bool) : Bool: True if calculating a stop loss price, false if calculating a take profit price.

isLong (bool) : Bool: True if the position is long, false if short.

Returns: The calculated stop price or take profit price, or na if no position or percentage is invalid.

@example

longSL = nineLivesUtilLib.calculateExitPrice(strategy.position_avg_price, stopLossPercent, true, true)

shortTP = nineLivesUtilLib.calculateExitPrice(strategy.position_avg_price, takeProfitPercent, false, false)

calculateTrailingStopLevel(positionAvgPrice, trailOffsetPercent, trailPercent, currentHigh, currentLow, isLong)

Calculates the current trailing stop level for a position.

Parameters:

positionAvgPrice (float) : Float: The average price of the current position (strategy.position_avg_price).

trailOffsetPercent (float) : Float 🔄: The percentage price movement to activate the trailing stop.

trailPercent (float) : Float 🔄: The percentage distance the stop trails behind the price.

currentHigh (float) : Float: The current bar's high (high).

currentLow (float) : Float: The current bar's low (low).

isLong (bool) : Bool: True if the position is long, false if short.

Returns: The calculated trailing stop price if active, otherwise na.

@example

longTrailStop = nineLivesUtilLib.calculateTrailingStopLevel(strategy.position_avg_price, trailOffset, trailPercent, high, low, true)

shortTrailStop = nineLivesUtilLib.calculateTrailingStopLevel(strategy.position_avg_price, trailOffset, trailPercent, high, low, false)

if not na(longTrailStop)

strategy.exit("Long Trail", from_entry="Long", stop=longTrailStop)

Dskyz (DAFE) AI Adaptive Regime - Beginners VersionDskyz (DAFE) AI Adaptive Regime - Pro: Revolutionizing Trading for All

Introduction

In the fast-paced world of financial markets, traders need tools that can keep up with ever-changing conditions while remaining accessible. The Dskyz (DAFE) AI Adaptive Regime - Pro is a groundbreaking TradingView strategy that delivers advanced, AI-driven trading capabilities to everyday traders. Available on TradingView (TradingView Scripts), this Pine Script strategy combines sophisticated market analysis with user-friendly features, making it a standout choice for both novice and experienced traders.

Core Functionality

The strategy is built to adapt to different market regimes—trending, ranging, volatile, or quiet—using a robust set of technical indicators, including:

Moving Averages (MA): Fast and slow EMAs to detect trend direction.

Average True Range (ATR): For dynamic stop-loss and volatility assessment.

Relative Strength Index (RSI) and MACD: Multi-timeframe confirmation of momentum and trend.

Average Directional Index (ADX): To identify trending markets.

Bollinger Bands: For assessing volatility and range conditions.

Candlestick Patterns: Recognizes patterns like bullish engulfing, hammer, and double bottoms, confirmed by volume spikes.

It generates buy and sell signals based on a scoring system that weighs these indicators, ensuring trades align with the current market environment. The strategy also includes dynamic risk management with ATR-based stops and trailing stops, as well as performance tracking to optimize future trades.

What Sets It Apart

The Dskyz (DAFE) AI Adaptive Regime - Pro distinguishes itself from other TradingView strategies through several unique features, which we compare to common alternatives below:

| Feature | Dskyz (DAFE) | Typical TradingView Strategies|

|---------|-------------|------------------------------------------------------------|

| Regime Detection | Automatically identifies and adapts to **four** market regimes | Often static or limited to trend/range detection |

| Multi‑Timeframe Analysis | Uses higher‑timeframe RSI/MACD for confirmation | Rarely incorporates multi‑timeframe data |

| Pattern Recognition | Detects candlestick patterns **with volume confirmation** | Limited or no pattern recognition |

| Dynamic Risk Management | ATR‑based stops and trailing stops | Often uses fixed stops or basic risk rules |

| Performance Tracking | Adjusts thresholds based on past performance | Typically static parameters |

| Beginner‑Friendly Presets | Aggressive, Conservative, Optimized profiles | Requires manual parameter tuning |

| Visual Cues | Color‑coded backgrounds for regimes | Basic or no visual aids |

The Dskyz strategy’s ability to integrate regime detection, multi-timeframe analysis, and user-friendly presets makes it uniquely versatile and accessible, addressing the needs of everyday traders who want professional-grade tools without the complexity.

-Key Features and Benefits

[Why It’s Ideal for Everyday Traders

⚡The Dskyz (DAFE) AI Adaptive Regime - Pro democratizes advanced trading by offering professional-grade tools in an accessible package. Unlike many TradingView strategies that require deep technical knowledge or fail in changing market conditions, this strategy simplifies complex analysis while maintaining robustness. Its presets and visual aids make it easy for beginners to start, while its adaptive features and performance tracking appeal to advanced traders seeking an edge.

🔄Limitations and Considerations

Market Dependency: Performance varies by market and timeframe. Backtesting is essential to ensure compatibility with your trading style.

Learning Curve: While presets simplify use, understanding regimes and indicators enhances effectiveness.

No Guaranteed Profits: Like all strategies, success depends on market conditions and proper execution. The Reddit discussion highlights skepticism about TradingView strategies’ universal success (Reddit Discussion).

Instrument Specificity: Optimized for futures (e.g., ES, NQ) due to fixed tick values. Test on other instruments like stocks or forex to verify compatibility.

📌Conclusion

The Dskyz (DAFE) AI Adaptive Regime - Pro is a revolutionary TradingView strategy that empowers everyday traders with advanced, AI-driven tools. Its ability to adapt to market regimes, confirm signals across timeframes, and manage risk dynamically. sets it apart from typical strategies. By offering beginner-friendly presets and visual cues, it makes sophisticated trading accessible without sacrificing power. Whether you’re a novice looking to trade smarter or a pro seeking a competitive edge, this strategy is your ticket to mastering the markets. Add it to your chart, backtest it, and join the elite traders leveraging AI to dominate. Trade like a boss today! 🚀

Use it with discipline. Use it with clarity. Trade smarter.

**I will continue to release incredible strategies and indicators until I turn this into a brand or until someone offers me a contract.

-Dskyz

DI+/- Cross Strategy with ATR SL and 2% TPDI+/- Cross Strategy with ATR Stop Loss and 2% Take Profit

📝 Script Description for Publishing:

This strategy is based on the directional movement of the market using the Average Directional Index (ADX) components — DI+ and DI- — to generate entry signals, with clearly defined risk and reward targets using ATR-based Stop Loss and Fixed Percentage Take Profit.

🔍 How it works:

Buy Signal: When DI+ crosses above 40, signaling strong bullish momentum.

Sell Signal: When DI- crosses above 40, indicating strong bearish momentum.

Stop Loss: Dynamically calculated using ATR × 1.5, to account for market volatility.

Take Profit: Fixed at 2% above/below the entry price, for consistent reward targeting.

🧠 Why it’s useful:

Combines momentum breakout logic with volatility-based risk management.

Works well on trending assets, especially when combined with higher timeframe filters.

Clean BUY and SELL visual labels make it easy to interpret and backtest.

✅ Tips for Use:

Use on assets with clear trends (e.g., major forex pairs, trending stocks, crypto).

Best on 30m – 4H timeframes, but can be customized.

Consider combining with other filters (e.g., EMA trend direction or Bollinger Bands) for even better accuracy.

Trend Confirmation StrategyComprehensive Trend Confirmation System

Indicator Features (Professional Description):

Comprehensive Trend Confirmation System is a versatile indicator meticulously designed to identify and confirm trend-based trading opportunities with exceptional efficiency. By seamlessly integrating analysis from a suite of leading technical tools, it aims to provide superior accuracy and reliability for informed trading decisions.

Key Features:

Intelligent Trend Identification: A robust trend analysis system that considers:

Adjustable Moving Averages: Utilizes three customizable moving average periods (fast, medium, slow) with user-selectable lengths and types (SMA, EMA, WMA, VWMA) to accurately determine the prevailing trend across different timeframes.

In-depth Price Action Analysis: Examines the formation of Higher Highs/Higher Lows (uptrend) and Lower Highs/Lower Lows (downtrend) to validate price direction.

Average Directional Index (ADX) with Adjustable Threshold: Measures the strength of a trend and employs the comparison between +DI and -DI to pinpoint the dominant momentum, featuring a customizable threshold to filter out weak signals.

Multi-Factor Signal Confirmation System: Enhances the reliability of trading signals through verification from four distinct confirmation tools:

Volume Analysis with Average Reference: Assesses whether trading volume supports price movements by comparing it to historical averages.

Relative Strength Index (RSI) with Reference Levels: Measures price momentum and identifies overbought/oversold conditions to confirm trend strength.

Moving Average Convergence Divergence (MACD) Divergence and Crossovers: Detects shifts in momentum and potential trend changes through the relationship between the MACD line and the Signal line.

Stochastic Oscillator with Reference Levels: Measures the current price's position relative to its historical range to evaluate overbought/oversold conditions and potential reversal opportunities.

Intelligent Signal Generation Logic:

Buy Signal: Triggered when a strong uptrend is identified (meeting defined criteria) and confirmed by at least three out of the four confirmation tools.

Sell Signal: Triggered when a strong downtrend is identified (meeting defined criteria) and confirmed by at least three out of the four confirmation tools.

User-Friendly Visualizations:

Moving Averages (MA): Displays three MA lines on the chart with user-configurable colors (default: fast-blue, medium-orange, slow-red) for easy visual trend analysis.

Clear Buy and Sell Signal Symbols: Presents distinct green upward-pointing triangles for buy signals and red downward-pointing triangles for sell signals at the corresponding candlestick.

Dynamic Candlestick Color Coding: Candlesticks are dynamically colored green upon a buy signal and red upon a sell signal for quick identification of trading opportunities.

Highly Customizable Parameters: Users have extensive control over the indicator's parameters, including:

Lengths and types of Moving Averages.

Length and Threshold of the ADX.

Length of the RSI.

Parameters for the MACD (Fast Length, Slow Length, Signal Length).

Parameters for the Stochastic Oscillator (%K Length, %D Length, Smoothing).

Ideal For:

Traders seeking a robust tool to accurately identify and confirm market trends.

Individuals aiming to reduce false signals and enhance the precision of their trading decisions.

Traders employing trend-following strategies in markets with clear directional movement.

Important Note:

While Comprehensive Trend Confirmation System is engineered to improve trading accuracy, no indicator can guarantee 100% profitable trades. Users are advised to utilize this indicator in conjunction with relevant fundamental analysis and sound risk management practices for optimal trading outcomes.

Professional MSTI+ Trading Indicator"Professional MSTI+ Trading Indicator" is a comprehensive technical analysis tool that combines over 20 indicators to generate high-quality trading signals and assess market sentiment. The script integrates standard indicators (MACD, RSI, Bollinger Bands, Stochastic, Simple Moving Averages, and Volume Analysis) with advanced components (Squeeze Momentum, Fisher Transform, True Strength Index, Heikin-Ashi, Laguerre RSI, Hull MA) and further includes metrics such as ADX, Chaikin Money Flow, Williams %R, VWAP, and EMA for in-depth market analysis.

Key Features:

Multiple Presets for Different Trading Styles:

Choose from optimal configurations like Professional, Swing Trading, Day Trading, Scalping, or Reversal Hunter. Note that the presets may not work perfectly on all pairs, and manual calibration might be required. This flexibility allows you to fine-tune the settings to align with your unique strategies and signals.

Multi-Layered Signal Filtering:

Filters based on trend, volume, and volatility help eliminate false signals, enhancing the accuracy of market entries.

Comprehensive Fear & Greed Index:

The indicator aggregates data from RSI, volatility, momentum, trend, and volume to gauge overall market sentiment, providing an additional layer of market context.

Dynamic Information Panel:

Displays detailed status updates for each component (e.g., MACD, RSI, Laguerre RSI, TSI, Fisher Transform, Squeeze, Hull MA, etc.) along with a visual strength bar that represents the intensity of the trading signal.

Signal Generation:

Buy and sell signals are generated when a predefined number of conditions are met and confirmed over multiple bars. These signals are clearly displayed on the chart with arrows, making it easier to spot potential entry and exit points.

Alert Setup:

Built-in alert conditions allow you to receive real-time notifications when trading signals are generated, helping you stay on top of market movements.

"Professional MSTI+ Trading Indicator" is designed to enhance your trading strategy by providing a multi-faceted market analysis and an intuitive visual interface. While the presets offer a robust starting point, they may require manual calibration on certain pairs, giving you the flexibility to configure your own unique strategies and signals.

Multi-Anchored Linear Regression Channels [TANHEF]█ Overview:

The 'Multi-Anchored Linear Regression Channels ' plots multiple dynamic regression channels (or bands) with unique selectable calculation types for both regression and deviation. It leverages a variety of techniques, customizable anchor sources to determine regression lengths, and user-defined criteria to highlight potential opportunities.

Before getting started, it's worth exploring all sections, but make sure to review the Setup & Configuration section in particular. It covers key parameters like anchor type, regression length, bias, and signal criteria—essential for aligning the tool with your trading strategy.

█ Key Features:

⯁ Multi-Regression Capability:

Plot up to three distinct regression channels and/or bands simultaneously, each with customizable anchor types to define their length.

⯁ Regression & Deviation Methods:

Regressions Types:

Standard: Uses ordinary least squares to compute a simple linear trend by averaging the data and deriving a slope and endpoints over the lookback period.

Ridge: Introduces L2 regularization to stabilize the slope by penalizing large coefficients, which helps mitigate multicollinearity in the data.

Lasso: Uses L1 regularization through soft-thresholding to shrink less important coefficients, yielding a simpler model that highlights key trends.

Elastic Net: Combines L1 and L2 penalties to balance coefficient shrinkage and selection, producing a robust weighted slope that handles redundant predictors.

Huber: Implements the Huber loss with iteratively reweighted least squares (IRLS) and EMA-style weights to reduce the impact of outliers while estimating the slope.

Least Absolute Deviations (LAD): Reduces absolute errors using iteratively reweighted least squares (IRLS), yielding a slope less sensitive to outliers than squared-error methods.

Bayesian Linear: Merges prior beliefs with weighted data through Bayesian updating, balancing the prior slope with data evidence to derive a probabilistic trend.

Deviation Types:

Regressive Linear (Reverse): In reverse order (recent to oldest), compute weighted squared differences between the data and a line defined by a starting value and slope.

Progressive Linear (Forward): In forward order (oldest to recent), compute weighted squared differences between the data and a line defined by a starting value and slope.

Balanced Linear: In forward order (oldest to newest), compute regression, then pair to source data in reverse order (newest to oldest) to compute weighted squared differences.

Mean Absolute: Compute weighted absolute differences between each data point and its regression line value, then aggregate them to yield an average deviation.

Median Absolute: Determine the weighted median of the absolute differences between each data point and its regression line value to capture the central tendency of deviations.

Percent: Compute deviation as a percentage of a base value by multiplying that base by the specified percentage, yielding symmetric positive and negative deviations.

Fitted: Compare a regression line with high and low series values by computing weighted differences to determine the maximum upward and downward deviations.

Average True Range: Iteratively compute the weighted average of absolute differences between the data and its regression line to yield an ATR-style deviation measure.

Bias:

Bias: Applies EMA or inverse-EMA style weighting to both Regression and/or Deviation, emphasizing either recent or older data.

⯁ Customizable Regression Length via Anchors:

Anchor Types:

Fixed: Length.

Bar-Based: Bar Highest/Lowest, Volume Highest/Lowest, Spread Highest/Lowest.

Correlation: R Zero, R Highest, R Lowest, R Absolute.

Slope: Slope Zero, Slope Highest, Slope Lowest, Slope Absolute.

Indicator-Based: Indicators Highest/Lowest (ADX, ATR, BBW, CCI, MACD, RSI, Stoch).

Time-Based: Time (Day, Week, Month, Quarter, Year, Decade, Custom).

Session-Based: Session (Tokyo, London, New York, Sydney, Custom).

Event-Based: Earnings, Dividends, Splits.

External: Input Source Highest/Lowest.

Length Selection:

Maximum: The highest allowed regression length (also fixed value of “Length” anchor).

Minimum: The shortest allowed length, ensuring enough bars for a valid regression.

Step: The sampling interval (e.g., 1 checks every bar, 2 checks every other bar, etc.). Increasing the step reduces the loading time, most applicable to “Slope” and “R” anchors.

Adaptive lookback:

Adaptive Lookback: Enable to display regression regardless of too few historical bars.

⯁ Selecting Bias:

Bias applies separately to regression and deviation.

Positive values emphasize recent data (EMA-style), negative invert, and near-zero maintains balance. (e.g., a length 100, bias +1 gives the newest price ~7× more weight than the oldest).

It's best to apply bias to both (regression and deviation) or just the deviation. Biasing only regression may distort deviation visually, while biasing both keeps their relationship intuitive. Using bias only for deviation scales it without altering regression, offering unique analysis.

⯁ Scale Awareness:

Supports linear and logarithmic price scaling, the regression and deviations adjust accordingly.

⯁ Signal Generation & Alerts:

Customizable entry/exit signals and alerts, detailed in the dedicated section below.

⯁ Visual Enhancements & Real-World Examples:

Optional on-chart table display summarizing regression input criteria (display type, anchor type, source, regression type, regression bias, deviation type, deviation bias, deviation multiplier) and key calculated metrics (regression length, slope, Pearson’s R, percentage position within deviations, etc.) for quick reference.

█ Understanding R (Pearson Correlation Coefficient):

Pearson’s R gauges data alignment to a straight-line trend within the regression length:

Range: R varies between –1 and +1.

R = +1 → Perfect positive correlation (strong uptrend).

R = 0 → No linear relationship detected.

R = –1 → Perfect negative correlation (strong downtrend).

This script uses Pearson’s R as an anchor, adjusting regression length to target specific R traits. Strong R (±1) follows the regression channel, while weak R (0) shows inconsistency.

█ Understanding the Slope:

The slope is the direction and rate at which the regression line rises or falls per bar:

Positive Slope (>0): Uptrend – Steeper means faster increase.

Negative Slope (<0): Downtrend – Steeper means sharper drop.

Zero or Near-Zero Slope: Sideways – Indicating range-bound conditions.

This script uses highest and lowest slope as an anchor, where extremes highlight strong moves and trend lines, while values near zero indicate sideways action and possible support/resistance.

█ Setup & Configuration:

Whether you’re new to this script or want to quickly adjust all critical parameters, the panel below shows the main settings available. You can customize everything from the anchor type and maximum length to the bias, signal conditions, and more.

Scale (select Log Scale for logarithmic, otherwise linear scale).

Display (regression channel and/or bands).

Anchor (how regression length is determined).

Length (control bars analyzed):

• Max – Upper limit.

• Min – Prevents regression from becoming too short.

• Step – Controls scanning precision; increasing Step reduces load time.

Regression:

• Type – Calculation method.

• Bias – EMA-style emphasis (>0=new bars weighted more; <0=old bars weighted more).

Deviation:

• Type – Calculation method.

• Bias – EMA-style emphasis (>0=new bars weighted more; <0=old bars weighted more).

• Multiplier - Adjusts Upper and Lower Deviation.

Signal Criteria:

• % (Price vs Deviation) – (0% = lower deviation, 50% = regression, 100% = upper deviation).

• R – (0 = no correlation, ±1 = perfect correlation; >0 = +slope, <0 = -slope).

Table (analyze table of input settings, calculated results, and signal criteria).

Adaptive Lookback (display regression while too few historical bars).

Multiple Regressions (steps 2 to 7 apply to #1, #2, and #3 regressions).

█ Signal Generation & Alerts:

The script offers customizable entry and exit signals with flexible criteria and visual cues (background color, dots, or triangles). Alerts can also be triggered for these opportunities.

Percent Direction Criteria:

(0% = lower deviation, 50% = regression line, 100% = upper deviation)

Above %: Triggers if price is above a specified percent of the deviation channel.

Below %: Triggers if price is below a specified percent of the deviation channel.

(Blank): Ignores the percent‐based condition.

Pearson's R (Correlation) Direction Criteria:

(0 = no correlation, ±1 = perfect correlation; >0 = positive slope, <0 = negative slope)

Above R / Below R: Compares the correlation to a threshold.

Above│R│ / Below│R│: Uses absolute correlation to focus on strength, ignoring direction.

Zero to R: Checks if R is in the 0-to-threshold range.

(Blank): Ignores correlation-based conditions.

█ User Tips & Best Practices:

Choose an anchor type that suits your strategy, “Bar Highest/Lowest” automatically spots commonly used regression zones, while “│R│ Highest” targets strong linear trends.

Consider enabling or disabling the Adaptive Lookback feature to ensure you always have a plotted regression if your chart doesn’t meet the maximum-length requirement.

Use a small Step size (1) unless relying on R-correlation or slope-based anchors as the are time-consuming to calculate. Larger steps speed up calculations but reduce precision.

Fine-tune settings such as lookback periods, regression bias, and deviation multipliers, or trend strength. Small adjustments can significantly affect how channels and signals behave.

To reduce loading time , show only channels (not bands) and disable signals, this limits calculations to the last bar and supports more extreme criteria.

Use the table display to monitor anchor type, calculated length, slope, R value, and percent location at a glance—especially if you have multiple regressions visible simultaneously.

█ Conclusion:

With its blend of advanced regression techniques, flexible deviation options, and a wide range of anchor types, this indicator offers a highly adaptable linear regression channeling system. Whether you're anchoring to time, price extremes, correlation, slope, or external events, the tool can be shaped to fit a variety of strategies. Combined with customizable signals and alerts, it may help highlight areas of confluence and support a more structured approach to identifying potential opportunities.

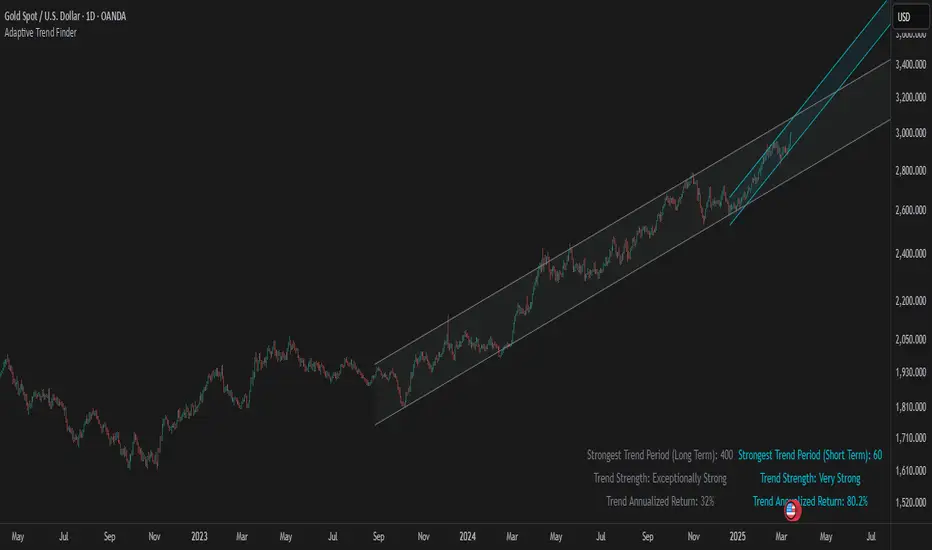

Adaptive Trend FinderAdaptive Trend Finder - The Ultimate Trend Detection Tool

Introducing Adaptive Trend Finder, the next evolution of trend analysis on TradingView. This powerful indicator is an enhanced and refined version of Adaptive Trend Finder (Log), designed to offer even greater flexibility, accuracy, and ease of use.

What’s New?

Unlike the previous version, Adaptive Trend Finder allows users to fully configure and adjust settings directly within the indicator menu, eliminating the need to modify chart settings manually. A major improvement is that users no longer need to adjust the chart's logarithmic scale manually in the chart settings; this can now be done directly within the indicator options, ensuring a smoother and more efficient experience. This makes it easier to switch between linear and logarithmic scaling without disrupting the analysis. This provides a seamless user experience where traders can instantly adapt the indicator to their needs without extra steps.

One of the most significant improvements is the complete code overhaul, which now enables simultaneous visualization of both long-term and short-term trend channels without needing to add the indicator twice. This not only improves workflow efficiency but also enhances chart readability by allowing traders to monitor multiple trend perspectives at once.

The interface has been entirely redesigned for a more intuitive user experience. Menus are now clearer, better structured, and offer more customization options, making it easier than ever to fine-tune the indicator to fit any trading strategy.

Key Features & Benefits

Automatic Trend Period Selection: The indicator dynamically identifies and applies the strongest trend period, ensuring optimal trend detection with no manual adjustments required. By analyzing historical price correlations, it selects the most statistically relevant trend duration automatically.

Dual Channel Display: Traders can view both long-term and short-term trend channels simultaneously, offering a broader perspective of market movements. This feature eliminates the need to apply the indicator twice, reducing screen clutter and improving efficiency.

Fully Adjustable Settings: Users can customize trend detection parameters directly within the indicator settings. No more switching chart settings – everything is accessible in one place.

Trend Strength & Confidence Metrics: The indicator calculates and displays a confidence score for each detected trend using Pearson correlation values. This helps traders gauge the reliability of a given trend before making decisions.

Midline & Channel Transparency Options: Users can fine-tune the visibility of trend channels, adjusting transparency levels to fit their personal charting style without overwhelming the price chart.

Annualized Return Calculation: For daily and weekly timeframes, the indicator provides an estimate of the trend’s performance over a year, helping traders evaluate potential long-term profitability.

Logarithmic Adjustment Support: Adaptive Trend Finder is compatible with both logarithmic and linear charts. Traders who analyze assets like cryptocurrencies, where log scaling is common, can enable this feature to refine trend calculations.

Intuitive & User-Friendly Interface: The updated menu structure is designed for ease of use, allowing quick and efficient modifications to settings, reducing the learning curve for new users.

Why is this the Best Trend Indicator?

Adaptive Trend Finder stands out as one of the most advanced trend analysis tools available on TradingView. Unlike conventional trend indicators, which rely on fixed parameters or lagging signals, Adaptive Trend Finder dynamically adjusts its settings based on real-time market conditions. By combining automatic trend detection, dual-channel visualization, real-time performance metrics, and an intuitive user interface, this indicator offers an unparalleled edge in trend identification and trading decision-making.

Traders no longer have to rely on guesswork or manually tweak settings to identify trends. Adaptive Trend Finder does the heavy lifting, ensuring that users are always working with the strongest and most reliable trends. The ability to simultaneously display both short-term and long-term trends allows for a more comprehensive market overview, making it ideal for scalpers, swing traders, and long-term investors alike.

With its state-of-the-art algorithms, fully customizable interface, and professional-grade accuracy, Adaptive Trend Finder is undoubtedly one of the most powerful trend indicators available.

Try it today and experience the future of trend analysis.

This indicator is a technical analysis tool designed to assist traders in identifying trends. It does not guarantee future performance or profitability. Users should conduct their own research and apply proper risk management before making trading decisions.

// Created by Julien Eche - @Julien_Eche

Market Trend Levels Non-Repainting [BigBeluga X PineIndicators]This strategy is based on the Market Trend Levels Detector developed by BigBeluga. Full credit for the concept and original indicator goes to BigBeluga.

The Market Trend Levels Detector Strategy is a non-repainting trend-following strategy that identifies market trend shifts using two Exponential Moving Averages (EMA). It also detects key price levels and allows traders to apply multiple filters to refine trade entries and exits.

This strategy is designed for trend trading and enables traders to:

Identify trend direction based on EMA crossovers.

Detect significant market levels using labeled trend lines.

Use multiple filter conditions to improve trade accuracy.

Avoid false signals through non-repainting calculations.

How the Market Trend Levels Detector Strategy Works

1. Core Trend Detection Using EMA Crossovers

The strategy detects trend shifts using two EMAs:

Fast EMA (default: 12 periods) – Reacts quickly to price movements.

Slow EMA (default: 25 periods) – Provides a smoother trend confirmation.

A bullish crossover (Fast EMA crosses above Slow EMA) signals an uptrend , while a bearish crossover (Fast EMA crosses below Slow EMA) signals a downtrend .

2. Market Level Detection & Visualization

Each time an EMA crossover occurs, a trend level line is drawn:

Bullish crossover → A green line is drawn at the low of the crossover candle.

Bearish crossover → A purple line is drawn at the high of the crossover candle.

Lines can be extended to act as support and resistance zones for future price action.

Additionally, a small label (●) appears at each crossover to mark the event on the chart.

3. Trade Entry & Exit Conditions

The strategy allows users to choose between three trading modes:

Long Only – Only enters long trades.

Short Only – Only enters short trades.

Long & Short – Trades in both directions.

Entry Conditions

Long Entry:

A bullish EMA crossover occurs.

The trade direction setting allows long trades.

Filter conditions (if enabled) confirm a valid long signal.

Short Entry:

A bearish EMA crossover occurs.

The trade direction setting allows short trades.

Filter conditions (if enabled) confirm a valid short signal.

Exit Conditions

Long Exit:

A bearish EMA crossover occurs.

Exit filters (if enabled) indicate an invalid long position.

Short Exit:

A bullish EMA crossover occurs.

Exit filters (if enabled) indicate an invalid short position.

Additional Trade Filters

To improve trade accuracy, the strategy allows traders to apply up to 7 additional filters:

RSI Filter: Only trades when RSI confirms a valid trend.

MACD Filter: Ensures MACD histogram supports the trade direction.

Stochastic Filter: Requires %K line to be above/below threshold values.

Bollinger Bands Filter: Confirms price position relative to the middle BB line.

ADX Filter: Ensures the trend strength is above a set threshold.

CCI Filter: Requires CCI to indicate momentum in the right direction.

Williams %R Filter: Ensures price momentum supports the trade.

Filters can be enabled or disabled individually based on trader preference.

Dynamic Level Extension Feature

The strategy provides an optional feature to extend trend lines until price interacts with them again:

Bullish support lines extend until price revisits them.

Bearish resistance lines extend until price revisits them.

If price breaks a line, the line turns into a dotted style , indicating it has been breached.

This helps traders identify key levels where trend shifts previously occurred, providing useful support and resistance insights.

Customization Options

The strategy includes several adjustable settings :

Trade Direction: Choose between Long Only, Short Only, or Long & Short.

Trend Lengths: Adjust the Fast & Slow EMA lengths.

Market Level Extension: Decide whether to extend support/resistance lines.

Filters for Trade Confirmation: Enable/disable individual filters.

Color Settings: Customize line colors for bullish and bearish trend shifts.

Maximum Displayed Lines: Limit the number of drawn support/resistance lines.

Considerations & Limitations

Trend Lag: As with any EMA-based strategy, signals may be slightly delayed compared to price action.

Sideways Markets: This strategy works best in trending conditions; frequent crossovers in sideways markets can produce false signals.

Filter Usage: Enabling multiple filters may reduce trade frequency, but can also improve trade quality.

Line Overlap: If many crossovers occur in a short period, the chart may become cluttered with multiple trend levels. Adjusting the "Display Last" setting can help.

Conclusion

The Market Trend Levels Detector Strategy is a non-repainting trend-following system that combines EMA crossovers, market level detection, and customizable filters to improve trade accuracy.

By identifying trend shifts and key price levels, this strategy can be used for:

Trend Confirmation – Using EMA crossovers and filters to confirm trend direction.

Support & Resistance Trading – Identifying dynamic levels where price reacts.

Momentum-Based Trading – Combining EMA crossovers with additional momentum filters.

This strategy is fully customizable and can be adapted to different trading styles, timeframes, and market conditions.

Full credit for the original concept and indicator goes to BigBeluga.

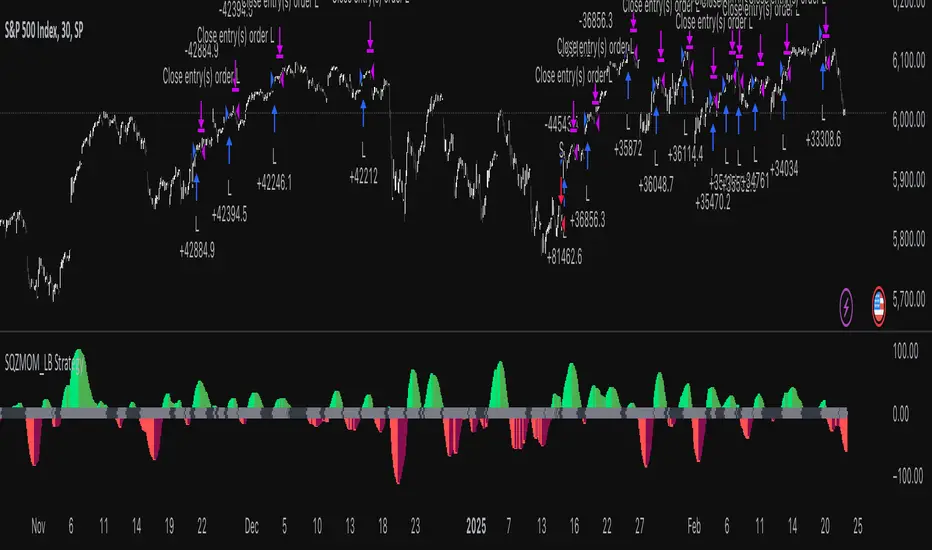

Squeeze Momentum Indicator Strategy [LazyBear + PineIndicators]The Squeeze Momentum Indicator Strategy (SQZMOM_LB Strategy) is an automated trading strategy based on the Squeeze Momentum Indicator developed by LazyBear, which itself is a modification of John Carter's "TTM Squeeze" concept from his book Mastering the Trade (Chapter 11). This strategy is designed to identify low-volatility phases in the market, which often precede explosive price movements, and to enter trades in the direction of the prevailing momentum.

Concept & Indicator Breakdown

The strategy employs a combination of Bollinger Bands (BB) and Keltner Channels (KC) to detect market squeezes:

Squeeze Condition:

When Bollinger Bands are inside the Keltner Channels (Black Crosses), volatility is low, signaling a potential upcoming price breakout.

When Bollinger Bands move outside Keltner Channels (Gray Crosses), the squeeze is released, indicating an expansion in volatility.

Momentum Calculation:

A linear regression-based momentum value is used instead of traditional momentum indicators.

The momentum histogram is color-coded to show strength and direction:

Lime/Green: Increasing bullish momentum

Red/Maroon: Increasing bearish momentum

Signal Colors:

Black: Market is in a squeeze (low volatility).

Gray: Squeeze is released, and volatility is expanding.

Blue: No squeeze condition is present.

Strategy Logic

The script uses historical volatility conditions and momentum trends to generate buy/sell signals and manage positions.

1. Entry Conditions

Long Position (Buy)

The squeeze just released (Gray Cross after Black Cross).

The momentum value is increasing and positive.

The momentum is at a local low compared to the past 100 bars.

The price is above the 100-period EMA.

The closing price is higher than the previous close.

Short Position (Sell)

The squeeze just released (Gray Cross after Black Cross).

The momentum value is decreasing and negative.

The momentum is at a local high compared to the past 100 bars.

The price is below the 100-period EMA.

The closing price is lower than the previous close.

2. Exit Conditions

Long Exit:

The momentum value starts decreasing (momentum lower than previous bar).

Short Exit:

The momentum value starts increasing (momentum higher than previous bar).

Position Sizing

Position size is dynamically adjusted based on 8% of strategy equity, divided by the current closing price, ensuring risk-adjusted trade sizes.

How to Use This Strategy

Apply on Suitable Markets:

Best for stocks, indices, and forex pairs with momentum-driven price action.

Works on multiple timeframes but is most effective on higher timeframes (1H, 4H, Daily).

Confirm Entries with Additional Indicators:

The author recommends ADX or WaveTrend to refine entries and avoid false signals.

Risk Management:

Since the strategy dynamically sizes positions, it's advised to use stop-losses or risk-based exits to avoid excessive drawdowns.

Final Thoughts

The Squeeze Momentum Indicator Strategy provides a systematic approach to trading volatility expansions, leveraging the classic TTM Squeeze principles with a unique linear regression-based momentum calculation. Originally inspired by John Carter’s method, LazyBear's version and this strategy offer a refined, adaptable tool for traders looking to capitalize on market momentum shifts.

DrawIndicatorOnTheChartLibrary "DrawIndicatorOnTheChart"

this library is used to show an indicator (such RSI, CCI, MOM etc) on the main chart with indicator's horizontal lines in a window. Location of the window is calculated dynamically by last price movemements

drawIndicator(enabled, indicatorName, indicator1, indicator2, indicator3, indicatorcolors, period, indimax_, indimin_, levels, precision, xlocation, lnwidth)

draws the realted indicator on the chart

Parameters:

enabled (bool) : if it's enabled to show

indicatorName (string) : is the indicator name as string such "RSI", "CCI" etc

indicator1 (float) : is first indicator you want to show, such rsi(close, 14), mom(close, 10) etc

indicator2 (float) : is second indicator you want to show, such -DI of DMI

indicator3 (float) : is third indicator you want to show, such ADX of DMI

indicatorcolors (array)

period (int) : is the length of the window to show

indimax_ (float) : is the maximum value of the indicator, for example for RSI it's 100.0, if the indicator (such CCI, MOM etc) doesn't have maximum value then use "na"

indimin_ (float) : is the minimum value of the indicator, for example for RSI it's 0.0, if the indicator (such CCI, MOM etc)doesn't have maximum value then use "na"

levels (array) : is the levels of the array for the horizontal lines. for example if you want horizontal lines at 30.0, and 70.0 then use array.from(30.0, 70.0). if no horizontal lines then use array.from(na)

precision (int) : is the precision/nuber of decimals that is used to show indicator values, for example for RSI set it 2

xlocation (int) : is end location of the indicator window, for example if xlocation = 0 window is created on the index of the last bar/candle

lnwidth (int) : is the line width of the indicator lines

Returns: none