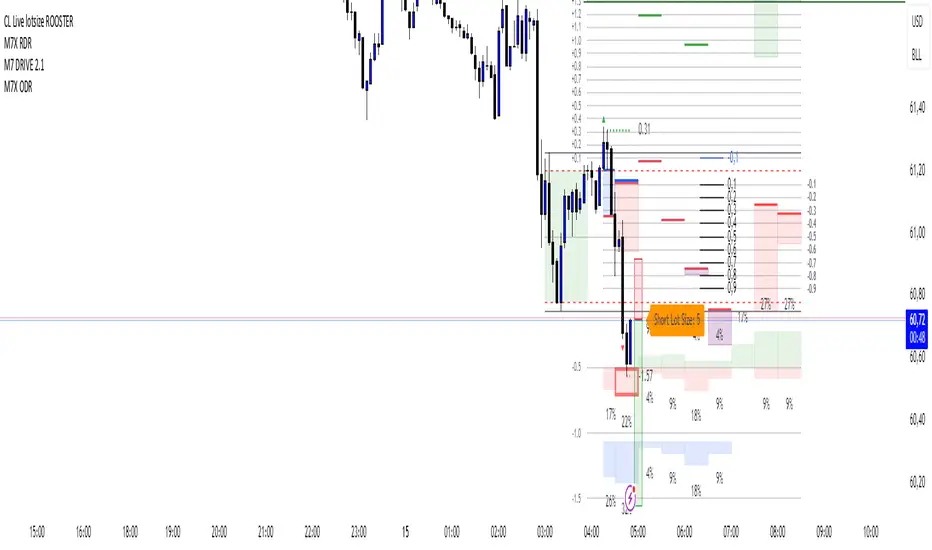

CL Live lotsize ROOSTER📄 Description:

This is a utility script designed for manual futures traders who enter with market orders and want to size their positions precisely based on $ risk.

⚙️ Features:

✅ Calculates live contract size based on:

A fixed dollar risk amount (e.g. $100)

A manually set static stop-loss price

The live market price as your entry

✅ Uses a configurable risk-reward ratio (e.g. 1:3)

✅ Plots entry, stop, and target levels on the chart

✅ Displays calculated contract size as a floating label

🎯 Why this tool?

Built to support fast execution workflows , this tool helps traders who:

Enter trades at candle close or open

Want to pre-calculate their market order size before the signal

Prefer a visual, consistent, real-time R:R validation system

Avoid fumbling with the long/short position tool at the last second

🔧 Settings:

Static Stop-Loss Price: Enter the price level where you'd place your SL

Account Risk ($): How much you’re willing to risk per trade

Risk-Reward Ratio: Set your target multiplier (e.g. 3 for 3R)

Wyszukaj w skryptach "Oil"

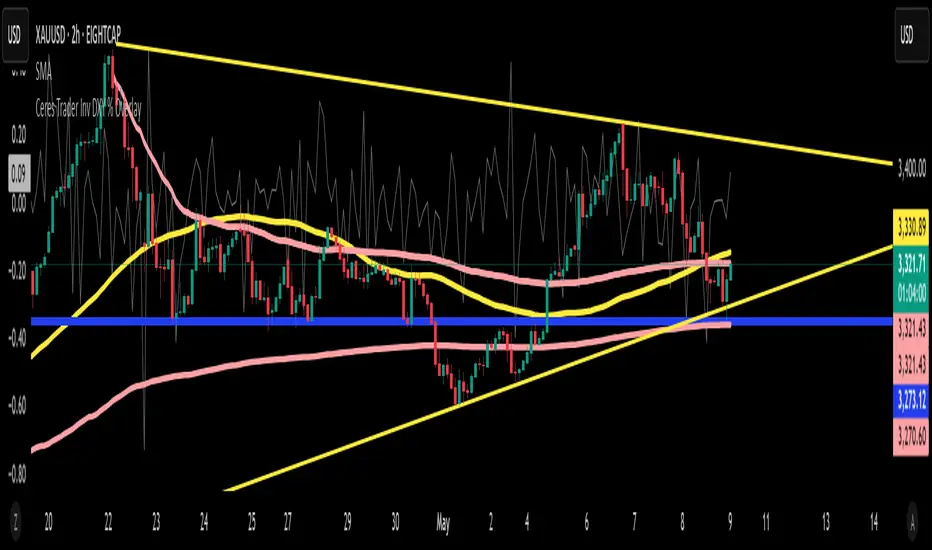

Ceres Trader Inv DXY % OverlayIntroducing the “Inverse DXY % Overlay” for TradingView

What it does:

• Plots the U.S. Dollar Index (DXY) as an inverted %-change line directly over your primary chart (e.g. XAUUSD).

• Dollar strength shows as a downward line; dollar weakness shows as an upward line—instantly highlighting negative correlation.

Why it helps:

• Trend confirmation – Ride Gold breakouts only when the dollar is actually weakening.

• Divergence signals – Spot early turn setups when Gold and DXY % don’t move in sync.

• Risk management – Trim or tighten stops when the dollar pivots against your position.

Key features:

Overlay on any symbol (Gold, Silver, Oil, Crypto, equities)

Auto-scaled to left-axis %, so your price chart stays on the right

Lightweight & transparent—1 px grey line, minimal clutter

Now you’ll have a real-time, inverted DXY % line beneath your candles—perfect for gauging USD flow before you pull the trigger on any trade.

Happy trading! 🚀

—Michael (Ceres Trader)

Ticker DataThis script mostly for Pine coders but may be useful for regular users too.

I often find myself needing quick access to certain information about a ticker — like its full ticker name, mintick, last bar index and so on. Usually, I write a few lines of code just to display this info and check it.

Today I got tired of doing that manually, so I created a small script that shows the most essential data in one place. I also added a few extra fields that might be useful or interesting to regular users.

Description for regular users (from Pine Script Reference Manual)

tickerid - full ticker name

description - description for the current symbol

industry - the industry of the symbol. Example: "Internet Software/Services", "Packaged software", "Integrated Oil", "Motor Vehicles", etc.

country - the two-letter code of the country where the symbol is traded

sector - the sector of the symbol. Example: "Electronic Technology", "Technology services", "Energy Minerals", "Consumer Durables", etc.

session - session type (regular or extended)

timezone - timezone of the exchange of the chart

type - the type of market the symbol belongs to. Example: "stock", "fund", "index", "forex", "futures", "spread", "economic", "fundamental", "crypto".

volumetype - volume type of the current symbol.

mincontract - the smallest amount of the current symbol that can be traded

mintick - min tick value for the current symbol (the smallest increment between a symbol's price movements)

pointvalue - point value for the current symbol

pricescale - a whole number used to calculate mintick (usually (when minmove is 1), it shows the resolution — how many decimal places the price has. For example, a pricescale 100 means the price will have two decimal places - 1 / 100 = 0.01)

bar index - last bar index (if add 1 (because indexes starts from 0) it will shows how many bars available to you on the chart)

If you need some more information at table feel free to leave a comment.

Custom Opening Range - CommoditiesThe Custom Opening Range Indicator for Commodities is designed for instruments that trade nearly 24 hours, such as crude oil or natural gas. It allows traders to define the Opening Range based on Indian Standard Time (IST)—typically starting at 3:30 AM IST, which aligns with the global commodities market open. Users can customize both the start time and duration of the range (e.g., 5, 15, or 30 minutes). The indicator dynamically plots the high and low of this range and shades the area between them, providing a clear visual reference for breakout or reversal setups during the rest of the trading session.

Highlight Candle Body ≤ 10 Ticks (Clean & Subtle)Purpose:

This indicator highlights candlesticks where the body size (difference between open and close) is 10 ticks or less, specifically for instruments like Crude Oil futures (CL) where 1 tick = 0.01.

How it works:

It calculates the body size: abs(close - open)

If the body is ≤ 0.10 (10 ticks), the candle is softly colored in muted orange.

Wicks are ignored — only the body is considered.

No additional shapes or markers — clean and minimal.

Use case:

Helps identify periods of indecision or low momentum — such as potential pause candles, traps, or setups just before volatility returns.

Z-Score Normalized Volatility IndicesVolatility is one of the most important measures in financial markets, reflecting the extent of variation in asset prices over time. It is commonly viewed as a risk indicator, with higher volatility signifying greater uncertainty and potential for price swings, which can affect investment decisions. Understanding volatility and its dynamics is crucial for risk management and forecasting in both traditional and alternative asset classes.

Z-Score Normalization in Volatility Analysis

The Z-score is a statistical tool that quantifies how many standard deviations a given data point is from the mean of the dataset. It is calculated as:

Z = \frac{X - \mu}{\sigma}

Where X is the value of the data point, \mu is the mean of the dataset, and \sigma is the standard deviation of the dataset. In the context of volatility indices, the Z-score allows for the normalization of these values, enabling their comparison regardless of the original scale. This is particularly useful when analyzing volatility across multiple assets or asset classes.

This script utilizes the Z-score to normalize various volatility indices:

1. VIX (CBOE Volatility Index): A widely used indicator that measures the implied volatility of S&P 500 options. It is considered a barometer of market fear and uncertainty (Whaley, 2000).

2. VIX3M: Represents the 3-month implied volatility of the S&P 500 options, providing insight into medium-term volatility expectations.

3. VIX9D: The implied volatility for a 9-day S&P 500 options contract, which reflects short-term volatility expectations.

4. VVIX: The volatility of the VIX itself, which measures the uncertainty in the expectations of future volatility.

5. VXN: The Nasdaq-100 volatility index, representing implied volatility in the Nasdaq-100 options.

6. RVX: The Russell 2000 volatility index, tracking the implied volatility of options on the Russell 2000 Index.

7. VXD: Volatility for the Dow Jones Industrial Average.

8. MOVE: The implied volatility index for U.S. Treasury bonds, offering insight into expectations for interest rate volatility.

9. BVIX: Volatility of Bitcoin options, a useful indicator for understanding the risk in the cryptocurrency market.

10. GVZ: Volatility index for gold futures, reflecting the risk perception of gold prices.

11. OVX: Measures implied volatility for crude oil futures.

Volatility Clustering and Z-Score

The concept of volatility clustering—where high volatility tends to be followed by more high volatility—is well documented in financial literature. This phenomenon is fundamental in volatility modeling and highlights the persistence of periods of heightened market uncertainty (Bollerslev, 1986).

Moreover, studies by Andersen et al. (2012) explore how implied volatility indices, like the VIX, serve as predictors for future realized volatility, underlining the relationship between expected volatility and actual market behavior. The Z-score normalization process helps in making volatility data comparable across different asset classes, enabling more effective decision-making in volatility-based strategies.

Applications in Trading and Risk Management

By using Z-score normalization, traders can more easily assess deviations from the mean in volatility, helping to identify periods when volatility is unusually high or low. This can be used to adjust risk exposure or to implement volatility-based trading strategies, such as mean reversion strategies. Research suggests that volatility mean-reversion is a reliable pattern that can be exploited for profit (Christensen & Prabhala, 1998).

References:

• Andersen, T. G., Bollerslev, T., Diebold, F. X., & Vega, C. (2012). Realized volatility and correlation dynamics: A long-run approach. Journal of Financial Economics, 104(3), 385-406.

• Bollerslev, T. (1986). Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 31(3), 307-327.

• Christensen, B. J., & Prabhala, N. R. (1998). The relation between implied and realized volatility. Journal of Financial Economics, 50(2), 125-150.

• Whaley, R. E. (2000). Derivatives on market volatility and the VIX index. Journal of Derivatives, 8(1), 71-84.

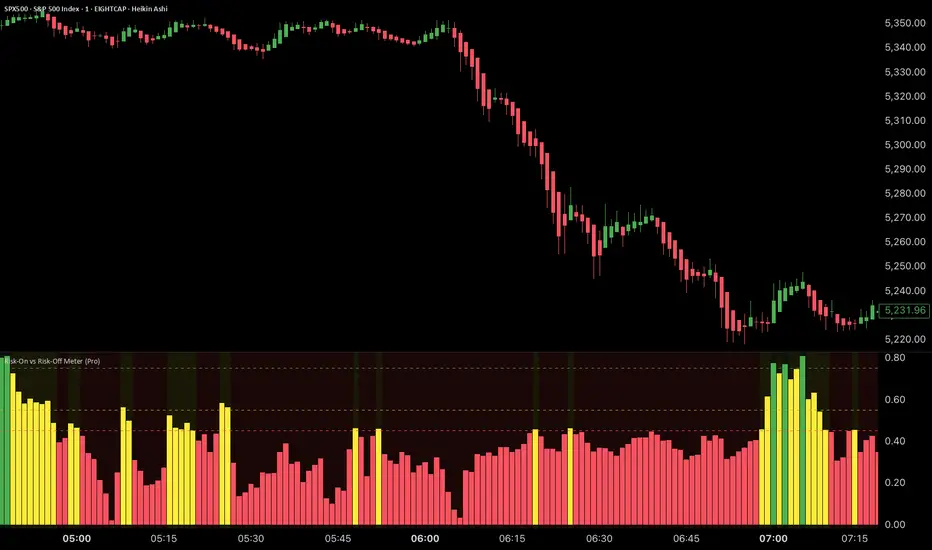

Risk-On vs Risk-Off Meter (Pro)Risk-On vs Risk-Off Meter (Pro)

This macro-based tool analyzes capital flows across key assets to gauge overall market risk sentiment. It does not use ES, SPY, or stock data directly—making it a powerful confirmation tool for ES traders looking to align with macro forces.

🔹 Core Idea:

Tracks capital rotation between copper/gold, bonds, dollar, crude oil, VIX, and yield spreads to generate a normalized risk score (0–1). This score reflects whether macro money is flowing into risk or safety.

🔹 Use:

Use this indicator as confirmation of directional bias when scalping or day trading ES.

– Green Zone (>0.75): Risk-On environment. Favor long setups.

– Red Zone (<0.45): Risk-Off. Favor short setups or stand aside.

– Yellow Zone: Neutral, use caution.

– Divergence Alerts: Signals when ES price disagrees with macro risk trend—potential reversals or exhaustion zones.

HOT TO USE

– Combine with your existing price action or order flow signals

– Avoid trading against the macro sentiment unless strong setup

– Use divergence as a heads-up for fading or exiting trades

This gives you a macro-informed lens to validate or filter your entries.

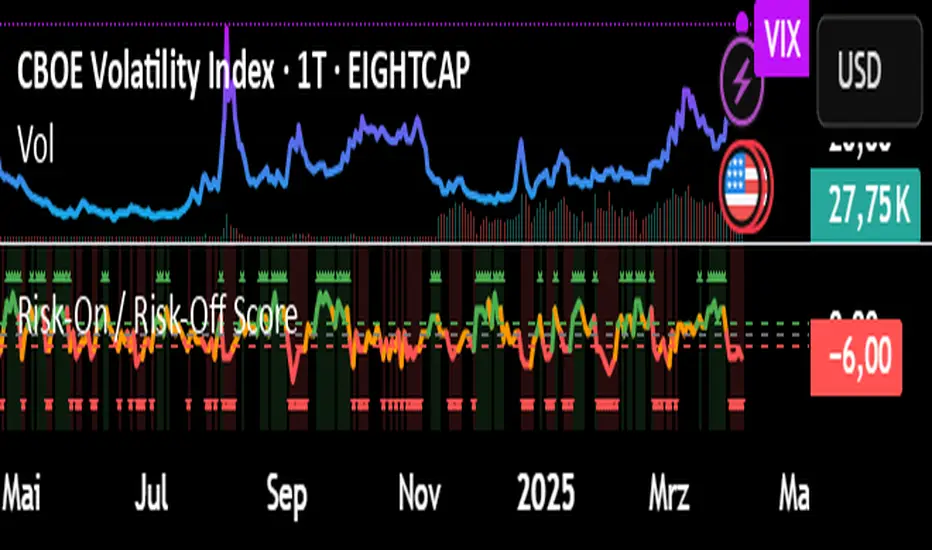

Risk-On / Risk-Off ScoreRisk-On / Risk-Off Score (Macro Sentiment Indicator)

This indicator calculates a custom Risk-On / Risk-Off Score to objectively assess the current market risk sentiment using a carefully selected basket of macroeconomic assets and intermarket relationships.

🧠 What does this indicator do?

The score is based on 14 key components grouped into three categories:

🟢 Risk-On Assets (rising = appetite for risk)

(+1 if performance over X days is positive, otherwise –1)

NASDAQ 100 (NAS100USD)

S&P 500 (SPX)

Bitcoin (BTCUSD)

Copper (HG1!)

WTI Crude Oil (CLK2025)

🔴 Risk-Off Assets (rising = flight to safety)

(–1 if performance is positive, otherwise +1)

Gold (XAUUSD)

US Treasury Bonds (TLT ETF) (TLT)

US Dollar Index (DXY)

USD/CHF

USD/JPY

US 10Y Yields (US10Y) (yields are interpreted inversely)

⚖️ Risk Spreads / Relative Indicators

(+1 if rising, –1 if falling)

Copper/Gold Ratio → HG1! / XAUUSD

NASDAQ/VIX Ratio → NAS100USD / VIX

HYG/TLT Ratio → HYG / TLT

📏 Score Calculation

Total score = sum of all components

Range: from –14 (extreme Risk-Off) to +14 (strong Risk-On)

Color-coded output:

🟢 Score > 2 = Risk-On

🟠 –2 to +2 = Neutral

🔴 Score < –2 = Risk-Off

Displayed as a line plot with background color and signal markers

🧪 Timeframe of analysis:

Default: 5 days (adjustable via input)

Calculated using Rate of Change (% change)

🧭 Use Cases:

Quickly assess macro sentiment

Filter for position sizing, hedging, or intraday bias

Especially useful for:

Swing traders

Day traders with macro filters

Volatility and options traders

📌 Note:

This is not a buy/sell signal indicator, but a contextual sentiment tool designed to help you stay aligned with overall market conditions.

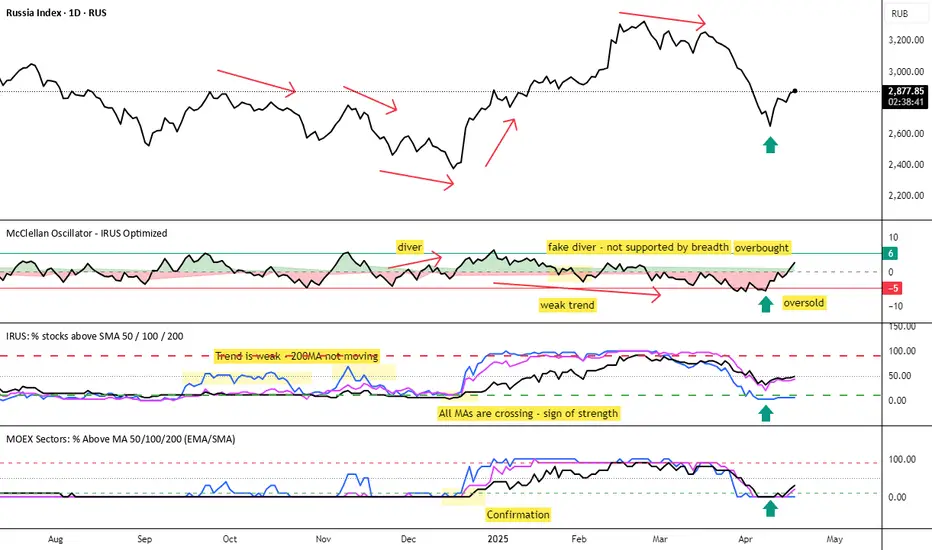

MOEX Sectors: % Above MA 50/100/200 (EMA/SMA)🧠 Name:

MOEX Sectors: % Above MA 50/100/200 (EMA/SMA)

📋 Description (for TradingView “Description” tab):

This indicator shows the percentage of Moscow Exchange sectoral indices trading above the selected moving average (SMA or EMA) with periods of 50, 100, or 200.

It uses 10 official MOEX sector indices:

MOEXOG (Oil & Gas)

MOEXCH (Chemicals)

MOEXMM (Metals & Mining)

MOEXTN (Transport)

MOEXCN (Consumer)

MOEXFN (Financials)

MOEXTL (Telecom)

MOEXEU (Utilities)

MOEXIT (IT)

MOEXRE (Real Estate)

The indicator plots up to 3 lines representing the % of sectors trading above MA 50, 100, and/or 200. The MA type is user-selectable: EMA (default) or SMA.

Horizontal reference levels (90, 50, 10) help interpret market conditions:

🔼 >90% — Overbought zone, potential market exhaustion

⚖️ ~50% — Neutral state

🔽 <10% — Oversold zone, possible rebound

📈 How to Use in Strategy:

✅ 1. Trend Filter

If >50% of sectors are above MA 200 → market in long-term uptrend

If <50% → avoid long bias, bearish regime likely

✅ 2. Bottom Detection

When <10% of sectors are above MA 200, the market is heavily oversold — often a bottoming signal

✅ 3. Trend Confirmation

If the main index is rising and % of sectors above MA is growing, the trend is supported by breadth

If the index rises while breadth declines → bearish divergence

✅ 4. Contrarian Setups

>90% of sectors above MA 50 → market may be overheated, watch for pullback

<20% above MA 50 → potential local bottom

⚙️ Tips:

Overlay this indicator on the IMOEX index chart to detect narrow leadership

Combine with other breadth metrics or RSI on the index

Use the EMA/SMA toggle to fine-tune sensitivity

Pivot S/R with Volatility Filter## *📌 Indicator Purpose*

This indicator identifies *key support/resistance levels* using pivot points while also:

✅ Detecting *high-volume liquidity traps* (stop hunts)

✅ Filtering insignificant pivots via *ATR (Average True Range) volatility*

✅ Tracking *test counts and breakouts* to measure level strength

---

## *⚙ SETTINGS – Detailed Breakdown*

### *1️⃣ ◆ General Settings*

#### *🔹 Pivot Length*

- *Purpose:* Determines how many bars to analyze when identifying pivots.

- *Usage:*

- *Low values (5-20):* More pivots, better for scalping.

- *High values (50-200):* Fewer but stronger levels for swing trading.

- *Example:*

- Pivot Length = 50 → Only the most significant highs/lows over 50 bars are marked.

#### *🔹 Test Threshold (Max Test Count)*

- *Purpose:* Sets how many times a level can be tested before being invalidated.

- *Example:*

- Test Threshold = 3 → After 3 tests, the level is ignored (likely to break).

#### *🔹 Zone Range*

- *Purpose:* Creates a price buffer around pivots (±0.001 by default).

- *Why?* Markets often respect "zones" rather than exact prices.

---

### *2️⃣ ◆ Volatility Filter (ATR)*

#### *🔹 ATR Period*

- *Purpose:* Smoothing period for Average True Range calculation.

- *Default:* 14 (standard for volatility measurement).

#### *🔹 ATR Multiplier (Min Move)*

- *Purpose:* Requires pivots to show *meaningful price movement*.

- *Formula:* Min Move = ATR × Multiplier

- *Example:*

- ATR = 10 pips, Multiplier = 1.5 → Only pivots with *15+ pip swings* are valid.

#### *🔹 Show ATR Filter Info*

- Displays current ATR and minimum move requirements on the chart.

---

### *3️⃣ ◆ Volume Analysis*

#### *🔹 Volume Change Threshold (%)*

- *Purpose:* Filters for *unusual volume spikes* (institutional activity).

- *Example:*

- Threshold = 1.2 → Requires *120% of average volume* to confirm signals.

#### *🔹 Volume MA Period*

- *Purpose:* Lookback period for "normal" volume calculation.

---

### *4️⃣ ◆ Wick Analysis*

#### *🔹 Wick Length Threshold (Ratio)*

- *Purpose:* Ensures rejection candles have *long wicks* (strong reversals).

- *Formula:* Wick Ratio = (Upper Wick + Lower Wick) / Candle Range

- *Example:*

- Threshold = 0.6 → 60% of the candle must be wicks.

#### *🔹 Min Wick Size (ATR %)*

- *Purpose:* Filters out small wicks in volatile markets.

- *Example:*

- ATR = 20 pips, MinWickSize = 1% → Wicks under *0.2 pips* are ignored.

---

### *5️⃣ ◆ Display Settings*

- *Show Zones:* Toggles support/resistance shaded areas.

- *Show Traps:* Highlights liquidity traps (▲/▼ symbols).

- *Show Tests:* Displays how many times levels were tested.

- *Zone Transparency:* Adjusts opacity of zones.

---

## *🎯 Practical Use Cases*

### *1️⃣ Liquidity Trap Detection*

- *Scenario:* Price spikes *above resistance* then reverses sharply.

- *Requirements:*

- Long wick (Wick Ratio > 0.6)

- High volume (Volume > Threshold)

- *Outcome:* *Short Trap* signal (▼) appears.

### *2️⃣ Strong Support Level*

- *Scenario:* Price bounces *3 times* from the same level.

- *Indicator Action:*

- Labels the level with test count (3/5 = 3 tests out of max 5).

- Turns *red* if broken (Break Count > 0).

Deep Dive: How This Indicator Works*

This indicator combines *four professional trading concepts* into one powerful tool:

1. *Classic Pivot Point Theory*

- Identifies swing highs/lows where price previously reversed

- Unlike basic pivot indicators, ours uses *confirmed pivots only* (filtered by ATR)

2. *Volume-Weighted Validation*

- Requires unusual trading volume to confirm levels

- Filters out "phantom" levels with low participation

3. *ATR Volatility Filtering*

- Eliminates insignificant price swings in choppy markets

- Ensures only meaningful levels are plotted

4. *Liquidity Trap Detection*

- Spots institutional stop hunts where markets fake out traders

- Uses wick analysis + volume spikes for high-probability signals

---

Deep Dive: How This Indicator Works*

This indicator combines *four professional trading concepts* into one powerful tool:

1. *Classic Pivot Point Theory*

- Identifies swing highs/lows where price previously reversed

- Unlike basic pivot indicators, ours uses *confirmed pivots only* (filtered by ATR)

2. *Volume-Weighted Validation*

- Requires unusual trading volume to confirm levels

- Filters out "phantom" levels with low participation

3. *ATR Volatility Filtering*

- Eliminates insignificant price swings in choppy markets

- Ensures only meaningful levels are plotted

4. *Liquidity Trap Detection*

- Spots institutional stop hunts where markets fake out traders

- Uses wick analysis + volume spikes for high-probability signals

---

## *📊 Parameter Encyclopedia (Expanded)*

### *1️⃣ Pivot Engine Settings*

#### *Pivot Length (50)*

- *What It Does:*

Determines how many bars to analyze when searching for swing highs/lows.

- *Professional Adjustment Guide:*

| Trading Style | Recommended Value | Why? |

|--------------|------------------|------|

| Scalping | 10-20 | Captures short-term levels |

| Day Trading | 30-50 | Balanced approach |

| Swing Trading| 50-200 | Focuses on major levels |

- *Real Market Example:*

On NASDAQ 5-minute chart:

- Length=20: Identifies levels holding for ~2 hours

- Length=50: Finds levels respected for entire trading day

#### *Test Threshold (5)*

- *Advanced Insight:*

Institutions often test levels 3-5 times before breaking them. This setting mimics the "probe and push" strategy used by smart money.

- *Psychology Behind It:*

Retail traders typically give up after 2-3 tests, while institutions keep testing until stops are run.

---

### *2️⃣ Volatility Filter System*

#### *ATR Multiplier (1.0)*

- *Professional Formula:*

Minimum Valid Swing = ATR(14) × Multiplier

- *Market-Specific Recommendations:*

| Market Type | Optimal Multiplier |

|------------------|--------------------|

| Forex Majors | 0.8-1.2 |

| Crypto (BTC/ETH) | 1.5-2.5 |

| SP500 Stocks | 1.0-1.5 |

- *Why It Matters:*

In EUR/USD (ATR=10 pips):

- Multiplier=1.0 → Requires 10 pip swings

- Multiplier=1.5 → Requires 15 pip swings (fewer but higher quality levels)

---

### *3️⃣ Volume Confirmation System*

#### *Volume Threshold (1.2)*

- *Institutional Benchmark:*

- 1.2x = Moderate institutional interest

- 1.5x+ = Strong smart money activity

- *Volume Spike Case Study:*

*Before Apple Earnings:*

- Normal volume: 2M shares

- Spike threshold (1.2): 2.4M shares

- Actual volume: 3.1M shares → STRONG confirmation

---

### *4️⃣ Liquidity Trap Detection*

#### *Wick Analysis System*

- *Two-Filter Verification:*

1. *Wick Ratio (0.6):*

- Ensures majority of candle shows rejection

- Formula: (UpperWick + LowerWick) / Total Range > 0.6

2. *Min Wick Size (1% ATR):*

- Prevents false signals in flat markets

- Example: ATR=20 pips → Min wick=0.2 pips

- *Trap Identification Flowchart:*

Price Enters Zone →

Spikes Beyond Level →

Shows Long Wick →

Volume > Threshold →

TRAP CONFIRMED

---

## *💡 Master-Level Usage Techniques*

### *Institutional Order Flow Analysis*

1. *Step 1:* Identify pivot levels with ≥3 tests

2. *Step 2:* Watch for volume contraction near levels

3. *Step 3:* Enter when trap signal appears with:

- Wick > 2×ATR

- Volume > 1.5× average

### *Multi-Timeframe Confirmation*

1. *Higher TF:* Find weekly/monthly pivots

2. *Lower TF:* Use this indicator for precise entries

3. *Example:*

- Weekly pivot at $180

- 4H shows liquidity trap → High-probability reversal

---

## *⚠ Critical Mistakes to Avoid*

1. *Using Default Settings Everywhere*

- Crude oil needs higher ATR multiplier than bonds

2. *Ignoring Trap Context*

- Traps work best at:

- All-time highs/lows

- Major psychological numbers (00/50 levels)

3. *Overlooking Cumulative Volume*

- Check if volume is building over multiple tests

Keltner Channel StrategyOverview

The Keltner Channel Strategy is a powerful trend-following and mean-reversion system that leverages the Keltner Channels, EMA crossovers, and ATR-based stop-losses to optimize trade entries and exits. This strategy has proven to be highly effective, particularly when applied to Gold (XAUUSD) and other commodities with strong trend characteristics.

📈 How It Works

This strategy incorporates two trading approaches: 1️⃣ Keltner Channel Reversal Trades – Identifies overbought and oversold conditions when price touches the outer bands.

2️⃣ Trend Following Trades – Uses the 9 EMA & 21 EMA crossover, with confirmation from the 50 EMA, to enter trades in the direction of the trend.

🔍 Entry & Exit Criteria

📊 Keltner Channel Entries (Reversal Strategy)

✅ Long Entry: When the price crosses below the lower Keltner Band (potential reversal).

✅ Short Entry: When the price crosses above the upper Keltner Band (potential reversal).

⏳ Exit Conditions:

Long positions close when price crosses back above the mid-band (EMA-based).

Short positions close when price crosses back below the mid-band (EMA-based).

📈 Trend Following Entries (Momentum Strategy)

✅ Long Entry: When the 9 EMA crosses above the 21 EMA, and price is above the 50 EMA (bullish momentum).

✅ Short Entry: When the 9 EMA crosses below the 21 EMA, and price is below the 50 EMA (bearish momentum).

⏳ Exit Conditions:

Long positions close when the 9 EMA crosses back below the 21 EMA.

Short positions close when the 9 EMA crosses back above the 21 EMA.

📌 Risk Management & Profit Targeting

ATR-based Stop-Losses:

Long trades: Stop set at 1.5x ATR below entry price.

Short trades: Stop set at 1.5x ATR above entry price.

Take-Profit Levels:

Long trades: Profit target 2x ATR above entry price.

Short trades: Profit target 2x ATR below entry price.

🚀 Why Use This Strategy?

✅ Works exceptionally well on Gold (XAUUSD) due to high volatility.

✅ Combines reversal & trend strategies for improved adaptability.

✅ Uses ATR-based risk management for dynamic position sizing.

✅ Fully automated alerts for trade entries and exits.

🔔 Alerts

This script includes automated TradingView alerts for:

🔹 Keltner Band touches (Reversal signals).

🔹 EMA crossovers (Momentum trades).

🔹 Stop-loss & Take-profit activations.

📊 Ideal Markets & Timeframes

Best for: Gold (XAUUSD), NASDAQ (NQ), Crude Oil (CL), and trending assets.

Recommended Timeframes: 15m, 1H, 4H, Daily.

⚡️ How to Use

1️⃣ Add this script to your TradingView chart.

2️⃣ Select a 15m, 1H, or 4H timeframe for optimal results.

3️⃣ Enable alerts to receive trade notifications in real time.

4️⃣ Backtest and tweak ATR settings to fit your trading style.

🚀 Optimize your Gold trading with this Keltner Channel Strategy! Let me know how it performs for you. 💰📊

Market Structure Break with Volume & ATR#### Indicator Overview:

The *Market Structure Break with Volume & ATR (MSB+VolATR)* indicator is designed to identify significant market structure breakouts and breakdowns using a combination of price action, volume analysis, and volatility (ATR). It is particularly useful for traders who rely on higher timeframes for swing trading or positional trading. The indicator highlights bullish and bearish breakouts, retests, fakeouts, and potential buy/sell signals based on RSI overbought/oversold conditions.

---

### Key Features:

1. *Market Structure Analysis*:

- Identifies swing highs and lows on a user-defined higher timeframe.

- Detects breakouts and breakdowns when price exceeds these levels with volume and ATR validation.

2. *Volume Validation*:

- Ensures breakouts are accompanied by above-average volume, reducing the likelihood of false signals.

3. *ATR Filter*:

- Filters out insignificant breakouts by requiring the breakout size to exceed a multiple of the ATR.

4. *RSI Integration*:

- Adds a momentum filter by considering overbought/oversold conditions using RSI.

5. *Visual Enhancements*:

- Draws colored boxes to highlight breakout zones.

- Labels breakouts, retests, and fakeouts for easy interpretation.

- Displays stop levels for potential trades.

6. *Alerts*:

- Provides alert conditions for buy and sell signals, enabling real-time notifications.

---

### Input Settings and Their Effects:

1. **Timeframe (tf):

- Determines the higher timeframe for market structure analysis.

- *Effect*: A higher timeframe (e.g., 1D) reduces noise and provides more reliable swing points, while a lower timeframe (e.g., 4H) may generate more frequent but less reliable signals.

2. **Lookback Period (length):

- Defines the number of historical bars used to identify significant highs and lows.

- *Effect*: A longer lookback period (e.g., 50) captures broader market structure, while a shorter period (e.g., 20) reacts faster to recent price action.

3. **ATR Length (atr_length):

- Sets the period for ATR calculation.

- *Effect*: A shorter ATR length (e.g., 14) reacts faster to recent volatility, while a longer length (e.g., 21) smooths out volatility spikes.

4. **ATR Multiplier (atr_multiplier):

- Filters insignificant breakouts by requiring the breakout size to exceed ATR × multiplier.

- *Effect*: A higher multiplier (e.g., 0.2) reduces false signals but may miss smaller breakouts.

5. **Volume Multiplier (volume_multiplier):

- Sets the volume threshold for breakout validation.

- *Effect*: A higher multiplier (e.g., 1.0) ensures stronger volume confirmation but may reduce the number of signals.

6. **RSI Length (rsi_length):

- Defines the period for RSI calculation.

- *Effect*: A shorter RSI length (e.g., 10) makes the indicator more sensitive to recent price changes, while a longer length (e.g., 20) smooths out RSI fluctuations.

7. *RSI Overbought/Oversold Levels*:

- Sets the thresholds for overbought (default: 70) and oversold (default: 30) conditions.

- *Effect*: Adjusting these levels can make the indicator more or less conservative in generating signals.

8. **Stop Loss Multiplier (SL_Multiplier):

- Determines the distance of the stop-loss level from the entry price based on ATR.

- *Effect*: A higher multiplier (e.g., 2.0) provides wider stops, reducing the risk of being stopped out prematurely but increasing potential losses.

---

### How It Works:

1. *Breakout Detection*:

- A bullish breakout occurs when the close exceeds the highest high of the lookback period, with volume above the threshold and breakout size exceeding ATR × multiplier.

- A bearish breakout occurs when the close falls below the lowest low of the lookback period, with similar volume and ATR validation.

2. *Retest Logic*:

- After a breakout, if price retests the breakout zone without closing beyond it, a retest label is displayed.

3. *Fakeout Detection*:

- If price briefly breaks out but reverses back into the range, a fakeout label is displayed.

4. *Buy/Sell Signals*:

- A sell signal is generated when price reverses below a bullish breakout zone and RSI is overbought.

- A buy signal is generated when price reverses above a bearish breakout zone and RSI is oversold.

5. *Stop Levels*:

- Stop-loss levels are plotted based on ATR × SL_Multiplier, providing a visual guide for risk management.

---

### Who Can Use It and How:

1. *Swing Traders*:

- Use the indicator on daily or 4-hour timeframes to identify high-probability breakout trades.

- Combine with other technical analysis tools (e.g., trendlines, Fibonacci levels) for confirmation.

2. *Positional Traders*:

- Apply the indicator on weekly or daily charts to capture long-term trends.

- Use the stop-loss levels to manage risk over extended periods.

3. *Algorithmic Traders*:

- Integrate the buy/sell signals into automated trading systems.

- Use the alert conditions to trigger trades programmatically.

4. *Risk-Averse Traders*:

- Adjust the ATR and volume multipliers to filter out low-probability trades.

- Use wider stop-loss levels to avoid premature exits.

---

### Where to Use It:

- *Forex*: Identify breakouts in major currency pairs.

- *Stocks*: Spot trend reversals in high-volume stocks.

- *Commodities*: Trade breakouts in gold, oil, or other commodities.

- *Crypto*: Apply to Bitcoin, Ethereum, or other cryptocurrencies for volatile breakout opportunities.

---

### Example Use Case:

- *Timeframe*: 1D

- *Lookback Period*: 50

- *ATR Length*: 14

- *ATR Multiplier*: 0.1

- *Volume Multiplier*: 0.5

- *RSI Length*: 14

- *RSI Overbought/Oversold*: 70/30

- *SL Multiplier*: 1.5

In this setup, the indicator will:

1. Identify significant swing highs and lows on the daily chart.

2. Validate breakouts with volume and ATR filters.

3. Generate buy/sell signals when price reverses and RSI confirms overbought/oversold conditions.

4. Plot stop-loss levels for risk management.

---

### Conclusion:

The *MSB+VolATR* indicator is a versatile tool for traders seeking to capitalize on market structure breakouts with added confirmation from volume and volatility. By customizing the input settings, traders can adapt the indicator to their preferred trading style and risk tolerance. Whether you're a swing trader, positional trader, or algorithmic trader, this indicator provides actionable insights to enhance your trading strategy.

The Investment Clock Orbital GraphThe Investment Clock Orbital Graph is an advanced visualization tool designed to help traders and investors track economic cycles using a dynamic scatter plot of GDP growth vs. CPI inflation rates.

This indicator is a fusion of two powerful TradingView indicators:

LuxAlgo ’s Relative Strength Scatter Plot – A robust scatter plot for tracking relative strength.

The Investment Clock Indicator – A cycle-based approach to market rotation. This indicator contains more information regarding The Investment Clock.

By combining these approaches, the Investment Clock Orbital Graph enables traders to visualize economic momentum and inflationary trends in a unique, orbital-style scatter plot.

Key Features & Improvements

Orbital Graph Representation – Displays GDP growth and CPI inflation as a dynamic, evolving scatter plot, showing how the economy moves through different phases.

Quadrant-Based Market Regimes – Identifies four key economic phases:

1)🔥 Overheating (High Growth, High Inflation)

2)📉 Stagflation (Low Growth, High Inflation)

3)🤒 Recovery (High Growth, Low Inflation)

4)🎈 Reflation (Low Growth, Low Inflation)

Data-Driven Analysis – Utilizes FRED (Federal Reserve Economic Data) for accurate real-world GDP & CPI data.

Trailing Path of Economic Evolution – Tracks historical economic cycles over time to show momentum and cyclical movements.

Customizable Parameters – Set sustainable GDP growth and inflation thresholds, adjust trail length, and fine-tune scatter plot resolution.

Auto-Labeled Quadrants & Revised Accurate Market Guidance – Each quadrant includes newly updated tooltips and annotations (like ETF suggestions) to help traders make informed decisions.

Live Macro Forecasting Tool – Helps traders anticipate future market conditions, rate hikes/cuts, and sector rotations.

How to Use for Trading Decisions

The Investment Clock Orbital Graph helps traders and macro investors by identifying market phases and providing insights into asset class performance during different economic conditions.

📌 Step 1: Identify the Current Quadrant

Locate the most recent point on the orbital graph to see if the economy is in Overheating, Stagflation, Recovery, or Reflation.

📌 Step 2: Forecast Market Trends

The trajectory of the points can predict upcoming economic shifts:

Overheating → Stagflation ➡️ Expect economic slowdowns, bearish stock markets.

Stagflation → Reflation ➡️ Interest rate cuts likely, bonds and defensive stocks perform well.

Reflation → Recovery ➡️ Risk-on rally, technology and cyclicals perform best.

Recovery → Overheating ➡️ Commodities surge, inflation rises, and central banks intervene.

📌 Step 3: Align Trading & Investing Strategies

🔥 Overheating – Favor commodities & energy (Oil, Industrial Stocks, Materials).

📉 Stagflation – Favor defensive assets (Cash, Utilities, Healthcare).

🤒 Recovery – Favor growth stocks (Technology, Consumer Discretionary).

🎈 Reflation – Favor bonds, value stocks, and financials.

📌 Step 4: Monitor Trends Over Time

The indicator visualizes economic movement over multiple months, allowing traders to confirm long-term trends vs. short-term noise.

The Investment Clock Orbital Graph is an essential macro trading tool, providing a real-time visualization of economic conditions. By tracking GDP growth vs. CPI inflation, traders and investors can align their portfolios with major macroeconomic shifts, predict sector rotations, and anticipate central bank policy changes.

Market Crashes & Recessions (1907-Present)Included Recession Periods:

Panic of 1907 (1907–1908)

Post-WWI Recession (1918–1919)

Great Depression (1929–1933)

1937–1938 Recession

1953, 1957, & 1973 Oil Crises Recessions

Early 1980s Recession (1980–1982)

Early 1990s Recession (1990–1991)

Dot-com Bubble (2000–2002)

Global Financial Crisis (2007–2009)

COVID-19 Recession (2020)

2022 Market Correction

Casa_SessionsLibrary "Casa_Sessions"

Advanced trading session management library that enhances TradingView's default functionality:

Key Features:

- Accurate session detection for futures markets

- Custom session hour definitions

- Drop-in replacements for standard TradingView session functions

- Flexible session map customization

- Full control over trading windows and market hours

Perfect for traders who need precise session timing, especially when working

with futures markets or custom trading schedules.

SetSessionTimes(session_type_input, custom_session_times_input, syminfo_type, syminfo_root, syminfo_timezone)

Parameters:

session_type_input (simple string) : Input string for session selection:

- 'Custom': User-defined session times

- 'FX-Tokyo': Tokyo forex session

- 'FX-London': London forex session

- 'FX-New York': NY forex session

- 'Overnight Session (ON)': After-hours trading

- 'Day Session (RTH)': Regular trading hours

custom_session_times_input (simple string) : Session parameter for custom time windows

Only used when session_type_input is 'Custom'

syminfo_type (simple string)

syminfo_root (simple string)

syminfo_timezone (simple string)

Returns:

session_times: Trading hours for selected session

session_timezone: Market timezone (relevant for forex)

getSessionMap()

Get futures trading session hours map

Keys are formatted as 'symbol:session', examples:

- 'ES:market' - Regular trading hours (RTH)

- 'ES:overnight' - Extended trading hours (ETH)

- 'NQ:market' - NASDAQ futures RTH

- 'CL:overnight' - Crude Oil futures ETH

Returns: Map

Key: Symbol:session identifier

Value: Session hours in format "HH:MM-HH:MM"

getSessionString(session, symbol, sessionMap)

Returns a session string representing the session hours (and days) for the requested symbol (or the chart's symbol if the symbol value is not provided). If the session string is not found in the collection, it will return a blank string.

Parameters:

session (string) : A string representing the session hour being requested. One of: market (regular trading hours), overnight (extended/electronic trading hours), postmarket (after-hours), premarket

symbol (string) : The symbol to check. Optional. Defaults to chart symbol.

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

inSession(session, sessionMap, barsBack)

Returns true if the current symbol is currently in the session parameters defined by sessionString.

Parameters:

session (string) : A string representing the session hour being requested. One of: market (regular trading hours), overnight (extended/electronic trading hours), postmarket (after-hours), premarket

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

barsBack (int) : Private. Only used by futures to check islastbar. Optional. The default is 0.

ismarket(sessionMap)

Returns true if the current bar is a part of the regular trading hours (i.e. market hours), false otherwise. Works for futures (TradingView's methods do not).

Parameters:

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: bool

isfirstbar()

Returns true if the current bar is the first bar of the day's session, false otherwise. If extended session information is used, only returns true on the first bar of the pre-market bars. Works for futures (TradingView's methods do not).

Returns: bool

islastbar()

Returns true if the current bar is the last bar of the day's session, false otherwise. If extended session information is used, only returns true on the last bar of the post-market bars. Works for futures (TradingView's methods do not).

Returns: bool

ispremarket(sessionMap)

Returns true if the current bar is a part of the pre-market, false otherwise. On non-intraday charts always returns false. Works for futures (TradingView's methods do not).

Parameters:

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: bool

ispostmarket(sessionMap)

Returns true if the current bar is a part of the post-market, false otherwise. On non-intraday charts always returns false. Works for futures (TradingView's methods do not).

Parameters:

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: bool

isfirstbar_regular(sessionMap)

Returns true on the first regular session bar of the day, false otherwise. The result is the same whether extended session information is used or not. Works for futures (TradingView's methods do not).

Parameters:

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: bool

islastbar_regular(sessionMap)

Returns true on the last regular session bar of the day, false otherwise. The result is the same whether extended session information is used or not. Works for futures (TradingView's methods do not).

Parameters:

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: bool

isovernight(sessionMap)

Returns true if the current bar is a part of the pre-market or post-market, false otherwise. On non-intraday charts always returns false.

Parameters:

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: bool

getSessionHighAndLow(session, sessionMap)

Returns a tuple containing the high and low print during the specified session.

Parameters:

session (string) : The session for which to get the high & low prints. Defaults to market.

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: A tuple containing

getSessionHigh(session, sessionMap)

Convenience function to return the session high. Necessary if you want to call this function from within a request.security expression where you can't return a tuple.

Parameters:

session (string) : The session for which to get the high & low prints. Defaults to market.

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: The high of the session

getSessionLow(session, sessionMap)

Convenience function to return the session low. Necessary if you want to call this function from within a request.security expression where you can't return a tuple.

Parameters:

session (string) : The session for which to get the high & low prints. Defaults to market.

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: The low of the session

Celestial Pair Spread Hello friends, after a very long time!

Today, I tried to put into code an idea that came to my mind spontaneously and suddenly.

Note :

This script is experimental and improvable.

I haven't had a chance to try it yet.

TIMEFRAME : 1D (Daily Bars)

CELESTIAL SPREAD

The spread moves in a very limited area and is consistent within itself, especially on days far from the end of the contract.

That's why there is a reassuring sky atmosphere. That's why this name was given completely improvised.

Basic logic of the script

We enter the name of the CME Futures contract we want to enter:

Ex : CL1! , ES1! , ZC1! , NQ1!

The script creates us a pair trade parity divided into secondary contracts.

Example : ES1!/ES2!

What is pair trading?

I will explain briefly here.

For users who are wondering:

www.investopedia.com

Let's get back to our topic.

Now we have created a parity that does not actually exist.

This parity is the manifestation of the relative movements of two contracts.

When the parity rises, ES1! increased,ES2! has fallen.

In the opposite case, We can say: ES1! Contract has been dropped ES2! has increased.

Pair trading is generally a trade that needs to be kept in mind from time to time.

It is a method preferred by professionals who can process very quickly.

Market risk is minimal, but since 2 contracts are purchased, more money is paid and very low percentage profits are made.

It is very expensive to do pair trading, especially with oil and its derivatives and interest security derivatives.

The contract we are considering has micros. (small-item contracts tied to the same value)

So when we switch to our broker MES1!/MES2! We will trade.

For all CME futures :

www.cmegroup.com

Anyway, let's continue:

The script created the parity showing its relationship with the next contract and plotted it as bars.

Celestial bands are just like Bollinger bands, but they consist of 3 bands based on percentage changes rather than standard deviation.

The middle band is obtained from moving averages.

The upper and lower bands are the middle band subjected to a threshold value.

The threshold value can be changed.

0.15 percent was charged for this script.

CAUTION :

As can be seen in the example below;

The most important thing is not to make any transactions when the contract switch dates are approaching.

Therefore, it is recommended to use it just below the main chart.

The blue bars in the parity are

Values that outside the upper and lower threshold values are colored blue.

For this condition

Alerts has been added.

Don't forget to add alert and edit.

MAIN PURPOSE

It is aimed to start a pair trade when such conditions come and to quickly close the trades when the parity basis reaches the value.

OTHER IMPORTANT POINTS

Other issues are broker related issues.

Difference between initial margins and maintanence margins of contracts (between 1! and 2!)

It shouldn't be too high.

The commission should not be too high.

Leverage must be high because the profit percentage is very low.

To calculate leverage you must divide your contract size by the relevant margin requirement.

Sample margin requirement table:

www.interactivebrokers.com

RISKS

It is an experimental and intellectual script,

the risk of contract price differences (maybe it will not leave a profit except for very extreme values)

I remind you of the quickness risk that comes from a two-legged trade.

Alerts definitely synchronized with an audible alert sent to a smartphone as an e-mail notification and displayed on the locked screen for quick action.

Best regards!

Excess Liquidity IndicatorExcess Liquidity Indicator

This script visualizes excess liquidity trends in relation to risk assets. It estimates excess liquidity by combining various macroeconomic factors such as WW M2 money supply, central bank balance sheets, and interest rates, oil, and the dollar index, and it substracts WW GDP. The tool helps traders analyze liquidity-driven market trends in a structured manner.

Note: This script is for research purposes only and does not provide financial advice.

I cannot point names cause I get banned but work is inspired by others...

Doji Double Top & Double Bottom

FUNCTION :

This indicator checks if 2 consecutive candlesticks are formed in such a way that both the lows or both the highs of the consecutive candlesticks are almost at the same level and either of them is a doji

TIMEFRAMES :

it works on daily, weekly, monthly and higher timeframes

CRITERIA :

There is maximum difference value between 2 consecutive candlesticks' lows or 2 consecutive candlesticks' highs

Minimum value of the doji's wick size

Maximum value of the doji's body size

These 3 conditions need to be fulfilled for the 2 consecutive candlesticks to be considered as a Double top or Double bottom by this indicator

EXAMPLES :

Here the indicator is giving only double Bottom signals on CRUDE OIL chart

Here the indicator is giving only double top signals on GOLD chart

Here the indicator gives both double top & double bottom signals on EUR/USD Daily chart

Here the indicator is giving both double top & double bottom signals on EUR/USD Half-Yearly chart

DEFINITIONS :

There are 2 types -

DOJI DOUBLE BOTTOM - if the lows of 2 consecutive candlesticks are almost at the same level & either of them is doji then it is called Double Bottom and market is supposed to go higher after forming it.

DOJI DOUBLE TOP - if the highs of 2 consecutive candlesticks are almost at the same level & either of them is doji then it is called Double Top and market is supposed to go lower after forming it.

SETTINGS :

There are options to change the value of each of the 3 parameters within the indicator's settings for daily, weekly & monthly chart [

LIMITATIONS :

You should not trade based on the signals from this indicator solely, you should check other parameters too before making trading decision

MATA GOLD RATIOMata Gold Instrument: User Guide

The Instrument to Gold Oscillator is a technical analysis tool that normalizes the ratio of an instrument's price (e.g., BTC/USD) to the price of gold (XAU/USD) into a 0-100 scale. This provides a clear and intuitive way to evaluate the relative performance of an instrument compared to gold over a specified period.

---

How It Works

1. Calculation of the Ratio:

The ratio is calculated as:

\text{Ratio} = \frac{\text{Instrument Price}}{\text{Gold Price}}

2. Normalization:

The ratio is normalized using the highest and lowest values over a user-defined period (length), typically 14 periods:

\text{Normalized Ratio} = \frac{\text{Ratio} - \text{Min(Ratio)}}{\text{Max(Ratio)} - \text{Min(Ratio)}} \times 100

3. Overbought/Oversold Levels:

Above 80: The instrument is relatively expensive compared to gold (overbought).

Below 20: The instrument is relatively cheap compared to gold (oversold).

---

How to Use the Oscillator

1. Identify Overbought and Oversold Levels:

If the oscillator rises above 80, the instrument may be overvalued relative to gold. This could signal a potential reversal or correction.

If the oscillator falls below 20, the instrument may be undervalued relative to gold. This could signal a buying opportunity.

2. Track Trends:

Rising oscillator values indicate the instrument is gaining value relative to gold.

Falling oscillator values indicate the instrument is losing value relative to gold.

3. Crossing the Midline (50):

When the oscillator crosses above 50, the instrument's value is gaining strength relative to gold.

When it crosses below 50, the instrument is weakening relative to gold.

4. Combine with Other Indicators:

Use this oscillator alongside other technical indicators (e.g., RSI, MACD, STOCH) for more robust decision-making.

Confirm signals from the oscillator with price action or volume analysis.

---

Example Scenarios

1. Trading Cryptocurrencies Against Gold:

If BTC/USD's oscillator value is above 80, Bitcoin may be overvalued relative to gold. Consider reducing exposure or looking for short opportunities.

If BTC/USD's oscillator value is below 20, Bitcoin may be undervalued relative to gold. This could be a good time to accumulate.

2. Commodities vs. Gold:

Analyze the relative strength of commodities (e.g., oil, silver) against gold using the oscillator to identify periods of overperformance or underperformance.

---

Advantages of the Oscillator

Relative Performance Insight: Tracks the performance of an instrument relative to gold, providing a macro perspective.

Clear Visual Representation: The 0-100 scale makes it easy to identify overbought/oversold conditions and trend shifts.

Customizable Periods: The user-defined length allows flexibility in analyzing short- or long-term trends.

---

Limitations

Dependence on Gold: As the oscillator is based on gold prices, any external shocks to gold (e.g., geopolitical events) can influence its signals.

No Absolute Buy/Sell Signals: The oscillator should not be used in isolation but as part of a broader analysis strategy.

---

By using the Instrument to Gold Oscillator effectively, traders and investors can gain valuable insights into the relative valuation and performance of assets compared to gold, enabling more informed trading and investment decisions.

Previous High and Low Count with Probabilities + Risk On/Off1. Purpose of the Script:

This trading script combines two important concepts:

Previous High and Low Count: It tracks whether the current price exceeds the previous day’s high or low and calculates probabilities for the next price movement (up or down).

Risk On / Risk Off Indicator: It evaluates market sentiment through various indicators (such as the Fear & Greed Index, VIX, and others) and shows whether the market is in a risk-on or risk-off state. This information impacts the probabilities of price movement.

2. How it Works:

Previous High and Low:

The script tracks how often the price exceeds the previous day’s high or low and calculates the probability of an upward or downward movement based on that. This gives you an idea of how often the market reacts at the previous day's high or low.

Risk On / Risk Off:

Based on various market factors (Fear & Greed Index, VIX, Put-Call Ratio, etc.), the script calculates the Risk On or Risk Off state.

In Risk On, the probability of an upward movement increases, and the probability of a downward movement decreases. In Risk Off, it’s the opposite.

Adjusted Probabilities:

The probabilities for an Up or Down movement are adjusted based on the current Risk On / Risk Off state. In a Risk On environment, the probability for an upward move increases, while in a Risk Off environment, the probability for a downward move increases.

3. How to Use the Script:

Add the Script in TradingView:

TradingView:

Click on "Add to Chart" to apply the script to your chart.

Manual Input of Indicators:

For the Fear & Greed Index, VIX, and other indicators, you need to manually enter the current values. You can get these values from various publicly available sources:

Fear & Greed Index: CNN Fear & Greed Index

VIX (Volatility Index): VIX Index

Other indicators like Put-Call Ratio, Bitcoin Volatility, Oil Prices, and US Dollar Index can also be manually inputted, and they can be found on finance websites like Yahoo Finance, MarketWatch, and Bloomberg.

Observe the Colors and Symbols:

If the market is in a Risk On state, the background will turn green, and a green triangle will appear below the candle.

If the market is in a Risk Off state, the background will turn red, and a red triangle will appear above the candle.

Track the Probabilities:

A label will appear on the chart showing the calculated probabilities for Up and Down movements. These probabilities are adjusted based on the current market state (Risk On/Off).

4. Meaning of the Probabilities:

Up Probability: Indicates the probability that the price will rise.

Down Probability: Indicates the probability that the price will fall.

The probabilities are dynamic and adjust based on the Risk On / Risk Off state, helping you make better decisions based on the current market conditions.

Performance Summary and Shading (Offset Version)Modified "Recession and Crisis Shading" Indicator by @haribotagada (Original Link: )

The updated indicator accepts a days offset (positive or negative) to calculate performance between the offset date and the input date.

Potential uses include identifying performance one week after company earnings or an FOMC meeting.

This feature simplifies input by enabling standardized offset dates, while still allowing flexibility to adjust ranges by overriding inputs as needed.

Summary of added features and indicator notes:

Inputs both positive and negative offset.

By default, the script calculates performance from the close of the input date to the close of the date at (input date + offset) for positive offsets, and from the close of (input date - offset) to the close of the input date for negative offsets. For example, with an input date of November 1, 2024, an offset of 7 calculates performance from the close on November 1 to the close on November 8, while an offset of -7 calculates from the close on October 25 to the close on November 1.

Allows user to perform the calculation using the open price on the input date instead of close price

The input format has been modified to allow overrides for the default duration, while retaining the original capabilities of the indicator.

The calculation shows both the average change and the average annualized change. For bar-wise calculations, annualization assumes 252 trading days per year. For date-wise calculations, it assumes 365 days for annualization.

Carries over all previous inputs to retain functionality of the previous script. Changes a few small settings:

Calculates start to end date performance by default instead of peak to trough performance.

Updates visuals of label text to make it easier to read and less transparent.

Changed stat box color scheme to make the text easier to read

Updated default input data to new format of input with offsets

Changed default duration statistic to number of days instead of number of bars with an option to select number of bars.

Potential Features to Add:

Import dataset from CSV files or by plugging into TradingView calendar

Example Input Datasets:

Recessions:

2020-02-01,COVID-19,59

2007-12-01,Subprime mortgages,547

2001-03-01,Dot-com,243

1990-07-01,Oil shock,243

1981-07-01,US unemployment,788

1980-01-01,Volker,182

1973-11-01,OPEC,485

Japan Revolving Door Elections

2006-09-26, Shinzo Abe

2007-09-26, Yasuo Fukuda

2008-09-24, Taro Aso

2009-09-16, Yukio Hatoyama

2010-07-08, Naoto Kan

2011-09-02, Yoshihiko Noda

Hope you find the modified indicator useful and let me know if you would like any features to be added!

Futures Beta Overview with Different BenchmarksBeta Trading and Its Implementation with Futures

Understanding Beta

Beta is a measure of a security's volatility in relation to the overall market. It represents the sensitivity of the asset's returns to movements in the market, typically benchmarked against an index like the S&P 500. A beta of 1 indicates that the asset moves in line with the market, while a beta greater than 1 suggests higher volatility and potential risk, and a beta less than 1 indicates lower volatility.

The Beta Trading Strategy

Beta trading involves creating positions that exploit the discrepancies between the theoretical (or expected) beta of an asset and its actual market performance. The strategy often includes:

Long Positions on High Beta Assets: Investors might take long positions in assets with high beta when they expect market conditions to improve, as these assets have the potential to generate higher returns.

Short Positions on Low Beta Assets: Conversely, shorting low beta assets can be a strategy when the market is expected to decline, as these assets tend to perform better in down markets compared to high beta assets.

Betting Against (Bad) Beta

The paper "Betting Against Beta" by Frazzini and Pedersen (2014) provides insights into a trading strategy that involves betting against high beta stocks in favor of low beta stocks. The authors argue that high beta stocks do not provide the expected return premium over time, and that low beta stocks can yield higher risk-adjusted returns.

Key Points from the Paper:

Risk Premium: The authors assert that investors irrationally demand a higher risk premium for holding high beta stocks, leading to an overpricing of these assets. Conversely, low beta stocks are often undervalued.

Empirical Evidence: The paper presents empirical evidence showing that portfolios of low beta stocks outperform portfolios of high beta stocks over long periods. The performance difference is attributed to the irrational behavior of investors who overvalue riskier assets.

Market Conditions: The paper suggests that the underperformance of high beta stocks is particularly pronounced during market downturns, making low beta stocks a more attractive investment during volatile periods.

Implementation of the Strategy with Futures

Futures contracts can be used to implement the betting against beta strategy due to their ability to provide leveraged exposure to various asset classes. Here’s how the strategy can be executed using futures:

Identify High and Low Beta Futures: The first step involves identifying futures contracts that have high beta characteristics (more sensitive to market movements) and those with low beta characteristics (less sensitive). For example, commodity futures like crude oil or agricultural products might exhibit high beta due to their price volatility, while Treasury bond futures might show lower beta.

Construct a Portfolio: Investors can construct a portfolio that goes long on low beta futures and short on high beta futures. This can involve trading contracts on stock indices for high beta stocks and bonds for low beta exposures.

Leverage and Risk Management: Futures allow for leverage, which means that a small movement in the underlying asset can lead to significant gains or losses. Proper risk management is essential, using stop-loss orders and position sizing to mitigate the inherent risks associated with leveraged trading.

Adjusting Positions: The positions may need to be adjusted based on market conditions and the ongoing performance of the futures contracts. Continuous monitoring and rebalancing of the portfolio are essential to maintain the desired risk profile.

Performance Evaluation: Finally, investors should regularly evaluate the performance of the portfolio to ensure it aligns with the expected outcomes of the betting against beta strategy. Metrics like the Sharpe ratio can be used to assess the risk-adjusted returns of the portfolio.

Conclusion

Beta trading, particularly the strategy of betting against high beta assets, presents a compelling approach to capitalizing on market inefficiencies. The research by Frazzini and Pedersen emphasizes the benefits of focusing on low beta assets, which can yield more favorable risk-adjusted returns over time. When implemented using futures, this strategy can provide a flexible and efficient means to execute trades while managing risks effectively.

References

Frazzini, A., & Pedersen, L. H. (2014). Betting against beta. Journal of Financial Economics, 111(1), 1-25.

Fama, E. F., & French, K. R. (1992). The cross-section of expected stock returns. Journal of Finance, 47(2), 427-465.

Black, F. (1972). Capital Market Equilibrium with Restricted Borrowing. Journal of Business, 45(3), 444-454.

Ang, A., & Chen, J. (2010). Asymmetric volatility: Evidence from the stock and bond markets. Journal of Financial Economics, 99(1), 60-80.

By utilizing the insights from academic literature and implementing a disciplined trading strategy, investors can effectively navigate the complexities of beta trading in the futures market.

Futures Daily Settlement PricesDaily settlement prices reflect the fair market value of the underlying commodity or financial instrument, as determined by buyers and sellers during the settlement period or “close”. The price quoted in the evening news for items like a bush of corn, a barrel of crude oil, or a 10-year U.S. Treasury note frequently use the settlement price for the corresponding futures product that day.

Settlement prices are used to mark traders’ positions to market daily, determining profits or losses. Daily settlement prices play a key role in facilitating price discovery, risk management, and market integrity.

This indicator plots up to 30 settlement prices as well as the date of settlement on your chart, on time frames under 1 hour.

Customizable line types, colors, and label colors.