Options Volume Indicator

Volume Indicator for Option Trading, it is a simple indicator based on Relative Strength Index. There are two horizontal lines are mention 10 and -10, if bar crossed above the (Line 10) then go for buy and when Bar cross under (Line -10) go for sell side.

If Bar Color changed to Respective color of the previous bar i.e. color gets darker then you can exit/ trail SL there because it overbought / Oversold position and vice versa for Sell Side.

this volume indicator works on any Script.

The Black Floating Line indicates the Average volume

Wyszukaj w skryptach "10年期国债收益率+曲线图+数据来源"

Estrategia Larry Connors [JoseMetal]============

ENGLISH

============

- Description:

This strategy is based on the original Larry Connors strategy, using 2 SMAs and RSI.

The strategy has been optimized for better total profit and works better on 4H (tested on BTCUSDT).

LONG:

Price must be ABOVE the slow SMA.

When a candle closes in RSI oversold area, the next candle closes out of the oversold area and the closing price is BELOW the fast SMA = open LONG.

LONG is closed when a candle closes ABOVE the fast SMA.

SHORT:

Price must be BELOW the slow SMA.

When a candle closes in RSI overbought area, the next candle closes out of the overbought area and the closing price is ABOVE the fast SMA = open SHORT.

SHORT is closed when a candle closes BELOW the fast SMA.

*Larry Connor's strategy does NOT use a fixed Stop Loss or Take Profit, as he said, that reduces performance significantly.

- Visual:

Both SMAs (fast and slow) are shown in the chart.

By default, the fast SMA is aqua color, the slow changes between green and red depending on the "trend" (price over slow SMA = bullish, below = bearish).

RSI can't be shown because TradingView doesn't allow to show both overlay and panel indicators, so candles get a RED color when RSI is in OVERBOUGHT area and GREEN when they're on OVERSOLD area to help with that.

Background is colored when conditions are met and a position is going to be open, green for LONGs red for SHORTs.

- Usage and recommendations:

As this is a coded strategy, you don't even have to check for indicators, just open and close trades as the strategy shows.

The original strategy uses a 5 period SMA instead of the 10, and 10/90 for oversold/overbought levels, this has been optimized after the testings and results but feel free to change settings and test by yourself.

Also, the original strategy was developed for daily, but seems to work better en 4H.

- Customization:

As usual I like to make as many aspects of my indicators/strategies customizable, indicators, colors etc., feel free to ask if you feel that something that should be configurable is missing or if you have any ideas to optimize the strategy.

============

ESPAÑOL

============

- Descripción:

Esta estrategia está basada en la estrategia original de Larry Connors, utilizando 2 SMAs y RSI.

La estrategia ha sido optimizada para un mejor beneficio total y funciona mejor en 4H (probado en BTCUSDT).

LONG:

El precio debe estar por encima de la SMA lenta.

Cuando una vela cierra en la zona de sobreventa del RSI, la siguiente vela cierra fuera de la zona de sobreventa y el precio de cierre está POR DEBAJO de la SMA rápida = abre LONG.

Se cierra cuando una vela cierra POR ENCIMA de la SMA rápida.

SHORT:

El precio debe estar POR DEBAJO de la SMA lenta.

Cuando una vela cierra en la zona de sobrecompra del RSI, la siguiente vela cierra fuera de la zona de sobrecompra y el precio de cierre está POR ENCIMA de la SMA rápida = abre SHORT.

Se cierra cuando una vela cierra POR DEBAJO de la SMA rápida.

*La estrategia de Larry Connor NO utiliza un Stop Loss o Take Profit fijo, como él dijo, eso reduce el rendimiento significativamente.

- Visual:

Ambas SMAs (rápida y lenta) se muestran en el gráfico.

Por defecto, la SMA rápida es de color aqua, la lenta cambia entre verde y rojo dependiendo de la "tendencia" (precio por encima de la SMA lenta = alcista, por debajo = bajista).

El RSI no puede mostrarse porque TradingView no permite mostrar tanto los indicadores superpuestos como los del panel, así que las velas obtienen un color ROJO cuando el RSI está en el área de SOBRECOMPRA y VERDE cuando están en el área de VENTA para ayudar a ello.

El fondo se colorea cuando se cumplen las condiciones y se va a abrir una posición, verde para LONGs rojo para SHORTs.

- Uso y recomendaciones:

Como se trata de una estrategia ya programada, ni siquiera hay que comprobar los indicadores, sólo hay que abrir y cerrar las operaciones tal y como muestra la estrategia en el gráfico.

La estrategia original utiliza una SMA de 5 periodos en lugar de 10, y 10/90 para los niveles de sobreventa/sobrecompra, esto ha sido optimizado después de las pruebas y los resultados, pero sé libre de cambiar la configuración y probarla por sí mismo.

Además, la estrategia original fue desarrollada para diario, pero parece funcionar mejor en 4H.

- Personalización:

Como siempre me gusta hacer personalizables todos los aspectos de mis indicadores/estrategias, indicadores, colores, etc., preguntar si notas que falta algo que debería ser configurable o si tienes alguna idea para optimizar la estrategia.

Library CommonLibrary "LibraryCommon"

A collection of custom tools & utility functions commonly used with my scripts

@description TODO: add library description here

getDecimals() Calculates how many decimals are on the quote price of the current market

Returns: The current decimal places on the market quote price

truncate(float, float) Truncates (cuts) excess decimal places

Parameters:

float : number The number to truncate

float : decimalPlaces (default=2) The number of decimal places to truncate to

Returns: The given number truncated to the given decimalPlaces

toWhole(float) Converts pips into whole numbers

Parameters:

float : number The pip number to convert into a whole number

Returns: The converted number

toPips(float) Converts whole numbers back into pips

Parameters:

float : number The whole number to convert into pips

Returns: The converted number

getPctChange(float, float, int) Gets the percentage change between 2 float values over a given lookback period

Parameters:

float : value1 The first value to reference

float : value2 The second value to reference

int : lookback The lookback period to analyze

av_getPositionSize(float, float, float, float) Calculates OANDA forex position size for AutoView based on the given parameters

Parameters:

float : balance The account balance to use

float : risk The risk percentage amount (as a whole number - eg. 1 = 1% risk)

float : stopPoints The stop loss distance in POINTS (not pips)

float : conversionRate The conversion rate of our account balance currency

Returns: The calculated position size (in units - only compatible with OANDA)

bullFib(priceLow, priceHigh, fibRatio) Calculates a bullish fibonacci value

Parameters:

priceLow : The lowest price point

priceHigh : The highest price point

fibRatio : The fibonacci % ratio to calculate

Returns: The fibonacci value of the given ratio between the two price points

bearFib(priceLow, priceHigh, fibRatio) Calculates a bearish fibonacci value

Parameters:

priceLow : The lowest price point

priceHigh : The highest price point

fibRatio : The fibonacci % ratio to calculate

Returns: The fibonacci value of the given ratio between the two price points

getMA(int, string) Gets a Moving Average based on type (MUST BE CALLED ON EVERY CALCULATION)

Parameters:

int : length The MA period

string : maType The type of MA

Returns: A moving average with the given parameters

getEAP(float) Performs EAP stop loss size calculation (eg. ATR >= 20.0 and ATR < 30, returns 20)

Parameters:

float : atr The given ATR to base the EAP SL calculation on

Returns: The EAP SL converted ATR size

getEAP2(float) Performs secondary EAP stop loss size calculation (eg. ATR < 40, add 5 pips, ATR between 40-50, add 10 pips etc)

Parameters:

float : atr The given ATR to base the EAP SL calculation on

Returns: The EAP SL converted ATR size

barsAboveMA(int, float) Counts how many candles are above the MA

Parameters:

int : lookback The lookback period to look back over

float : ma The moving average to check

Returns: The bar count of how many recent bars are above the MA

barsBelowMA(int, float) Counts how many candles are below the MA

Parameters:

int : lookback The lookback period to look back over

float : ma The moving average to reference

Returns: The bar count of how many recent bars are below the EMA

barsCrossedMA(int, float) Counts how many times the EMA was crossed recently

Parameters:

int : lookback The lookback period to look back over

float : ma The moving average to reference

Returns: The bar count of how many times price recently crossed the EMA

getPullbackBarCount(int, int) Counts how many green & red bars have printed recently (ie. pullback count)

Parameters:

int : lookback The lookback period to look back over

int : direction The color of the bar to count (1 = Green, -1 = Red)

Returns: The bar count of how many candles have retraced over the given lookback & direction

getBodySize() Gets the current candle's body size (in POINTS, divide by 10 to get pips)

Returns: The current candle's body size in POINTS

getTopWickSize() Gets the current candle's top wick size (in POINTS, divide by 10 to get pips)

Returns: The current candle's top wick size in POINTS

getBottomWickSize() Gets the current candle's bottom wick size (in POINTS, divide by 10 to get pips)

Returns: The current candle's bottom wick size in POINTS

getBodyPercent() Gets the current candle's body size as a percentage of its entire size including its wicks

Returns: The current candle's body size percentage

isHammer(float, bool) Checks if the current bar is a hammer candle based on the given parameters

Parameters:

float : fib (default=0.382) The fib to base candle body on

bool : colorMatch (default=false) Does the candle need to be green? (true/false)

Returns: A boolean - true if the current bar matches the requirements of a hammer candle

isStar(float, bool) Checks if the current bar is a shooting star candle based on the given parameters

Parameters:

float : fib (default=0.382) The fib to base candle body on

bool : colorMatch (default=false) Does the candle need to be red? (true/false)

Returns: A boolean - true if the current bar matches the requirements of a shooting star candle

isDoji(float, bool) Checks if the current bar is a doji candle based on the given parameters

Parameters:

float : wickSize (default=2) The maximum top wick size compared to the bottom (and vice versa)

bool : bodySize (default=0.05) The maximum body size as a percentage compared to the entire candle size

Returns: A boolean - true if the current bar matches the requirements of a doji candle

isBullishEC(float, float, bool) Checks if the current bar is a bullish engulfing candle

Parameters:

float : allowance (default=0) How many POINTS to allow the open to be off by (useful for markets with micro gaps)

float : rejectionWickSize (default=disabled) The maximum rejection wick size compared to the body as a percentage

bool : engulfWick (default=false) Does the engulfing candle require the wick to be engulfed as well?

Returns: A boolean - true if the current bar matches the requirements of a bullish engulfing candle

isBearishEC(float, float, bool) Checks if the current bar is a bearish engulfing candle

Parameters:

float : allowance (default=0) How many POINTS to allow the open to be off by (useful for markets with micro gaps)

float : rejectionWickSize (default=disabled) The maximum rejection wick size compared to the body as a percentage

bool : engulfWick (default=false) Does the engulfing candle require the wick to be engulfed as well?

Returns: A boolean - true if the current bar matches the requirements of a bearish engulfing candle

isInsideBar() Detects inside bars

Returns: Returns true if the current bar is an inside bar

isOutsideBar() Detects outside bars

Returns: Returns true if the current bar is an outside bar

barInSession(string, bool) Determines if the current price bar falls inside the specified session

Parameters:

string : sess The session to check

bool : useFilter (default=true) Whether or not to actually use this filter

Returns: A boolean - true if the current bar falls within the given time session

barOutSession(string, bool) Determines if the current price bar falls outside the specified session

Parameters:

string : sess The session to check

bool : useFilter (default=true) Whether or not to actually use this filter

Returns: A boolean - true if the current bar falls outside the given time session

dateFilter(int, int) Determines if this bar's time falls within date filter range

Parameters:

int : startTime The UNIX date timestamp to begin searching from

int : endTime the UNIX date timestamp to stop searching from

Returns: A boolean - true if the current bar falls within the given dates

dayFilter(bool, bool, bool, bool, bool, bool, bool) Checks if the current bar's day is in the list of given days to analyze

Parameters:

bool : monday Should the script analyze this day? (true/false)

bool : tuesday Should the script analyze this day? (true/false)

bool : wednesday Should the script analyze this day? (true/false)

bool : thursday Should the script analyze this day? (true/false)

bool : friday Should the script analyze this day? (true/false)

bool : saturday Should the script analyze this day? (true/false)

bool : sunday Should the script analyze this day? (true/false)

Returns: A boolean - true if the current bar's day is one of the given days

atrFilter()

fillCell()

SuperTrend OptimizerHello!

This indicator attempts to optimize Supertrend parameters. To achieve this, 102 parameter combinations are tested concurrently - the top three performers are listed in descending order.

Parameters,

Factor: Changes to this parameter shifts the tested factor range. For instance, increasing the factor measure from 3.00 to 3.01 (+0.01) will remove 3.00 from the tested range - this setting controls the lower threshold of the range. The upper threshold, in all instances, is the lower Factor threshold + 3.3 (i.e. 3.0(lower) - 6.3(upper), 4.0(lower) - 7.3(upper), 2.5(lower) - 5.8(upper))

ATR period: Changes to this parameter shifts the tested ATR period range. For instance, increasing the ATR measure from 10 to 11 (+1) will remove 10 from the tested range - this setting controls the lower threshold of the range. The upper threshold, in all instances, is the lower threshold + 2 (i.e. 10(lower) - 12(upper), 11(lower) - 13(upper), 9(lower), - 11(upper))

The Factor parameter is modifiable to any positive decimal number; the ATR parameter is modifiable to any positive integer. Changing either parameter shifts the tested parameter combination range. Both parameters can be changed in the settings, to which you control the lower threshold of the range. If, for instance, you were to change the Factor measurement from 3.0 to 4.1 (+1.1) the 4.0 Factor measurement, and all Factor measures less than 4.0, will be excluded from the performance test.

Consequently, a Supertrend test will be performed with a Factor of 4.1 and an ATR period of 10 (default). This test repeats at 0.1 Factor intervals and 1.0 ATR intervals.

Therefore, assume you modify the Factor lower threshold to 3.1 and the ATR lower threshold to 10. The indicator will test three Supertrend systems with a Factor of 3.1 and an ATR period of 10.. then 11.. 12, then three systems with a Factor of 3.2 and an ATR period of 10.. then 11.. 12... until (lower Factor threshold + 3.3) and (lower ATR threshold + 2) are tested... which in this example is... a Factor of 6.4 and an ATR period of 12.

The tested Factor range and ATR range are displayed in a bottom right table alongside the top performing parameter combinations.

Of course, you can change the the lower thresholds, which means you can test numerous Supertrend parameter combinations! However, no greater than 102 parameter combinations will be tested simultaneously; the best performing Supertrend parameters are plotted on the chart automatically.

I will be working on this indicator more tomorrow! Let me know if you have questions or anything you would like included!

(I of course added something fun in the script. Be sure to try it with bar replay!)

Top 40 High Low Strategy for SPY, 5minThis strategy is developed based on my High Low Index SPY Top 40 indicator

Notes:

- this strategy is only developed for SPY on the 5 min chart . It seems to work with QQQ as well, but it isn't optimized for it

- P/L shown is based on 10 SPY option contracts, call or put, with strike price closest to the entry SPY price and expiry of 0 to 1 day. This includes commissions (can be changed). This is only an estimate calculated using an arbitrary multiplier factor, this can be changed in the setting

- P/L is based on $5000 initial capital

- Works with both regular / extended trading session turned on/off. However, max drawdown is 1/2 with extended trading session ON

- there is still a bug that doesn't allow alert to be created due to calculation error, will update once fixed

This strategy combines signals from the following indicators to determine entry signals:

- High Low Index SPY Top 40

- MACD

- Linear Regression Slope

Entry signal is triggered when:

- High Low Index line crosses the EMA line

- MACD trending in the same direction

- Linear Regression slope is accelerating above a threshold in the same direction, indicating a strong trend

Profit target(PT) and stop loss(SL) are determined using ATR value, with 2:1 Reward to Risk ratio as default.

Exit signal may be triggered prior to PT or SL trigger when:

- High Low Index SPY Top 40 shows a reversal after overbought or oversold conditions (optional)

- Opposite entry signal is triggered

There are a number of optional settings:

- Turn on/off "option trading", P/L will be calculated using share price only without multiplication factor for trading option contracts

- # of options per trade, default to 10

- Reinvest with profit made

- Trade with trailing SL after PT hit

- Take profit early based on Top 40 overbought/oversold

- Trade 0/1 day expiry. This will signal exit by the end of the day on Mon/Wed/Fri, and only exits 1/2 of positions (if in profit) on Tues/Thurs

- Can reduce the SL level without impacting PT

- No entry between 10:05 - 10:20 (don't ask me why, but statistically it performs better)

Consider donating me some of your profit if you make $$$ hahaha~ ;)

Enjoy~~

Williams Alligator Trend Filter HeatmapHello I've decided that the alligator lines can be used to find a trend. This script expands on that and checks 10 different multipliers to see trend over the long term and have 10 values. Those 10 values each give a color to one of the 10 lines in turn giving this Fire like plotting. I personaly use this to see if there is fear (red) in the markets or greed (blue), plotted 9 different crypto coins on the chart and have 4 columns in my setup to see the values on different timeframes. In the chart preview this is 1H,30M,10M,1M to see current environment. The colors use alot of data to generate especialy the bottom part, that colors based on a very long time zone.

Up & Down Trend following trading strategy for BTC/USDT 3hThis strategy is based on multi time frame technical indicators such as;

1. RSI (10,50,100)

2. MFI (10,50,100)

3. RVI (10,50,100)

4. BOP (10,50,100)

5. Super Trend

6. SAR indicator

7. Higher highs and lower lows

8. SMA (9,500)

9. EMA (9,200)

After evaluating different parameters provided by those indicators, script is in a possition to determine optimul positions to enter in to market as well as exit from the market. In some cases stratergy will exit fully or partially depends on the situation. Other than that, this strategy is in a possition to calculate and specify the quantity you need to buy or sell depending on market situation. You can specify amount available for investment and how many times you are going to average (if downtrend). Parameters are optimised to BTC/USDT, 3h standerd candlestic chart.

goodluck

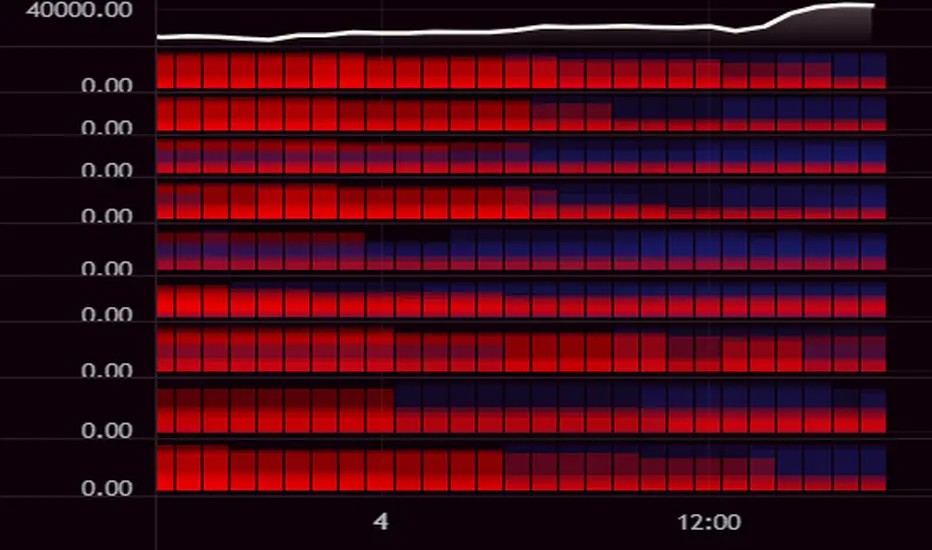

RVOL Relative Volume - IntradayHello All,

Relative Volume is one of the most important indicators and Traders should check it while trading/analyzing. it is used to identify whether the volume flows are increasing or decreasing. Relative volume measures current volume in relation to the “usual” volume for this time of the day. What is considered “usual"? For that, we have to use a historical baseline known as the average daily volume. That means how much volume a security does on a daily basis over a defined period. (This scripts runs on the time frames greater or equal 1 minute and less than 1 day)

The common definition for real-time relative volume is: Current volume for this time of day / Average volume for this time of day. It does not mean taking the volume (for example) from 10:30 am to 10:45 am and comparing it to what it does from 10:30 am to 10:45 am every day. What it truly means is to compare cumulative volumes. Therefore, this is the precise definition of real-time relative volume:

Current cumulative volume up to this time of day / Average cumulative volume up to this time of day

What should we understand while checking RVOL;

- Relative volume tell us if volume flows are increasing or decreasing

- A high relative volume tells us that there is increased trading activity in a security today

- Increased volume flows often accompany higher volatility i.e. a significant price move

Let see an example:

P.S. if you want to get more info about RVOL/Relative Volume then you can search it on the net. While developing the script this was used as reference, you can also check it for more info.

Enjoy!

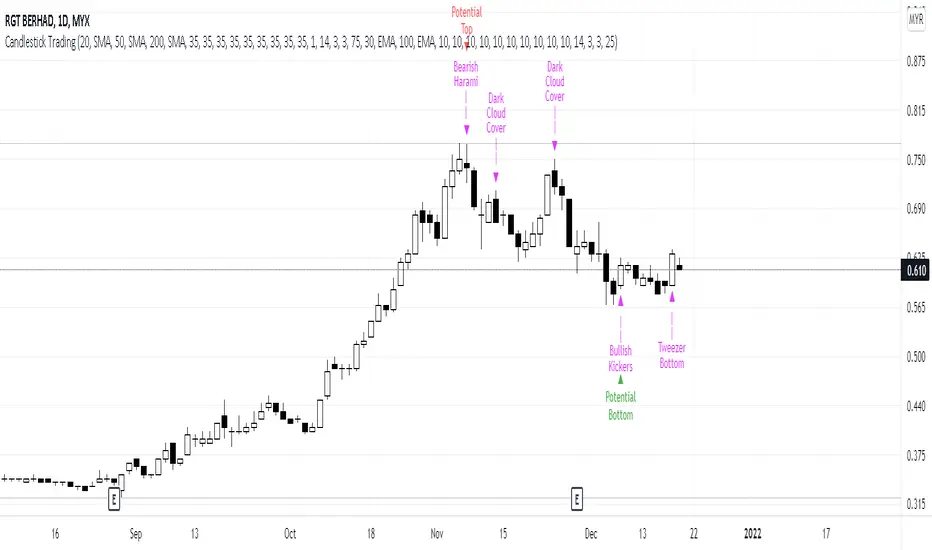

Candlestick Trading (Malaysia Stock Market)1. This indicator will indicate signals of bearish/bullish candlestick as below:

- 10 Bear Candles: Dark Cloud Cover, Bearish Kickers, Bearish Engulfing, Evening Star, Three Black Crows, Hanging Man, Shooting Star, Tweezer Top, Bearish Harami, Doji

- 10 Bull Candles: Piercing, Bullish Kickers, Bullish Engulfing, Morning Star, Three White Soldiers, Hammer, Inverted Hammer, Tweezer Bottom, Bearish Harami, Doji

2. In order for the Bear Candle signals to appear, these conditions should be met:

- Price must be above MA 1 (preset at SMA 20)

- Price must be above MA 2 (preset at SMA 50)

- Price must be above MA 3 (preset at SMA 200)

- In the range of specified trading days (preset at latest 10 days of trading)

3. For a strong bearish signal, a namely 'Potential Top' signal will appear on the top of the bearish candlestick signal. This 'Potential Top' signal will only appear under the condition of:

- Stochastic is at overbought area (preset at 75%)

4. In order for the Bull Candle signals to appear, these conditions should be met:

- Price must be in between MA 4 (preset at EMA 30) and MA 5 (preset at EMA 100)

- In the range of specified trading days (preset at latest 10 days of trading)

5. For a strong bullish signal, a namely 'Potential Bottom' signal will appear at the bottom of the bullish candlestick signal. This 'Potential Bottom' signal will only appear under the condition of:

- Stochastic is at oversold area (preset at 25%)

6. This indicator can help one to enter/exit a trade based on the bullish/bearish candlestick patterns that appear at the beginning/end of a trend, especially when the 'Potential Bottom/Top' appears with any of bullish/bearish candlestick signal.

7. However, this indicator is only designed for Malaysian Stocks Market as the script is based on the bids/pips calculation of the Malaysian Stocks Market. Nevertheless, I let the script open for everyone to modify it based on your own preference markets/instruments.

8. Hope you guys enjoy it. Thanks.

Tendency EMA + RSI [Alorse]A very simple and highly effective strategy LONG & SHORT that combines only 2 indicators:

RSI

3 Moving Average Exponential (EMA)

LONG Entry conditions are:

EMA 20 cross over EMA 10

EMA 10 is above EMA 100

LONG Exit conditions are:

RSI greater than 70

Or when X number of candles have passed and the trade is in profit. (Check Settings)

SHORT Entry conditions are:

EMA 20 cross under EMA 10

EMA 10 is below EMA 100

SHORT Exit conditions are:

RSI is less than 30

Or when X number of candles have passed and the trade is in profit. (Check Settings)

4 SMAs & Inside Bar (Colored)SMAs and Inside Bar strategy is very common as far as Technical analysis is concern. This script is a combination of 10-20-50-200 SMA and Inside Bar Candle Identification.

SMA Crossover:

4 SMAs (10, 20, 50 & 200) are combined here in one single indicator.

Crossover signal for Buy as "B" will be shown in the chart if SMA 10 is above 20 & 50 and SMA 20 is above 50.

Crossover signal for Sell as "S" will be shown in the chart if SMA 10 is below 20 & 50 and SMA 20 is below 50.

Inside Bar Identification:

This is to simply identify if there is a inside bar candle. The logic is very simple - High of the previous candle should be higher than current candle and low of the previous candle should be lower than the current candle.

If the previous candle is red, the following candle would be Yellow - which may give some bullish view in most of the cases but not always

If the previous candle is green, the following candle would be Black - which may give some bearish view in most of the cases but not always

Be Cautious when you see alternate yellow and black candle, it may give move on the both side

Please comment if you have any interesting ideas to improve this indicator.

Webhook Starter Kit [HullBuster]

Introduction

This is an open source strategy which provides a framework for webhook enabled projects. It is designed to work out-of-the-box on any instrument triggering on an intraday bar interval. This is a full featured script with an emphasis on actual trading at a brokerage through the TradingView alert mechanism and without requiring browser plugins.

The source code is written in a self documenting style with clearly defined sections. The sections “communicate” with each other through state variables making it easy for the strategy to evolve and improve. This is an excellent place for Pine Language beginners to start their strategy building journey. The script exhibits many Pine Language features which will certainly ad power to your script building abilities.

This script employs a basic trend follow strategy utilizing a forward pyramiding technique. Trend detection is implemented through the use of two higher time frame series. The market entry setup is a Simple Moving Average crossover. Positions exit by passing through conditional take profit logic. The script creates ten indicators including a Zscore oscillator to measure support and resistance levels. The indicator parameters are exposed through 47 strategy inputs segregated into seven sections. All of the inputs are equipped with detailed tool tips to help you get started.

To improve the transition from simulation to execution, strategy.entry and strategy.exit calls show enhanced message text with embedded keywords that are combined with the TradingView placeholders at alert time. Thereby, enabling a single JSON message to generate multiple execution events. This is genius stuff from the Pine Language development team. Really excellent work!

This document provides a sample alert message that can be applied to this script with relatively little modification. Without altering the code, the strategy inputs can alter the behavior to generate thousands of orders or simply a few dozen. It can be applied to crypto, stocks or forex instruments. A good way to look at this script is as a webhook lab that can aid in the development of your own endpoint processor, impress your co-workers and have hours of fun.

By no means is a webhook required or even necessary to benefit from this script. The setups, exits, trend detection, pyramids and DCA algorithms can be easily replaced with more sophisticated versions. The modular design of the script logic allows you to incrementally learn and advance this script into a functional trading system that you can be proud of.

Design

This is a trend following strategy that enters long above the trend line and short below. There are five trend lines that are visible by default but can be turned off in Section 7. Identified, in frequency order, as follows:

1. - EMA in the chart time frame. Intended to track price pressure. Configured in Section 3.

2. - ALMA in the higher time frame specified in Section 2 Signal Line Period.

3. - Linear Regression in the higher time frame specified in Section 2 Signal Line Period.

4. - Linear Regression in the higher time frame specified in Section 2 Signal Line Period.

5. - DEMA in the higher time frame specified in Section 2 Trend Line Period.

The Blue, Green and Orange lines are signal lines are on the same time frame. The time frame selected should be at least five times greater than the chart time frame. The Purple line represents the trend line for which prices above the line suggest a rising market and prices below a falling market. The time frame selected for the trend should be at least five times greater than the signal lines.

Three oscillators are created as follows:

1. Stochastic - In the chart time frame. Used to enter forward pyramids.

2. Stochastic - In the Trend period. Used to detect exit conditions.

3. Zscore - In the Signal period. Used to detect exit conditions.

The Stochastics are configured identically other than the time frame. The period is set in Section 2.

Two Simple Moving Averages provide the trade entry conditions in the form of a crossover. Crossing up is a long entry and down is a short. This is in fact the same setup you get when you select a basic strategy from the Pine editor. The crossovers are configured in Section 3. You can see where the crosses are occurring by enabling Show Entry Regions in Section 7.

The script has the capacity for pyramids and DCA. Forward pyramids are enabled by setting the Pyramid properties tab with a non zero value. In this case add on trades will enter the market on dips above the position open price. This process will continue until the trade exits. Downward pyramids are available in Crypto and Range mode only. In this case add on trades are placed below the entry price in the drawdown space until the stop is hit. To enable downward pyramids set the Pyramid Minimum Span In Section 1 to a non zero value.

This implementation of Dollar Cost Averaging (DCA) triggers off consecutive losses. Each loss in a run increments a sequence number. The position size is increased as a multiple of this sequence. When the position eventually closes at a profit the sequence is reset. DCA is enabled by setting the Maximum DCA Increments In Section 1 to a non zero value.

It should be noted that the pyramid and DCA features are implemented using a rudimentary design and as such do not perform with the precision of my invite only scripts. They are intended as a feature to stress test your webhook endpoint. As is, you will need to buttress the logic for it to be part of an automated trading system. It is for this reason that I did not apply a Martingale algorithm to this pyramid implementation. But, hey, it’s an open source script so there is plenty of room for learning and your own experimentation.

How does it work

The overall behavior of the script is governed by the Trading Mode selection in Section 1. It is the very first input so you should think about what behavior you intend for this strategy at the onset of the configuration. As previously discussed, this script is designed to be a trend follower. The trend being defined as where the purple line is predominately heading. In BiDir mode, SMA crossovers above the purple line will open long positions and crosses below the line will open short. If pyramiding is enabled add on trades will accumulate on dips above the entry price. The value applied to the Minimum Profit input in Section 1 establishes the threshold for a profitable exit. This is not a hard number exit. The conditional exit logic must be satisfied in order to permit the trade to close. This is where the effort put into the indicator calibration is realized. There are four ways the trade can exit at a profit:

1. Natural exit. When the blue line crosses the green line the trade will close. For a long position the blue line must cross under the green line (downward). For a short the blue must cross over the green (upward).

2. Alma / Linear Regression event. The distance the blue line is from the green and the relative speed the cross is experiencing determines this event. The activation thresholds are set in Section 6 and relies on the period and length set in Section 2. A long position will exit on an upward thrust which exceeds the activation threshold. A short will exit on a downward thrust.

3. Exponential event. The distance the yellow line is from the blue and the relative speed the cross is experiencing determines this event. The activation thresholds are set in Section 3 and relies on the period and length set in the same section.

4. Stochastic event. The purple line stochastic is used to measure overbought and over sold levels with regard to position exits. Signal line positions combined with a reading over 80 signals a long profit exit. Similarly, readings below 20 signal a short profit exit.

Another, optional, way to exit a position is by Bale Out. You can enable this feature in Section 1. This is a handy way to reduce the risk when carrying a large pyramid stack. Instead of waiting for the entire position to recover we exit early (bale out) as soon as the profit value has doubled.

There are lots of ways to implement a bale out but the method I used here provides a succinct example. Feel free to improve on it if you like. To see where the Bale Outs occur, enable Show Bale Outs in Section 7. Red labels are rendered below each exit point on the chart.

There are seven selectable Trading Modes available from the drop down in Section 1:

1. Long - Uses the strategy.risk.allow_entry_in to execute long only trades. You will still see shorts on the chart.

2. Short - Uses the strategy.risk.allow_entry_in to execute short only trades. You will still see long trades on the chart.

3. BiDir - This mode is for margin trading with a stop. If a long position was initiated above the trend line and the price has now fallen below the trend, the position will be reversed after the stop is hit. Forward pyramiding is available in this mode if you set the Pyramiding value in the Properties tab. DCA can also be activated.

4. Flip Flop - This is a bidirectional trading mode that automatically reverses on a trend line crossover. This is distinctively different from BiDir since you will get a reversal even without a stop which is advantageous in non-margin trading.

5. Crypto - This mode is for crypto trading where you are buying the coins outright. In this case you likely want to accumulate coins on a crash. Especially, when all the news outlets are talking about the end of Bitcoin and you see nice deep valleys on the chart. Certainly, under these conditions, the market will be well below the purple line. No margin so you can’t go short. Downward pyramids are enabled for Crypto mode when two conditions are met. First the Pyramiding value in the Properties tab must be non zero. Second the Pyramid Minimum Span in Section 1 must be non zero.

6. Range - This is a counter trend trading mode. Longs are entered below the purple trend line and shorts above. Useful when you want to test your webhook in a market where the trend line is bisecting the signal line series. Remember that this strategy is a trend follower. It’s going to get chopped out in a range bound market. By turning on the Range mode you will at least see profitable trades while stuck in the range. However, when the market eventually picks a direction, this mode will sustain losses. This range trading mode is a rudimentary implementation that will need a lot of improvement if you want to create a reliable switch hitter (trend/range combo).

7. No Trade. Useful when setting up the trend lines and the entry and exit is not important.

Once in the trade, long or short, the script tests the exit condition on every bar. If not a profitable exit then it checks if a pyramid is required. As mentioned earlier, the entry setups are quite primitive. Although they can easily be replaced by more sophisticated algorithms, what I really wanted to show is the diminished role of the position entry in the overall life of the trade. Professional traders spend much more time on the management of the trade beyond the market entry. While your trade entry is important, you can get in almost anywhere and still land a profitable exit.

If DCA is enabled, the size of the position will increase in response to consecutive losses. The number of times the position can increase is limited by the number set in Maximum DCA Increments of Section 1. Once the position breaks the losing streak the trade size will return the default quantity set in the Properties tab. It should be noted that the Initial Capital amount set in the Properties tab does not affect the simulation in the same way as a real account. In reality, running out of money will certainly halt trading. In fact, your account would be frozen long before the last penny was committed to a trade. On the other hand, TradingView will keep running the simulation until the current bar even if your funds have been technically depleted.

Entry and exit use the strategy.entry and strategy.exit calls respectfully. The alert_message parameter has special keywords that the endpoint expects to properly calculate position size and message sequence. The alert message will embed these keywords in the JSON object through the {{strategy.order.alert_message}} placeholder. You should use whatever keywords are expected from the endpoint you intend to webhook in to.

Webhook Integration

The TradingView alerts dialog provides a way to connect your script to an external system which could actually execute your trade. This is a fantastic feature that enables you to separate the data feed and technical analysis from the execution and reporting systems. Using this feature it is possible to create a fully automated trading system entirely on the cloud. Of course, there is some work to get it all going in a reliable fashion. Being a strategy type script place holders such as {{strategy.position_size}} can be embedded in the alert message text. There are more than 10 variables which can write internal script values into the message for delivery to the specified endpoint.

Entry and exit use the strategy.entry and strategy.exit calls respectfully. The alert_message parameter has special keywords that my endpoint expects to properly calculate position size and message sequence. The alert message will embed these keywords in the JSON object through the {{strategy.order.alert_message}} placeholder. You should use whatever keywords are expected from the endpoint you intend to webhook in to.

Here is an excerpt of the fields I use in my webhook signal:

"broker_id": "kraken",

"account_id": "XXX XXXX XXXX XXXX",

"symbol_id": "XMRUSD",

"action": "{{strategy.order.action}}",

"strategy": "{{strategy.order.id}}",

"lots": "{{strategy.order.contracts}}",

"price": "{{strategy.order.price}}",

"comment": "{{strategy.order.alert_message}}",

"timestamp": "{{time}}"

Though TradingView does a great job in dispatching your alert this feature does come with a few idiosyncrasies. Namely, a single transaction call in your script may cause multiple transmissions to the endpoint. If you are using placeholders each message describes part of the transaction sequence. A good example is closing a pyramid stack. Although the script makes a single strategy.close() call, the endpoint actually receives a close message for each pyramid trade. The broker, on the other hand, only requires a single close. The incongruity of this situation is exacerbated by the possibility of messages being received out of sequence. Depending on the type of order designated in the message, a close or a reversal. This could have a disastrous effect on your live account. This broker simulator has no idea what is actually going on at your real account. Its just doing the job of running the simulation and sending out the computed results. If your TradingView simulation falls out of alignment with the actual trading account lots of really bad things could happen. Like your script thinks your are currently long but the account is actually short. Reversals from this point forward will always be wrong with no one the wiser. Human intervention will be required to restore congruence. But how does anyone find out this is occurring? In closed systems engineering this is known as entropy. In practice your webhook logic should be robust enough to detect these conditions. Be generous with the placeholder usage and give the webhook code plenty of information to compare states. Both issuer and receiver. Don’t blindly commit incoming signals without verifying system integrity.

Setup

The following steps provide a very brief set of instructions that will get you started on your first configuration. After you’ve gone through the process a couple of times, you won’t need these anymore. It’s really a simple script after all. I have several example configurations that I used to create the performance charts shown. I can share them with you if you like. Of course, if you’ve modified the code then these steps are probably obsolete.

There are 47 inputs divided into seven sections. For the most part, the configuration process is designed to flow from top to bottom. Handy, tool tips are available on every field to help get you through the initial setup.

Step 1. Input the Base Currency and Order Size in the Properties tab. Set the Pyramiding value to zero.

Step 2. Select the Trading Mode you intend to test with from the drop down in Section 1. I usually select No Trade until I’ve setup all of the trend lines, profit and stop levels.

Step 3. Put in your Minimum Profit and Stop Loss in the first section. This is in pips or currency basis points (chart right side scale). Remember that the profit is taken as a conditional exit not a fixed limit. The actual profit taken will almost always be greater than the amount specified. The stop loss, on the other hand, is indeed a hard number which is executed by the TradingView broker simulator when the threshold is breached.

Step 4. Apply the appropriate value to the Tick Scalar field in Section 1. This value is used to remove the pipette from the price. You can enable the Summary Report in Section 7 to see the TradingView minimum tick size of the current chart.

Step 5. Apply the appropriate Price Normalizer value in Section 1. This value is used to normalize the instrument price for differential calculations. Basically, we want to increase the magnitude to significant digits to make the numbers more meaningful in comparisons. Though I have used many normalization techniques, I have always found this method to provide a simple and lightweight solution for less demanding applications. Most of the time the default value will be sufficient. The Tick Scalar and Price Normalizer value work together within a single calculation so changing either will affect all delta result values.

Step 6. Turn on the trend line plots in Section 7. Then configure Section 2. Try to get the plots to show you what’s really happening not what you want to happen. The most important is the purple trend line. Select an interval and length that seem to identify where prices tend to go during non-consolidation periods. Remember that a natural exit is when the blue crosses the green line.

Step 7. Enable Show Event Regions in Section 7. Then adjust Section 6. Blue background fills are spikes and red fills are plunging prices. These measurements should be hard to come by so you should see relatively few fills on the chart if you’ve set this up as intended. Section 6 includes the Zscore oscillator the state of which combines with the signal lines to detect statistically significant price movement. The Zscore is a zero based calculation with positive and negative magnitude readings. You want to input a reasonably large number slightly below the maximum amplitude seen on the chart. Both rise and fall inputs are entered as a positive real number. You can easily use my code to create a separate indicator if you want to see it in action. The default value is sufficient for most configurations.

Step 8. Turn off Show Event Regions and enable Show Entry Regions in Section 7. Then adjust Section 3. This section contains two parts. The entry setup crossovers and EMA events. Adjust the crossovers first. That is the Fast Cross Length and Slow Cross Length. The frequency of your trades will be shown as blue and red fills. There should be a lot. Then turn off Show Event Regions and enable Display EMA Peaks. Adjust all the fields that have the word EMA. This is actually the yellow line on the chart. The blue and red fills should show much less than the crossovers but more than event fills shown in Step 7.

Step 9. Change the Trading Mode to BiDir if you selected No Trades previously. Look on the chart and see where the trades are occurring. Make adjustments to the Minimum Profit and Stop Offset in Section 1 if necessary. Wider profits and stops reduce the trade frequency.

Step 10. Go to Section 4 and 5 and make fine tuning adjustments to the long and short side.

Example Settings

To reproduce the performance shown on the chart please use the following configuration: (Bitcoin on the Kraken exchange)

1. Select XBTUSD Kraken as the chart symbol.

2. On the properties tab set the Order Size to: 0.01 Bitcoin

3. On the properties tab set the Pyramiding to: 12

4. In Section 1: Select “Crypto” for the Trading Model

5. In Section 1: Input 2000 for the Minimum Profit

6. In Section 1: Input 0 for the Stop Offset (No Stop)

7. In Section 1: Input 10 for the Tick Scalar

8. In Section 1: Input 1000 for the Price Normalizer

9. In Section 1: Input 2000 for the Pyramid Minimum Span

10. In Section 1: Check mark the Position Bale Out

11. In Section 2: Input 60 for the Signal Line Period

12. In Section 2: Input 1440 for the Trend Line Period

13. In Section 2: Input 5 for the Fast Alma Length

14. In Section 2: Input 22 for the Fast LinReg Length

15. In Section 2: Input 100 for the Slow LinReg Length

16. In Section 2: Input 90 for the Trend Line Length

17. In Section 2: Input 14 Stochastic Length

18. In Section 3: Input 9 Fast Cross Length

19. In Section 3: Input 24 Slow Cross Length

20. In Section 3: Input 8 Fast EMA Length

21. In Section 3: Input 10 Fast EMA Rise NetChg

22. In Section 3: Input 1 Fast EMA Rise ROC

23. In Section 3: Input 10 Fast EMA Fall NetChg

24. In Section 3: Input 1 Fast EMA Fall ROC

25. In Section 4: Check mark the Long Natural Exit

26. In Section 4: Check mark the Long Signal Exit

27. In Section 4: Check mark the Long Price Event Exit

28. In Section 4: Check mark the Long Stochastic Exit

29. In Section 5: Check mark the Short Natural Exit

30. In Section 5: Check mark the Short Signal Exit

31. In Section 5: Check mark the Short Price Event Exit

32. In Section 5: Check mark the Short Stochastic Exit

33. In Section 6: Input 120 Rise Event NetChg

34. In Section 6: Input 1 Rise Event ROC

35. In Section 6: Input 5 Min Above Zero ZScore

36. In Section 6: Input 120 Fall Event NetChg

37. In Section 6: Input 1 Fall Event ROC

38. In Section 6: Input 5 Min Below Zero ZScore

In this configuration we are trading in long only mode and have enabled downward pyramiding. The purple trend line is based on the day (1440) period. The length is set at 90 days so it’s going to take a while for the trend line to alter course should this symbol decide to node dive for a prolonged amount of time. Your trades will still go long under those circumstances. Since downward accumulation is enabled, your position size will grow on the way down.

The performance example is Bitcoin so we assume the trader is buying coins outright. That being the case we don’t need a stop since we will never receive a margin call. New buy signals will be generated when the price exceeds the magnitude and speed defined by the Event Net Change and Rate of Change.

Feel free to PM me with any questions related to this script. Thank you and happy trading!

CFTC RULE 4.41

These results are based on simulated or hypothetical performance results that have certain inherent limitations. Unlike the results shown in an actual performance record, these results do not represent actual trading. Also, because these trades have not actually been executed, these results may have under-or over-compensated for the impact, if any, of certain market factors, such as lack of liquidity. Simulated or hypothetical trading programs in general are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profits or losses similar to these being shown.

RedK Volume-Weighted Directional Efficiency Index (DXF)RedK Volume-Weighted Directional Efficiency Index (DXF) is a momentum indicator - that builds on Kaufman's Efficiency Ratio (ER) concept.

DXF utilizes a restricted +100/-100 oscillator to represent the "quality" of a trend, and does a good job in detecting the possibility of an upcoming trend change (in both direction and quality), improving our ability to make decisions on trade entries and exits.

Here's a quick background on Kaufman's Efficiency Ratio (ER)

------------------------------------------------------------------------------- Copied from internet sources -----------------------------

Developed by Perry Kaufman and introduced in his book “New Trading Systems and Methods”, the Efficiency Ratio reflects relative market speed to volatility. There are cases, when it is used as a filter, which helps a trader to avoid ”choppy” markets or trading ranges and to identify smoother trends.

ER is the result of dividing the net change in price movement during n-periods by the sum of all bar-to-bar price changes during the same n-periods. In case the market is trending smoother, then the ratio will be higher. In case the ratio shows readings in proximity to zero, this implies that market movement is inefficient and ”choppy”.

If the Efficiency Ratio shows a reading of +100, this means that the trading instrument is in a bull trend and trending with perfect efficiency.

If the Efficiency Ratio shows a reading of -100, this means that the trading instrument is in a bear trend and trending with perfect efficiency.

It is impossible for any instrument to have a perfect Efficiency ratio, because any movement against the major trend during the examined period of time would cause the ratio to drop.

If the Efficiency Ratio shows a reading above +30 (common setting for the "Significant Level"), this is indicative of a quality bull trend. If the ratio shows a reading below -30, this is indicative of a quality bear trend.

------------------------------------------------------------------------------- End of Copy -------------------------------------------------------------------------------------------------------

Kaufman also used the ER as basis for his famous Kaufman Adaptive Moving Average (KAMA).

Read more on ER & Kama here

How is DXF different from other ER-based indicators?

------------------------------------------------------------------

- Let's get the easy part out of the way: DXF has a "volume-weighting" option ✔

This option is OFF by default (to avoid errors with instruments with no volume data)

- once this option is applied, it provides the benefit of combining the volume effect into the calculation - those who appreciate the effect of volume on price action will hopefully find this option valuable

- The calculation of ER and how it can be "best utilized":

Let's examine the ER concept a bit closer: as a (math) concept, the (original) Efficiency Ratio (ER) takes the positive change of the price of an instrument during a certain period, and divide it by the sum of (absolute) price moves that were observed during that same period.

So, in the trader's language, we will be saying "out of a total of $20 moves (up and down) that MSFT did in the past 10 days, MSFT only made a net change of $5 up during that period" - so the "10-day ER" for MSFT in that case is 5/20 = 25% -- then we continue to observe that ongoing "10-day ER" and if it increases, we can expect that MSFT is going to establish a strong move (trend) up --- right?

the magic word here is to "observe the ongoing ER" - many of the ER based indicators just use the ER as calculated by Kaufman's original method. IMHO, these are just "point-in-time readings" - if we hope to get real insights from the ER, we need to take an average of that reading - for our "time window" we're interested in - and only then we can identify trends and patterns in the ER value as it changes during that windowss- DXF does that - and that allows a trader to say "the (weighted) 5-day average of the 10-day ER for MSFT is increasing, and that why i expect an up-trend" -- makes sense ? both the "Lookback" used to calculate the ER, and the Length of observed "window" for the Average ER are adjustable in DXF settings

Other Uses and Settings :

---------------------------------

- As a momentum indicator, DXF can predict an upcoming change of trend - cause that will reflect on the average ER value. There are few examples in the chart where the price move and ER trend *do not agree* - The trader can see these signs and take decisions accordingly

- DXF can help reveal best entries and exits: assume we are long-term bullish on MSFT, and we want to "buy the dip" - DXF can help reveal the time where price is recovering from extreme weakness - and that would be the ideal buy opportunities for us - exampled marked on the chart

- the Stepping & Smoothing options enable better visualization of the DXF plot. the "raw" DXF is still shown as a silver line.

- The "Significant Levels" option is available and is set to -20/+20 by default .. also adjustable in indicator settings.

- Please use DXF in combination with other trend and volume indicators, and with thorough chart / price action analysis and not in isolation to ensure you get proper signal confirmation for trades. In the chart above, you can see DXF combined with a moving average that can act as a filter and to confirm the price moves.

---------------------------------------------------

As usual, feedback & comments are welcome - if you find this work useful in your trading arsenal, please share a comment - i would be more than happy to learn about that. Good luck!

Jakes Index------------

English

I introduce the community to the Jakes Index. Basically, this is an index containing the top 10 cryptocurrencies, classified according to their Marketcap. The purpose of this index is to show a general market context, without being tied to a single crypto. With an overview of the market, it is easier to identify the market trend, in addition to being an excellent indicator to gauge the performance of your Crypt portfolio. Supply data comes from CoinMarktCap, and price data comes mostly from Binance, however some crypts are not yet available for trading by it, so the prices used come from the first broker indicated by TradingView in the search.

Given that one of the crypts was launched very recently, Internet Computer to be more exact, I decided to leave it out of the index, adding "//" to the code in all references to it. If you want to see the performance of the index with the included cryptography, just delete the bars that follow in front of your code, such parts: "ASSET8; SUPPLY8; PESO8; QOC8; FINM8" after that add "//" in "PESO11" and remove the bars from "PESSO11F", in addition to also removing the F. Do the same with "JAKESINDEX" at the end of the code, and you will have the result with the Internet Computer included.

The calculation of the index takes into account the Marketcap of the crypto, which is divided by the sum of the Marketcap of all the others, and then the result is multiplied by the market value of the Cryptocurrency. Thus, we have an index weighted by Marketcap with the 10 most important cryptocurrencies in the market AT THE TIME. It is important to remember that this index must be updated, both in terms of the currencies that change their place in the ranking with certain frequency, as the Supply that each one has, since coins with active mining, as is the case of Bitcoin, change their Supply frequently.

To keep the index up to date, I will do ONE Monthly update, always posting the code with the new changes.

------------

Português

Apresento a comunidade o Jakes Index. Basicamente, este é um índice contendo as 10 principais criptomoedas, classificadas de acordo com seu Marketcap. O objetivo deste índice é mostrar um contexto geral do mercado, sem ficar preso a uma única cripto. Com um apanhado geral sobre o mercado, fica mais fácil identificar a tendência do mercado, além de ser um excelente indicador para balizar o desempenho da sua carteira de Criptos. Os dados referentes a Supply são advindos do CoinMarktCap, e os dados dos preços vem em sua maioria da Binance, porém algumas criptos ainda não estão disponíveis para negociação pela mesma, portanto os preços utilizados vem da primeira corretora indicada pelo TradingView na busca.

Tendo em vista que uma das criptos foi lançada muito recentemente, a Internet Computer para ser mais exato, decidi deixa-la de fora do índice, adicionando "//" no código em todas as referencias a mesma. Caso queira ver o desempenho do índice com a cripto incluída, basta apagar as barras que seguem na frente de seu código, sendo tais partes: "ASSET8; SUPPLY8; PESO8; QOC8; FINM8" após isso adicione "//" em "PESO11" e remova as barras de "PESSO11F", além de remover também o F. Faça o mesmo com "JAKESINDEX" no fim do código, e terá o resultado com a Internet Computer incluída.

O calculo do índice leva em conta o Marketcap da cripto, que é dividio pela soma do Marketcap de todas as outras, e então o resultado é multiplicado pelo valor a mercado da Criptomoeda. Dessa forma, temos um índice ponderado pelo Marketcap com as 10 Criptomoedas mais importantes do mercado NO MOMENTO. É importante lembrar que este índice deve ser atualizado, tanto em questão das moedas que mudam com certa frequência seu lugar no ranking, como o Supply que cada uma tem, visto que moedas com mineração ativa, como é o caso do Bitcoin, mudam seu Supply com frequência.

Para manter o índice atualizado, farei UMA atualização Mensal, postando sempre o código com as novas alterações.

VT R Cloudsettings for the VT R Indicator

VT R TIme (Minues) = 10

Session Time = 09:25 - 09:35

Show VT R Ticked

Show VWMA Ticked

VWMA Period = 10

Long Trade Rules

1. Close ABove buy above

2. trade above ma

3. volume > ma (volume Settings Given Below)

4. sl below sell below

Short Trade Rules

1. close below sell below

2. trade below ma

3. volume > ma (volume Settings Given Below)

4. sl above buy above

Volume Indicator has to be added manually i suggest to use the default Volume Indicator

Settings for the Volume Indicator

Lookback = 10

ShowMA Ticked

LengthMA = 10

Normalized Quantitative Qualitative Estimation nQQENormalized version of Quantitative Qualitative Estimation QQE:

Normalized QQE tries to overcome the problems of false signals due to RSI divergences on the original QQE indicator.

The main purpose is to determine and ride the trend as far as possible.

So users can identify:

UPTREND : when nQQE Histogram is GREEN (nQQE is above 10)

DOWNTREND : when nQQE Histogram is RED (nQQE is below -10)

SIDEWAYS: when nQQE Histogram is YELLOW (nQQE is between -10 and 10)

Calculation is very simple;

RSI based QQE oscillates between 0-100

nQQE is simply calculated as:

nQQE=QQE-50

to make the indicator fluctuate around 0 level to get more accurate signals.

Various alarms added.

Kıvanç Özbilgiç

BTC and ETH Long strategy - version 2I wrote my first article in May 2020. See below

BTC and ETH Long strategy - version1

After 6 months, it is now time to check the result of my script for the last 6 months.

XBTUSD (4H): 14/05/2020 --> 22/11/2020 = +78% in 4 trades

ETHXBT (4H): 14/05/2020 --> 22/11/2020 = +21% in 9 trades

ETHUSD (4H): 14/05/2020 --> 22/11/2020 = +90% in 6 trades

Using the signals from this strategy to trade manually has shown that this was a bit frustrating because of the low rate of winning trades.

If you have to enter 100 trades and see 75% of them failing and 25% winning, this is frustrating. For sure the strategy makes good money but it is difficult to hold this mentality.

So, I have reviewed and modified it to get a higher winning rate.

After few days of work, tests and validation, I managed to get a wining rate close to 60%.

The key element was also to decrease the number of trades by using a higher time frame. (4H candles instead of 2H candles).

- Entry in position is based on

MACD, EMA (20), SMA (100), SMA (200) moving up

AND EMA (20) > SMA (100)

AND SMA (100) > SMA (200)

- Exit the position if: Stoploss is reached OR EMA (20) crossUnder SMA (100)

The goal of this new script is to be able to follow the signals manually and only make few trades per years.

I have also validated it against some other altcoins where some are giving very good results.

Here are some results for 2020 (from 01/01/2020 until now (22/11/2020). Those results are the one I get when using 4H candles.

ETH/USD: +144% in 8 trades.

BTC/USD: +120% in 7 trades.

ETH/BTC: +33% in 9 trades.

ICX/USD: +123% in 10 trades.

LINK/USD: +155% in 11 trades.

MLN/USD: +388% in 8 trades.

ADA/USD: +180% in 7 trades.

LINK/BTC: +97% in 10 trades.

The best is that above results are without considering compound effect. If you re-invest all gains done in each new trade, this will give you the below results :)

ETH/USD: +189% in 8 trades.

BTC/USD: +260% in 7 trades.

ETH/BTC: +29% in 9 trades.

ICX/USD: +112% in 10 trades.

LINK/USD: +222% in 11 trades.

MLN/USD: +793% in 8 trades.

ADA/USD: +319% in 7 trades.

LINK/BTC: +103% in 10 trades.

As you can see, the results are good and the number of trades for 11 months is not big, which allows the trader to place orders manually.

But still, I'm lazy :), so, I have also coded this strategy in HaasScript language which allows you to automate this strategy using the HaasOnline software specialized in automated crypto trading.

I hope that this strategy will give you ideas or will be the starting point for your own strategy.

Let me know if you need more details.

Pipe Bottoms Indicator Based on Thomas Bulkowski's TheoriesPipe bottom is a great indicator of short-term bullish reversal trading. Pipe bottoms appear as 2 "spikes" on the chart after a 2 weeks price drop downtrend, which look like 2 parallel lines on the chart. Based on Bulkowski and the definition on his Patternsite, those 2 "spikes" candles can be any shape, whether doji or any other kinds, thus, wicks length or candle bodies are NOT required in this type of trends. However, a wide price range for these 2 spikes compared to other candles that appeared in 2 weeks is required, so I made sure these 2 pipe bottoms have true ranges (candle length) bigger than the average true ranges in the past 10 trading days (14 calendar days).

Then, a large price overlap must be between these 2 pipe bottoms, so I made sure that the high of either candle of the 2 pipe bottoms must be bigger than 40% of the true range added from the low of another candle, which in short, means that the high of the lower candle will at least be around the middle of the higher candle, and that will ensure price overlap. You can make this 50%, 60% or even 70% of the true range to ensure even greater price overlap, but you will find out that the signal amounts will decrease quite a lot after adjusting.

Bulkowski also suggested 1% variation of the bottom price (low) of those 2 candles, I put it 5% (0.05) personally to get more signals since I do not solely rely on this indicator, and I want more pipe bottoms to show up on my chart for screening purposes. So, feel free to adjust that number for the identification of this pattern.

Finally, the way I ensure it has been a downtrend or price drop is by checking if the price today is below the average of the last 10 trading days (14 calendar days), the price of the pipe bottoms must be below the moving averages of the past 10 trading days. I use hl2 here, feel free to change it to close or open as fit your strategy. Also, you can do this by making sure the candle close prices are decreasing in the past 10 trading days, or any other ways to ensure it's been in a downtrend, but for me, this works fine since again, this is just one of the many patterns I use, so I want more indicators to show up.

So, as you can see on the chart. Whenever the pattern fits the indicator, a small white cross will show up under the candle with "Pipe" text next to it. But do NOT rush to buy yet, because in order to satisfy the pipe bottom pattern, the current close price must be higher than the high of the pipe bottom. And you will see green arrowups when a pipe bottom occurred the last candle, and the current close price is above the high of the pipe bottoms, that would be the entry point of this indicator.

Overall it's a good pattern, especially for a trading bullish reversal after a huge price drop. You can adjust many numbers as I mentioned above to fit your needs, but make sure to add this with other indicators for your strategy, using only 1 indicator or pattern along is never a wise thing, especially in trading. Thanks guys, please like and share.

BTC VIP EMA CROSS Buy/Sell (GC & DC)EMA cross 5&10 standard-setting with add on of BUY/SELL signal ( GC & DC) which will make the traders have an indication of buy and sell easily and clearly.

An exponential moving average strategy, or EMA strategy, is used to identify the predominant trend in the market. It can also provide the support and resistance level to execute your trade. Indicators: v4 (default setting), EMA 5 10 Crossover (default setting)

Preferred Time Frame(s):15-Minute, 30-Minute, 1-Hour, 4-Hour, 1-Day

Strategy

Long Entry Rules

Enter a buy in the market if the following indicator or chart pattern takes center stage:

If the blue upward pointing arrow of the EMA 5 10 Crossover custom indicator gets aligned just somewhat below the candlesticks as seen in Fig. 1.0, the market sentiment is said to be bullish, hence a trigger to go long on the pair of interest.

If the light blue line of the custom indicator gets outlined just below price bars as illustrated in Fig. 1.0, price is said to be pushed somewhat higher i.e. a trigger to buy the asset of focus.

Exit Strategy/Take Profit for Buy Entry

Exit or take profit if the following rules or conditions takes precedence:

If the red downward pointing arrow of the EMA 5 10 Crossover custom indicator forms above price bars as depicted in Fig. 1.0 while a buy signal is ongoing in the market, a possible price dip is said to be looming, as such an exit or take profit is advised.

If the red line of the custom indicator forms above the candlestick during a bullish trend, it is a pointer to a possible price dip, hence an exit or take profit is advised.

Intrinsic value calculation Intrinsic value calculator based on Warren Buffet's and Ben Graham's work

In value investing determing the true value of a COMPANY instead of a stock price is crucial.

This little indicator shows the "Intrinsic value" of the choosen stock meaning the value of the stock in 10 years time. Calculation is based on historical book value's average annual growth rate and dividends paid.

Since this is about long therm investing, use monthly charts.

"Intrinsic value can be defined simply: It is the discounted value of the cash that can be taken out of a business during its remaining life.”

– Warren Buffett

One way to calculate that is by the growth in per share book value and dividends taken in the forseeable future (10 years) than discount it with the prevailing 10 year note's rate.

In the inputs you have to set 2 variables:

1. How many years back you have the first data for book value per share available?

2. What was the per share book value that year?

(Bookvalue is ploted in olive colour and you can get the oldest one if you move your cursor over the latest data on the left)

CAUTION! You have to reenter it for every stock you analyse as this is stock-specific data!

After setting the input data, you will see the "Intrinsic Value"'s pink curve ploted over the price chart.

If the price is well below the pink line, the company is undervalued and can be a possible applicant for long therm investment.

Margin of safety: when the current price is 50% below the intrinsic value that means a 10% yearly growth potential (100% growth in 10 years) or a 100% margin of safety.

I am a beginer in Pine so please excuse my coding...

If anybody knows hot to extract historical data from 15 years ago, please share it with me, so I can automate the whole calculation without inputs necessary.

M-OscillatorM-Oscillator developed By Mohamed Fawzy, MFTA, CFTe

as Written in IFTA Journal 2018 Edition

more info : ifta.org

Interpretation

• M-Oscillator is a bounded oscillator that moves between (-14) and (+14),

• Movement above 10 is considered overbought, and movement below -10 is oversold.

Overbought/Oversold rule:

• Buy when the M-Oscillator violates the (-10) level to the downside and crosses back to the upside.

• Sell when the M-Oscillator crosses above the (+10) level and crosses back to the downside.

Crossover on Extreme Levels

• Sell signals are triggered when the M-Oscillator crosses its signal line above (13), which indicates an extreme market condition

• Buy signals are triggered when the M-Oscillator crosses its signal line below (- 13)

2-Period RSI strategy (with filter)2-period RSI strategy backtest described in several books of the trader Larry Connors . This strategy uses a 2 periods RSI , one slow arithmetic moving average and one fast arithmetic moving average.

Entry signal:

- RSI 2 value below oversold level (Larry Connors usually sets oversold to be below 5, but other authors prefer to work below 10 due to the higher number of signals).

- Closing above the slow average (200 periods).

- Entry at closing of candle or opening of next candle.

Exit signal:

- Occurs when the candlestick closes above the fast average (the most common fast average is 5 periods, but some traders also suggest the 10 period average).

Entry Filter (modification made by me):

- Applied an RSI2 arithmetic moving average to smooth out oscillations.

- Entered only when RSI2 is below oversold level and RSI2 moving average is below 30.

* NOTE: In the stocks that I evaluate daily the averages of 4 and 6 periods work very well as a filter.

Comments:

This strategy works very well in Daily charts but can be applied in other chart times as well. As this is a strategy to catch market fluctuations, it presents different results with different stocks.

I have been applying this strategy to the stocks of the Brazilian market (BOVESPA) and have enjoyed the result. Every day I evaluate the stocks that are generating entry signals and choose which one to trade based on the stocks with the highest Profit Value.

The RSI 2 averaging filter probably will reduce profit of the backtests because reduces the number of signals, but the Profit Value will usually increase. For me this was a good thing because without the filter, this strategy usually shows more signals than I have capital to allocate.

Before entering a trade I look at which fast average the paper has the highest Profit Value and then I use this average as my output signal for that trade (this change has greatly improved the result of the outputs).

This strategy does not use Stop Loss because normally Stop Loss decreases effectiveness (profit). In any case, the option to apply a percentage Stop Loss if desired is added in the script. As the strategy does not use stop, extra caution with risk management is advisable. I advise not to allocate more than 20% of the trade capital in the same operation.

I'm still studying ways to improve this strategy, but so far this is the best setup I've found. Suggestions are always welcome and we can test to see if they improve the backtest result.

Good luck and good trades.

================================================

Backtest das estratégia do IFR de 2 períodos descrita em varios livros do trader Larry Connors . Esta estratégia usa um IFR de 2 períodos, uma média movel aritmética lenta e uma média movel aritmética rápida.

Sinal de entrada:

- Valor do IFR 2 abaixo do nível de sobrevenda (Larry Connors usualmente define sobrevenda sendo abaixo de 5, mas outros autores preferem trabalhar abaixo de 10 devido ao maior número de sinais).

- Fechamento acima da média lenta (200 períodos).

- Realizado a compra no fechamento do candle ou na abertura do candle seguinte.

Sinal de saída:

- Ocorre quando o candle fecha acima da média rápida (a média rápida mais comum é a de 5 períodos, mas alguns traders sugerem também a média de 10 períodos).

Filtro para entrada (modificação feita por mim):

- Aplicado uma média móvel aritmética do IFR2 para suavisar as oscilações.

- Realizado a entrada apenas quando o IFR2 está abaixo do nível de sobrevenda e a média móvel do IFR2 está abaixo de 30.

*OBS: nos ativos que avalio diariamente as médias de 4 e 6 períodos funcionam muito bem como filtro.

Comentários:

Esta estratégia funciona muito bem no tempo gráfico Diário mas pode ser aplicada tambem em outros tempos gráficos. Como trata-se de uma estratégia para pegar oscilações do mercado, ela apresenta diferentes resultados com diferentes ativos.

Eu venho aplicando esta estratégia nos ativos do mercado brasileiro (BOVESPA) e tenho gostado do resultado. Diariamente eu avalio os papeis que estão gerando entrada e escolho qual irei realizar o trade baseado nos papeis que apresentam maior Profit Value.

O filtro da média do IFR 2 reduz o lucro nos backtests pois reduz também a quantidade de sinais, mas em compensação o Profit Value irá normalmente aumentar. Para mim isto foi algo positivo pois, sem o filtro, normalmente esta estratégia apresenta mais sinais do que possuo capital para alocar.

Antes de entrar em um trade eu olho em qual média rápida o papel apresenta maior Profit Value e então eu utilizo está média como meu sinal de saída para aquele trade (esta mudança tem melhorado bastante o resultado das saídas).

Está estratégia não utiliza Stop Loss pois normalmente o Stop Loss diminui a eficácia (lucro). De qualquer maneira, foi acrescentado no script a opção de aplicar um Stop Loss percentual caso seja desejado. Como a estratégia não utiliza stop é aconselhável um cuidado redobrado com o gerenciamento de risco. Eu aconselho não alocar mais de 20% do capital de trade em uma mesma operação.

Ainda estou estudando formas de melhorar esta estratégia, mas até o momento está é a melhor configuração que encontrei. Sugestões são sempre bem vindas e podemos testar para verificar se melhoram o resultado do backtest.

Boa sorte e bons trades.

Pinescript v3 Compatibility Framework (v4 Migration Tool)Pinescript v3 Compatibility Framework (v4 Migration Tool)

This code makes most v3 scripts work in v4 with only a few minor changes below. Place the framework code before the first input statement.

You can totally delete all comments.

Pros:

- to port to v4 you only need to make a few simple changes, not affecting the core v3 code functionality

Cons:

- without #include - large redundant code block, but can be reduced as needed

- no proper syntax highlighting, intellisence for substitute constant names

Make the following changes in v3 script:

1. standard types can't be var names, color_transp can't be in a function, rename in v3 script:

color() => color.new()

bool => bool_

integer => integer_

float => float_

string => string_

2. init na requires explicit type declaration