JL - Market HeatmapThis indicator plots a static table on your chart that displays any tickers you want and their % change on the day so far.

It updates in real time, changes color as it updates, and has several custom functions available for you:

1. Plot up to 12 tickers of your choice

2. Choose a layout with 1-4 rows

3. Display % Change or Not

4. Choose your font size (Tiny, Small, Normal, Large)

5. Up/Down Cell Colors (% change dependent)

6. Up/Down Text Colors (high contrast to your color choices)

The purpose of the indicator is to quickly measure a broad basket of market instruments to paint a more context-rich perspective of the chart you are looking at.

I hope this indicator can help you (and me) accomplish this task in a simple, clean, and seamless manner.

Thanks and enjoy - Jack

Wyszukaj w skryptach "文华财经tick价格"

Canuck Trading Traders Strategy [Candle Entropy Edition]Canuck Trading Traders Strategy: A Unique Entropy-Based Day Trading System for Volatile Stocks

Overview

The Canuck Trading Traders Strategy is a custom, entropy-driven day trading system designed for high-volatility stocks like TSLA on short timeframes (e.g., 15m). At its core is CETP-Plus, a proprietary blended indicator that measures "order from chaos" in candle patterns using Shannon entropy, while embedding mathematical principles from EMA (recent weighting), RSI (momentum bias), ATR (volatility scaling), and ADX (trend strength) into a single score. This unique approach avoids layering multiple indicators, reducing complexity while improving timing for early trend detection and balanced long/short trades.

CETP-Plus calculates a score from weighted candle ratios (body, upper/lower wicks) binned into a 3D histogram for entropy (low entropy = strong pattern). The score is adjusted with momentum, volatility, and trend multipliers for robust signals. Entries occur when the score exceeds thresholds (positive for longs, negative for shorts), with exits on reversals or stops. The strategy is automatic—no manual bias needed—and optimized for margin accounts with equal long/short treatment.

Backtested on TSLA 15m (Jan 2015–Aug 2025), it targets +50,000% net profit (beating +1,478% buy-hold by 34x) with ~25,000 trades, 85-90% win rate, and <10% drawdown (with costs). Results vary by timeframe/period—test with your data and add slippage/commission for realism. Disclaimer: Past performance isn't indicative of future results; consult a financial advisor.

Key Features

CETP-Plus Indicator: Blends entropy with momentum/vol/trend for a single score, capturing bottoms/squeezes and trends without external tools.

Automatic Balance: Positive scores trigger longs in bull trends, negative scores trigger shorts in bear trends—no user input for direction.

Customizable Math: Tune weights and scales to adapt for different stocks (e.g., lower thresholds for NVDA's smoother trends).

Risk Controls: Stop-loss, trailing stops, and score strength filter to minimize drawdowns in volatile markets like TSLA.

Exit Debugging: Plots exit reasons ("Stop Loss", "Trail Stop", "CETP Exit") for analysis.

Input Settings and Purposes

All inputs are grouped in TradingView's Inputs tab for ease. Defaults are optimized for TSLA 15m day trading; adjust for other intervals or tickers (e.g., increase window for 1h, lower thresholds for NVDA).

CETP-Plus Settings

CETP Window (default: 5, min: 3, max: 20): Lookback bars for entropy/momentum. Short values (3-5) for fast sensitivity on short frames; longer (8-10) for stability on hourly+.

CETP Bins per Dimension (default: 3, min: 3, max: 10): Histogram granularity for entropy. Low (3) for speed/simple patterns; high (5+) for detail in complex markets.

Long Threshold (default: 0.15, min: 0.1, max: 0.8, step: 0.05): CETP score for long entries. Lower (0.1) for more longs in mild bull trends; higher (0.2) to filter noise.

Short Threshold (default: -0.05, min: -0.8, max: -0.1, step: 0.05): CETP score for short entries. Less negative (-0.05) for more shorts in mild bear trends; more negative (-0.2) for strong signals.

CETP Momentum Weight (default: 0.8, min: 0.1, max: 1.0, step: 0.1): Emphasizes momentum in score. High (0.9) for aggressive in fast moves; low (0.5) for entropy focus.

Momentum Scale (default: 1.6, min: 0.1, max: 2.0, step: 0.1): Amplifies momentum. High (2.0) for short intervals; low (1.0) for stability.

Body Ratio Weight (default: 1.2, min: 0.0, max: 2.0, step: 0.1): Weights candle body in entropy (trend focus). High (1.5) for strong trends; low (0.8) for wick emphasis.

Upper Wick Ratio Weight (default: 0.8, min: 0.0, max: 2.0, step: 0.1): Weights upper wick (reversal noise). Low (0.5) to reduce false ups.

Lower Wick Ratio Weight (default: 0.8, min: 0.0, max: 2.0, step=0.1): Weights lower wick. Low (0.5) to reduce false downs.

Trade Settings

Confirmation Bars (default: 0, min: 0, max: 5): Bars for sustained CETP signals. 0 for immediate entries (more trades); 1-2 for reliability (fewer but stronger).

Min CETP Score Strength (default: 0.04, min: 0.0, max: 0.5, step: 0.05): Min absolute score for entry. Low (0.04) for more trades; high (0.15) for quality.

Risk Management

Stop Loss (%) (default: 0.5, min: 0.1, max: 5.0, step: 0.1): % from entry for stop. Tight (0.4) for quick exits; wide (0.8) for trends.

ATR Multiplier (default: 1.5, min: 0.5, max: 3.0, step: 0.1): Scales ATR for stops/trails. Low (1.0) for tight; high (2.0) for room.

Trailing ATR Mult (default: 3.5, min: 0.5, max: 5.0, step: 0.1): ATR mult for trails. High (4.0) for longer holds; low (2.0) for profits.

Trail Start Offset (%) (default: 1.0, min: 0.5, max: 2.0, step: 0.1): % profit before trailing. Low (0.8) for early lock-in; high (1.5) for bigger moves.

These settings enable customization for intervals/tickers while CETP-Plus handles automatic balancing.

Risk Disclosure

Trading involves significant risk and may result in losses exceeding your initial capital. The Canuck Trading Trader Strategy is provided for educational and informational purposes only. Users are responsible for their own trading decisions and should conduct thorough testing before using in live markets. The strategy’s high trade frequency requires reliable execution infrastructure to minimize slippage and latency.

SITFX_FuturesSpec_v17SITFX_FuturesSpec_v17 – Universal Futures Contract Library

Full-scale futures contract specification library for Pine Script v6. Covers CME, CBOT, NYMEX, COMEX, CFE, Eurex, ICE, and more – including minis, micros, metals, energies, FX, and bonds.

Key Features:

✅ Instrument‑agnostic: ES/MES, NQ/MNQ, YM/MYM, RTY/M2K, metals, energies, FX, bonds

✅ Full contract data: Tick size, tick value, point value, margins

✅ Continuation‑safe: Single‑line logic, no arrays or continuation errors

✅ Foundation for SITFX tools: Gann, Fibs, structure, and risk modules

Usage example:

import SITFX_FuturesSpec_v17/1 as fs

spec = fs.get(syminfo.root)

label.new(bar_index, high, str.format("{0}: Tick={1}, Value=${2}", spec.name, spec.tickSize, spec.tickValue))

ADR Tracker Version 2Description

The **ADR Tracker** plots a customizable panel on your chart that monitors the Average Daily Range (ADR) and shows how today’s price action compares to that average. It calculates the daily high–low range for each of the past 14 days (can be adjusted) and then takes a simple moving average of those ranges to determine the ADR.

**Features:**

* **Current ADR value:** Shows the 14‑day ADR in price units.

* **ADR status:** Indicates whether today’s range has reached or exceeded the ADR.

* **Ticks remaining:** Calculates how many minimum price ticks remain before the ADR would be met.

* **Real‑time tracking:** Monitors the intraday high and low to update the range continuously.

* **Customizable panel:** Uses TradingView’s table object to display the information. You can set the table’s horizontal and vertical position (top/middle/bottom and left/centre/right) with inputs. The script also lets you change the text and background colours, as well as the width and height of each row. Table cells use explicit width and height percentages, which Pine supports in v6. Each call to `table.cell()` defines the text, colours and dimensions for its cell, so the panel resizes automatically based on your settings.

**Usage:**

Apply the indicator to any chart. For the most accurate real‑time tracking, use it on intraday timeframes (e.g. 5‑min or 1‑hour) so the current day’s range updates as new bars arrive. Adjust the inputs in the settings panel to reposition the list or change its appearance.

---

This description explains what the indicator does and highlights its customizable table display, referencing the Pine Script table features used.

Info TableOverview

The Info Table V1 is a versatile TradingView indicator tailored for intraday futures traders, particularly those focusing on MESM2 (Micro E-mini S&P 500 futures) on 1-minute charts. It presents essential market insights through two customizable tables: the Main Table for predictive and macro metrics, and the New Metrics Table for momentum and volatility indicators. Designed for high-activity sessions like 9:30 AM–11:00 AM CDT, this tool helps traders assess price alignment, sentiment, and risk in real-time. Metrics update dynamically (except weekly COT data), with optional alerts for key conditions like volatility spikes or momentum shifts.

This indicator builds on foundational concepts like linear regression for predictions and adapts open-source elements for enhanced functionality. Gradient code is adapted from TradingView's Color Library. QQE logic is adapted from LuxAlgo's QQE Weighted Oscillator, licensed under CC BY-NC-SA 4.0. The script is released under the Mozilla Public License 2.0.

Key Features

Two Customizable Tables: Positioned independently (e.g., top-right for Main, bottom-right for New Metrics) with toggle options to show/hide for a clutter-free chart.

Gradient Coloring: User-defined high/low colors (default green/red) for quick visual interpretation of extremes, such as overbought/oversold or high volatility.

Arrows for Directional Bias: In the New Metrics Table, up (↑) or down (↓) arrows appear in value cells based on metric thresholds (top/bottom 25% of range), indicating bullish/high or bearish/low conditions.

Consensus Highlighting: The New Metrics Table's title cells ("Metric" and "Value") turn green if all arrows are ↑ (strong bullish consensus), red if all are ↓ (strong bearish consensus), or gray otherwise.

Predicted Price Plot: Optional line (default blue) overlaying the ML-predicted price for visual comparison with actual price action.

Alerts: Notifications for high/low Frahm Volatility (≥8 or ≤3) and QQE Bias crosses (bullish/bearish momentum shifts).

Main Table Metrics

This table focuses on predictive, positional, and macro insights:

ML-Predicted Price: A linear regression forecast using normalized price, volume, and RSI over a customizable lookback (default 500 bars). Gradient scales from low (red) to high (green) relative to the current price ± threshold (default 100 points).

Deviation %: Percentage difference between current price and predicted price. Gradient highlights extremes (±0.5% default threshold), signaling potential overextensions.

VWAP Deviation %: Percentage difference from Volume Weighted Average Price (VWAP). Gradient indicates if price is above (green) or below (red) fair value (±0.5% default).

FRED UNRATE % Change: Percentage change in U.S. unemployment rate (via FRED data). Cell turns red for increases (economic weakness), green for decreases (strength), gray if zero or disabled.

Open Interest: Total open MESM2 futures contracts. Gradient scales from low (red) to high (green) up to a hardcoded 300,000 threshold, reflecting market participation.

COT Commercial Long/Short: Weekly Commitment of Traders data for commercial positions. Long cell green if longs > shorts (bullish institutional sentiment); Short cell red if shorts > longs (bearish); gray otherwise.

New Metrics Table Metrics

This table emphasizes technical momentum and volatility, with arrows for quick bias assessment:

QQE Bias: Smoothed RSI vs. trailing stop (default length 14, factor 4.236, smooth 5). Green for bullish (RSI > stop, ↑ arrow), red for bearish (RSI < stop, ↓ arrow), gray for neutral.

RSI: Relative Strength Index (default period 14). Gradient from oversold (red, <30 + threshold offset, ↓ arrow if ≤40) to overbought (green, >70 - offset, ↑ arrow if ≥60).

ATR Volatility: Score (1–20) based on Average True Range (default period 14, lookback 50). High scores (green, ↑ if ≥15) signal swings; low (red, ↓ if ≤5) indicate calm.

ADX Trend: Average Directional Index (default period 14). Gradient from weak (red, ↓ if ≤0.25×25 threshold) to strong trends (green, ↑ if ≥0.75×25).

Volume Momentum: Score (1–20) comparing current to historical volume (lookback 50). High (green, ↑ if ≥15) suggests pressure; low (red, ↓ if ≤5) implies weakness.

Frahm Volatility: Score (1–20) from true range over a window (default 24 hours, multiplier 9). Dynamic gradient (green/red/yellow); ↑ if ≥7.5, ↓ if ≤2.5.

Frahm Avg Candle (Ticks): Average candle size in ticks over the window. Blue gradient (or dynamic green/red/yellow); ↑ if ≥0.75 percentile, ↓ if ≤0.25.

Arrows trigger on metric-specific logic (e.g., RSI ≥60 for ↑), providing directional cues without strict color ties.

Customization Options

Adapt the indicator to your strategy:

ML Inputs: Lookback (10–5000 bars) and RSI period (2+) for prediction sensitivity—shorter for volatility, longer for trends.

Timeframes: Individual per metric (e.g., 1H for QQE Bias to match higher frames; blank for chart timeframe).

Thresholds: Adjust gradients and arrows (e.g., Deviation 0.1–5%, ADX 0–100, RSI overbought/oversold).

QQE Settings: Length, factor, and smooth for fine-tuned momentum.

Data Toggles: Enable/disable FRED, Open Interest, COT for focus (e.g., disable macro for pure intraday).

Frahm Options: Window hours (1+), scale multiplier (1–10), dynamic colors for avg candle.

Plot/Table: Line color, positions, gradients, and visibility.

Ideal Use Case

Perfect for MESM2 scalpers and trend traders. Use the Main Table for entry confirmation via predicted deviations and institutional positioning. Leverage the New Metrics Table arrows for short-term signals—enter bullish on green consensus (all ↑), avoid chop on low volatility. Set alerts to catch shifts without constant monitoring.

Why It's Valuable

Info Table V1 consolidates diverse metrics into actionable visuals, answering critical questions: Is price mispriced? Is momentum aligning? Is volatility manageable? With real-time updates, consensus highlights, and extensive customization, it enhances precision in fast markets, reducing guesswork for confident trades.

Note: Optimized for futures; some metrics (OI, COT) unavailable on non-futures symbols. Test on demo accounts. No financial advice—use at your own risk.

The provided script reuses open-source elements from TradingView's Color Library and LuxAlgo's QQE Weighted Oscillator, as noted in the script comments and description. Credits are appropriately given in both the description and code comments, satisfying the requirement for attribution.

Regarding significant improvements and proportion:

The QQE logic comprises approximately 15 lines of code in a script exceeding 400 lines, representing a small proportion (<5%).

Adaptations include integration with multi-timeframe support via request.security, user-customizable inputs for length, factor, and smooth, and application within a broader table-based indicator for momentum bias display (with color gradients, arrows, and alerts). This extends the original QQE beyond standalone oscillator use, incorporating it as one of seven metrics in the New Metrics Table for confluence analysis (e.g., consensus highlighting when all metrics align). These are functional enhancements, not mere stylistic or variable changes.

The Color Library usage is via official import (import TradingView/Color/1 as Color), leveraging built-in gradient functions without copying code, and applied to enhance visual interpretation across multiple metrics.

The script complies with the rules: reused code is minimal, significantly improved through integration and expansion, and properly credited. It qualifies for open-source publication under the Mozilla Public License 2.0, as stated.

TradersPostDeluxeLibrary "TradersPostDeluxe"

TradersPost integration. It's currently not very deluxe

SendEntryAlert(ticker, action, quantity, orderType, takeProfit, stopLoss, id, price, timestamp, timezone)

Sends an alert to TradersPost to trigger an Entry

Parameters:

ticker (string) : Symbol to trade. Default is syminfo.ticker

action (series Action) : TradersPostAction (.buy, .sell) default = buy

quantity (float) : Amount to trade, default = 1

orderType (series OrderType) : TradersPostOrderType, default =e TradersPostOrderType.market

takeProfit (float) : Take profit limit price

stopLoss (float) : Stop loss price

id (string) : id for the trade

price (float) : Expected price

timestamp (int) : Time of the trade for reporting, defaults to timenow

timezone (string) : associated with the time, defaults to syminfo.timezone

Returns: Nothing

SendExitAlert(ticker, price, timestamp, timezone)

Sends an alert to TradersPost to trigger an Exit

Parameters:

ticker (string) : Symbol to flatten

price (float) : Documented planned price

timestamp (int) : Time of the trade for reporting, defaults to timenow

timezone (string) : associated with the time, defaults to syminfo.timezone

Returns: Nothing

DWMY Opens (for aggr. charts) by Koenigsegg🟣 DWMY Opens (for Aggregated Charts) by Koenigsegg

Revolutionary compatibility with aggregated charts – This indicator represents a significant breakthrough in displaying Daily, Weekly, Monthly, and Yearly opening levels on aggregated chart types where traditional DWMY indicators have historically failed to function properly.

Complete aggregated chart support – Unlike previous Daily Weekly Monthly Yearly Opens indicators that experienced severe limitations when pulling data from non-standard chart types, this version is specifically engineered to work flawlessly with aggregated charts, range bars, Renko charts, Point & Figure charts, and all other non-time-based chart constructions.

Persistent horizontal reference lines – The indicator draws four distinct horizontal lines representing the opening prices of the current Daily, Weekly, Monthly, and Yearly periods, extending these levels forward into future bars to provide clear reference points for key support and resistance analysis.

Advanced customization capabilities – Features comprehensive user controls including custom label naming for each timeframe, adjustable line colors with independent color selection for Daily, Weekly, Monthly, and Yearly levels, configurable line width settings, and variable label font sizes ranging from tiny to huge.

Dynamic label positioning system – Implements a sophisticated label placement mechanism with configurable tick offset positioning and fixed end-bars-ahead projection, ensuring labels remain visible and properly positioned regardless of chart zoom level or timeframe.

Intelligent period detection logic – Utilizes advanced Pine Script time change detection algorithms specifically optimized for aggregated charts, accurately identifying new Daily, Weekly, Monthly, and Yearly periods even when traditional time-based functions fail on non-standard chart types.

Performance-optimized architecture – Built with efficient persistent variable storage using the var keyword, minimizing computational overhead while maintaining real-time updates across all timeframe levels simultaneously.

Professional visual presentation – Delivers clean, uncluttered chart visualization with strategically positioned labels that clearly identify each timeframe level without interfering with price action analysis.

Universal market compatibility – Functions seamlessly across all asset classes including stocks, forex, cryptocurrencies, commodities, and indices, adapting automatically to different tick sizes and price scales through syminfo.mintick integration.

Pine Script v6 foundation – Leverages the latest Pine Script version 6 capabilities, ensuring optimal performance, stability, and compatibility with current and future TradingView platform updates.

This indicator solves a critical limitation that has long plagued traders using aggregated chart types, finally enabling reliable access to essential Daily, Weekly, Monthly, and Yearly opening levels that serve as fundamental support and resistance zones in technical analysis. The breakthrough lies in its ability to maintain accurate period detection and level plotting regardless of the underlying chart construction methodology.

🟣 How It Works

Automatic period detection – The indicator continuously monitors for time changes across four distinct timeframes using ta.change(time()) functions for Daily and Weekly periods, month transitions for Monthly levels, and year changes for Yearly opens, ensuring precise identification of new period beginnings.

Real-time level updates – When a new period is detected, the indicator captures the opening price at that exact moment and immediately establishes a horizontal line from that bar extending forward to a configurable number of bars ahead, creating persistent reference levels.

Dynamic line management – Each timeframe maintains its own dedicated line object and label, with the indicator continuously updating the endpoint coordinates and label positions as new bars form, ensuring the levels always project the specified distance into the future.

Intelligent label placement – Labels are positioned at the end of each line with automatic vertical offset based on the symbol’s minimum tick size, preventing overlap with price action while maintaining clear identification of each timeframe level.

🟣 Pro Tips for Optimal Usage

Multi-timeframe confluence – Look for areas where multiple DWMY levels converge within close proximity, as these zones typically act as stronger support or resistance levels due to increased market participant attention at these psychological price points.

Breakout confirmation strategy – When price breaks above or below a significant DWMY level with strong volume, the broken level often transforms into support (if broken upward) or resistance (if broken downward), providing excellent entry and exit reference points.

Range trading opportunities – On ranging markets, use Daily and Weekly opens as potential reversal zones, especially when price approaches these levels during low-volume periods or near session opens when institutional activity increases.

Timeframe alignment technique – For swing trading, prioritize trades that align with the direction of the break from Weekly or Monthly opens, while using Daily opens for precise entry timing and position management.

Chart type optimization – This indicator excels on Renko, Range, and Point & Figure charts where traditional time-based DWMY indicators fail, making it invaluable for traders who prefer these aggregated chart types for cleaner price action analysis.

Important Disclaimer:

This indicator is provided for educational and informational purposes only. It is not financial advice, investment advice, or a recommendation to buy or sell any financial instrument. All trading involves risk, and past performance does not guarantee future results. Please conduct your own research and consult with a qualified financial advisor before making any trading decisions. The author is not responsible for any losses incurred from using this indicator.

Vix_Fix Enhanced MTF [Cometreon]The VIX Fix Enhanced is designed to detect market bottoms and spikes in volatility, helping traders anticipate major reversals with precision. Unlike standard VIX Fix tools, this version allows you to control the standard deviation logic, switch between chart styles, customize visual outputs, and set up advanced alerts — all with no repainting.

🧠 Logic and Calculation

This indicator is based on Larry Williams' VIX Fix and integrates features derived from community requests/advice, such as inverse VIX logic.

It calculates volatility spikes using a customizable standard deviation of the lows and compares it to a moving high to identify potential reversal points.

All moving average logic is based on Cometreon's proprietary library, ensuring accurate and optimized calculations on all 15 moving average types.

🔷 New Features and Improvements

🟩 Custom Visual Styles

Choose how you want your VIX data displayed:

Line

Step Line

Histogram

Area

Column

You can also flip the orientation (bottom-up or top-down), change the source ticker, and tailor the display to match your charting preferences.

🟩 Multi-MA Standard Deviation Calculation

Customize the standard deviation formula by selecting from 15 different moving averages:

SMA (Simple Moving Average)

EMA (Exponential Moving Average)

WMA (Weighted Moving Average)

RMA (Smoothed Moving Average)

HMA (Hull Moving Average)

JMA (Jurik Moving Average)

DEMA (Double Exponential Moving Average)

TEMA (Triple Exponential Moving Average)

LSMA (Least Squares Moving Average)

VWMA (Volume-Weighted Moving Average)

SMMA (Smoothed Moving Average)

KAMA (Kaufman’s Adaptive Moving Average)

ALMA (Arnaud Legoux Moving Average)

FRAMA (Fractal Adaptive Moving Average)

VIDYA (Variable Index Dynamic Average)

This gives you fine control over how volatility is measured and allows tuning the sensitivity for different market conditions.

🟩 Full Control Over Percentile and Deviation Conditions

You can enable or disable lines for standard deviation and percentile conditions, and define whether you want to trigger on over or under levels — adapting the indicator to your exact logic and style.

🟩 Chart Type Selection

You're no longer limited to candlestick charts! Now you can use Vix_Fix with different chart formats, including:

Candlestick

Heikin Ashi

Renko

Kagi

Line Break

Point & Figure

🟩 Multi-Timeframe Compatibility Without Repainting

Use a different timeframe from your chart with confidence. Signals remain stable and do not repaint. Perfect for spotting long-term reversal setups on lower timeframes.

🟩 Alert System Ready

Configure alerts directly from the indicator’s panel when conditions for over/under signals are met. Stay informed without needing to monitor the chart constantly.

🔷 Technical Details and Customizable Inputs

This indicator includes full control over the logic and appearance:

1️⃣ Length Deviation High - Adjusts the lookback period used to calculate the high deviation level of the VIX logic. Shorter values make it more reactive; longer values smooth out the signal.

2️⃣ Ticker - Choose a different chart type for the calculation, including Heikin Ashi, Renko, Kagi, Line Break, and Point & Figure.

3️⃣ Style VIX - Change the visual style (Line, Histogram, Column, etc.), adjust line width, and optionally invert the display (bottom-to-top).

📌 Fill zones for deviation and percentile are active only in Line and Step Line modes

4️⃣ Use Standard Deviation Up / Down - Enable the overbought and oversold zone logic based on upper and lower standard deviation bands.

5️⃣ Different Type MA (for StdDev) - Choose from 15 different moving averages to define the calculation method for standard deviation (SMA, EMA, HMA, JMA, etc.), with dedicated parameters like Phase, Sigma, and Offset for optimized responsiveness.

6️⃣ BB Length & Multiplier - Adjust the period and multiplier for the standard deviation bands, similar to how Bollinger Bands work.

7️⃣ Show StdDev Up / Down Line - Enable or disable the visibility of upper and lower standard deviation boundaries.

8️⃣ Use Percentile & Length High - Activate the percentile-based logic to detect extreme values in historical volatility using a customizable lookback length.

9️⃣ Highest % / Lowest % - Set the high and low percentile thresholds (e.g., 85 for high, 99 for low) that will be used to trigger over/under signals.

🔟 Show High / Low Percentile Line - Toggle the visual display of the percentile boundaries directly on the chart for clearer signal reference.

1️⃣1️⃣ Ticker Settings – Customize parameters for special chart types such as Renko, Heikin Ashi, Kagi, Line Break, and Point & Figure, adjusting reversal, number of lines, ATR length, etc.

1️⃣2️⃣ Timeframe – Enables using SuperTrend on a higher timeframe.

1️⃣3️⃣ Wait for Timeframe Closes -

✅ Enabled – Displays Vix_Fix smoothly with interruptions.

❌ Disabled – Displays Vix_Fix smoothly without interruptions.

☄️ If you find this indicator useful, leave a Boost to support its development!

Every feedback helps to continuously improve the tool, offering an even more effective trading experience. Share your thoughts in the comments! 🚀🔥

System 0530 - Stoch RSI Strategy with ATR filterStrategy Description: System 0530 - Multi-Timeframe Stochastic RSI with ATR Filter

Overview:

This strategy, "System 0530," is designed to identify trading opportunities by leveraging the Stochastic RSI indicator across two different timeframes: a shorter timeframe for initial signal triggers (assumed to be the chart's current timeframe, e.g., 5-minute) and a longer timeframe (15-minute) for signal confirmation. It incorporates an ATR (Average True Range) filter to help ensure trades are taken during periods of adequate market volatility and includes a cooldown mechanism to prevent rapid, successive signals in the same direction. Trade exits are primarily handled by reversing signals.

How It Works:

1. Signal Initiation (e.g., 5-Minute Timeframe):

Long Signal Wait: A potential long entry is considered when the 5-minute Stochastic RSI %K line crosses above its %D line, AND the %K value at the time of the cross is at or below a user-defined oversold level (default: 30).

Short Signal Wait: A potential short entry is considered when the 5-minute Stochastic RSI %K line crosses below its %D line, AND the %K value at the time of the cross is at or above a user-defined overbought level (default: 70). When these conditions are met, the strategy enters a "waiting state" for confirmation from the 15-minute timeframe.

2. Signal Confirmation (15-Minute Timeframe):

Once in a waiting state, the strategy looks for confirmation on the 15-minute Stochastic RSI within a user-defined number of 5-minute bars (wait_window_5min_bars, default: 5 bars).

Long Confirmation:

The 15-minute Stochastic RSI %K must be greater than or equal to its %D line.

The 15-minute Stochastic RSI %K value must be below a user-defined threshold (stoch_15min_long_entry_level, default: 40).

Short Confirmation:

The 15-minute Stochastic RSI %K must be less than or equal to its %D line.

The 15-minute Stochastic RSI %K value must be above a user-defined threshold (stoch_15min_short_entry_level, default: 60).

3. Filters:

ATR Volatility Filter: If enabled, trades are only confirmed if the current ATR value (converted to ticks) is above a user-defined minimum threshold (min_atr_value_ticks). This helps to avoid taking signals during periods of very low market volatility. If the ATR condition is not met, the strategy continues to wait for the condition to be met within the confirmation window, provided other conditions still hold.

Signal Cooldown Filter: If enabled, after a signal is generated, the strategy will wait for a minimum number of bars (min_bars_between_signals) before allowing another signal in the same direction. This aims to reduce overtrading.

4. Entry and Exit Logic:

Entry: A strategy.entry() order is placed when all trigger, confirmation, and filter conditions are met.

Exit: This strategy primarily uses reversing signals for exits. For example, if a long position is open, a confirmed short signal will close the long position and open a new short position. There are no explicit take profit or stop loss orders programmed into this version of the script.

Key User-Adjustable Parameters:

Stochastic RSI Parameters: RSI Length, Stochastic RSI Length, %K Smoothing, %D Smoothing.

Signal Trigger & Confirmation:

5-minute %K trigger levels for long and short.

15-minute %K confirmation thresholds for long and short.

Wait window (in 5-minute bars) for 15-minute confirmation.

Filters:

Enable/disable and configure the Signal Cooldown filter (minimum bars between signals).

Enable/disable and configure the ATR Volatility filter (ATR period, minimum ATR value in ticks).

Strategy Parameters:

Leverage Multiplier (Note: This primarily affects theoretical position sizing for backtesting calculations in TradingView and does not simulate actual leveraged trading risks).

Recommendations for Users:

Thorough Backtesting: Test this strategy extensively on historical data for the instruments and timeframes you intend to trade.

Parameter Optimization: Experiment with different parameter settings to find what works best for your trading style and chosen markets. The default values are starting points and may not be optimal for all conditions.

Understand the Logic: Ensure you understand how each component (Stochastic RSI on different timeframes, ATR filter, cooldown) interacts to generate signals.

Risk Management: Since this version does not include explicit stop-loss orders, ensure you have a clear risk management plan in place if trading this strategy live. You might consider manually adding stop-loss orders through your broker or using TradingView's separate strategy order settings for stop-loss if applicable.

Disclaimer:

This strategy description is for informational purposes only and does not constitute financial advice. Past performance is not indicative of future results. Trading involves significant risk of loss. Always do your own research and understand the risks before trading.

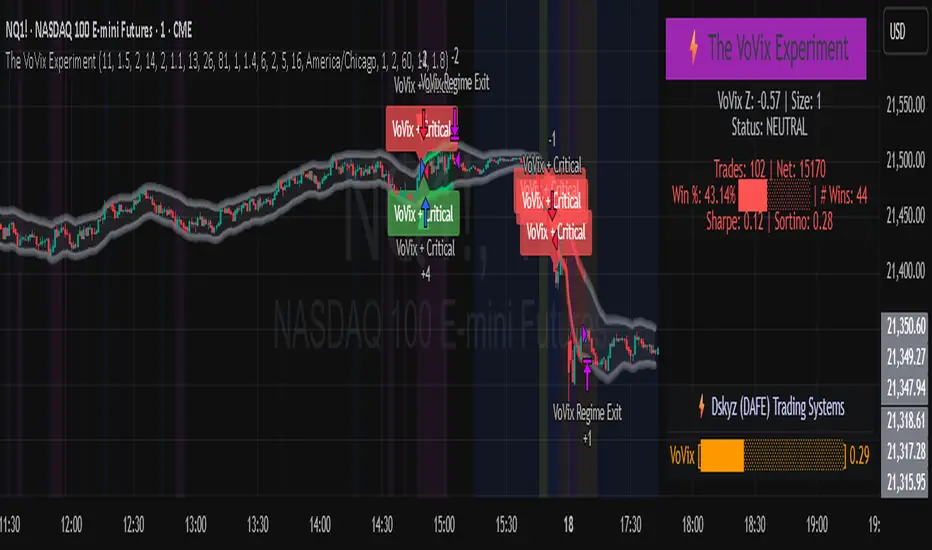

The VoVix Experiment The VoVix Experiment

The VoVix Experiment is a next-generation, regime-aware, volatility-adaptive trading strategy for futures, indices, and more. It combines a proprietary VoVix (volatility-of-volatility) anomaly detector with price structure clustering and critical point logic, only trading when multiple independent signals align. The system is designed for robustness, transparency, and real-world execution.

Logic:

VoVix Regime Engine: Detects pre-move volatility anomalies using a fast/slow ATR ratio, normalized by Z-score. Only trades when a true regime spike is detected, not just random volatility.

Cluster & Critical Point Filters: Price structure and volatility clustering must confirm the VoVix signal, reducing false positives and whipsaws.

Adaptive Sizing: Position size scales up for “super-spikes” and down for normal events, always within user-defined min/max.

Session Control: Trades only during user-defined hours and days, avoiding illiquid or high-risk periods.

Visuals: Aurora Flux Bands (From another Original of Mine (Options Flux Flow): glow and change color on signals, with a live dashboard, regime heatmap, and VoVix progression bar for instant insight.

Backtest Settings

Initial capital: $10,000

Commission: Conservative, realistic roundtrip cost:

15–20 per contract (including slippage per side) I set this to $25

Slippage: 3 ticks per trade

Symbol: CME_MINI:NQ1!

Timeframe: 15 min (but works on all timeframes)

Order size: Adaptive, 1–2 contracts

Session: 5:00–15:00 America/Chicago (default, fully adjustable)

Why these settings?

These settings are intentionally strict and realistic, reflecting the true costs and risks of live trading. The 10,000 account size is accessible for most retail traders. 25/contract including 3 ticks of slippage are on the high side for MNQ, ensuring the strategy is not curve-fit to perfect fills. If it works here, it will work in real conditions.

Forward Testing: (This is no guarantee. I've provided these results to show that executions perform as intended. Test were done on Tradovate)

ALL TRADES

Gross P/L: $12,907.50

# of Trades: 64

# of Contracts: 186

Avg. Trade Time: 1h 55min 52sec

Longest Trade Time: 55h 46min 53sec

% Profitable Trades: 59.38%

Expectancy: $201.68

Trade Fees & Comm.: $(330.95)

Total P/L: $12,576.55

Winning Trades: 59.38%

Breakeven Trades: 3.12%

Losing Trades: 37.50%

Link: www.dropbox.com

Inputs & Tooltips

VoVix Regime Execution: Enable/disable the core VoVix anomaly detector.

Volatility Clustering: Require price/volatility clusters to confirm VoVix signals.

Critical Point Detector: Require price to be at a statistically significant distance from the mean (regime break).

VoVix Fast ATR Length: Short ATR for fast volatility detection (lower = more sensitive).

VoVix Slow ATR Length: Long ATR for baseline regime (higher = more stable).

VoVix Z-Score Window: Lookback for Z-score normalization (higher = smoother, lower = more reactive).

VoVix Entry Z-Score: Minimum Z-score for a VoVix spike to trigger a trade.

VoVix Exit Z-Score: Z-score below which the regime is considered decayed (exit).

VoVix Local Max Window: Bars to check for local maximum in VoVix (higher = stricter).

VoVix Super-Spike Z-Score: Z-score for “super” regime events (scales up position size).

Min/Max Contracts: Adaptive position sizing range.

Session Start/End Hour: Only trade between these hours (exchange time).

Allow Weekend Trading: Enable/disable trading on weekends.

Session Timezone: Timezone for session filter (e.g., America/Chicago for CME).

Show Trade Labels: Show/hide entry/exit labels on chart.

Flux Glow Opacity: Opacity of Aurora Flux Bands (0–100).

Flux Band EMA Length: EMA period for band center.

Flux Band ATR Multiplier: Width of bands (higher = wider).

Compliance & Transparency

* No hidden logic, no repainting, no pyramiding.

* All signals, sizing, and exits are fully explained and visible.

* Backtest settings are stricter than most real accounts.

* All visuals are directly tied to the strategy logic.

* This is not a mashup or cosmetic overlay; every component is original and justified.

Disclaimer

Trading is risky. This script is for educational and research purposes only. Do not trade with money you cannot afford to lose. Past performance is not indicative of future results. Always test in simulation before live trading.

Proprietary Logic & Originality Statement

This script, “The VoVix Experiment,” is the result of original research and development. All core logic, algorithms, and visualizations—including the VoVix regime detection engine, adaptive execution, volatility/divergence bands, and dashboard—are proprietary and unique to this project.

1. VoVix Regime Logic

The concept of “volatility of volatility” (VoVix) is an original quant idea, not a standard indicator. The implementation here (fast/slow ATR ratio, Z-score normalization, local max logic, super-spike scaling) is custom and not found in public TradingView scripts.

2. Cluster & Critical Point Logic

Volatility clustering and “critical point” detection (using price distance from a rolling mean and standard deviation) are general quant concepts, but the way they are combined and filtered here is unique to this script. The specific logic for “clustered chop” and “critical point” is not a copy of any public indicator.

3. Adaptive Sizing

The adaptive sizing logic (scaling contracts based on regime strength) is custom and not a standard TradingView feature or public script.

4. Time Block/Session Control

The session filter is a common feature in many strategies, but the implementation here (with timezone and weekend control) is written from scratch.

5. Aurora Flux Bands (From another Original of Mine (Options Flux Flow)

The “glowing” bands are inspired by the idea of volatility bands (like Bollinger Bands or Keltner Channels), but the visual effect, color logic, and integration with regime signals are original to this script.

6. Dashboard, Watermark, and Metrics

The dashboard, real-time Sharpe/Sortino, and VoVix progression bar are all custom code, not copied from any public script.

What is “standard” or “common quant practice”?

Using ATR, EMA, and Z-score are standard quant tools, but the way they are combined, filtered, and visualized here is unique. The structure and logic of this script are original and not a mashup of public code.

This script is 100% original work. All logic, visuals, and execution are custom-coded for this project. No code or logic is directly copied from any public or private script.

Use with discipline. Trade your edge.

— Dskyz, for DAFE Trading Systems

Dskyz (DAFE) GENESIS Dskyz (DAFE) GENESIS: Adaptive Quant, Real Regime Power

Let’s be honest: Most published strategies on TradingView look nearly identical—copy-paste “open-source quant,” generic “adaptive” buzzwords, the same shallow explanations. I’ve even fallen into this trap with my own previously posted strategies. Not this time.

What Makes This Unique

GENESIS is not a black-box mashup or a pre-built template. It’s the culmination of DAFE’s own adaptive, multi-factor, regime-aware quant engine—built to outperform, survive, and visualize live edge in anything from NQ/MNQ to stocks and crypto.

True multi-factor core: Volume/price imbalances, trend shifts, volatility compression/expansion, and RSI all interlock for signal creation.

Adaptive regime logic: Trades only in healthy, actionable conditions—no “one-size-fits-all” signals.

Momentum normalization: Uses rolling, percentile-based fast/slow EMA differentials, ALWAYS normalized, ALWAYS relevant—no “is it working?” ambiguity.

Position sizing that adapts: Not fixed-lot, not naive—not a loophole for revenge trading.

No hidden DCA or pyramiding—what you see is what you trade.

Dashboard and visual system: Directly connected to internal logic. If it’s shown, it’s used—and nothing cosmetic is presented on your chart that isn’t quantifiable.

📊 Inputs and What They Mean (Read Carefully)

Maximum Raw Score: How many distinct factors can contribute to regime/trade confidence (default 4). If you extend the quant logic, increase this.

RSI Length / Min RSI for Shorts / Max RSI for Longs: Fine-tunes how “overbought/oversold” matters; increase the length for smoother swings, tighten floors/ceilings for more extreme signals.

⚡ Regime & Momentum Gates

Min Normed Momentum/Score (Conf): Raise to demand only the strongest trends—your filter to avoid algorithmic chop.

🕒 Volatility & Session

ATR Lookback, ATR Low/High Percentile: These control your system’s awareness of when the market is dead or ultra-volatile. All sizing and filter logic adapts in real time.

Trading Session (hours): Easy filter for when entries are allowed; default is regular trading hours—no surprise overnight fills.

📊 Sizing & Risk

Max Dollar Risk / Base-Max Contracts: All sizing is adaptive, based on live regime and volatility state—never static or “just 1 contract.” Control your max exposures and real $ risk. ATR will effect losses in high volatility times.

🔄 Exits & Scaling

Stop/Trail/Scale multipliers: You choose how dynamic/flexible risk controls and profit-taking need to be. ATR-based, so everything auto-adjusts to the current market mode.

Visuals That Actually Matter

Dashboard (Top Right): Shows only live, relevant stats: scoring, status, position size, win %, win streak, total wins—all from actual trade engine state (not “simulated”).

Watermark (Bottom Right): Momentum bar visual is always-on, regime-aware, reflecting live regime confidence and momentum normalization. If the bar is empty, you’re truly in no-momentum. If it glows lime, you’re riding the strongest possible edge.

*No cosmetics, no hidden code distractions.

Backtest Settings

Initial capital: $10,000

Commission: Conservative, realistic roundtrip cost:

15–20 per contract (including slippage per side) I set this to $25

Slippage: 3 ticks per trade

Symbol: CME_MINI:NQ1!

Timeframe: 1 min (but works on all timeframes)

Order size: Adaptive, 1–3 contracts

No pyramiding, no hidden DCA

Why these settings?

These settings are intentionally strict and realistic, reflecting the true costs and risks of live trading. The 10,000 account size is accessible for most retail traders. 25/contract including 3 ticks of slippage are on the high side for NQ, ensuring the strategy is not curve-fit to perfect fills. If it works here, it will work in real conditions.

Why It Wins

While others put out “AI-powered” strategies with little logic or soul, GENESIS is ruthlessly practical. It is built around what keeps traders alive:

- Context-aware signals, not just patterns

- Tight, transparent risk

- Inputs that adapt, not confuse

- Visuals that clarify, not distract

- Code that runs clean, efficient, and with minimal overfitting risk (try it on QQQ, AMD, SOL, etc. out of the box)

Disclaimer (for TradingView compliance):

Trading is risky. Futures, stocks, and crypto can result in significant losses. Do not trade with funds you cannot afford to lose. This is for educational and informational purposes only. Use in simulation/backtest mode before live trading. No past performance is indicative of future results. Always understand your risk and ownership of your trades.

This will not be my last—my goal is to keep raising the bar until DAFE is a brand or I’m forced to take this private.

Use with discipline, use with clarity, and always trade smarter.

— Dskyz , powered by DAFE Trading Systems.

SBC ProtfoSBC Portfo PNL Indicator

Description

The SBC Portfo PNL Indicator is a user-friendly tool designed for Hebrew-speaking traders to track the Profit and Loss (PNL) of their stock portfolios on TradingView charts. It supports up to 5 distinct portfolios, each capable of holding an unlimited number of stocks with unlimited buy commands, allowing real-time monitoring of portfolio performance.

Key Features

- Multi-Portfolio Support: Track up to 5 separate portfolios for different trading strategies or accounts.

- Unlimited Stock Entries: Add unlimited stocks and buy commands per portfolio.

- Detailed Buy Commands: Input for each stock:

- Stock Ticker (e.g., AAPL, TSLA).

- Buy Price (e.g., 150.25).

- Buy Amount (e.g., 10).

- Hebrew-Friendly Interface: Intuitive settings dialog with clear instructions in Hebrew.

- Customizable PNL Tracking: Visualize PNL on charts with real-time updates based on market data.

How to Use

1. Add the Indicator:

- Go to the Indicators menu in TradingView and add the "SBC Portfo" PNL Indicator.

2. Configure Portfolios:

- Open the indicator’s settings dialog.

- For each portfolio (up to 5), enter data in the provided input fields using this format:

PortfolioName:StockTicker:BuyPricexBuyAmount;StockTicker:BuyPricexBuyAmount

Example:

Portfolio1:AAPL:150.25x10;TSLA:266.72x5

- This represents a portfolio named "Portfolio1" with:

- 10 shares of AAPL bought at $150.25.

- 5 shares of TSLA bought at $266.72.

- Repeat for additional portfolios (e.g., Portfolio2, Portfolio3).

- Add multiple buy commands for the same stock if needed (e.g., AAPL:160.50x20).

3. Apply Settings:

- Save settings to display PNL based on current market prices.

4. Monitor PNL:

- View PNL for each portfolio on the chart via tables, labels, or graphical overlays (based on settings).

Input Format

Enter portfolio data manually in the settings dialog, one input field per portfolio:

PortfolioName:StockTicker:BuyPricexBuyAmount;StockTicker:BuyPricexBuyAmount

- PortfolioName: Unique name (e.g., Portfolio1, Growth).

- StockTicker: Stock symbol (e.g., AAPL).

- BuyPrice: Purchase price per share (e.g., 150.25).

- BuyAmount: Number of shares (e.g., 10).

- Use

: to separate portfolio name, ticker, and buy data

x to separate price and amount

; for multiple stocks in the portfolio

Example:

- Portfolio 1: GrowthPortfolio:AAPL:150.25x10;TSLA:266.72x5

- Portfolio 2: DividendPortfolio:KO:55.20x50;PG:145.30x30

Notes

- Hebrew Support: Settings and labels are optimized for Hebrew users.

- Manual Input: Enter portfolio data manually in the settings dialog using the correct format.

- Compatibility: Works with any stock ticker supported by TradingView.

תיאור אינדיקטור SBC Portfo PNL הוא כלי ידידותי למשתמש שתוכנן במיוחד עבור סוחרים דוברי עברית למעקב אחר רווח והפסד (PNL) של תיקי המניות שלהם ישירות בגרפים של TradingView. הוא תומך בעד 5 תיקים נפרדים, כאשר כל תיק יכול להכיל מספר בלתי מוגבל של מניות עם פקודות קנייה בלתי מוגבלות, ומאפשר מעקב בזמן אמת אחר ביצועי התיק.

תכונות עיקריות

- תמיכה בריבוי תיקים: מעקב אחר עד 5 תיקים נפרדים עבור אסטרטגיות מסחר או חשבונות שונים.

- רישום מניות ללא הגבלה: הוספת מספר בלתי מוגבל של מניות ופקודות קנייה לכל תיק.

- פקודות קנייה מפורטות: הזנת נתונים עבור כל מניה:

- סימול המניה (למשל, AAPL, TSLA).

- מחיר קנייה (למשל, 150.25).

- כמות קנייה (למשל, 10).

- ממשק ידידותי לעברית: חלונית הגדרות אינטואיטיבית עם הוראות ברורות בעברית.

- מעקב PNL הניתן להתאמה: הצגת רווח והפסד בגרפים עם עדכונים בזמן אמת בהתבסס על נתוני השוק.

כיצד להשתמש

1. הוספת האינדיקטור:

- נווט לתפריט האינדיקטורים ב-TradingView והוסף את "SBC Portfo PNL Indicator".

2. הגדרת תיקים:

- פתח את חלונית ההגדרות של האינדיקטור.

- עבור כל תיק (עד 5), הזן נתונים בשדות המסופקים בפורמט הבא:

PortfolioName:StockTicker:BuyPricexBuyAmount;StockTicker:BuyPricexBuyAmount

לדוגמה:

Portfolio1:AAPL:150.25x10;TSLA:266.72x5

שורה זו מייצגת תיק בשם "Portfolio1" עם:

- 10 מניות של AAPL שנקנו ב-$150.25.

- 5 מניות של TSLA שנקנו ב-$266.72.

- חזור על התהליך עבור תיקים נוספים (למשל, Portfolio2, Portfolio3).

- ניתן להוסיף פקודות קנייה מרובות לאותה מניה לפי הצורך (למשל, AAPL:160.50x20).

3. החלת ההגדרות:

- שמור את ההגדרות להצגת ה-PNL בהתבסס על מחירי השוק הנוכחיים.

4. מעקב אחר PNL:

- צפה ב-PNL עבור כל תיק בגרף באמצעות טבלאות, תוויות או שכבות גרפיות (בהתאם להגדרות).

פורמט קלט הזן נתוני תיק ידנית בחלונית ההגדרות, שדה קלט אחד לכל תיק: PortfolioName:StockTicker:BuyPricexBuyAmount;StockTicker:BuyPricexBuyAmount

PortfolioName: שם ייחודי (למשל, Portfolio1, Growth).

StockTicker: סימול המניה (למשל, AAPL).

BuyPrice: מחיר רכישה למניה (למשל, 150.25).

BuyAmount: מספר המניות (למשל, 10).

השתמש ב-

: להפרדה בין שם התיק, סימול ונתוני קנייה

x להפרדה בין מחיר וכמות

; להפרדה בין מניות מרובות

דוגמה:

- תיק 1: GrowthPortfolio:AAPL:150.25x10;TSLA:266.72x5

- תיק 2: DividendPortfolio:KO:55.20x50;PG:145.30x30

Release Notes

Version 1.1 includes:

- Calculations for extended hours (Pre-Market & After-Hours).

- Option to display portfolio summary data for stocks not in the portfolio (enable via settings checkbox).

- Table background for better visibility; click to bring table to the front.

- Updated text strings (names, titles, tooltips).

הערות

תמיכה בעברית: ההגדרות והתוויות מותאמות למשתמשים דוברי עברית.

הזנה ידנית: הזן נתוני תיק ידנית בחלונית ההגדרות תוך שימוש בפורמט הנכון.

תאימות: עובד עם כל סימול מניה הנתמך על ידי TradingView.

גרסה 1.1 מכילה:

1. חישובים כוללים שעות מסחר מורחבות (Pre-Market ו-After-Hours).

2. אפשרות להציג נתוני תיק כוללים עבור מניות שאינן בתיק (הפעל באמצעות תיבת סימון בהגדרות).

3. צבע רקע לטבלה לשיפור הנראות; לחיצה על הטבלה מביאה אותה לחזית.

4. תיקון נוסחים (שמות, כותרות, וטולטיפים).

Market Sentiment Index US Top 40 [Pt]▮Overview

Market Sentiment Index US Top 40 [Pt} shows how the largest US stocks behave together. You pick one simple measure—High Low breakouts, Above Below moving average, or RSI overbought/oversold—and see how many of your chosen top 10/20/30/40 NYSE or NASDAQ names are bullish, neutral, or bearish.

This tool gives you a quick view of broad-market strength or weakness so you can time trades, confirm trends, and spot hidden shifts in market sentiment.

▮Key Features

► Three Simple Modes

High Low Index: counts stocks making new highs or lows over your lookback period

Above Below MA: flags stocks trading above or below their moving average

RSI Sentiment: marks overbought or oversold stocks and plots a small histogram

► Universe Selection

Top 10, 20, 30, or 40 symbols from NYSE or NASDAQ

Option to weight by market cap or treat all symbols equally

► Timeframe Choice

Use your chart’s timeframe or any intraday, daily, weekly, or monthly resolution

► Histogram Smoothing

Two optional moving averages on the sentiment bars

Markers show when the faster average crosses above or below the slower one

► Ticker Table

Optional on-chart table showing each ticker’s state in color

Grid or single-row layout with adjustable text size and color settings

▮Inputs

► Mode and Lookback

Pick High Low, Above Below MA, or RSI Sentiment

Set lookback length (for example 10 bars)

If using Above Below MA, choose the moving average type (EMA, SMA, etc.)

► Universe Setup

Market: NYSE or NASDAQ

Number of symbols: 10, 20, 30, or 40

Weights: on or off

Timeframe: blank to match chart or pick any other

► Moving Averages on Histogram

Enable fast and slow averages

Set their lengths and types

Choose colors for averages and markers

► Table Options

Show or hide the symbol table

Select text size: tiny, small, or normal

Choose layout: grid or one-row

Pick colors for bullish, neutral, and bearish cells

Show or hide exchange prefixes

▮How to Read It

► Sentiment Bars

Green means bullish

Red means bearish

Near zero means neutral

► Zero Line

Separates bullish from bearish readings

► High Low Line (High Low mode only)

Smooth ratio of highs versus lows over your lookback

► MA Crosses

Fast MA above slow MA hints rising breadth

Fast MA below slow MA hints falling breadth

► Ticker Table

Each cell colored green, gray, or red for bull, neutral, or bear

▮Use Cases

► Confirm Market Trends

Early warning when price makes highs but breadth is weak

Catch rallies when breadth turns strong while price is flat

► Spot Sector Rotation

Switch between NYSE and NASDAQ to see which group leads

Watch tech versus industrial breadth to track money flow

► Filter Trade Signals

Enter longs only when breadth is bullish

Consider shorts when breadth turns negative

► Combine with Other Indicators

Use RSI Sentiment with trend tools to spot overextended moves

Add volume indicators in High Low mode for breakout confirmation

► Timeframe Analysis

Daily for big-picture bias

Intraday (15-min) for precise entries and exits

Bitcoin Impact AnalyzerSummary of the "Bitcoin Impact Analyzer" script, the adjustments users can make, and an explanation of what the chart and table represent:

Script Summary:

The "Bitcoin Impact Analyzer" script is designed to help traders and analysts understand the relationship between a chosen altcoin and Bitcoin (BTC). It does this by:

Fetching price data for the specified altcoin and Bitcoin.

Calculating several key comparative metrics:

Normalized Prices: Shows the percentage performance of both assets from a common starting point.

Price Correlation: Measures how similarly the two assets' prices move over a defined period.

Beta: Indicates the altcoin's volatility relative to Bitcoin.

Altcoin/BTC Ratio: Shows the altcoin's value expressed in Bitcoin.

Fetching and displaying Bitcoin Dominance (BTC.D) data.

Visualizing these metrics on the chart as distinct plots.

Displaying the current values of these key metrics in a data table on the chart for quick reference.

The script aims to provide insights into whether an altcoin is outperforming or underperforming Bitcoin, how closely its price movements are tied to Bitcoin's, and its relative volatility.

User Adjustments:

Users can customize the script's behavior through several input settings:

Symbol Inputs:

Altcoin Symbol: Users can enter the ticker symbol for any altcoin they wish to analyze (e.g., BINANCE:ETHUSDT, KUCOIN:SOLUSDT).

Bitcoin Reference Symbol: Users can specify the Bitcoin pair to use as a reference, though BINANCE:BTCUSDT is a common default.

Lookback for Correlation/Beta:

Lookback Period: This integer value (default 50 periods) determines how many past candles are used to calculate the price correlation and beta.

A shorter lookback makes the metrics more sensitive to recent price action.

A longer lookback provides a smoother, more stable indication of the longer-term relationship.

Plot Visibility Options:

Users can toggle on or off the display of each individual plot on the chart:

Normalized BTC & Altcoin Prices

Altcoin/BTC Ratio

Correlation Plot

Bitcoin Dominance (BTC.D)

Beta Plot

This allows users to focus on specific metrics and reduce chart clutter.

What the Chart Represents:

The chart visually displays the historical trends and relationships of the selected metrics:

Normalized Prices Plot: Two lines (typically orange for BTC, blue for the altcoin) show the percentage growth of each asset from the start of the loaded chart data (or the first available data point for each symbol). This makes it easy to see which asset has performed better over time on a relative basis.

Correlation Plot: A single line (purple) oscillates between -1 and +1.

Values near +1 indicate a strong positive correlation (altcoin and BTC prices tend to move in the same direction).

Values near -1 indicate a strong negative correlation (they tend to move in opposite directions).

Values near 0 indicate little to no linear relationship.

Lines at +0.7 and -0.7 are often plotted as thresholds for "strong" correlation.

Beta Plot (if enabled): A single line (teal) shows the altcoin's volatility relative to BTC.

A Beta of 1 (often marked by a dashed line) means the altcoin has, on average, the same volatility as BTC.

Beta > 1 suggests the altcoin is more volatile than BTC (moves by a larger percentage for a given BTC move).

Beta < 1 suggests the altcoin is less volatile than BTC.

Bitcoin Dominance Plot: An area plot (gray) shows the percentage of the total cryptocurrency market capitalization that Bitcoin holds. This helps understand broader market sentiment and capital flows.

Altcoin/BTC Ratio Plot: A line (fuchsia) shows the price of the altcoin denominated in BTC.

An upward trend means the altcoin is gaining value against Bitcoin (outperforming).

A downward trend means the altcoin is losing value against Bitcoin (underperforming).

What the Table Represents:

The data table, typically located in the bottom-right corner of the chart, provides a snapshot of the current values for the most important calculated metrics. It includes:

Altcoin: The ticker symbol of the analyzed altcoin.

Bitcoin Ref: The ticker symbol of the Bitcoin reference.

Correlation (lookback): The current correlation coefficient between the altcoin and BTC, based on the specified lookback period. The value is color-coded (e.g., green for strong positive, red for strong negative).

Beta (lookback): The current beta value of the altcoin relative to BTC, based on the specified lookback period. The value may be color-coded to highlight significantly high or low volatility.

BTC.D Current: The current Bitcoin Dominance percentage.

ALT/BTC Ratio: The current price of the altcoin expressed in Bitcoin.

The table offers a quick, at-a-glance summary of the present market dynamics between the two assets without needing to interpret the lines on the chart for their exact current values.

Key Recent Highs and LowsKey Recent Highs & Lows — Session‐Aware Market Structure

TL;DR

This tool plots the most important intraday price extremes for every U.S.‑equity trading segment—Early Premarket • Western Premarket • Regular Hours • Post‑Market Hours • Yesterday’s Range—and labels them so you can trade break‑outs, retests and mean‑reversion with instant context.

📐 Theory & Why These Levels Matter

Liquidity Pools

Visible session extremes attract resting orders (stop‑losses, take‑profits, opening prints). Price often accelerates into them and reacts at them.

Market Memory

The previous day’s high/low is a widely‑watched pivot for gap fills, overnight inventory corrections and multi‑day breakouts.

Mean‑Reversion Windows

Statistically, pre‑ and post‑market ranges are thin; an aggressive spike outside those bands often retraces when full liquidity returns.

Break‑Out Confirmation

A true breakout isn’t just a tick above RTH‑high—it usually closes or at least consolidates above the prior extreme. Seeing all bands lets you gauge whether a push is “real” or just probing thinner sessions.

Put simply, these levels help you decide:

Break‑out ➜ trade in the direction of expansion past a session extreme with follow‑through.

Fade/Mean‑Revert ➜ fade a spike that tags an extreme without commitment (e.g., hits Western‑Premkt‑High then stalls before RTH).

🔍 What the Script Draws

Session (UTC‑4 EST) Default Color / Style Typical Use‑Case

Early Premarket 4 – 7 AM Thick semi‑transparent orange line detect overnight retail spikes / fade plays

Western Premarket 7 – 9 : 30 AM Dashed orange‑red breakout watch as U.S. brokers open

Regular Session (RTH) 9 : 30 – 16 : 00 Bold teal dotted line core intraday structure; classic highs/lows

Post‑Market 16 – 23 : 59 Soft indigo band after‑hours news moves, earnings fades

Previous‑Day RTH Solid teal gap‑fill targets, trend continuation filters

(All colors, thicknesses and transparencies are editable in the settings.)

✨ Features

Real‑Time Updates

Levels refresh tick‑by‑tick inside their own session—no repainting later.

One‑Click Visibility Toggles

Show or hide any session extreme independently.

Clean Auto‑Labels

Optional right‑edge tags (“RTH High”, “Premkt Low”, etc.) keep your chart readable even when lines overlap.

Automatic Daily Reset

At midnight Eastern, buffers clear and yesterday’s extremes roll into the “Prev‑Day” pair.

Zero‑Noise Design

Transparencies and line styles are tuned so you can overlay on any symbol / timeframe without drowning candles.

📈 How to Trade with It

Intraday Breakout Strategy

Mark confluence (e.g., price pushes through Western Premkt High and Yesterday’s High).

Wait for a pullback that holds above the reclaimed band.

Enter with stop under that session line; target next band or measured‑move.

Fade / Mean‑Reversion

Pre‑market headline sends price 5 % above Early Premkt High.

Volume dries up before RTH open.

Short into exhaustion; cover near Western Premkt High or VWAP.

Gap‑Fill & Trend Days

Cash open gaps above Prev‑Day High.

If first 15‑min candle closes back inside yesterday’s range, bias shifts to downside fade.

If it holds above, treat gap as breakout and track RTH High extensions.

Pair it with volume‑profile, VWAP, or momentum oscillators for even higher‑confidence setups.

⚙️ Settings Cheat‑Sheet

Setting Effect

Show Regular / Premarket / Post‑market High/Low Master visibility per session

Show Previous Day High/Low Toggle yesterday’s anchor range

Show Session Labels Turn the right‑edge tags on/off

Style Panel Change each line’s color, width, transparency, dash/dot

🛠️ Best Practices

Works on any intraday timeframe (1‑min to 1‑hour).

Crypto or 24 h markets: adjust session times to match your exchange.

Combine with alerts (e.g., “price crossing RTH High”) for hands‑free monitoring.

Put KRHL on your chart and you’ll never wonder which high matters most again—because they’re all right there, clearly labeled and color‑coded. Trade breakouts or fades with confidence, armed with the exact market structure everyone else is watching.

Sector 50MA vs 200MA ComparisonThis TradingView indicator compares the 50-period Moving Average (50MA) and 200-period Moving Average (200MA) of a selected market sector or index, providing a visual and analytical tool to assess relative strength and trend direction. Here's a detailed breakdown of its functionality:

Purpose: The indicator plots the 50MA and 200MA of a chosen sector or index on a separate panel, highlighting their relationship to identify bullish (50MA > 200MA) or bearish (50MA < 200MA) trends. It also includes a histogram and threshold lines to gauge momentum and key levels.

Inputs:

Resolution: Allows users to select the timeframe for calculations (Daily, Weekly, or Monthly; default is Daily).

Sector Selection: Users can choose from a list of sectors or indices, including Tech, Financials, Consumer Discretionary, Utilities, Energy, Communication Services, Materials, Industrials, Health Care, Consumer Staples, Real Estate, S&P 500 Value, S&P 500 Growth, S&P 500, NASDAQ, Russell 2000, and S&P SmallCap 600. Each sector maps to specific ticker pairs for 50MA and 200MA data.

Data Retrieval:

The indicator fetches closing prices for the 50MA and 200MA of the selected sector using the request.security function, based on the chosen timeframe and ticker pairs.

Visual Elements:

Main Chart:

Plots the 50MA (blue line) and 200MA (red line) for the selected sector.

Fills the area between the 50MA and 200MA with green (when 50MA > 200MA, indicating bullishness) or red (when 50MA < 200MA, indicating bearishness).

Threshold Lines:

Horizontal lines at 0 (zero line), 20 (lower threshold), 50 (center), 80 (upper threshold), and 100 (upper limit) provide reference points for the 50MA's position.

Fills between 0-20 (green) and 80-100 (red) highlight key zones for potential overbought or oversold conditions.

Sector Information Table:

A table in the top-right corner displays the selected sector and its corresponding 50MA and 200MA ticker symbols for clarity.

Alerts:

Generates alert conditions for:

Bullish Crossover: When the 50MA crosses above the 200MA (indicating potential upward momentum).

Bearish Crossover: When the 50MA crosses below the 200MA (indicating potential downward momentum).

Use Case:

Traders can use this indicator to monitor the relative strength of a sector's short-term trend (50MA) against its long-term trend (200MA).

The visual fill between the moving averages and the threshold lines helps identify trend direction, momentum, and potential reversal points.

The sector selection feature allows for comparative analysis across different market segments, aiding in sector rotation strategies or market trend analysis.

This indicator is ideal for traders seeking to analyze sector performance, identify trend shifts, and make informed decisions based on moving average crossovers and momentum thresholds.

Bullish and Bearish Breakout Alert for Gold Futures PullbackBelow is a Pine Script (version 6) for TradingView that includes both bullish and bearish breakout conditions for my intraday trading strategy on micro gold futures (MGC). The strategy focuses on scalping two-legged pullbacks to the 20 EMA or key levels with breakout confirmation, tailored for the Apex Trader Funding $300K challenge. The script accounts for the Daily Sentiment Index (DSI) at 87 (overbought, favoring pullbacks). It generates alerts for placing stop-limit orders for 175 MGC contracts, ensuring compliance with Apex’s rules ($7,500 trailing threshold, $20,000 profit target, 4:59 PM ET close).

Script Requirements

Version: Pine Script v6 (latest for TradingView, April 2025).

Purpose:

Bullish: Alert when price breaks above a rejection candle’s high after a two-legged pullback to the 20 EMA in a bullish trend (price above 20 EMA, VWAP, higher highs/lows).

Bearish: Alert when price breaks below a rejection candle’s low after a two-legged pullback to the 20 EMA in a bearish trend (price below 20 EMA, VWAP, lower highs/lows).

Context: 5-minute MGC chart, U.S. session (8:30 AM–12:00 PM ET), avoiding overbought breakouts above $3,450 (DSI 87).

Output: Alerts for stop-limit orders (e.g., “Buy: Stop=$3,377, Limit=$3,377.10” or “Sell: Stop=$3,447, Limit=$3,446.90”), quantity 175 MGC.

Apex Compliance: 175-contract limit, stop-losses, one-directional news trading, close by 4:59 PM ET.

How to Use the Script in TradingView

1. Add Script:

Open TradingView (tradingview.com).

Go to “Pine Editor” (bottom panel).

Copy the script from the content.

Click “Add to Chart” to apply to your MGC 5-minute chart .

2. Configure Chart:

Symbol: MGC (Micro Gold Futures, CME, via Tradovate/Apex data feed).

Timeframe: 5-minute (entries), 15-minute (trend confirmation, manually check).

Indicators: Script plots 20 EMA and VWAP; add RSI (14) and volume manually if needed .

3. Set Alerts:

Click the “Alert” icon (bell).

Add two alerts:

Bullish Breakout: Condition = “Bullish Breakout Alert for Gold Futures Pullback,” trigger = “Once Per Bar Close.”

Bearish Breakout: Condition = “Bearish Breakout Alert for Gold Futures Pullback,” trigger = “Once Per Bar Close.”

Customize messages (default provided) and set notifications (e.g., TradingView app, SMS).

Example: Bullish alert at $3,377 prompts “Stop=$3,377, Limit=$3,377.10, Quantity=175 MGC” .

4. Execute Orders:

Bullish:

Alert triggers (e.g., stop $3,377, limit $3,377.10).

In TradingView’s “Order Panel,” select “Stop-Limit,” set:

Stop Price: $3,377.

Limit Price: $3,377.10.

Quantity: 175 MGC.

Direction: Buy.

Confirm via Tradovate.

Add bracket order (OCO):

Stop-loss: Sell 175 at $3,376.20 (8 ticks, $1,400 risk).

Take-profit: Sell 87 at $3,378 (1:1), 88 at $3,379 (2:1) .

Bearish:

Alert triggers (e.g., stop $3,447, limit $3,446.90).

Select “Stop-Limit,” set:

Stop Price: $3,447.

Limit Price: $3,446.90.

Quantity: 175 MGC.

Direction: Sell.

Confirm via Tradovate.

Add bracket order:

Stop-loss: Buy 175 at $3,447.80 (8 ticks, $1,400 risk).

Take-profit: Buy 87 at $3,446 (1:1), 88 at $3,445 (2:1) .

5. Monitor:

Green triangles (bullish) or red triangles (bearish) confirm signals.

Avoid bullish entries above $3,450 (DSI 87, overbought) or bearish entries below $3,296 (support) .

Close trades by 4:59 PM ET (set 4:50 PM alert) .

BIN Based Support and Resistance [SS]This indicator presents a version of an alternative way to determine support and resistance, using a method called "Bins".

Bins provide for a flexible and interesting way to determine support and resistance levels.

First off, let's discuss BINS:

Bins are ranges or containers into which your data points can be sorted. For example, if you're grouping ages, you might have bins like 0–18, 19–35, 36–50, and 51+. Any data point within these intervals gets placed in the corresponding bin.

Binning simplifies complex data sets by grouping values into categories. This is useful for such things as

Visualizing data in histograms or bar charts.

Reducing noise and highlighting trends.

This indicator groups the price action into 10 separate bins. It determines the Support / Resistance level by averaging the values in the Bins to find an iteration of the "central tendency" or average reoccurring value.

Pros and Cons

Since this is a different approach to support and resistance, I think its important to highlight some of the pros and advantages, but also be open about the cons.

First off the PROS

Bin Based Support and Resistance Levels dynamically adjust to ranges as opposed to hard / fast peaks and valleys. This makes them better at analyzing price action vs simply drawing lines at random peaks and valleys.

Because Bins are analyzing ALL PA within a period's max and min range, Bin Support and Resistance can actually be used similar to Volume profile, where you are able to identify a pseudo-POC, or areas where price tends to consolidate. Take a look at this example on SPY:

You can see these 2 SR lines are close together. This represents that this general price range is an area where price likes to accumulate/consolidate. You can see the SPY ended up coming back to this range and consolidating there for a bit.

This is a strength of using a BIN based approach to calculating support and resistance, because as indicated before, it looks at price action vs peaks and valleys.

As a tip, these areas are areas you want to wait for a break in one direction or the other.

The indicator provides for backtest results of the support and resistance lines, to see how many times certain areas acted as resistance or support. Because this is analyzing and distributing PA evenly throughout the period's max and min, the indicator can tell you which areas tend to have higher rejection zones and which have higher support zones.

Now the CONS

Because bin based SR take an average approach, the SR lines can sometimes be slightly broken before the ticker finds rejection:

To combat this, make sure there is confirmed support. How the indicator actually backtests these lines is by waiting to see if the ticker has 3 consecutive closes above the support line or below the resistance line. So these are things to be mindful of.

It doesn't consider pivots. Most support and resistance indicators either identify max and min peaks and valleys or use pivot points. Pivot points are a great way to identify peaks and valleys and thus by extension support and resistance. However, this is also somewhat of a strength, as using BINS forces the indicator to consider ALL price action and not just the extremes (highs and lows).

Can be slightly skewed in highly volatile environments. Any time there is a massive drop or rally, it can skew the indicator to give extreme ranges to both ends. For example, the Tariff news collapse on ES1!:

Owning to limitations in lookback length, sometimes the min and max range can be exceeded and other traditional areas of support / resistance is where a ticker will find support.

Using the indicator

Here are some basic use/functionalities of the indicator:

Selecting display of backtest results: You can select to have the backtest results shown in a table:

Or directly on the lines:

Inversely, you can toggle them off completely:

You can modify the lookback length. The suggested lookback length is between 250 to 500 candles on smaller timeframes. I also suggest 252 on daily timeframes (which represents 1 trading year).

And that's the indicator!

It is very easy to use, so you should pick it up in no time!

Enjoy and as always, 🚀🚀 safe trades! 🚀🚀

Cartera SuperTrends v4 PublicDescription

This script creates a screener with a list of ETFs ordered by their average ROC in three different periods representing 4, 6 and 8 months by default. The ETF

BIL

is always included as a reference.

The previous average ROC value shows the calculation using the closing price from last month.

The current average ROC value shows the calculation using the current price.

The previous average column background color represents if the ETF average ROC is positive or negative.

The current average column background color represents if the ETF average ROC is positive or negative.

The current average column letters color represents if the current ETF average ROC is improving or not from the previous month.

Changes from V2 to V3

Added the option to make the calculation monthly, weekly or daily

Changes from V3 to V4

Adding up to 25 symbols

Highlight the number of tickers selected

Highlight the sorted column

Complete refactor of the code using a matrix of arrays

Options

The options available are:

Make the calculation monthly, weekly or daily

Adjust Data for Dividends

Manual calculation instead of using ta.roc function

Sort table

Sort table by the previous average ROC or the current average ROC

Number of tickers selected to highlight

First Period in months, weeks or days

Second Period in months, weeks or days

Third Period in months, weeks or days

Select the assets (max 25)

Usage

Just add the indicator to your favorite indicators and then add it to your chart.

Casa_VolumeProfileSessionLibrary "Casa_VolumeProfileSession"

Analyzes price and volume during regular trading hours to provide a session volume profile,

including Point of Control (POC), Value Area High (VAH), and Value Area Low (VAL).

Calculates and displays these levels historically and for the developing session.

Offers customizable visualization options for the Value Area, POC, histogram, and labels.