ATR%The time period can be customized, which is suitable for finding short-term high-volatility trading pairs, and may be suitable for finding grid trading.

M-oscillator

Smart Price Divergence (MACD Filter) + EMA📌 Purpose

This indicator detects Price Divergences with MACD filtered by a 200 EMA trend condition.

It helps identify high-probability reversal zones aligned with market trend context.

🧠 How It Works

1. MACD Divergence Logic

Bearish Divergence:

Price makes a higher high.

MACD makes a lower high.

Price is above EMA (indicating possible exhaustion in bullish trend).

Bullish Divergence:

Price makes a lower low.

MACD makes a higher low.

Price is below EMA (indicating possible exhaustion in bearish trend).

2. EMA Trend Filter

EMA(200) is used as a directional filter:

Bearish divergences considered above EMA (extended bullish conditions).

Bullish divergences considered below EMA (extended bearish conditions).

3. Visual & Alerts

EMA(200) plotted on chart in orange.

Red triangles for Bearish Divergence.

Green triangles for Bullish Divergence.

Alerts fire for both divergence types.

📈 How to Use

Look for divergence signals as potential reversal alerts.

Combine with support/resistance or price action for confirmation.

EMA ensures signals occur in extended zones, increasing reliability.

Recommended Timeframes: 1h, 4h, D.

Markets: Forex, Crypto, Stocks.

⚙️ Inputs

MACD Fast / Slow / Signal Length

EMA Length (default 200)

⚠️ Disclaimer

This script is for educational purposes only. It does not constitute financial advice.

Always test thoroughly before live trading.

Smart RSI Divergence PRO | Auto Lines + Alerts📌 Purpose

This indicator automatically detects Regular and Hidden RSI Divergences between price action and the RSI oscillator.

It plots divergence lines directly on the chart, labels signals, and includes alerts for automated monitoring.

🧠 How It Works

1. RSI Calculation

RSI is calculated using the selected Source (default: Close) and RSI Length (default: 14).

2. Divergence Detection via Fractals

Swing points on both price and RSI are detected using fractal logic (5-bar patterns).

Regular Divergence:

Bearish: Price forms a higher high, RSI forms a lower high.

Bullish: Price forms a lower low, RSI forms a higher low.

Hidden Divergence:

Bearish: Price forms a lower high, RSI forms a higher high.

Bullish: Price forms a higher low, RSI forms a lower low.

3. Auto Drawing Lines

Lines are drawn automatically between divergence points:

Red = Regular Bearish

Green = Regular Bullish

Orange = Hidden Bearish

Blue = Hidden Bullish

Line width and transparency are adjustable.

4. Labels and Alerts

Labels mark divergence points with up/down arrows.

Alerts trigger for each divergence type.

📈 How to Use

Use Regular Divergences to anticipate trend reversals.

Use Hidden Divergences to confirm trend continuation.

Combine with support/resistance, trendlines, or volume for higher probability setups.

Recommended Timeframes: Works on all timeframes; more reliable on 1h, 4h, and Daily.

Markets: Forex, Crypto, Stocks.

⚙️ Inputs

Source (Close, HL2, etc.)

RSI Length

Toggle Regular / Hidden Divergence visibility

Toggle Lines / Labels

Line Width & Line Transparency

⚠️ Disclaimer

This script is for educational purposes only. It does not constitute financial advice.

Always test thoroughly before using in live trading.

Smart Impulse Exhaustion Finder (ATR + ADX Filter)📌 Purpose

This indicator detects potential exhaustion of strong bullish or bearish impulses at fresh swing highs/lows by combining multiple price action and volatility-based filters.

🧠 How It Works

A signal is triggered only when all core conditions are satisfied:

1. Swing High/Low Detection

Current high (or low) must be the highest (or lowest) over the last Extremum Lookback bars (default: 50).

This ensures the move is significant relative to recent price action.

2. Impulse Confirmation

Price must extend by at least 1 × ATR from the previous swing point.

This filters out minor fluctuations.

3. Exhaustion Conditions (at least 2 out of 3 must be met)

RSI Extreme: RSI > Overbought Level (default: 80) for bearish signals, RSI < Oversold Level (default: 20) for bullish signals.

Volume Spike: Volume > SMA(Volume, Volume SMA Length) × Volume Spike Multiplier.

Candle Wick Rejection: Upper wick ≥ Wick Threshold % for bearish setups, Lower wick ≥ Wick Threshold % for bullish setups.

4. Trend Filter

ADX > ADX Threshold ensures the market is trending and filters out sideways conditions.

5. Candle Body Filter

Candle body must be ≥ Body Size ATR Factor × ATR.

This avoids weak signals from small candles or doji formations.

📈 How to Use

Bearish Signal:

Appears at fresh swing highs with exhaustion conditions met. Useful for tightening stops, taking partial profits, or counter-trend shorts.

Bullish Signal:

Appears at fresh swing lows with exhaustion conditions met. Useful for trailing stops, profit-taking, or counter-trend longs.

Recommended Timeframes: Works best on 1h, 4h, and Daily charts.

Markets: Crypto, Forex, Stocks — wherever volatility and trends are present.

⚙️ Inputs

RSI Length / Overbought / Oversold

Volume SMA Length & Volume Spike Multiplier

Wick Threshold %

Extremum Lookback (bars for highs/lows)

ADX Length & Threshold

Body Size ATR Factor

⚠️ Disclaimer

This script is for educational purposes only and does not constitute financial advice.

Always test thoroughly and apply proper risk management before live trading.

💡 Tip: Combine this tool with your own market context and confluence factors for higher probability setups.

JHW Volume Based Buy and Sell MomentumThe JHW Volume-Based Buy and Sell Momentum indicator is a custom momentum oscillator designed to capture market sentiment based on volume dynamics and price rate of change (ROC). It aims to identify bullish or bearish momentum by analyzing how price reacts to increasing or decreasing trading volume.

Core Logic:

The indicator calculates the Rate of Change (ROC) of the closing price.

It then accumulates this ROC separately based on whether the current volume is lower or higher than the previous bar:

If volume decreases, the ROC is added to a "negative volume index" accumulator.

If volume increases, the ROC is added to a "positive volume index" accumulator.

These two accumulators are combined to form a net momentum line.

Smoothing:

A Simple Moving Average (SMA) is applied to both accumulators over a user-defined period (default: 25 bars).

The sum of these smoothed values forms the signal line.

Visualization:

The indicator plots:

The net momentum line (yellow).

The smoothed signal line (blue).

The area between the two lines is filled with color:

Yellow when momentum is above the signal (bullish).

Blue when momentum is below the signal (bearish).

Bar colors are also adjusted to reflect the current momentum state.

Use Case:

This indicator helps traders:

Detect volume-driven momentum shifts.

Identify potential buy or sell zones based on volume behavior.

Confirm trends or spot early reversals.

XRSI-Momentum IndexThe XRSI Momentum Index is an enhanced, presentation‑ready implementation of the classic Relative Strength Index (RSI) for TradingView.

It retains the mathematical simplicity of J. Welles Wilder’s RSI while adding a modern visual layer and alert framework that makes momentum assessment faster and less error‑prone on intraday as well as swing charts.

Interpretation Guide

Momentum confirmation

RSI above the Neutral (50) → bullish bias; below → bearish bias.

Noise filters

When RSI oscillates only between OB Noise & OS Noise, ignore whipsaw and stay flat or trend‑follow with reduced size.

Reversal scout

A full cross into the OB or OS band (beyond the noise area) followed by a cross back into the Noise band signals early exhaustion.

EMA overlay

• RSI > EMA RSI → momentum acceleration.

• RSI < EMA RSI → momentum cooling.

Combine with price structure (higher‑highs / lower‑lows) for divergence detection.

Quick‑Start

Add to Chart

Indicators → Invite‑only scripts → XRSI Momentum Index (or paste the source into Pine editor).

Tune Zones

For volatile pairs (e.g., GBPJPY), widen OB/OS to 80 / 20.

For range‑bound assets (e.g., EURCHF), tighten to 60 / 40.

Set Alerts

Right‑click indicator → Add alert → choose condition (e.g., “Entry Into Oversold Area”) → route to webhook or app.

Optional EMA Strategy

Overlay price 50/200 EMA on chart; trade only when XRSI and price trend agree.

Trigonometric StochasticTrigonometric Stochastic - Mathematical Smoothing Oscillator

Overview

A revolutionary approach to stochastic oscillation using sine wave mathematical smoothing. This indicator transforms traditional stochastic calculations through trigonometric functions, creating an ultra-smooth oscillator that reduces noise while maintaining sensitivity to price changes.

Mathematical Foundation

Unlike standard stochastic oscillators, this version applies sine wave smoothing:

• Raw Stochastic: (close - lowest_low) / (highest_high - lowest_low) × 100

• Trigonometric Smoothing: 50 + 50 × sin(2π × raw_stochastic / 100)

• Result: Naturally smooth oscillator with mathematical precision

Key Features

Advanced Smoothing Technology

• Sine Wave Filter: Eliminates choppy movements while preserving signal integrity

• Natural Boundaries: Mathematically constrained between 0-100

• Reduced False Signals: Trigonometric smoothing filters market noise effectively

Traditional Stochastic Levels

• Overbought Zone: 80 level (dashed line)

• Oversold Zone: 20 level (dashed line)

• Midline: 50 level (dotted line) - equilibrium point

• Visual Clarity: Clean oscillator panel with clear level markings

Smart Signal Generation

• Anti-Repaint Logic: Uses confirmed previous bar values

• Buy Signals: Generated when crossing above 30 from oversold territory

• Sell Signals: Generated when crossing below 70 from overbought territory

• Crossover Detection: Precise entry/exit timing

Professional Presentation

• Separate Panel: Dedicated oscillator window (overlay=false)

• Price Format: Formatted as price indicator with 2-decimal precision

• Theme Adaptive: Automatically matches your chart color scheme

Parameters

• Cycle Length (5-200): Period for highest/lowest calculations

- Shorter periods = more sensitive, more signals

- Longer periods = smoother, fewer but stronger signals

Trading Applications

Momentum Analysis

• Overbought/Oversold: Clear visual identification of extreme levels

• Momentum Shifts: Early detection of momentum changes

• Trend Strength: Monitor oscillator position relative to midline

Signal Trading

• Long Entries: Buy when crossing above 30 (oversold bounce)

• Short Entries: Sell when crossing below 70 (overbought rejection)

• Confirmation Tool: Use with trend indicators for higher probability trades

Divergence Detection

• Bullish Divergence: Price makes lower lows, oscillator makes higher lows

• Bearish Divergence: Price makes higher highs, oscillator makes lower highs

• Early Warning: Spot potential trend reversals before they occur

Trading Strategies

Scalping (5-15min timeframes)

• Use cycle length 10-14 for quick signals

• Focus on 20/80 level bounces

• Combine with price action confirmation

Swing Trading (1H-4H timeframes)

• Use cycle length 20-30 for reliable signals

• Wait for clear crossovers with momentum

• Monitor divergences for reversal setups

Position Trading (Daily+ timeframes)

• Use cycle length 50+ for major signals

• Focus on extreme readings (below 10, above 90)

• Combine with fundamental analysis

Advantages Over Standard Stochastic

1. Smoother Action: Sine wave smoothing reduces whipsaws

2. Mathematical Precision: Trigonometric functions provide consistent behavior

3. Maintained Sensitivity: Smoothing doesn't compromise signal quality

4. Reduced Noise: Cleaner signals in volatile markets

5. Visual Appeal: More aesthetically pleasing oscillator movement

Best Practices

• Market Context: Consider overall trend direction

• Multiple Timeframe: Confirm signals on higher timeframes

• Risk Management: Always use proper position sizing

• Backtesting: Test parameters on your preferred instruments

• Combination: Works excellently with trend-following indicators

Built-in Alerts

• Buy Alert: Trigonometric stochastic oversold crossover

• Sell Alert: Trigonometric stochastic overbought crossunder

Technical Specifications

• Pine Script Version: v6

• Panel: Separate oscillator window

• Format: Price indicator with 2-decimal precision

• Performance: Optimized for all timeframes

• Compatibility: Works with all instruments

Free and open-source indicator. Modify, improve, and share with the community!

Educational Value: Perfect for traders wanting to understand how mathematical smoothing improves oscillators and trigonometric applications in technical analysis.

COT Comm OsciDescription

The COT Comm Osci is a sentiment oscillator based on net positions from the weekly Commitments of Traders (COT) report.

It transforms net positions of Commercials, Noncommercials, or Nonreportables into a 0–100 index.

A value of 100 = highest net position within the selected timeframe.

A value of 0 = lowest net position.

You can define three historical intervals (e.g. 26/ 52 / 156 weeks).

Tip

To improve your analysis, it's recommended to add a separate COT indicator that visualizes raw Long/Short or net positions directly. This helps interpret the oscillator in context.

This script is based on “Commercial Index–Buschi” by MagicEins and has been extended with new features and error handling.

Features

Select between Commercial, Noncommercial, or Nonreportable trader groups

Proper handling of HG Futures (Copper)

Displays a warning if the root code is invalid (unsupported market symbol)

Assets Correlation AnalyzerAssets Correlation Analyzer

---------------------------------------------

What is it?

The Assets Correlation Analyzer is a technical indicator that measures and visualizes the statistical relationship between any two financial assets (a 'Base Asset' vs. a 'Comparison Asset', example Gold vs. SPY or Nasdaq vs. Bitcoin). The indicator calculates dynamic correlation tracking using statistical methods, confidence intervals, and category-wide analysis capabilities.

---------------------------------------------

Why was it built? / Potential Benefits

This indicator was developed to help analyze inter-asset relationships in portfolio management and trading strategies. The indicator can be used for:

Risk Assessment: Identify when assets begin moving together

Diversification Analysis: Monitor portfolio component relationships

Pairs Trading: Identify when correlated assets diverge

Market Analysis: Recognize shifts in market conditions through correlation patterns

Asset Analysis: Support decision-making based on correlation dynamics

Hedging Analysis: Identify relationships between different instruments

---------------------------------------------

How it Works

The indicator employs established statistical methods to calculate rolling correlations between two selected assets:

Data Collection: Retrieves price data for both selected assets using TradingView's security function

Returns Calculation: Computes logarithmic or simple returns based on user preference

Outlier Filtering: Optionally removes extreme price movements (beyond 2.5 standard deviations) to improve accuracy

Correlation Computation: Calculates either Pearson or Spearman rank correlation over the specified period

Signal Generation: Applies smoothing and generates a signal line (EMA) for momentum detection

Confidence Assessment: Evaluates data quality and provides confidence metrics

---------------------------------------------

How to Read the Oscillator

Main Correlation Line

Values Range: -1.0 to +1.0

+1.0: Perfect positive correlation (assets move identically)

+0.7 to +0.99: Strong positive correlation

+0.3 to +0.69: Moderate positive correlation

-0.3 to +0.29: Weak/No significant correlation

-0.69 to -0.31: Moderate negative correlation

-0.99 to -0.7: Strong negative correlation

-1.0: Perfect negative correlation (assets move oppositely)

Color Coding System

Green shades: Positive correlation levels, with brighter green indicating stronger positive correlation

Red shades: Negative correlation levels, with brighter red indicating stronger negative correlation

Gray: Insufficient data or transitional periods

The color intensity reflects both correlation strength and momentum relative to the signal line.

Signal Line (Gray)

The EMA-based signal line helps identify momentum changes:

Correlation above signal: Positive momentum in correlation

Correlation below signal: Negative momentum in correlation

Crossovers: Potential turning points in the relationship

Background Fills

Gradient fills provide a quick visual assessment of correlation strength, with intensity indicating the degree of correlation.

---------------------------------------------

Correlation Calculation Methods and Options

Calculation Methods

Spearman Rank Correlation (Default)

Uses ranked values rather than raw prices

Less sensitive to outliers and non-linear relationships

Suitable for volatile or non-normally distributed assets

Pearson Correlation (Traditional)

Standard linear correlation method

More sensitive to outliers

Suitable for assets with normal distribution patterns

---------------------------------------------

Customization Options

Correlation Period (7-500 bars): Determines the lookback window for calculation

Signal Line Period (1-200 bars): Controls the smoothing of the signal line

Outlier Removal: Automatically filters extreme price movements

Return Type: Choose between logarithmic (recommended) or simple returns

Smoothing Period: Reduces noise in correlation readings

---------------------------------------------

Asset Categories

The indicator includes 80+ pre-configured assets across multiple categories:

Metals: Gold, Silver, Copper, Platinum, Palladium, Nickel, Zinc, Aluminum

Energy: WTI/Brent Crude, Natural Gas, Uranium

Agriculture: Corn, Soybeans, Wheat, Coffee

ETFs: Major indices, sector, geographic, and specialty ETFs

Bonds: Government and corporate bond instruments

Financial: Currency pairs, treasury yields, volatility indices

Cryptocurrencies: Major digital assets and market cap indices

Real Estate: REITs and real estate focused instruments

---------------------------------------------

For Whom This Indicator Is Designed

Intended Users

Portfolio Managers: Asset allocation and risk assessment

Quantitative Traders: Correlation-based strategy development

Risk Analysts: Correlation monitoring and analysis

Institutional Investors: Diversification analysis

Active Traders: Pairs trading and arbitrage analysis

Skill Level

Intermediate to Advanced: Requires understanding of correlation concepts and statistical interpretation

Experience with Statistics: Users should be familiar with correlation analysis concepts

---------------------------------------------

Information Tables

Main Analysis Table

Displays current correlation value, data confidence percentage, and selected asset information.

Category Correlation Table

Shows correlation strength between the selected 'Base Asset' (in the chart, Gold) and all assets in the comparison asset's category.

---------------------------------------------

Alert Conditions

Four built-in alert types:

Strong Stable Positive Correlation: Triggers when correlation exceeds +0.8 with low volatility

Strong Stable Negative Correlation: Triggers when correlation falls below -0.8 with low volatility

Bullish Correlation Momentum: Signals when correlation crosses above the signal line

Bearish Correlation Momentum: Signals when correlation crosses below the signal line

---------------------------------------------

Usage Notes

Longer periods (30-50 bars) provide more stable analysis

Shorter periods (10-20 bars) provide more responsive signals

Monitor confidence levels - correlations with <75% confidence should be interpreted cautiously

Correlations tend to increase during market stress periods

Should be used in conjunction with other analysis tools

---------------------------------------------

Important Disclaimer

This indicator is for educational and informational purposes only. It should not be considered as financial advice or a recommendation to buy, sell, or hold any financial instrument. Past correlation patterns do not guarantee future relationships between assets. Users should conduct their own research and consider consulting with a qualified financial advisor before making investment decisions. Trading and investing involve substantial risk of loss, and correlation analysis cannot eliminate these risks. The accuracy of correlation calculations depends on data quality and market conditions, which can change rapidly.

Blue Dot Pullback with Bollinger BonusKey FeaturesCore Blue Dot Condition:ATH Pulse: Checks if the highest high in the lookback period (default: 60 bars) is within 1% of the all-time high (over 5000 bars), using recentHigh >= allTimeHigh * 0.99.

Pullback: Price must be below the recent high (close < recentHigh ) but above a 10-period SMA (close > sma10) to ensure a bullish context.

Stochastic Crossover: Stochastic %K must cross above 20 (ta.crossover(k, stochOverSold)).

When these conditions are met, a blue dot is plotted below the bar.

Purple Dot Condition (Bollinger Band Bonus):Includes all blue dot conditions plus the price being within 2% of the lower Bollinger Band (close <= lowerBB * bbProximity).

When met, a purple dot is plotted instead of a blue dot to highlight the stronger signal.

Plotting Logic:Blue dots are plotted only when blueDotCondition is true and purpleDotCondition is false to avoid overlap.

Purple dots are plotted when purpleDotCondition is true (includes Bollinger Band proximity).

Alerts:Added separate alertcondition calls for blue and purple dots, allowing you to set up notifications in TradingView for each signal type.

Visualization:Stochastic %K and %D are plotted in a separate pane for reference, along with the oversold line (20).

You can disable the Stochastic plot by setting display=display.none in the plot functions.

Why This Should WorkCore Setup Alignment: The blue dot condition focuses on the core requirements (ATH, pullback, Stochastic crossover), which should produce signals similar to or more frequently than the ChatGPT script, as it omits the Bollinger Band requirement unless the purple dot condition is met.

Bollinger Band Bonus: The purple dot incorporates the Bollinger Band proximity check (bbNear), matching the ChatGPT script’s additional filter, ensuring purple dots appear when the price is near the lower Bollinger Band.

Flexible ATH Detection: Using recentHigh >= allTimeHigh * 0.99 makes the ATH condition less strict, increasing the likelihood of signals compared to my original script.

How to UseAdd to TradingView:Open the Pine Editor in TradingView.

Copy and paste the script.

Click "Add to Chart" to apply it.

Interpret Dots:Blue Dot: Indicates a stock near an ATH, in a pullback (above 10-period SMA), with a Stochastic crossover above 20. This is the core Dr. Wish setup.

Purple Dot: Same as blue dot but with the price also within 2% of the lower Bollinger Band, suggesting a stronger pullback signal.

Test and Compare:Apply the script to the same stock and timeframe where the ChatGPT script showed blue dots (e.g., NVDA or TSLA on a daily chart).

Check if blue dots appear at similar points and if purple dots appear when the price is near the lower Bollinger Band.

Adjust lookbackATH (e.g., 60 to 100) or bbProximity (e.g., 1.02 to 1.05) if signals are too rare or frequent.

Set Alerts:Use TradingView’s alert feature to create notifications for “Blue Dot Alert” or “Purple Dot Alert” when signals occur.

TroubleshootingIf you’re still not seeing blue or purple dots:Check the Chart: Ensure the stock has recently hit an ATH and pulled back. Test on volatile stocks like NVDA, TSLA, or AAPL on daily or weekly timeframes.

Timeframe Sensitivity: The script may produce fewer signals on lower timeframes (e.g., 1-hour) due to fewer ATH occurrences. Try a daily or weekly chart.

Parameter Tuning: Increase bbProximity (e.g., to 1.05) to allow purple dots for prices slightly further from the lower Bollinger Band, or increase lookbackATH to capture more ATHs.

Compare with ChatGPT Script: Run both scripts on the same chart to identify where signals differ. Share the ticker, timeframe, or a screenshot if you need help debugging specific cases.

Additional NotesThe 10-period SMA in the pullback condition (isPullback) is a simple bullish context filter. You can replace it with another condition (e.g., 20-period SMA or trend filter) if preferred.

The Bollinger Band parameters (bbLength=20, bbMult=2.0) are standard but can be adjusted to match your trading style.

The script uses a 5000-bar lookback for allTimeHigh to approximate a true ATH. If your chart has limited historical data, reduce this value (e.g., to 1000).

EMA-VWAP Super Reversal (Final Advanced Version)EMA-VWAP Super Reversal – User Guide

This indicator is designed for high-probability reversal trading setups on futures such as NQ1! and ES1!, following strict confluence conditions.

✅ Signal Types

🟢 / 🔴 Mean Reversion Dots

Appear when all 4 stochastics (15m, 5m, 1m) are extreme (>80 or <20)

AND price is far (>0.05% by default, adjustable) from EMA21 on the 15m.

Indicates potential snapback to EMAs.

🔺 Green / Orange EMA Reversal Triangles

Appear when stochastics are extreme

AND price pulls back into EMAs while the EMAs are correctly postured (bullish or bearish).

Indicates a high-probability reversal.

💎 Purple Diamond Super Reversal

Appears when EMA reversal conditions are met

AND there is divergence on the fast stochastic (Stoch1).

Strongest reversal signal.

✅ Confluence Checks Built In

✔ Multi-timeframe stochastic alignment (15m, 5m, 1m)

✔ EMA posture (bullish or bearish stack)

✔ EMA pullback logic or EMA distance check

✔ VWAP reversion point consideration

✔ Divergence detection for strongest signals

✅ How to Use

Use on a 15-minute chart (optimal).

Look for Super Reversal diamonds first (highest conviction).

Confirm with price action and key levels before entry.

Combine with order flow, liquidity sweeps, or market structure for best results.

⚙ Settings

EMA Distance Threshold (%) → Default 0.05 (for Mean Reversion Dots).

Increase for fewer, stronger signals.

Decrease for more sensitivity.

📌 Best Practices

Focus on reversals during London & NY sessions.

Avoid trading against strong higher timeframe trends without extra confirmation.

Use tight stops and let winners run when the setup is strong.

💡 This tool is built to highlight only the cleanest reversal setups with layered confluence. Use it to filter noise and stay disciplined with your entries.

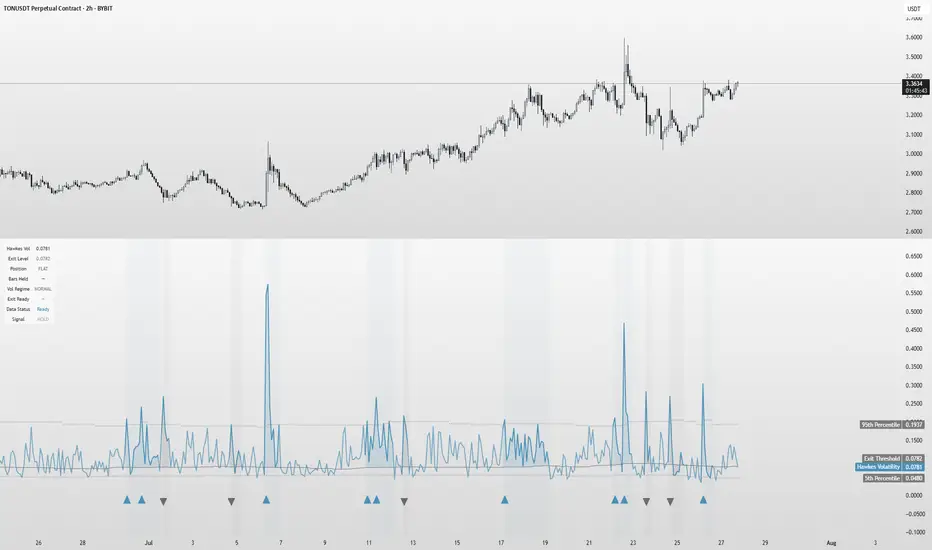

Hawkes Volatility Exit IndicatorOverview

The Hawkes Volatility Exit Indicator is a powerful tool designed to help traders capitalize on volatility breakouts and exit positions when momentum fades. Built on the Hawkes process, it models volatility clustering to identify optimal entry points after quiet periods and exit signals during volatility cooling. Designed to be helpful for swing traders and trend followers across markets like stocks, forex, and crypto.

Key Features Volatility-Based Entries: Detects breakouts when volatility spikes above the 95th percentile (adjustable) after quiet periods (below 5th percentile).

This indicator is probably better on exits than entries.

Smart Exit Signals: Triggers exits when volatility drops below a customizable threshold (default: 30th percentile) after a minimum hold period.

Hawkes Process: Uses a decay-based model (kappa) to capture volatility clustering, making it responsive to market dynamics.

Visual Clarity: Includes a volatility line, exit threshold, percentile bands, and intuitive markers (triangles for entries, X for exits).

Status Table: Displays real-time data on position (LONG/SHORT/FLAT), volatility regime (HIGH/LOW/NORMAL), bars held, and exit readiness.

Customizable Alerts: Set alerts for breakouts and exits to stay on top of trading opportunities.

How It Works Quiet Periods: Identifies low volatility (below 5th percentile) that often precede significant moves.

Breakout Entries: Signals bullish (triangle up) or bearish (triangle down) entries when volatility spikes post-quiet period.

Exit Signals: Suggests exiting when volatility cools below the exit threshold after a minimum hold (default: 3 bars).

Visuals & Table: Tracks volatility, position status, and signals via lines, shaded zones, and a detailed status table.

Settings

Hawkes Kappa (0.1): Adjusts volatility decay (lower = smoother, higher = more sensitive).

Volatility Lookback (168): Sets the period for percentile calculations.

ATR Periods (14): Normalizes volatility using Average True Range.

Breakout Threshold (95%): Volatility percentile for entries.

Exit Threshold (30%): Volatility percentile for exits.

Quiet Threshold (5%): Defines quiet periods.

Minimum Hold Bars (3): Ensures positions are held before exiting.

Alerts: Enable/disable breakout and exit alerts.

How to Use

Entries: Look for triangle markers (up for long, down for short) and confirm with the status table showing "ENTRY" and "LONG"/"SHORT."

Exits: Exit on X cross markers when the status table shows "EXIT" and "Exit Ready: YES."

Monitoring: Use the status table to track position, bars held, and volatility regime (HIGH/LOW/NORMAL).

Combine: Pair with price action, support/resistance, or other indicators for better context.

Tips : Adjust thresholds for your market: lower breakout thresholds for more signals, higher exit thresholds for earlier exits.

Test on your asset to ensure compatibility (best for markets with volatility clustering).

Use alerts to automate signal detection.

Limitations Requires sufficient data (default: 168 bars) for reliable signals. Check "Data Status" in the table.

Focuses on volatility, not price direction—combine with trend tools.

May lag slightly due to the smoothing nature of the Hawkes process.

Why Use It?

The Hawkes Volatility Exit Indicator offers a unique, data-driven approach to timing trades based on volatility dynamics. Its clear visuals, customizable settings, and real-time status table make it a valuable addition to any trader’s toolkit. Try it to catch breakouts and exit with precision!

This indicator is based on neurotrader888's python repo. All credit to him. All mistakes mine.

This conversion published for wider attention to the Hawkes method.

RV Indicator This Pine Script defines a custom Relative Volatility (RV) Indicator, which measures the ratio of directional price movement to volatility over a specified number of bars. Below is a full explanation of what this script does.

Title:

RV Indicator — Relative Volatility Oscillator

Purpose:

This indicator measures how aggressively price is moving compared to recent volatility, and smooths the result with a signal line. It can be used to gauge momentum shifts and trend strength.

How It Works – Step by Step

1. Measuring Price Momentum (v1)

It calculates the difference between the close and open prices of the last 4 candles.

A weighted average is applied:

The current candle and the one 3 bars ago get weight 1.

The two middle candles (1 and 2 bars ago) get weight 2.

This creates a smoothed momentum measure:

If close > open (bullish), v1 is positive.

If close < open (bearish), v1 is negative.

2. Measuring Volatility (v2)

Similarly, it calculates the high-low range for the last 4 candles.

The same weighting (1, 2, 2, 1) is applied.

This gives a smoothed volatility measure.

3. Combining Momentum and Volatility (RV Ratio)

For the past ti bars (default: 10), it sums up:

All v1 values (momentum sum)

All v2 values (volatility sum)

Then it divides them:

𝑅𝑉= sum of price momentum % sum of volatility

This produces the RV value:

RV > 0: Momentum is bullish (price is generally moving up relative to its volatility).

RV < 0: Momentum is bearish (price is moving down relative to its volatility).

4. Smoothed Signal Line (rvsig)

A smoothed version of the RV is created using a weighted average of the latest 4 RV values.

This acts like a signal line, similar to how MACD uses a signal line.

Crossovers between RV and this signal line can be used to detect shifts in momentum.

5. Visual Output

Orange Line (RV): Shows the raw momentum/volatility ratio.

Blue Line (Signal): A smoother line that follows RV more slowly.

Zero Line: Divides bullish vs. bearish momentum.

How to Use It in Trading

1. Look for Crossovers:

If RV crosses above its signal line → Possible buy signal (momentum turning bullish).

If RV crosses below its signal line → Possible sell signal (momentum turning bearish).

2. Check the Zero Line:

If both RV and Signal are above zero, momentum is bullish.

If both are below zero, momentum is bearish.

3. Filter False Signals:

Combine RV with a trend filter (like a 50 or 200 EMA) to avoid trading against the main trend.

Disclaimer: This script is for informational and educational purposes only. It does not constitute financial advice or a recommendation to buy or sell any asset. All trading decisions are solely your responsibility. Use at your own risk.

The Boring Strategy (TQQQ 2h Signals Only)TQQQ strategy on 2h timeframe.

Based on a combination of stochastic oscillator and moving average filters.

Please use it on TQQQ chart in 2h. You can use signals to trade any NASDAQ Index product (Futures, CFDs, ETFs, Prop-firms assets, etc..) but keep the chart on TQQQ for charting and volume structure.

Settings are already optimized.

You just have to setup your Buy / Sell alerts.

My Ultimate Reversal Probability Signal (Adaptive)Adaptive indicator combining RSI, T3, ZigZag, Torben, TDI, POB, and reversal probability (credit to original Author) to identify potential trend reversals with customizable settings.

My Ultimate Reversal Probability Signal (Adaptive)

Overview:

This advanced technical indicator is designed to help traders identify potential trend reversals by combining multiple analytical methods into a single, customizable tool. It integrates adaptive RSI, T3 Moving Average, ZigZag Multi-Scale, Torben Moving Median, Trend Direction Index (TDI), Point of Balance (POB) Oscillator, and a Trend Reversal Probability model. The indicator provides clear visual signals and a detailed table for real-time market analysis, making it suitable for traders of all experience levels.

Key Features:

Adaptive RSI: Dynamically adjusts RSI length based on market volatility, with customizable min/max lengths (5–50).

T3 Moving Average: Smooths price data with adaptive length (5–50) for trend detection.

ZigZag Multi-Scale: Identifies key swing points with adaptive length (3–20) and plots an average line.

Torben Moving Median: Provides robust trend bands using a median-based approach (5–50).

Trend Direction Index (TDI): Assesses future trend direction with adaptive length (3–7) and ADX integration.

Point of Balance (POB) Oscillator: Measures market equilibrium with adaptive length (5–50).

Trend Reversal Probability: Estimates reversal likelihood using a statistical model based on SMA crossovers.

Reversal Zones: Highlights overbought/oversold conditions with RSI-based zones (default: 70/30).

Future Trend Visualization: Projects potential price movements using volume delta analysis.

Comprehensive Table: Displays real-time values for RSI length, T3 length, ZigZag length, Torben length, TDI length, POB length, Delta1, and reversal probability.

Backtesting Metrics: Tracks win rate, profit factor, and total trades within a user-defined date range.

Customizable Settings: Extensive input options for enabling/disabling components, adjusting lengths, and tweaking volatility influence.

How It Works:

The indicator combines multiple signals to generate buy/sell conditions, visualized as upward (▲) or downward (▼) arrows on the chart. Each component (RSI, T3, etc.) can be enabled or disabled via the settings panel, allowing traders to tailor the tool to their strategy. The adaptive lengths adjust dynamically based on market conditions, ensuring relevance across different timeframes and assets. A table in the bottom-left corner provides a snapshot of key metrics, including the newly added Delta1 (volume delta for the first period), enhancing decision-making.

Usage Tips:

Timeframes: Works on any timeframe, but higher timeframes (e.g., 1H, 4H, Daily) may reduce noise.

Assets: Suitable for stocks, forex, cryptocurrencies, and commodities.

Confirmation: Combine with price action or other indicators for stronger signals.

Settings: Adjust RSI overbought/oversold levels (default 70/30) and enable/disable components to match your trading style.

Backtesting: Use the built-in win rate and profit factor metrics to evaluate performance within a custom date range.

Settings:

Main Settings: ATR period (14), RSI length (min 5, max 50, default 14).

Signal Filtering: Enable/disable T3, ZigZag, VolDelta, Torben, TDI, POB, Reversal Probability, and Reversal Zones.

T3 Settings: Adaptive/static length (5–50), volume factor (0.7), volatility influence (0.3).

VolDelta Settings: Adaptive/static length (3–20), volatility influence (0.3).

Torben Settings: Adaptive/static length (5–50), volatility influence (0.3).

Trend Reversal Settings: Adaptive/static length (5–50), SMA periods (5/34).

TDI Settings: Adaptive/static length (3–7), ATR/ADX periods (14), smoothing factor (0.5).

POB Settings: Adaptive/static length (5–50), volatility influence (0.3).

Colors: Customize up/down colors and volatility band display.

Backtest Date Range: Set start/end dates for performance metrics.

Visual Elements:

Plots: T3 line, ZigZag average line, Torben bands, volatility bands, reversal zones.

Shapes: Buy (▲) and sell (▼) signals, T3 crossover markers (🞛).

Boxes: Volume delta-based future trend boxes (drawn on the last bar).

Table: Displays adaptive lengths, Delta1, and reversal probability.

Labels: Optional reversal labels for overbought/oversold conditions.

Intended Audience:

Day traders seeking precise reversal signals.

Swing traders analyzing multi-timeframe trends.

Technical analysts combining multiple indicators.

Beginners learning adaptive indicator mechanics.

Disclaimer:

This indicator is for educational and analytical purposes only. It does not guarantee profits or predict future market movements. Always conduct your own research, use proper risk management, and consider market conditions before trading. The author is not responsible for any financial losses incurred.

Feedback:

I welcome your feedback and suggestions to improve this indicator. Please share your experience in the comments or contact me directly. Happy trading!

Williams Percent Range with ThresholdEnhance your trading analysis with the "Williams Percent Range with Threshold" indicator, a powerful modification of the classic Williams %R oscillator. This custom version introduces customizable uptrend and downtrend thresholds, combined with dynamic candlestick coloring to visually highlight market trends. Originally designed to identify overbought and oversold conditions, this script takes it a step further by allowing traders to define specific threshold levels for trend detection, making it a versatile tool for momentum and trend-following strategies.

Key Features:

Customizable Thresholds: Set your own uptrend (default: -16) and downtrend (default: -67) thresholds to adapt the indicator to your trading style.

Dynamic Candlestick Coloring: Candles turn green during uptrends, red during downtrends, and gray in neutral conditions, providing an intuitive visual cue directly on the price chart.

Flexible Length: Adjust the lookback period (default: 50) to fine-tune sensitivity.

Overlay Design: Integrates seamlessly with your price chart, enhancing readability without clutter.

How It Works:

The Williams %R calculates the current closing price's position relative to the highest and lowest prices over a specified period, expressed as a percentage between -100 and 0. This version adds trend detection based on user-defined thresholds, with candlestick colors reflecting the trend state. The indicator plots the %R line with color changes (green for uptrend, red for downtrend) and includes dashed lines for the custom thresholds.

Usage Tips:

Use the uptrend threshold (-16 by default) to identify potential buying opportunities when %R exceeds this level.

Apply the downtrend threshold (-67 by default) to spot selling opportunities when %R falls below.

Combine with other indicators (e.g., moving averages or support/resistance levels) for confirmation signals.

Adjust the length and thresholds based on the asset's volatility and your trading timeframe.

Delta Weighted Momentum Oscillator @MaxMaserati DELTA WEIGHTED MOMENTUM OSCILLATOR

This advanced indicator analyzes the battle between buyers and sellers by measuring volume distribution within each candle. Unlike traditional volume indicators, it reveals WHO is winning the fight - buyers or sellers - and shows you when smart money is accumulating or distributing.

📊 KEY FEATURES:

- Normalized 0-100 scale (works on any timeframe/instrument)

- Real-time delta pressure detection

- Cumulative session flow tracking

- Volume-weighted signal confirmation

- Smart money flow detection

- Multi-signal system (triangles, circles, diamonds)

- Customizable signal sizes and colors

- Professional info panel

🎯 TRADING SIGNALS EXPLAINED:

🔺 TRIANGLES (Main Entry Signals):

- Green Triangle UP: Buying pressure takes control (above 50 line)

- Red Triangle DOWN: Selling pressure takes control (below 50 line)

- Best used with volume confirmation

⚫ CIRCLES (Zone Confirmations):

- Green Circle: Strong bullish zone entry (above 70)

- Red Circle: Strong bearish zone entry (below 30)

- Use for position additions or late entries

💎 DIAMONDS (Extreme Warnings):

- Green Diamond: Extreme bullish levels (above 85) - Consider profit-taking

- Red Diamond: Extreme bearish levels (below 15) - Consider profit-taking

🎨 VISUAL ELEMENTS:

📏 KEY LINES:

- Black Dotted Line (50): The decision zone - above = bullish control, below = bearish control

- Main Delta Line: Real-time buying vs selling pressure (thick line)

- Cumulative Flow Line: Session's net money flow direction (thin line)

- Volume Area: Bottom colored area showing participation levels

🎨 BACKGROUND ZONES:

- Light Green: Bullish zones (70-85)

- Light Red: Bearish zones (15-30)

- Stronger colors: Extreme zones (above 85 / below 15)

📋 INFO PANEL:

- Delta: Current pressure reading (0-100)

- Cumulative: Session's total flow direction

- Volume: Current participation level

- Trend: Overall market sentiment

- Signal: Current recommended action

⚙️ CUSTOMIZATION OPTIONS:

- Session length (for cumulative tracking)

- Lookback period (for normalization)

- Delta smoothing (noise reduction)

- Zone thresholds (bullish/bearish/extreme levels)

- Signal sizes (tiny/small/normal)

- All colors and visual elements

- Show/hide any component

⚠️ REVERSAL SIGNALS:

1. Watch for diamonds in extreme zones

2. Look for divergence between delta and price

3. Wait for opposite triangle for confirmation

4. Manage risk carefully in extreme zones

💡 PRO TIPS:

- Don't trade triangles alone - wait for circle confirmation

- Higher volume = stronger signals

- The 50 line is your key decision point

- Diamonds = caution, not new entries

- Cumulative line shows session bias

- Works best when delta aligns with price action

⚡ BEST TIMEFRAMES:

- 1-5 minutes: Scalping and day trading

- 15-60 minutes: Swing trading

- Daily: Position trading and trend analysis

🎯 UNIQUE ADVANTAGES:

- Normalized scale works on any market

- Combines delta, volume, and flow analysis

- Clear visual hierarchy

- Professional-grade normalization

- Real-time smart money detection

- Session-based cumulative tracking

This indicator is perfect for traders who want to understand the real market sentiment beyond just price action. See exactly when institutions are buying or selling, and trade with the smart money flow!

RSS-Stochastik [afterworktrading]Hi all,

this is the first script from the series "afterworktrading". The goal is to develop and provide tools for traders with a fulltime job or little time for trading/analyzing charts.

Over time some of the scripts will also be linked to complete trading systems.

Let's start with my favourite one, the "RSS-Stochastik" with alert function.

The RSS-concept (Relative Spread Strength, developed by Ian Copsey) is based on the variance between a "short" and a "long" moving averages (or "slow" and "fast"), here between two EMA.

This variance is calculated and plotted in a RSI-diagram to show "overbought" and "oversold" conditions, helping to identify an ideal entry setup for trend continuation or catching a possible reversal.

Compared to the conventional RSI etc., possible reversal or trend continuation areas are often better represented in terms of quality, as an example see the Amazon-Chart.

The EMA-values, limit value thresholds and background colors can be set in the script. As a special feature, alarms can be set to be notified when a value has reached the extreme range. This reduces the screen time to the minimum.

In my personal trading, this indicator forms the basis for almost all trades, but is not a pure signal indicator on its own.

However, the informative value can be further improved if volume or support/resistance zones etc. are linked to the RSS, see example NASDAQ future with support zone price or 200 EMA.

Example for a possible RSS-Trade-Setup:

- choose an asset with a strong trend

- set alerts for crossing the oversold or overbought condition in direction of the trend

- in case of an alert check possible support/resistance areas on the current chart level (EMA, price zones, volume zones, anchored VWAP etc.)

- trade in the direction of the trend using your preferred entry setup

In my opinion, the system can be used very well, especially in trend phases, in order to obtain optimal entries.

Does it works also on lower timeframes?

Yes, it might work on every timeframe with a strong trend of high quality. Please see attached a 5m-Chart of GPBUSD-pair, notice the signal quality in direction of the trend.

Like every trading system this is not the "holy grail setup" and you will have losing trades. But handling this indicator with care you can have better entries especially in trend direction with less screen time due to the alert function.

Good luck with it! Further indicators will be published in the coming months, some will also be based on the RSS system.

As always: no liability for losing trades, no investment advice etc. Observe the risk limit for every trade!

Signalgo BBSignalgo BB: Technical Overview

Signalgo BB is a Bollinger Bands (BB) indicator for TradingView, designed to provide a multi-dimensional view of volatility, trend, and trading opportunities within a single overlay. Below is a detailed, impartial explanation of its workings, inputs, and trading logic.

Core Mechanics

Signalgo BB operates on the principle of nested volatility bands and moving averages. It calculates:

Fast & Slow Bands: Two sets of Bollinger Bands (BB), using different moving average types (EMA or SMA), lengths, and standard deviation multipliers.

Volatility Cloud: A dynamic visual layer indicating when price is inside both, one, or neither band.

Filtering: A short-term RSI is used to confirm trend direction and filter out weak signals.

Inputs & Components

MA Type: Choice between EMA, SMA for both fast and slow MA calculations.

Fast/Slow Lengths

Fast/Slow Deviations

RSI Length/Thresholds

Show Cloud: Toggle for the visual volatility cloud.

Signal Mode: Band Break.

Prevent Repeated Signals: Option to suppress duplicate signals in the same direction.

TP/SL & Trailing Logic: Advanced, automated trade management with ATR-based distances, three take-profit levels, and a dynamic trailing stop.

Signal Generation

Band Break: Triggers when price crosses the fast BB band.

RSI Filter: All signals require RSI confirmation.

Prevent Repeated Signals: Optionally only marks the first breakout in a series to reduce overtrading.

Entry/Exit Marks: Labels are plotted for visual clarity, and signals can trigger TradingView alerts.

Trade Management

Stop Loss (SL): Set at a multiple of ATR from the entry price, adapting to current volatility.

Take Profits (TP1, TP2, TP3): Three levels scaled by risk-reward ratios, supporting partial exits.

Trailing Stop: After the first TP is hit, SL moves to breakeven and then trails at a user-defined multiple of ATR, locking in further gains.

Event Markers: Each TP, SL, and trailing stop event is labeled on the chart.

Direction State: The indicator tracks active trades, allowing for only one open position per direction at a time.

Cloud Visualization: The background color changes depending on whether price is inside both, one, or no bands, making it easier to visualize market conditions.

Multiple Signal Logics: It doesn’t just look at breakouts, it includes cloud crossings, mean reversion, and a choice of how to combine them.

Rigorous Filtering: Signals require RSI trend confirmation, reducing false entries during weak phases.

Automated Trade Management: Built-in TP/SL and trailing logic, dynamically adapting to volatility.

Signal Suppression: Option to prevent repeated signals, reducing noise and overtrading.

Customizable MA Types: Supports EMA, SMA, and a selection algorithm for future expansion.

Trading Strategy Application

Volatility Regimes: The cloud’s color indicates whether price is inside, between, or outside the bands, helping traders identify trending, ranging, or breakout conditions.

Signals: entries can be based on breakouts filtered by RSI trend strength.

Risk Management: All active trades are managed by TP/SL logic, trailing stops after TP1, and visual feedback on exits.

Visual Alerts: Both signals and TP/SL events are marked on the chart for manual review.

Flexibility: Users can switch modes or suppress repeated signals as needed, depending on trading style.

Practical Usage

Intraday to Swing: Suitable for timeframes from minutes to days, depending on the MA periods and volatility profile.

Manual or Automated: The visual overlay and alerts support both manual trading and automated strategies.

Education & Review: The colored cloud and event markers make it easy to review past price action and learn from signals.

What separates this indicator from traditional ones:

1. Dual Bollinger Bands

Traditional: Most indicators use a single set of Bollinger Bands (two standard deviations above/below a moving average).

Signalgo BB: Implements two sets of bands—a "fast" set (shorter moving average, narrower deviation) and a "slow" set (longer moving average, wider deviation). This provides both immediate (fast) and broader context (slow) for volatility and price action.

2. Volatility Cloud Visualization

Traditional: Standard Bollinger Bands display as two lines, with the area between sometimes shaded as a "band" but without dynamic color changes.

Signalgo BB: The background is colored differently depending on whether price is within both, one, or neither band, offering a visual "cloud" that distinguishes trending, ranging, or breakout regimes at a glance.

3. RSI Filtering

Traditional: Many indicators either don’t filter signals, or if they do, it’s not always configurable.

Signalgo BB: Adds an optional RSI filter, requiring signals to be confirmed by short-term RSI overbought/oversold conditions. This reduces false signals in range-bound or low-trend environments.

4. Prevention of Repeated Signals

Traditional: Most indicators will keep firing signals as long as conditions are met, which can cause overtrading.

Signalgo BB: Offers a user-toggleable option to suppress repeated signals in the same direction until the opposite signal occurs. This reduces noise for discretionary traders.

5. Integrated Trade Management

Traditional: Manual or separate coding is required for stop-loss, take-profit, and trailing stop logic.

Signalgo BB: Builds in dynamic, ATR-based stop-loss; up to three take-profit levels and a trailing stop that activates after the first TP is hit. All levels are visually plotted on the chart, and events (TP/SL hits) are labeled, aiding strategy review and automation.

6. Event Labeling and Alerts

Traditional: Alerts may exist for entry/exit, but rarely for each TP/SL event.

Signalgo BB: Places labels for every entry, exit, and TP/SL event. It also provides TradingView alertconditions for each event, enabling automated notifications or integration with trading bots.

7. Directional State Tracking

Traditional: Indicators typically do not track the "state" of a trade (e.g., active long/short/flat) beyond simple signals.

Signalgo BB: Maintains persistent variables for entry price, SL, TP, trailing stop, and trade direction, ensuring only one active signal per direction. This prevents overlapping entries and mimics realistic trade management.

8. User Customization

Traditional: Default settings are often hardcoded, or customization is limited.

Signalgo BB: Offers extensive user inputs for MA type and TP/SL logic—making the tool adaptable to many strategies and timeframes.

BanShen MACD Ultimate Multi Signal System[SpeculationLab]🧠 How This Script Works (Detailed Logic Breakdown)

This script is a closed-source, fully self-developed modular trading system centered around MACD divergence detection. It also includes auxiliary modules such as:

Vegas Tunnel trend filtering

Dynamic ATR-based stop placement

Engulfing candlestick pattern detection

RSI/OBV divergence modules

Fair Value Gap (FVG) recognition

A smart signal panel that consolidates all signals in real time

These components work together through a signal resonance framework, helping traders identify high-confluence, high-probability entry opportunities.

🔍 Why MACD Divergence Is the Core (Real-World Strategy Basis)

This system is based on a real-world trading strategy I’ve personally used and refined over time.

Through discretionary trading and backtesting, I discovered that divergence between price action and the MACD histogram — especially when certain structural conditions are met — produces a very high win rate.

Key observations include:

MACD peaks/troughs that are clean and well-shaped (defined pivot structure)

Large vertical differences between two MACD histogram extremes

Price making a higher high or lower low, while MACD does the opposite

Two or more divergences appearing consecutively, which creates a powerful reversal signal

These setups have proven extremely reliable in my experience. This script automates the detection of these conditions using strict logic filters.

🔷 1. MACD Divergence Engine (Core Module)

At its core, this script implements a multi-layered MACD divergence detection system, capable of identifying both **regular** and **consecutive** bullish/bearish divergences.

Key components of the logic:

- **Pivot-Based Peak Detection:**

Peaks and troughs in the MACD histogram are located using left/right lookback lengths.

These define valid turning points by requiring the center bar to be the highest (or lowest) compared to its neighbors.

- **Peak Size Thresholding:**

The height of the histogram peaks is compared to the standard deviation of MACD values.

Only peaks above a configurable multiplier (e.g., 0.1× stdev) are considered significant, filtering out noise.

- **Peak Ratio Filtering:**

For divergence to be valid, the size ratio between two histogram peaks must exceed a minimum threshold.

This prevents "flat" divergences with no meaningful MACD movement from triggering false signals.

- **Noise Suppression:**

A customizable threshold filters out weak histogram fluctuations between divergence points.

- **Price Action Confirmation:**

The divergence is only confirmed when the price forms a new high or low (depending on the type), and the MACD forms an opposing structure.

- **Consecutive Divergence Detection:**

For high-conviction setups, the script detects sequences of two or more divergences in the same direction.

These use stricter filters and flag rare but powerful market turning points.

Signals are plotted using plotshape() with visual differentiation between regular and consecutive setups. You can enable/disable each type individually.

⏰ Note: Histogram colors are styled similarly to TradingView’s built-in MACD for visual familiarity. However, this script is built entirely from scratch and does not reuse any internal TV code.

---

🔷 2. Trend Filtering via Vegas Tunnel

The **Vegas Tunnel** module plots 5 configurable EMAs (default: 12, 144, 169, 576, 676) to evaluate trend direction.

The trend is considered **bullish** when short EMAs (144/169) are positioned above long EMAs (576/676), and the price is interacting with the short EMA tunnel.

Conversely, a bearish condition is detected when the opposite is true.

A visual triangle marker highlights trend zones, and users can hide/show individual EMAs.

---

🔷 3. ATR-Based Dynamic Stop Loss

This module plots dynamic stop levels above and below the current price based on ATR.

Default setting uses 13-period ATR, and users can customize the multiplier or disable the plot.

It serves as a visual guide for risk management in live trades.

---

🔷 4. Engulfing Pattern Recognition

Candlestick-based signal detection:

- **Bullish Engulfing** occurs when a candle closes above the prior high, and the prior bar is bearish.

- **Bearish Engulfing** when a candle closes below the prior low, and the prior bar is bullish.

Users can modify the logic to use open/close levels for looser or stricter detection.

These patterns are highlighted using plotshape markers and optionally included in the signal table.

---

🔷 5. RSI and OBV Divergence Modules

These modules follow similar logic to the MACD engine:

- Use pivotlow() / pivothigh() to detect swing points.

- Confirm divergence only when price moves in one direction while RSI or OBV moves in the opposite direction.

- Require a minimum distance (in bars) between the two pivots.

- Require a certain ratio between two indicator values and their corresponding prices.

You can only enable **one of MACD/RSI/OBV divergences at a time** to avoid visual overlap, as they share the same subplot.

---

🔷 6. FVG (Fair Value Gap) Auto Detection

This module detects large single-direction price moves where price leaves a visible gap between candle 3 bars ago and 1 bar ago.

- **Bullish FVG**: high < low

- **Bearish FVG**: low > high

ATR-based filters are applied to eliminate minor gaps.

Each gap is drawn as a box and optionally extended, with a central line marking the midpoint (CE - Consequent Encroachment) level.

Traders often look for price to return to this level as an entry signal.

---

🔷 7. Smart Signal Table

All active signals (MACD, Vegas, RSI, OBV, Engulfing) are collected into a **real-time table** that displays current market bias.

- Each module reports whether it is currently giving a bullish (🟢) or bearish (🔴) condition.

- Helps users assess signal alignment (confluence).

- The table is updated every bar and appears in the bottom-right corner.

---

🔷 8. Watermark & Branding

The watermark displays the script name and author at the top-right, and can be toggled via settings.

📌 Not a Mashup — Structured System, Not a Stack of Indicators

⚠️ This is not a random mashup of unrelated indicators.

Every module in this system was intentionally designed to support the core MACD divergence logic by filtering, validating, or amplifying its signals.

Here's how the system achieves signal confluence and structure:

Vegas Tunnel acts as a macro trend filter, helping users determine whether to favor long or short trades.

For example, bullish MACD divergence is more reliable when confirmed by an uptrend in the Vegas EMAs. This prevents users from trading against momentum.

Engulfing Patterns serve as entry-level price action confirmation.

When a bullish engulfing candle appears near a MACD bullish divergence — and trend conditions from Vegas are aligned — the confluence increases dramatically.

This is especially powerful when multiple modules confirm in the same direction on the right side of the chart.

RSI and OBV Divergence modules offer redundant but independent momentum views.

Users may enable them selectively to validate MACD signals, or to use them as standalone alternatives when MACD is flat or noisy.

FVG Zones provide context for entries or targets.

For instance, a MACD bullish divergence forming near a bullish FVG gap increases the odds of reversal.

Price often "fills" these imbalances, which aligns well with reversal setups.

The Smart Signal Table aggregates signals from all modules and provides a visual, real-time overview of the current market bias.

This allows traders to act only when multiple signals are aligned — for example, when MACD is bullish, trend is up, and a bullish engulfing just printed.

Together, this framework creates a coherent decision-making system, where each tool has a defined role: trend filtering, signal confirmation, risk management, or entry detection.

🧩 It is modular in architecture, but not modular in purpose.

This system was not built by stacking indicators, but by integrating logic across modules to support a high-conviction MACD-based strategy.

🧬 Originality Statement

This script is entirely original, developed from scratch without using external libraries or public script code. The logic is fully custom, especially the consecutive divergence detection system and signal integration.

⚠️ Disclaimer

This script is for educational and informational purposes only and does not constitute financial advice. Trade at your own risk.

---

📘 中文简要说明:

这是一个完全原创、闭源的交易系统,核心逻辑为 MACD 柱状图背离信号的识别,配合多模块共振判断,构建出一个高胜率的多信号共振策略。

本指标模块化结构清晰,主要包括:

- MACD 背离识别(支持连续背离)

- Vegas EMA 隧道趋势过滤

- RSI / OBV 背离模块

- 吞没形态识别

- FVG 平衡区间自动标注

- ATR 动态止损提示

- 智能信号面板(整合所有信号并可视化)

所有模块均可单独开启/关闭,适配顺势、逆势或多周期的交易风格。

本脚本为个人实战策略的程序化实现,逻辑完全由零开发,未使用任何公用代码。适合希望提高交易胜率和信号精准度的用户使用。

免责声明:本指标仅用于技术分析学习与参考,不构成任何投资建议。请您独立判断,自行承担交易风险。

Elite RSI Strategy Elite RSI Strategy

________________________________________

🔍 Overview

The Elite RSI Strategy combines multiple technical indicators into a unified visual toolkit, providing deep insights into market strength, reversals, and momentum shifts. Designed for serious traders who value confluence, clarity, and customizability.

________________________________________

📊 Core Components

🔸 Relative Strength Index (RSI)

• Classic RSI calculation with customizable length and price source.

• Dynamic background shading on RSI/MA crosses.

• Gradient fills highlight overbought and oversold zones.

• Alerts on RSI-MA crossovers for bullish or bearish momentum signals.

🔸 Smoothing Moving Averages (MA)

• Choose from SMA, EMA, SMMA, WMA, or VWMA.

• Configurable length and style.

• MA plotted over RSI for cross signal visualization.

________________________________________

🔸 WaveTrend Oscillator (WT)

• Built-in WaveTrend calculation using dual smoothing.

• Color-coded histogram based on oscillator direction:

o 🟢 Green: Bullish momentum

o 🔴 Red: Bearish momentum

• Optional candle coloring based on WT sentiment.

• Alert system for WT trend shifts.

________________________________________

🔸 Money Flow Index (MFI)

• Centered around 0 for clear trend polarity:

o Positive → Bullish Bias

o Negative → Bearish Bias

• Includes custom MFI smoothing, not available in standard indicators.

• Custom levels plotted: +30, +15, 0, -15, -30 for confluence.

• Dynamic color changes on zero-line crosses.

• Alert-ready behavior on trend shifts.

________________________________________

🖌️ Customization & Styling

• Toggle visibility for:

o RSI

o WT

o MFI

o Bar Colors

o Level Lines

• Style options for all plot types: line, area, or columns.

• Full color customization for bullish and bearish signals.

________________________________________

🚨 Built-In Alerts

• 📈 RSI crosses above MA

• 📉 RSI crosses below MA

• 🔄 RSI/MA Cross (any)

• 🟢 WT turns Bullish

• 🔴 WT turns Bearish

• 🔁 WT Direction Change

________________________________________

🧠 Why Use Elite RSI Strategy?

• Combines momentum, volume flow, and trend structure.

• Helps filter false signals through multi-layer confluence.

• Increases confidence in entry/exit decisions.

• Fully customizable to suit any trading style.

________________________________________

Disclaimer:

This indicator script is intended for educational and informational purposes only. It does not constitute investment advice or a recommendation to buy or sell any asset.

Always seek guidance from a licensed financial advisor or broker. You are solely responsible for your own trading decisions.

Thank you.

[Pandora] Laguerre Ultimate Explorations MulticatorIt's time to begin demonstrations differentiating the difference between known and actual feasibility beyond imagination... Welcome to my algorithmic twilight zone .

INTRODUCTION:

Hot off my press, I present this Laguerre multicator employing PSv6.0, originally formulated by John Ehlers for TASC - July 2025 Traders Tips. Basically I transcended Ehlers' notions of transversal filtration with an overhaul of his Laguerre design with my "what if" Pandora notions included. Striving beyond John Ehlers' original intended design. This action packed indicator is a radically revamped version of his original filter using novel techniques. My aim was to explore whether providing even more enhanced responsiveness and lesser lag is possible and how. Presented here is my mind warping results to witness.

EHLERS' LAGUERRE EXPLAINED:

First and foremost, the concept of Ehlers' Laguerre-izing method deserves a comprehensive deep dive. Ehlers' Laguerre filter design, as it functions originally, begins with his Ultimate Smoother (US) followed by a gang of four LERP (jargon for Linear intERPolation) filters. Following a myriad of cascading LERPs is a window-like FIR filter tapped into the LERP delay values to provide extra smoothness via the output.

On a side note, damping factor controlled LERP filters resemble EMAs indeed, but aren't exactly "periodic" filters that would have a period/length parameter and their subsequent calculations. I won't go into fine-grained relationship details, but EMA and LERP are indeed related in approach, being cousins of similar pedigree.

EXAMINING LAGUERRE:

I focused firstly on US initialization obstacles at Pine's bar_index==0 with nz() in abundance. The next primary notion of intrigue I mostly wondered about was, why are there four LERP elements instead of fewer or more. Why not three or why not two LERPs, etc... 1-4-6-4-1, I remember seeing those coefficients before in high pass filters.

Gathering my thoughts from that highpass knowledge base, I devised other tapped configuration modes to inspect their behavior out of curiosity. Eureka! There is actually more to Laguerre than Ehlers' mind provided, now that I had formulated additional modes. Each mode exhibits it's own lag/smoothness characteristics better than the quad LERPed version. I narrowed it down to a total of 5 modes for exploration. Mode 0 is just the raw US by itself.

ANALYZING FILTER BEHAVIORS:

Which option might be possibly superior, and how may I determine that? Fortunately, I have a custom-built analyzer allowing me to thoroughly examine transient responses across multiple periodicities simultaneously, providing remarkable visual insights.

While Ehlers has meagerly touched upon presenting general frequency responses in his books, I have excelled far beyond that. This robust filter analysis capability enables me to observe finer aspects hidden to others, ultimately leading to the deprecation of numerous existing filters. Not only this, but inventing entirely new species of filtration whether lowpass, highpass, or bandpass is already possible with a thorough comprehensive evaluation.

Revealing what's quirky with each filter and having the ability to discover what filters may be lacking in performance, is one of it's implications. I'm just going to explain this: For example US has a little too much overshoot to my liking, along with nonconformant cutoff frequency compliance with the period parameter. Perhaps Ehlers should inspect US coefficients a bit closer... I hope stating this is not received in an ill manner, as it's not my intention here.

What this technically eludes to is that UltimateSmoother can be further improved, analogous to my Laguerre alterations described above. I will also state Laguerre can indeed be reformulated to an even greater extent concerning group delay, from what I have already discussed. Another exciting time though... More investigative research is warranted.

LAGUERRE CONCLUSIONS:

After analyzing Laguerre's frequency compliance, transient responses, amplitudes, lag, symmetry across periodicities, noise rejection, and smoothness... I favor mode 3 for a multitude of reasons over the mode 4 configuration, but mostly superb smoothing with less lag, AND I also appreciated mode 1 & 2 for it's lower lag performance options.

Each mode and lag (phase shift) damping value has it's own unique characteristics at extremes, yet they demonstrate additional finesse in it's new hybrid form without adding too much more complexity. This multicator has a bunch of Laguerre filters in the overlay chart over many periodicities so you can easily witness it's differing periodic symmetries on an input signal while adjusting lag and mode.

LAGUERRE OSCILLATOR:

The oscillator is integrated into the laguerreMulti() function for the intention of posterity only. I performed no evaluation on it, only providing the code in Pine. That wasn't part of my intended exploration adventure, as I'm more TREND oriented for the time being, focusing my efforts there.

Market analysis has two primary aspects in my observations, one cyclic while the other is trending dynamics... There's endless oscillators, but my expectations for trend analysis seems a little lesser explored in my opinion, hence my laborious trend endeavors. Ehlers provided both indicator facets this time around, and I hope you find the filtration aspect more intriguing after absorption of this reading.

FUNCTION MODULES EXPLAINED:

The Ultimate Smoother is an advanced IIR lowpass smoothing filter intended to minimize noise in time series data with minimal group delay, similar to a traditional biquad filter. This calculation helps to create a smoother version of the original signal without the distortions of short-term fluctuations and with minimal lag, adjustable by period.

The Modified Laguerre Lowpass Filter (MLLF) enhances the functionality of US by introducing a Laguerre mode parameter along side the lag parameter to refine control over the amount of additional smoothing/lag applied to the signal. By tethering US with this LERPed lag mechanism, MLLF achieves an effective balance between responsiveness and smoothness, allowing for customizable lag adjustments via multiple inputs. This filter ends with selecting from a choice of weighted averages derived from a gang of up to four cascading LERP calculations, resulting with smoother representations of the data.

The Laguerre Oscillator is a momentum-like indicator derived from the output of US and a singular LERPed lowpass filter. It calculates the difference between the US data and Laguerre filter data, normalizing it by the root mean square (RMS). This quasi-normalization technique helps to assess the intensity of the momentum on any timeframe within an expected bound range centered around 0.0. When the Laguerre Oscillator is positive, it suggests that the smoothed data is trending upward, while a negative value indicates a downward trend. Adjustability is controlled with period, lag, Laguerre mode, and RMS period.

MVRV Altcoins📌 Technical Description of Indicator: MVRV Altcoins

This advanced script calculates the Market Value to Realized Value (MVRV) ratio across multiple cryptocurrencies simultaneously. It offers two analytical modes: Normal and Z-Score, optimized for visual comparison and real-time monitoring of up to 13 predefined assets. If a user applies the indicator to a symbol that is not among the 13 programmed assets, the default behavior displays the Bitcoin chart as a fallback reference.

🔍 What Is MVRV and Why Is It Important?

MVRV is an on-chain metric designed to assess whether a cryptocurrency is overvalued or undervalued by comparing its market capitalization to its realized capitalization.

- Market Cap: The total circulating supply multiplied by the current market price.

- Realized Cap: The sum value of all coins based on the price at the time they last moved on-chain, offering a time-weighted valuation.

Normal Calculation:

MVRV_Normal = Market Cap / Realized Cap

This version reflects investor profitability and identifies potential accumulation or distribution zones.

📊 Z-Score Calculation:

MVRV_ZScore = (Market Cap − Realized Cap) / Standard Deviation of Market Cap

This formula evaluates how extreme the current market conditions are compared to historical norms. It normalizes the difference using statistical dispersion, turning it into a volatility-aware metric that better reflects valuation extremes.

🔎 How Market Cap Is Computed

Unlike conventional indicators relying on consolidated feeds, this script uses modular components from CoinMetrics to construct the active capitalization more accurately, especially for altcoins. Here's the breakdown:

Active Capitalization = MARKETCAPFF + MARKETCAPACTSPLY

Realized Capitalization = MARKETCAPREAL

Component Definitions:

- MARKETCAPFF: Market Cap Free Float — total valuation based only on truly circulating coins.

- MARKETCAPACTSPLY: Capitalization from actively circulating supply — filters dormant or locked coins.

- MARKETCAPREAL: Realized Cap — historical valuation weighted by the last on-chain movement of each coin.

This method offers enhanced precision and compatibility across assets that may lack comprehensive data from centralized providers.

⚙️ User-Configurable Parameters

- MVRV Mode: Choose between Normal and Z-Score.

- Percentage Scale View: If enabled, visual output is scaled using predefined divisors (100 / 3.5 or 100 / 6).

- Thresholds for Analysis:

- Normal mode: Define overbought and oversold levels (default 1.0 and 3.5).

- Z-Score mode: Configure statistical boundaries (default 0.0 and 6.0).

- Table Controls: