Previous Day OHLC Dashboard (Last N Days)Indicator: Previous Day OHLC Dashboard (Multi-Day)

This indicator displays a dashboard-style table on your chart that shows the Open, High, Low, and Close (OHLC) of the previous trading days. It’s designed to help traders quickly reference key daily levels that often act as important support and resistance zones.

🔑 Features:

Dashboard Table: Shows OHLC data for the last N trading days (default = 3, up to 10).

Customizable Appearance:

Change the position of the dashboard (Top-Right, Top-Left, Bottom-Right, Bottom-Left).

Adjust text size (Tiny → Huge).

Customize colors for header, labels, and each OHLC column.

Yesterday’s OHLC Lines (optional): Plots horizontal lines on the chart for the previous day’s Open, High, Low, and Close.

Intraday & Multi-Timeframe Compatible: Works on all timeframes below Daily — values update automatically from the daily chart.

📊 Use Cases:

Quickly identify yesterday’s key levels for intraday trading.

Track how current price reacts to previous day’s support/resistance.

Keep a multi-day reference for trend bias and range context.

⚙️ How it Works:

The indicator pulls daily OHLC values using request.security() with lookahead_on to ensure prior day’s values are extended across the next session.

These values are displayed in a compact table for quick reference.

Optionally, the most recent daily levels (D-1) are plotted as chart lines.

✅ Perfect for day traders, scalpers, and swing traders who rely on yesterday’s price action to plan today’s trades.

Educational

OSOK KatxumotoThe OSOK Dynamic Box Enhanced is designed for scalpers and traders using the OSOK (One Shot, One Kill) method on futures like the NQ.

Features include:

A midline that dynamically follows the current price in real-time.

Upper (LS) and lower (LI) protection lines at configurable distances from the current price, representing stop or protection levels.

Target lines offset from LS and LI according to your risk/reward strategy, also fully configurable.

Customizable colors and thickness for all lines, allowing you to adapt the visualization to your trading style.

All lines automatically extend to the right from the current price, keeping the chart clean without accumulating old lines.

This indicator helps traders quickly visualize key levels, manage risk, and set objectives efficiently—perfect for scalping and high-precision setups.

Configurable parameters:

Protection distance (LS/LI) in points

Target distance from LS/LI in points

Line colors and thickness

Line extension to the right

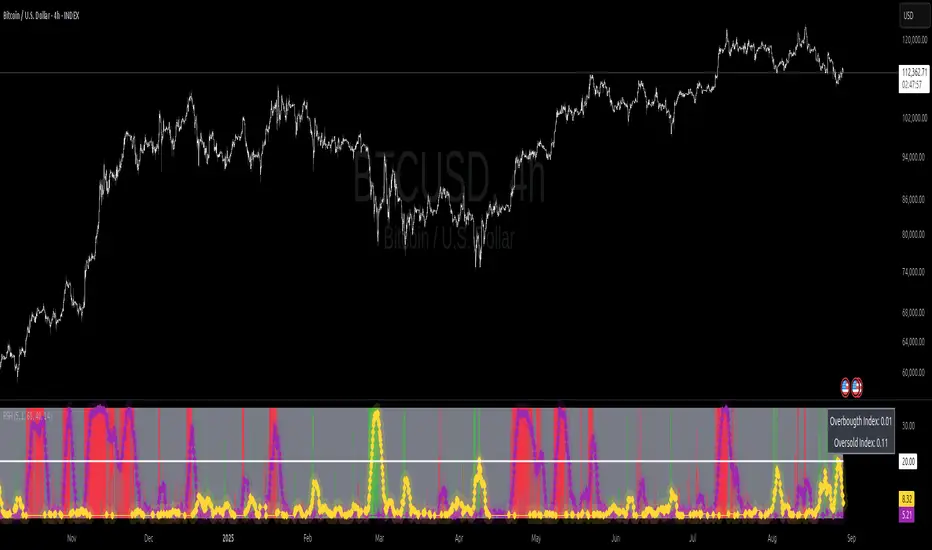

Relative Strength Heat [InvestorUnknown]The Relative Strength Heat (RSH) indicator is a relative strength of an asset across multiple RSI periods through a dynamic heatmap and provides smoothed signals for overbought and oversold conditions. The indicator is highly customizable, allowing traders to adjust RSI periods, smoothing methods, and visual settings to suit their trading strategies.

The RSH indicator is particularly useful for identifying momentum shifts and potential reversal points by aggregating RSI data across a range of periods. It presents this data in a visually intuitive heatmap, with color-coded bands indicating overbought (red), oversold (green), or neutral (gray) conditions. Additionally, it includes signal lines for overbought and oversold indices, which can be smoothed using RAW, SMA, or EMA methods, and a table displaying the current index values.

Features

Dynamic RSI Periods: Calculates RSI across 31 periods, starting from a user-defined base period and incrementing by a specified step.

Heatmap Visualization: Displays RSI strength as a color-coded heatmap, with red for overbought, green for oversold, and gray for neutral zones.

Customizable Smoothing: Offers RAW, SMA, or EMA smoothing for overbought and oversold signals.

Signal Lines: Plots scaled overbought (purple) and oversold (yellow) signal lines with a midline for reference.

Information Table: Displays real-time overbought and oversold index values in a table at the top-right of the chart.

User-Friendly Inputs: Allows customization of RSI source, period ranges, smoothing length, and colors.

How It Works

The RSH indicator aggregates RSI calculations across 31 periods, starting from the user-defined Starting Period and incrementing by the Period Increment. For each period, it computes the RSI and determines whether the asset is overbought (RSI > threshold_ob) or oversold (RSI < threshold_os). These states are stored in arrays (ob_array for overbought, os_array for oversold) and used to generate the following outputs:

Heatmap: The indicator plots 31 horizontal bands, each representing an RSI period. The color of each band is determined by the f_col function:

Red if the RSI for that period is overbought (>threshold_ob).

Green if the RSI is oversold (

Indian market session on Gift Nifty chartsGift Nifty Market Session Highlighter

This indicator highlights the official Indian market session on Gift Nifty charts — from 9:15 AM to 3:30 PM IST. It shades the background during this time window so traders can instantly identify when the local market is open.

Features:

Marks 9:15 AM to 3:30 PM (IST) session on intraday charts.

Adjustable highlight color and transparency.

Works seamlessly across lower timeframes (1m, 5m, 15m, etc.).

Helps traders align Gift Nifty activity with NSE market hours.

Use Cases:

Quickly distinguish active market hours from overnight or global sessions.

Backtest trading strategies specific to Indian session volatility.

Improv

e focus on expiry-day setups and intraday opportunities.

Disclaimer:

This tool is provided for educational and informational purposes only. It is not financial advice, nor does it guarantee trading success. Always do your own research and consult a licensed financial professional before making investment decisions.

Globex Trap w/ percentage [SLICKRICK]Globex Trap w/ Percentage

Overview

The Globex Trap w/ Percentage indicator is a powerful tool designed to help traders identify high-probability trading opportunities by analyzing price action during the Globex (overnight) session and regular trading hours. By combining Globex session ranges with Supply & Demand zones, this indicator highlights potential "trap" areas where significant price reactions may occur. Additionally, it calculates the Globex session range as a percentage of the daily Average True Range (ATR), providing valuable context for assessing market volatility.

This indicator is ideal for traders in futures markets or other instruments traded during Globex sessions, offering a visual and analytical edge for spotting key price levels and potential reversals or breakouts.

Key Features

Globex Session Tracking:

Visualizes the high and low of the Globex session (default: 3:00 PM to 6:30 AM PST) with customizable time settings.

Displays a semi-transparent box to mark the Globex range, with labels for "Globex High" and "Globex Low."

Calculates the Globex range as a percentage of the daily ATR, displayed as a label for quick reference.

Supply & Demand Zones:

Identifies Supply & Demand zones during regular trading hours (default: 6:00 AM to 8:00 AM PST) with customizable time settings.

Draws semi-transparent boxes to highlight these zones, aiding in the identification of key support and resistance areas.

Trap Area Identification:

Highlights potential trap zones where Globex ranges and Supply & Demand zones overlap, indicating areas where price may reverse or consolidate due to trapped traders.

Customizable Settings:

Adjust Globex and Supply & Demand session times to suit your trading preferences.

Toggle visibility of Globex and Supply & Demand zones independently.

Customize box colors for better chart readability.

Set the lookback period (default: 10 days) to control how many historical zones are displayed.

Configure the ATR length (default: 14) for the percentage calculation.

PST Timezone Default:

All times are based on Pacific Standard Time (PST) by default, ensuring accurate session tracking for users in this timezone or those aligning with U.S. West Coast market hours.

Recommended Usage

Timeframes: Best used on 1-hour charts or lower (e.g., 15-minute, 5-minute) for precise entry and exit points.

Markets: Optimized for futures (e.g., ES, NQ, CL) and other instruments traded during Globex sessions.

Historical Data: Ensure at least 10 days of historical data for optimal visualization of zones.

Strategy Integration: Use the indicator to identify potential reversals or breakouts at Globex highs/lows or Supply & Demand zones. The ATR percentage provides context for whether the Globex range is significant relative to typical daily volatility.

How It Works

Globex Session:

Tracks the high and low prices during the user-defined Globex session (default: 3:00 PM to 6:30 AM PST).

When the session ends, a box is drawn from the start to the end of the session, capturing the high and low prices.

Labels are placed at the midpoint of the session, showing "Globex High," "Globex Low," and the range as a percentage of the daily ATR (e.g., "75.23% of Daily ATR").

Supply & Demand Zones:

Tracks the high and low prices during the user-defined regular trading hours (default: 6:00 AM to 8:00 AM PST).

Draws a box to mark these zones, which often act as key support or resistance levels.

ATR Percentage:

Calculates the Globex range (high minus low) and divides it by the daily ATR to express it as a percentage.

This metric helps traders gauge whether the overnight price movement is significant compared to the instrument’s typical volatility.

Time Handling:

Uses PST (UTC-8) for all time calculations, ensuring accurate session timing for users aligning with this timezone.

Properly handles overnight sessions that cross midnight, ensuring seamless tracking.

Input Settings

Globex Session Settings:

Show Globex Session: Enable/disable Globex session visualization (default: true).

Globex Start/End Time: Set the start and end times for the Globex session (default: 3:00 PM to 6:30 AM PST).

Globex Box Color: Customize the color of the Globex session box (default: semi-transparent gray).

Supply & Demand Zone Settings:

Show Supply & Demand Zone: Enable/disable zone visualization (default: true).

Zone Start/End Time: Set the start and end times for Supply & Demand zones (default: 6:00 AM to 8:00 AM PST).

Zone Box Color: Customize the color of the zone box (default: semi-transparent aqua).

General Settings:

Days to Look Back: Number of historical days to display zones (default: 10).

ATR Length: Period for calculating the daily ATR (default: 14).

Notes

All times are in Pacific Standard Time (PST). Adjust the start and end times if your market operates in a different timezone or if you prefer different session windows.

The indicator is optimized for instruments with active Globex sessions, such as futures. Results may vary for non-24/5 markets.

A typo in the label "Globe Low" (should be "Globex Low") will be corrected in future updates.

Ensure your TradingView chart is set to display sufficient historical data to view the full lookback period.

Why Use This Indicator?

The Globex Trap w/ Percentage indicator provides a unique combination of session-based range analysis, Supply & Demand zone identification, and volatility context via the ATR percentage. Whether you’re a day trader, swing trader, or scalper, this tool helps you:

Pinpoint key price levels where institutional traders may act.

Assess the significance of overnight price movements relative to daily volatility.

Identify potential trap zones for high-probability setups.

Customize the indicator to fit your trading style and market preferences.

Statistical FootprintStatistical Footprint - Behavioral Support & Resistance

This indicator identifies key price levels based on actual market behavior rather than traditional pivot calculations. It analyzes how bulls and bears have historically moved price from session opens, creating statistical zones where future reactions are most likely.

The concept is simple: track how far bullish candles typically push above the open versus how far bearish candles drop below it. These patterns reveal the market's behavioral "footprint" - showing where momentum typically stalls and reverses.

Key Features:

- Separate analysis for daily and weekly timeframes

- Smart zone merging when levels cluster together (within 5 points)

- Uses both mean and median calculations for more robust levels

- XGBoost-optimized lookback periods for maximum statistical significance

- Clean zone-only display focused on actionable price areas

How it Works:

The code separates bullish and bearish sessions, measuring their typical range extensions from the open. It then projects these statistical ranges forward from current session opens, creating "behavioral zones" where the market has historically shown consistent reactions.

When daily and weekly levels align closely, they merge into combined zones with enhanced significance. Labels show both the mean and median values when they differ meaningfully.

Best Used For:

- Identifying high-probability reversal zones

- Setting profit targets based on historical behavior

- Understanding market sentiment shifts at key levels

- Confluence analysis between different timeframes

The lookback periods have been optimized using machine learning to find the most predictive historical sample sizes for current market conditions.

Prev RTH FibsThis study captures the previous day’s Regular Trading Hours (RTH) range (default 09:30–16:00 America/New_York), then projects it onto the current session. It draws HIGH, LOW, and an optional 50% midpoint, plus a configurable set of inside fib-style percentages measured from the HIGH downward. Every level extends a short distance to the right of the current price and shows a clean numeric label (no box) on the right edge.

Key features

Prev-day RTH range tracked automatically; plotted each new session.

Inside levels (from HIGH ↓): 11%, 25%, 29.5%, 38.2%, 45%, 55%, 62% (OTE), 70.5%, 75%, 78.6%, 85% (toggle any on/off).

Clean right-side labels: numbers only, resizable (Tiny → Huge) with transparent background.

Line styling: HIGH/LOW and 50% are solid; inside levels can be Solid/Dashed/Dotted with independent color/width.

Smart right padding: lines/labels extend a few bars past the latest candle, so annotations stay beside price without violating TradingView’s “>500 bars in future” rule.

Works on any symbol/timeframe; RTH window and timezone are adjustable.

Inputs you control

Session: RTH session string and timezone.

Right-side padding (bars) and number size.

Visibility & style for HIGH, LOW, and 50%.

Which inside levels to show, plus their style/color/width.

Goldbach Time Indicator🔧 Key Fixes Applied:

1. Time Validation & Bounds Checking:

Hour/Minute Bounds: Ensures hours stay 0-23, minutes stay 0-59

Edge Case Handling: Prevents invalid time calculations from causing missing data

UTC Conversion Safety: Better handling of timezone edge cases

2. Enhanced Value Validation:

NA Checking: Validates all calculated values before using them

Goldbach Detection: Only flags valid, non-NA values as Goldbach hits

Plot Safety: Prevents plotting invalid or NA values that could cause gaps

3. Improved Plot Logic:

Core Level Colors: Blue for core levels (29,35,71,77), yellow/lime/orange for regular hits

Debug Mode Enhanced: Shows all calculations with gray dots when enabled

Better Filtering: Only plots positive, valid values for minus calculations

4. Background vs Dots Issue:

The large green/blue background you see suggests the indicator is detecting Goldbach times correctly, but the dots weren't plotting due to validation issues. This should now be fixed.

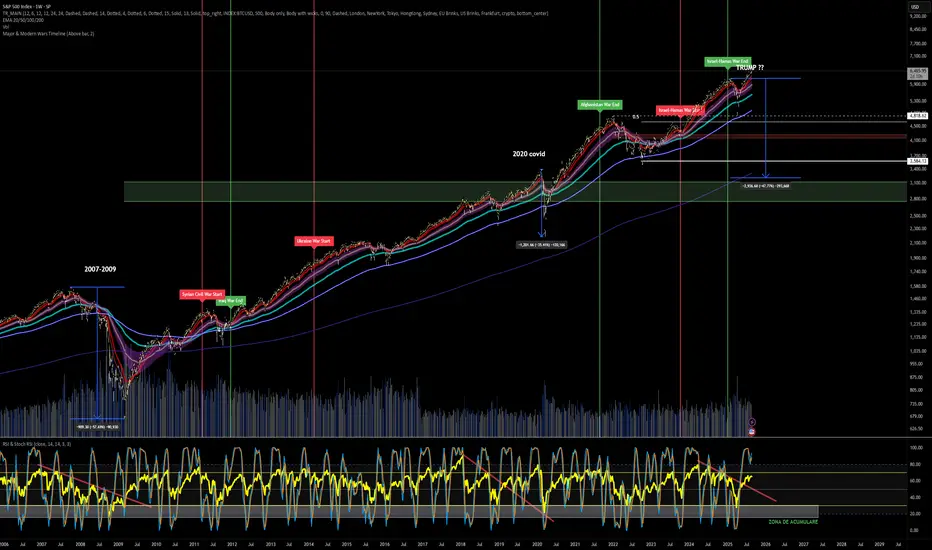

Major & Modern Wars TimelineDescription:

This indicator overlays vertical lines and labels on your chart to mark the start and end dates of major global wars and modern conflicts.

Features:

Displays start (red line + label) and end (green line + label) for each war.

Covers 20th century wars (World War I, World War II, Korean War, Vietnam War, Gulf War, Afghanistan, Iraq).

Includes modern conflicts: Syrian Civil War, Ukraine War, and Israel–Hamas War.

For ongoing conflicts, the end date is set to 2025 for timeline visualization.

Customizable: label position (above/below bar), line width.

Works on any chart timeframe, overlaying events on financial data.

Use case:

Useful for historical market analysis (e.g., gold, oil, S&P 500), helping traders and researchers see how wars and conflicts align with market movements.

Daily Start Vertical Lines (≤1H)This indicator automatically plots vertical lines at the start of each new trading day, based on the selected chart’s timezone. Unlike the default daily session boundaries (which often start at 17:00 New York time), this tool ensures that lines are drawn precisely at 00:00 midnight of the chart’s timezone.

🔹 Features:

Plots a vertical line at every new day start (midnight).

Fully time-zone aware → lines adjust automatically when you change the chart’s timezone.

Customizable line style, width, and color.

Option to limit plotting to specific timeframes (e.g., show only on ≤ 1H charts).

Lightweight & optimized (does not clutter higher-timeframe charts).

🔹 Use Cases:

Quickly identify daily boundaries for intraday analysis.

Helps scalpers and day traders align trades with new day opens.

Useful for strategies that depend on daily session resets.

This tool is especially helpful for traders who want clarity when working across different time zones.

Candle ShapeCandle Shape

This indicator visualizes rolling candles that aggregate price action over a chosen lookback period, allowing you to see how OHLC dynamics evolve in real time.

Instead of waiting for a higher timeframe (HTF) bar to close, you can track its development directly from a lower timeframe chart.

For example, view how a 1-hour candle is forming on a 1-minute chart — complete with rolling open, high, low, and close levels, as well as colored body and wick areas.

---

🔹 How it works

- Lookback Period (n) → sets the bucket size, defining how many bars are merged into a “meta-candle.”

- The script continuously updates the meta-open, meta-high, meta-low, and meta-close.

- Body and wick areas are filled with color , making bullish/bearish transitions easy to follow.

---

🔹 Use cases

- Monitor the intra-development of higher timeframe candles.

- Analyze rolling OHLC structures to understand how price dynamics shift across different aggregation windows.

- Explore unique perspectives for strategy confirmation, breakout anticipation, and market structure analysis.

---

✨ Candle Shape bridges the gap between timeframes and uncovers new layers of price interaction.

VWAP Price ChannelVWAP Price Channel cuts the crust off of a traditional price channel (Donchian Channel) by anchoring VWAPs at the highs and lows. By doing this, the flat levels, characteristic of traditional Donchian Channels, are no more!

Author's Note: This indicator is formed with no inherent use, and serves solely as a thought experiment.

> Concept

I would be hesitant to call this a "predictive" indicator, however the behavior of it would suggest it could be considered at least partially predictive

Essentially, the Anchored VWAPs creates something from otherwise nothing.

While the DC upper or lower values are staying flat, the VWAPs improvise based on price and volume to project a level that may be a better representation of where future highs or lows may settle.

Visually, this looks like we have cut off the corners of the Donchian Channel.

Note: Notice how we are calculating values before the corners are realized.

> Implementation

While this is only a concept indicator, The specific application I've gone with for this, is a sort of supertrend-ish display (A Trend Flipping Trailing Stop Loss).

The script uses basic logic to create a trend direction, and then displays the Anchored VWAPs as a form of trailing stop loss.

While "In Trend", the script fills in the area between the VWAP and Price in the direction of trend.

When new highs or lows are made while in trend, the opposite VWAP will start to generate at the new highs or lows. These happen on every new high or low, so they are not indicating the trend shift, but could be interpreted as breakout levels for the current trend direction in order for continuation.

Note: All values are drawn live, but when using higher timeframes, there is a natural calculation discrepancy when using live data vs. historical.

> Technicals

In this script, I'm simply detecting new highs or lows from the DC and using those as the anchor frequency on the built-in VWAP function.

So each time a new high or low is made based on DC, the VWAP function re-anchors to the high or low of the candle.

Past that, I have implemented some logic in order to account for a common occurrence I faced during development.

Frequently, the price would outpace the anchored VWAP, so we would end up with the VWAP being further from price than the actual DC upper or lower.

Due to this, what I have ended up with was a third value which, rather than switching between raw VWAP values and DC values, it adjusts the value based on the change in the VWAP value.

This can be simply thought of as a "Start + Change" type of setup.

By doing this, I can use the change values from the actual anchored VWAP, and under normal conditions, this will also be the true VWAP value.

However, situationally, I am able to update the start value which we're applying the VWAP change to.

In other words, when these situations happen, the VWAP change is added to the new (closer to price) DC value.

The specific trend logic being used is nothing fancy at all, we are simply checking if a new high or low is created and setting the trend in that direction.

This is in line with some traditional DC Strategies.

To those who made it here,

Just remember:

The chart may be ugly, but it's the fastest analysis of the data you can get.

Nicer displays often come at the hidden cost of latency.

You have to shoot your shot to make it.

Choose 2: Fast, Clean, Useful

Enjoy!

Market Cap Landscape 3DHello, traders and creators! 👋

Market Cap Landscape 3D. This project is more than just a typical technical analysis tool; it's an exploration into what's possible when code meets artistry on the financial charts. It's a demonstration of how we can transcend flat, two-dimensional lines and step into a vibrant, three-dimensional world of data.

This project continues a journey that began with a previous 3D experiment, the T-Virus Sentiment, which you can explore here:

The Market Cap Landscape 3D builds on that foundation, visualizing market data—particularly crypto market caps—as a dynamic 3D mountain range. The entire landscape is procedurally generated and rendered in real-time using the powerful drawing capabilities of polyline.new() and line.new() , pushed to their creative limits.

This work is intended as a guide and a design example for all developers, born from the spirit of learning and a deep love for understanding the Pine Script™ language.

---

🧐 Core Concept: How It Works

The indicator synthesizes multiple layers of information into a single, cohesive 3D scene:

The Surface: The mountain range itself is a procedurally generated 3D mesh. Its peaks and valleys create a rich, textured landscape that serves as the canvas for our data.

Crypto Data Integration: The core feature is its ability to fetch market cap data for a list of cryptocurrencies you provide. It then sorts them in descending order and strategically places them onto the 3D surface.

The Summit: The highest point on the mountain is reserved for the asset with the #1 market cap in your list, visually represented by a flag and a custom emblem.

The Mountain Labels: The other assets are distributed across the mountainside, with their rank determining their general elevation. This creates an intuitive visual hierarchy.

The Leaderboard Pole: For clarity, a dedicated pole in the back-right corner provides a clean, ranked list of the symbols and their market caps, ensuring the data is always easy to read.

---

🧐 Example of adjusting the view

To evoke the feeling of flying over mountains

To evoke the feeling of looking at a mountain peak on a low plain

🧐 Example of predefined colors

---

🚀 How to Use

Getting started with the Market Cap Landscape 3D:

Add to Chart: Apply the "Market Cap Landscape 3D" indicator to your active chart.

Open Settings: Double-click anywhere on the 3D landscape or click the "Settings" icon next to the indicator's name.

Customize Your Crypto List: The most important setting is in the Crypto Data tab. In the "Symbols" text area, enter a comma-separated list of the crypto tickers you want to visualize (e.g., BTC,ETH,SOL,XRP ). The indicator supports up to 40 unique symbols.

> Important Note: This indicator exclusively uses TradingView's `CRYPTOCAP` data source. To find valid symbols, use the main symbol search bar on your chart. Type `CRYPTOCAP:` (including the colon) and you will see a list of available options. For example, typing `CRYPTOCAP:BTC` will confirm that `BTC` is a valid ticker for the indicator's settings. Using symbols that do not exist in the `CRYPTOCAP` index will result in a script error. or, to display other symbols, simply type CRYPTOCAP: (including the colon) and you will see a list of available options.

Adjust Your View: Use the settings in the Camera & Projection tab to rotate ( Yaw ), tilt ( Pitch ), and scale the landscape until you find a view you love.

Explore & Customize: Play with the color palettes, flag design, and other settings to make the landscape truly your own!

---

⚙️ Settings & Customization

This indicator is highly customizable. Here’s a breakdown of what each setting does:

#### 🪙 Crypto Data

Symbols: Enter the crypto tickers you want to track, separated by commas. The script automatically handles duplicates and case-insensitivity.

Show Market Cap on Mountain: When checked, it displays the full market cap value next to the symbol on the mountain. When unchecked, it shows a cleaner look with just the symbol and a colored circle background.

#### 📷 Camera & Projection

Yaw (°): Rotates the camera view horizontally (side to side).

Pitch (°): Tilts the camera view vertically (up and down).

Scale X, Y, Z: Stretches or compresses the landscape in width, depth, and height, respectively. Fine-tune these to get the perfect perspective.

#### 🏞️ Grid / Surface

Grid X/Y resolution: Controls the detail level of the 3D mesh. Higher values create a smoother surface but may use more resources.

Fill surface strips: Toggles the beautiful color gradient on the surface.

Show wireframe lines: Toggles the visibility of the grid lines.

Show nodes (markers): Toggles the small dots at each grid intersection point.

#### 🏔️ Peaks / Mountains

Fill peaks volume: Draws vertical lines on high peaks, giving them a sense of volume.

Fill peaks surface: Draws a cross-hatch pattern on the surface of high peaks.

Peak height threshold: Defines the minimum height for a peak to receive the fill effect.

Peak fill color/density: Customizes the appearance of the fill lines.

#### 🚩 Flags (3D)

Show Flag on Summit: A master switch to show or hide the flag and emblem entirely.

Flag height, width, etc.: Provides full control over the dimensions and orientation of the flag on the highest peak.

#### 🎨 Color Palette

Base Gradient Palette: Choose from 13 stunning, pre-designed color themes for the landscape, from the classic SUNSET_WAVE to vibrant themes like NEON_DREAM and OCEANIC .

#### 🛡️ Emblem / Badge Controls

This section gives you granular control over every element of the custom emblem on the flag. Tweak rotation, offsets, and scale to design your unique logo.

---

👨💻 Developer's Corner: Modifying the Core Logic

If you're a developer and wish to customize the indicator's core data source, this section is for you. The script is designed to be modular, making it easy to change what data is being ranked and visualized.

The heart of the data retrieval and ranking logic is within the f_getSortedCryptoData() function. Here’s how you can modify it:

1. Changing the Data Source (from Market Cap to something else):

The current logic uses request.security("CRYPTOCAP:" + syms.get(i), ...) to fetch market capitalization data. To change this, you need to modify this line.

Example: Ranking by RSI (14) on the Daily timeframe.

First, you'll need a function to calculate RSI. Add this function to the script:

f_getRSI(symbol, timeframe, length) =>

request.security(symbol, timeframe, ta.rsi(close, length))

Then, inside f_getSortedCryptoData() , find the `for` loop that populates the `caps` array and replace the `request.security` call:

// OLD LINE:

// caps.set(i, request.security("CRYPTOCAP:" + syms.get(i), timeframe.period, close))

// NEW LINE for RSI:

// Note: You'll need to decide how to format the symbol name (e.g., "BINANCE:" + syms.get(i) + "USDT")

caps.set(i, f_getRSI("BINANCE:" + syms.get(i) + "USDT", "D", 14))

2. Changing the Data Formatting:

The ranking values are formatted for display using the f_fmtCap() function, which currently formats large numbers into "M" (millions), "B" (billions), etc.

If you change the data source to something like RSI, you'll want to change the formatting. You can modify f_fmtCap() or create a new formatting function.

Example: Formatting for RSI.

// Modify f_fmtCap or create f_fmtRSI

f_fmtRSI(float v) =>

str.tostring(v, "#.##") // Simply format to two decimal places

Remember to update the calls to this function in the main drawing loop where the labels are created (e.g., str.format("{0}: {1}", crypto.symbol, f_fmtCap(crypto.cap)) ).

By modifying these key functions ( f_getSortedCryptoData and f_fmtCap ), you can adapt the Market Cap Landscape 3D to visualize and rank almost any dataset you can imagine, from technical indicators to fundamental data.

---

We hope you enjoy using the Market Cap Landscape 3D as much as we enjoyed creating it. Happy charting! ✨

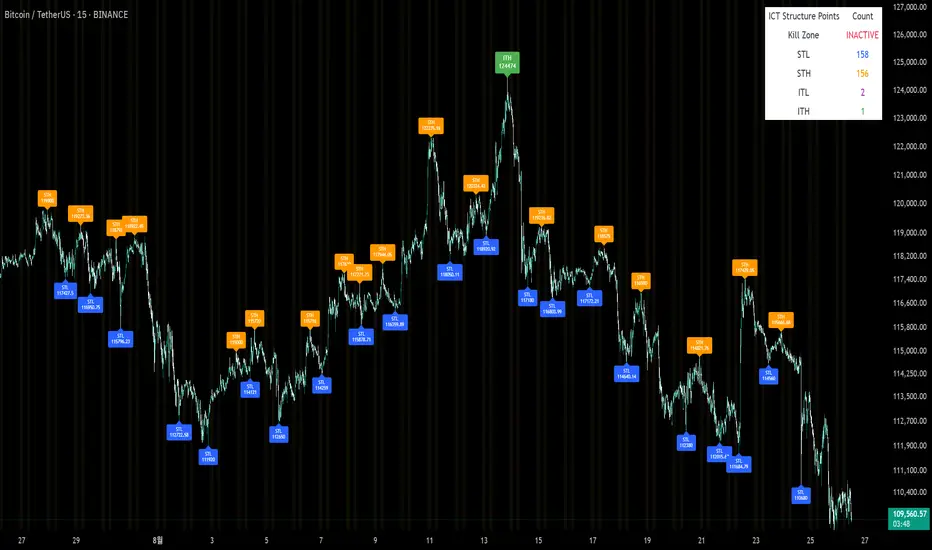

Sunmool's Silver Bullet Model FinderICT Silver Bullet Model Indicator - Complete Guide

📈 Overview

The ICT Silver Bullet Model indicator is a supplementary tool for utilizing ICT's (Inner Circle Trader) market structure analysis techniques. This indicator detects institutional liquidity hunting patterns and automatically identifies structural levels, helping traders analyze market structure more effectively.

🎯 Core Features

1. Structural Level Identification

STL (Short Term Low): Recent support levels formed in the short term

STH (Short Term High): Recent resistance levels formed in the short term

ITL (Intermediate Term Low): Stronger support levels with more significance

ITH (Intermediate Term High): Stronger resistance levels with more significance

2. Kill Zone Time Display

London Kill Zone: 02:00-05:00 (default)

New York Kill Zone: 08:30-11:00 (default)

These are the most active trading hours for institutional players where significant price movements occur

3. Smart Sweep Detection

Bear Sweep (🔻): Pattern where price sweeps below lows then recovers - Simply indicates sweep occurrence

Bull Sweep (🔺): Pattern where price sweeps above highs then declines - Simply indicates sweep occurrence

Important: Sweep labels only mark liquidity hunting locations, not directional bias.

🔧 Configuration Parameters

Basic Settings

Sweep Detection Lookback: Number of candles for sweep detection (default: 20)

Structure Point Lookback: Number of candles for structural point detection (default: 10)

Sweep Threshold: Percentage threshold for sweep validation (default: 0.1%)

Time Settings

London Kill Zone: Active hours for London session

New York Kill Zone: Active hours for New York session

Visualization Settings

Customizable colors for each level type

Enable/disable alert notifications

📊 How to Use

1. Chart Setup

Most effective on 1-minute to 1-hour timeframes

Recommended for major currency pairs (EUR/USD, GBP/USD, etc.)

Also applicable to cryptocurrencies and indices

2. Signal Interpretation

🔻 Bear Sweep / 🔺 Bull Sweep Labels

Simply indicate liquidity hunting occurrence points

Not directional bias indicators

Reference for understanding overall context on HTF

🟢 Silver Bullet Long (Huge Green Triangle)

After Bear Sweep occurrence

Within Kill Zone timeframe

Current price positioned above swept level

→ Actual BUY entry signal

🔴 Silver Bullet Short (Huge Red Triangle)

After Bull Sweep occurrence

Within Kill Zone timeframe

Current price positioned below swept level

→ Actual SELL entry signal

3. Risk Management

Use swept levels as stop-loss reference points

Approach signals outside Kill Zone hours with caution

Recommended to use alongside other technical analysis tools

💡 Trading Strategies

Silver Bullet Strategy

Preparation Phase: Monitor charts 30 minutes before Kill Zone

Sweep Observation: Identify liquidity hunting points with 🔻🔺 labels (reference only)

Entry: Enter ONLY when huge triangle Silver Bullet signal appears within Kill Zone

Take Profit: Target opposite structural level or 1:2 reward ratio

Stop Loss: Beyond the swept level

Important: Small sweep labels are NOT trading signals!

Multi-Timeframe Approach

Step 1: HTF (Higher Time Frame) Sweep Reference

Observe 🔻🔺 sweep labels on 4-hour and daily charts

Reference only sweeps occurring at major structural levels

HTF sweeps are used to identify liquidity hunting points

Reference only, not for directional bias

Step 2: Transition to LTF (Lower Time Frame)

Move to 15-minute, 5-minute, and 1-minute charts

Analyze LTF with reference to HTF sweep information

Use STL, STH, ITL, ITH for precise entry point identification

Structural levels on LTF are the core of actual trading decisions

Only huge triangle (Silver Bullet) signals are actual entry signals

Recommended Usage

Identify overall sweep occurrence points on HTF (🔻🔺 labels)

Use this indicator on LTF to identify structural levels

Reference only huge triangle signals for actual trading during Kill Zone

Small sweep labels (🔻🔺) are for reference only, not entry signals

📋 Information Table Interpretation

Real-time information in the top-right table:

Kill Zone Status: Current active session status

Level Counts: Number of each structural level type

⚠️ Important Disclaimers

Backtesting results do not guarantee future performance

Exercise caution during high market volatility periods

Always apply proper risk management

Recommend comprehensive analysis with other analytical tools

🎓 Learning Resources

Study original ICT concepts through free YouTube educational content

Research Market Structure analysis techniques

Optimize through backtesting for personal use

🔬 Technical Implementation

Algorithm Logic

Pivot Point Detection: Uses TradingView's built-in pivot functions to identify swing highs and lows

Classification System: Automatically categorizes levels based on recent price action frequency

Sweep Validation: Confirms legitimate sweeps through price action analysis

Time-Based Filtering: Prioritizes signals during institutional active hours

Performance Optimization

Efficient array management prevents memory overflow

Dynamic level cleanup maintains chart clarity

Real-time calculation ensures minimal lag

🛠️ Customization Tips

Adjust lookback periods based on market volatility

Modify kill zone times for different market sessions

Experiment with sweep threshold for different instruments

Color-code levels according to personal preference

📈 Expected Outcomes

When properly implemented, this indicator can help traders:

Identify high-probability reversal points

Time entries with institutional flow

Reduce false signals through kill zone filtering

Improve risk-to-reward ratios

This indicator automates ICT's concepts into a user-friendly tool that can be enhanced through continuous learning and practical application. Success depends on understanding the underlying market structure principles and combining them with proper risk management techniques.

Weekly pecentage tracker by PRIVATE

Settings Picture below this link: 👇

i.ibb.co

What it is

A lightweight “Weekly % Tracker” overlay that lets you manually enter weekly performance (in percent) for XAUUSD + up to 10 FX pairs, then shows:

a small table panel with each enabled symbol and its % result

one TOTAL row (Sum / Average / Compounded across all enabled symbols)

an optional mini badge showing the % for a single selected symbol

Nothing is auto-calculated from price—you type the % yourself.

Key settings

Panel: show/hide, position, number of decimals, colors (background, text, green/red).

Total mode:

Sum – adds percentages

Average – mean of enabled rows

Compounded –

(

∏

(

1

+

𝑝

/

100

)

−

1

)

×

100

(∏(1+p/100)−1)×100

Symbols:

XAUUSD (toggle + label + % input)

10 FX pairs (each has On/Off, label text, % input). You can rename labels to any symbol text you want.

Mini badge: show/hide, position, and symbol to display.

How it works

Overlay indicator: overlay=true; just draws UI on the chart (no plots).

Arrays (syms, vals, ons) collect the row data in order: XAU first, then FX1…FX10.

Helpers:

posFrom() converts a position string (e.g., “Top Right”) into a position.* constant.

wp_col() picks green/red/neutral based on the sign of the %.

wp_round() rounds values to the selected decimals.

calc_total() computes the TOTAL with the chosen mode over enabled rows only.

Table creation logic:

Counts how many rows are enabled.

If none enabled or panel is off: the panel table is deleted, so no box/background is visible.

If enabled and on: the panel is (re)created at the chosen position.

On each last bar (barstate.islast), it clears the table to transparent (bgcolor=na) and then fills one row per enabled symbol, followed by a single TOTAL row.

Mini badge:

Always (re)created on position change.

Shows selected symbol’s % (or “-” if that symbol isn’t enabled or has no value).

Colors text green/red by sign.

Notes & limits

It’s manual input—the script doesn’t read trades or P/L from price.

You can rename each row’s label to match any symbol name you want.

When no rows are enabled, the panel disappears entirely (no empty background).

Designed to be light: only draws tables; no heavy plotting.

If you want the TOTAL row to be optional, or different color thresholds, or CSV-style export/import of the values, say the word and I’ll add it.

Floating Dashboard + KDE (v6)Simple indicator that displays ADX, RSI, MACD, ATR, Average Volume and KDE with dynamic Table and Label.

Prev 1 & 2 Day Close (Intraday)it give 1 day ago close and give good sentimate that if breaks level then big fal in intraday

Previous Closes (1 & 2 Days Ago)it give closing price of last 2 days, generally of 2 days close broken then you get good move for intraday

MATEOANUBISANTIDear traders, investors, and market enthusiasts,

We are excited to share our High-Low Indicator Range for on . This report aims to provide a clear and precise overview of the highest and lowest values recorded by during this specific hour, equipping our community with a valuable tool for making informed and strategic market decisions.

Mikula's Master 360° Square of 12Mikula’s Master 360° Square of 12

An educational W. D. Gann study indicator for price and time. Anchor a compact Square of 12 table to a start point you choose. Begin from a bar’s High or Low (or set a manual start price). From that anchor you can progress or regress the table to study how price steps through cycles in either direction.

What you’re looking at :

Zodiac rail (far left): the twelve signs.

Degree rail: 24 rows in 15° steps from 15° up to 360°/0°.

Transit rail and Natal rail: track one planet per rail. Each planet is placed at its current row (℞ shown when retrograde). As longitude advances, the planet climbs bottom → top, then wraps to the bottom at the next sign; during retrograde it steps downward.

Hover a planet’s cell to see a tooltip with its exact longitude and sign (e.g., 152.4° ♌︎). The linked price cell in the grid moves with the planet’s row so you can follow a planet’s path through the zodiac as a path through price.

Price grid (right): the 12×24 Square of 12. Each column is a cycle; cells are stepped price levels from your start price using your increment.

Bottom rail: shows the current square number and labels the twelve columns in that square.

How the square is read

The square always begins at the bottom left. Read each column bottom → top. At the top, return to the bottom of the next column and read up again. One square contains twelve cycles. Because the anchor can be a High or a Low, you can progress the table upward from the anchor or regress it downward while keeping the same bottom-to-top reading order.

Iterate Square (shifting)

Iterate Square shifts the entire 12×24 grid to the next set of twelve cycles.

Square 1 shows cycles 1–12; Square 2 shows 13–24; Square 3 shows 25–36, etc.

Visibility rules

Pivot cells are table-bound. If you shift the square beyond those prices, their highlights won’t appear in the table.

A/B levels and Transit/Natal planetary lines are chart overlays and can remain visible on the table as you shift the square.

Quick use

Choose an anchor (date/time + High/Low) or enable a manual start price .

Set the increment. If you anchored with a Low and want the table to step downward from there, use a negative value.

Optional: pick Transit and Natal planets (one per rail), toggle their plots, and hover their cells for longitude/sign.

Optional: turn on A/B levels to display repeating bands from the start price.

Optional: enable swing pivots to tint matching cells after the anchor.

Use Iterate Square to shift to later squares of twelve cycles.

Examples

These are exploratory examples to spark ideas:

Overview layout (zodiac & degree rails, Transit/Natal rails, price grid)

A-levels plotted, pivots tinted on the table, real-time price highlighted

Drawing angles from the anchor using price & time read from the table

Using a TradingView Gann box along the A-levels to study reactions

Attribution & originality

This script is an original implementation (no external code copied). Conceptual credit to Patrick Mikula, whose discussion of the Master 360° Square of 12 inspired this study’s presentation.

Further reading (neutral pointers)

Patrick Mikula, Gann’s Scientific Methods Unveiled, Vol. 2, “W. D. Gann’s Use of the Circle Chart.”

W. D. Gann’s Original Commodity Course (as provided by WDGAN.com).

No affiliation implied.

License CC BY-NC-SA 4.0 (non-commercial; please attribute @Javonnii and link the original).

Dependency AstroLib by @BarefootJoey

Disclaimer Educational use only; not financial advice.

Reversal Triggers + 200 EMA + Prior D1 + Bias TableKeep it simple stupid.

D1 bias

H1 bias

H1 ORB (momentum)