Chande Volatility-Based Trailing Stops This indicator is developed from a description outlined in the Chande - Kroll book, "The New Technical Trader". It is designed to help control risk by plotting two lines that function as long and short trailing stops.

How does it work?

"These stops are derived from recent highest high or lowest low. They adjust based on volatility. However, to avoid giving up a sizable chunk of profit before the stop is hit, it is modified in such a way that the stop can only advance with price, not retreat. This will lock in a greater portion of potential profits..."

Settings:

The default settings are those described in the book. They are described as being best for intermediate term trades. Use the multiplier to tighten or loosen the stop. A smaller multiplier will result in tighter stops. It is recommended to adjust this value for your preferred timeframe. You can toggle the trailing stop lines on or off as well as cross over marker.

Chande

Chande Kroll Trend Strategy (SPX, 1H) | PINEINDICATORSThe "Chande Kroll Stop Strategy" is designed to optimize trading on the SPX using a 1-hour timeframe. This strategy effectively combines the Chande Kroll Stop indicator with a Simple Moving Average (SMA) to create a robust method for identifying long entry and exit points. This detailed description will explain the components, rationale, and usage to ensure compliance with TradingView's guidelines and help traders understand the strategy's utility and application.

Objective

The primary goal of this strategy is to identify potential long trading opportunities in the SPX by leveraging volatility-adjusted stop levels and trend-following principles. It aims to capture upward price movements while managing risk through dynamically calculated stops.

Chande Kroll Stop Parameters:

Calculation Mode: Offers "Linear" and "Exponential" options for position size calculation. The default mode is "Exponential."

Risk Multiplier: An adjustable multiplier for risk management and position sizing, defaulting to 5.

ATR Period: Defines the period for calculating the Average True Range (ATR), with a default of 10.

ATR Multiplier: A multiplier applied to the ATR to set stop levels, defaulting to 3.

Stop Length: Period used to determine the highest high and lowest low for stop calculation, defaulting to 21.

SMA Length: Period for the Simple Moving Average, defaulting to 21.

Calculation Details:

ATR Calculation: ATR is calculated over the specified period to measure market volatility.

Chande Kroll Stop Calculation:

High Stop: The highest high over the stop length minus the ATR multiplied by the ATR multiplier.

Low Stop: The lowest low over the stop length plus the ATR multiplied by the ATR multiplier.

SMA Calculation: The 21-period SMA of the closing price is used as a trend filter.

Entry and Exit Conditions:

Long Entry: A long position is initiated when the closing price crosses over the low stop and is above the 21-period SMA. This condition ensures that the market is trending upward and that the entry is made in the direction of the prevailing trend.

Exit Long: The long position is exited when the closing price falls below the high stop, indicating potential downward movement and protecting against significant drawdowns.

Position Sizing:

The quantity of shares to trade is calculated based on the selected calculation mode (linear or exponential) and the risk multiplier. This ensures position size is adjusted dynamically based on current market conditions and user-defined risk tolerance.

Exponential Mode: Quantity is calculated using the formula: riskMultiplier / lowestClose * 1000 * strategy.equity / strategy.initial_capital.

Linear Mode: Quantity is calculated using the formula: riskMultiplier / lowestClose * 1000.

Execution:

When the long entry condition is met, the strategy triggers a buy signal, and a long position is entered with the calculated quantity. An alert is generated to notify the trader.

When the exit condition is met, the strategy closes the position and triggers a sell signal, accompanied by an alert.

Plotting:

Buy Signals: Indicated with an upward triangle below the bar.

Sell Signals: Indicated with a downward triangle above the bar.

Application

This strategy is particularly effective for trading the SPX on a 1-hour timeframe, capitalizing on price movements by adjusting stop levels dynamically based on market volatility and trend direction.

Default Setup

Initial Capital: $1,000

Risk Multiplier: 5

ATR Period: 10

ATR Multiplier: 3

Stop Length: 21

SMA Length: 21

Commission: 0.01

Slippage: 3 Ticks

Backtesting Results

Backtesting indicates that the "Chande Kroll Stop Strategy" performs optimally on the SPX when applied to the 1-hour timeframe. The strategy's dynamic adjustment of stop levels helps manage risk effectively while capturing significant upward price movements. Backtesting was conducted with a realistic initial capital of $1,000, and commissions and slippage were included to ensure the results are not misleading.

Risk Management

The strategy incorporates risk management through dynamically calculated stop levels based on the ATR and a user-defined risk multiplier. This approach ensures that position sizes are adjusted according to market volatility, helping to mitigate potential losses. Trades are sized to risk a sustainable amount of equity, adhering to the guideline of risking no more than 5-10% per trade.

Usage Notes

Customization: Users can adjust the ATR period, ATR multiplier, stop length, and SMA length to better suit their trading style and risk tolerance.

Alerts: The strategy includes alerts for buy and sell signals to keep traders informed of potential entry and exit points.

Pyramiding: Although possible, the strategy yields the best results without pyramiding.

Justification of Components

The Chande Kroll Stop indicator and the 21-period SMA are combined to provide a robust framework for identifying long trading opportunities in trending markets. Here is why they work well together:

Chande Kroll Stop Indicator: This indicator provides dynamic stop levels that adapt to market volatility, allowing traders to set logical stop-loss levels that account for current price movements. It is particularly useful in volatile markets where fixed stops can be easily hit by random price fluctuations. By using the ATR, the stop levels adjust based on recent market activity, ensuring they remain relevant in varying market conditions.

21-Period SMA: The 21-period SMA acts as a trend filter to ensure trades are taken in the direction of the prevailing market trend. By requiring the closing price to be above the SMA for long entries, the strategy aligns itself with the broader market trend, reducing the risk of entering trades against the overall market direction. This helps to avoid false signals and ensures that the trades are in line with the dominant market movement.

Combining these two components creates a balanced approach that captures trending price movements while protecting against significant drawdowns through adaptive stop levels. The Chande Kroll Stop ensures that the stops are placed at levels that reflect current volatility, while the SMA filter ensures that trades are only taken when the market is trending in the desired direction.

Concepts Underlying Calculations

ATR (Average True Range): Used to measure market volatility, which informs the stop levels.

SMA (Simple Moving Average): Used to filter trades, ensuring positions are taken in the direction of the trend.

Chande Kroll Stop: Combines high and low price levels with ATR to create dynamic stop levels that adapt to market conditions.

Risk Disclaimer

Trading involves substantial risk, and most day traders incur losses. The "Chande Kroll Stop Strategy" is provided for informational and educational purposes only. Past performance is not indicative of future results. Users are advised to adjust and personalize this trading strategy to better match their individual trading preferences and risk tolerance.

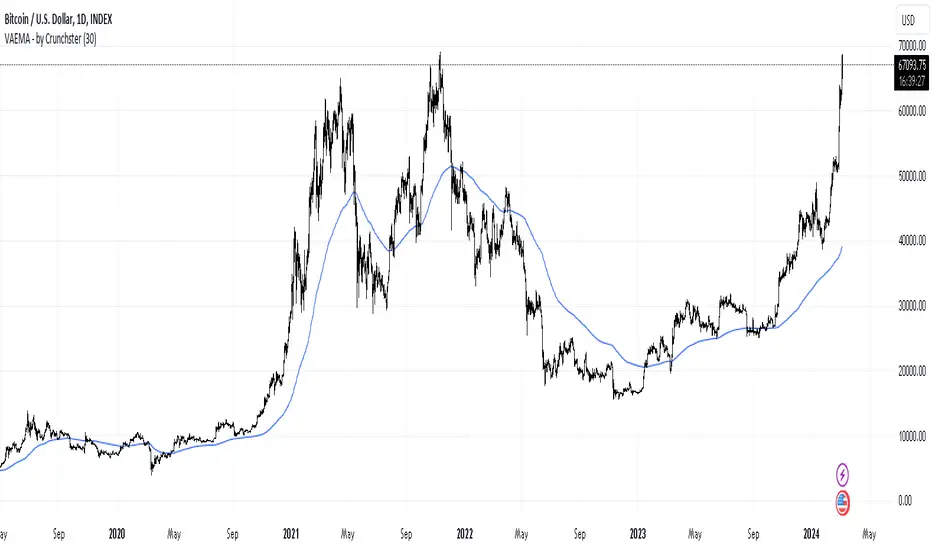

Volatility Adjusted EMA - by CrunchsterApplies recent volatility adjustment to the exponential moving average, where the smoothing factor is 2/(N + 1) - N being the lookback period or span

Volatility of recent 30 days returns is calculated using standard deviation with a thirty day lookback.

Increased smoothing compared to a standard EMA, which also adjusts to market conditions, as first described by Chande in 1991.

Activity & Chop ScoreRelease Notes:

The Activity and Chop Score was designed to help traders quickly determine if a market is active and/or choppy (not moving with any urgency). Slow and chopping markets should be approached with caution or avoided.

How does it work? The Activity Score incorporates momentum and the linear regression. Momentum (change in price over time) is compared over a long and short time period. Active markets are when those are moving together. This is combined with a linear regression of the price to determine the Correlation Coefficient (r^2) to measure of trend strength. The score is a is the average of the two momentum values, normalized by the standard deviation, and scaled by the trend (r^2 value). Chop is defined as divergence between long and short momentum periods. The divergences (chop) are quantified with a Jaccard Similarity Score, normalized by the standard deviation, and averaged to create a score.

How can you use it? This indicator is best used on lower timeframes. Activity Scores Values below 1 are considered low and values over 2 are high. Avoid markets where the Activity Score is below 1. There is an alert threshold in the options. Pivots are worth paying attention too as well as they indicate the start and stop of a recent move. You can compare markets or assets with the Chop Score. You make chose to avoid those with higher Chop Score. The position of the two lines relative to each other are useful. Ideally, the Activity Score is higher than the Chop Score. As with any indicators, it should be used in combination with others that best suits your trading style.

Weekday Change & Volume Average TableHaving a reference point for comparing with current data has always been an important task in market analysis. This script tried to give a better understanding based on weekdays.

This script shows that in the current ticker, what is the average movement of the price (High-Low) and volume for each weekday. Depending on the market and the exchange it should be different.

The Interesting point is that, for example in BINANCE:BTCUSDT , on Saturday and Sunday, volume is about 30% less and the price movement is about 20% less.

The script can be used on any timeframe and any symbol, just remember that the data shown is based on the candles on the chart, so it is different also based on your tradingview's account since Historical bars available for Basic is 5K, Pro & Pro+ is 10K and Premium is 20K; And in lower timeframes it is calculating more recent data.

Adaptive Fisherized CMOIntroduction

Heyo, here is another no-repaint adaptive fisherized indicator.

I added Inverse Fisher Transform, Ehlers dominant cycle analysis and smoothing to the Chande Momentum Oscillator (CMO).

Usage

The CMO is a momentum oscillator which shows the usual movement of an asset.

I recommend to use it from a lower timeframe with a higher timeframe set.

Signals

(Signal mode will come soon.)

Zero Line

CMO crosses above zero line => enter long

CMO cross below zero line => ente short

Overbought/Oversold

CMO crosses above bottom band => enter long

CMO crosses under top band => enter short

MA (Maybe this signals will vary. Then, check update notes.)

CMO crosses above MA => enter long

CMO crosses below MA => enter short

Enjoy and share your experience with it!

More to read: CMO Explanationsp

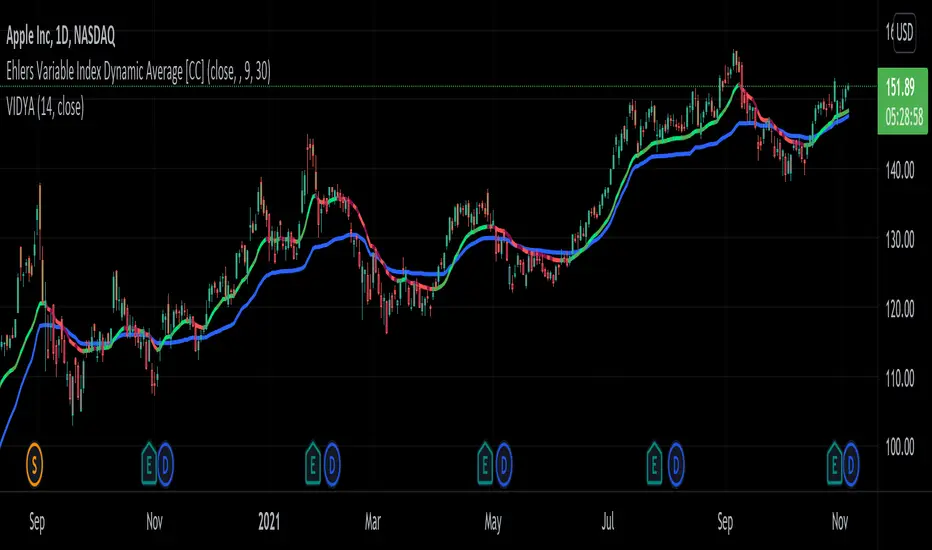

STD-Stepped VIDYA w/ Quantile Bands [Loxx]STD-Stepped VIDYA w/ Quantile Bands is a VIDYA moving average with Standard Deviation step filtering on either/neither/both price and VIDYA. Also included are quantile bands to identify breakouts/breakdowns/reversals.

What is VIDYA?

Variable Index Dynamic Average Technical Indicator ( VIDYA ) was developed by Tushar Chande. It is an original method of calculating the Exponential Moving Average ( EMA ) with the dynamically changing period of averaging.

What is Quantile Bands?

In statistics and the theory of probability, quantiles are cutpoints dividing the range of a probability distribution into contiguous intervals with equal probabilities, or dividing the observations in a sample in the same way. There is one less quantile than the number of groups created. Thus quartiles are the three cut points that will divide a dataset into four equal-size groups ( cf . depicted example). Common quantiles have special names: for instance quartile, decile (creating 10 groups: see below for more). The groups created are termed halves, thirds, quarters, etc., though sometimes the terms for the quantile are used for the groups created, rather than for the cut points.

q-Quantiles are values that partition a finite set of values into q subsets of (nearly) equal sizes. There are q − 1 of the q-quantiles, one for each integer k satisfying 0 < k < q. In some cases the value of a quantile may not be uniquely determined, as can be the case for the median (2-quantile) of a uniform probability distribution on a set of even size. Quantiles can also be applied to continuous distributions, providing a way to generalize rank statistics to continuous variables. When the cumulative distribution function of a random variable is known, the q-quantiles are the application of the quantile function (the inverse function of the cumulative distribution function) to the values {1/q, 2/q, …, (q − 1)/q}.

Included:

3 types of signal options

Alerts

Bar coloring

Loxx's Expanded Source Types

STD Aadaptive, floating RSX Dynamic Momentum Index [Loxx]STD Aadaptive, floating RSX Dynamic Momentum Index is an attempt to improve Chande's original work on Dynamic Momentum Index. The full name of this indicator is "Standard-Deviation-Adaptive, floating-level, Dynamic Momentum Index on Jurik's RSX".

What Is Dynamic Momentum Index?

The dynamic momentum index is used in technical analysis to determine if a security is overbought or oversold. This indicator, developed by Tushar Chande and Stanley Kroll, is very similar to the relative strength index (RSI). The main difference between the two is that the RSI uses a fixed number of time periods (usually 14), while the dynamic momentum index uses different time periods as volatility changes, typically between five and 30.

What is RSX?

RSI is a very popular technical indicator, because it takes into consideration market speed, direction and trend uniformity. However, the its widely criticized drawback is its noisy (jittery) appearance. The Jurk RSX retains all the useful features of RSI, but with one important exception: the noise is gone with no added lag.

Differences

RSX is used instead of RSI for the calculation, producing a much smoother result

Standard deviation is used to adapt the RSX calculation

Floating levels are used instead of fixed levels for OB/OS

Included

-Change bar colors

Adaptive, Relative Strength EMA (RSEMA) [Loxx]TASC's May 2022 edition Traders' Tipsl includes the "Relative Strength Moving Averages" article authored by Vitali Apirine. This is the code implementing the Relative Strength Exponential Moving Average (RS EMA) indicator introduced in this publication.

This indicator adds onto Vitali Apirine's work by including three different types of momentum used to calculate RSEMA as well as fixed and adaptive cycle calculations to be used as dynamic inputs to calculate momentum. The purpose of these additional calculation methods is to attempt to filter out noice and track trends by using different methods and inputs to calculation momentum.

Momentum methods

-Wilder relative strength

-Chande momentum

-Momentum component of Jurik's RSX RSI

Cycle calculation methods

-Fixed

-Vertical horizontal filter

-Ehlers' Autocorrelation Dominant Cycle

What is Wilder relative strength?

The Relative Strength Index (RSI), developed by J. Welles Wilder, is a momentum oscillator that measures the speed and change of price movements. The RSI oscillates between zero and 100. Traditionally the RSI is considered overbought when above 70 and oversold when below 30.

What is Chande momentum?

Chande Momentum was designed specifically to track the movement and momentum of a security. It calculates the difference between the sum of both recent gains and recent losses, then dividing the result by the sum of all price movement over the same period.

What is the momentum component of Jurik's RSX RSI?

RSI is a very popular technical indicator, because it takes into consideration market speed, direction and trend uniformity. However, the its widely criticized drawback is its noisy (jittery) appearance. The Jurk RSX retains all the useful features of RSI , but with one important exception: the noise is gone with no added lag. For our purposes here, we derive momentum minus the lag.

Vertical horizontal filter?

Vertical Horizontal Filter (VHF) was created by Adam White to identify trending and ranging markets. VHF measures the level of trend activity, similar to ADX in the Directional Movement System. Trend indicators can then be employed in trending markets and momentum indicators in ranging markets.

What is autocorrelation?

Ehlers Autocorrelation is used in the calculation of dominant cycle length to be injected into standard technical analysis tools to improve TA accuracy. Its main purpose is to eliminate noise from the price data, reduce effects of the “spectral dilation” phenomenon, and reveal dominant cycle periods.

As the first step, Autocorrelation uses Mr. Ehlers’s previous installment, Ehlers Roofing Filter, in order to enhance the signal-to-noise ratio and neutralize the spectral dilation. This filter is based on aerospace analog filters and when applied to market data, it attempts to only pass spectral components whose periods are between 10 and 48 bars.

Autocorrelation is then applied to the filtered data: as its name implies, this function correlates the data with itself a certain period back. As with other correlation techniques, the value of +1 would signify the perfect correlation and -1, the perfect anti-correlation.

Happy trading!

Aroon Oscillator of Adaptive RSI [Loxx]Aroon Oscillator of Adaptive RSI uses RSI to calculate AROON in attempt to capture more trend and momentum quicker than Aroon or RSI alone. Aroon Oscillator of Adaptive RSI has three different types of RSI calculations and the choice of either fixed, VHF Adaptive, or Band-pass Adaptive cycle measures to calculate RSI.

Arron Oscillator:

The Aroon Oscillator was developed by Tushar Chande in 1995 as part of the Aroon Indicator system. Chande’s intention for the system was to highlight short-term trend changes. The name Aroon is derived from the Sanskrit language and roughly translates to “dawn’s early light.”

The Aroon Oscillator is a trend-following indicator that uses aspects of the Aroon Indicator (Aroon Up and Aroon Down) to gauge the strength of a current trend and the likelihood that it will continue.

Aroon oscillator readings above zero indicate that an uptrend is present, while readings below zero indicate that a downtrend is present. Traders watch for zero line crossovers to signal potential trend changes. They also watch for big moves, above 50 or below -50 to signal strong price moves.

Wilders' RSI:

The Relative Strength Index (RSI) is a well versed momentum based oscillator which is used to measure the speed (velocity) as well as the change (magnitude) of directional price movements. Essentially RSI, when graphed, provides a visual mean to monitor both the current, as well as historical, strength and weakness of a particular market. The strength or weakness is based on closing prices over the duration of a specified trading period creating a reliable metric of price and momentum changes. Given the popularity of cash settled instruments (stock indexes) and leveraged financial products (the entire field of derivatives); RSI has proven to be a viable indicator of price movements.

RSX RSI:

RSI is a very popular technical indicator, because it takes into consideration market speed, direction and trend uniformity. However, the its widely criticized drawback is its noisy (jittery) appearance. The Jurk RSX retains all the useful features of RSI, but with one important exception: the noise is gone with no added lag.

Rapid RSI:

Rapid RSI Indicator, from Ian Copsey's article in the October 2006 issue of Stocks & Commodities magazine.

RapidRSI resembles Wilder's RSI, but uses a SMA instead of a WilderMA for internal smoothing of price change accumulators.

VHF Adaptive Cycle:

Vertical Horizontal Filter (VHF) was created by Adam White to identify trending and ranging markets. VHF measures the level of trend activity, similar to ADX DI. Vertical Horizontal Filter does not, itself, generate trading signals, but determines whether signals are taken from trend or momentum indicators. Using this trend information, one is then able to derive an average cycle length.

Band-pass Adaptive Cycle

Even the most casual chart reader will be able to spot times when the market is cycling and other times when longer-term trends are in play. Cycling markets are ideal for swing trading however attempting to “trade the swing” in a trending market can be a recipe for disaster. Similarly, applying trend trading techniques during a cycling market can equally wreak havoc in your account. Cycle or trend modes can readily be identified in hindsight. But it would be useful to have an objective scientific approach to guide you as to the current market mode.

There are a number of tools already available to differentiate between cycle and trend modes. For example, measuring the trend slope over the cycle period to the amplitude of the cyclic swing is one possibility.

We begin by thinking of cycle mode in terms of frequency or its inverse, periodicity. Since the markets are fractal ; daily, weekly, and intraday charts are pretty much indistinguishable when time scales are removed. Thus it is useful to think of the cycle period in terms of its bar count. For example, a 20 bar cycle using daily data corresponds to a cycle period of approximately one month.

When viewed as a waveform, slow-varying price trends constitute the waveform's low frequency components and day-to-day fluctuations (noise) constitute the high frequency components. The objective in cycle mode is to filter out the unwanted components--both low frequency trends and the high frequency noise--and retain only the range of frequencies over the desired swing period. A filter for doing this is called a bandpass filter and the range of frequencies passed is the filter's bandwidth.

Included:

-Toggle on/off bar coloring

-Customize RSI signal using fixed, VHF Adaptive, and Band-pass Adaptive calculations

-Choose from three different RSI types

Happy trading!

Chande Kroll Stop + ADX filter strategyDear TV''ers,

Hereby a script where i created a simple strategy using the underappreciated chande kroll stop indicator. Short signal is when the close crosses under the orange line and a long signal is generated upon a crossover of a close candle of the blue line.

Additionally you have the option to filter using ADX the minimize getting rekt in a choppy market.

good luck trading!

Ehlers Variable Index Dynamic Average [CC]The Variable Index Dynamic Average was created by Tushar Chande and this is a variation of that original formula created by John Ehlers. As you can see I have included the default Vidya from a script by @everget and as you can see the Ehlers version is able to follow the price much closer. I have included strong buy and sell signals in addition to normal ones and so darker colors are strong signals and lighter colors are normal ones. Buy when the line turns green and sell when it turns red.

Let me know if there are any other scripts you would like to see me publish!

CT Reverse Chande Momentum OscillatorIntroducing the Caretakers Reverse Chande Momentum Oscillator.

The Chande momentum oscillator is a technical momentum indicator which calculates the difference between the sum of recent gains and the sum of recent losses and then divides the result by the sum of all price movement over the same period.

It is used to gauge “pure momentum”.

It bears similarities to other momentum indicators such as the Stochastic, Rate of Change and the Relative Strength Index, but other unique features render it a handy tool in the traders handset.

The CMO was developed by Tushar Chande.

The author introduced the indicator in his 1994 book “The New Technical Trader “.

The CMO has a normal range of values between +100 and -100.

I have reverse engineered the CMO formula to derive a dual purpose function.

The function can calculate the chart price at which the CMO will reach a particular CMO scale value.

The function can also calculate the chart price at which the CMO will equal its previous value.

I have employed this function here to give the price level where the CMO will equal :

Upper alert level ( default 50 )

Zero-Line

Lower alert level ( default -50 )

Previous CMO value

These crossover levels are displayed via an optional infobox with choice of user selected info.

The advantage of knowing the exact prices that this will happen should give the user an additional edge and precision in risk management.

Traditionally traders and analysts will consider:

Positives values above 50 indicate an “overbought” condition

Negative values below -50 indicate an “oversold” condition

Common traditional ways to derive signals from the CMO :

When the CMO crosses above the zeroline, a buy signal is generated.

When the CMO crosses below the zeroline, a sell signal is generated.

When the SMI crosses below -50 and then moves back above it, a buy signal is generated.

When the SMI crosses above +50 and then moves back below it, a sell signal is generated.

Traditionally, traders also look for divergences between the CMO and price action.

Chande Momentum oscillating in a narrower band around the zero line, with no penetration of the Overbought and Oversold levels indicates a ranging market.

This should not be confused with Chande Momentum oscillating between either the Overbought and the zero line, or the Oversold level and the zero line, which indicates a strong up, or down-trend.

It is traditionally considered that the strongest trend signals are from failed swing patterns.

It measures momentum on both up and down days and does not smooth results, triggering more frequent oversold and overbought penetrations.

The CMO is often used to determine overall market trendiness in conjunction with the SMI where the SMI is used to determine the direction of the trend, and also with volume indicators to show if the momentum carries significant selling or buying pressure.

Volatility Index of Range Verification█ OVERVIEW

This is a volatility indicator created by extending concepts from Tushar Chande's Range Action Verification Index (RAVI).

█ CONCEPTS

This indicator constructs range of the RAVI indicator. It uses this range to build a histogram that represents how fast the range is changing, or a measure of volatility. A line is then constructed, either from a moving average or standard deviation depending on the settings that can serve as an action trigger.

█ INPUTS

• Fast MA Period: the period of the quickest moving average that is used to build the RAVI indicator line

• Slow MA Period: the period of the slowest moving average that is used to build the RAVI indicator line

• MA Type: the type of moving average to use, either Simple or Exponential

• Price Source: the type of price source to use; close, high, low, hlc3, etc.

• Lookback Period: how far back to construct the minimum and maximum of the range

• Standard Range: the standard range of the indicator. a smaller range will exaggerate differences in the columns, and vice-versa

• Volatility Period: the period used for the trigger line moving average

• Std. Deviation Mode?: Whether the trigger line will plot using a moving average or a multiple of Standard Deviation.

• Deviation Multiplier: How many deviations to use if the trigger line is in Std. Deviation Mode

Indicator: Weight Of Middle [xQT5]This is my original indicator that was inspired by "Mayer Multiple" and "Chande Forecast Oscillator" (CFO).

I decided to search truth of trend power with SMA and LinReg and found it in a somewhere of the middle. Also, I added a limit area, where you need to keep a more attention, because it can show a potential reversal.

You can change parametrs with a your own look.

One more signal for indicator:

- If "WOM" is above "1" - it's a bullish direction;

- If "WOM" is below "1" - it's a bearish direction.

Enjoy it!

Mass Thrust OscillatorThis is a custom indicator that turns my Mass Thrust Indicator into an oscillator which is loosely based on Tushar S. Chande's Market Thrust Oscillator (Stocks & Commodities V. 10:8 (347-350))

Let me know if you would like a custom script or if you want to see me publish any other indicators!

Mass Thrust IndicatorThis is a custom indicator of mine that I based loosely on Tushar S. Chande's Market Thrust Indicator (Stocks & Commodities V. 10:8 (347-350)). Buy the stock if the indicator is green and sell when it turns red.

Let me know if you would like to see more scripts or if you have custom requests!

Midpoint OscillatorThe Midpoint Oscillator was created by Tushar Chande Ph.D. (Stocks & Commodities V. 9:11 (431-434)) and it does a great job of tracking extreme changes in the price. Buy when the line is green and sell when it turns red.

Let me know if you would like me to write more scripts!

Chande Momentum Oscillator + WaveTrend Oscillator [ChuckBanger]This is a combination of Lazybears WaveTrend Oscillator (purple line) and Chande Momentum Oscillator (blue line with the orange line as a signal line). Use WaveTrend as a confirmation tool. It is consider as a selling point when CMO is over the red horizontal dotted line. The opposite applies if CMO line is under the red horizontal dotted line.

You can also use this with WaveTrand to confirm the sell or buy point. When WT line is over center line and CMO has crossed over it's signal line. It is a buy point. The opposite applies if WT line is under the center line and CMO is under its signal line.

QuantCat Chande Swinger StrategyQuantCat Chande Swinger

This strategy is designed to be used on the 1 minute with mainly bitcoin, and cryptocurrencies. But parameters can be adjusted to ANY pair.

After some long research about chande momentum oscillator, I decided to create a strategy using normal distribution percentage levels to snipe entries. This in turn on the 1 minute can create a nice profit over a consecutive amount of days, the end goal is to get a stronger version of this strategy running on a bot and print some money. This strategy is tightly defined, and can be loosened up to make more trades too- giving a higher sample size and better sharpe ratio.

The strategy checks to see if the Chande value is in an extreme percentile based on the last few hundred chande values- if it is it will open a position.

No stoploss or take profit implemented into the swinger yet, but this will be the next addition to really minimise loss and amplify potential profits.

Any liquid crypto pair on the low timesframes will net a good result with this strategy.

We also have a free 15M and 1H strategy available too.

You can join our discord server to get live alerts for the strategies as well as speak to our devs! Link in signature below!!!

CKSDHi. It's simply histogram that shows divergence between the lines of the Chande Kroll Stop ind (built-in TradingView ind). I noticed that the lines intersect or are very close to each other if the volatility decreases. You can use MA like the main line or just 5, 10 lines how I do. Sorry for code Im not a programmer

Combo Backtest 123 Reversal & CMO & WMA This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots Chande Momentum Oscillator and its WMA on the

same chart. This indicator plots the absolute value of CMO.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change,

etc. It is most closely related to Welles Wilder?s RSI, yet it differs

in several ways:

- It uses data for both up days and down days in the numerator, thereby

directly measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term

extreme movements in price are not hidden. Once calculated, smoothing

can be applied to the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly

see changes in net momentum using the 0 level. The bounded scale also allows

you to conveniently compare values across different securities.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Strategy 123 Reversal & CMO & WMA This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots Chandre Momentum Oscillator and its WMA on the

same chart. This indicator plots the absolute value of CMO.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change,

etc. It is most closely related to Welles Wilder?s RSI, yet it differs

in several ways:

- It uses data for both up days and down days in the numerator, thereby

directly measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term

extreme movements in price are not hidden. Once calculated, smoothing

can be applied to the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly

see changes in net momentum using the 0 level. The bounded scale also allows

you to conveniently compare values across different securities.