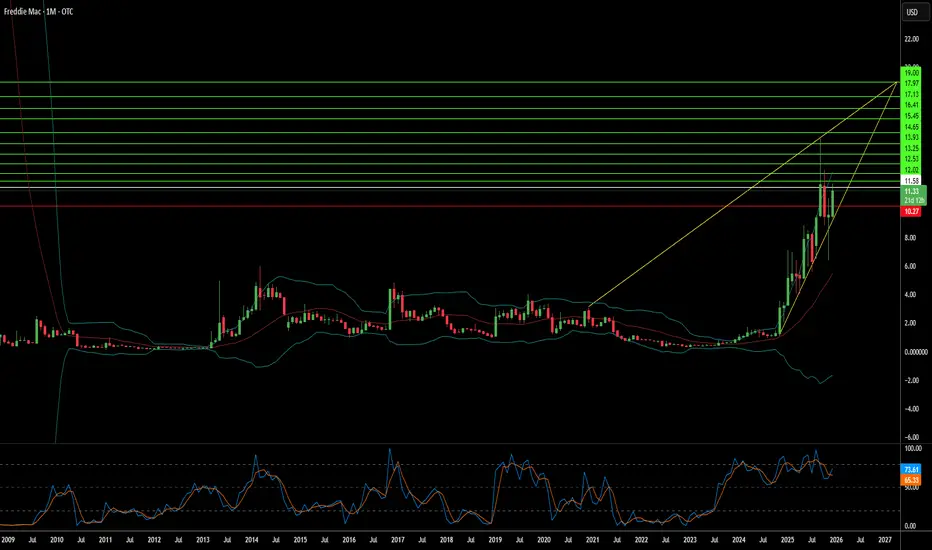

Freddie Mac stands at a critical inflection point as Michael Burry, the legendary investor from "The Big Short," takes a significant position in the government-sponsored enterprise. Trading over-the-counter at a fraction of its potential value, the company has transformed from a mortgage guarantor into a technological powerhouse with robust AI patents, zero-trust cybersecurity architecture, and automated underwriting systems that save lenders approximately $1,700 per loan. The stock currently trades well below book value, yet Burry projects a post-privatization valuation of 1.25x to 2x book value, representing massive upside if regulatory uncertainties resolve.

The privatization thesis centers on ending the Net Worth Sweep, building capital reserves, and eventually relisting the company. However, significant hurdles remain, particularly the Treasury's warrants for 79.9% of common stock, a massive dilution overhang that suppresses prices. Despite these challenges, Freddie Mac's operational fundamentals are strong: the housing market shows resilience with low delinquency rates around 2.12%, the company retains earnings for the first time in over a decade, and its geopolitical importance as a pillar of dollar hegemony makes it strategically indispensable to U.S. financial power.

Beyond traditional mortgage operations, Freddie Mac's intellectual property moat includes patents for location-quality assessment using machine learning, automated software testing for rapid deployment, and data-integrity systems. The company's zero-trust cybersecurity architecture positions it as a fortress against increasingly sophisticated threats from state actors and cybercriminals. With explorations into quantum computing for portfolio optimization and FHFA-directed pilots on cryptocurrency reserves, Freddie Mac is positioning itself at the intersection of finance and cutting-edge technology.

The asymmetric opportunity is clear: limited downside given the deep discount, enormous upside potential upon relisting and normalization. Foreign holders, such as Japan ($1.13 trillion) and China ($757 billion), anchor demand for Agency debt, providing structural support. While the path remains "windy and rocky" as Burry acknowledges, the convergence of strong fundamentals, technological leadership, geopolitical necessity, and a determined activist investor creates a compelling case for what may be one of the decade's most consequential value plays.

The privatization thesis centers on ending the Net Worth Sweep, building capital reserves, and eventually relisting the company. However, significant hurdles remain, particularly the Treasury's warrants for 79.9% of common stock, a massive dilution overhang that suppresses prices. Despite these challenges, Freddie Mac's operational fundamentals are strong: the housing market shows resilience with low delinquency rates around 2.12%, the company retains earnings for the first time in over a decade, and its geopolitical importance as a pillar of dollar hegemony makes it strategically indispensable to U.S. financial power.

Beyond traditional mortgage operations, Freddie Mac's intellectual property moat includes patents for location-quality assessment using machine learning, automated software testing for rapid deployment, and data-integrity systems. The company's zero-trust cybersecurity architecture positions it as a fortress against increasingly sophisticated threats from state actors and cybercriminals. With explorations into quantum computing for portfolio optimization and FHFA-directed pilots on cryptocurrency reserves, Freddie Mac is positioning itself at the intersection of finance and cutting-edge technology.

The asymmetric opportunity is clear: limited downside given the deep discount, enormous upside potential upon relisting and normalization. Foreign holders, such as Japan ($1.13 trillion) and China ($757 billion), anchor demand for Agency debt, providing structural support. While the path remains "windy and rocky" as Burry acknowledges, the convergence of strong fundamentals, technological leadership, geopolitical necessity, and a determined activist investor creates a compelling case for what may be one of the decade's most consequential value plays.

Connecting the dots to Decode the Invisible. This post is a summary. To understand the rigged game, you need the evidence. Access the Full Analysis + Raw Sources (Lab Reports, Patents, Academic Research & Cyber Intel). See the reality here ➜ udisview.com

Wyłączenie odpowiedzialności

Informacje i publikacje nie stanowią i nie powinny być traktowane jako porady finansowe, inwestycyjne, tradingowe ani jakiekolwiek inne rekomendacje dostarczane lub zatwierdzone przez TradingView. Więcej informacji znajduje się w Warunkach użytkowania.

Connecting the dots to Decode the Invisible. This post is a summary. To understand the rigged game, you need the evidence. Access the Full Analysis + Raw Sources (Lab Reports, Patents, Academic Research & Cyber Intel). See the reality here ➜ udisview.com

Wyłączenie odpowiedzialności

Informacje i publikacje nie stanowią i nie powinny być traktowane jako porady finansowe, inwestycyjne, tradingowe ani jakiekolwiek inne rekomendacje dostarczane lub zatwierdzone przez TradingView. Więcej informacji znajduje się w Warunkach użytkowania.