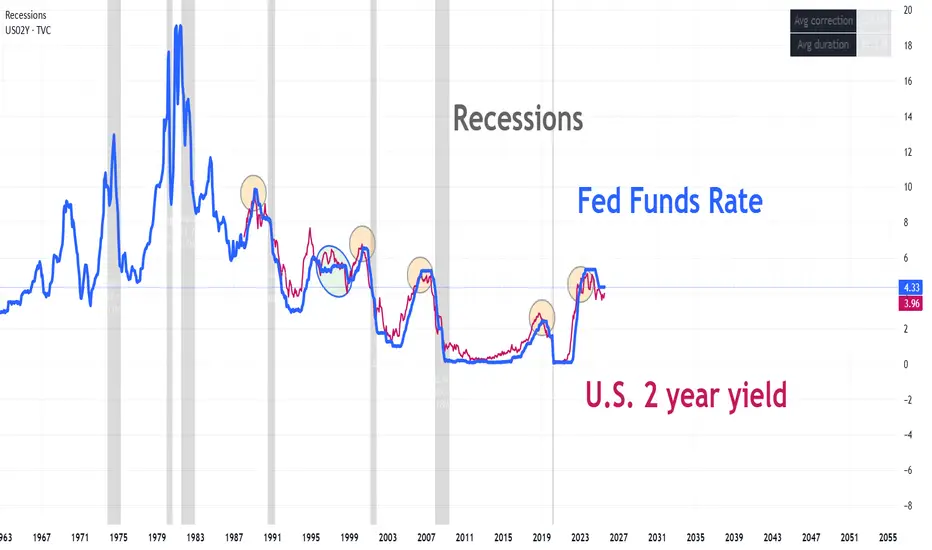

On August 4, we published a report analyzing the relationship between the 2-year yield and the Fed rate. At first glance, it looks like a technical oscillator, except in this case it represents market expectations for the 2-year rate. It embeds the expected real rate, expected inflation, and the term premium. Every time it gave a short signal, a recession followed shortly after. It generated one false signal and correctly anticipated the last four recessions. Two weeks after the report, Jackson Hole brought the pseudo-confirmation of the rate cut.

@intermarketflow

Wyłączenie odpowiedzialności

Informacje i publikacje przygotowane przez TradingView lub jego użytkowników, prezentowane na tej stronie, nie stanowią rekomendacji ani porad handlowych, inwestycyjnych i finansowych i nie powinny być w ten sposób traktowane ani wykorzystywane. Więcej informacji na ten temat znajdziesz w naszym Regulaminie.

@intermarketflow

Wyłączenie odpowiedzialności

Informacje i publikacje przygotowane przez TradingView lub jego użytkowników, prezentowane na tej stronie, nie stanowią rekomendacji ani porad handlowych, inwestycyjnych i finansowych i nie powinny być w ten sposób traktowane ani wykorzystywane. Więcej informacji na ten temat znajdziesz w naszym Regulaminie.